Coconut Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

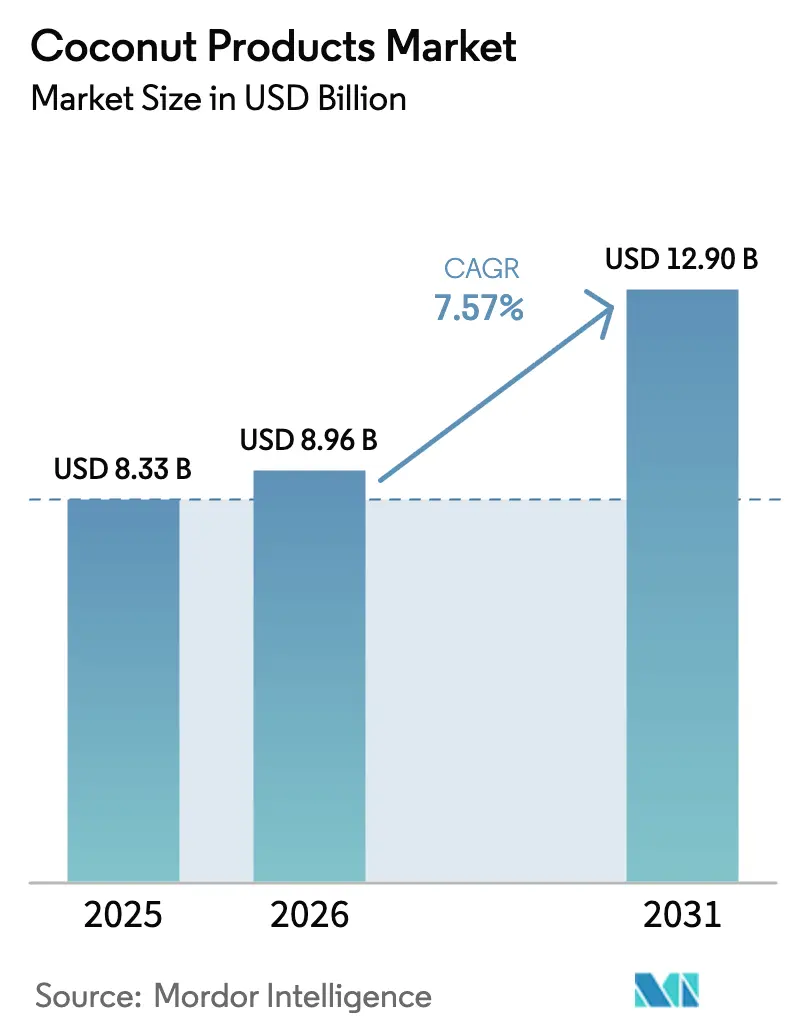

| Market Size (2026) | USD 8.96 Billion |

| Market Size (2031) | USD 12.90 Billion |

| Growth Rate (2026 - 2031) | 7.57% CAGR |

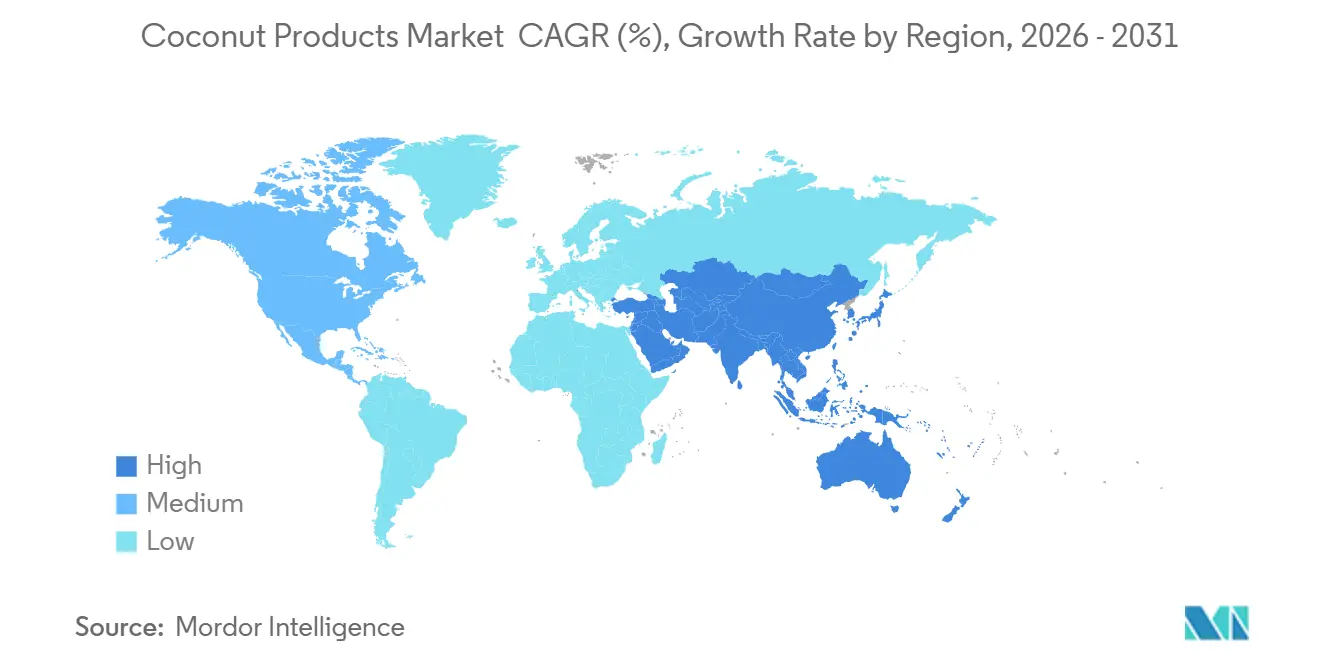

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coconut Products Market Analysis by Mordor Intelligence

The Coconut Products Market size was valued at USD 8.33 billion in 2025 and is estimated to grow from USD 8.96 billion in 2026 to reach USD 12.90 billion by 2031, at a CAGR of 7.57% during the forecast period (2026-2031). This sustained expansion stems from rising demand for plant-based nutrition, clean-label ingredients, and functional hydration solutions that coconut-derived offerings uniquely satisfy. The Asia-Pacific region remains pivotal because the Philippines, Indonesia, Thailand, and India supply more than 70% of the world's coconuts, giving processors a structural cost advantage over import-reliant buyers in North America and Europe, according to the International Coconut Community. Liquid formats, such as coconut water and milk, continue to dominate retail shelves, yet solid and powder forms are gaining traction as ambient-stable solutions for bakery, confectionery, and sports nutrition blends. Rapid e-commerce adoption is enabling niche labels to bypass traditional gatekeepers and target health-conscious millennials who reward organic, fair-trade, and sustainability claims with brand loyalty. Competitive intensity remains moderate, as no single firm exceeds a low double-digit share, forcing incumbents and challengers alike to secure raw material supplies through vertical integration and long-term grower contracts.

Key Report Takeaways

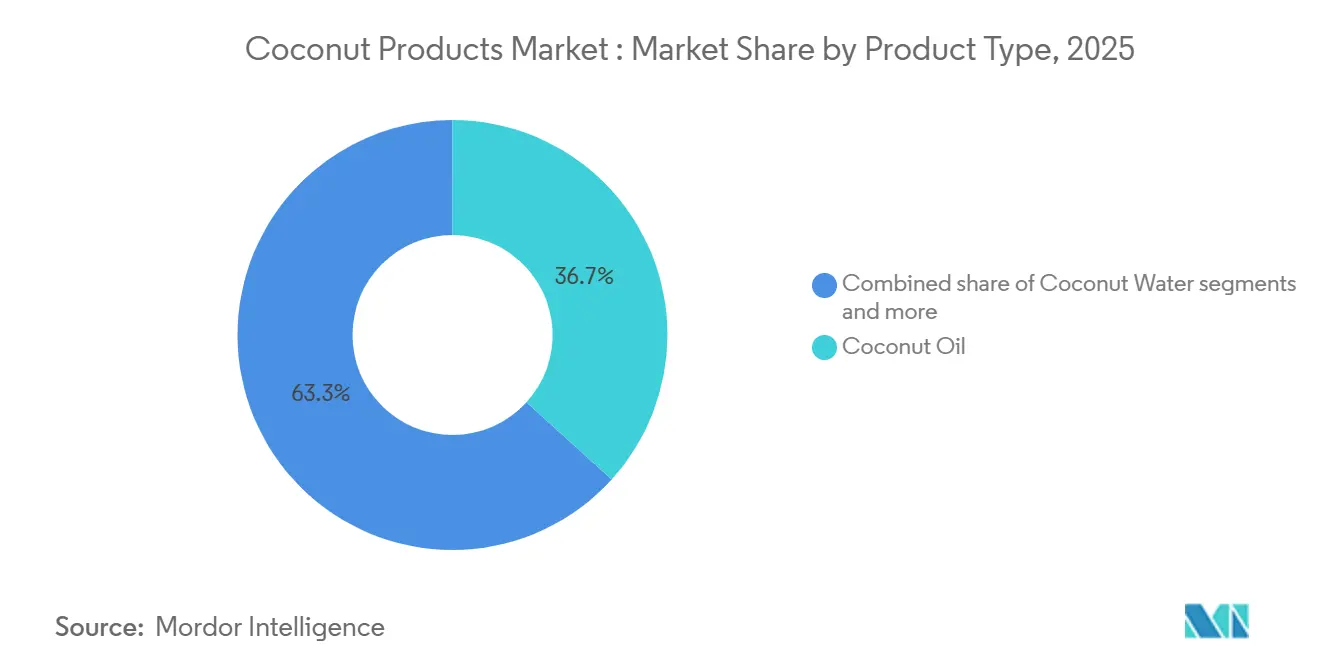

- By product type, coconut oil led with 36.72% revenue share in 2025; coconut milk is projected to expand at an 8.82% CAGR through 2031.

- By form, liquid formats accounted for 72.39% share of the coconut products market size in 2025, while solid and powder formats are advancing at a 9.64% CAGR to 2031.

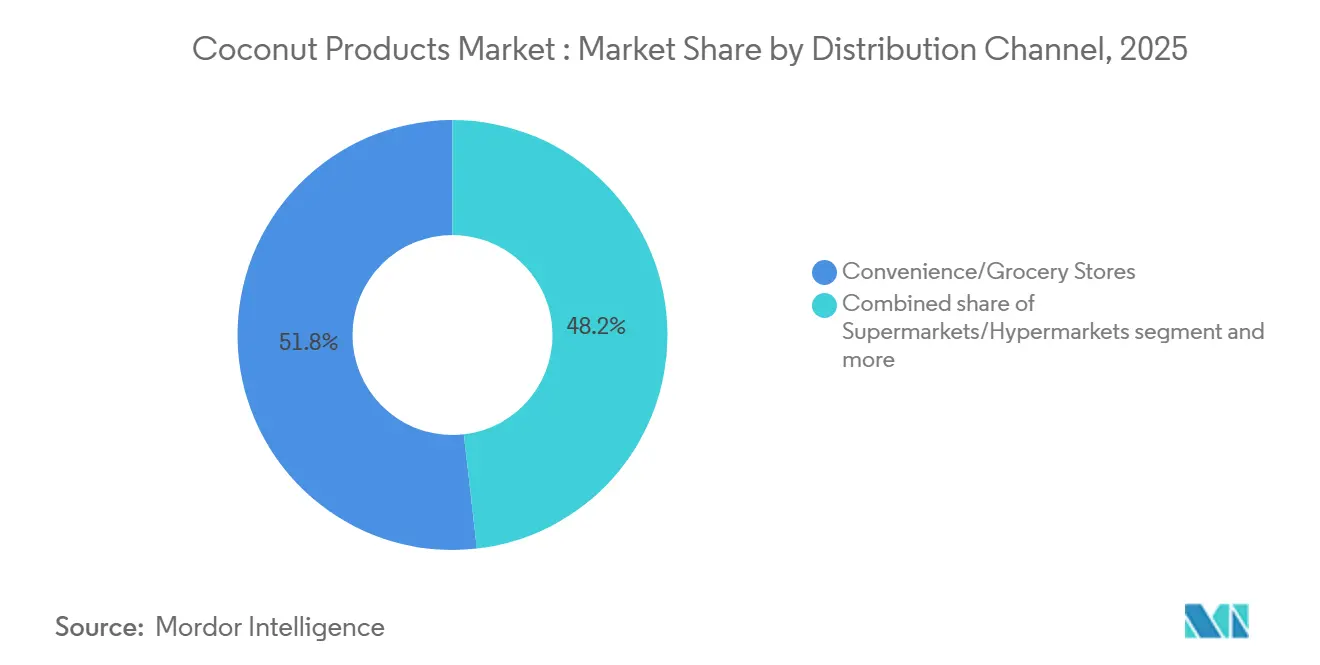

- By distribution channel, convenience and grocery stores held 51.81% of the coconut products market share in 2025, while online retail stores are projected to expand at a 9.98% CAGR through 2031.

- By geography, the Asia-Pacific region captured a 34.85% share of the coconut products market size in 2025 and is expected to expand at a 9.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coconut Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness driving demand for natural and plant-based products | +1.8% | Global with focus on North America and Europe | Medium term (2–4 years) |

| Coconut water gaining popularity as a low-calorie hydration beverage | +1.2% | North America, Europe, expanding to Asian cities | Short term (≤ 2 years) |

| Growth in vegan and dairy-free diets boosting demand for coconut milk and cream | +1.5% | Global, led by North America and Europe | Medium term (2–4 years) |

| E-commerce platforms expanding access to premium and organic coconut products | +0.9% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Growth of ayurveda and traditional medicine is reviving interest in coconut-based remedies | +0.8% | Asian core, spill-over to North America wellness markets | Long term (≥ 4 years) |

| Increasing global culinary use of coconut products is driving demand | +1.0% | Global, with regional variations in product preferences | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness is driving demand for natural and plant-based products

As consumers become more health-conscious, they're increasingly turning to coconut products, viewing them as natural alternatives to both processed foods and synthetic supplements. The 2025 United States Dietary Guidelines Advisory Committee has recommended replacing saturated fats with plant-based alternatives, further boosting the appeal of coconut oil. This regulatory nod not only spurs innovation in premium-priced virgin coconut oil and MCT (medium-chain triglyceride) oil derivatives but also underscores their perceived health advantages, such as improved metabolism and potential cardiovascular benefits[1]Source: US Department of Health and Human Services, “Scientific Report of the 2025 Dietary Guidelines Advisory Committee,” dietaryguidelines.gov. Additionally, the growing awareness of the environmental impact of food choices has positioned coconut products as sustainable options, aligning with the preferences of eco-conscious consumers. With the rising demand for clean-label products and the trend towards functional foods, coconut products are carving out a niche, satisfying both taste and wellness needs. These dynamics, combined with increasing consumer education on the benefits of plant-based alternatives, point to a robust growth trajectory for coconut products, suggesting a continued market expansion in the years ahead.

Coconut water gaining popularity as low-calorie hydration beverage

Coconut water is steadily replacing traditional sports drinks as consumers favor natural electrolytes with fewer calories and no added sugars, appealing strongly to health-conscious buyers. It offers hydration comparable to isotonic beverages while naturally providing potassium and magnesium. Brands are capitalizing on this shift, with The Vita Coco Company launching Vita Coco Spiked to tap into higher-margin alcoholic segments. E-commerce further fuels growth by effectively communicating functional and sustainability benefits. At the same time, advances in UHT processing, such as Tetra Pak’s Direct Ultra High Temperature (UHT) technology, have extended shelf life and expanded reach into markets with limited cold-chain infrastructure. These innovations have enabled product launches, such as Tata Consumer Products’ Lyfe+ coconut water in 2025, reinforcing coconut water’s competitive position in the global beverage market.

Growth in vegan and dairy-free diets boosting demand for coconut milk and cream

Rising dairy avoidance, driven by lactose intolerance, ethical considerations, and health perception, is expanding demand for coconut milk and cream, especially in foodservice and bakery applications where functionality and flavor are critical. In the U.S., 40% of adults consumed plant-based meat or dairy alternatives in 2024, with 24% doing so monthly, and coconut-based products hold a notable share despite competition from oat and almond products, according to the Good Food Institute[2]Source: Good Food Institute, “Consumer Snapshot: Plant-Based 2024,” gfi.org. Coconut milk’s high fat content and creamy texture make it a preferred option for dairy-free lattes, ice creams, and yogurts, where other alternatives struggle to match dairy's richness. This strength is reflected in The Coconut Collab’s GBP 1.5 million Series B raise in January 2024, which supports European expansion and highlights the resilience and defensible position of coconut-based products in indulgent plant-based dairy categories.

Growth of ayurveda and traditional medicine reviving interest in coconut-based remedies

Coconut oil, particularly virgin coconut oil, is experiencing renewed demand in India and Southeast Asia as consumers reconnect with traditional wellness practices, supported by the AYUSH Ministry's policies that promote Ayurvedic formulations. Used in roughly 40% of Ayurvedic medicines, coconut oil is benefiting from efforts to integrate traditional medicine into mainstream healthcare, boosting both domestic demand and export potential for certified organic and virgin variants. This has created a bifurcated market: low-margin commodity coconut oil for cooking and industrial use, and premium virgin coconut oil positioned for health and wellness applications. Brands such as Nutiva have capitalized on this shift by marketing Fair Trade Certified Virgin Coconut Oil, which undergoes extensive third-party testing, thereby appealing to transparency-driven consumers. As Ayurvedic-inspired wellness gains traction in Western markets, coconut oil is increasingly viewed as a functional health product rather than a basic cooking staple, which supports higher price points and reduces exposure to commodity price fluctuations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility due to weather-sensitive coconut farming affects market stability | -1.4% | Global, concentrated in Asia-Pacific producing regions | Short term (≤ 2 years) |

| Limited shelf life of fresh coconut products hampers supply chain efficiency | -0.8% | Global, acute in regions distant from production centers | Medium term (2–4 years) |

| Competition from alternative plant-based ingredients (e.g., almond, oat) limits growth | -1.1% | North America and Europe primarily, expanding to urban Asia-Pacific region | Medium term (2–4 years) |

| High processing and export costs reduce margins for manufacturers | -0.7% | Asia-Pacific producing regions, affecting global competitiveness | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price volatility due to weather-sensitive coconut farming affecting stability

Coconut farming is highly exposed to typhoons, droughts, and erratic monsoons, with climate shocks in 2024 quickly translating into supply shortages and price volatility. In the Philippines, Typhoons Kristine and Pepito damaged nearly 39,000 hectares of coconut farms, affecting over 1.2 million farmers and causing losses exceeding USD 20 million, while El Niño-driven droughts cut Indonesian yields by 15–20%, raising coconut oil production costs. These disruptions led to sharp export price increases, with desiccated coconut prices rising 26% year-over-year in the Philippines, 76.8% in Indonesia, and 62% in Sri Lanka[3]Source: International Coconut Community, “Market Review of Desiccated Coconut October 2024,” coconutcommunity.org. For food manufacturers in North America and Europe, this volatility strains procurement planning, forcing a choice between margin erosion and higher consumer prices, and weakening competitiveness versus oat and almond alternatives with more stable supply chains.

Limited shelf life of fresh coconut products hampers supply chain efficiency

Fresh coconut water typically lasts only 24-48 hours without processing, prompting manufacturers to adopt high-pressure processing (HPP), ultra-high-temperature (UHT) treatment, or aseptic packaging, each of which adds cost and impacts taste or nutrient retention. HPP preserves bioactive compounds and fresh flavor, offering a 30-45 day shelf life, but requires expensive equipment and continuous cold-chain logistics, which limits its application to premium brands targeting health-conscious consumers. UHT extends shelf life to 12 months, eliminating cold-chain requirements, but diminishes flavor and nutrients, making it suitable for price-sensitive segments. This trade-off creates a bifurcated market: premium HPP brands, such as Vita Coco, command higher prices, while UHT-based private-label and value brands compete on cost. For coconut milk and cream, aseptic packaging enhances shelf life and enables ambient distribution; however, high capital requirements remain a barrier for smaller processors in the Philippines, Indonesia, and Thailand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coconut Milk Accelerates as Dairy-Free Demand Surges

Coconut milk is projected to grow at an 8.82% CAGR through 2031, fueled by rising demand for creamy dairy alternatives that perform well in coffeehouse drinks, ready meals, and other prepared foods. While coconut oil remains the largest segment, holding a 36.72% market share in 2025, its dominance is gradually declining amid growing scrutiny of saturated fats. Desiccated coconut remains a staple in baking applications, while niche products like coconut sugar appeal to diabetic and health-conscious consumers, despite their higher price points. The Vita Coco Company’s 15% revenue increase to USD 463.8 million in the first nine months of 2024 demonstrates how beverage-focused brands can accelerate growth by layering new coconut-milk SKUs onto existing water supply chains.

Shifts in consumer behavior are further driving the mainstream adoption of coconut milk. In the U.K., the rise of café culture and plant-based trends has led to 27% of households purchasing plant-based milk monthly, expanding opportunities for coconut milk across retail and foodservice channels. Thailand’s Theppadungporn Coconut, which exports 95% of its output, reported USD 262 million in nine-month revenue on strong coconut milk shipments, highlighting how specialist processors leverage global foodservice demand. Collectively, these trends position coconut milk as the primary growth engine of the coconut products market, supported by both domestic adoption and international export opportunities.

By Form: Solid and Powder Formats Gain Ground in Ambient-Stable Applications

Solid and powder coconut derivatives, including desiccated coconut, coconut flour, and milk powder, are growing at a 9.64% CAGR, outpacing liquid forms that require cold-chain logistics. Although liquids still account for 72.39% of the segment in 2025, rising freight costs and carbon-reduction mandates are shifting demand toward lightweight, dry ingredients that can be rehydrated on-site. Philippine desiccated coconut exports increased 9.5% to 81,728 metric tons in the first half of 2024, with the United States and the Netherlands absorbing most shipments, according to the International Coconut Community. This trend reflects a broader move toward more sustainable, logistically efficient formats that maintain performance while reducing transportation and storage costs.

Processors are also creating value through certification and sustainable practices to capture premium segments. Nutiva’s acquisition of Coconut Secret expands its portfolio to include coconut aminos, targeting soy-free Asian sauces where organic and fair-trade credentials drive brand loyalty. Similarly, Century Pacific Food’s USD 40 million acquisition of Coco Harvest integrates renewable energy from coconut shells, aligning operations with European carbon reporting standards and enhancing gross-margin resilience. Together, these initiatives demonstrate how product innovation, certification, and sustainability are reshaping the solid and powdered coconut segment while supporting profitability and global competitiveness.

By Distribution Channel: Online Retail Disrupts Grocery Dominance

Convenience and grocery outlets still account for 51.81% of coconut products sales, but online retail is expanding rapidly at a 9.98% CAGR, driven by younger consumers who favor subscriptions and digital touchpoints that highlight ingredient transparency, sourcing, and sustainability. Platforms like Thrive Market and Amazon Fresh showcase certifications, sustainability badges, and user reviews that encourage trial of emerging coconut SKUs, broadening the category and accelerating adoption, according to the Organic Trade Association. Direct-to-consumer channels have become a key growth engine for premium brands, with Califia Farms citing DTC (Direct-to-Consumer) sales in its SEC filings as evidence of the scalability of online storytelling for coconut beverages. These channels allow brands to communicate provenance, functional benefits, and wellness claims more effectively than traditional retail, fostering deeper consumer engagement and loyalty.

At the same time, supermarkets and convenience stores are expanding their private-label coconut assortments to protect foot traffic, putting pressure on branded products unless they can differentiate through functionality, taste, or sustainability narratives. This evolving retail landscape underscores the importance of agile fulfillment, inventory visibility, and supply-chain responsiveness. Brands that combine high-quality products with compelling digital storytelling and efficient delivery are best positioned to capture market share over the next five years, leveraging both e-commerce growth and traditional retail presence to drive trial, repeat purchases, and long-term loyalty.

Geography Analysis

Asia-Pacific leads the coconut products market with a 34.85% share in 2025 and is projected to grow at a 9.49% CAGR through 2031, driven by integrated farming and processing ecosystems that provide proximity to raw materials and favorable labor economics, according to the International Coconut Community. The Philippines produced 2.56 million metric tons of copra in 2024/25 and maintained USD 482 million in coconut exports during Q1 2024 despite typhoon-related losses, highlighting the sector’s structural resilience, per the Philippine Coconut Authority[4]Source: Philippine Coconut Authority, “Typhoon Damage Report 2024,” pca.gov.ph. Thailand exported USD 341.11 million in coconut milk in the first ten months of 2024, with 70.5% destined for the United States, reflecting the country's export-focused orientation, according to Thailand’s Ministry of Commerce.

India harvested 21.37 billion coconuts in FY24 and shipped USD 452 million in value-added coconut products, supported by a resurgence in Ayurveda and growing demand from the EU for organic grades, as noted by the Coconut Development Board. These dynamics position the Asia-Pacific region as the backbone of global supply chains, catering to both domestic consumption and international demand. North America and Europe rely heavily on imports, underscoring the importance of traceability, certifications, and quality assurance in maintaining consumer trust. The European Union imported 105,104 metric tons of coconuts valued at USD 156 million in 2023, with the Netherlands re-exporting 47% to regional processors, according to Eurostat. U.S. organic food sales reached USD 71.6 billion in 2024, driving demand for certified coconut milk and yogurt, per the Organic Trade Association, while USDA (U.S. Department of Agriculture) quarantine rules under 7 CFR Part 319 impose strict phytosanitary controls, raising compliance costs but ensuring pest-free entry.

South America, the Middle East, and Africa contribute smaller volumes but offer growth potential through urbanization and tourism. Brazil imported 11,579 metric tons in 2023, and the United Arab Emirates (UAE) imported 75,848 metric tons valued at USD 40.9 million, establishing Dubai as a logistics hub for Gulf Cooperation Council states, according to the World Integrated Trade Solution (WITS). South Africa and Nigeria show rising personal-care demand for coconut oil, yet import-dependent supply chains highlight opportunities for joint ventures with Asia-Pacific processors to develop local packaging and distribution.

Competitive Landscape

The coconut products market is moderately fragmented, with the top five players, Zico Rising, Ducoco Alimentos, The Vita Coco Company, Coco do Vale, and Sambu Group, holding a meaningful but non-dominant share. Competitive dynamics center on securing a reliable supply, effective brand storytelling, and diversifying distribution channels to enhance market reach. For example, the Vita Coco Company secured 90 million liters of coconut water through a five-year agreement with Century Pacific Food, supporting a USD 40 million expansion of processing lines and a farmer seedling initiative to plant 10 million trees by 2030. These strategies demonstrate how leading brands utilize scale, long-term supply agreements, and sustainability initiatives to maintain their market relevance.

Regional specialists and innovators are also scaling to capture growth opportunities. Thailand’s Theppadungporn Coconut generated USD 262 million in nine-month revenue, underscoring the country’s export strength, while the Philippines’ Axelum Resources is doubling desiccated coconut capacity to meet European bakery demand. Nutiva’s acquisition of Coconut Secret positions it to lead the soy-free condiment segment, demonstrating how bolt-on deals can expand category reach.

Technology adoption, including high-pressure processing (HPP) and aseptic packaging, extends shelf life and supports premium pricing, enabling smaller players to compete effectively even amid private-label pressure. Interest from private equity and strategic investors remains strong, as reflected in Califia Farms’ IPO prospectus, signaling confidence in differentiated beverage portfolios that blend coconut with oat and almond bases. Together, these trends point to a phase of selective consolidation, where companies deploy capital to secure certified supply chains and proprietary processing capabilities while defending market share.

Coconut Products Industry Leaders

Zico Rising, Inc.

Ducoco Alimentos SA

The Vita Coco Company, Inc.

Coco do Vale

Sambu Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PHILCO Food Processing, Inc., part of the Thai World Group of Companies, is investing over PHP 1 billion in a new coconut processing facility in Misamis Oriental, as reported by the Philippine Economic Zone Authority (PEZA). The Philippine Information Agency (PIA) notes that the plant, spanning 39,596 square meters, aims to produce 78,000 tons of ultra-high-temperature-treated coconut milk and frozen coconut meat each year.

- April 2025: HLB Specialties launched a line of premium drinking coconuts sourced from Costa Rica and Southeast Asia. The company introduced the coconuts at the Viva Fresh show in Houston. These peeled, ready-to-drink coconuts are packed with coconut water for hydration, post-workout recovery, and tropical refreshment. They are available for retail and foodservice.

- February 2025: Thai Coconut Public Company Limited invested 430 million baht to set up its inaugural international manufacturing plant in Mindanao. Slated to commence operations early next year, this facility is poised to elevate Thai Coconut's production capacity by more than 60%. Furthermore, the company projects a rise in its annual coconut milk production, jumping from 99,000 tons to 155,000 tons. While the factory will initially concentrate on producing canned coconut milk, plans are in place for future diversification into other packaging formats.

- July 2024: Califia Farms, LLC launched plant-based milk: Organic Coconut Milk. These products are suitable for cereal, coffee, baking, and cooking applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the coconut products market as all food-grade and cosmetic-grade goods manufactured from coconut meat, water, or sap; spanning oil, milk and cream, water, sugar or syrup, desiccated flakes, and allied value-added formats that reach retail, food-service, or industrial end users worldwide. According to Mordor Intelligence, equipment, shell charcoal, coir fiber, and plantation services are excluded as they sit outside processed consumer product supply chains.

(Scope exclusions: husk-derived coir, activated carbon, raw nuts, plantation inputs.)

Segmentation Overview

- By Product Type

- Coconut Oil

- Coconut Water

- Coconut Milk and Cream

- Desiccated Coconut

- Coconut Sugar and Syrup

- Others

- By Form

- Liquid

- Solid/Powder

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Discussions with coconut processors, ingredient buyers, Asian farmer co-operatives, North American beverage formulators, and EMEA importers verified average selling prices, derivative conversion ratios, and emerging application shares; thereby closing secondary data gaps and challenging early model assumptions.

Desk Research

We collected baseline facts from open datasets such as UN Comtrade shipment codes for coconut oil, milk, and powder; FAO production yields; USDA Foreign Agricultural Service trade briefs; export tariff dashboards of the Philippines and Indonesia; and nutrition journals tracking medium-chain triglyceride usage. Company 10-Ks, retailer price scans, and news wires within Dow Jones Factiva supplemented supply, price, and demand signals. Subscription utilities like D&B Hoovers helped our analysts profile revenue splits of leading processors. The sources listed illustrate but do not exhaust the broader library referred to during data build and validation.

Market-Sizing & Forecasting

We first reconstruct a top-down demand pool by aligning FAO kernel output, average kernel-to-product recovery, and import-export balances; which are then valued using weighted average selling prices captured from retailer audits and distributor quotations. Select bottom-up checks, like sampled processor revenues split by product line, serve to sense-check and fine-tune totals. Key variables in our model include plantation yield per hectare, proportion of nuts diverted to oil crushing, retail ASP progression for coconut water, new plant-based SKU launches, and regional lactose-intolerant population growth. Forecasts use multivariate regression blended with scenario analysis that flexes yield shocks and price elasticity; coefficients are benchmarked with consensus collected during expert calls. Wherever supplier roll-ups are incomplete, we adjust with historic trade share patterns and documented processing losses.

Data Validation & Update Cycle

Outputs flow through variance screens against historic trade, retail price indices, and corporate earnings. An analyst reviews anomalies, reconvenes sources if swings exceed preset thresholds, and only then signs off. Reports refresh annually, while material events, such as cyclones or major regulatory shifts, trigger ad-hoc updates.

Why Our Coconut Products Baseline Commands Reliability

Published estimates often diverge because firms pick different product baskets, price ladders, and refresh cadences.

Key gap drivers emerge from scope stretch into non-consumer derivatives, unadjusted re-export loops, or single-source price plugs that exaggerate value.

Mordor's disciplined exclusion of coir and charcoal, yearly model reruns, and dual-path validation keep our 2025 figure balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.33 B (2025) | Mordor Intelligence | - |

| USD 20.24 B (2022) | Regional Consultancy A | Bundles industrial husk products and upstream farm services which inflate value |

| USD 21.92 B (2024) | Global Consultancy B | Relies on headline trade data without netting re-exports and uses uniform premium pricing |

| USD 12.88 B (2024) | Industry Association C | Applies global beverage CAGR to all segments, ignoring slower moving cooking formats |

In sum, the comparison shows how careful product scoping, price stratification, and multi-source triangulation allow Mordor Intelligence to deliver a transparent, repeatable baseline that decision-makers can trust for strategic planning.

Key Questions Answered in the Report

What is the forecast size of the Coconut products market by 2031?

The Coconut products market size is projected to reach USD 12.90 billion by 2031, reflecting a 7.57% CAGR from 2026 to 2031.

Which region will grow fastest over the forecast period?

The Asia-Pacific region is projected to achieve a CAGR of 9.49% through 2031, driven by the development of integrated farming and processing ecosystems in countries such as Indonesia, the Philippines, Thailand, and India.

Which product type is gaining the most momentum?

Coconut milk is the fastest-growing segment, advancing at an 8.82% CAGR as consumers seek dairy-free options with creamy texture.

How is e-commerce affecting coconut sales?

Online retail is expanding at a 9.98% CAGR because digital platforms highlight sustainability credentials and bypass traditional shelf-space constraints.

What major risk could disrupt supply?

Extreme weather events such as typhoons and droughts can slash harvests, driving price spikes that challenge downstream manufacturers.

Page last updated on: