Saudi Arabia Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

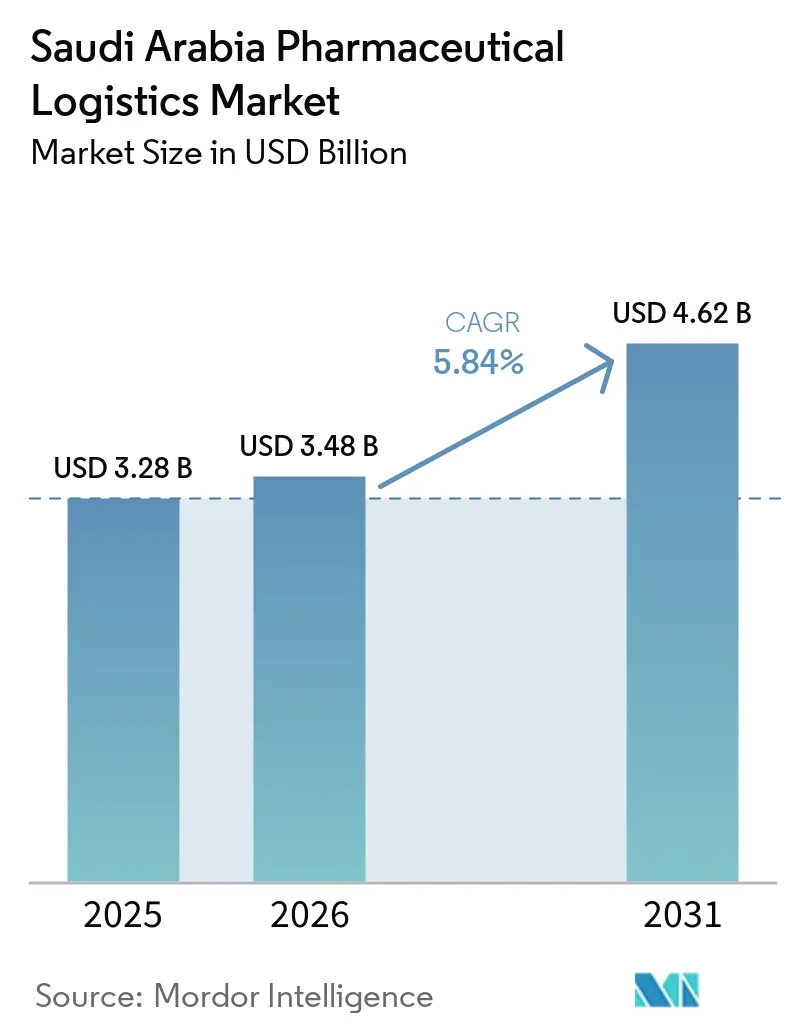

| Base Year Market Size (2025) | USD 3.28 Billion |

| Market Size (2026) | USD 3.48 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

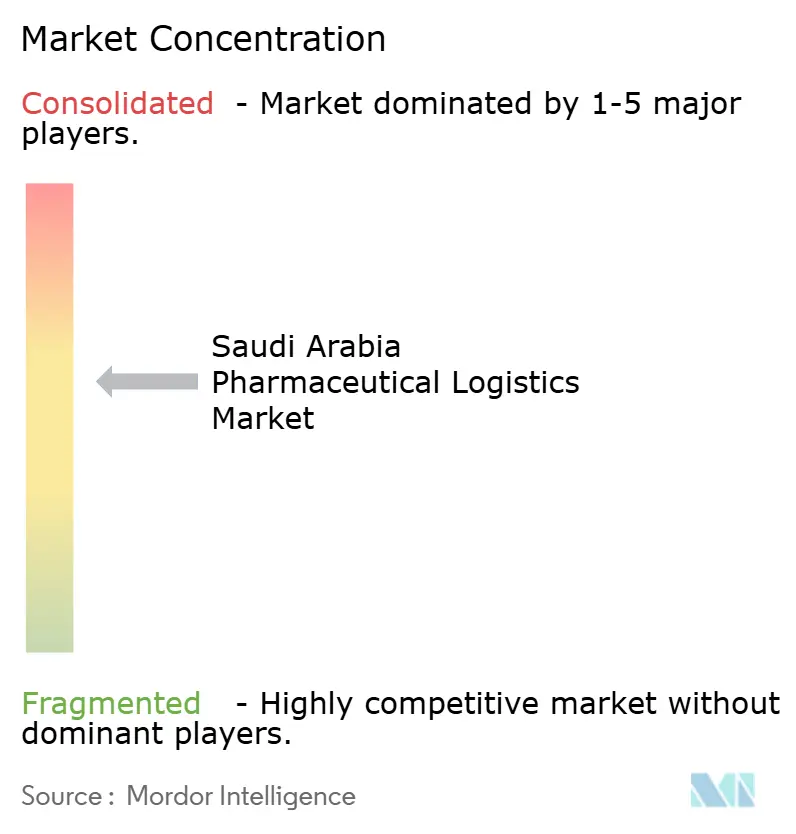

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The Saudi Arabia pharmaceutical logistics market size was valued at USD 3.28 billion in 2025 and estimated to grow from USD 3.48 billion in 2026 to reach USD 4.62 billion by 2031, at a CAGR of 5.84% during the forecast period (2026-2031).

The Saudi Arabia pharmaceutical logistics market is supported by durable demand, as the Kingdom remains the largest pharmaceutical market in the GCC and still relies on imports for 70% to 80% of its pharmaceutical supply, keeping logistics capacity central to the availability of medicines across hospitals, pharmacies, and public procurement channels. Government-led healthcare transformation is widening the number of care delivery points, raising distribution complexity, and increasing the need for flexible hub-and-spoke models that can handle higher SKU counts and more frequent replenishment cycles. The Saudi Arabia pharmaceutical logistics market is also being shaped by tighter cold-chain enforcement, broader adoption of biologics, and a visible shift toward value-added services such as serialization support, temperature deviation reporting, and direct-to-patient fulfillment. Competitive strategy is moving toward larger in-country footprints, multimodal integration, and digitally enabled import handling as international and domestic operators commit new assets in Riyadh, Jeddah, and Dammam. Opportunity remains strongest in certified cold-chain infrastructure, higher-value compliance services, and regional distribution corridors linked to manufacturing localization and remote healthcare delivery.

Key Report Takeaways

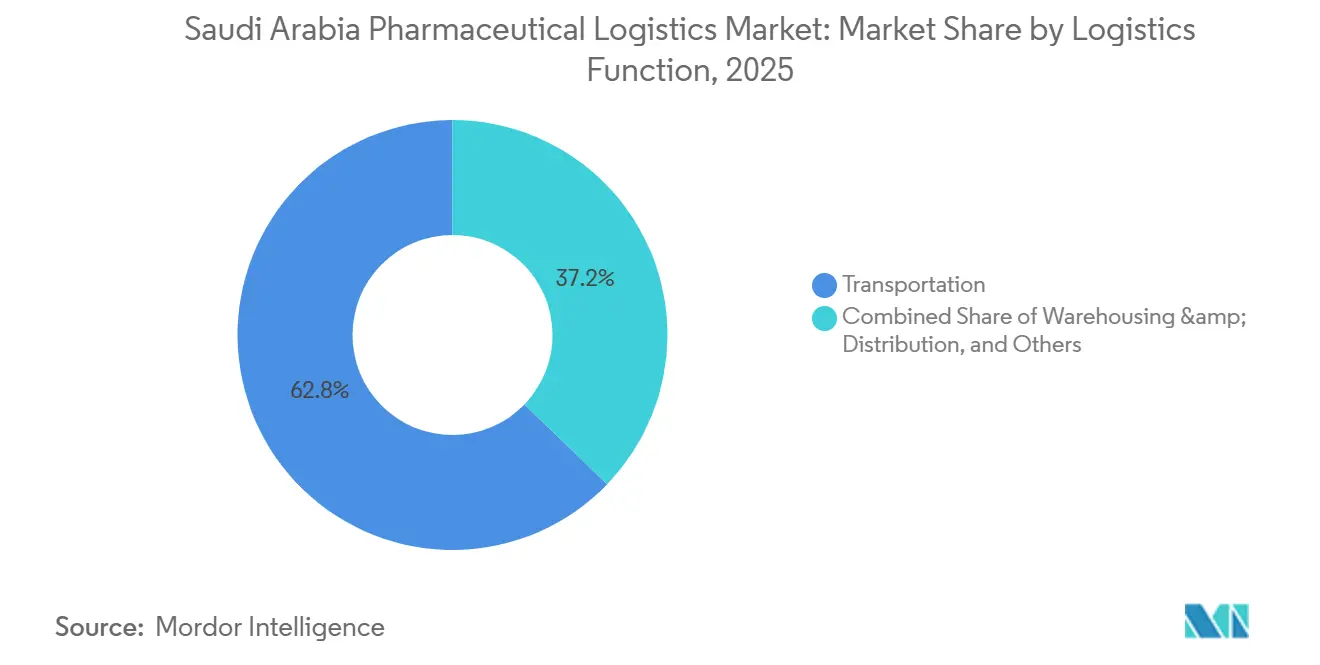

- By logistics function, transportation held 62.78% of Saudi Arabia pharmaceutical logistics market share in 2025, while value-added services are projected to expand at 8.67% CAGR through 2031.

- By mode of operation, non-cold-chain logistics represented 59.97% of Saudi Arabia pharmaceutical logistics market size in 2025, while cold-chain logistics is forecast to grow at 7.84% CAGR through 2031.

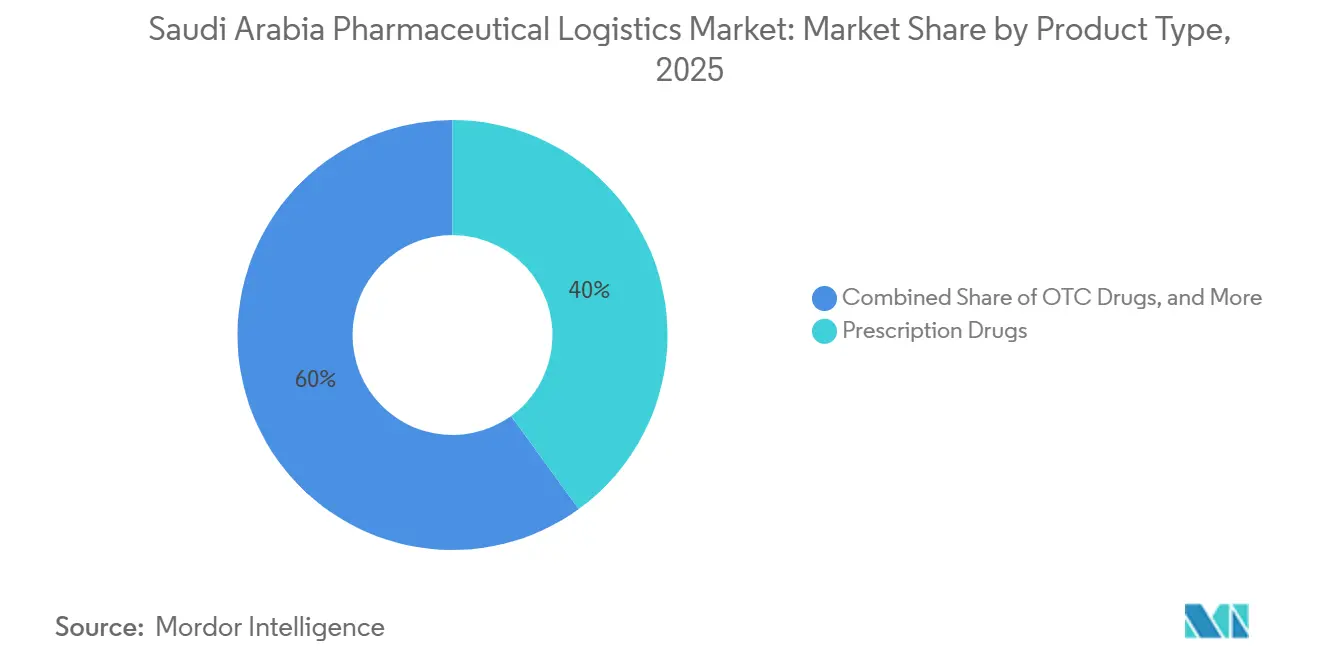

- By product type, prescription drugs accounted for 40% of Saudi Arabia pharmaceutical logistics market share in 2025, while cell and gene therapies are projected to grow at 8.98% CAGR through 2031.

- By region, the Central region held 33.12% of Saudi Arabia pharmaceutical logistics market size in 2025, while the Western region is forecast to expand at 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Healthcare Transformation | +1.4% | KSA-wide, concentrated in Riyadh, Jeddah, and Dammam health clusters | Long term (≥ 4 years) |

| SFDA Cold-Chain Regulation Enforcement | +0.9% | KSA-wide, most stringent at Jeddah Islamic Port and King Khalid International Airport | Medium term (2-4 years) |

| Rising Chronic-Disease Demand for Biologics | +1.1% | KSA-wide, with Central and Eastern regions leading | Long term (≥ 4 years) |

| Growth of E-Pharmacy and Home Delivery | +0.7% | Urban cores, including Riyadh, Jeddah, and Dammam, with spillover to Makkah and Medina | Medium term (2-4 years) |

| NEOM and Giga-Project Remote Supply Chains | +0.5% | Northwest Saudi Arabia, especially the Tabuk-NEOM corridor | Long term (≥ 4 years) |

| PPP-Driven Foreign 3PL Pharma Hubs | +0.6% | SILZ in Riyadh, KAEC in Jeddah, and Dammam industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Healthcare Transformation

Saudi Arabia’s healthcare overhaul is changing the demand profile of the Saudi Arabia pharmaceutical logistics market beyond the effect of new hospitals alone. The 2025 national budget allocated SAR 260 billion (USD 69 billion) to health and social development, which kept healthcare among the Kingdom’s largest spending priorities. The plan to corporatize and privatize 290 hospitals and 2,300 primary health centers increases the number of operating nodes that need regular medicine replenishment and service-level consistency[1]Saudi Vision 2030, “Health Sector Transformation Program,” Saudi Vision 2030, vision2030.gov.sa. This shift reduces reliance on a single centralized distribution logic and raises the value of providers that can manage more institutional buyers, denser routes, and tighter inventory visibility. In practice, the Saudi Arabian pharmaceutical logistics market benefits from healthcare reform, which makes delivery reliability a core operating requirement rather than a support function.

SFDA Cold-Chain Regulation Enforcement

The Saudi Arabia pharmaceutical logistics market is being lifted by tighter SFDA enforcement of Good Distribution Practice standards across temperature-sensitive handling. Continuous data logging, automated temperature deviation alerts, and validated sensor coverage are now embedded in compliance expectations for cold-chain shipments, which raises the infrastructure threshold for service providers. Operators without certified equipment and documented processes are increasingly excluded from high-value biologic and vaccine tenders, which shifts more volume toward qualified networks. The SFDA’s audit and licensing activities are also driving new investment in warehouse validation, fleet upgrades, and reporting systems across the Kingdom[2]Saudi Food and Drug Authority, “Guidance for the Storage and Transport of Time- and Temperature-Sensitive Pharmaceutical Products,” SFDA, sfda.gov.sa. A parallel constraint remains on the labor side, as the 2025 logistics skills report identified major gaps in digital tools, cold-chain management, and specialized logistics roles, with 42% of logistics companies reporting that many employees still lacked these capabilities.

Rising Chronic-Disease Demand For Biologics

The Saudi Arabia pharmaceutical logistics market is also expanding, as biologics and biosimilars require tighter temperature control and shorter transit times than conventional therapies. These products often require continuous handling at 2-8 °C, while advanced therapies may require ultra-low or cryogenic storage conditions, which sharply increase handling complexity. The SFDA continued to broaden biosimilar approvals through 2025 across oncology, autoimmune, and diabetes categories, which widened the pool of products that must move through validated cold-chain pathways. In August 2025, MS Pharma inaugurated MENA’s first biologics manufacturing facility in Riyadh. This USD 50 million GMP-approved site added new domestic cold-chain flows to the Kingdom’s established import corridors. This means the Saudi Arabia pharmaceutical logistics market is now serving both inbound biologic imports and intra-Kingdom distribution linked to local production.

Growth Of E-Pharmacy And Home Delivery

The Saudi Arabia pharmaceutical logistics market is gaining support from e-pharmacy growth and the normalization of home delivery for prescription fulfillment. Internet penetration above 95% and the expansion of SFDA-regulated digital health have made online ordering and remote dispensing more practical across major urban centers. As more medicines move directly to patients, GDP-compliant handling is needed throughout the last mile, rather than only in hospitals, retail pharmacies, and central warehouses. This shift underscores the value of route optimization, proof-of-delivery controls, and temperature integrity at the doorstep handoff. The Saudi Arabia pharmaceutical logistics market, therefore, sees growth not only from higher shipment counts but also from the higher service intensity required for home-based pharmaceutical distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cold-Chain Operating Costs In Desert Climate | -1.0% | KSA-wide, most acute in inland cities such as Riyadh and Hail during the summer months | Long term (≥ 4 years) |

| Customs Clearance Delays | -0.7% | Jeddah Islamic Port, King Abdulaziz International Airport, and Riyadh Dry Port | Medium term (2-4 years) |

| GDP-Certified Workforce Shortage | -0.5% | Eastern Province, Riyadh air cargo, and national driver pool | Medium term (2-4 years) |

| Rural Last-Mile Fragmentation | -0.4% | Northern areas, including Al-Jouf and Arar, and Southern areas, including Jazan and Najran | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cold-Chain Operating Costs In Desert Climate

The Saudi Arabia pharmaceutical logistics market faces a persistent cost burden because GDP-compliant refrigeration in desert conditions requires heavier cooling loads than most temperate-climate systems. Summer temperatures above 45 °C raise energy use, shorten equipment life, and increase maintenance cycles across warehouses, trucks, and airport handling facilities. Smaller operators feel this pressure most because they do not have the asset scale or route density that global 3PLs can use to spread fixed costs across larger throughput. The challenge becomes sharper in cryogenic logistics, where storage at very low temperatures creates a separate cost structure above standard 2-8 °C operations. Energy optimization pilots using AI and ML have shown potential in Riyadh and Jeddah, but adoption remains limited because the upfront capital requirements remain high.

Customs Clearance Delays

The Saudi Arabia pharmaceutical logistics market also faces measurable friction at import gateways because customs and regulatory clearance have become more time-consuming since late 2025. New Saudi customs procedures removed broker warehouse access, introduced manual handling request flows, and added extra transfer steps at points of entry, which extended clearance cycles for imported cargo. Pharmaceutical shipments already move through a dual-authority process involving both SFDA port inspections and ZATCA customs, so adding procedural steps deepens a bottleneck that was already present. The SFDA’s clearance guidance states that lab testing for new pharmaceutical products can take 7 to 10 business days, and initial product registration commonly requires 1 to 3 years, which is especially difficult for time-sensitive biologics that must remain refrigerated during delays[3]Saudi Food and Drug Authority, “Drug Registration Guide - Clearance Conditions and Requirements,” SFDA, sfda.gov.sa . Until gateway procedures become more predictable, the Saudi Arabia pharmaceutical logistics market will continue to absorb higher dwell costs and greater scheduling uncertainty for imported therapies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Anchors Revenue, Value-added Services Redefine Margin Mix

Transportation accounted for 62.78% of the Saudi Arabia pharmaceutical logistics market share in 2025, confirming that cross-border movement and domestic line-haul still form the commercial core of the sector. This dominance reflects the import-driven structure of Saudi medicine supply, where large inbound volumes enter through key airports and seaports before moving into hospital, pharmacy, and government procurement channels. Road transport remains the main distribution backbone from ports and airports into secondary cities and care networks, offering the broadest reach across the Kingdom. Air freight continues to play a critical role in the movement of urgent biologics and specialty products through Riyadh and Jeddah. At the same time, sea routes through Jeddah and Dammam continue to handle bulk pharmaceutical volumes at lower unit cost.

Value-added services are projected to grow at 8.76% CAGR through 2031, making them the fastest-moving part of the functional mix in the Saudi Arabia pharmaceutical logistics market. This growth comes from rising demand for serialization support, GDP documentation, temperature excursion reporting, reverse logistics, and direct-to-patient fulfillment rather than from transport volume alone. Warehousing and distribution are also being repositioned from a cost center into a resilience asset as the government hub strategy encourages larger in-country buffer stocks at Riyadh, Jeddah, and other strategic nodes. DHL Supply Chain’s EUR 130 million (USD 141 million) investment in a 78,000 m² multi-user warehouse at Riyadh’s SILZ illustrates this shift. It shows how capacity expansion is being tied directly to pharmaceutical service depth rather than simple storage growth.

By Mode Of Operation: Non-Cold-Chain Majority Persists, Cold Chain Sets The Growth Pace

Cold-chain logistics is forecast to grow at a 7.84% CAGR through 2031, driven by product mix changes and regulatory tightening. The SFDA’s GDP expectations for continuous monitoring and validated handling are bringing more shipments into certified temperature-controlled pathways, even where ambient treatment was previously common. NAQEL Express has expanded this capacity through 14 regional GDP-compliant offices and dedicated temperature zones for ambient, chilled, and frozen healthcare products across its network. In 2025, AJEX Logistics Services inaugurated Saudi Arabia’s first GMP-GxP-certified logistics depot in Riyadh, featuring 2 °C-8 °C chambers for vaccines and biologics and -20 °C chambers for frozen therapies, demonstrating that compliance-grade cold-chain infrastructure is becoming a threshold requirement rather than a premium add-on.

Cold-chain logistics is forecast to grow at a 7.84% CAGR through 2031, driven by product mix changes and regulatory tightening. The SFDA’s GDP expectations for continuous monitoring and validated handling are bringing more shipments into certified temperature-controlled pathways, even where ambient treatment was previously common. NAQEL Express has expanded this capacity through 14 regional GDP-compliant offices and dedicated temperature zones for ambient, chilled, and frozen healthcare products across its network. In 2025, AJEX Logistics Services inaugurated Saudi Arabia’s first GMP-GxP-certified logistics depot in Riyadh, featuring 2 °C-8 °C chambers for vaccines and biologics and -20 C chambers for frozen therapies, demonstrating that compliance-grade cold-chain infrastructure is becoming a threshold requirement rather than a premium add-on.

By Product Type: Prescription Drugs Lead Volume, Cell And Gene Therapies Reset Infrastructure Standards

Prescription drugs accounted for 40% of the Saudi Arabia pharmaceutical logistics market size in 2025, making them the largest product segment by revenue. Their lead comes from the steady movement of chronic disease therapies across cardiovascular, diabetes, and oncology care pathways, especially through hospital and retail pharmacy channels in major urban regions. OTC drugs and medical devices remain important secondary segments because they benefit from e-pharmacy growth and broad everyday demand. Vaccines and blood products also retain a strategic role within the Saudi Arabia pharmaceutical logistics industry because SFDA storage and transport rules keep cold-chain integrity central to public health distribution.

Cell and gene therapies are projected to grow at a 8.98% CAGR through 2031, making them the fastest-growing product category in the Saudi Arabia pharmaceutical logistics market. This segment changes infrastructure requirements because cryogenic handling, validated chain-of-custody controls, and highly specialized packaging are not interchangeable with conventional pharmaceutical logistics. DHL strengthened its position in this area through the acquisition of CRYOPDP in 2025, bringing cryogenic logistics capabilities across 135 countries and improving its ability to serve advanced therapy flows linked to Saudi Arabia. Clinical trial materials logistics is also becoming more relevant to the Saudi Arabia pharmaceutical logistics industry as biotech activity in newer corridors raises demand for validated investigational product distribution.

Geography Analysis

The Central region accounted for 33.12% of Saudi Arabia's pharmaceutical logistics market in 2025, and its lead stems from a reinforcing mix of policy, infrastructure, and customer concentration. Riyadh combines NUPCO-linked procurement flows, proximity to King Khalid International Airport, and bonded logistics assets at SILZ, providing providers with a strong base for national redistribution. DHL’s November 2025 decision to invest EUR 130 million (USD 141 million) in a multi-user warehouse at SILZ showed that large operators see Riyadh as the main anchor for future network density and service depth. The Eastern region supports this structure through import handling at King Abdulaziz Seaport and steady downstream demand across Dammam, Al-Khobar, and Jubail. A 2025 study in the Saudi Pharmaceutical Journal found that 78% of pharmaceutical manufacturers in Saudi Arabia cited compliance and supply chain data transparency as operational obstacles, which helps explain why certified handling and visibility tools are gaining value in the Eastern corridor.

The Western region is projected to grow at 7.22% CAGR through 2031, and the growth case is broader than simple import volume expansion. Jeddah remains a critical entry point for pharmaceuticals. Still, the region is also benefiting from manufacturing localization, stronger demand for healthcare services, and future biotech activity along the Tabuk-NEOM axis. The Makkah healthcare cluster’s higher prescription volume and home-delivery activity show that last-mile demand in the west already extends beyond pilot programs and retail convenience. Compliance pressure at Jeddah’s air and sea gateways also favors larger, certified operators, as port-facing cold-chain integrity, halal standards, and audit readiness matter more as biologic volumes rise.

The Northern and Southern regions still account for a smaller share of the Saudi Arabia pharmaceutical logistics market because distance and terrain make distribution economics more challenging. Populations are thinner, road legs from main depots are longer, and dedicated pharmaceutical cold-chain assets remain limited in many areas. NUPCO’s February 2025 MoUs with Aramex and SMSA to support direct-to-patient delivery show that policymakers and logistics providers recognize the need for a more structured last-mile model outside the main urban belt[4]Aramex, “Aramex Opens First Regional Healthcare Hub at Dubai South Free Zone,” Aramex, aramex.com . Until shared infrastructure or public-service delivery obligations become more formalized, these regions will remain longer-horizon opportunities rather than immediate revenue centers for large operators.

Competitive Landscape

The Saudi Arabia pharmaceutical logistics market shows moderate concentration in the certified premium tier and wider fragmentation across the broader regional freight-forwarding market. Operators with national GDP-compliant cold-chain assets, audited facilities, and multimodal coverage sit in a stronger competitive position than firms that compete mainly on price in ambient transport or local forwarding. The largest strategic move in the current cycle came in February 2026, when DSV completed the in-country integration of DB Schenker and created a unified Saudi organization across air and sea, contract logistics, and road operations spanning 29 facilities. That move raised the scale bar in the Saudi Arabian pharmaceutical logistics market, as few domestic competitors can match a similar asset footprint without major new capital commitments. The result is a clearer separation between national full-service providers and smaller firms that remain limited to narrower route, mode, or compliance capabilities.

Partnership-led localization is becoming another defining feature of competition in the Saudi Arabia pharmaceutical logistics market. CEVA Logistics and Almajdouie finalized their Saudi joint venture in 2024, blending global healthcare logistics capabilities with local market reach and temperature-controlled distribution assets. Kuehne+Nagel also formed an exclusive partnership with Tamer Logistics covering the Kingdom’s major cities, which shows how international operators increasingly rely on established domestic infrastructure and regulatory familiarity to win healthcare contracts. These models reduce entry friction and help foreign groups participate in healthcare tenders without having to build every element of a local network from scratch.

Technology and specialty capability are becoming the main points of differentiation at the high end of the Saudi Arabia pharmaceutical logistics market. DHL’s 2025 acquisitions of CRYOPDP and SDS Rx strengthened its offer in cryogenic logistics, clinical trial support, and specialty pharmaceutical distribution, all of which matter more as biologics and advanced therapies grow. FedEx added another layer in May 2026 by launching the FedEx Import Tool in Saudi Arabia to provide centralized import documentation and real-time visibility, which directly addresses a market where clearance predictability has become a competitive issue. Three areas still appear less developed than the rest of the market, namely GDP-compliant direct-to-patient delivery at scale, cryogenic logistics for cell and gene therapies, and integrated clinical trial materials handling for emerging biotech clusters. That leaves room for operators to combine certified infrastructure, digital control, and local execution into a single service model.

Saudi Arabia Pharmaceutical Logistics Industry Leaders

Tamer Logistics

Kuehne+Nagel

DSV (Incl. DB Schenker)

DHL Group

UPS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: FedEx launched the FedEx Import Tool in Saudi Arabia, a digital platform offering real-time import visibility, centralized documentation management, and streamlined customs clearance workflows.

- February 2026: DSV completed the full in-country integration of DB Schenker in Saudi Arabia, creating a single unified organization spanning Air & Sea, Contract Logistics, and Road operations across 29 Kingdom facilities. The combined entity significantly expands multimodal pharmaceutical logistics capacity under one operator, reducing transaction friction for multi-leg pharmaceutical shipments.

- October 2025: NEOM and WuXi AppTec signed a strategic MoU to localize pharmaceutical R&D and manufacturing at Oxagon, NEOM’s advanced manufacturing city in northwest Saudi Arabia. The collaboration creates the framework for a world-class CRDMO facility, generating specialized biopharma logistics demand in a corridor that previously had none.

- September 2025: DHL Supply Chain agreed to acquire SDS Rx, extending its specialty pharmaceutical distribution and consumer health logistics capabilities. This was DHL’s second healthcare acquisition in 2025 and forms part of DHL Health Logistics’ growth agenda under Strategy 2030, broadening its healthcare SKU coverage relevant to Saudi Arabia’s pharmaceutical supply chain.

Saudi Arabia Pharmaceutical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Medical Devices and Diagnostics |

| Veterinary Medicine |

| Others |

| Central (Riyadh, Al-Qassim, and Hail) |

| Eastern (Ash-Sharqiyah) |

| Western (Al-Bahah, Makkah, Medina, and Tabuk) |

| Northern (Al-Jouf and Arar) |

| Southern (Asir, Jazan, and Najran) |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices and Diagnostics | ||

| Veterinary Medicine | ||

| Others | ||

| By Region | Central (Riyadh, Al-Qassim, and Hail) | |

| Eastern (Ash-Sharqiyah) | ||

| Western (Al-Bahah, Makkah, Medina, and Tabuk) | ||

| Northern (Al-Jouf and Arar) | ||

| Southern (Asir, Jazan, and Najran) |

Key Questions Answered in the Report

What is the 2031 value forecast for pharmaceutical logistics in Saudi Arabia?

The sector is forecast to reach USD 4.62 billion by 2031, up from USD 3.48 billion in 2026, with a 5.84% CAGR over 2026-2031.

Which logistics function generates the most revenue in Saudi Arabia?

Transportation is the largest function, accounting for 62.78% of revenue in 2025, as imports and national redistribution still dominate pharmaceutical movement.

Why is cold-chain capacity growing faster than the rest of the sector?

Cold-chain logistics is projected to grow at a 7.84% CAGR through 2031, driven by the need for stricter temperature control and stronger compliance with SFDA regulations for biologics, vaccines, and advanced therapies.

Which product category drives the highest logistics demand today?

Prescription drugs accounted for 40% of revenue in 2025, supported by chronic disease treatment flows across hospital and retail pharmacy networks.

Which region is the most important distribution hub?

The Central region led with 33.12% of revenue in 2025, driven by Riyadh's NUPCO-linked procurement flows, proximity to airports, and SILZ's bonded logistics assets.

What is the fastest-growing regional corridor in Saudi Arabia?

The Western region is forecast to grow at 7.22% CAGR through 2031, supported by Jeddah’s gateway role, healthcare demand in Makkah and Medina, and future biotech activity linked to NEOM.

Page last updated on: