China Healthcare Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

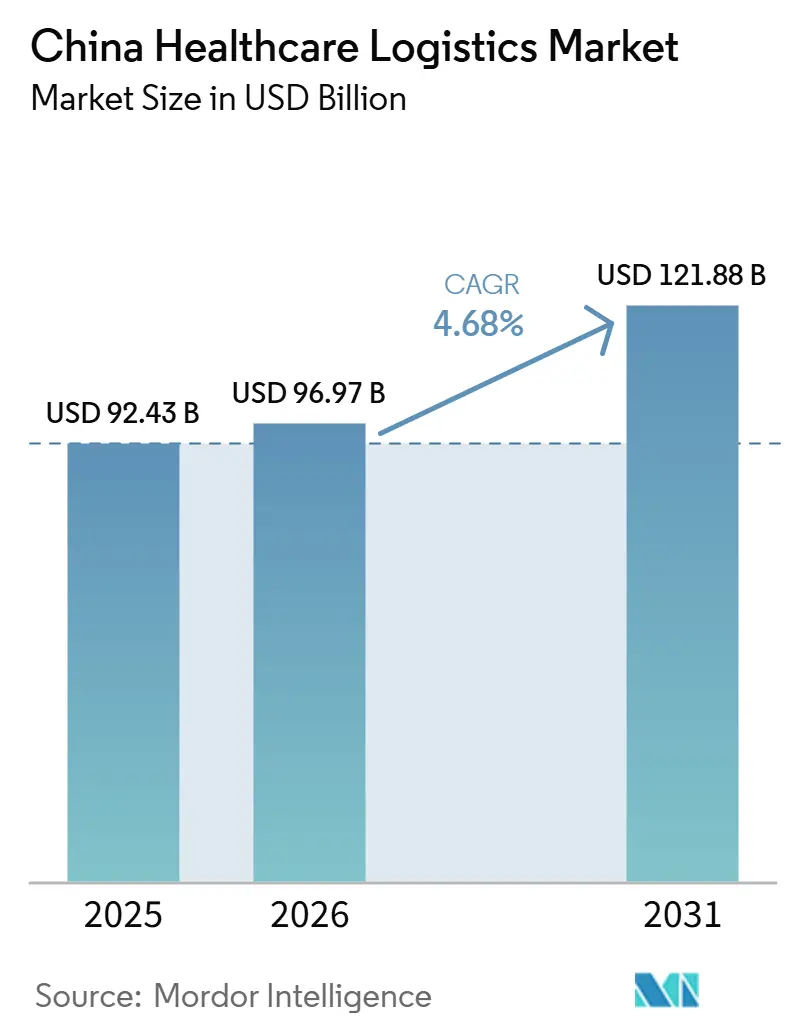

| Base Year Market Size (2025) | USD 92.43 Billion |

| Market Size (2026) | USD 96.97 Billion |

| Market Size (2031) | USD 121.88 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Healthcare Logistics Market Analysis by Mordor Intelligence

The China healthcare logistics market size is expected to increase from USD 92.43 billion in 2025 to USD 96.97 billion in 2026, and reach USD 121.88 billion by 2031, growing at a CAGR of 4.68% from 2026 to 2031.

Policy-backed expansion of pharmaceutical cold chain facilities at the county and township levels is supporting a broader distribution base for the China healthcare logistics market, especially for products that require validated handling conditions. The shift from hospital dispensing toward accredited retail pharmacy channels is increasing delivery points and raising the need for reliable last-mile fulfillment across the China healthcare logistics market. Digital traceability is also becoming a baseline operating requirement, as real-time temperature data, auditable records, and computerized management systems move from optional tools to standard compliance needs in the China healthcare logistics market. Competitive positioning is increasingly shaped by who can combine qualified cold-chain assets, patient-facing service capabilities, and scalable multimodal networks, leaving the strongest opportunity in higher-complexity services rather than in basic bulk distribution alone.

Key Report Takeaways

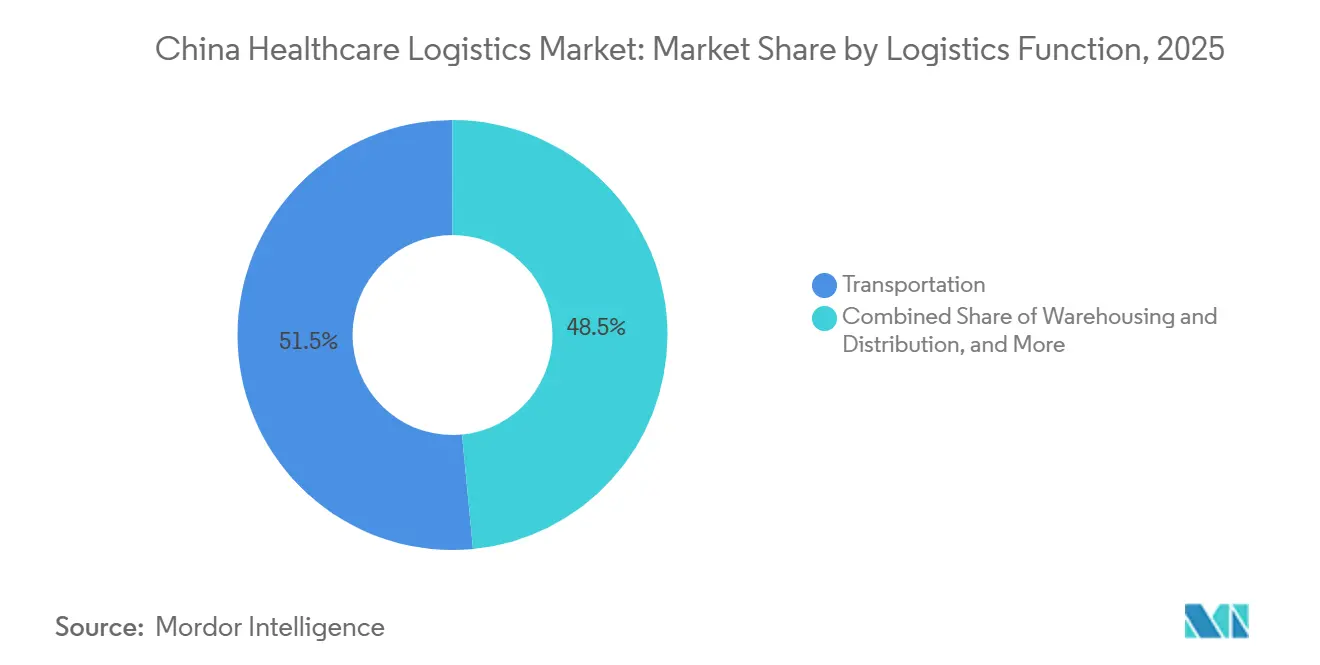

- By logistics function, transportation accounted for 51.52% of the China healthcare logistics market share in 2025, while value-added services and others are projected to grow at a 6.44% CAGR through 2031.

- By temperature type, non-temperature-controlled logistics accounted for 78.53% of the China healthcare logistics market size in 2025, while temperature-controlled logistics are forecast to expand at a 6.58% CAGR through 2031.

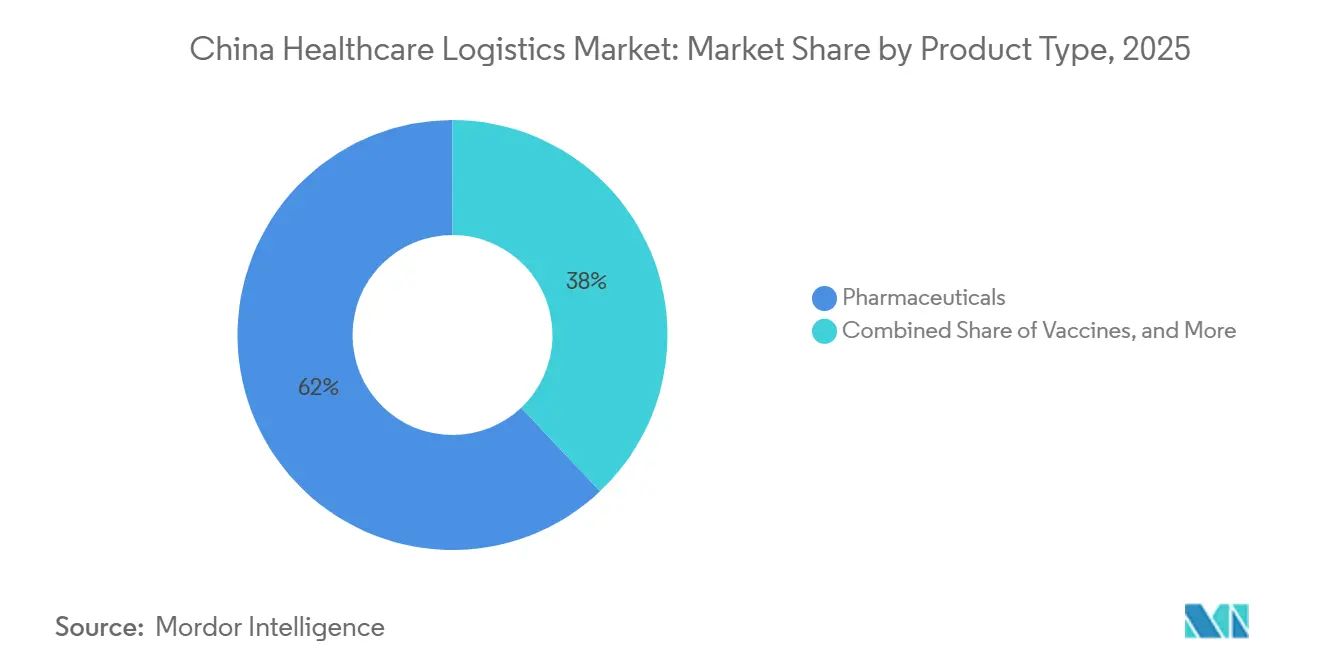

- By product type, pharmaceuticals accounted for 62.04% of the China healthcare logistics market size, while cell and gene therapies are expected to grow at a 10.74% CAGR through 2031.

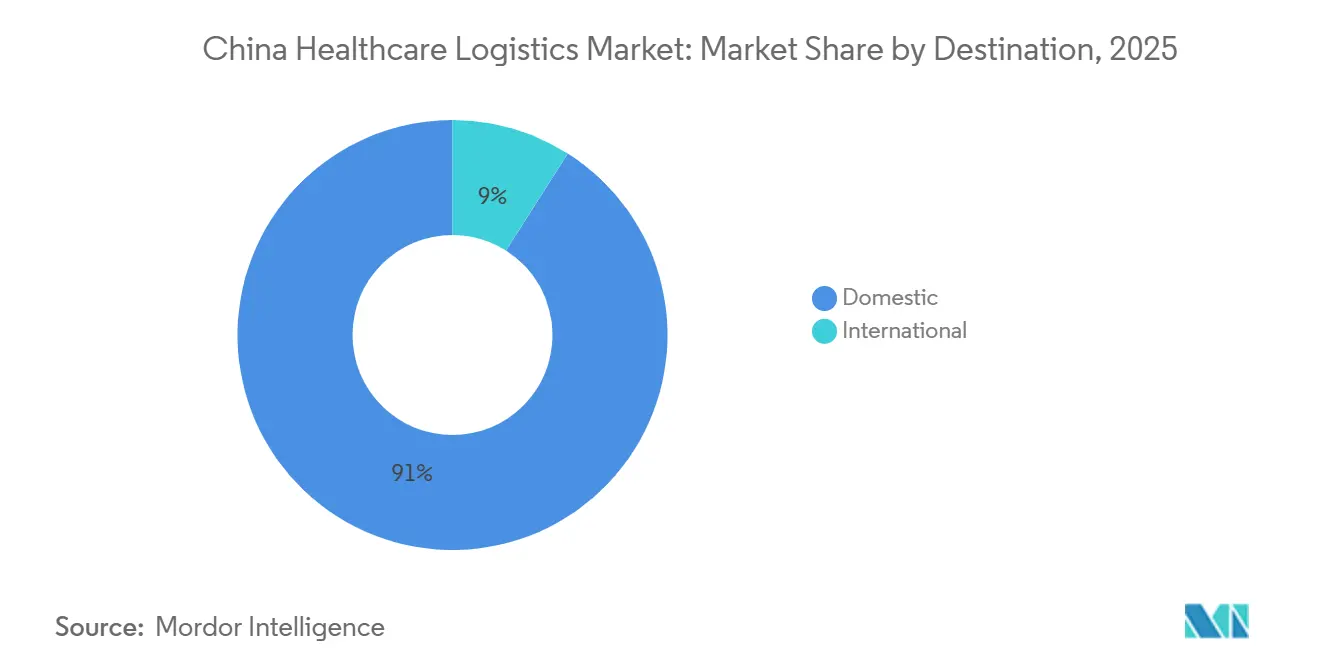

- By destination, domestic logistics accounted for 91.00% of the China healthcare logistics market share in 2025, while international logistics is projected to grow at a 5.74% CAGR through 2031.

- By end user, pharmaceutical companies held 42.49% of the China healthcare logistics market share in 2025, while biopharmaceutical manufacturers are forecast to grow at a 7.32% CAGR through 2031.

- By geography, East China accounted for 32.11% of the China healthcare logistics market size in 2025, while Southwest China is projected to expand at a 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Healthcare Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Biopharmaceutical and Vaccine Distribution Networks | +1.20% | National, concentrated in East and South China | Medium term (2-4 years) |

| Shift Toward Out-of-Hospital Drug Consumption | +0.90% | National, early gains in East and South | Short term (≤ 2 years) |

| Rapid Digitization of Temperature Monitoring and Traceability | +0.60% | National, with APAC cross-border relevance | Short term (≤ 2 years) |

| Multimodal Capacity Expansion Across Trunk and Last-Mile Routes | +0.50% | National, especially Southwest and Northwest corridors | Medium term (2-4 years) |

| Growth In Clinical Trial and Specialty Therapy Logistics | +0.50% | East and South China | Long term (≥ 4 years) |

| Rising Demand for Ultra-Low Temperature and Deep-Frozen Handling | +0.40% | National, with larger gaps in Central and Northwest China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Biopharmaceutical and Vaccine Distribution Networks

Industry and policy bodies are directing funding toward pharmaceutical cold chain expansion beyond large urban hubs, which is widening the addressable service base of the China healthcare logistics market. The county and township rollout matters because vaccine flows and temperature-sensitive drug volumes need qualified storage and transport at each handoff. The same pattern supports a stronger demand for distribution models that can handle more sensitive products with tighter documentation needs. As more innovative therapies reach patients through structured supply chains, logistics demand becomes longer-lasting rather than episodic. This is raising the value of operators that can combine cold chain capacity, audit readiness, and broad geographic coverage in the China healthcare logistics market[1]“Interpretation of National Standard, Requirements for Traceability Management of Pharmaceutical Cold Chain Logistics (GB/T 46204-2025),” China Federation of Logistics & Purchasing, chinawuliu.com.cn .

Shift Toward Out-of-Hospital Drug Consumption

Retail pharmacy reform is changing where prescription medicines are dispensed, and that is reshaping delivery economics in the China healthcare logistics market. Hospital-oriented distribution usually concentrates volume into fewer stops, while retail and patient-facing fulfillment spreads the same volume across many more delivery points. That shift increases the need for route planning, smaller cold chain shipments, and better proof of delivery. It also favors logistics providers that can link transport with patient support, medication access, and follow-up coordination. The result is a broader service mix in the China healthcare logistics market, with more value shifting toward consumer-facing fulfillment rather than solely institutional distribution.

Rapid Digitization of Temperature Monitoring and Traceability

Digital traceability is becoming a core operating layer rather than a premium add-on in the China healthcare logistics market. The current regulatory framework calls for independent computerized systems and stronger data capture across pharmaceutical logistics activities. The national traceability standard also raises expectations for consistent records across the cold chain. This makes temperature sensing, event logging, and exception tracking necessary for day-to-day compliance and for customer retention. Over time, early digital adopters are likely to keep a cost and execution advantage as the compliance floor rises across the China healthcare logistics market.

Multimodal Capacity Expansion Across Trunk and Last-Mile Routes

Multimodal buildout is expanding the physical reach of the China healthcare logistics market across long-distance, time-sensitive lanes. In addition, cold chain vehicles are growing faster than the broader pharmaceutical vehicle fleet, suggesting a steady shift toward more controlled transport capacity. Rail corridors are also becoming more relevant for cross-border pharmaceutical cargo, where transit time matters but air transport is not always economical[2]GMP Compliance Academy, “China’s NMPA, Guiding Opinions & Q&A on Standardising Modern Pharmaceutical Logistics,” GMP Compliance Academy, gmp-compliance.org. On the roadside, new automated distribution nodes are shortening access times into Central Asia and the western inland corridor. This gives pharmaceutical companies more flexibility to extend service coverage without matching every new corridor with owned assets, which supports wider network use in the China healthcare logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Centralized Procurement Pressure on Logistics Margins | -0.80% | National, pronounced in East and North China | Short term (≤ 2 years) |

| High Compliance Cost for End-To-End Temperature Integrity | -0.50% | National, disproportionate for smaller operators | Long term (≥ 4 years) |

| Regional Gaps in Cold Chain Validation Standards | -0.40% | Central, Southwest, Northwest, and Northeast China | Medium term (2-4 years) |

| Fragmented Service Quality Across Lower-Tier Cities | -0.30% | Tier-3 to Tier-5 cities, especially inland China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Centralized Procurement Pressure on Logistics Margins

Centralized drug procurement is putting pressure on revenue models tied closely to product value in the China healthcare logistics market. Moreover, procurement reform can raise concentration among leading suppliers while leaving smaller participants more exposed. That matters for logistics because volume commitments may rise even while pricing room narrows. Operators with a narrow service mix are more vulnerable when large contract volumes are accompanied by low margin tolerance. This creates a split in the China healthcare logistics market between bulk distributors that depend on scale and providers that can earn more from specialized handling or bundled services.

High Compliance Cost for End-To-End Temperature Integrity

Compliance costs are rising because qualified cold rooms, vehicles, monitoring systems, and auditable records all need ongoing investment. The burden is uneven across the China healthcare logistics market because large national operators can spread these costs across a wider revenue base. Smaller and regional providers face a harder choice between heavy spending and a narrower service offering. The national traceability standard adds another layer of recordkeeping discipline to cold chain operations. Over time, this raises entry barriers and supports further scale advantages for fully qualified operators in the China healthcare logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Leads Scale While Value-added Services Improve Revenue Quality

Transportation held 51.52% of the China healthcare logistics market share in 2025, which confirms that national product movement remains the core service layer. The segment benefits from China’s extensive pharmaceutical distribution network and the need to connect manufacturing centers with hospitals, pharmacies, and clinics over long distances. Cold chain vehicles also expanded faster than the broader pharmaceutical fleet in 2025, which shows where transport investment is being directed. That trend keeps transportation at the center of the China healthcare logistics industry even as service complexity rises.

Value-added services and others are projected to grow at a 6.44% CAGR through 2031, making it the fastest-expanding logistics function. These services include higher-touch workflows such as coordinated fulfillment, compliance support, and processing activities that sit above basic transport. JD Logistics' automation deployment in Beijing shows how providers are lifting throughput and serving more downstream pharmacies without matching volume growth with the same level of added floor space. As a result, the China healthcare logistics market is gradually shifting more value toward service layers that improve speed, visibility, and compliance rather than movement alone.

By Temperature Type: Ambient Volume Is Larger While Controlled Logistics Shapes Future Mix

Non-temperature-controlled logistics held 78.53% of the China healthcare logistics market size in 2025, reflecting the large volume of ambient pharmaceuticals, devices, and healthcare supplies moving through the network. That volume dominance keeps ambient handling important for scale in the China healthcare logistics market. The traceability standard has raised documentation expectations for cold chain shipments across storage and transport activities. The difference shows that value is moving toward shipments that need stricter thermal control and better traceability.

Temperature-controlled logistics, however, is forecast to grow at a 6.58% CAGR through 2031, and this part of the China healthcare logistics market size is expanding faster than the overall average.The current regulatory direction is also pushing operators to maintain better systems, qualified equipment, and cleaner records across controlled logistics. This supports providers that can manage multiple temperature bands within a single network rather than relying on separate, specialized handoffs. As more sensitive therapies move through the system, controlled logistics should command a larger strategic role within the China healthcare logistics industry.

By Product Type: Pharmaceuticals Provide the Base, While Cell And Gene Therapies Lift Complexity

Pharmaceuticals accounted for a 62.04% of the China healthcare logistics market share in 2025, keeping them as the main volume anchor across the market. The segment includes the broad flow of prescription drugs, specialty medicines, and over-the-counter products that need reliable national distribution. Retail reform and broader patient access pathways are also supporting greater pharmacy-linked fulfillment of drug products. That combination keeps pharmaceuticals central to day-to-day network utilization.

Cell and gene therapies is projected to grow at a 10.74% CAGR through 2031, making it the fastest-growing product segment. This segment depends on a stronger chain of custody, tighter handling discipline, and closer coordination among logistics providers, manufacturers, and care sites. The growth of innovative drug support programs also underscores why higher-complexity product flows are becoming increasingly important in the China healthcare logistics market. As a result, product mix is not only changing volume patterns but also raising the service threshold needed to compete in the China healthcare logistics market.

By Destination: Domestic Demand Dominates While International Routes Add Faster Growth

Domestic logistics captured 91.00% of the China healthcare logistics market size in 2025, underscoring the market's strong reliance on internal pharmaceutical demand. This concentration reflects the scale of hospital, pharmacy, and manufacturer flows that must be served inside the country every day. It also means that network design is still mainly driven by domestic replenishment, compliance, and cold chain service needs. The large domestic base keeps national route density and inland redistribution critical to service economics.

International logistics is forecast to grow at a 5.74% CAGR through 2031, and this part of the China healthcare logistics market size is gaining support from export-oriented and bonded corridor development. CEVA’s Alashankou distribution center is one example of infrastructure that improves access into Central Asia while also supporting trans-Eurasian cargo flows. Kerry Logistics’ Greater Bay Area work with Teva also shows how cross-border and regional pharmaceutical coordination is becoming more structured. These routes remain smaller than domestic volumes, but they offer faster growth and a more specialized service mix for the China healthcare logistics market.

By End User: Pharmaceutical Companies Hold the Largest Base While Biopharma Users Need More Specialized Support

Pharmaceutical companies held 42.49% of the China healthcare logistics market share in 2025, making them the largest end-user group served by the market. Their demand is tied to the broad distribution of finished drugs into hospital, wholesale, pharmacy, and clinic channels. This user group still supports the largest shipment base and the most regular replenishment cycles. Its service model is more mature and usually more volume-oriented than specialty therapy logistics.

Biopharmaceutical manufacturers are projected to grow at a 7.32% CAGR through 2031, and this segment of the China healthcare logistics market is rising amid more demanding service requirements. These customers need stronger cold-chain support, clearer records, and better coordination between logistics activities and patient access workflows. That is why providers with integrated service capability are becoming more relevant to this end-user group. The end-user mix, therefore, points to steady bulk demand on one side and faster premium service growth on the other within the China healthcare logistics market.

Geography Analysis

East China held 32.11% of the regional share in 2025, which made it the largest geographic block in the China healthcare logistics market. The region benefits from dense pharmaceutical manufacturing, strong port access, and a well-developed cold-chain infrastructure. Its mix of bonded logistics, large hospital systems, and advanced compliance practices keeps it at the center of premium distribution activity. This concentration gives East China a lasting scale advantage in the China healthcare logistics market.

South China remains the other major coastal hub because Guangdong manufacturing and Hong Kong-linked supply chain capability support both domestic and cross-border pharmaceutical flows. North China matters for procurement and tertiary care demand, even though its manufacturing density is not as strong as that of the main coastal production clusters. Northeast China still has an established logistics infrastructure, but its growth is slower than that of the leading coastal regions. Central China plays an important role in redistribution because its inland location makes it useful for balancing networks across several major corridors. These patterns keep the China healthcare logistics market centered on coastal leadership with inland hubs supporting national reach.

Southwest China is projected to grow at a 5.98% CAGR through 2031, and this geography is the fastest-growing part of the China healthcare logistics market size. Industry sources point to ongoing cold chain expansion into western county and township settings, which supports better access for vaccines and temperature-sensitive medicines. Northwest China still faces the toughest infrastructure challenge because long distances and lower density make qualified service harder to scale. New corridor assets such as the Alashankou distribution center improve the case for investment by linking domestic western demand with trans-Eurasian cargo opportunities. That should gradually narrow, but not fully remove, the regional gap inside the China healthcare logistics market[3] “A Study on the Availability of National Centralized Drug Procurement in Regions With Different Levels of Economic Development, An Investigation and Analysis of 31 Provincial-Level Administrative Regions in China,” Frontiers in Pharmacology, frontiersin.org.

Competitive Landscape

The China healthcare logistics market is moderately concentrated at the top and fragmented across the broader field. Sinopharm Logistics remains a major domestic anchor because of its scale, pharmaceutical distribution background, and deep institutional links across healthcare supply chains. Jointown Pharmaceutical Group Logistics is also positioned strongly in domestic pharmaceutical distribution, which keeps national incumbents important in the basic flow of drug logistics. Large domestic players benefit from their ability to meet compliance, network, and procurement-linked execution requirements at scale. This leaves smaller operators at a disadvantage when customers want both reach and validated quality.

International and hybrid operators are strongest where service complexity is high and cross-border coordination is more important. Kerry Logistics strengthened this position through its exclusive 4PL agreement with Teva in the Greater Bay Area. Logistics added another strategic move by opening its automated Alashankou distribution center in May 2026. DHL Group and JD.com also moved to deepen end-to-end logistics cooperation for flows between China and Europe in February 2026.

Competitive advantage is increasingly tied to cold chain qualification, network design, and digital control rather than only warehouse count or transport volume. The providers with the best positioning are those that can connect compliance systems with patient-facing fulfillment and cross-border service where needed. This is why high-complexity niches such as advanced cold chain, specialty therapies, and integrated pharmacy support remain the main white-space areas. The current regulatory direction also acts as a screening mechanism because underinvested operators may find it harder to retain relevance as standards tighten[4]China State Council Information Office, “China’s Inland Municipality Emerges as Global Logistics Nexus,” China State Council Information Office, scio.gov.cn.

China Healthcare Logistics Industry Leaders

Sinopharm Logistics Co., Ltd.

Shanghai Pharmaceuticals Logistics

JD Logistics Co., Ltd.

SF Express (KEX-SF)

Sinotrans Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CEVA Logistics inaugurated a 4,300 sqm automated distribution center in the Alashankou Free Trade Zone (China-Kazakhstan border), reducing China-to-Central Asia pharmaceutical and cargo transit from 20 days to 9-11 days and strengthening its Trans-Eurasian corridor with RFID, AI measurement technology, and electric autonomous forklifts. Lenovo is an anchor customer for the new facility.

- May 2026: JD Logistics deployed its LangzuTech goods-to-person automation system in pharmaceutical warehouse operations in the Beijing region, increasing processing capacity by approximately 600% without expanding the warehouse footprint and now serving hundreds of downstream retail pharmacies from a single facility.

- March 2026: China's NMPA published "Guiding Opinions on the Standardization of Modern Pharmaceutical Logistics" alongside an official Q&A, establishing the first nationally unified baseline for pharmaceutical wholesale and third-party logistics, directly addressing provincial standard fragmentation and mandating real-time temperature data upload to national traceability platforms.

- February 2026: DHL Group and JD.com signed a Memorandum of Understanding to provide end-to-end logistics for German brands entering China and Chinese products accessing European retail via JD.com's Joybuy platform, with JD Logistics and DHL collaborating on customs clearance, warehousing, and last-mile delivery under a preferential B2C import duty framework.

China Healthcare Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Temperature Controlled | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (less than -20 °C) | |

| Non-Temperature Controlled |

| Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | |

| Biopharmaceuticals (Biologics and Biosimilars) | |

| Vaccines | |

| Clinical Trial Materials | |

| Cell and Gene Therapies | |

| Medical Devices | |

| Veterinary Medicine | |

| Blood, Plasma and Blood Components | |

| Diagnostic and Laboratory Products | |

| Organs and Human Tissues | |

| Others |

| Domestics |

| International |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Hospitals and Clinics |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| North |

| Northeast |

| East |

| Central |

| South |

| Southwest |

| Northwest |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Temperature Controlled | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than -20 °C) | ||

| Non-Temperature Controlled | ||

| By Product Type | Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | ||

| Biopharmaceuticals (Biologics and Biosimilars) | ||

| Vaccines | ||

| Clinical Trial Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices | ||

| Veterinary Medicine | ||

| Blood, Plasma and Blood Components | ||

| Diagnostic and Laboratory Products | ||

| Organs and Human Tissues | ||

| Others | ||

| By Destination | Domestics | |

| International | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Hospitals and Clinics | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Region | North | |

| Northeast | ||

| East | ||

| Central | ||

| South | ||

| Southwest | ||

| Northwest | ||

Key Questions Answered in the Report

What is the 2026 value of China healthcare logistics?

The China healthcare logistics market is valued at USD 96.97 billion in 2026 and is forecast to reach USD 121.88 billion by 2031 at a 4.68% CAGR.

Which logistics function leads revenue in China healthcare logistics?

Transportation is the largest function, with 51.52% share in 2025, because national movement of pharmaceutical products remains the core service layer.

Which product area is growing the fastest in this space?

Cell and gene therapies is the fastest-growing product segment, with a projected 10.74% CAGR through 2031, driven by more demanding handling and documentation needs.

Why is cold chain becoming more important in pharmaceutical distribution in China?

Temperature-controlled logistics is forecast to grow at 6.58% through 2031, faster than the overall market, because more products need validated temperature integrity and traceability.

Which region leads pharmaceutical logistics activity in China?

East China holds the largest regional share at 32.11% in 2025, supported by dense manufacturing, port access, and advanced logistics infrastructure.

What is changing competition among logistics providers in China?

Competition is moving toward compliance capability, digital traceability, and specialized cold chain execution, while CEVA, Kerry Logistics, and DHL with JD.com are expanding through targeted strategic moves.

Page last updated on: