Cash Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.86 Billion |

| Market Size (2031) | USD 36.97 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

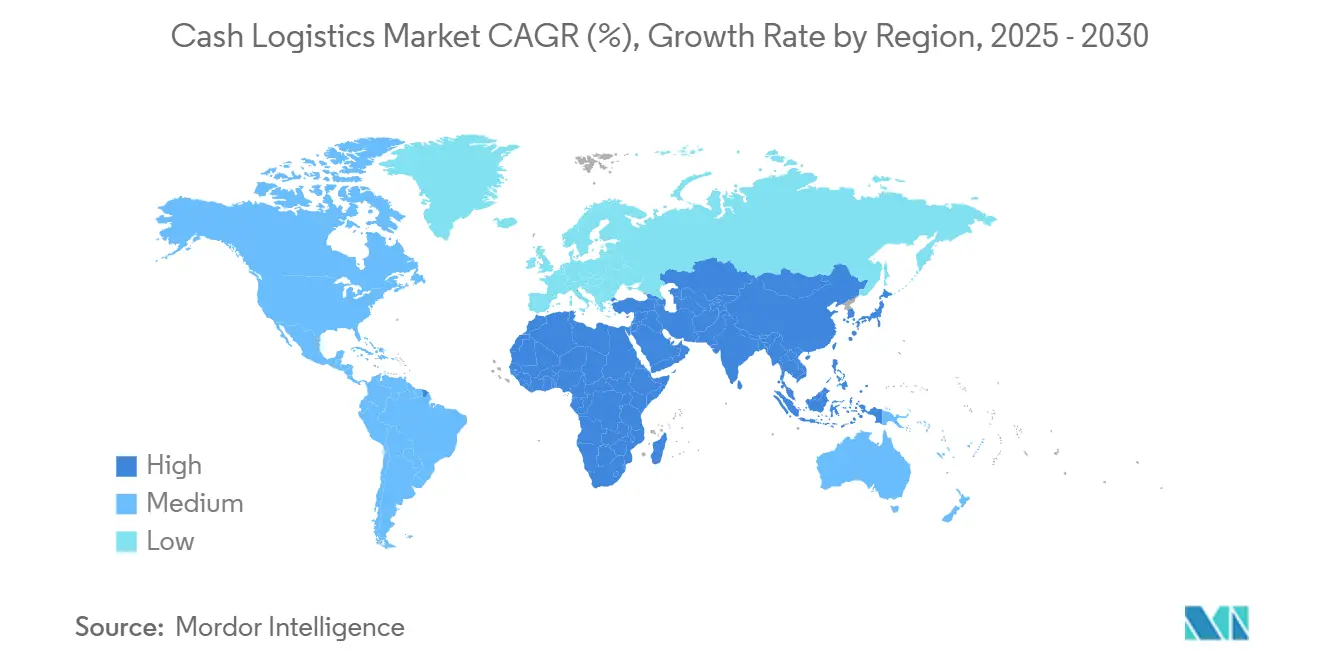

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

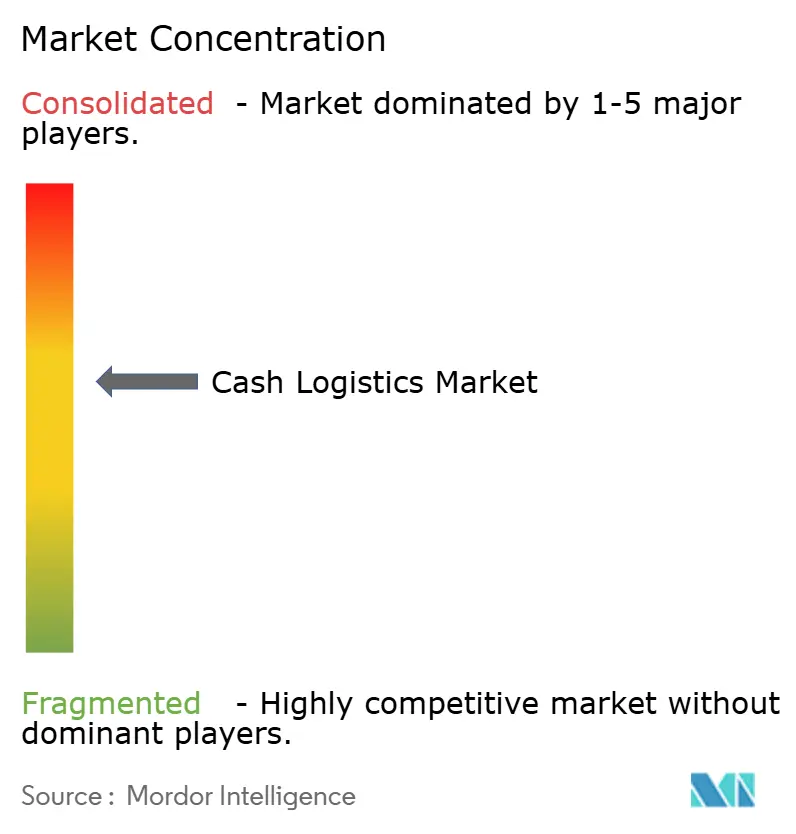

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cash Logistics Market Analysis by Mordor Intelligence

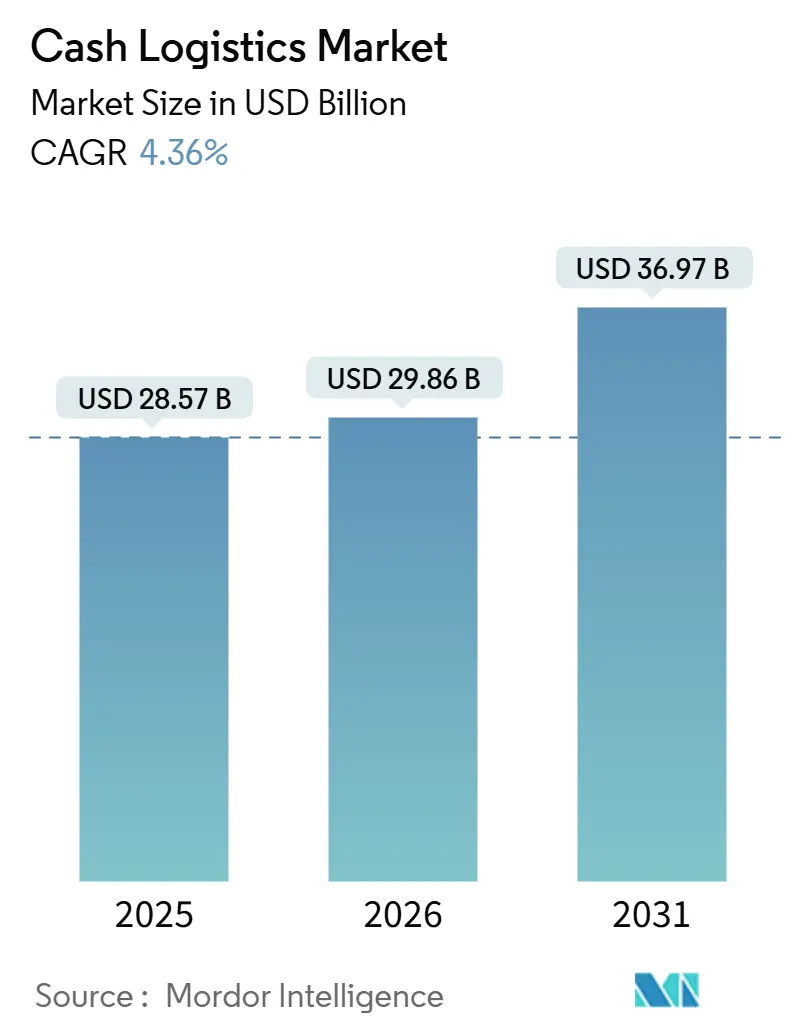

The cash logistics market size is projected to be USD 28.57 billion in 2025, USD 29.86 billion in 2026, and reach USD 36.97 billion by 2031, growing at a CAGR of 4.36% from 2026 to 2031.

Strong inflationary trends in several emerging economies are keeping physical currency in active circulation, which supports consistent volumes for secure transport and processing. At the same time, retailers in North America and Europe are accelerating the adoption of smart safes and IoT-enabled recyclers that cut labor hours and shrinkage, reinforcing demand for integrated cash management contracts. Multinational service providers are modernizing fleets with electric armored vehicles to comply with tightening emission regulations and lower operating costs. Meanwhile, remittance-heavy markets in Asia-Pacific and Latin America continue to rely on ATMs, sustaining logistics activity for cash replenishment and maintenance. The mix of inflation resilience, technology-driven efficiency, and region-specific cash usage keeps the cash logistics market on a measured growth path while reshaping service priorities toward automation and sustainability.

Key Report Takeaways

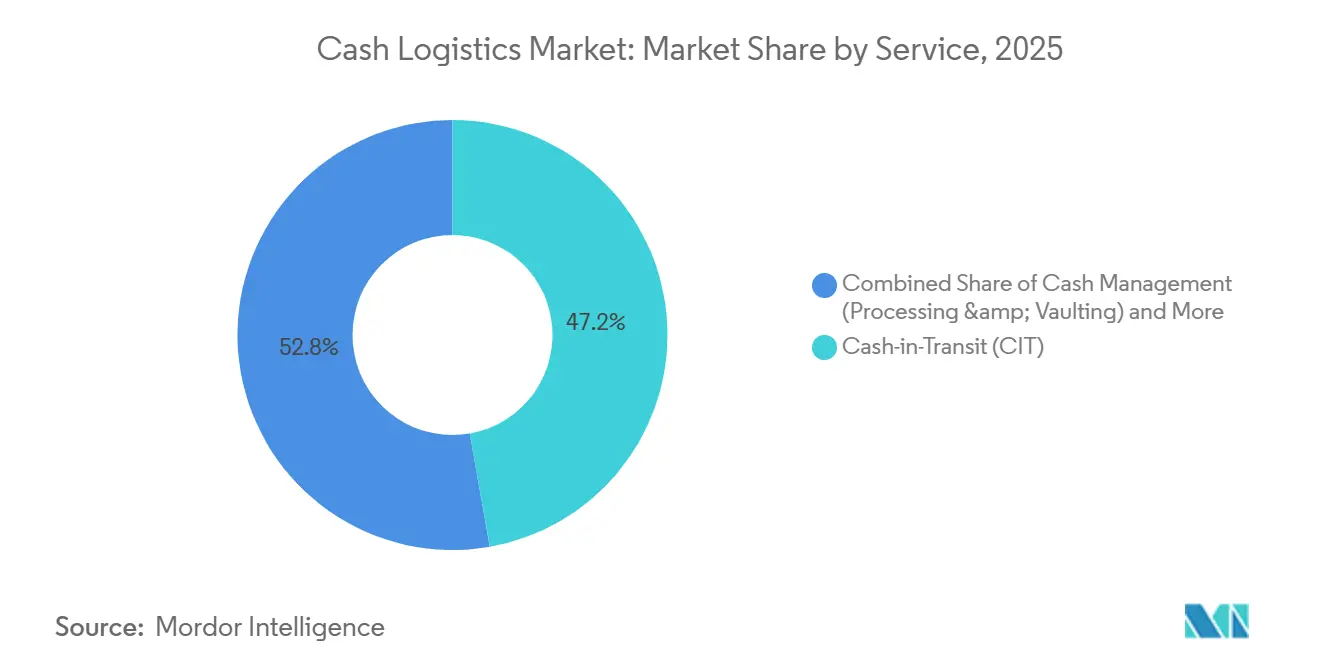

- By service type, cash-in-transit captured 47.23% of the cash logistics market share in 2025, and cash management is advancing at a 6.13% CAGR through 2031.

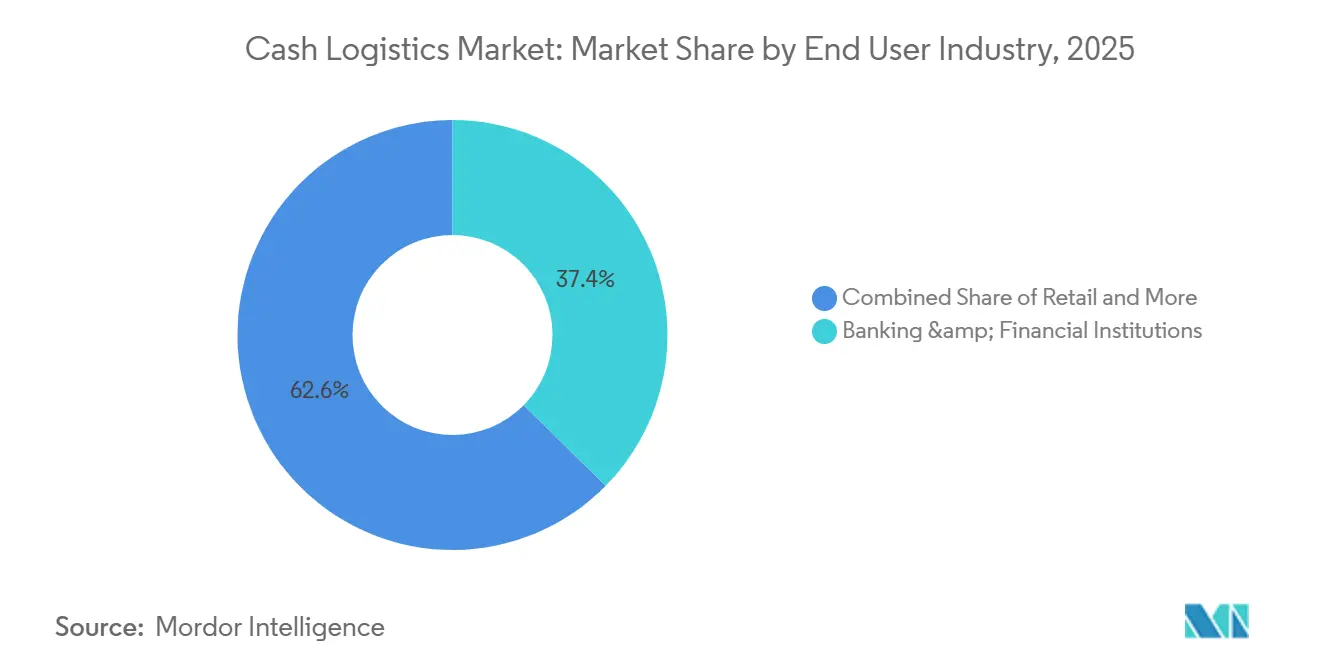

- By end-user, banking and financial institutions held 37.37% of the cash logistics market size in 2025, while retail is forecast to expand at a 7.44% CAGR to 2031.

- By region, North America led with 29.97% of the cash logistics market share in 2025, whereas Asia-Pacific is projected to register the fastest 6.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cash Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven expansion in physical currency circulation | +1.3% | Global, acute in Latin America & MEA | Medium term (2-4 years) |

| Retail deployment of smart safes and cash automation devices | +0.9% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Persistent ATM demand in remittance-heavy economies | +0.7% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Rural micro-ATM / agent-banking network proliferation | +0.5% | India, Southeast Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Corporate cyber-resilience plans are boosting on-site cash reserves | +0.4% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| IoT-enabled cash recyclers are reducing manual touchpoints | +0.3% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Expansion in Physical Currency Circulation

Central banks lifted note issuance after inflation surpassed 5% in many economies during 2024, which left more currency in public hands and raised the frequency of vault rotations and line-haul trips. Emerging markets where 8%-plus inflation persisted saw businesses store higher nominal cash balances, generating immediate volume upside for logistics firms. Providers with established central bank contracts benefited first because they could scale transport runs quickly and add temporary processing shifts. Despite digital wallet growth, IMF research confirms that currency in circulation remains a key monetary component, proving that cash stays relevant under high-price conditions. The boost is expected to normalize after macro-pressures ease, yet the wider base of banknotes will still require ongoing service, anchoring the cash logistics market[1]Federal Reserve Financial Services, “Cash Visibility,” frbservices.org.

Retail Deployment of Smart Safes and Cash Automation Devices

Labor shortages and higher minimum wages prompted United States and European retailers to roll out smart safes that validate, count, and secure deposits in real time, cutting nightly reconciliation and giving managers back several hours per week. Same-day provisional credit provided by banks improves working-capital cycles, a priority when interest rates remain elevated. Logistics providers now bundle device leasing, monitoring, and cash processing into multiyear contracts, shifting part of their revenue base from distance-driven pickups to subscription technology services. Mid-tier merchants are following big-box chains, widening the total addressable device pool. This momentum continues to lift integrated cash management revenue faster than traditional transport, a factor behind the robust outlook for the cash logistics market[2]Giesecke+Devrient, “Cash-in-Transit Management Software,” gi-de.com .

Persistent ATM Demand in Remittance-Heavy Economies

Recipients of cross-border transfers in the Philippines, Mexico, and Nigeria still prefer withdrawing funds as cash, supporting dense ATM networks that must be replenished several times per week. Operators rely on predictive algorithms to balance fill levels against route costs, yet the absolute number of trips climbs in line with remittance volumes. For logistics companies, the segment offers stable, service-rich contracts that include first-line maintenance, cash forecasting, and remote monitoring. Even where mobile money adoption is accelerating, central bank data show ATM transactions holding steady because informal commerce depends on cash liquidity. As overseas worker populations expand, long-term demand for ATM servicing underpins regional growth in the cash logistics market.

Rural Micro-ATM and Agent-Banking Network Proliferation

Financial-inclusion mandates in India, Indonesia, and Kenya sparked large-scale rollouts of handheld micro-ATMs operated by village agents who dispense and collect cash for basic banking. Each device carries modest value per visit, so providers design milk-run routes using lighter vehicles and shared stops to protect margins. Contracts often bundle cash supply, device swap, and cassette cleaning into single SLAs, improving stickiness. As rural economies digitize commerce, cash throughput per location will rise, making early movers with optimized rural networks well placed for compound growth. The long horizon of inclusion programs ensures that this driver will support the cash logistics market beyond 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating insurance & liability premiums for armored fleets | -0.9% | Global, acute in high-crime urban markets | Short term (≤ 2 years) |

| Shortage of licensed armed guards is inflating labor costs | -0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Urban low-emission zones restricting diesel armored trucks | -0.5% | EU core, expanding to North America & APAC | Medium term (2-4 years) |

| Rising incidence of high-grade counterfeits nudging digital shift | -0.3% | Global, concentrated in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Insurance and Liability Premiums for Armored Fleets

A single USD 30 million theft at an armored vault in California led underwriters to reprice risk across the sector, sending premiums sharply higher during 2025. Smaller regionals without spotless loss histories face renewal hikes exceeding 25%, eroding net margins. Many respond by raising minimum contract values or exiting high-crime districts, which could constrain competitive options for banks and retailers. The cost squeeze encourages investments in smart tracking, dual-authentication vault access, and captive insurance to mitigate premium escalation[3]Los Angeles Times Staff, “The Reason $30 Million Was in a GardaWorld Warehouse and Not a Bank,” Los Angeles Times, latimes.com.

Shortage of Licensed Armed Guards Inflating Labor Costs

Strict background checks and firearm certifications limit the pipeline of qualified guards, especially in large urban centers where private security demand also comes from cannabis retail and high-net-worth residential services. Resulting wage inflation reached double digits in 2025, adding pressure to shift toward two-person crews and driver-only drop models that leverage automation in store back rooms. Providers with strong training academies and retention programs gain a clear advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated Platforms Propel Cash Management Upside

Cash-in-transit retained the largest slice of the cash logistics market at 47.23% cash logistics market share in 2025. However, cash management services are forecast to compound at 6.13% CAGR by 2031. Clients view outsourced processing, vaulting, and reconciliation as a single workflow, so they now issue tenders that bundle physical and digital components. Logistics leaders respond with cloud dashboards that show end-to-end cash positions and predictive replenishment alerts. A shift from mileage-based billing to per-transaction fees improves margin stability.

GardaWorld’s Sesami platform illustrates the pivot: by acquiring Tidel and Gunnebo’s cash operations, it built an integrated stack that offers IoT smart safes, armored pickup, and AI analytics under one SLA. Similar moves by Brink’s and Loomis signal an industry consensus that automation and data services will dominate future growth in the cash logistics market.

By End-User Industry: Retail Leads Growth as Working-Capital Pressure Mounts

Banks and financial institutions contributed 37.37% of the cash logistics market size in 2025, anchored by regulatory mandates for secure handling. Retail’s adoption of smart safes lifts its forecast 7.44% CAGR by 2031. Same-day credit turns idle till money into immediate liquidity, appealing when borrowing costs hover near decade highs.

Clip Money’s partnership with Green Dot added USD 4,000 cash deposit points at Walmart and Walgreens, showing how non-bank infrastructure is broadening merchant options. Hospitality and public-sector users remain niche but steady segments that value service continuity and compliance. Collectively, these dynamics keep the cash logistics market diversified across user verticals.

Geography Analysis

Asia-Pacific is projected to expand at 6.01% CAGR by 2031 as governments push rural inclusion and remittance corridors deepen. India’s state-level ATM rollouts and Indonesia’s agent-banking incentives increase pickup points that need low-volume but high-frequency service. China, despite mobile-payment dominance, still circulates large cash volumes for rural trade and festival gifting, requiring high-capacity vaults and multi-currency sorters.

North America held 29.97% of global value in 2025, underpinned by a century-old outsourcing culture and tech-rich service portfolios. Brink’s reported USD 5,012 million revenue in 2024, with 12% organic uplift driven by digital retail solutions and ATM managed services. Rolling fleet electrification programs and e-manifest mandates from the Federal Reserve are reshaping operational standards and lowering route miles.

Europe shows mid-single-digit gains as sustainability rules bite. Prosegur’s electric truck cut 15 tons of CO₂ per year while dropping total vehicle weight 30%, proving regulatory compliance can coexist with cost savings. Low-emission zones in London and Paris accelerate similar upgrades across the region. Latin America and the Middle East & Africa grow from lower bases, with volumes tied to remittance inflows, tourist receipts, and gradual formalization of retail sectors, all of which stimulate incremental demand for the cash logistics market[4]Brink’s Company, “Brink’s Announces Fourth-Quarter and Full-Year 2024 Results,” brinks.com .

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The top five providers, Brink’s, Loomis, GardaWorld, Prosegur Cash, and CMS Info Systems, control significant global revenue, signaling a moderately concentrated market where scale, trust, and long-term client relationships are key advantages. Consolidation moves, such as the Armaguard–Prosegur merger in Australia, highlight how firms are protecting margins as cash usage gradually declines. Beyond size, incumbents benefit from strong reputations, deep banking ties, and high switching costs, which help sustain their leadership despite slower market growth.

Competition is increasingly shaped by technology, automation, and sustainability initiatives. Investments like Sesami’s platform, Brink’s NoteMachine rollout, and Loomis’s electric vehicle adoption reflect a shift toward more efficient, data-driven operations. While niche players are emerging in areas like crypto custody and smart kiosks, high regulatory and capital barriers limit their scale. This keeps established firms firmly ahead, even as the industry evolves.

Cash Logistics Industry Leaders

Brink’s Company

Loomis AB

GardaWorld Cash Services

Prosegur Cash

G4S Secure Solutions (acquired by Allied Universal)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Prosegur continued to scale its joint venture Movistar Prosegur Alarmas with Telefónica, reaching around 600,000 alarm connections in Spain. This growth highlights the success of their partnership in expanding integrated security and monitoring services.

- January 2026: Brink’s completed the onboarding of 1,370 Sainsbury’s ATMs under a multiyear managed-services contract, expanding its U.K. estate to over 12,000 machines.

- July 2025: Prosegur Cash and Armaguard Group agreed to merge their Australian operations, giving Prosegur a 35% stake in a combined entity targeting cost optimization and product innovation.

- March 2025: Prosegur Change entered Changi and Wellington airports, extending its forex booth and multi-currency ATM footprint to 20 global airports.

Global Cash Logistics Market Report Scope

| Cash-in-Transit (CIT) |

| Cash Management (Processing & Vaulting) |

| ATM Services (Installation, Replenishment, Monitoring) |

| Banking and Financial Institutions |

| Retail |

| Hospitality |

| Government & Public Sector |

| Others (Events, Healthcare, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service Type | Cash-in-Transit (CIT) | |

| Cash Management (Processing & Vaulting) | ||

| ATM Services (Installation, Replenishment, Monitoring) | ||

| By End-User Industry | Banking and Financial Institutions | |

| Retail | ||

| Hospitality | ||

| Government & Public Sector | ||

| Others (Events, Healthcare, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How large will the cash logistics market be in 2031?

It is forecast to reach USD 36.97 billion by 2031, advancing at a 4.36% CAGR over 2026-2031.

Which region is growing fastest for cash logistics services?

Asia-Pacific is projected to record a 6.01% CAGR through 2031, driven by rural banking expansion and strong remittance flows.

What service type is expanding the quickest?

Cash management, which covers processing and vaulting, is expected to grow 6.13% per year to 2031 because clients want integrated, tech-enabled solutions.

How are providers addressing environmental pressures on armoured fleets?

Market leaders are adopting hybrid and battery-electric trucks and lightweight armour to cut fuel costs and meet emerging emission standards.

Why is retail demand rising in cash logistics?

Merchants adopt smart safes that provide same-day credit and cut labor costs, lifting retail cash logistics spending at a 7.44% CAGR

How are sustainability rules affecting armored fleets?

Low-emission zones in the EU and the United States push carriers to invest in hybrid and electric trucks, adding capex but reducing future fuel and maintenance expenses.

Page last updated on: