Cardiovascular And Soft Tissue Repair Patches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

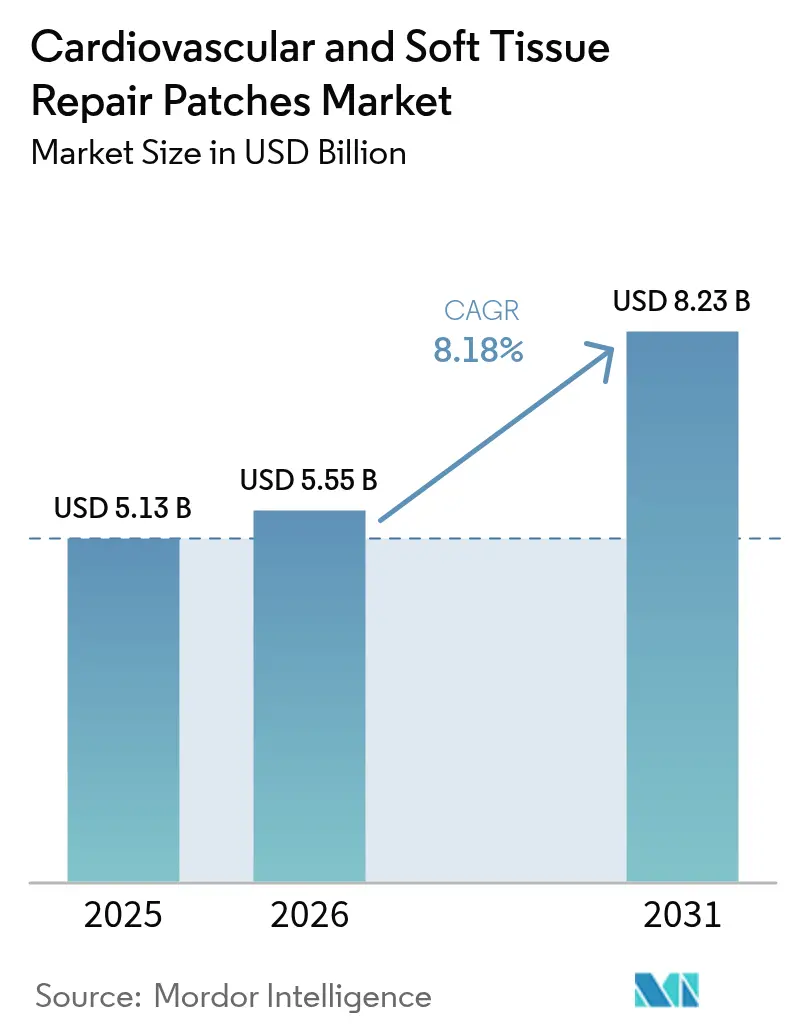

| Market Size (2026) | USD 5.55 Billion |

| Market Size (2031) | USD 8.23 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiovascular And Soft Tissue Repair Patches Market Analysis by Mordor Intelligence

The cardiovascular and soft tissue repair patches market size is expected to grow from USD 5.13 billion in 2025 to USD 5.55 billion in 2026 and is forecast to reach USD 8.23 billion by 2031 at 8.18% CAGR over 2026-2031. The cardiovascular and soft tissue repair patches market is shifting away from conventional sutures toward bio-engineered scaffolds that integrate more naturally with host tissue and reduce repeat procedures. Rising procedure volumes tied to aging populations, rapid progress in 3D-printed extracellular-matrix platforms, and clear clinical evidence that biologic options lower re-intervention rates anchor demand. Manufacturers are broadening synthetic portfolios to address raw-material shortages in bovine and porcine pericardium, while defense-funded regenerative projects accelerate product clearances. Hospitals still represent the largest customer pool, yet specialty cardiovascular clinics and ambulatory centers are adopting minimally invasive techniques that rely on thinner, self-adhering patches, creating new revenue streams across the cardiovascular and soft tissue repair patches market.[1]Author not listed, “Stem-cell heart patch shows potential,” Nature, nature.com

Key Report Takeaways

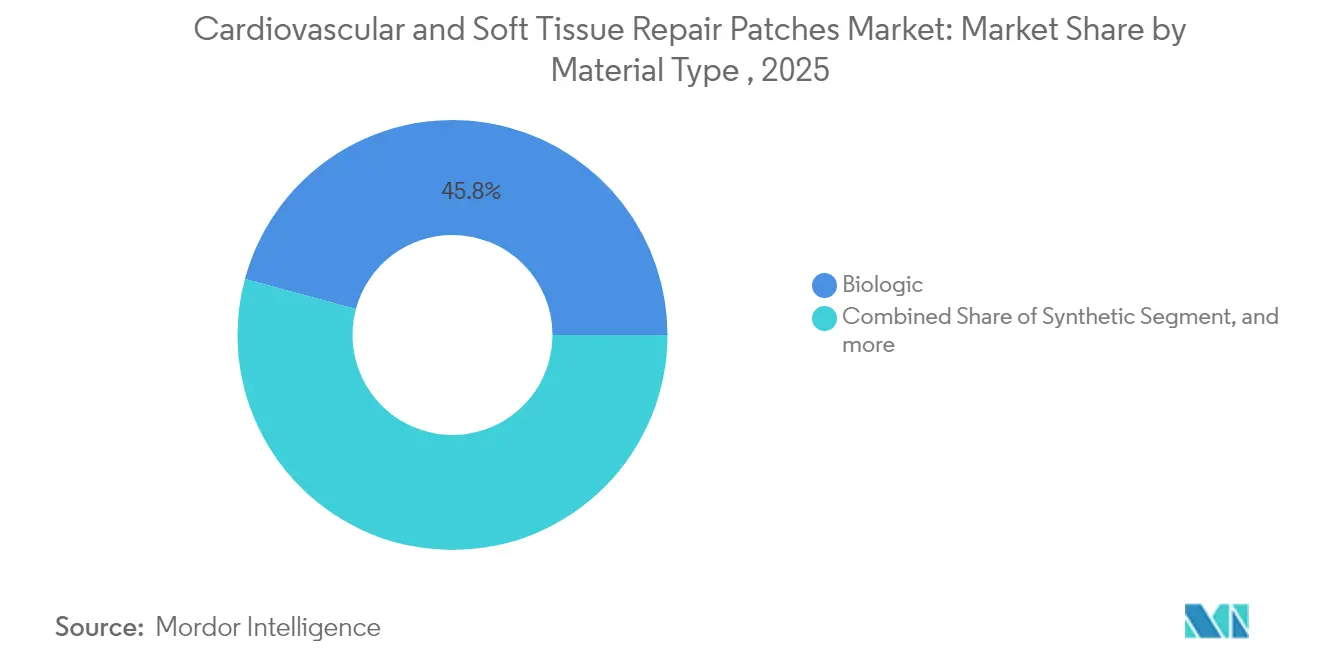

- By material type, synthetic patches led with 54.20% of the cardiovascular and soft tissue repair patches market share in 2025, whereas biologic options are on track for the fastest 8.52% CAGR through 2031.

- By application, soft-tissue repair captured 39.95% revenue in 2025, while cardiac repair is projected to advance at an 8.46% CAGR to 2031.

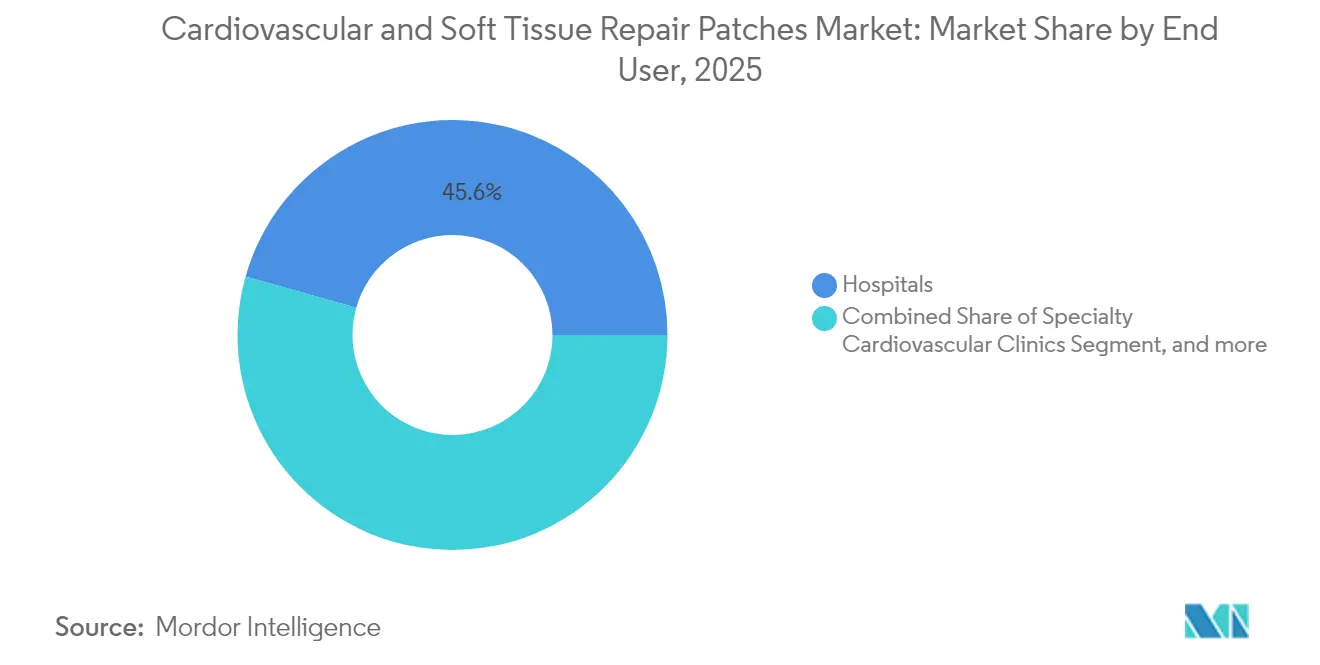

- By end user, hospitals held 45.62% of the cardiovascular and soft tissue repair patches market size in 2025; specialty cardiovascular clinics will grow the quickest at an 8.62% CAGR.

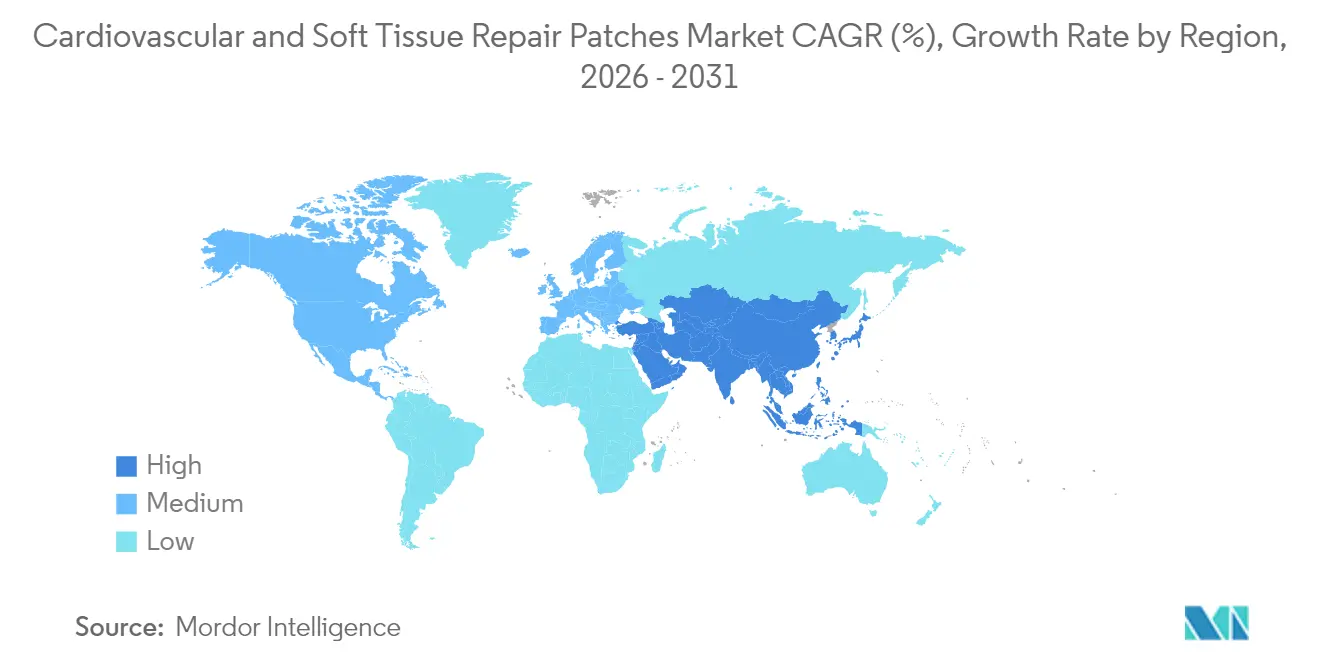

- By geography, North America accounted for 39.98% of sales in 2025; Asia-Pacific is positioned for an 8.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiovascular And Soft Tissue Repair Patches Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologic patch superiority lowering re-intervention rates | +1.8% | Global | Medium term (2-4 years) |

| Rapid adoption of minimally invasive cardiac defect closures | +1.5% | North America, EU; rising in Asia-Pacific | Short term (≤ 2 years) |

| Aging population boosting valve and septal repair volumes | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Reimbursement expansion for congenital heart repair in emerging markets | +0.9% | Asia-Pacific core | Medium term (2-4 years) |

| Bio-printed ECM scaffolds entering clinical pipelines | +0.7% | North America & EU, with selective APAC adoption | Long term (≥ 4 years) |

| Defense-funded regenerative medicine programs accelerating approvals | +0.4% | North America, with technology transfer to allies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biologic Patch Superiority Lowering Re-intervention Rates

Clinical follow-up shows biologic matrices cut repeat operations by 25-40%, steering surgeons toward bovine and porcine pericardial options that integrate with living tissue. Early-stage stem-cell patches registered marked gains in left-ventricular ejection fraction in multicenter trials. New keratin-based scaffolds add biodegradability and stimulate cell proliferation, broadening choices for pediatric and high-risk populations. Cost savings accrue when fewer revisions are needed, which strengthens hospital purchasing arguments. Collectively these gains push biologic adoption across the cardiovascular and soft tissue repair patches market at an accelerated clip.

Rapid Adoption of Minimally Invasive Cardiac Defect Closures

Smaller incisions paired with robot-assisted delivery let surgeons seat patches precisely, cut operating time, and shorten recovery. FDA clearance of multipoint pacing and self-adhering collagen fleece materials signals regulatory support for less-invasive hardware. Hospitals advertise faster discharge times to attract referrals, and specialty clinics deploy dedicated cath-lab suites for atrial-septal repairs. This momentum feeds growth in high-margin cardiac-use patches, strengthening future revenue visibility for the cardiovascular and soft tissue repair patches market.

Aging Population Boosting Valve & Septal Repair Volumes

Populations over age 65 are climbing sharply, pushing caseloads higher for degenerative valve and septal pathology. Valve-sparing patch procedures offer less trauma than full replacement, a point that resonates with older patients who present multiple comorbidities. Asia-Pacific shows the fastest elderly growth, which underpins its 8.89% CAGR outlook. Health authorities expand reimbursement to mitigate the fiscal burden of untreated cardiovascular disease, thereby widening the addressable base across the cardiovascular and soft tissue repair patches market.

Reimbursement Expansion for Congenital Heart Repair in Emerging Markets

India, China, and Brazil widen coverage for pediatric defect repairs, turning previously unmet needs into funded procedures. Government cardiac centers receive technology-transfer support from global NGOs, enabling implantation of advanced biologic matrices. Private insurers in urban regions underwrite premium materials for middle-income families. As coverage broadens, cardiac repair becomes the most dynamic application segment within the cardiovascular and soft tissue repair patches market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High comparative cost versus suturing and graft substitutes | -1.3% | Global | Short term (≤ 2 years) |

| Limited long-term durability data for bio-engineered tissue | -0.8% | North America, EU | Medium term (2-4 years) |

| Supply Shortage of Medical-grade Bovine & Porcine Pericardium | -0.5% | Medium term (2-4 years) | |

| Stricter EU MDR Evidence Requirements Delaying Launches | -0.4% | Medium term (2-4 years) | |

| Source: Mordor Intelligence | |||

High Comparative Cost Versus Suturing and Graft Substitutes

Premium biologic patches can retail for five to ten times the cost of a simple suture set, impeding adoption where capital budgets are strained. Administrators weigh immediate outlays more heavily than downstream savings from fewer revisions. Payers have been slow to realign reimbursement schedules, although value-based contracts are gaining traction in larger systems. Until upfront pricing narrows, price-sensitive facilities may favor traditional materials, dampening near-term install rates in the cardiovascular and soft tissue repair patches market.

Limited Long-term Durability Data for Bio-engineered Tissue

Regulators mandate decade-long data for pediatric implants, lengthening approval cycles for next-generation biomaterials. Conservative surgeons await proven safety before switching away from tried-and-true PTFE. The FDA’s rolling updates for AI-enabled devices reflect a broad caution around novel technologies, and similar rigor now applies to tissue substitutes. This uncertainty tempers the commercial ramp for bio-printed scaffolds within the cardiovascular and soft tissue repair patches market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Synthetic Strength Confronts Biologic Momentum

Synthetic products retained a 54.20% share of the cardiovascular and soft tissue repair patches market in 2025. PTFE’s mechanical strength and predictable supply chains keep it popular in high-volume centers. However, biologic matrices are growing at an 8.52% CAGR, reflecting demand for superior integration and lower calcification risk. Hybrid designs marry synthetic reinforcement with biologic coatings, a route that promises the durability clinicians expect while improving biocompatibility. Supply shortages of bovine pericardium spur R&D into keratin and algae-derived polymers, ensuring material diversity. Composite and 3D-printed options, though small in absolute terms, receive disproportionate venture funding, signaling investor belief in long-run disruption of the cardiovascular and soft tissue repair patches market.

Biologic growth is further fueled by pediatric needs where patches must expand with patient anatomy. Studies show growth-accommodating bovine patches cut secondary interventions by up to 30%. Manufacturers respond with decellularized tissues that leave natural collagen intact, boosting host-cell migration. FDA pathway reforms encourage cell-seeded constructs that may one day render inert synthetics obsolete. As data accumulate, biologics are expected to erode synthetic dominance, reshaping competitive stakes across the cardiovascular and soft tissue repair patches market.

By Application: Cardiac Surge Gains Challenge Soft-Tissue Lead

Soft-tissue repairs captured 39.95% of 2025 revenue due to the sheer volume of hernia, breast, and trauma cases. Yet cardiac repair is the top gainer at an 8.46% CAGR, energizing suppliers to refine materials for dynamic, high-pressure environments. Ventricular-septal defect closures now rely on thin flexible composites that tolerate constant motion. Valve annuloplasty rings integrated with collagen fleece limit leakage, pushing biologics deeper into OR routines. Vascular reconstruction benefits from similar advances, as endovascular surgeons request patches compliant enough to avoid kinking yet firm enough to resist dilation.

In soft-tissue settings, absorbable collagen sponges shorten wound-closure time, lowering infection risk. Orthopedic surgeons adopt keratin gels to bridge tendon tears. Trauma centers employ algae-derived hemostats that seal bleeding in under one minute. These cross-disciplinary wins keep soft-tissue's headline share intact even as cardiac volumes scale. The tug-of-war between segments enriches innovation pipelines throughout the cardiovascular and soft tissue repair patches market.

By End User: Specialty Clinics Narrow the Gap With Hospitals

Hospitals accounted for 45.62% of the cardiovascular and soft tissue repair patches market size in 2025, bolstered by comprehensive emergency services and broad insurance contracts. Large systems negotiate bundled deals that squeeze supplier margins on synthetics while carving premium tiers for complex biologics. Specialty cardiovascular clinics clock the highest growth at an 8.62% CAGR, capitalizing on reputation for high success rates. Their focused teams perform large case volumes, making them attractive early adopters of cutting-edge materials.

Ambulatory surgery centers escalate purchases for outpatient hernia and breast reconstructions where same-day discharge counts. These sites prefer self-adhering patches to minimize OR time and anesthesia exposure. Emergency medical services incorporate rapid-acting gels that stabilize trauma patients en route to definitive care, creating a niche yet expanding slice of demand. Across all channels, procurement decisions increasingly hinge on clinical outcome data, aligning purchasing logic with the emerging value ethos that permeates the cardiovascular and soft tissue repair patches market.

Geography Analysis

North America’s 39.98% share rests on sophisticated cardiac programs, extensive insurance coverage, and a pipeline of defense-funded regenerative initiatives that speed clearances. The United States surpasses 600,000 cardiac surgeries annually, giving suppliers an unmatched volume base. Canada’s single-payer model rewards lower total-care costs, nudging hospitals toward biologics that reduce readmission risk. Mexico adds outpatient demand via medical tourism corridors. Regulators maintain brisk review timelines, with more than 1,000 AI-enabled devices green-lit by March 2025. Pricing pressures persist under value-based rules, challenging suppliers to demonstrate real-world savings, yet the region remains the launchpad for next-wave technologies, cementing its influence on the cardiovascular and soft tissue repair patches market.

Asia-Pacific leads growth at an 8.67% CAGR. Japan and South Korea face pronounced aging curves, boosting valve-repair volumes. China scales tertiary hospitals in tier-two cities, adding capacity that funnels bulk orders for synthetic PTFE. India’s state insurance covers pediatric heart surgery for low-income families, unlocking biologic adoption. Governments back domestic manufacturing to cut import bills, and local startups tap 3D-printing know-how to supply custom scaffolds. Medical-tourism hubs in Thailand and Singapore market minimally invasive options to international patients, reinforcing premium sales. These converging forces position Asia-Pacific as the prime accelerator within the cardiovascular and soft tissue repair patches market.

Europe stays competitive through quality-focused procurement and rigorous evidence demands under the Medical Device Regulation. Germany anchors regional output with established PTFE capacity, while the United Kingdom powers transplantation research. France champions public–private consortia exploring decellularized matrices. National health funds reimburse products that show clear quality-adjusted life-year benefits, favoring biologics with durable data. Stricter launch requirements slow entry for newcomers yet raise overall safety standards. Cross-border care agreements deploy high-performance patches across the continent, keeping European clinicians current and patients mobile. These structural hallmarks sustain steady expansion and innovation engagement across the cardiovascular and soft tissue repair patches market.

Competitive Landscape

The cardiovascular and soft tissue repair patches market shows moderate concentration. Edwards Lifesciences, Medtronic, and Abbott leverage decades of brand equity, extensive field sales, and complementary valve and stent portfolios to secure preferred-vendor status. Their R&D budgets fuel incremental refinements—thinner PTFE layers, antimicrobial coatings—that extend product life cycles. Patent cliffs invite fast-followers from Asia, tightening price points on commoditized synthetics while prompting incumbents to bundle solutions with monitoring software to lock in accounts.

Disruptors pursue breakthrough biology. Capricor Therapeutics advances deramiocel, an allogeneic cell-therapy patch that won FDA priority review in 2025[3]Regulatory Affairs Professionals Society, “FDA Grants Priority Review to Deramiocel,” raps.org. Smaller firms deploy 3D bioprinters to fabricate patient-specific scaffolds from keratin or algae polymers, targeting rare congenital defects. Venture investors channel capital into platforms that combine growth factors with resorbable meshes to accelerate healing. To hedge against obsolescence, multinationals acquire or partner with these innovators, as observed in recent tie-ups between med-tech giants and university spin-outs specializing in extracellular-matrix design.

Pricing power is shifting. Hospitals exploit group-purchasing contracts to dictate synthetic patch discounts. Meanwhile, specialty clinics pay premiums for biologics that enhance outcomes and prestige. Raw-material shortages in bovine pericardium tighten supply, creating windfalls for synthetic-only producers in the short run but reinforcing long-term demand for alternative biologic sources. Intellectual-property skirmishes over printing recipes and decellularization protocols foreshadow the next competitive battleground across the cardiovascular and soft tissue repair patches market.

Cardiovascular And Soft Tissue Repair Patches Industry Leaders

LeMaitre Vascular Inc

Baxter

Cryolife, Inc.

CorMatrix, Inc

Anteris

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Capricor Therapeutics earned FDA priority review for deramiocel, an allogeneic cardiosphere-derived cell therapy for Duchenne cardiomyopathy, with a target action date of Aug 31 2025.

- December 2024: A Nature-branded Scientific Reports paper confirmed that decellularized scaffolds combined with iPSC-derived neural stem cells improved axonal regeneration in spinal-cord models, offering insight for cardiovascular patch design.

- August 2024: FDA cleared Traumagel, an algae-derived hemostatic gel that stops severe bleeding within seconds, now sold to emergency responders.

- November 2024: Peer-reviewed research highlighted keratin-based biomaterials with strong biodegradability and cell-support profiles, expanding the toolbox for future patch substrates.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cardiovascular and soft-tissue repair patches market as the sale of pre-sterilized biologic or synthetic patch materials specifically engineered to close, reconstruct, or reinforce cardiac septal defects, vascular walls, and soft-tissue defects arising from trauma, hernia, or congenital malformations. Products assessed include ePTFE, composite, and xenogeneic pericardial patches that are implanted through open or minimally invasive procedures.

Scope exclusion: disposable wearable ECG patches and hemostatic dressings are not included.

Segmentation Overview

- By Material Type

- Biologic

- Synthetic

- Next-gen Bio-printed/Composite

- By Application

- Cardiac Repair

- Atrial & Ventricular Septal Defect Closure

- Valve Reconstruction & Annuloplasty

- Soft-Tissue Repair

- Vascular Repair & Reconstruction

- Others

- Cardiac Repair

- By End User

- Hospitals

- Specialty Cardiovascular Clinics

- Ambulatory Surgery Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with cardiothoracic surgeons, general surgeons, biomaterial scientists, and hospital sourcing managers across North America, Europe, and key Asia-Pacific countries. These conversations tested incidence assumptions, price corridors, and replacement rates, while surveys with procurement heads revealed real-world mix shifts between biologic and synthetic patches. Insights from device distributors confirmed seasonality and tender dynamics.

Desk Research

We began with clinical and procedural data from open sources such as the World Health Organization surgical atlas, the American Heart Association's hospital statistics, Eurostat's inpatient procedure database, and national hernia registries. Regulatory filings (FDA 510k summaries, CE technical files), customs shipment data from UN Comtrade, and peer-reviewed biomaterials journals added insight on product flows and material adoption. Commercial context was enriched through company 10-Ks and investor decks, plus subscription inputs from D&B Hoovers and Dow Jones Factiva for revenue splits. These sources framed incidence rates, unit demand, and indicative average selling prices. The list is illustrative; many other public and proprietary references supported data gathering and cross-checks.

Second-level validation drew on specialty association reports, such as the Society for Vascular Surgery device surveys and the International Hernia Society guidelines, which clarified average patch utilization per procedure and regional practice patterns. This layering of macro health statistics and micro clinical metrics ensured the secondary foundation was grounded before interviews started.

Market-Sizing & Forecasting

A top-down build linked procedure volumes (e.g., atrial septal defect repairs, carotid endarterectomies, ventral hernia closures) to patch penetration and weighted average price. Select bottom-up checks, such as supplier revenue roll-ups and sampled ASP x volume from hospital tenders, were then used to tune totals. Core drivers modeled include aging-adjusted cardiac surgery incidence, hernia surgery growth, biologic patch premium trends, reimbursement tariff movements, bioprinted patch pipeline commercialization, and regional health-expenditure elasticity. Forecasts to 2030 employ multivariate regression with scenario analysis, allowing variables such as congenital heart disease screening rates or raw material inflation to flex within expert-endorsed bands. Data gaps, for example, private-hospital procedure counts, were bridged by ratio analysis against confirmed public-sector volumes.

Data Validation & Update Cycle

Outputs pass three-layer triangulation: automated variance scans, peer analyst review, and a senior domain lead sign-off. We refresh models annually and re-run critical nodes if material events, such as product recalls or reimbursement shifts, emerge, ensuring clients see the latest vetted view before each download.

Why Mordor's Cardiovascular and Soft Tissue Repair Patches Baseline Stands Up to Scrutiny

Published values often diverge because analysts choose different inclusion rules, price mixes, and refresh cadences.

Key gap drivers with other publishers include broader device baskets that mix wearable monitoring patches, omission of procedure decline in 2020-21 backlog recovery, or static ASP assumptions that overlook the biologic premium lift captured in Mordor's base case.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.13 B (2025) | Mordor Intelligence | - |

| USD 4.85 B (2025) | Regional Consultancy A | Excludes synthetic patch price escalation post-2023 |

| USD 4.50 B (2023) | Global Consultancy B | Uses 2019-2021 procedure averages without backlog normalization |

| USD 4.10 B (2022) | Trade Journal C | Bundles diagnostic ECG patches with implantables |

In sum, Mordor's disciplined scope, mixed-method modeling, and yearly refresh give decision-makers a balanced, transparent baseline that traces every figure to clear variables and repeatable steps, something clients tell us they can comfortably defend in board-room discussions.

Key Questions Answered in the Report

What is the current size of the cardiovascular and soft tissue repair patches market?

The cardiovascular and soft tissue repair patches market size reached USD 5.55 billion in 2026.

How fast is the market expected to grow?

The market is projected to register an 8.18% CAGR, pushing revenue to USD 8.23 billion by 2031.

Which material segment is expanding the quickest?

Biologic patches are forecast to grow at an 8.52% CAGR, outpacing synthetic alternatives.

Why are specialty cardiovascular clinics gaining share?

Their high procedure volumes, minimally invasive focus, and superior outcome metrics support an 8.62% CAGR, the strongest among end users.

Which region will contribute the highest incremental revenue?

Asia-Pacific, driven by aging demographics and expanded insurance coverage, is anticipated to show an 8.67% CAGR through 2031.

What remains the biggest barrier to wider biologic adoption?

Upfront cost differentials versus suturing and limited long-term durability data continue to slow uptake in price-sensitive systems.

Page last updated on: