Cassava Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

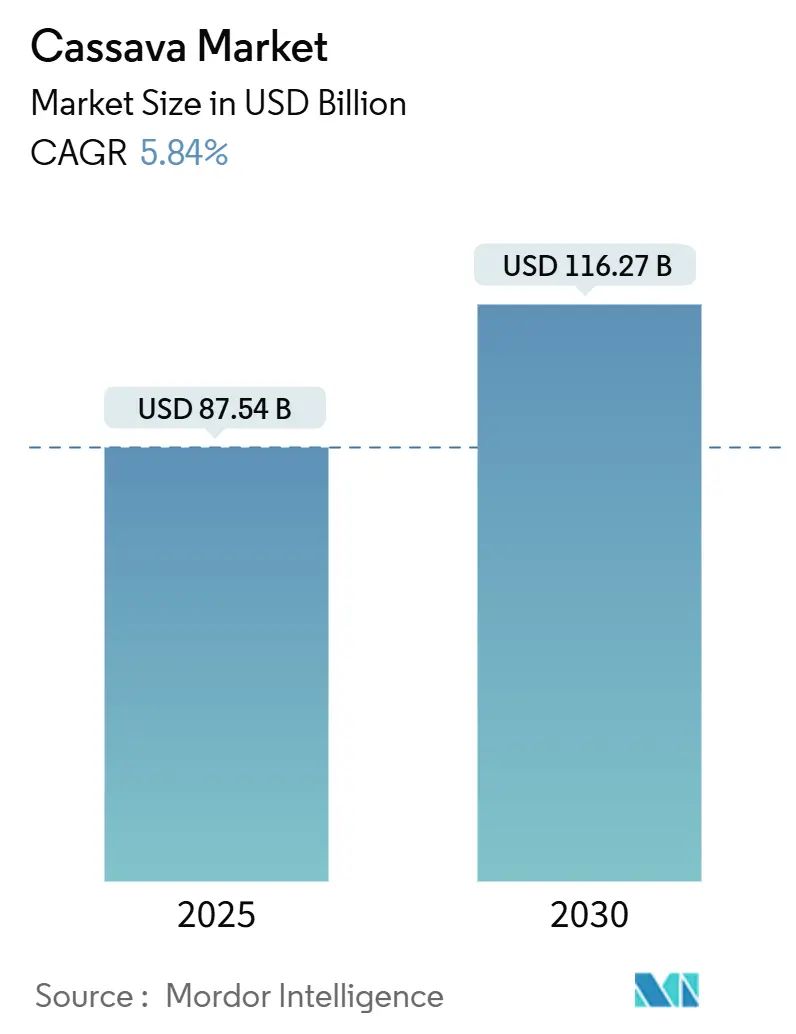

| Market Size (2025) | USD 87.54 Billion |

| Market Size (2030) | USD 116.27 Billion |

| Growth Rate (2025 - 2030) | 5.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cassava Market Analysis by Mordor Intelligence

The cassava market size stood at USD 87.54 billion in 2025 and is forecast to reach USD 116.27 billion by 2030, translating into a 5.84% CAGR over the period. Improved recognition of cassava as a climate-resilient staple, rising demand for gluten-free starches, and expanding biofuel mandates collectively underpin this growth trajectory. Producers benefit from the crop’s tolerance to marginal soils and drought, which lowers agronomic risk while offering a hedge against climate volatility. Industrial processors increasingly substitute costlier corn and potato starches with cassava to stabilize input costs, while governments in emerging economies embed cassava in food-security strategies that emphasize local value addition. Competitive intensity remains moderate, leaving scope for capacity expansions and new entrants that can secure reliable root supplies and deploy modern processing technologies.

Key Report Takeaways

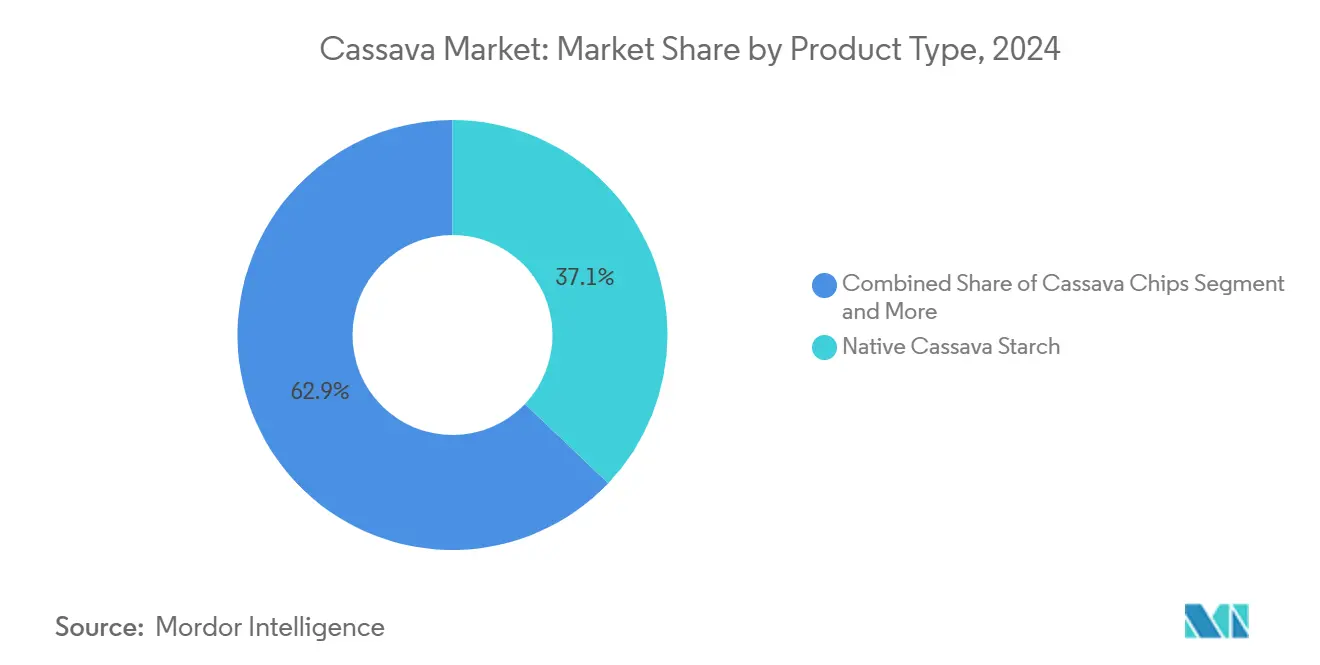

- By product type, native cassava starch led with 37.49% cassava market share in 2024; modified cassava starch and derivatives posted the highest projected CAGR at 8.63% through 2030.

- By form, dried products accounted for 51.95% of the cassava market size in 2024, whereas frozen products are projected to record a 9.28% CAGR between 2025-2030.

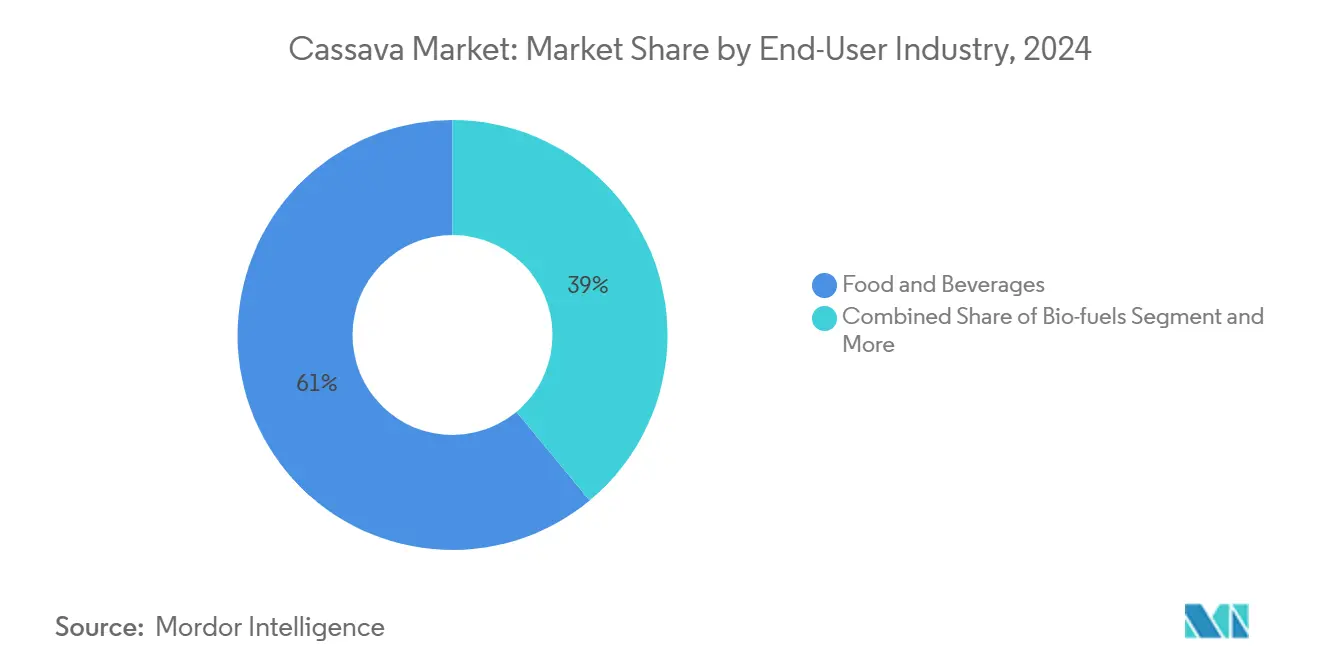

- By end-use industry, food and beverages held 61.64% of the cassava market size in 2024, while biofuels are forecast to expand at a 9.74% CAGR through 2030.

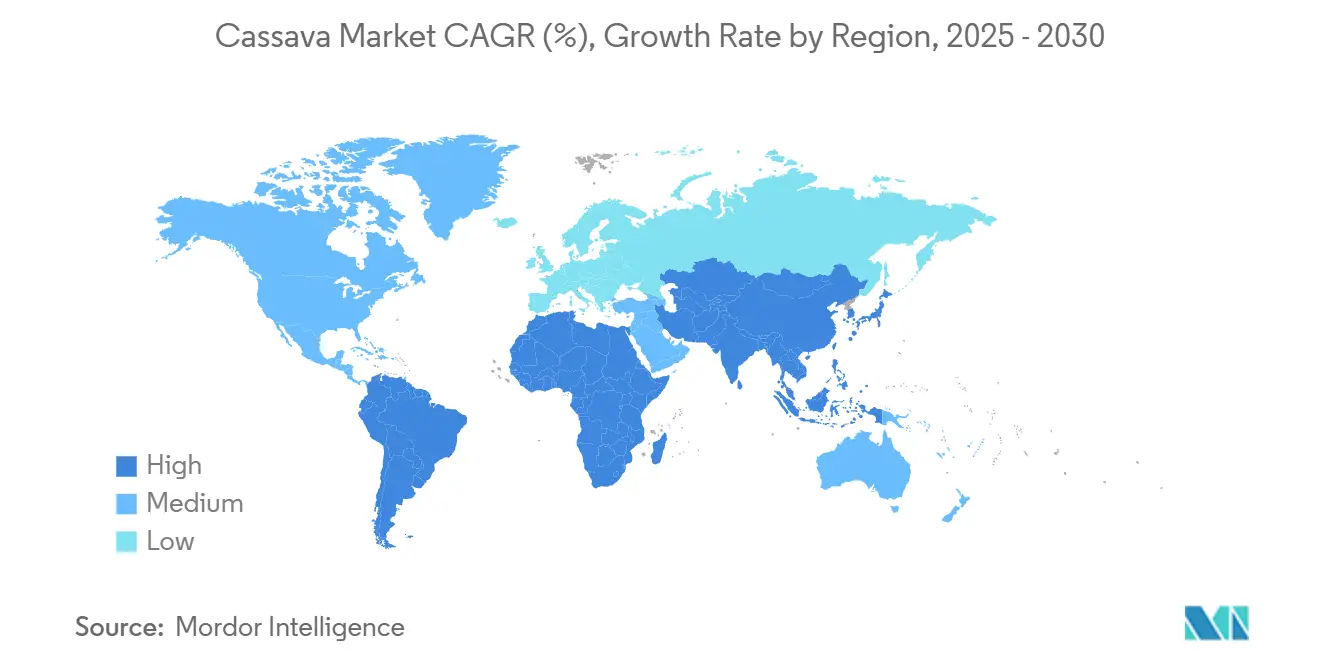

- By geography, North America captured 31.48% cassava market share in 2024, and Asia-Pacific is projected to advance at a 6.37% CAGR to 2030.

Global Cassava Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for gluten-free and clean-label starches | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Bioethanol and other biofuel feedstock expansion | +0.9% | Brazil, Thailand, Indonesia, with spillover to APAC | Long term (≥ 4 years) |

| Food-security driven cassava programs in emerging economies | +1.1% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Industrial shift toward cost-effective starch sweeteners | +0.8% | Global, early adoption in APAC manufacturing hubs | Medium term (2-4 years) |

| Climate-resilient cultivation attracting investment | +0.7% | Africa, drought-prone regions in Asia and Latin America | Long term (≥ 4 years) |

| Gene-edited virus-resistant varieties boosting yields | +1.0% | Africa, Southeast Asia with technology transfer globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for gluten-free and clean-label starches

As consumers increasingly gravitate towards gluten-free options, cassava is rising as the go-to substitute, thanks to its inherent gluten-free nature and neutral flavor. Modified cassava starches now represent 14% of the global starch production, playing pivotal roles as thickeners, stabilizers, and emulsifiers in functional foods. The clean-label movement is giving a significant boost to cassava starch. Food manufacturers are on the lookout for minimally processed ingredients, aligning with the growing demand for transparency. This push is speeding up the integration of cassava in bakeries, where it can substitute up to 30% of wheat flour without altering texture or nutrition. In the EU, a regulatory tilt towards natural food additives is giving cassava-derived ingredients an edge over synthetic counterparts. Meanwhile, industrial food processors are channeling investments into technologies that modify cassava starch, aiming to boost its functional properties while upholding clean-label standards.

Bioethanol and other biofuel feedstock expansion

In Brazil, government mandates for renewable fuel blending have spurred significant investments in cassava-based ethanol production. In 2022, Brazil's ethanol output hit 31.66 billion liters, marking a 6% uptick from the prior year[1]U.S. Department of Agriculture. "Brazil: Biofuels Annual." April 13, 2023. https://www.fas.usda.gov/data/brazil-biofuels-annual-9. Meanwhile, Indonesia's biodiesel initiative aims for 1.2 billion liters of sugarcane ethanol by 2030, inadvertently boosting demand for cassava as a substitute feedstock. Cassava boasts a unique advantage: it thrives on marginal lands that aren't suitable for food crops, effectively sidestepping the food-versus-fuel dilemma that hampers corn ethanol's growth. In Thailand, government measures in the cassava market, with a keen focus on ethanol production, have led to a notable 53% surge in cassava chip prices since early 2024. The economic feasibility of cassava ethanol sees a marked improvement when cassava prices hover between 60-70% of maize equivalents, a benchmark increasingly met in regions grappling with drought. Furthermore, cutting-edge fermentation technologies are boosting cassava's conversion efficiency, positioning it as a formidable competitor to conventional biofuel feedstocks.

Food-security driven cassava programs in emerging economies

National food security strategies are increasingly prioritizing cassava as a climate-resilient staple crop. In Nigeria, presidential intervention programs have successfully boosted cassava yields. Meanwhile, Kenya's agricultural research organization has rolled out disease-resistant cassava varieties. This innovation allows farmers in drought-prone areas to pivot from maize cultivation. The UNDP, in the Democratic Republic of Congo, is championing climate adaptation programs that spotlight cassava. Given that cassava is a staple for 70% of the population, these programs meld climate-smart practices with enhancements in processing. In Cambodia, the government, under its Industrial Development Policy 2015-2025[2]BINUS Business School. "Foreign Direct Investment Opportunity for Modified Cassava Starch in Indonesia." January 31, 2021. https://journal.binus.ac.id/index.php/BECOSS/article/download/7010/3988/36827, has spotlighted cassava as the nation's second-largest agricultural crop. Over a decade, public investments in cassava have reaped economic benefits thrice the initial costs. Such initiatives underscore a growing demand as governments weave cassava deeper into national agricultural strategies. The International Atomic Energy Agency advocates for cassava production, highlighting nuclear and isotopic techniques. These methods aim to boost nitrogen use efficiency, crucial for optimizing yields in climate-stressed settings.

Industrial shift toward cost-effective starch sweeteners

Driven by price volatility in traditional sources and the superior functional properties of cassava, manufacturing industries are increasingly turning to cassava starch as a cost-effective alternative to corn and potato starches. Cassava starch's exceptional water-holding capacity and stable viscosity make it invaluable in paper manufacturing, enhancing strength and surface finish. The textile industry embraces cassava starch for sizing, finishing, and printing, drawn by its smooth viscosity and compatibility with synthetic fibers. Adhesive manufacturers favor cassava starch for paper bonding, citing its superior smoothness and bonding strength over alternatives. The pharmaceutical sector is increasingly using cassava starch as an excipient in tablet formulations, leveraging its hypoallergenic properties and consistent quality. Cost advantages are evident when cassava starch prices sit 15-20% below corn starch, a differential becoming common in Asian manufacturing hubs. Industrial processors are channeling investments into modified cassava starch production, crafting specialized derivatives for high-value applications like biodegradable packaging and pharmaceutical-grade excipients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility from pests and diseases | -1.4% | Sub-Saharan Africa, Southeast Asia | Short term (≤ 2 years) |

| Substitution threat from corn and potato starch | -0.8% | Global, particularly in established industrial markets | Medium term (2-4 years) |

| Land-use regulations curbing cassava expansion | -0.6% | Brazil, Indonesia, parts of Africa | Long term (≥ 4 years) |

| Low mechanisation elevating labour cost | -0.9% | Africa, small-scale farming regions globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price volatility from pests and diseases

Viral diseases severely disrupt cassava production. Cassava brown streak disease can cause yield losses of up to 70%, while cassava mosaic disease leads to production losses ranging from 25% to 95% in affected areas. These losses translate to an economic impact of USD 1.2-2.3 billion annually in sub-Saharan Africa alone[3]APS Net Features. "Cassava Mosaic Disease: A Curse to Food Security in Sub-Saharan Africa." June 17, 2024. https://www.apsnet.org/edcenter/apsnetfeatures/Pages/cassava.aspx, leading to significant price volatility and undermining market predictability. Climate change worsens these issues by boosting whitefly populations, which transmit viral diseases. Additionally, drought conditions heighten cyanide toxicity in cassava roots, posing food safety concerns in regions where cassava constitutes two-thirds of the diet. In the Democratic Republic of Congo, cassava mosaic disease results in yield losses of 25-95% across various altitude agroecosystems, with early infections inflicting the most damage. Many producing regions lack adequate disease surveillance systems, hindering early intervention and perpetuating price instability. The concentration of cassava production in tropical regions, which are prone to disease, creates a systemic vulnerability impacting global supply chains and pricing mechanisms.

Substitution threat from corn and potato starch

Industrial users are increasingly turning to cassava starch, weighing it against corn and potato alternatives, focusing on functional performance and cost. For cassava to remain economically viable in animal feed, its price must be 60-70% that of maize. While corn starch boasts established supply chains and consistent quality, leading to switching costs for processors, especially in developed markets, potato starch's superior gel strength and clarity in select food applications pose challenges for cassava's premium market penetration, even with cassava's cost edge. Historically, the EU's Common Agricultural Policy favored cassava imports for livestock feed. However, recent shifts towards regional grain production have diminished cassava's competitive stance. Research indicates cassava can replace up to 50% of maize in broiler diets without performance loss, but exceeding this level hampers feed efficiency. Industrial buyers, wary of supply chain disruptions, lean towards established starch sources over cassava, especially when consistent quality is paramount. Furthermore, the rise of genetically modified corn with enhanced starch properties amplifies the competitive challenge for cassava in industrial uses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Native Starch Dominance Amid Derivative Innovation

In 2024, Native Cassava Starch captures a 37.49% market share, underscoring its broad acceptance in food processing, industrial uses, and traditional applications. Its dominance is attributed to its cost-effectiveness and versatility, serving purposes from food thickening to paper manufacturing. Here, native starch's natural binding properties deliver performance without incurring extra processing costs. Industrial food processors favor native cassava starch for its neutral taste and gluten-free nature, aligning with the rising consumer demand for transparency in clean-label formulations.

Modified Cassava Starch and its derivatives emerge as the fastest-growing segment, boasting an 8.63% CAGR forecasted through 2030. This growth is fueled by innovative chemical modifications that bolster functional properties for niche applications. In Indonesia, the modified cassava starch market is on an upward trajectory, with local production satisfying a mere 1% of domestic demand. This gap signals a lucrative opportunity for foreign direct investment. While Cassava Flour enjoys consistent demand in bakeries, Cassava Chips find their primary use as animal feed and export items. Cassava Roots hold significance for fresh consumption in traditional markets. Additionally, the 'Others' category, encompassing pellets, pearls, and sago, is witnessing niche growth in specialty food applications.

By Form: Dried Products Lead While Frozen Innovation Accelerates

In 2024, dried cassava products command a dominant 51.95% market share, capitalizing on their extended shelf life, lower transportation costs, and a robust processing infrastructure tailored for large-scale industrial use. The dried variant's popularity is largely due to its versatility: it's favored for starch extraction, animal feed production, and in export markets where regulations prioritize dehydrated products with specific moisture content. Processing facilities in Thailand and Vietnam have fine-tuned their dried cassava production to align with international quality benchmarks, bolstering the segment's leading market position.

Frozen cassava is the segment witnessing the most rapid growth, boasting a 9.28% CAGR projected through 2030. This surge is attributed to advancements in freezing technologies that not only preserve nutritional value but also extend shelf life, catering to both retail and food service sectors. Research from Indonesia highlights the successful development of frozen cassava products, boosting market value and opening new avenues for rural communities. While fresh cassava holds its ground in local markets and ethnic food sectors, especially in North America, imports cater to the rising immigrant demographic craving traditional foods. The uptick in the frozen segment aligns with urbanization trends and a shift in consumer preferences towards convenient, ready-to-cook cassava products that retain their fresh attributes.

By End-Use Industry: Food Applications Anchor Growth While Biofuels Surge

In 2024, Food and Beverage applications dominate with a 61.64% market share, underscoring cassava's pivotal role as both a dietary staple and an industrial food ingredient worldwide. Within this realm, the bakery and confectionery sectors significantly boost volumes by using cassava flour as a wheat substitute and a gluten-free option. Meanwhile, snacks and convenience foods capitalize on cassava's unique texture and processing traits. Beverage producers harness cassava starch for thickening and stabilization, especially in dairy alternatives and functional drinks aimed at health-conscious consumers. This segment's prominence highlights cassava's adaptability in food processing and its resonance with clean-label trends that prioritize natural ingredients over synthetic ones.

Biofuels emerge as the fastest-growing segment, boasting a 9.74% CAGR through 2030. This surge is driven by government mandates for renewable fuel blending and the advantages cassava offers as a feedstock from a non-food crop. Brazil's ethanol production hit 31.66 billion liters in 2022, showcasing the segment's growth potential. Concurrently, Indonesia's ambition of achieving 1.2 billion liters of bioethanol by 2030 further fuels demand. In the realm of Animal Feed, cassava stands out as a cost-effective alternative to maize, with studies indicating a 25-30% savings in poultry feed formulations. Beyond food, cassava starch finds its way into industrial applications like paper, packaging, textiles, and adhesives. The Pharmaceuticals and Personal Care sectors also appreciate cassava for its hypoallergenic traits and consistent quality standards.

Geography Analysis

In 2024, North America commands a dominant 31.48% share of the market, driven by strong ethnic food consumption, industrial starch applications, and a reliable import infrastructure. The region's market leadership is supported by growing Hispanic and Asian populations, which increase fresh cassava demand. Industrial processors utilize cassava starch in food manufacturing, paper production, and pharmaceuticals. Fresh cassava imports are rising due to ethnic population growth and interest in ethnic foods among non-immigrants, though product recognition remains limited outside traditional user groups. Canada's food processing industry increasingly adopts cassava starch for gluten-free products, while the U.S. maintains high demand for cassava-based animal feed supplements.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 6.37% through 2030. The region is both the world's largest cassava producer and a growing consumer market for processed cassava products. Thailand leads global cassava starch exports, valued at USD 1.49 billion in 2023, while Vietnam's USD 1.06 billion export value highlights its production capacity. China's role as a major importer drives demand, with projections of 21-23 million tons of additional cassava imports needed for food and ethanol production. The Philippines' cassava industry is expanding, supported by a PHP 756.24 million (USD 13.5 million) investment from Korean firm Daesang in a tapioca starch facility, increasing national production by 9%. Indonesia's modified cassava starch market offers significant foreign investment opportunities, as local production meets only 1% of domestic demand despite high industrial requirements.

Europe and other regions maintain smaller but stable market positions. The European Union relies on imports for livestock feed applications under the Common Agricultural Policy framework. Africa's cassava production, led by Nigeria's 63 million tonnes, focuses on domestic consumption and food security rather than export markets. Latin America, driven by Brazil's biofuel programs and industrial applications, shows moderate growth potential as governments prioritize renewable energy and food security initiatives favoring cassava cultivation and processing.

Competitive Landscape

The global cassava market, with a concentration score of 4 out of 10, showcases moderate fragmentation. This score highlights ample opportunities for capacity expansion and new entrants, especially as established players anchor themselves in regional strongholds rather than pursuing global integration. Companies boasting integrated supply chains — from cultivation and processing to distribution — stand to gain, especially in major producing regions like Thailand, Vietnam, and Brazil, where their closeness to raw materials translates to cost benefits. Moreover, technology adoption is proving pivotal; leading processors are channeling investments into gene-edited, virus-resistant cassava varieties and cutting-edge starch modification techniques, aiming to boost both product quality and yield consistency.

Strategic trends indicate a rise in vertical integration, with processors aiming to mitigate supply chain risks tied to disease outbreaks and price fluctuations. In contrast, smaller entities are carving out niches, focusing on organic cassava products and specialized industrial starches. Notably, there's a gap in modified cassava starch production in regions with high industrial demand but scant local processing. Take Indonesia, for instance: its domestic production satisfies a mere 1% of the demand for modified starches.

Meanwhile, the landscape is witnessing the emergence of disruptors. Biotechnology firms are pioneering enhanced cassava varieties via gene editing, and agri-tech companies are rolling out mechanization solutions, tackling labor cost issues in traditional producing areas. The competitive arena increasingly favors those melding age-old processing know-how with cutting-edge agricultural technologies and sustainable practices, all while staying attuned to environmental standards and consumer inclinations.

Cassava Industry Leaders

-

Cargill, Inc

-

Ingredion Incorporated

-

Tate & Lyle PLC

-

Tereos Group

-

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Natural Grocers®, the largest family-run organic and natural grocery chain in the U.S., has added three new non-GMO Peruvian chip varieties to its product lineup. The newly introduced snacks, certified non-GMO among other accolades, feature: Sea Salt Sweet Potato Chips, Sea Salt Kettle Potato Chips, and Sea Salt Cassava Chips.

- November 2024: YARP Foods, a notable victor of the KIC 2024 AgriTech Challenge Pro, inaugurated its latest cassava flour production facility, situated in Akumsa Dumase within the Bono East Region.

Global Cassava Market Report Scope

| Cassava Roots |

| Cassava Chips |

| Cassava Flour |

| Native Cassava Starch |

| Modified Cassava Starch & Derivatives |

| Others |

| Fresh |

| Dried |

| Frozen |

| Food and Beverage | Bakery and Confectionery |

| Snacks and Convenience Foods | |

| Beverages | |

| Animal Feed | |

| Industrial | Paper and Packaging |

| Textile | |

| Adhesives | |

| Biofuels | |

| Pharmaceuticals and Personal Care |

| By Product Type | Cassava Roots | |

| Cassava Chips | ||

| Cassava Flour | ||

| Native Cassava Starch | ||

| Modified Cassava Starch & Derivatives | ||

| Others | ||

| By Form | Fresh | |

| Dried | ||

| Frozen | ||

| By End-Use Industry | Food and Beverage | Bakery and Confectionery |

| Snacks and Convenience Foods | ||

| Beverages | ||

| Animal Feed | ||

| Industrial | Paper and Packaging | |

| Textile | ||

| Adhesives | ||

| Biofuels | ||

| Pharmaceuticals and Personal Care | ||

Key Questions Answered in the Report

What is the projected value of the cassava market by 2030?

The cassava market is expected to reach USD 116.27 billion by 2030.

Which region is forecast to grow fastest through 2030?

Asia-Pacific is projected to post a 6.37% CAGR through 2030.

Which product type currently leads in market share?

Native Cassava Starch held 37.49% share of the cassava market in 2024.

How significant is biofuel demand for future growth?

Biofuels represent the fastest-growing end-use segment with a 9.74% CAGR forecast to 2030, buoyed by blending mandates in Brazil and Indonesia.

What is the primary restraint facing cassava producers?

Viral diseases such as brown streak and mosaic drive yield losses up to 95%, introducing price volatility that dampens growth.

Page last updated on: