Saudi Arabia Contract Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

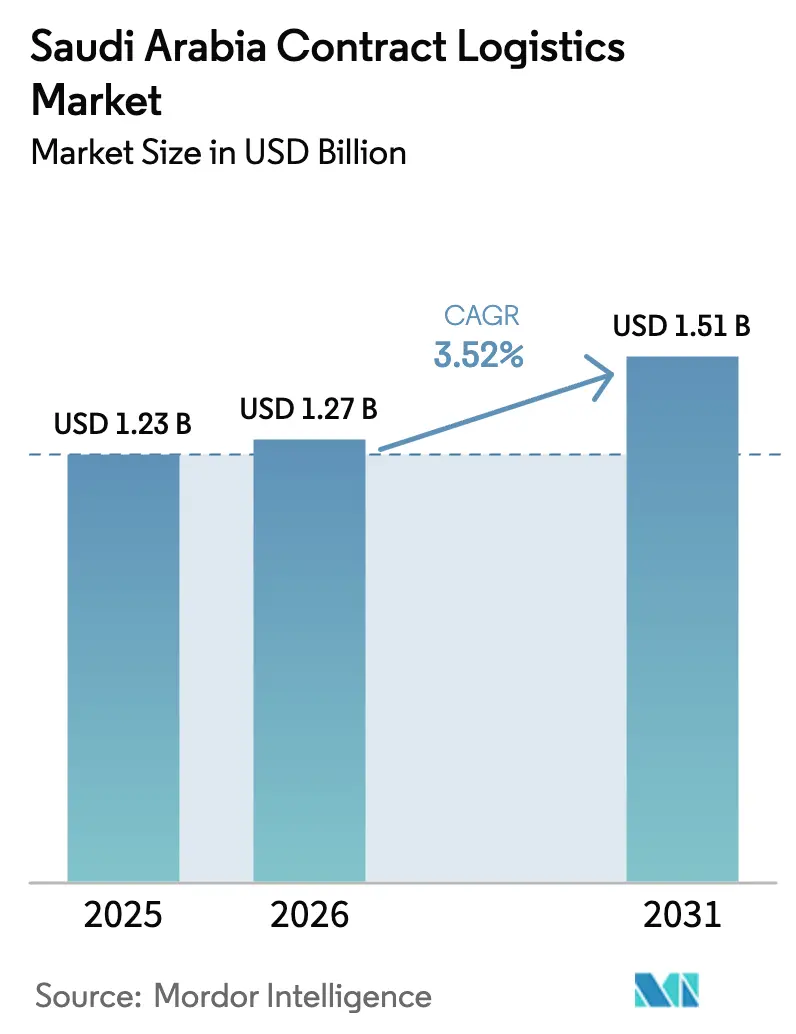

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

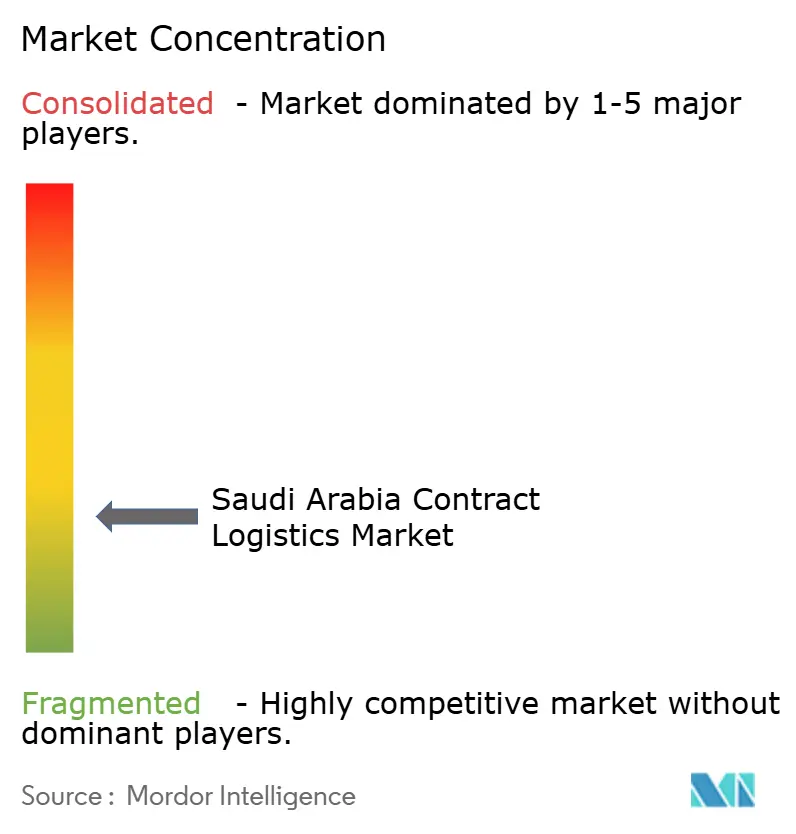

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Contract Logistics Market Analysis by Mordor Intelligence

The Saudi Arabia Contract Logistics Market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.27 billion in 2026 to reach USD 1.51 billion by 2031, at a CAGR of 3.52% during the forecast period (2026-2031).

Vision 2030 infrastructure programs, cross-border e-commerce flows, and manufacturer outsourcing strategies position the Saudi Arabia contract logistics market for steady expansion. Transportation services continue to anchor revenue because most domestic freight still moves by road along the Riyadh–Dammam–Jeddah corridor, yet value-added services such as kitting and postponement are gathering momentum as clients seek leaner inventories. Long-term contracts dominate because shippers want supply-chain continuity, while new special economic zones grant 50-year tax holidays that draw foreign manufacturers and spur demand for bonded warehousing.

Key Report Takeaways

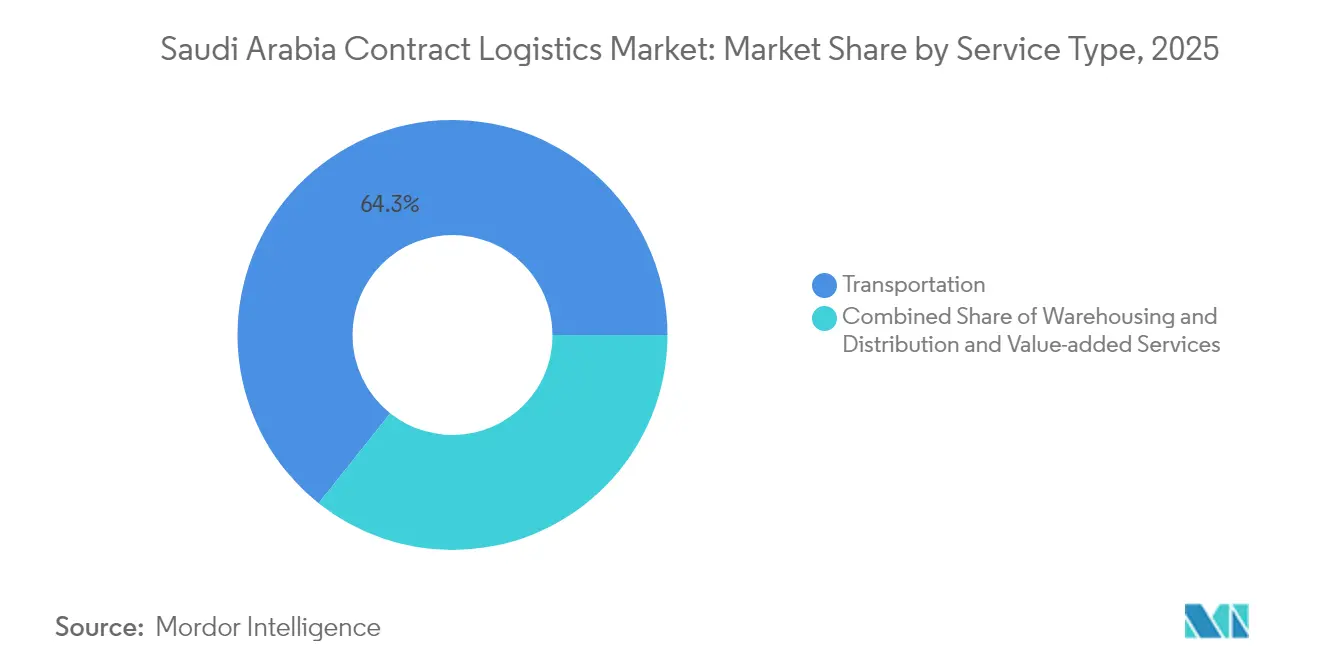

- By service type, transportation captured 64.30% of the Saudi Arabia contract logistics market share in 2025; value-added services are forecast to grow at a 3.05% CAGR through 2031.

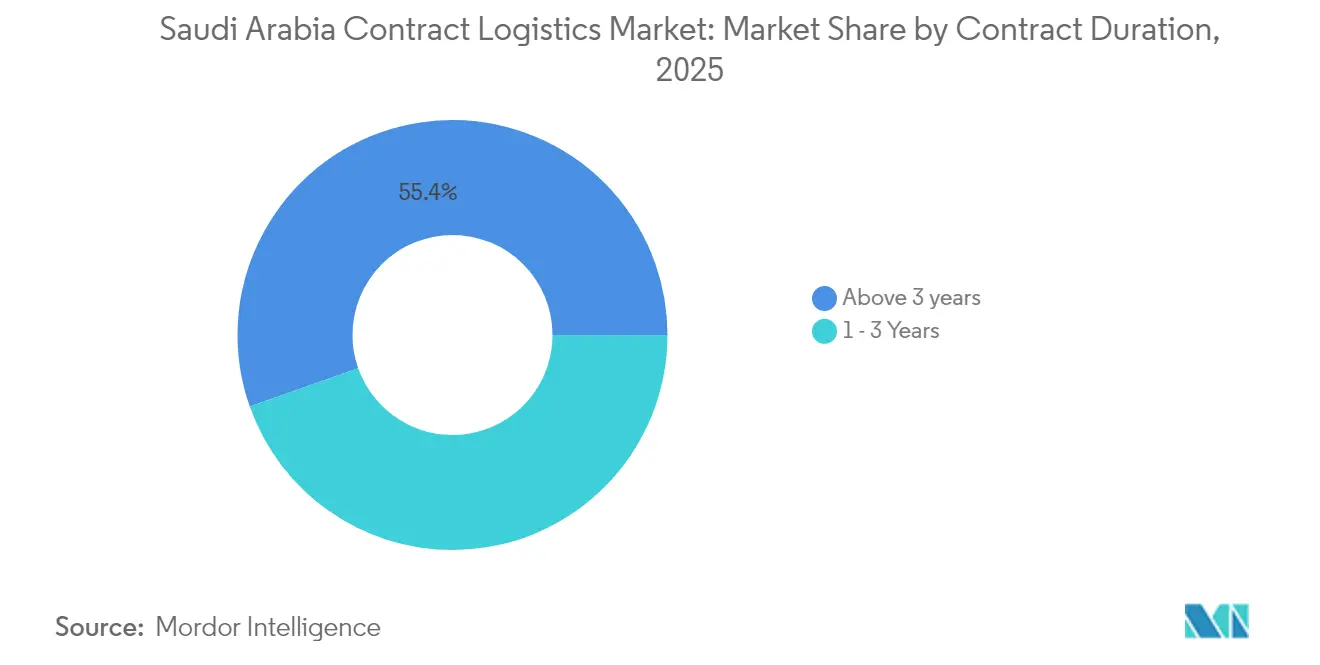

- By contract duration, agreements longer than three years held a 55.40% share in 2025, while they are projected to expand at a 3.72% CAGR to 2031.

- By end-user industry, retail and e-commerce accounted for 26.60% of the Saudi Arabia contract logistics market size in 2025; healthcare and pharmaceuticals are expected to advance at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 logistics infrastructure megaprojects | +1.2% | National hubs in Riyadh, Eastern Province, NEOM | Long term (≥ 4 years) |

| Rapid e-commerce expansion & cross-border parcel flows | +0.8% | Riyadh, Jeddah, Dammam corridors | Medium term (2-4 years) |

| Manufacturer shift toward strategic outsourcing (3PL adoption) | +0.6% | Industrial zones nationwide | Medium term (2-4 years) |

| Special Economic & Logistics Zones with 50-year tax holidays | +0.4% | SILZ, KAEC, Jazan, Ras Al Khair | Long term (≥ 4 years) |

| Automation & cold-chain tech adoption | +0.3% | Major urban centers | Medium term (2-4 years) |

| Local supply-chain localization for giga-projects | +0.2% | NEOM, Red Sea, Qiddiya sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Logistics Infrastructure Megaprojects

Massive port, rail, and road programs are concentrating cargo flows into purpose-built hubs that require integrated contract logistics solutions. The Saudi Port Authority has earmarked USD 4.5 billion to modernize container yards, digital gates, and bulk terminals, reducing vessel dwell times and lifting throughput reliability[1]Saudi Ports Authority, “Official Website,” ports.gov.sa. Rail track length will stretch from 3,650 km in 2025 to 8,000 km by 2030, compelling shippers to seek single-provider contracts covering rail, road, and warehouse processes. Private-sector participation is expected to cover 80% of logistics capital outlays, translating into SAR 240 billion (USD 64 billion) of opportunities for third-party providers. Multimodal nodes inside the planned Logistics Centers are designed with bonded storage, automated cross-docks, and customs one-stop shops, all of which intensify demand for end-to-end contract logistics agreements.

Rapid E-commerce Expansion & Cross-Border Parcel Flows

Online retail sales keep rising at double-digit rates, and parcel traffic increasingly originates from outside the Kingdom. Saudi customs agency ZATCA scrapped all export service fees in October 2024, lowering the cost of cross-border fulfillment for local merchants[2]Saudi Customs (ZATCA), “Media Center,” zatca.gov.sa. A flat SAR 15 (USD 4) clearance for shipments below SAR 1,000 (USD 266) boosts small-parcel economics and prompts 3PLs to add customs paperwork bundles inside their service menus. International parcel specialist J&T Express entered the Kingdom in 2024, adding competitive pressure and signaling confidence in local infrastructure. Contract logistics providers have responded by opening multi-channel fulfillment centers near airports where inventory, pick-pack, and clearance teams work under one roof.

Manufacturer Shift Toward Strategic Outsourcing (3PL Adoption)

Saudi Arabia’s Industrial Production Index rose 7.9% year-on-year in June 2025, led by an 11.1% surge in manufacturing and an 18.7% jump in chemicals. As factory capacity tightens, plant managers offload warehousing, inbound material planning, and export booking to seasoned 3PLs. Most agreements exceed three years, giving providers the time horizon to invest in fleet telematics, crane automation, and in-plant logistics cells. Local content requirements in government tenders further motivate manufacturers to partner with logistics firms that already embed Saudization programs and regulatory know-how.

Special Economic & Logistics Zones Offering 50-Year Tax Holidays

Free-trade enclaves such as the Saudi Industrial Logistics Zone grant 0% income tax for up to five decades, enticing multinationals to base Gulf distribution hubs inside the Kingdom[3]Ministry of Investment, “Special Economic Zones,” invest.saudi.gov.sa. Warehouse operators inside these zones handle bonded inventory, duty deferral, and light assembly, creating high-margin niches for contract logistics specialists. The Regional Headquarters initiative, which allows 0% corporate tax for 30 years, further cements Riyadh’s status as a control tower for Middle East supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shipment visibility gaps | -0.6% | Rural lanes nationwide | Short term (≤ 2 years) |

| Road freight cost inflation amid capacity crunches | -0.4% | Intercity corridors | Medium term (2-4 years) |

| Acute shortage of skilled warehouse-automation technicians | -0.3% | Industrial parks | Medium term (2-4 years) |

| Customs-clearance unpredictability for cross-border e-commerce | -0.2% | Ports, airports, borders | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Shipment Visibility Gaps Across Domestic Transport

Real-time tracking remains patchy outside trunk highways, causing missed delivery windows and eroding shipper confidence. Although larger carriers deploy IoT tags and geofencing, many subcontracted trucks still rely on manual status updates. The deficiency is acute for cold-chain pharmaceuticals that require continuous temperature logs for regulatory audits. FSL Saudi’s Frescon dashboard, launched in 2025, is one of the few locally built platforms offering end-to-end multimodal visibility.

Acute Shortage of Skilled Warehouse-Automation Technicians

Saudi labor laws encourage local hiring, yet certified technicians able to install and maintain AS/RS cranes, AMRs, and sortation belts remain scarce. Bahri Logistics partnered with the Saudi Logistics Academy in 2024 to run mechatronics up-skilling cohorts, but the talent pipeline will take years to match demand. Smaller 3PLs struggle to fund scholarships, hindering the broad adoption of productivity-boosting automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Drives Market Structure

Transportation services generated 64.30% of 2025 revenue, reaffirming their status as the backbone of the Saudi Arabia contract logistics market. Road haulage remains irreplaceable for east-west flows that feed population centers and oil complexes. The Saudi Arabia contract logistics market size attributable to transportation is set to expand modestly as fleet telematics, drop-and-hook models, and rail-road intermodal lanes lift asset utilization. Value-added services, although smaller in absolute terms, are forecast to outpace all other categories with a 3.05% CAGR through 2031 because shippers now prefer to outsource postponement, labeling, and light assembly together with core carriage.

The shift reflects a broader transition toward one-stop solutions where 3PLs assume inventory risk in multi-client campuses. Mandatory palletization rules issued under Circular 6/2025 stimulate demand for pre-stow engineering, while e-commerce sellers request late-cut-off cross-docks that blend parcel sortation with returns handling. Providers that deploy automated put-wall stations and cloud WMS can command premium yields, sharpening competitive lines inside the Saudi Arabia contract logistics market.

By Contract Duration: Long-Term Partnerships Reflect Strategic Relationships

Contracts exceeding three years controlled 55.40% of 2025 billings and are projected to widen their lead with a 3.72% CAGR to 2031. The tilt toward long tenors underpins capex-heavy investments in dedicated fleets, climate-controlled chambers, and IT integrations that would be uneconomical under short retainers. Consequently, many global shippers negotiate gain-share clauses that reward 3PLs for continuous improvement savings, locking both sides into partnership mindsets rather than transactional bidding cycles.

Shorter 1–3-year contracts persist in industries with rapidly shifting demand or in pilot projects where clients test service quality before full rollout. Still, the structural preference for longer durations signals the Saudi Arabia contract logistics market’s maturing risk profile. Providers with robust balance sheets and ISO-certified processes capture the largest slices because they can guarantee service continuity over multi-year concessions aligned to giga-project construction schedules.

By End-User Industry: Healthcare Transformation Drives Fastest Growth

Retail and e-commerce remained the prime demand engine, contributing 26.60% of total 2025 revenue as smartphone adoption and digital wallets lift online spending. Yet healthcare and pharmaceuticals show the sharpest trajectory, tracking a 4.12% CAGR through 2031 thanks to a projected USD 7.04 billion domestic pharma market by 2028. The Saudi Arabia contract logistics market size linked to healthcare is expected to grow faster than any other segment because hospitals mandate GDP compliance, validated cold boxes, and batch-level traceability.

Manufacturing, automotive, chemicals, and food-and-beverage segments deliver steady baseline volumes that cushion cyclicality in consumer spending. Hazardous-goods handling and ISO tank cleaning services add revenue diversity for chemical shippers, while halal food exporters require HACCP-certified storage. The multiplicity of verticals reduces reliance on a single customer set, reinforcing resilience in the Saudi Arabia contract logistics market.

Geography Analysis

Riyadh and its surrounding Central Province generate the highest contract logistics spend, leveraging a population above 7 million and a growing cluster of regional headquarters. E-commerce volumes funneled into the province’s automated fulfillment centers underscore its role as a national distribution fulcrum. Jeddah anchors the Western Province with King Abdulaziz Port handling Red Sea trade lanes, pilgrimage flows, and new hospitality builds that require synchronized hotel-OS&E supply chains.

The Eastern Province benefits from oil-field services, petrochemicals, and metals processing near Jubail and Ras Al Khair. As refineries diversify into specialty chemicals, storage and drumming operations enlarge value-added revenue pools for contract logistics providers. Northern and Southern border areas enjoy new truck stops, bonded yards, and customs e-gateways that simplify trade with Jordan, Iraq, Yemen, and Oman, broadening the geographic spread of the Saudi Arabia contract logistics market.

Competitive Landscape

The Saudi Arabia contract logistics market hosts a blend of global integrators, regional champions, and homegrown specialists. DHL, DSV, and Maersk leverage worldwide networks, standardized IT stacks, and compliance protocols to service multinational customers. DHL’s 2025 pledge to invest EUR 500 million (USD 520 million) across Gulf countries, alongside its joint venture with Aramco’s ASMO, showcases long-term confidence in the Kingdom’s growth arc.

Regional operators such as Aramex and CEVA Logistics exploit deep familiarity with GCC customs processes and Arabic-language service desks. CEVA’s 2024 tie-up with Almajdouie created a hybrid entity that blends international SOPs with local asset bases, forming one of the largest multi-client platforms inside the Saudi Arabia contract logistics market. Domestic groups, including NAQEL Express, Almajdouie, and Bahri Logistics, excel in regulatory navigation, Saudization compliance, and desert-condition fleet maintenance, winning sizable shares of government and energy vertical contracts.

Technology intensity increasingly differentiates competitors. Market leaders deploy robotics, AI-driven slotting algorithms, and digital twins to deliver double-digit productivity gains. Bahri’s Infor WMS integration produced real-time labor visibility and 30% faster dock-to-stock cycles, sharpening its appeal to pharmaceutical importers. Smaller players may turn into acquisition targets if they cannot meet the capital demands of automation and ESG retrofits. The current configuration suggests gradual consolidation, yet niche specialists offering cold-chain or giga-project logistics continue to enter, preserving moderate market fragmentation.

Saudi Arabia Contract Logistics Industry Leaders

Almajdouie Group

Aramex

GAC

Bahri Logistics.

NAQEL Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DHL Group confirmed a EUR 500 million (USD 520 million) Middle East investment, earmarking significant funds for Saudi facilities upgrades and green fleet renewals.

- February 2025: Maersk inaugurated a 20,000 m² warehousing and distribution site in Jeddah’s Nakheel District.

- November 2024: Bahri Logistics completed the implementation of Infor WMS with SNS Global, modernizing warehouse automation and financial integration.

- October 2024: CEVA Logistics and Almajdouie Group finalized their joint venture, creating one of the Kingdom’s largest integrated logistics platforms.

Saudi Arabia Contract Logistics Market Report Scope

Contract logistics refers to the outsourcing of resource management duties to a third-party company. Contract logistics companies handle a variety of duties including supply chain development and planning, facility design, warehousing, delivery, and distribution, order processing, payment collection, inventory management, and some types of customer assistance.

The report provides a comprehensive background analysis of the Saudi Arabia Contract Logistics market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the industry's competitive landscape. Additionally, the COVID-19 impact has been incorporated and considered during the study. The Saudi Arabia Contract Logistics Market is segmented By Type (Insourced and Outsourced), By End User (Manufacturing and Automotive, Consumer Goods and Retail, High-Tech, Healthcare, Pharmaceuticals, Chemicals, Petrochemicals, and Other End Users). The report offers the Saudi Arabia Contract Logistics market size and forecasts in values (USD billion) for all the above segments.

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

| 1 – 3 Years |

| Above 3 years |

| Manufacturing & Automotive |

| Food & Beverage |

| Retail & E-commerce |

| Healthcare & Pharmaceuticals |

| Chemicals |

| Other Industries |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1 – 3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing & Automotive | |

| Food & Beverage | ||

| Retail & E-commerce | ||

| Healthcare & Pharmaceuticals | ||

| Chemicals | ||

| Other Industries |

Key Questions Answered in the Report

How large is the Saudi Arabia contract logistics market in 2026?

The market is valued at USD 1.27 billion in 2026 and is forecast to reach USD 1.51 billion by 2031.

Which service type generates the highest revenue?

Transportation services account for 64.30% of 2025 revenue, reflecting the dominance of road and emerging rail freight.

Which end-user segment is expanding fastest?

Healthcare and pharmaceuticals is projected to grow at a 4.12% CAGR through 2031 on the back of rising cold-chain demand.

What drives the preference for long-term logistics contracts?

Multi-year Vision 2030 projects and capex-intensive automation encourage shippers and 3PLs to lock in agreements longer than three years.

How do special economic zones affect logistics demand?

SEZs grant 50-year tax holidays and bonded procedures, drawing manufacturers that require dedicated warehousing, customs, and value-added services.

Page last updated on: