Coconut Syrup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

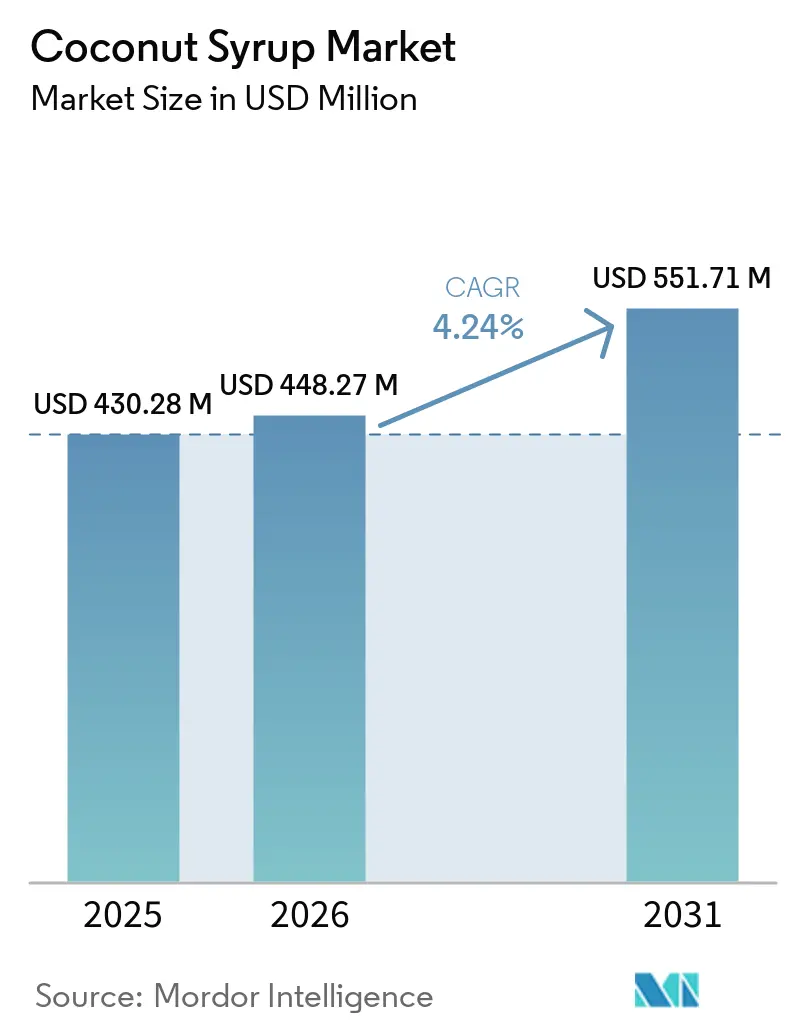

| Market Size (2026) | USD 448.27 Million |

| Market Size (2031) | USD 551.71 Million |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coconut Syrup Market Analysis by Mordor Intelligence

The coconut syrup market size was valued at USD 430.28 million in 2025 and estimated to grow from USD 448.27 million in 2026 to reach USD 551.71 million by 2031, at a CAGR of 4.24% during the forecast period (2026-2031). The coconut syrup market is expanding as more consumers move away from refined sweeteners and seek plant-based options that align with clean-label, lower-sugar, and digestive health preferences, especially when a product can support multiple wellness claims in the same formulation. Coconut syrup has a lower glycemic profile than refined sugar and also contains inulin, giving food and beverage companies a practical way to combine sweetness, simpler ingredient decks, and prebiotic positioning in a single ingredient system. The coconut syrup market also benefits from a strong supply base in Asia-Pacific, while demand is broadening in import-heavy regions where sugar reduction, transparency, and premium certification are shaping purchasing behavior in retail and food manufacturing channels. Competitive activity remains spread across flavor houses, organic specialists, and niche syrup brands, keeping the coconut syrup market moderately fragmented rather than concentrated in a few dominant producers. Growth still faces practical limits because raw sap is highly perishable and authenticity checks remain costly, so operational control and traceability continue to matter as much as brand positioning in the coconut syrup market.

Key Report Takeaways

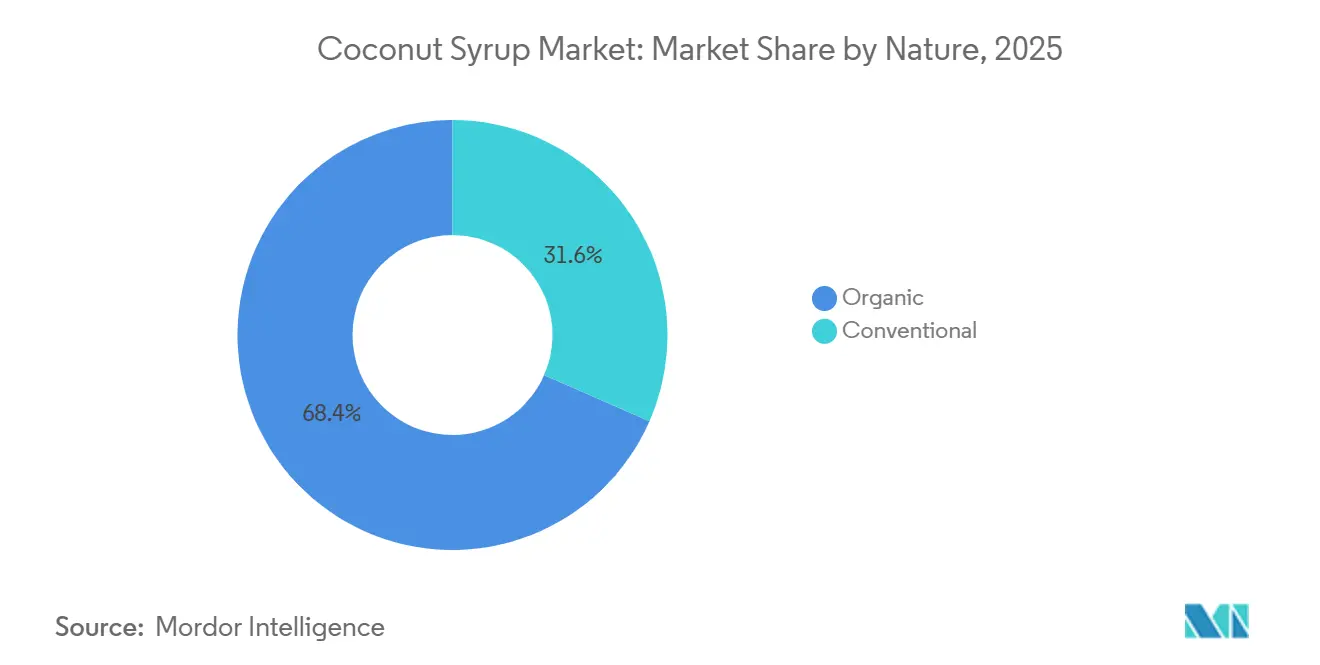

- By nature, conventional held 68.43% of the coconut syrup market share in 2025, while organic is forecast to expand at 6.21% through 2031.

- By end user, food and beverage manufacturing accounted for 43.58% of the coconut syrup market size in 2025, while nutraceutical and sports nutrition are projected to advance at 6.86% through 2031.

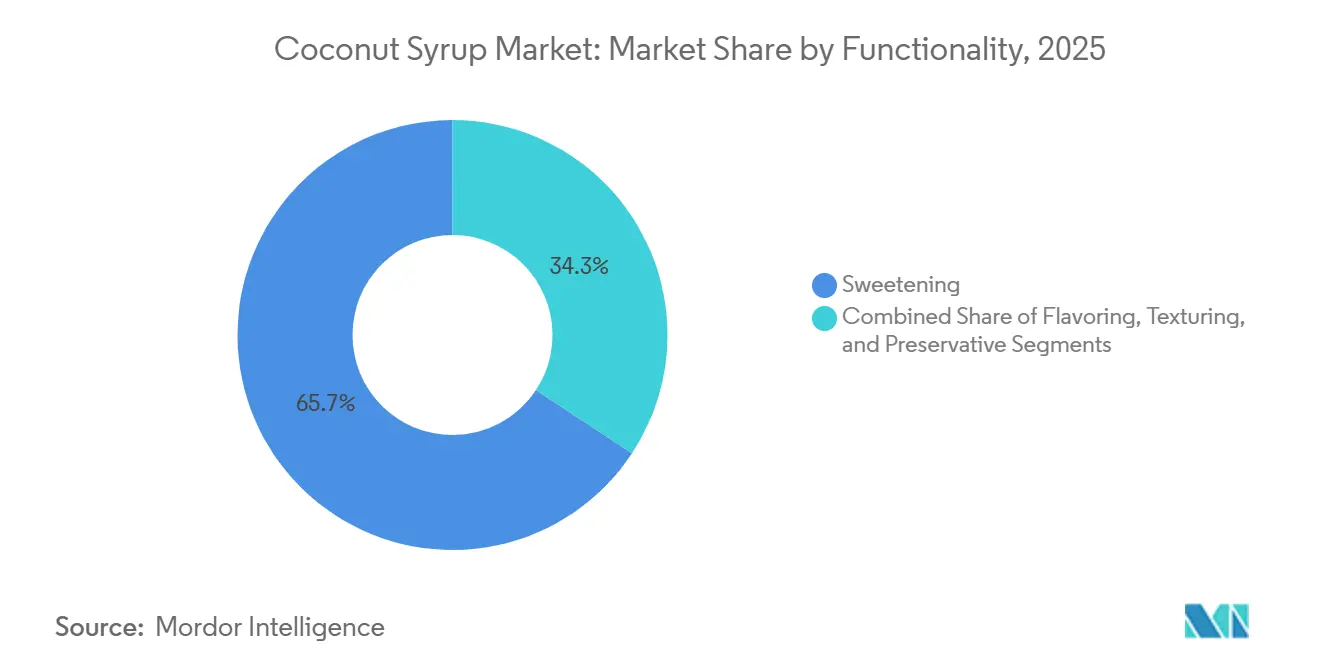

- By functionality, sweetening represented 65.74% of total demand in 2025, while flavoring is expected to grow at 5.74% through 2031.

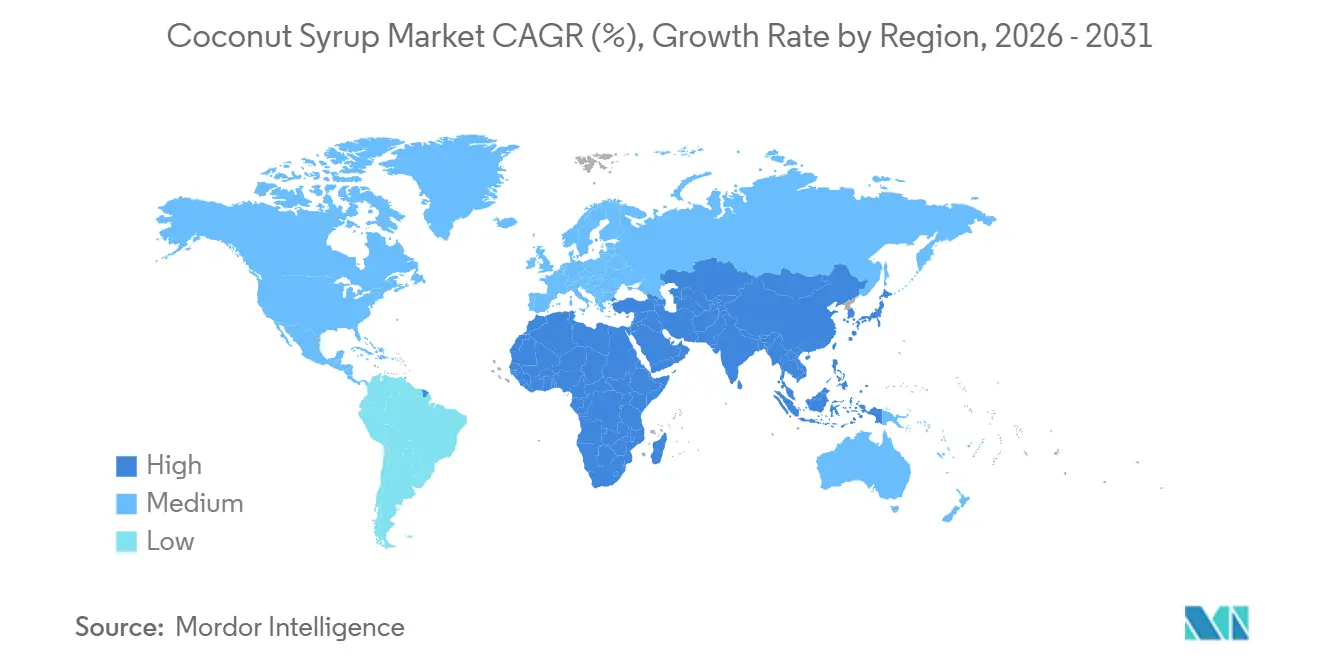

- By geography, Asia-Pacific held 46.87% of the global coconut syrup market share in 2025, while the Middle East and Africa are forecast to rise at 5.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coconut Syrup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for low-GI natural sweeteners | +1.2% | Global, strongest pull in North America and Europe | Short term (≤ 2 years) |

| Expansion of keto-friendly and low-carb coconut-based sweetener variants | +0.8% | North America and Europe, spill-over to APAC urban markets | Medium term (2-4 years) |

| Rising barista preference for coconut syrup in dairy-free flavored beverages | +0.7% | North America, Europe, APAC including South Korea, Australia, and Singapore | Short term (≤ 2 years) |

| Product innovation in infused coconut syrups | +0.6% | North America, Europe, APAC | Medium term (2-4 years) |

| Increasing penetration of coconut syrup in RTD beverages | +0.9% | APAC core, spill-over to North America and MEA | Medium term (2-4 years) |

| Adoption in sports nutrition as a natural energy booster ingredient | +0.5% | North America and Europe, early gains in South Korea and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for Low-GI natural sweeteners

The metabolic-health narrative has become the most commercially actionable positioning platform for coconut syrup in both retail and food manufacturing channels. A clinical study in the Asia-Pacific Journal of Science and Technology confirmed that organic coconut flower syrup (OCFS) carries a GI of 51.2 and, when enriched with 3% inulin, falls to 45.4, well within the low-GI threshold of 55, while simultaneously producing a significantly lower serum insulin response compared to a glucose reference food. The 2025 IFIC Food & Health Survey reinforces the commercial opportunity: 63% of Americans remained concerned about sugar consumption in 2025, and 75% were limiting or avoiding sugars, with 41% specifically seeking "natural" label claims as a primary purchasing criterion[1]Source: International Food Information Council, “2025 IFIC Food & Health Survey: The Full Report,” International Food Information Council, ific.org. What is frequently overlooked in mainstream analysis is that coconut syrup's inulin content, approximately 4.7 g per 100 g, allows manufacturers to stack a prebiotic gut-health claim alongside the glycaemic index benefit, effectively doubling the functional claim real estate without changing the base formula. In an environment where digestive health ranked among the top four health goals for American consumers in 2025, this multi-claim positioning offers a meaningful differentiation pathway that single-attribute sweeteners cannot replicate.

Rising barista preference for coconut syrup in dairy-free flavored beverages

The specialty coffee channel is restructuring demand for coconut syrup beyond seasonal menu cycles. Starbucks added toasted coconut syrup as a permanent year-round ingredient to its global menu in March 2026, debuting it in the Toasted Coconut Cream Cold Brew, the Toasted Coconut Latte, and the limited-time Iced Ube Coconut Macchiato, institutionalizing coconut syrup demand across the world's largest coffeehouse procurement chain. Monin named Toasted Coconut its 2026 Flavor of the Year in January 2026, citing 40% growth in coconut bottle sales across 2025 and noting that 63% of consumers like or love the coconut flavor profile; the company also identified 48% consumer interest in "savory" sweet-and-savory flavor combinations as a major format innovation driver[2]Source: Monin US, “Monin Announces Toasted Coconut as 2026 Flavor of the Year,” Monin US, monin.us. Coconut syrup occupies a unique intersection, allergen-free, vegan-compatible, and clean-label, that no other major flavor syrup achieves simultaneously, giving it structural advantages as dairy-free milk alternatives penetrate café menus globally. As customized cold and flavored beverages continue to gain share within specialty coffee, coconut syrup functions as both a sweetener and a flavor modifier, enabling operators to serve multiple dietary preference groups with a single SKU.

Increasing penetration of coconut syrup in ready-to-drink (RTD) beverages

RTD beverage manufacturers are incorporating coconut-derived sweetening bases to satisfy "clean energy" and "functional hydration" positioning requirements that synthetic sweeteners cannot credibly fulfill. In May 2026, Pop & Bottle entered the functional hydration segment with a Matcha Coconut Water RTD line, including Pomegranate Berry and Citrus varieties, available in Sprouts stores nationwide. Each SKU delivers 600-640 mg of natural electrolytes and 25 mg of caffeine from organic ingredients, with no added sugar. The strategic leverage for coconut syrup in RTD applications extends beyond sweetening: its viscosity enables formulators to reduce or eliminate added stabilizers and emulsifiers, improving overall clean-label scores, a consideration that has material consequences for market access in EU and North American natural food retail channels. Indonesian GMP- and FSSC 22000-certified producers are already offering custom-concentration coconut nectar syrups (at 70% Brix and above) to RTD private-label mandates in North America and Europe, indicating that supply-side capability is moving ahead of mainstream brand adoption. This forward positioning by ingredient suppliers creates a structural condition where large RTD brands can scale coconut-based sweetening without lead-time risk once the category tipping point is reached.

Product innovation in infused coconut syrups

Infused coconut syrups combining coconut nectar with botanical flavor additives such as vanilla, cardamom, chili, and adaptogens represent one of the highest-margin growth pockets within the broader market. Coconut Cartel launched its Coconut Nectar product in September 2024, positioning it as a premium mixology ingredient derived from organic coconut palm sap in Mexico, delivering a caramel-like sweetness, zinc, iron, and 17 amino acids, and targeting the premium cocktail and home-mixology channels. In November 2025, The Groovy Food Company (UK) introduced Organic Coconut Syrup at a GBP 4.00 (approximately USD 5.00) RRP in its first major product launch in four years, emphasizing zero-waste sourcing from coconut palm sap that is otherwise discarded, a regenerative framing that resonates with sustainability-conscious European retail buyers. A technical moat exists for producers who adopt the CPCRI (Central Plantation Crops Research Institute, India) chiller method, which prevents fermentation during sap collection, reduces processing time, and preserves bioactive phenolic compounds, yielding a higher-quality infusion base that commodity-grade open-vessel production cannot replicate. This process differentiation is becoming a credentialing point in B2B RFQ discussions with functional food manufacturers, particularly in Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life of raw sap affecting production efficiency | -0.4% | APAC including the Philippines, Indonesia, and India | Short term (≤ 2 years) |

| Lack of standardized grading systems for coconut syrup quality | -0.2% | Global, most acute in EU and North American export markets | Long term (≥ 4 years) |

| Seasonal variability in sap yield due to climatic conditions | -0.3% | APAC including India, Indonesia, and the Philippines, and South America including Brazil | Medium term (2-4 years) |

| Adulteration risks and authenticity testing costs | -0.2% | Global, with the highest enforcement burden in the EU, Canada, and the United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short shelf life of raw sap affecting production efficiency

Freshly tapped coconut inflorescence sap begins fermenting within hours of collection, constraining viable processing windows and imposing significant cold-chain and logistics requirements on upstream producers. Research at the Central Plantation Crops Research Institute (CPCRI), India, found that sap must be collected twice daily in sanitized containers and processed promptly to prevent microbial contamination; traditional open-vessel collection methods introduce insect fragments, pollen, and elevated yeast and mould counts, which complicate compliance with export quality standards. The raw yield constraint amplifies this problem: approximately 1 kg of coconut syrup requires the output of four trees per day under normal conditions, making large-scale, consistent supply inherently difficult even before post-harvest perishability is factored in. Smaller artisan producers, who represent a significant share of APAC-origin supply, typically lack the refrigeration infrastructure needed to extend the viable processing window, effectively capping their ability to fulfill long-term commercial contracts with global food manufacturers. Until cold-chain infrastructure investment in key producing regions reaches a level comparable to competing sap-based sweetener supply chains (e.g., maple syrup in North America), this structural constraint will continue to weigh on capacity utilisation rates for mid-scale processors.

Adulteration risks and authenticity testing costs

Food fraud is a structurally persistent constraint on the credibility of the coconut syrup market, driven by the significant price premium that incentivizes adulteration with cheaper cane, corn, or beet sugar. Research published in the European Food Research and Technology journal found that coconut sugar traded at 15-45 EUR per kg versus 0.75 EUR per kg for refined sugar in European markets, a 20-60× price differential that creates a strong financial motivation for adulteration throughout the supply chain. A peer-reviewed authentication study using stable carbon isotope analysis found that 31 of 109 Indonesian coconut sugar samples had δ13C values above the 24.8‰ threshold, indicating the addition of excess C4 sugar (cane or corn) beyond the internationally accepted 5% seeding allowance. The Canadian Food Inspection Agency's 2023-2024 Food Fraud Annual Report found that 21% of sampled coconut products failed authenticity tests, with Thailand and Vietnam among the primary sources of non-conforming products[3]Source: Canadian Food Inspection Agency, “Food Fraud Annual Report 2023 to 2024,” Canadian Food Inspection Agency, inspection.canada.ca. The cost of ATR-FTIR, IRMS, and ED-XRF authentication testing, with per-sample costs at accredited ISO 17025 laboratories running into hundreds of dollars, disproportionately disadvantages smaller certified-organic producers, effectively creating a quality assurance tax that erodes margin and competitiveness relative to large-scale players with dedicated QA budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Conventional Scale Holds Volume While Organic Gains Pricing Power

Conventional coconut syrup held 68.43% of the by nature segment in 2025, and that lead was rooted in volume-driven buying patterns across industrial food manufacturing and foodservice, where procurement teams focus first on cost consistency and supply reliability. In the coconut syrup market, conventional products remain the easier fit for large bakery, confectionery, sauce, and beverage runs because certification premiums can quickly raise formulation costs in high-volume applications. That practical cost gap explains why mainstream demand still concentrates in conventional formats even as consumer interest in traceability and sustainability rises. At the same time, organic is forecast to grow at 6.21% through 2031, indicating this tier is widening faster than the broader coconut syrup market as premium import channels increasingly demand verified origin and stricter process documentation. Buyers in Europe and North America are no longer treating organic certification as a niche extra; they are now using it as a first filter for supplier selection in premium natural sweetener portfolios.

This change matters because it narrows the effective field of competitors and favors suppliers that can prove full chain control from sap collection to finished syrup specification. The coconut syrup industry is therefore seeing organic certification operate as both a pricing tool and a gatekeeping mechanism, especially where USDA Organic, EU Organic, and regenerative credentials are stacked together. Big Tree Farms illustrates this shift because the company said in August 2025 that it works with more than 17,000 Indonesian smallholder farmers and is building growth across retail, private-label, and B2B channels under a certified model. The broader effect on the coconut syrup market is that organic supply at scale is becoming more credible, which reduces one of the barriers that historically limited adoption beyond specialty health food shelves.

By End User: Manufacturing Leads Current Demand While Sports Nutrition Raises the Growth Ceiling

Food and beverage manufacturing accounted for 43.58% of the end-user segment in 2025, indicating that the coconut syrup market still depends most heavily on industrial sweetening demand rather than purely on retail shelf movement. That position reflects coconut syrup’s wide use as a sucrose substitute in bakery, confectionery, condiments, syrup systems, and ready-to-drink beverages where buyers want a plant-based sweetener that also supports cleaner labels. Foodservice remains a major outlet as well, as café and beverage operators use coconut syrup in flavored drinks, specialty coffee, and dairy-free menu items, where one syrup can meet multiple dietary preferences. The fastest-growing outlet is nutraceutical and sports nutrition, which is forecast to rise at 6.86% through 2031 as formulators move toward ingredients that support natural energy positioning without weakening clean sports claims. This makes the coconut syrup market more attractive to brands selling active lifestyle products because it connects sweetness with a more natural mineral and amino acid story than conventional sugar systems.

Retail and household demand are becoming more format-specific, and online channels are helping the category reach consumers in markets where specialty physical distribution remains limited. GymBeam’s 2025 listing of BIO Coconut Syrup on its sports nutrition and natural food e-commerce platform reflects that widening access, even though physical placement is still uneven across several European markets. The coconut syrup industry is also benefiting from at-home drink customization trends because consumers increasingly recreate café-style beverages in domestic settings rather than relying only on coffeehouse purchases. This creates a longer-term pull for shelf-stable branded syrups, and it gives mid-market suppliers an opening to build repeat demand outside formal foodservice contracts.

By Functionality: Sweetening Stays Core While Flavoring Builds Premium Value

Sweetening accounted for 65.74% of the coconut syrup market in 2025, underscoring that the coconut syrup market remains led by its role as a direct replacement for refined sugar in both packaged foods and beverage systems. This structural lead is unlikely to change quickly because most buyers still enter the category through sweetness needs rather than through texture or preservation benefits. Texturizing remains the second functional layer because coconut syrup’s natural viscosity helps improve mouthfeel and moisture retention in baked goods, confectionery, dairy alternatives, and plant-based protein products. Flavoring is forecast to grow at 5.74% through 2031, faster than the total coconut syrup market and reflecting a stronger commercial focus on caramel, toasted, and butterscotch notes rather than sweetness alone. Monin’s 2026 global focus on toasted coconut shows how branded syrup makers are turning that sensory profile into a premium retail and foodservice offering rather than treating it as a supporting flavor.

The preservative role remains small in volume terms, but it is gaining attention because coconut sap contains phenolic compounds with antioxidant activity that can support cleaner ingredient positioning in selected formulations. This gives suppliers a way to present coconut syrup as a multi-functional ingredient rather than a one-purpose sweetener, which matters when procurement teams compare formulation complexity across categories. In the coconut syrup industry, this dual role between sweetening and flavoring creates a clear split between scale-oriented industrial supply and higher-margin infused specialty formats. The suppliers best placed to benefit are those that can back performance claims with traceability records, process evidence, and consistent finished-product specifications for multinational buyers.

Geography Analysis

Asia-Pacific accounted for 46.87% of the global market in 2025, and that leadership gives the coconut syrup market its clearest regional center of gravity. The region benefits from deep coconut cultivation, established processing knowledge, and a supply chain structure that links raw sap collection to export-oriented syrup production across several producing countries. Indonesia and the Philippines remain central to this position because they anchor a large share of global coconut output and continue to shape availability for downstream coconut sweetener processing. The coconut syrup market in this region also benefits from policy support for farm productivity and sector upgrading, including the extension of the Coconut Farmers and Industry Development Plan in the Philippines to 2028. That policy continuity matters because better planting material, farm support, and processing standards improve long-run sap availability and reduce some of the quality inconsistency that can slow export growth.

North America and Europe ranked behind Asia-Pacific in revenue terms, but their demand dynamics differ from the production-centered pattern seen in Asia-Pacific. In North America, the United States remains the main demand center, and the coconut syrup market is supported by strong consumer attention to sugar reduction, ingredient transparency, and natural labeling claims. Canada adds a stricter authenticity layer because CFIA monitoring has increased pressure on importers and suppliers to prove compliance, which helps raise the competitive floor for certified products entering the region. In Europe, premium demand is tied more closely to organic certification, traceability, and retailer confidence, so suppliers that can document chain integrity are better placed to defend pricing and secure repeat placements.

The Middle East and Africa is forecast to grow at 5.46% through 2031, making it the fastest-growing regional segment in the coconut syrup market. Growth here is linked to sugar-reduction policy direction in the Gulf, stronger labeling discipline, and rising urban demand for low-GI sweetening alternatives in imported packaged foods and beverage applications. Halal certification has also become a practical market access condition, so exporters with both food safety and religious compliance credentials have a clear edge when serving Gulf retail and foodservice channels. South America remains smaller, but it is strategically relevant because Brazil is building greater domestic processing interest around coconut-derived sweeteners as health-focused retail demand expands in major metropolitan areas. Taken together, these regional shifts show that the coconut syrup market is no longer shaped only by where coconuts are grown, but also by where health regulation, certification demand, and premium retail standards are moving fastest.

Competitive Landscape

The coconut syrup market is moderately fragmented, as leading companies do not compete from identical positions, which is one reason it has not consolidated around a single dominant model. Monin, Torani, and Kerry Group’s DaVinci Gourmet bring broad flavor portfolios and established distribution, while Big Tree Farms brings vertically integrated sourcing and organic depth, and Amoretti and smaller regional brands compete through premium specialization. This mix means the coconut syrup market is shaped by several strategic models simultaneously, including flavor-house breadth, certification-led origin control, and specialty café or mixology focus. As a result, competition depends as much on channel fit and formulation use as it does on headline scale.

Monin has taken one of the clearest category-building steps by naming Toasted Coconut its 2026 Flavor of the Year and extending the product through its international distribution system, which gives coconut syrup much wider menu and retail visibility than a limited launch would have delivered. The same company also expanded its sugar-free coconut positioning, showing that leading flavor houses are trying to meet both indulgence and calorie-conscious demand within the same brand architecture. Big Tree Farms has followed a different path by linking product development to its organic sourcing base and farmer network, and by using that supply model to support growth across retail, private-label, and B2B business lines. Its 2025 innovation push and farmer-linked certified sourcing show how the coconut syrup market is rewarding companies that can combine origin control with commercial flexibility rather than relying only on branding. The strategic lesson is clear, namely that companies with traceable supply, channel-specific product formats, and credible certification stacks are better placed to defend margins as authenticity scrutiny rises.

The white space in the coconut syrup market is still meaningful, especially in sports nutrition-grade products and in infused formats that combine flavor and function. Sports nutrition remains under-branded relative to the strength of forecast growth, which leaves room for suppliers that can meet stricter transparency expectations and position coconut syrup as a cleaner energy ingredient. There is also room in the functional flavored tier because no single brand has fully defined coconut syrup with botanicals, adaptogens, or electrolyte-led enhancement across global markets. Over the next few years, the coconut syrup market is likely to favor companies that can translate processing discipline, quality verification, and application support into long-term contracts with multinational food and beverage buyers rather than depending only on small-batch retail novelty.

Coconut Syrup Industry Leaders

Big Tree Farms

Monin

Torani

Kerry Group (DaVinci Gourmet)

Amoretti

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pop & Bottle (United States) entered the functional hydration segment with a new Matcha Coconut Water RTD line, available in Original, Pomegranate Berry, and Citrus varieties at Sprouts stores nationwide, each SKU delivering 600-640 mg of natural electrolytes and 25 mg of organic caffeine, with no added sugar.

- July 2025: Monin Americas has unveiled its latest flavor innovation: the 'Sugar Free Coconut' syrup. This no-sugar-added syrup encapsulates the creamy essence of coconut, delivering a smooth, tropical finish. Aimed at enhancing both beverages and desserts, this syrup infuses an indulgent island flair while aligning with wellness objectives.

- April 2025: President Ferdinand R. Marcos Jr. inaugurated the PHP350-million SUnRISE-ICPF in Misamis Oriental province. This public-private partnership seeks to transform the province's coconut industry. The facility aims to produce high-value coconut products, moving beyond the traditional copra. As per the Chief Executive, the initiative is set to directly benefit over 66,000 coconut farmers in the province.

Global Coconut Syrup Market Report Scope

Coconut syrup is a natural sweetener derived from the sap of coconut palm flowers, widely used for its distinctive flavor and functional properties in food and beverage applications. The coconut syrup market is segmented by nature, end user, functionality, and geography. By nature, the market includes organic and conventional coconut syrup products. Based on end user, the market covers food and beverage manufacturing, foodservice, nutraceutical and sports nutrition, and retail/household applications. The retail/household segment is further categorized into supermarkets/hypermarkets, health-food/specialty stores, online retailers, and others. Based on functionality, the market is segmented into sweetening, texturizing, flavoring, and preservative functions. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million).

| Organic |

| Conventional |

| Food and Beverage Manufacturing | |

| Foodservice | |

| Nutraceutical and Sports Nutrition | |

| Retail/Household | Supermarkets/Hypermarkets |

| Health-food/Specialty Stores | |

| Online retailers | |

| Others |

| Sweetening |

| Texturizing |

| Flavoring |

| Preservative |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Iran | |

| Turkey | |

| Rest of Middle East and Africa |

| By Nature | Organic | |

| Conventional | ||

| By End User | Food and Beverage Manufacturing | |

| Foodservice | ||

| Nutraceutical and Sports Nutrition | ||

| Retail/Household | Supermarkets/Hypermarkets | |

| Health-food/Specialty Stores | ||

| Online retailers | ||

| Others | ||

| By Functionality | Sweetening | |

| Texturizing | ||

| Flavoring | ||

| Preservative | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for coconut syrup through 2031?

The coconut syrup market is projected to move from USD 448.28 million in 2026 to USD 551.71 million by 2031, with a 4.24% CAGR over the forecast period.

Which region leads global demand for coconut syrup?

Asia-Pacific led in 2025 with 46.87% of global value, supported by its strong raw material base and established processing network.

Which end-user group contributes the most revenue?

Food and beverage manufacturing was the largest end-user segment in 2025 with a 43.58% share, driven by use in bakery, confectionery, condiments, and beverage applications.

Which segment is growing the fastest by end user?

Nutraceutical and sports nutrition is the fastest-growing end-user segment, with a forecast CAGR of 6.86% from 2026 to 2031.

Why are buyers shifting toward coconut syrup instead of refined sugar?

The shift is tied to lower glycemic positioning, natural label appeal, and the presence of inulin, which helps brands support digestive health claims along with sweetness.

Page last updated on: