Cardiogenic Shock Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

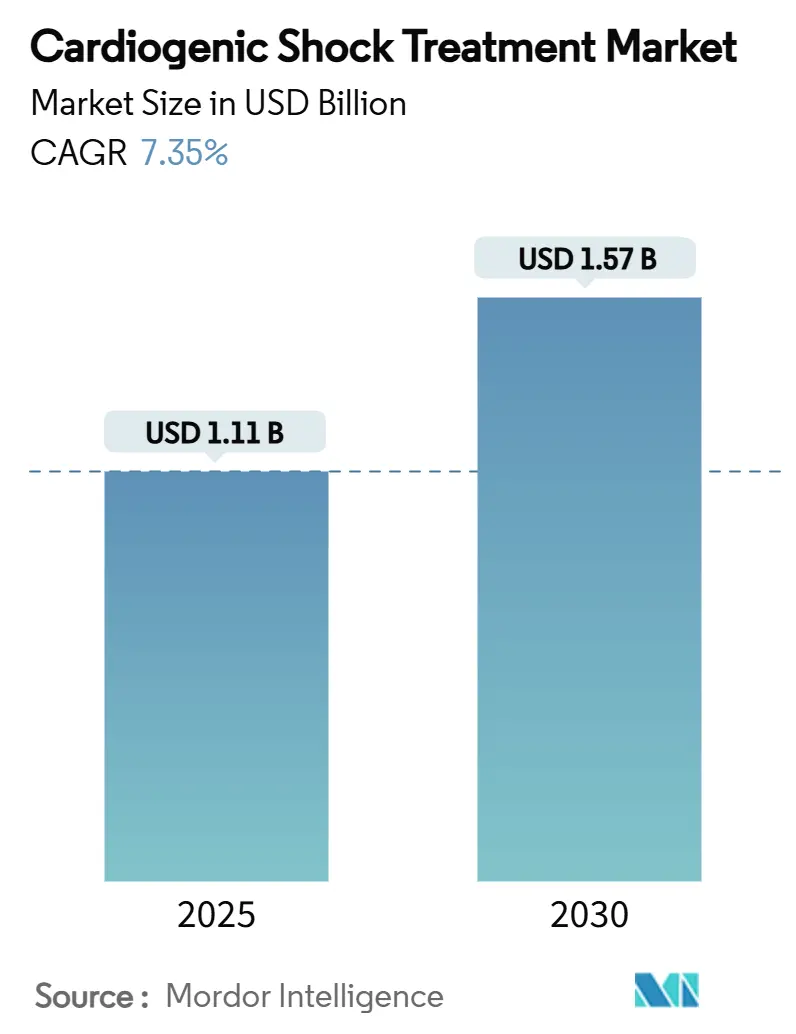

| Market Size (2025) | USD 1.11 Billion |

| Market Size (2030) | USD 1.57 Billion |

| Growth Rate (2025 - 2030) | 7.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiogenic Shock Treatment Market Analysis by Mordor Intelligence

The cardiogenic shock treatment market size reached USD 1.11 billion in 2025 and is forecast to rise to USD 1.57 billion by 2030, advancing at a 7.35% CAGR. The climb mirrors surging mechanical circulatory support (MCS) adoption, wider access to high-acuity cardiac care, and an aging population that sustains elevated acute myocardial infarction incidence. Early MCS placement within 24 hours halves average length of stay and trims 30-day mortality, steering hospitals toward protocolized device deployment.[1]Kevin G. Buda et al., “Early vs. Delayed Mechanical Circulatory Support in Patients with Acute Myocardial Infarction and Cardiogenic Shock,” European Heart Journal – Acute Cardiovascular Care, academic.oup.com Investment in predictive hemodynamic monitoring, rapid-response shock teams, and guideline-directed revascularization further broadens the addressable patient pool, while favorable reimbursement in the United States and Europe cushions capital budgets. Concurrently, fulminant myocarditis recognition, cath-lab-ready MCS hardware, and Asia-Pacific infrastructure programs inject fresh momentum into the cardiogenic shock treatment market.

Key Report Takeaways

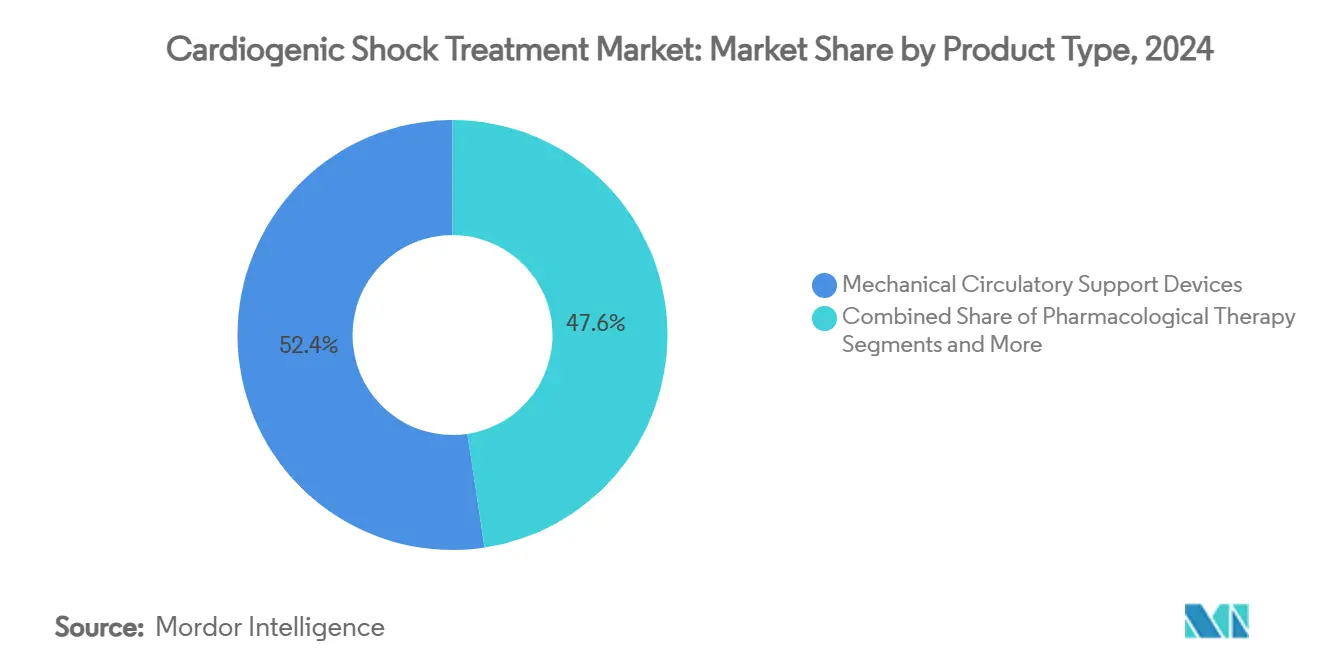

- By Product Type, Mechanical circulatory support devices led with 52.38% of cardiogenic shock treatment market share in 2024; pharmacological therapies expand at a slower 4.2% CAGR through 2030.

- By Severity Stage, Stage B Beginning Shock is projected to record the fastest 10.63% CAGR, while Stage C Classic Shock retained 41.38% share of the cardiogenic shock treatment market size in 2024.

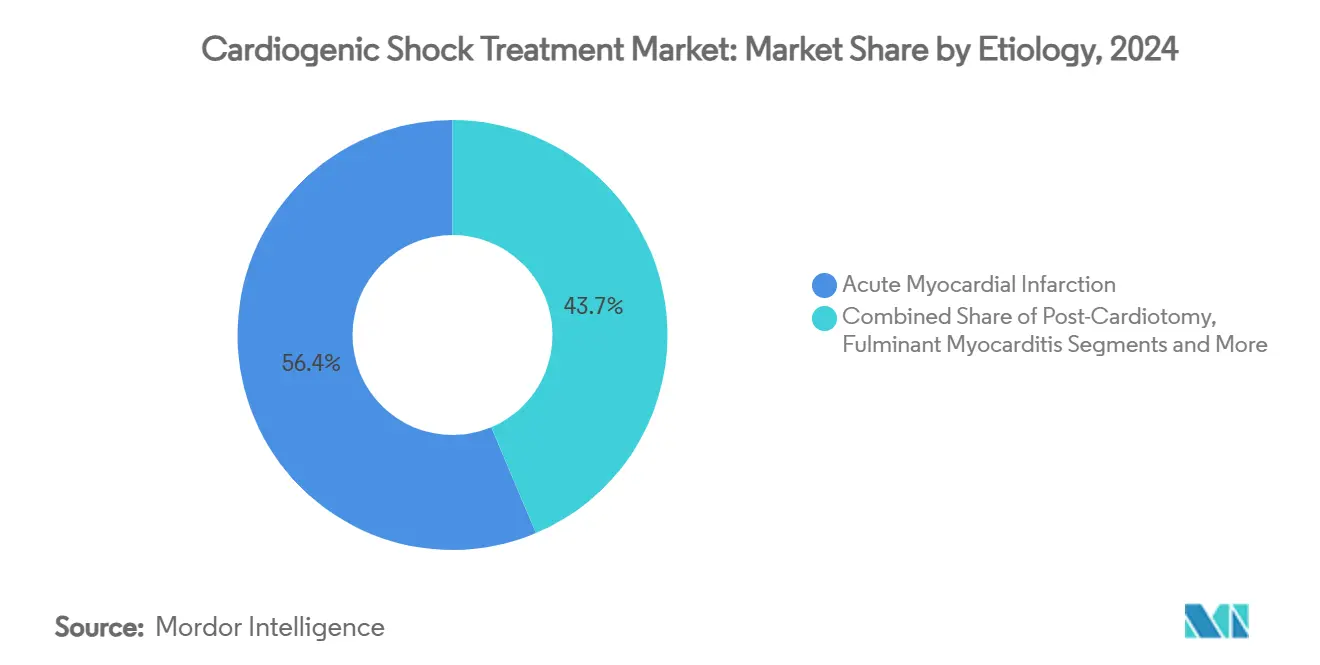

- By Etiology, Fulminant myocarditis captured 6.7% share of the cardiogenic shock treatment market size in 2024 and is poised for an 11.63% CAGR to 2030.

- By End User, Cardiac catheterization laboratories accounted for 18.6% of the cardiogenic shock treatment market size in 2024 and are on track for a 10.02% CAGR through 2030.

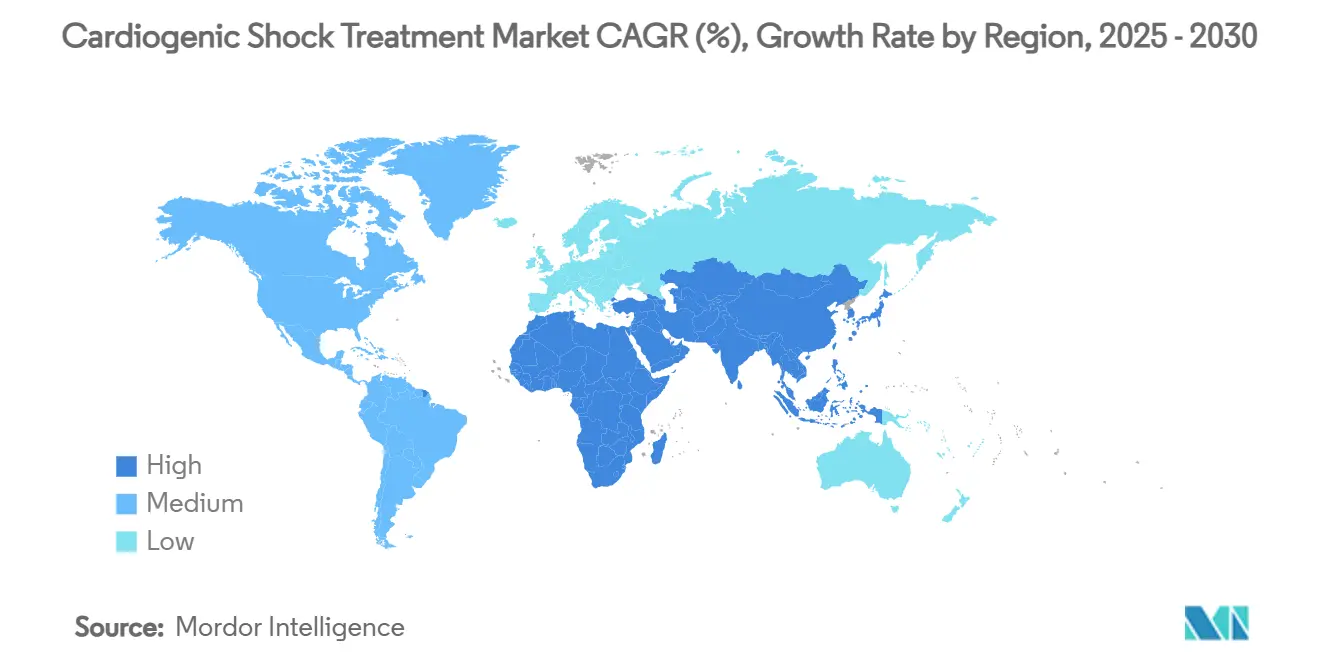

- By geography, North America held 36.59% cardiogenic shock treatment market share in 2024; Asia-Pacific is set to post a 9.71% CAGR to 2030.

Global Cardiogenic Shock Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of acute myocardial infarction & aging population | +1.8% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| Advancements in percutaneous mechanical circulatory support | +2.2% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Favorable reimbursement for mechanical support | +1.5% | North America & Europe | Short term (≤ 2 years) |

| Growing adoption of guideline-directed early revascularization | +1.3% | Global, led by developed markets | Medium term (2-4 years) |

| Emergence of micro-axial LVADs for cath-lab shock stabilization | +0.9% | North America & Europe | Long term (≥ 4 years) |

| AI-enabled predictive hemodynamic monitoring | +0.8% | Global; early uptake in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Acute Myocardial Infarction & Aging Population

Longer life expectancy and higher survival after first heart attacks swell the pool at risk of cardiogenic shock. Annual U.S. direct heart-failure expenditure already averages USD 30,000 per patient and is projected to hit USD 70 billion by 2030, with inpatient stays as the chief cost driver.[2]K.S. Shah, “The Economics of Heart Failure Care,” Progress in Cardiovascular Diseases, sciencedirect.com Hospitals therefore ramp up cardiogenic shock treatment market programs to curb readmissions and bolster value-based metrics. Transitional Coverage for Emerging Technologies fast-tracks novel MCS devices, further smoothing market penetration.[3]Centers for Medicare & Medicaid Services, “Final Notice—Transitional Coverage for Emerging Technologies,” cms.gov Continuous public-health surveillance in Europe and Japan reveals similar demand curves, reinforcing the growth trajectory.

Advancements in Percutaneous Mechanical Circulatory Support

Next-generation Impella pumps and compact ECMO consoles slash procedure times and move definitive therapy from the operating theater to the cath lab. Medtronic’s VitalFlow system integrates a single-use centrifugal pump with a low-surface-area oxygenator, reducing hemolysis risk and simplifying weaning protocols. Hemocompatible coatings minimize anticoagulation burdens, while real-time data feeds into hospital EMRs for swift troubleshooting. These enhancements expand candidacy to intermediate-risk patients, enlarging the cardiogenic shock treatment market and stimulating procurement among community hospitals.

Favorable Reimbursement for Mechanical Support in Developed Markets

The 2025 U.S. IPPS final rule authorizes separate payment for high-cost shock devices, easing margin pressure on tertiary centers. Cost-utility models show LVAD bridge-to-transplant therapy remains within accepted thresholds at USD 69,768 per QALY, sustaining payer confidence. Europe’s Coverage with Evidence Development programs mirror the approach, linking reimbursement to real-world outcomes and nudging faster adoption. Bundled payments tied to mortality and length-of-stay metrics encourage early device placement, underscoring the pull on the cardiogenic shock treatment market.

Growing Adoption of Guideline-Directed Early Revascularization

ACC/AHA 2025 guidelines advocate mechanical support initiation before or during PCI for threatened shock, catalyzing system-wide protocol revisions. Hospitals establish 24/7 shock teams that activate MCS within 60 minutes of arrival, mirroring door-to-balloon benchmarks. Coordinated pathways integrate emergency medicine, interventional cardiology, and critical care, trimming treatment delays and underpinning steady cardiogenic shock treatment market acceleration. AI-based triage tools flag impending hemodynamic collapse, further front-loading device demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & procedure cost of advanced MCS devices | -1.4% | Global; strongest in emerging markets | Medium term (2-4 years) |

| Device-related adverse events | -0.8% | Global | Short term (≤ 2 years) |

| Supply-chain bottlenecks for oxygenators & Impella catheters | -1.1% | Global; regional variability | Short term (≤ 2 years) |

| Shortage of trained perfusionists & critical-care staff | -0.9% | Global; acute in Asia-Pacific & emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Procedure Cost of Advanced MCS Devices

ECMO console fleets, disposables, and round-the-clock staffing demand upfront outlays exceeding USD 1 million, deterring low-volume centers. Average LVAD implant stays generate USD 193,192 revenue yet incur substantial follow-up costs, compressing margins. Emerging economies wrestle with currency swings that inflate device prices and hamper reimbursement alignment. Leasing and pay-per-use contracts are gaining favor but adoption remains patchy, restraining the cardiogenic shock treatment market in budget-constrained geographies.

Device-Related Adverse Events

Hemolysis, limb ischemia, and bleeding complicate up to 30% of MCS courses, prolonging ICU occupancy and dampening clinician enthusiasm. While newer surfaces and small-bore cannulas mitigate risk, vigilance requirements increase labor intensity. Regulatory updates mandate post-market surveillance, adding compliance overhead that smaller facilities find burdensome, slowing cardiogenic shock treatment market penetration among late entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: MCS Devices Drive Innovation Cycles

MCS devices dominated the cardiogenic shock treatment market with 52.38% share in 2024 and are projected to log an 11.57% CAGR to 2030. The evidence-backed capacity of temporary pumps and ECMO to improve survival against pharmacologic therapy secures budget prioritization. Robust clinical registries confirm early device use halves 30-day mortality, fueling purchasing in tertiary hubs and catalyzing cath-lab expansion. Impella systems spearhead uptake, underpinned by continuous pump refinements and broadening indications. The cardiogenic shock treatment market size for MCS is further magnified by ECMO consoles optimized for transport teams and pediatric ICUs.

Pharmacological therapy preserves a stabilizing role but yields market share to devices as operators favor unloading over high-dose inotropes. Revascularization procedures remain foundational; PCI volumes rise as radial access pairs seamlessly with percutaneous MCS. Artificial-intelligence-guided pump weaning software now calibrates support curves, shrinking ICU days and aligning with value-based care reimbursement, reinforcing the allure of the cardiogenic shock treatment market.

By Severity Stage: Early Intervention Paradigm Emerges

Stage C Classic Shock retained 41.38% share of the cardiogenic shock treatment market size in 2024, reflecting entrenched clinical presentations. Stage B Beginning Shock, however, is set for a 10.63% CAGR as health systems adopt preventive device placement in borderline patients. Shock teams activate micro-axial pumps before lactate spikes, converting would-be Stage C cases into shorter unit stays and lower resource spend.

Stage D Deteriorating and Stage E Extremis cases still generate heavy device needs but entail longer ICU tenure and higher complication risk. AI-driven dashboards identify Stage A and B individuals at escalation risk, enabling prophylactic cannulation and shifting case mix upward for the cardiogenic shock treatment market. These strategies align with insurers’ readmission penalties, compelling hospitals to treat early and aggressively.

By Etiology: Fulminant Myocarditis Shows Surprising Growth

Acute myocardial infarction captured 56.35% of cardiogenic shock treatment market share in 2024 and continues to anchor volume, yet fulminant myocarditis advances at 11.63% CAGR as MRI and biomarker adoption enhance diagnosis. Temporary ECMO supports recovery in inflammatory cardiomyopathy, attracting attention from high-acuity centers. Non-ischemic cardiomyopathy holds stable demand, largely in bridge-to-transplant algorithms employing durable LVADs.

Post-cardiotomy shock persists as a specialized indication concentrated in established surgical programs, while niche etiologies including peripartum cardiomyopathy feed incremental growth. Public-health monitoring of vaccine-associated myocarditis contributed to earlier recognition and guideline updates, adding momentum to the cardiogenic shock treatment market.

By End User: Cath Labs Gain Prominence

Tertiary-care hospitals owned 66.38% share in 2024, housing the multidisciplinary skills and capital equipment vital for comprehensive MCS programs. Yet cardiac catheterization laboratories are forecast to expand at 10.02% CAGR, reflecting device miniaturization and operator familiarity. Small-footprint pumps facilitate shock stabilization during complex PCI cases, trimming procedure-to-support times below 45 minutes and shortening ICU admissions.

Ambulatory surgical centers remain minor participants, focusing on follow-up device surveillance and driveline care. Emergency departments evolve into gatekeepers that trigger shock alerts and initiate vasopressors before cath-lab transfer, broadening the referral funnel for the cardiogenic shock treatment market. Tele-ICU platforms link rural hospitals to hub-center perfusionists, balancing access inequities.

Geography Analysis

North America commanded 36.59% cardiogenic shock treatment market share in 2024 thanks to robust reimbursement and entrenched shock networks. The region sustains pipeline innovation through FDA Breakthrough Device designations and CMS transitional coverage. Europe follows with established registries and stringent safety mandates that nevertheless support steady uptake.

Asia-Pacific is projected for a 9.71% CAGR, spurred by cardiovascular disease prevalence and government funding for cath-lab expansion. China’s Healthy China 2030 plan earmarks new cardiovascular centers, while India’s Ayushman Bharat insurance widens device affordability. Gulf Cooperation Council states spearhead Middle East adoption via public-private hospital partnerships, whereas South America’s progress tracks macroeconomic stability. Localization of disposables manufacturing in Singapore and Shenzhen relieves part of the import cost burden, lifting the regional cardiogenic shock treatment market outlook.

Competitive Landscape

The cardiogenic shock treatment market is moderately consolidated. Abbott reinforces its Impella franchise with algorithm-enhanced flow control and training portals that reduce learning curves. Medtronic leverages its cardiovascular ecosystem to bundle ECMO consoles with oxygenator disposables and remote monitoring SaaS. Getinge strengthens its IABP line while investing in portable ECMO carts targeting transport teams.

Boston Scientific enters the field through strategic collaborations on temporary right-heart support, aiming to cross-sell within its electrophysiology portfolio. Micro-medtech start-ups focus on hemocompatible coatings, centrifugal pump miniaturization, and pediatric indications. Intellectual-property navigation shapes deal-making, with larger incumbents acquiring early-stage innovators to circumvent patent thickets.

Supply-chain security emerges as a differentiator: firms diversify resin and membrane sourcing and deploy predictive analytics to anticipate component shortages. Service contracts bundle disposables, software, and on-site technicians, cementing customer loyalty and smoothing revenue recognition, fortifying each player’s stake in the cardiogenic shock treatment market.

Cardiogenic Shock Treatment Industry Leaders

Abbott Laboratories

Medtronic plc

Johnson & Johnson (Abiomed)

Getinge AB

LivaNova plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Medtronic received CE Mark for the VitalFlow ECMO System, introducing a single-use centrifugal pump with integrated oxygenator for streamlined transport and ICU workflows.

- February 2025: CMS finalized national coverage for FDA-approved implantable pulmonary artery pressure sensors under Coverage with Evidence Development, broadening early decompensation detection pathways.

- January 2024: CMS finalized national coverage for FDA-approved implantable pulmonary artery pressure sensors under Coverage with Evidence Development, broadening early decompensation detection pathways.

Global Cardiogenic Shock Treatment Market Report Scope

| Pharmacological Therapy | Inotropes |

| Vasopressors | |

| Mechanical Circulatory Support Devices | Intra-aortic Balloon Pump (IABP) |

| Percutaneous Ventricular Assist Devices (Impella) | |

| Extracorporeal Membrane Oxygenation (ECMO) | |

| Surgical Ventricular Assist Devices (LVAD, RVAD, BiVAD) | |

| Revascularisation Procedures | Percutaneous Coronary Intervention (PCI) |

| Coronary Artery Bypass Grafting (CABG) |

| Stage A – At Risk |

| Stage B – Beginning Shock |

| Stage C – Classic Shock |

| Stage D – Deteriorating |

| Stage E – Extremis |

| Acute Myocardial Infarction |

| Non-Ischaemic Cardiomyopathy |

| Post-Cardiotomy |

| Fulminant Myocarditis |

| Others |

| Tertiary-Care Hospitals |

| Cardiac Catheterisation Labs |

| Ambulatory Surgical Centres |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pharmacological Therapy | Inotropes |

| Vasopressors | ||

| Mechanical Circulatory Support Devices | Intra-aortic Balloon Pump (IABP) | |

| Percutaneous Ventricular Assist Devices (Impella) | ||

| Extracorporeal Membrane Oxygenation (ECMO) | ||

| Surgical Ventricular Assist Devices (LVAD, RVAD, BiVAD) | ||

| Revascularisation Procedures | Percutaneous Coronary Intervention (PCI) | |

| Coronary Artery Bypass Grafting (CABG) | ||

| By Severity Stage (SCAI) | Stage A – At Risk | |

| Stage B – Beginning Shock | ||

| Stage C – Classic Shock | ||

| Stage D – Deteriorating | ||

| Stage E – Extremis | ||

| By Etiology | Acute Myocardial Infarction | |

| Non-Ischaemic Cardiomyopathy | ||

| Post-Cardiotomy | ||

| Fulminant Myocarditis | ||

| Others | ||

| By End User | Tertiary-Care Hospitals | |

| Cardiac Catheterisation Labs | ||

| Ambulatory Surgical Centres | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the cardiogenic shock treatment market?

The cardiogenic shock treatment market size stands at USD 1.11 billion in 2025 and is projected to reach USD 1.57 billion by 2030.

Which product category is expanding fastest?

Mechanical circulatory support devices are poised for an 11.57% CAGR through 2030, outpacing pharmacological therapies.

Which severity stage offers the greatest growth potential?

Stage B Beginning Shock is forecast for a 10.63% CAGR as hospitals embrace earlier preventive intervention.

What geographic region is projected to grow most quickly?

Asia-Pacific leads with a 9.71% CAGR due to expanded cardiac infrastructure and rising cardiovascular disease burden.

How do supply-chain challenges affect availability?

Oxygenator membrane and catheter shortages create procedure delays, prompting providers to stock higher inventories and consider multi-vendor strategies to safeguard continuity.

Page last updated on: