Cassava Starch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

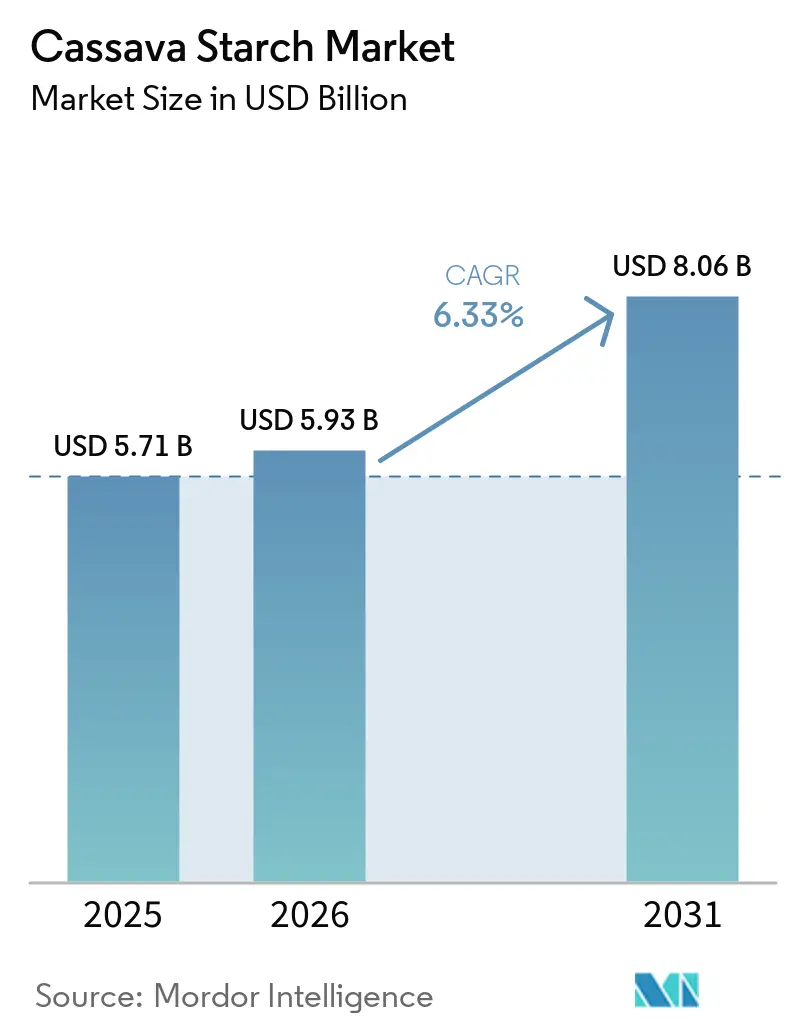

| Market Size (2026) | USD 5.93 Billion |

| Market Size (2031) | USD 8.06 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cassava Starch Market Analysis by Mordor Intelligence

The cassava starch market was valued at USD 5.71 billion in 2025, is projected to reach USD 5.93 billion in 2026, and is forecast to grow to USD 8.06 billion by 2031, registering a CAGR of 6.33% during 2026-2031. As food, packaging, and biofuel producers pivot from petroleum-derived inputs to plant-based polymers, industrial offtake is surging, driven by stricter sustainability mandates. Native grades maintain strong demand for their clean-label functionality at competitive prices. Meanwhile, specialty modified variants are witnessing rapid expansion, fueled by applications in 3D food printing, biodegradable films, and as pharmaceutical excipients. Investment momentum is evident: Ingredion greenlit a USD 150 million upgrade for North American capacity in 2025[1]Source: Ingredion Incorporated, “2025 Investor Presentation,” ingredion.com , and Thai Wah is optimizing Southeast Asian mills to ensure a resilient multi-origin supply, especially in light of the European Union's Deforestation Regulation (EUDR). Consequently, the cassava starch market is evolving from a volume-driven commodity trade to a focus on higher-margin specialty solutions, commanding traceable and deforestation-free premiums in export markets.

Key Report Takeaways

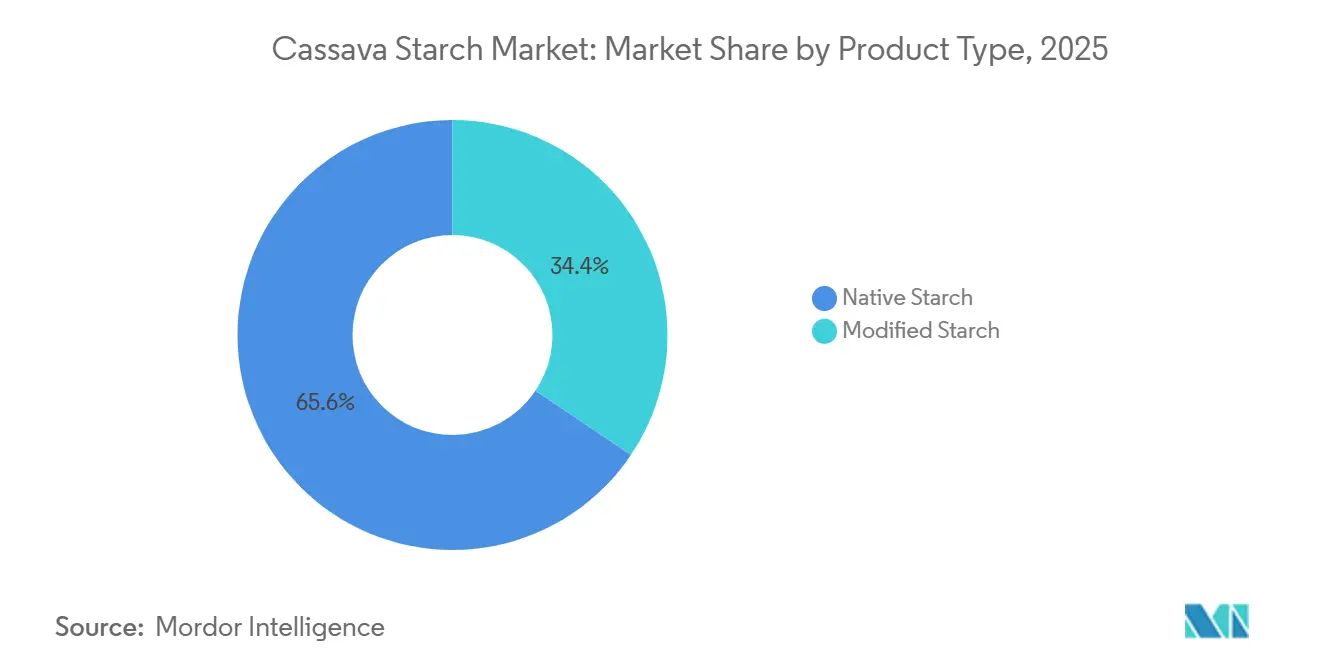

- By product type, native cassava starch accounted for 65.59% revenue in 2025, while modified cassava starch is advancing at a 7.96% CAGR through 2031.

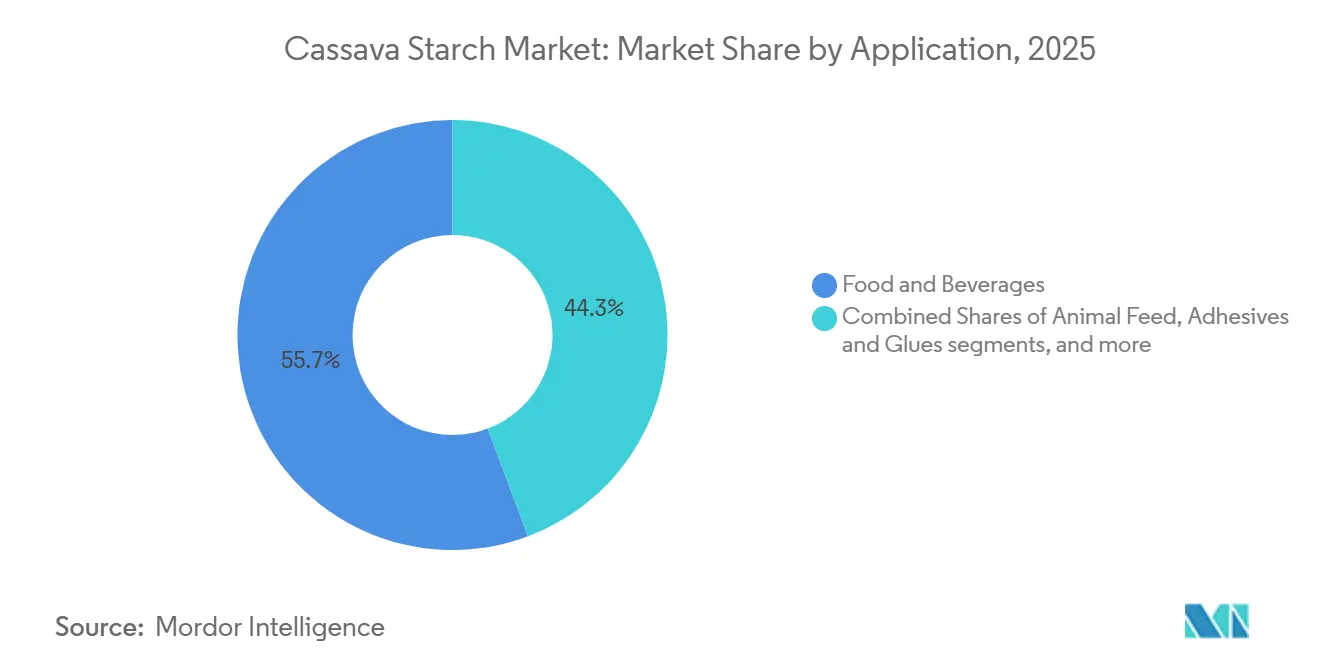

- By application, food and beverages captured 55.72% of the cassava starch market share in 2025, while animal feed is projected to expand at a 7.81% CAGR between 2026 and 2031.

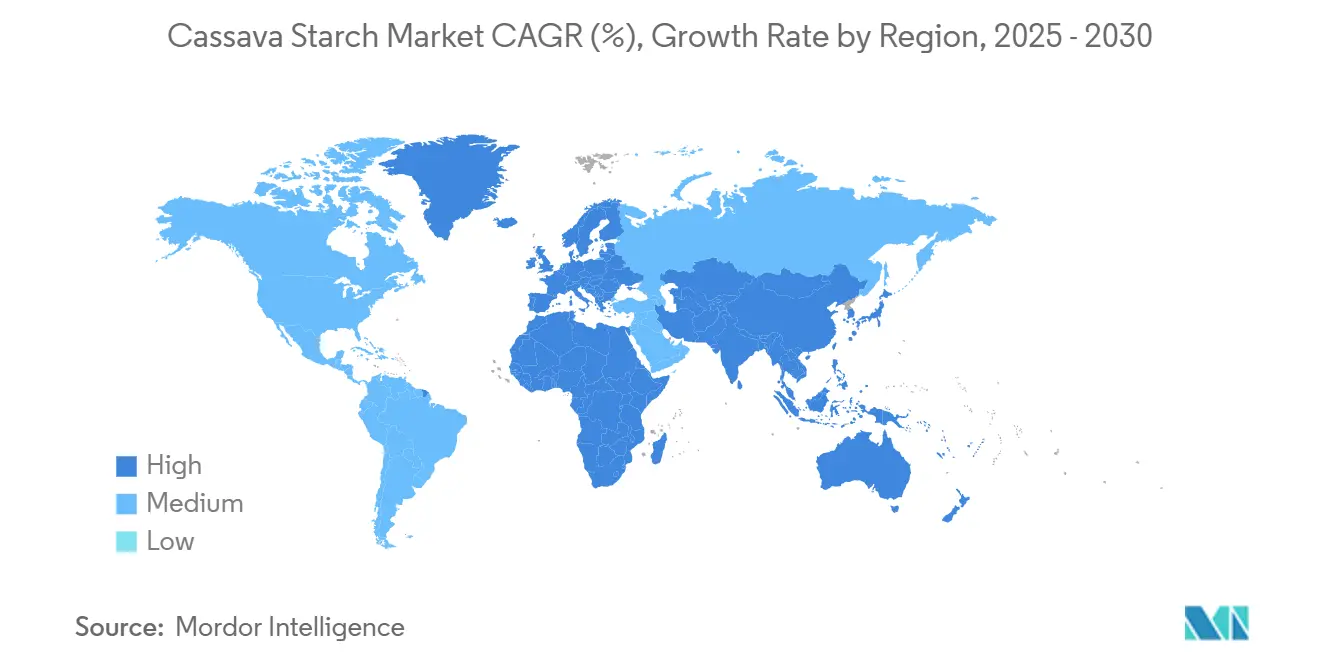

- By geography, Asia-Pacific captured 35.40% of the cassava starch market share in 2025 and is projected to expand at a 7.92% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cassava Starch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring demand for clean-label thickeners in gluten-free foods | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of the paper and packaging sector | +1.5% | Global, led by Asia-Pacific and Europe; spill-over to Latin America | Long term (≥ 4 years) |

| Government biofuel blending mandates in emerging markets | +1.0% | Nigeria, Vietnam, Philippines, China, Brazil | Medium term (2-4 years) |

| Cassava starch is gaining traction as an input for biodegradable plastics | +0.9% | Southeast Asia (Thailand, Indonesia), Brazil, and pilot projects in East Africa | Long term (≥ 4 years) |

| Digitization of root-to-mill traceability boosts industrial procurement | +0.6% | Global, with early adoption in Asia-Pacific and EU-facing supply chains | Short term (≤ 2 years) |

| Growth of specialty modified cassava starches for 3D food printing | +0.4% | North America, Europe, and urban Asia-Pacific innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Demand for Clean-Label Thickeners in Gluten-Free Foods

Food manufacturers are reshaping starch procurement by replacing modified corn and wheat starches with native and lightly modified cassava starches. These cassava starches boast non-GMO, gluten-free, and allergen-free claims. Waxy cassava starch, rich in amylopectin, offers enhanced freeze-thaw stability and expansion properties in gluten-free baking. This allows bakeries to achieve textures akin to wheat-based products, eliminating the need for hydrocolloid blends. In North America and Europe, ingredient transparency is a top priority for many shoppers. As a result, CPG brands are reformulating sauces, soups, and dairy alternatives with cassava-based thickeners. These thickeners can be simply labeled as "tapioca starch," avoiding the more complex modified starch E-numbers. The demand for cassava starch is especially pronounced in the gluten-free segment. Cassava starch's neutral flavor and smooth mouthfeel outshine those of pea and rice starches in high-moisture applications. Producers are using enzymatic and physical modification techniques, blending, heat-moisture treatment, and extrusion to boost viscosity and gel strength. These methods, free from chemical modification, uphold the clean-label status while ensuring functional performance for instant soups and ready-to-eat meals.

Expansion of Paper and Packaging Sector

Driven by circular-economy mandates and the EU and Asia-Pacific's push to phase out single-use plastics, the paper and packaging industry is rapidly adopting cassava starch. This starch is being utilized as a binder and coating agent in containerboard, corrugated packaging, and biodegradable films. In February 2025, Ingredion Incorporated made a strategic USD 50 million investment to boost specialty industrial starch capacity in Cedar Rapids, Iowa. This move is aimed squarely at packaging and papermaking sectors, emphasizing the need for enhanced strength, biodegradability, and recyclability. This positions cassava starch as a natural polymer, offering a sustainable alternative to synthetic adhesives. When blended with chitosan and polyvinyl alcohol (PVA), cassava starch films showcase tensile strength and flexibility on par with traditional plastics. Notably, these films can undergo industrial composting within 60 days, making them suitable for food-contact packaging and agricultural mulch films that are soil-friendly. In 2025, Thailand's paper industry ramped up its consumption of native cassava starch to an estimated 120,000 tonnes, marking a 15% year-on-year increase. This shift comes as mills pivot from imported corn starch, aiming to cut costs and shrink their carbon footprints. Furthermore, research from 2025 highlights the potential of cassava pomace, a by-product of processing. It can be transformed into paper-based packaging materials, presenting a closed-loop value proposition. This innovation not only curbs waste disposal costs but also opens new revenue avenues for starch processors.

Government Biofuel Blending Mandates in Emerging Markets

Governments are increasingly mandating ethanol blending, positioning cassava as a pivotal non-food biofuel feedstock. This shift is especially pronounced in countries aiming to curtail petroleum imports and bolster smallholder agriculture. In 2025, Nigeria unveiled a roadmap to weave cassava into its national biofuel tapestry by 2026. The initiative, spotlighting rural job creation and energy security, underscores Nigeria's commitment to the biofuel vision. Meanwhile, in January 2026, Vietnam rolled out E10 ethanol blending, mandating a 10% ethanol mix in gasoline[2]Source: Vietnam Ministry of Industry and Trade, “E10 Implementation Report 2026,” moit.gov.vn. This move, as highlighted by the Vietnam Ministry of Industry and Trade, spurred an immediate appetite for cassava-derived ethanol, poised to bridge gaps in sugarcane supplies. Over in China, cassava accounts for roughly 10% of the nation's fuel ethanol, with production hubs nestled in Guangxi province. Here, cassava's resilience to drought and its swift 8-12 month growing cycle provide a strategic edge over corn and sugarcane. The Philippines, eyeing the potential, is testing the waters with cassava ethanol blending in Mindanao. By tapping into its established cassava cultivation framework, the Philippines aims to diminish its dependence on imported petroleum. Cassava boasts a unique advantage: it thrives on marginal lands, often deemed unsuitable for food crops. This characteristic not only alleviates food-versus-fuel dilemmas but also, combined with its starch-rich composition (20-30% by weight), yields an impressive 150-180 liters of ethanol per tonne of fresh roots. Yet, the journey to scale these advantages hinges on the establishment of nimble collection networks and processing hubs. Given cassava's swift post-harvest deterioration, these facilities must be operational within a tight 24-48 hour window post-harvest.

Digitization of Root-to-Mill Traceability Boosting Industrial Procurement

To comply with the European Union Deforestation Regulation (EUDR), which requires proof of deforestation-free sourcing by the end of 2026, cassava supply chains are increasingly adopting blockchain, IoT sensors, and QR-code systems. In 2025, Vietnam's cassava sector, which exported over 3.9 million tonnes, with 93-94% going to China, is grappling with compliance hurdles. Smallholder farmers often lack geo-tagged plot data and harvest records. In response, processors are channeling investments into digital platforms to log root origins, harvest dates, and transport details, as highlighted by Vietnam Customs. Thai Wah Public Company, leveraging a multi-origin sourcing strategy across Thailand, Cambodia, Vietnam, and Laos, employs traceability systems. These systems not only facilitate dynamic export routing to sidestep trade barriers but also assure European buyers of supply-chain transparency. Industrial buyers in pharmaceuticals and food sectors are increasingly favoring suppliers with ISO 22000 food safety certification and ISO 14064-1 greenhouse gas accounting. This trend is pushing processors to embrace digital traceability as a key competitive edge. Digitization, while ensuring regulatory compliance, also curtails post-harvest losses by streamlining logistics. Given that cassava roots need processing within 24-48 hours post-harvest to avert enzymatic degradation, real-time quality monitoring becomes crucial in reducing batch rejections. Although establishing traceability infrastructure costs between USD 50,000-200,000 per processing facility, European buyers' premium pricing and enhanced inventory turnover are mitigating these costs. Early adopters in Indonesia and Brazil report payback periods of just 18-24 months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain volatility from cassava mosaic and brown streak viruses | -1.1% | Sub-Saharan Africa (Nigeria, Tanzania, Uganda), Southeast Asia (Thailand, Cambodia) | Short term (≤ 2 years) |

| Weak cold-storage infrastructure in key African producer nations | -0.7% | Nigeria, Tanzania, Uganda, Ghana | Medium term (2-4 years) |

| Rising anti-dumping duties on native starch imports in Europe and the United States | -0.5% | Exporters: Thailand, Vietnam, Indonesia; Importers: EU, United States | Medium term (2-4 years) |

| Substitution threat from rapidly advancing pea and rice starch | -0.6% | North America, Europe, and urban Asia-Pacific markets are prioritizing plant-based proteins | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility from Cassava Mosaic and Brown Streak Viruses

Whiteflies transmit cassava mosaic disease (CMD) and cassava brown streak disease (CBSD), and climate change exacerbates their impact. These diseases can slash yields by 50-100%, leading to significant disruptions for starch processors. Thailand, the globe's top cassava exporter, anticipates a CMD-infected expanse of 532,850 hectares by 2025. This could result in a staggering economic setback of USD 356 million, as farmers either abandon these plots or hastily harvest to salvage what they can, as reported by the Thai Tapioca Starch Association. Meanwhile, CBSD has made inroads in Tanzania, Uganda, and Kenya, nations where cassava holds staple status. This has compelled processors to either pay a premium for roots from uninfected areas or settle for diseased tubers with diminished starch content, hampering extraction efficiency and inflating processing costs. The swift spread of these viruses is tied to the expansion of whitefly populations during warm, dry spells. Consequently, a single outbreak can ripple across multiple provinces in one growing season, leaving processors short on feedstock and unable to run at full capacity. While the International Institute of Tropical Agriculture (IITA) has rolled out CMD-resistant cassava varieties, fewer than 30% of smallholder farmers have adopted them. This hesitance stems from challenges in accessing disease-free planting materials and extension services. In response, processors are broadening their sourcing strategies across nations. Take Thai Wah, for example: their strategy encompasses Thailand, Vietnam, Cambodia, and Laos. Yet, this multi-origin approach brings added logistical challenges and exposes the company to currency fluctuations and regulatory hurdles in different jurisdictions.

Weak Cold-Storage Infrastructure in Key African Producer Nations

In 2023, Nigeria produced over 60 million tonnes of cassava roots, while Tanzania, a key supplier in East Africa, grappled with a lack of cold-storage and rapid-processing infrastructure. Cassava roots start to degrade enzymatically within 24-48 hours post-harvest. This urgency demands swift transport to processing facilities or temporary storage in refrigerated units. Yet, as highlighted by the Nigeria Cassava Initiative, fewer than 15% of rural cassava-growing regions in both Nigeria and Tanzania have access to such cold-chain logistics. This infrastructural shortfall compels processors to establish facilities within a 50-kilometer radius of farming clusters. Such a limitation curtails economies of scale and hinders the consolidation witnessed in Thailand and Vietnam, where centralized mills handle an impressive 300,000-500,000 tonnes annually. In Nigeria, post-harvest losses are alarmingly estimated at 30-40% of harvested roots. This not only diminishes farmer incomes but also leads to feedstock shortages during peak demand. Furthermore, the absence of cold storage facilities stifles export potential. International buyers, seeking consistent quality and reliable delivery schedules, find it challenging to navigate the volatility tied to harvest seasons. However, there's a silver lining: investments in solar-powered cold rooms and mobile processing units are on the rise. A case in point is Agbeyewa Industries' strategic acquisition of Matna Foods in January 2026, with ambitious plans to modernize and expand processing operations in Ondo State. Yet, the journey to scale these innovative solutions isn't without its hurdles. Each facility demands a capital commitment ranging from USD 5-10 million, alongside a call for supportive policies, including tax incentives and guarantees for grid access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Modified Starch Captures Specialty Applications

In 2025, native starch held 65.59% of market revenue, driven by its use in commodity applications like food thickening, paper sizing, and animal feed, where cost and availability outweigh functional performance. Modified cassava starch is growing at a 7.96% CAGR through 2031, fueled by demand in 3D food printing, biodegradable packaging, and pharmaceutical excipients, which require precise control over viscosity, gel strength, and thermal stability. Techniques like enzymatic modification, physical treatments (heat-moisture, extrusion), and chemical cross-linking allow processors to tailor starch properties for applications such as instant noodles that rehydrate in 90 seconds and tablet binders that disintegrate within 15 minutes in gastric fluid. Thai Wah Public Company reported high-value-added (HVA) products, mainly modified starches, accounted for 47% of starch revenue in 2025, up from 45% in 2024, with HVA volume growing 1.7% year-on-year and strong export growth to Japan and Australia. Ingredion’s July 2024 launch of a cassava-derived modified starch line for food-tech and non-food applications highlights supplier investment in this segment.

Native starch’s clean-label status and lower cost make it the preferred choice for manufacturers in emerging economies where price sensitivity is critical. In 2025, Brazil’s native cassava starch exports reached 40,600 tonnes, a 13.9% year-on-year increase, as domestic producers supplied regional food manufacturers and industrial users in Argentina and Chile, according to the Center for Advanced Studies in Applied Economics[3]Source: Center for Advanced Studies on Applied Economics (CEPEA), “Brazil Tapioca Market 2025,” cepea.esalq.usp.br . Modified starch, though priced 20-30% higher, offers functional benefits that justify the cost in applications like frozen foods (freeze-thaw stability), sauces (shear resistance), and confectionery (controlled sweetness release). The segment also benefits from the growth of cassava-based bioplastics, where modified starches blended with biodegradable polymers achieve the mechanical properties needed for injection-molded cutlery and blown-film packaging. Regulatory support, including the European Union’s single-use plastics directive and Asia-Pacific bans on polystyrene foam, is accelerating the adoption of cassava-based TPS resins like Thai Wah’s Roseco line, positioned as a closed-loop solution from cultivation to composting.

By Application: Animal Feed Surges on Cost Competitiveness

In 2025, the food and beverage sector accounted for 55.72% of cassava starch consumption, driven by its use in gluten-free baking, instant noodles, sauces, and dairy alternatives. Waxy cassava starch, valued for its high amylopectin content, is widely used in frozen bakery products due to its resistance to syneresis during freeze-thaw cycles, extending shelf life without hydrocolloid stabilizers. Growth is supported by the global gluten-free market's 9.2% expansion and the rise of ready-to-eat (RTE) and ready-to-cook (RTC) meal kits featuring cassava-based noodles and vermicelli. Thai Wah's Double Dragon Ready brand launched RTE products in 2025, including Pad Cha Ta Lay hot plate with flat glass noodles and instant rice noodles in flavors like Tom Yum Bo Lan, targeting Thai consumers and export markets in ASEAN and the Middle East.

Animal feed was the fastest-growing application, with a 7.81% CAGR, due to cassava starch's cost-effectiveness compared to corn in livestock and poultry rations, especially in Southeast Asia and Latin America. Providing 3,500-3,800 kcal/kg of metabolizable energy, cassava starch matches corn's energy output but is priced 20-30% lower, making it a preferred energy source for swine and broiler producers. Fermented cassava products, which enhance digestibility, are increasingly used in aquaculture feed for shrimp and tilapia, particularly in Vietnam and Indonesia. Paper applications, accounting for 18-20% of cassava starch consumption, are growing as mills replace synthetic binders with cassava starch in packaging to meet recyclability standards. Smaller but stable segments include textile sizing, pharmaceutical tablet binders, and cosmetics. The "Others" category, including adhesives and construction binders, is seeing pilot-scale adoption in Brazil, where modified cassava starch is being tested as a binder in concrete to reduce reliance on petroleum-based polymers.

Geography Analysis

Asia-Pacific, holding 35.40% of the global market in 2025, is projected to grow at a 7.92% CAGR through 2031, driven by Thailand, Indonesia, and Vietnam leveraging low production costs and strong export infrastructure. Thailand exported over 8 million tonnes of cassava products in 2025, valued at THB 95 billion (USD 2.7 billion), with native tapioca starch prices reaching USD 480-500 per tonne FOB Bangkok in early 2026. Thai Wah Public Company, controlling 17% of global cassava starch exports, is shifting focus to Japan's premium gluten-free and non-GMO markets to reduce reliance on China. Indonesia, with 125 cassava starch companies operating at 43% capacity, is prioritizing import substitution and export growth, with Lampung province contributing 70% of domestic tapioca production and exports reaching USD 18.7 million through November 2025. Vietnam, the third-largest cassava exporter, shipped over 3.9 million tonnes worth USD 1.26-1.27 billion in 2025, with Tây Ninh province accounting for 60-65% of output. However, Vietnam faces EUDR compliance challenges due to a lack of geo-tagged traceability data required by end-2026. China's cassava starch imports from Thailand and Vietnam fell 37.88% in Q1 2026, prompting exporters to diversify into ASEAN, the Middle East, and Europe.

South America, led by Brazil, is scaling modified starch production and targeting exports through the pending Mercosur-EU trade agreement. Brazil's cassava root production reached 20.8 million tonnes in 2025, up 9.4% from 2024, while starch production hit 689,000 tonnes in 2024. Modified starch exports surged 44% to 68,400 tonnes in 2025. Paraná accounted for 65.6% of production, followed by Mato Grosso do Sul at 21.3% and São Paulo at 9.7%, enabling economies of scale and investments in higher-margin products like modified starches. Argentina imports cassava starch from Brazil for food and industrial uses, while Latin America is expanding in animal feed and biodegradable packaging as governments phase out single-use plastics.

Europe and North America, as net importers, prioritize clean-label, non-GMO, and organic cassava starches for gluten-free foods, specialty bakery, and pharmaceutical applications. Rising anti-dumping duties and EUDR traceability requirements favor suppliers with digital supply-chain infrastructure. In the Middle East and Africa, Nigeria, producing over 60 million tonnes of cassava roots in 2023, is shifting from low-margin food applications to industrial-grade starch and biofuel feedstocks. Agbeyewa Industries' acquisition of Matna Foods in January 2026 integrates cultivation in Ekiti State with processing in Ondo State. South Africa and Saudi Arabia import cassava starch, while Turkey acts as a re-export hub. Sub-Saharan Africa, despite challenges like weak infrastructure and cassava diseases, holds potential with over 200 million tonnes of cassava roots produced annually, contingent on addressing these issues.

Competitive Landscape

Multinational ingredient suppliers and regional processors dominate the Cassava Starch Market, holding a significant share of global capacity. Meanwhile, smaller and mid-sized mills are scattered across Asia-Pacific, Latin America, and Africa. The competitive landscape is split: commodity native starch producers focus on cost leadership, leveraging scale, multi-origin sourcing, and vertical integration into cassava farming. In contrast, specialty modified starch suppliers carve out their niche through research and development partnerships, clean-label certifications, and bespoke formulations for food-tech, pharmaceutical, and bioplastic sectors. Thai Wah Public Company showcases the importance of supply-chain resilience, boasting a 17% share of global exports, thanks to its multi-origin sourcing from Thailand, Vietnam, Cambodia, and Laos. This strategic positioning helps the company adeptly handle challenges like cassava mosaic disease outbreaks and trade disruptions. Ingredion Incorporated is making waves with a USD 150 million investment in February 2025, aiming to bolster specialty industrial starch capacity at its Cedar Rapids and Indianapolis facilities. This move underscores a strategic shift towards high-margin sectors like packaging and papermaking, where the functional performance of their products commands premium pricing.

Joint ventures are on the rise, serving as a strategic tool for companies to tap into local feedstock, exchange technology, and navigate the intricate web of regulations. A case in point: AGRANA and Ingredion's EUR 35 million joint venture in Romania, greenlit in June 2025, seeks to ramp up starch production and curtail import reliance across EMEA and MENA. Simultaneously, Thai Wah's THB 500 million collaboration with Fuji Nihon Corporation, sealed in January 2025, harnesses sugar-related expertise to innovate cassava starch functionalities. Emerging opportunities abound in cassava-based bioplastics, with Thai Wah's Roseco TPS resin family boasting a 14-22× economic value capture compared to raw roots. Additionally, systems that transform cassava peels and pulp into bioethanol, biogas, and livestock feed are gaining traction. These "waste-to-value" systems not only cut processing costs but also generate revenue streams in a circular economy, as highlighted by the Nigeria Cassava Initiative.

Technology is becoming a key differentiator in the market. Suppliers eyeing European buyers are increasingly adopting blockchain and IoT-enabled traceability systems, especially under the EUDR regulations. On the other hand, processors are turning to enzymatic modification platforms, allowing them to craft clean-label modified starches that meet performance standards without the need for E-number labeling. However, smaller players in regions like Nigeria, Indonesia, and Brazil face the threat of consolidation. As the industry leans towards capital-intensive investments, be it in traceability, disease-resistant planting, or cold-chain logistics, larger, well-capitalized firms are at an advantage. A testament to this trend is Agbeyewa Industries' acquisition of Matna Foods in January 2026. By merging large-scale cassava cultivation in Ekiti State with processing in Ondo State, Agbeyewa aims to streamline the value chain and boost production. Furthermore, industrial buyers in the pharmaceutical and food sectors are increasingly mandating certifications like ISO 22000 for food safety and ISO 14064-1 for greenhouse gas accounting. This trend is erecting barriers for processors who lack robust quality-management and sustainability reporting systems.

Cassava Starch Industry Leaders

Archer Daniels Midland Company

Ingredion Incorporated

Roquette Freres

Thai Wah Public Company Limited

Cargill Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Fuji Nihon Seito formed a joint venture with Thai Wah Public Company, a leading Thai cassava starch manufacturer, by establishing a new firm focused on cassava starch manufacturing and sales in Thailand, with Thai Wah holding a 49% stake.

- January 2026: Agbeyewa Industries Limited, a subsidiary of Cavista Holdings, acquired Matna Foods Company Limited, a cassava starch processor in Akure, Ondo State, to integrate large-scale cassava cultivation in Ekiti State with processing capacity and improve value-chain efficiency.

- April 2025: Thai Wah Public Company Limited and Fuji Nihon Corporation completed the formation of Thai Wah Fuji Nihon Company Limited, a strategic joint venture with Thai Wah holding 51% and Fuji Nihon Thailand Co., Ltd. 49%, following an initial announcement in November 2024. The partnership, with Fuji Nihon investing approximately THB 500 million (USD 14.3 million) for its 49% stake, aims to strengthen regional and global presence in cassava and tapioca starch ingredients, combine research and development expertise to develop high-quality tapioca starch products with novel functionalities, and diversify Thai Wah's product portfolio across Asia-Pacific.

Global Cassava Starch Market Report Scope

Cassava starch, commonly known as tapioca starch, is a fine, white, odorless carbohydrate powder extracted from the tuberous roots of the cassava plant. The cassava starch market is segmented by product type, application, and geography. By product type, the market is segmented into native starch and modified starch. By application, the market is segmented into food and beverages, animal feed, paper, textile, pharmaceuticals, cosmetics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Native Starch |

| Modified Starch |

| Food and Beverages |

| Animal Feed |

| Paper |

| Textile |

| Pharmaceuticals |

| Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Native Starch | |

| Modified Starch | ||

| Application | Food and Beverages | |

| Animal Feed | ||

| Paper | ||

| Textile | ||

| Pharmaceuticals | ||

| Cosmetics | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which product type is growing fastest?

Modified cassava starch leads growth at a 7.96% CAGR through 2031 because it addresses specialty needs in 3D food printing, bioplastics, and pharma excipients.

Why are animal-feed users shifting toward cassava?

Livestock integrators in Southeast Asia and Latin America favor cassava when its price sits 20-30% below corn yet still delivers 3,500-3,800 kcal/kg of energy, reducing ration costs without sacrificing performance.

How will EUDR influence the supply chain?

The European Union Deforestation Regulation requires traceable, deforestation-free cassava by late 2026, prompting exporters to install blockchain and IoT systems that verify farm-level provenance.

Which region holds the largest share of global supply?

Asia-Pacific accounts for 35.40% of the world’s cassava starch production and is projected to grow at 7.92% CAGR through 2031 as Thailand, Vietnam, and Indonesia scale output.

Page last updated on: