Acute Coronary Syndrome Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

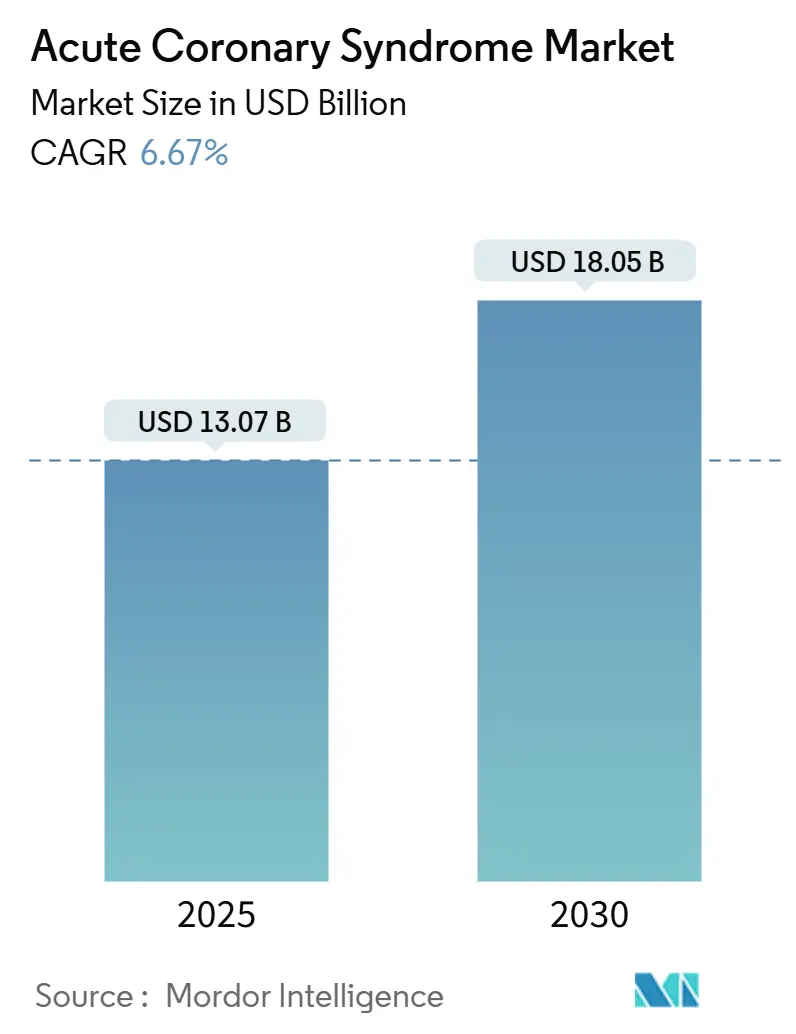

| Market Size (2025) | USD 13.07 Billion |

| Market Size (2030) | USD 18.05 Billion |

| Growth Rate (2025 - 2030) | 6.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Coronary Syndrome Market Analysis by Mordor Intelligence

The acute coronary syndrome market size stands at USD 13.07 billion in 2025 and is forecast to reach USD 18.05 billion by 2030, advancing at a 6.67% CAGR over the period. This upward trajectory is fueled by a sharp rise in coronary artery disease incidence, accelerated population aging, and continual guideline revisions that favor early invasive procedures and extended dual antiplatelet therapy. Innovation in drug-eluting stents, high-sensitivity biomarker testing, and next-generation P2Y12 inhibitors further amplifies demand, while artificial-intelligence-based triage tools improve diagnostic certainty and care pathways. The acute coronary syndrome market is also benefiting from hub-and-spoke STEMI networks across emerging economies that shorten reperfusion times and expand procedure volumes. Competitive intensity rises as pharmaceutical majors integrate with device specialists to deliver end-to-end treatment portfolios, creating defensible positions built on data analytics, clinical evidence, and premium reimbursement models.

Key Report Takeaways

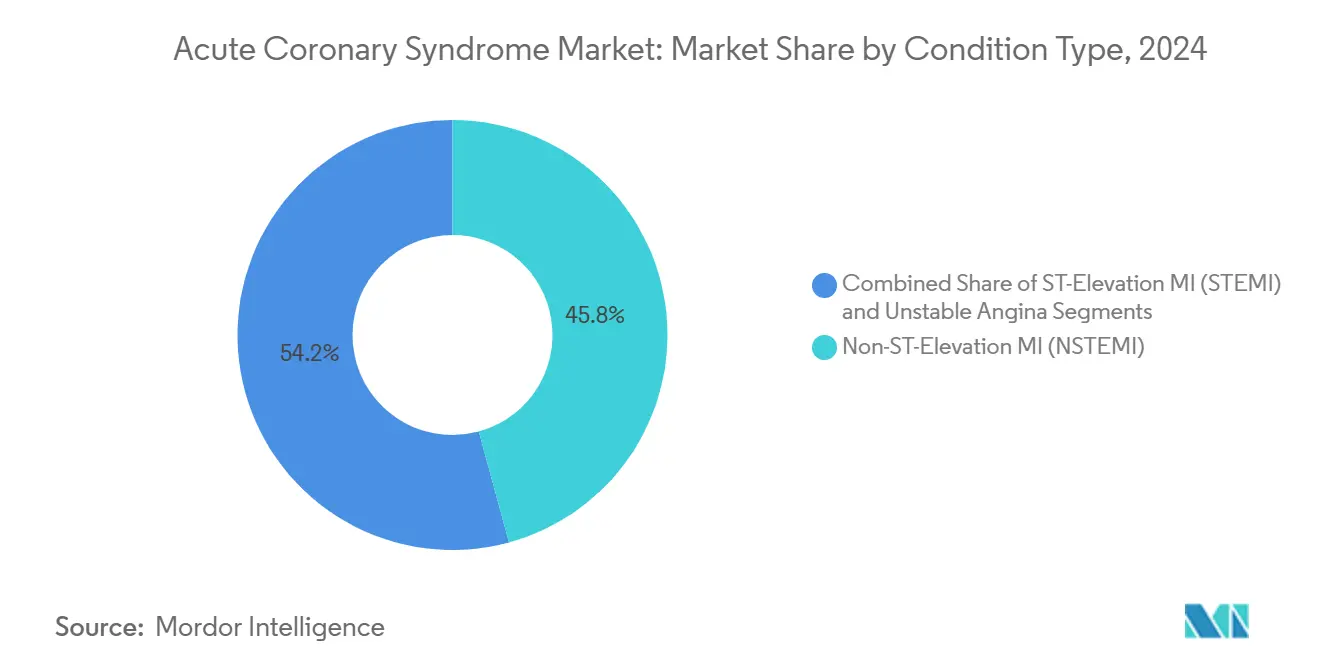

- By condition type, non-ST-elevation myocardial infarction accounted for 45.77% of the acute coronary syndrome market share in 2024, while ST-elevation MI is projected to expand at a 10.27% CAGR through 2030.

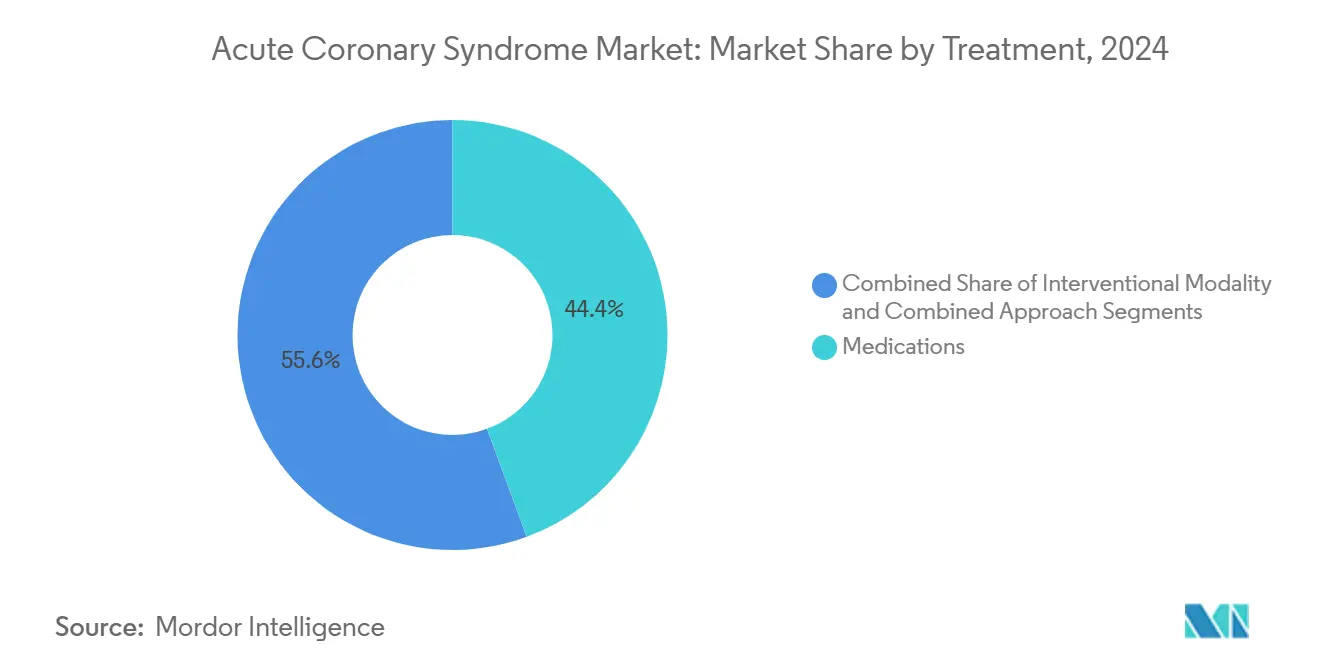

- By treatment, medications commanded 44.38% share of the acute coronary syndrome market size in 2024; interventional modalities are advancing at a 10.56% CAGR to 2030.

- By end user, hospitals captured 69.28% of the acute coronary syndrome market in 2024 and ambulatory surgical centers are growing fastest at an 8.45% CAGR through 2030.

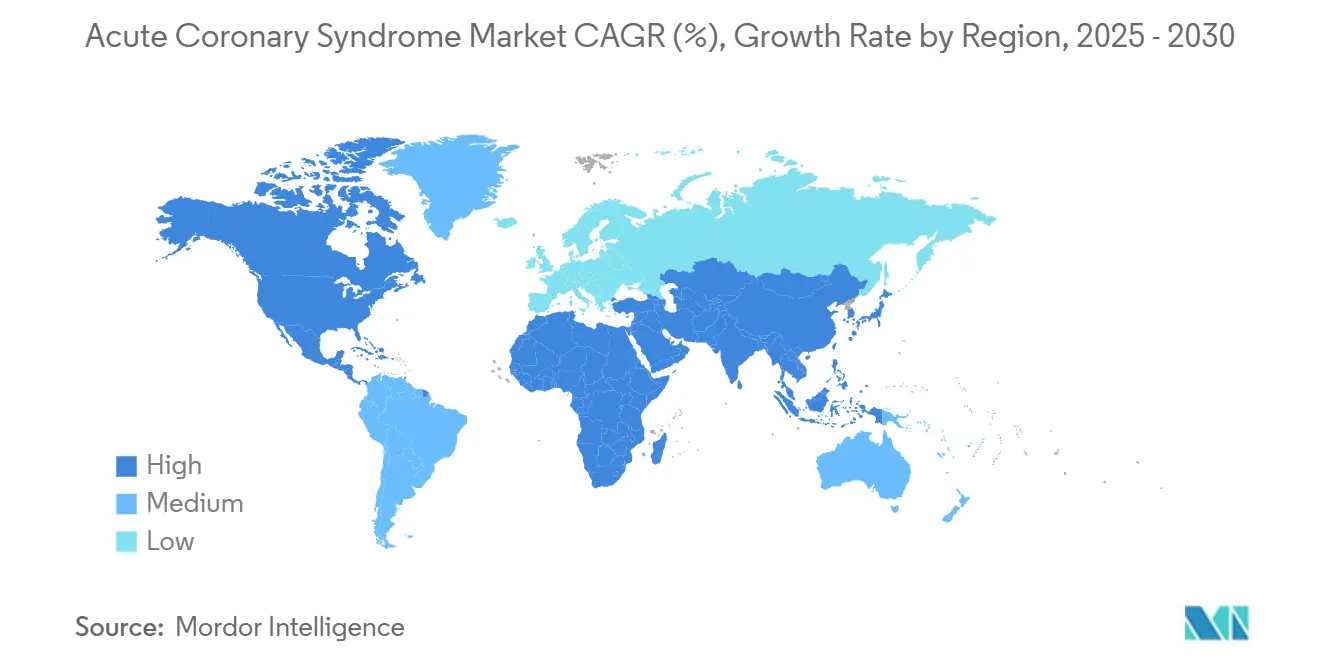

- By geography, North America led with 38.47% revenue share in 2024, whereas Asia-Pacific is forecast to register the highest CAGR at 8.36% to 2030.

Global Acute Coronary Syndrome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of coronary artery disease and aging population | +1.2% | Global; highest in North America and Europe | Long term (≥ 4 years) |

| Guideline updates favoring early invasive treatment and dual antiplatelet therapy | +0.8% | Global; rapid uptake in North America and EU | Medium term (2-4 years) |

| Technological advances in drug-eluting stents and next-generation P2Y12 inhibitors | +1.1% | Global; premium penetration in developed regions | Medium term (2-4 years) |

| Early adoption of high-sensitivity troponin tests in primary care | +0.9% | Asia-Pacific core, North America; emerging market spill-over | Short term (≤ 2 years) |

| AI-enabled ECG/biomarker triage for low-resource settings | +0.7% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Hub-and-spoke STEMI networks in emerging economies | +0.6% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Coronary Artery Disease & Aging Population

Global life-expectancy gains have tilted population pyramids toward older age brackets where acute coronary events cluster. Coronary artery disease remains the world’s leading cause of death, and the share of individuals over 65 years in North America and Europe now exceeds 19%. Parallel trends in metabolic syndrome and diabetes amplify risk in Asia-Pacific urban centers, enlarging the acute coronary syndrome market.[1]World Health Organization, “Cardiovascular Diseases (CVDs),” WHO.INT Sustained demand is therefore generated for both emergent revascularization procedures and long-term pharmaceutical management.

Guideline Updates Favoring Early Invasive Treatment & DAPT

The 2025 AHA/ACC guidance endorses door-to-balloon times below 90 minutes and extends dual antiplatelet therapy for high-risk cohorts. European Society of Cardiology statements mirror this stance, expanding the eligible pool for catheter-based intervention and premium antithrombotic agents. Hospitals worldwide are rewriting protocols to meet these benchmarks, elevating procedure volumes and prescription rates across the acute coronary syndrome market.[2]American College of Cardiology, “2025 AHA/ACC/HFSA Guideline for the Management of Heart Failure,” ACC.ORG

Technological Advances in DES & Next-Gen P2Y12 Inhibitors

Fourth-generation stents with bioabsorbable polymers, such as Boston Scientific’s Synergy, pair rapid endothelialization with low thrombogenicity, capturing share through superior outcomes. Simultaneously, investigational P2Y12 molecules that bypass CYP2C19 metabolic pathways improve platelet inhibition in Asian populations, enabling personalized therapy and opening premium revenue streams.

Early Adoption of High-Sensitivity Troponin Tests in Primary Care

Point-of-care assays deliver 0/1-hour rule-out algorithms in community clinics, cutting emergency department crowding and expediting transfers for invasive care. Validation studies show 98.8% sensitivity in ruling out myocardial infarction, creating an adjacent diagnostic segment within the broader acute coronary syndrome market.[3]Trond R. Johannessen, “Rapid Rule-Out of Acute Myocardial Infarction Using the 0/1-Hour Algorithm for Cardiac Troponins in Emergency Primary Care,” BMC Primary Care, bmcprimarycare.biomedcentral.com Rollout is brisk in Japan, South Korea, and select U.S. integrated systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of novel antithrombotics and drug-eluting stents in LMICs | -0.4% | Asia-Pacific emerging, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Bleeding-safety concerns limiting potent P2Y12 uptake | -0.3% | Global; heightened in elderly cohorts | Medium term (2-4 years) |

| Post-COVID catheterization-lab capacity backlog | -0.5% | Europe and North America | Short term (≤ 2 years) |

| CYP2C19 polymorphism-driven clopidogrel non-response in Asia | -0.2% | Asia-Pacific core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Novel Antithrombotics & DES in LMICs

Price gaps between generic clopidogrel and branded ticagrelor exceed 10:1 in India, while premium stents cost triple bare-metal alternatives. Budget constraints cause hospitals to default to legacy therapy, dampening adoption curves and suppressing the acute coronary syndrome market in low-income regions.

Bleeding-Safety Concerns Limiting Potent P2Y12 Uptake

Meta-analysis across 76,000 patients links ticagrelor and prasugrel to 35% higher major bleeding versus clopidogrel, prompting cautious prescriptions among elderly and chronic kidney disease cohorts. Clinicians often revert to lower-cost generics after acute phases, constraining sustained revenue streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Condition Type: NSTEMI Dominance Drives Market Stability

Non-ST-elevation myocardial infarction generated USD 5.98 billion, equal to 45.77% of the acute coronary syndrome market size in 2024, and benefits from high incidence among multimorbid seniors who often require lengthier hospital stays and multi-drug regimens. Detailed care pathways incorporate high-sensitivity troponin algorithms that clarify low-level biomarker elevations, thereby reclassifying many unstable-angina cases as NSTEMI. As guideline alignment progresses, this reclassification sustains segment leadership while improving coding accuracy and reimbursement capture.

ST-elevation MI, though smaller, is set for 10.27% CAGR, reflecting expanding PCI networks and EMS enhancements that enable primary PCI in under 120 minutes across many tier-2 Chinese cities. Outcome data show 12% relative mortality reduction where network maturation occurs, attracting public-health funding and device-maker focus. Unstable angina will shrink as high-sensitivity assays reduce diagnostic ambiguity, yet continued aspirin and statin utilization maintains baseline revenue. Cumulatively, these shifts keep the acute coronary syndrome market vibrant, reallocating value among segments without eroding aggregate demand.

By Treatment: Interventional Modalities Gain Momentum

Medications retained 44.38% of the acute coronary syndrome market share in 2024 because every patient receives antiplatelet and anticoagulant therapy, yet revenue growth slows as generics proliferate. Branded value now migrates toward potent P2Y12 agents, PCSK9 injectables for LDL reduction, and extended-release rivaroxaban for secondary prevention. Meanwhile, interventional modalities show 10.56% CAGR, propelled by fourth-generation stents, intravascular lithotripsy, and physiology-guided PCI that justify premium pricing through evidence-based outcome gains. The acute coronary syndrome market size for interventional modalities is estimated at USD 4.55 billion with robust pipeline momentum pointing to bioresorbable scaffold recovery post-earlier setbacks.

Combined approaches—leveraging optimized pharmacotherapy plus staged PCI—emerge in complex multivessel disease. Health-economic analyses in Japan reveal a 9-year cost-effectiveness advantage over surgery when fractional flow reserve guidance prevents unnecessary stents. Vendors able to bundle drugs, devices, and digital follow-up gain purchaser appeal, pushing the acute coronary syndrome market toward ecosystem competition rather than single-product rivalry.

By End User: Ambulatory Centers Challenge Hospital Dominance

Hospitals commanded 69.28% of the acute coronary syndrome market in 2024, reflecting their monopoly on emergent revascularization, intensive monitoring, and post-MI rehabilitation initiation. Yet rising labor expenses and bed shortages ignite payers’ interest in site-of-service shifts for elective and low-risk PCI. U.S. data show same-day radial-access PCI hospital costs are 18% higher than comparable ambulatory surgical center procedures. Consequently, the ambulatory segment is growing at 8.45% CAGR, with 42 new cardiac outpatient centers slated to open in India by 2027.

Cardiac centers—hybrid facilities offering diagnostics, day-case interventions, and tele-rehab—fill the middle ground. Their integration of imaging suites and catheter labs in one site trims referral leakage and improves patient adherence. As pay-for-performance schemes reward readmission reduction, these centers capture insurer contracts, diverting volumes from traditional hospitals and enlarging their slice of the acute coronary syndrome market size.

Geography Analysis

North America led the acute coronary syndrome market with 38.47% share in 2024, underpinned by broad insurance coverage, timely EMS activation, and over 1,800 PCI-capable labs. The U.S. spends 4 times Japan’s outlay on catheter hardware, enabling faster adoption of bioresorbable scaffolds and AI-driven lesion assessment tools. Canada’s single-payer model delivers stable procedure volumes, while Mexico’s public-private partnerships expand affordable stent programs to secondary cities.

Europe follows closely, emphasizing cost-effectiveness through health technology assessments. Germany and the U.K. spearhead uptake of drug-coated balloons, whereas Southern European systems negotiate volume-based rebates on antiplatelet bundles. Post-Brexit regulatory divergence accelerates U.K. approvals relative to EU timelines, creating a niche for early-market access in London trusts. However, fiscal pressures cap growth at mid-single-digit rates for the region.

Asia-Pacific is the fastest-rising territory, posting an 8.36% CAGR as China, India, and Indonesia upgrade cath-lab density. Chinese national insurance now reimburses radial-access PCI, sparking 17% annual volume growth, while India’s Ayushman Bharat scheme subsidizes generic ticagrelor post-stenting. Japan’s super-aged society drives recurring admissions, sustaining the acute coronary syndrome market despite flat population growth. Genetic diversity necessitates alternative antiplatelet strategies, creating differentiated product niches and reinforcing regional momentum.

Competitive Landscape

Competitive forces revolve around portfolio breadth, clinical evidence, and digital augmentation. AstraZeneca sustains share through long-term outcome data for ticagrelor while co-developing AI algorithms that identify relapse risk from ECG telemetry. Johnson & Johnson deepens vertical integration by pairing its P2Y12 pipeline with Biosense mapping catheters, ensuring supply continuity across acute care pathways. Abbott Laboratories leverages FDA approval for its Esprit BTK dissolving scaffold to enter complex peripheral-coronary crossover cases, widening addressable markets.

Device makers such as Boston Scientific emphasize polymer science breakthroughs, releasing Synergy XD with 60-day polymer absorption to minimize late thrombosis. Medtronic counters by embedding pressure-sensor chips within stent struts for real-time hemodynamic monitoring, bundling cloud analytics subscriptions that create annuity revenue. Start-ups deploy AI-triage engines atop vendor-neutral troponin analyzers, aiming to disintermediate incumbents via software-first value propositions.

M&A intensity climbs: 11 deals above USD 250 million closed in 2024, targeting imaging micro-catheters, resorbable metallic scaffolds, and pharmacogenomic diagnostics. Partnerships between lab chains and device vendors facilitate bundled reimbursements that favor integrated offerings over stand-alone products. As a result, the acute coronary syndrome market rewards scale yet leaves space for disruptive point-solution entrants capable of rapid clinical evidence generation.

Acute Coronary Syndrome Industry Leaders

AstraZeneca PLC

Sanofi

Johnson & Johnson

Abbott Laboratories

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Cardiology Society of India, Mysuru Chapter, launched the Mysuru Premature Acute Coronary Syndrome Registry (MPACS).

- June 2025: In a follow-up investigation into ticagrelor, The BMJ reported new concerns over platelet-function studies used in its FDA approval.

- March 2025: FDA approved tenecteplase for acute ischemic stroke, extending the thrombolytic’s utility and informing combination ACS-stroke protocols.

Global Acute Coronary Syndrome Market Report Scope

| ST-Elevation MI (STEMI) |

| Non-ST-Elevation MI (NSTEMI) |

| Unstable Angina |

| Medications | Antiplatelet Agents |

| Anticoagulants | |

| Beta-blockers | |

| ACE/ARB & Statins | |

| Others | |

| Interventional Modality | Percutaneous Coronary Intervention (PCI) |

| Coronary Artery Bypass Graft (CABG) | |

| Thrombolytic Therapy | |

| Coronary Stents (Bare-Metal, DES, Bioresorbable) | |

| Combined Approach |

| Hospitals |

| Cardiac Centres |

| Ambulatory Surgical Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Condition Type | ST-Elevation MI (STEMI) | |

| Non-ST-Elevation MI (NSTEMI) | ||

| Unstable Angina | ||

| By Treatment | Medications | Antiplatelet Agents |

| Anticoagulants | ||

| Beta-blockers | ||

| ACE/ARB & Statins | ||

| Others | ||

| Interventional Modality | Percutaneous Coronary Intervention (PCI) | |

| Coronary Artery Bypass Graft (CABG) | ||

| Thrombolytic Therapy | ||

| Coronary Stents (Bare-Metal, DES, Bioresorbable) | ||

| Combined Approach | ||

| By End User | Hospitals | |

| Cardiac Centres | ||

| Ambulatory Surgical Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the acute coronary syndrome market in 2030?

It is forecast to reach USD 18.05 billion, reflecting a 6.67% CAGR from 2025.

Which region shows the fastest growth for acute coronary care products?

Asia-Pacific leads with an 8.36% CAGR, driven by expanding cath-lab capacity and improving insurance coverage.

Why are ambulatory surgical centers gaining share in acute coronary treatment?

Radial-access techniques and payer cost-containment favor same-day PCI outside traditional hospitals, resulting in an 8.45% CAGR for ambulatory venues.

What technology trends most influence competitive dynamics?

Bioabsorbable polymer stents, AI-driven diagnostic algorithms, and high-sensitivity troponin point-of-care assays redefine product differentiation.

How do guideline updates affect product demand?

2025 ACC/AHA recommendations for early invasive treatment and longer dual antiplatelet therapy raise procedure volumes and premium drug utilization.

Which patient subgroup demands personalized antiplatelet therapy?

East Asian populations with high CYP2C19 loss-of-function allele prevalence require alternatives to clopidogrel for optimal platelet inhibition.

Page last updated on: