Infant Resuscitators Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

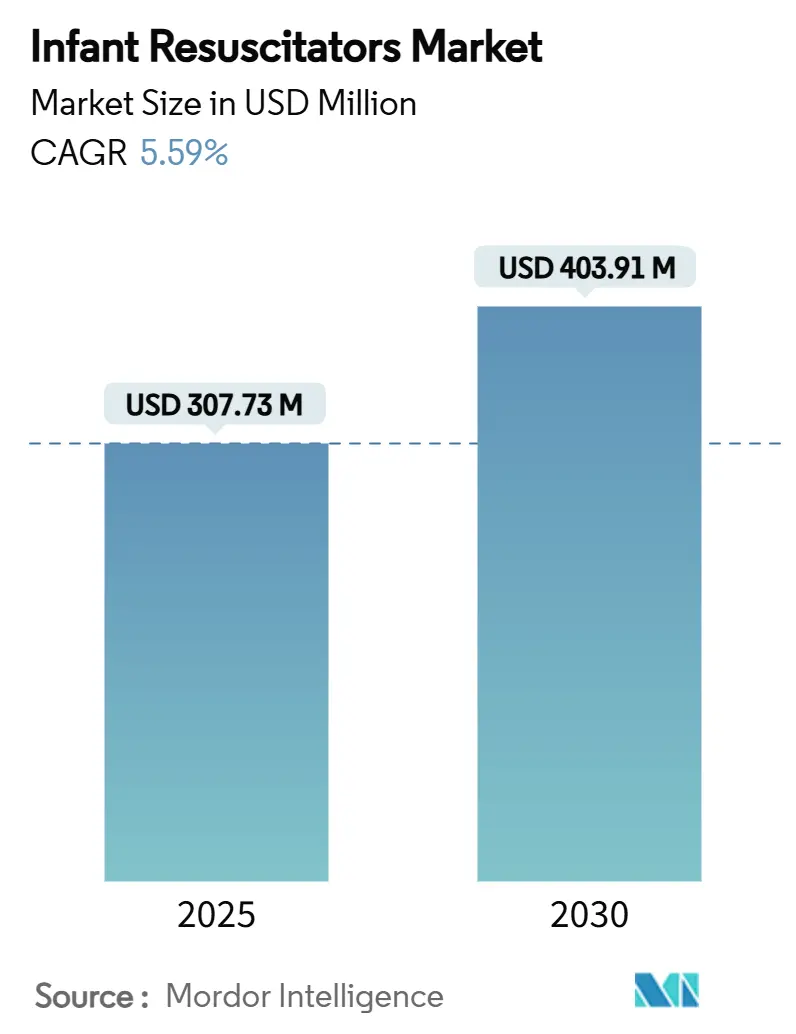

| Market Size (2025) | USD 307.73 Million |

| Market Size (2030) | USD 403.91 Million |

| Growth Rate (2025 - 2030) | 5.59% CAGR |

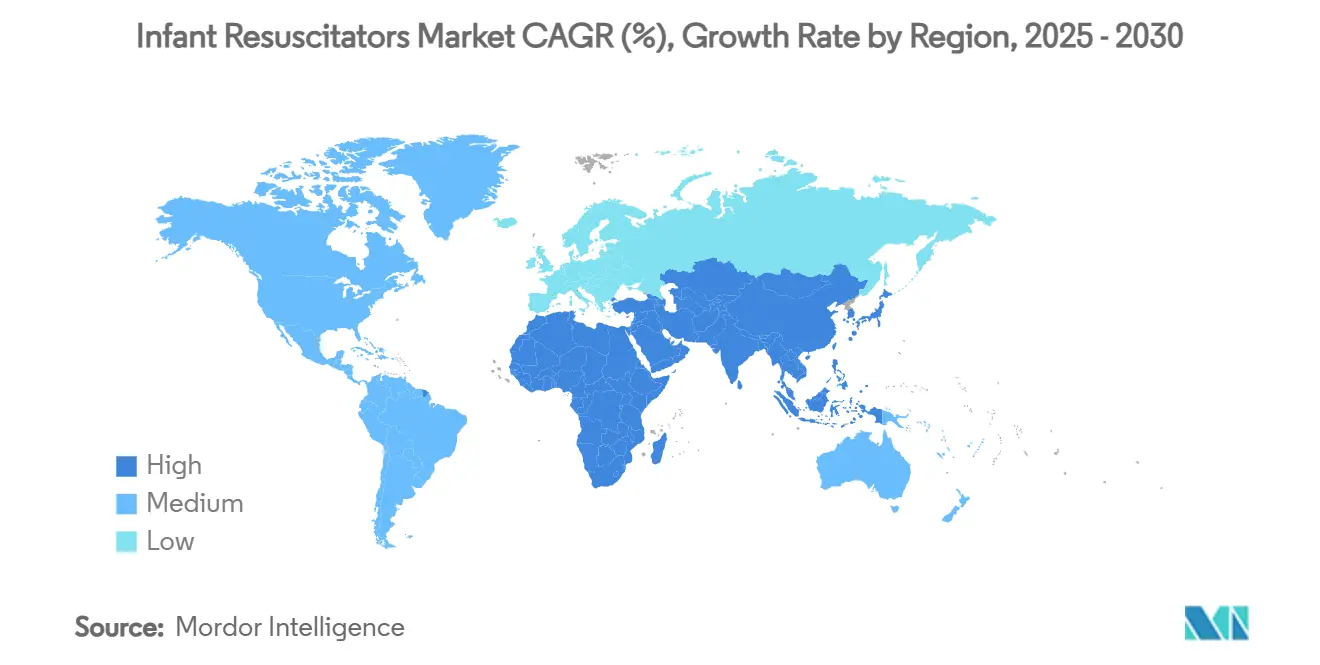

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

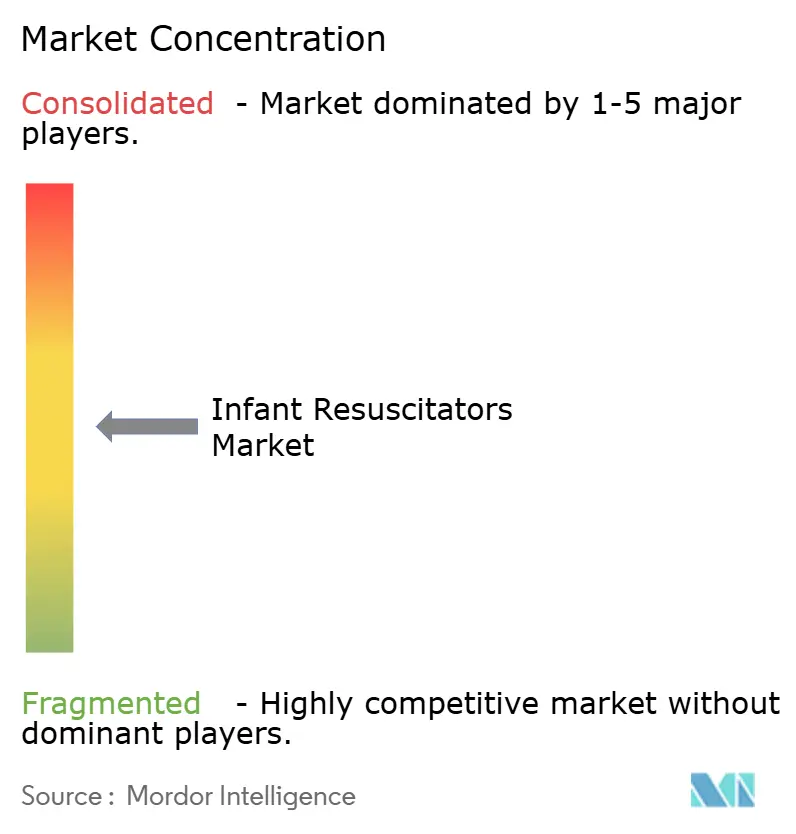

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infant Resuscitators Market Analysis by Mordor Intelligence

The infant resuscitators market size is valued at USD 307.3 million in 2025 and is forecast to climb to USD 403.91 million by 2030, registering a 5.59% CAGR. Strong demand stems from the need to curb the estimated 2.4 million newborn deaths each year, with birth asphyxia accounting for nearly 23% of these fatalities. Rapid neonatal-intensive-care-unit (NICU) expansion across Asia-Pacific, combined with new clinical guidelines that favor T-piece devices over conventional bag-valve-mask systems, is accelerating equipment upgrades in both developed and emerging economies.[1]Krisa Van Meurs, “2023 American Heart Association and American Academy of Pediatrics Focused Update on Neonatal Resuscitation,” Circulation, ahajournals.org Hospitals are prioritizing single-use devices to meet stricter infection-control rules, while integrated pressure-feedback sensors are moving resuscitation practice toward data-driven precision care. At the same time, large-scale “Helping Babies Breathe” programs in low- and middle-income countries (LMICs) are boosting volume demand for cost-effective kits, even as compliance costs and silicone supply constraints weigh on smaller manufacturers. Competitive intensity remains moderate; leading firms leverage regulatory know-how and broad distribution networks, whereas newcomers focus on low-cost, rugged designs for underserved regions.

Key Report Takeaways

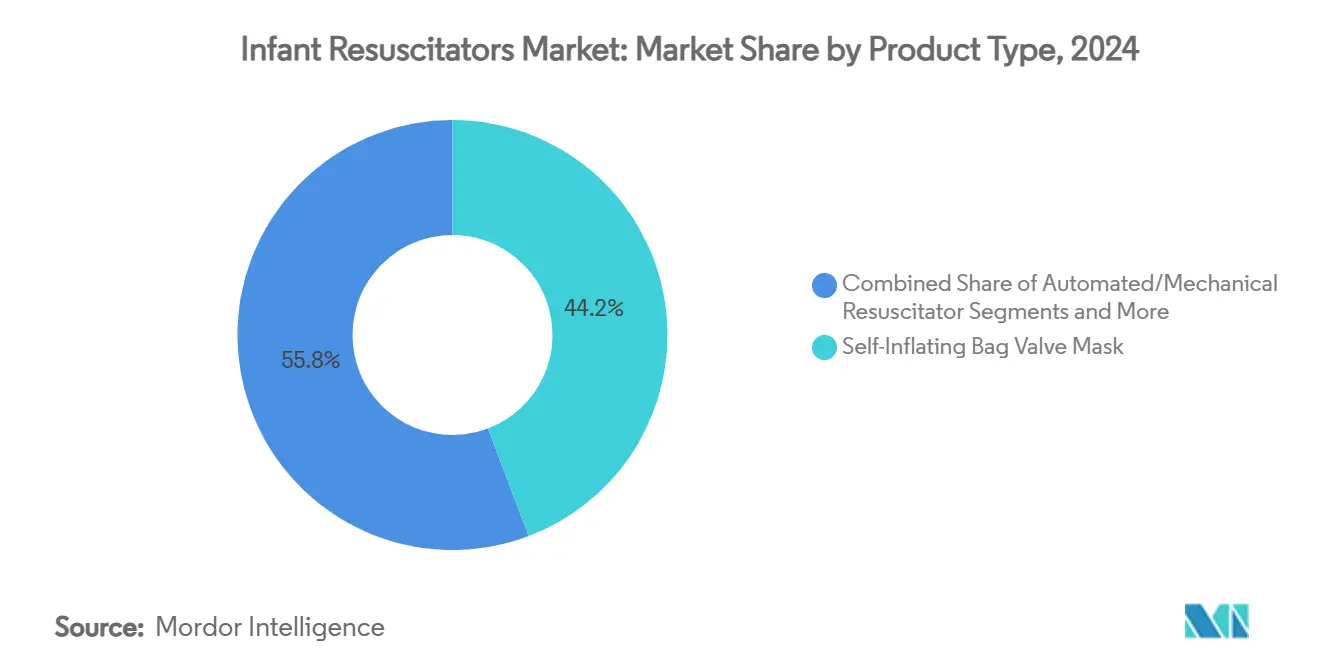

- By product type, self-inflating bag-valve masks led with 44.23% revenue share in 2024, while automated/mechanical resuscitators are projected to expand at an 8.43% CAGR through 2030.

- By modality, disposable devices captured 62.34% of 2024 revenue and are expected to register the fastest 9.05% CAGR over the forecast period.

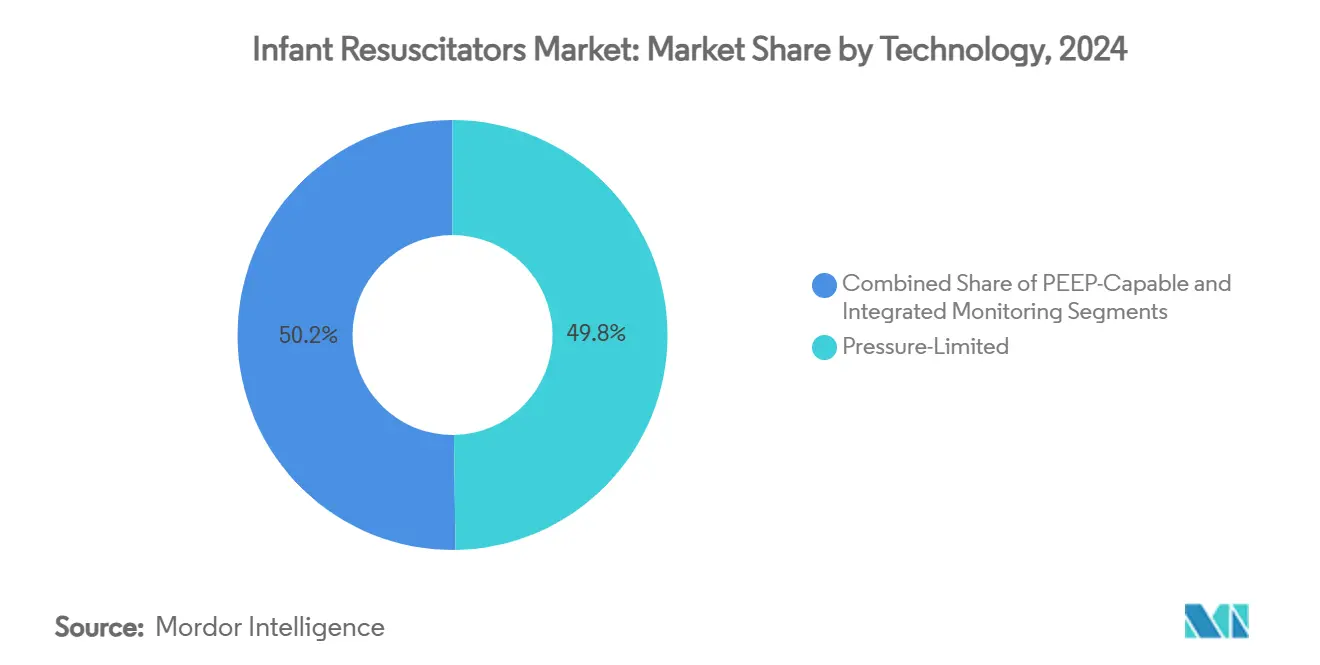

- By technology, pressure-limited systems held the largest 49.77% share in 2024; integrated-monitoring platforms are forecast to grow at a leading 9.23% CAGR to 2030.

- By end user, hospitals and NICUs commanded 56.48% of 2024 revenue, whereas EMS and pre-hospital settings are poised for the quickest 7.83% CAGR through 2030.

- By geography, North America accounted for 34.23% of global revenue in 2024, while Asia-Pacific is set to post the highest 8.21% CAGR during the projection window.

Global Infant Resuscitators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid NICU Expansion In Asia-Pacific | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Rising Guideline Preference For T-Piece Resuscitators | +0.9% | Global | Short term (≤ 2 years) |

| Shift Toward Disposable Single-Use BVMs In Infection-Control Protocols | +0.8% | Global | Short term (≤ 2 years) |

| Integration Of Smart Pressure-Feedback Sensors | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Government "Helping Babies Breathe" Roll-Outs In LMICs | +0.6% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Venture-Funded Development Of Ultra-Low-Cost Reusable Kits | +0.4% | LMICs, rural healthcare settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid NICU Expansion in Asia-Pacific

Governments across China, India and Southeast Asia are spending heavily to boost NICU bed density, creating a multiplier effect because every additional bed requires round-the-clock access to several infant resuscitators.[2]Yiwen Qian, “The CARE-Preterm Cohort Study Design and Baseline Characteristics,” BMC Pediatrics, biomedcentral.comThe CARE-Preterm cohort, covering 60 Chinese NICUs and more than 10,000 very-preterm births, reports a 10.74% mortality rate, underscoring the need for better devices and trained staff. Policy makers now tie capital grants to equipment quality, not just capacity, pushing hospitals to procure pressure-controlled systems over basic bag-valve masks. International development agencies also channel funds toward secondary- and tertiary-care upgrades, broadening the addressable base for premium devices. As urban hospitals modernize, provincial centers follow suit, sustaining double-digit unit demand growth through mid-decade.

Rising Guideline Preference for T-Piece Resuscitators

The 2023 focused update from the American Heart Association and American Academy of Pediatrics explicitly recommends T-piece devices for neonatal positive-pressure ventilation because they deliver more consistent peak inspiratory pressure than manual bags. Parallel endorsements by the European Resuscitation Council and ILCOR reinforce a global procurement pivot. Studies show mean peak inspiratory pressure of 16.5 cm H₂O with T-piece systems versus 20.7 cm H₂O for self-inflating bags, lowering ventilator-induced lung-injury risk. Training curricula have already shifted: the Neonatal Resuscitation Program now mandates device-specific competencies, catalyzing aftermarket demand for simulation units and spare circuits. Early adoption in the United States and Western Europe is spilling into Latin America and parts of Asia as multilateral health projects standardize resuscitation protocols.

Shift Toward Disposable Single-Use BVMs

Heightened infection-control awareness since the COVID-19 pandemic has pushed hospitals to limit reusable equipment in NICUs, where vulnerable infants face disproportionate sepsis risk. Updated U.S. Centers for Disease Control and Prevention guidelines flag the reprocessing challenges of devices with hidden lumens and complex valves, a profile that fits many reusable resuscitators. Device makers such as Ambu have pivoted to single-use lines, positioning disposables as a straightforward route to regulatory compliance and litigation risk reduction. FDA guidance on validating reprocessed single-use devices further tilts the cost-benefit equation toward disposables because the burden of proof shifts to the facility, not the manufacturer. Higher per-patient cost is increasingly offset by savings in staff time, sterilization chemicals and insurance premiums, anchoring disposables as the dominant modality.

Integration of Smart Pressure-Feedback Sensors

Roughly two-thirds of mechanically ventilated neonates experience inadvertent positive end-expiratory pressure (PEEP) greater than 1 cm H₂O, a condition that reduces lung compliance and impairs gas exchange.[3]Megan Peters, “Inadvertent Positive End-Expiratory Pressure in Mechanically Ventilated Newborn Infants,” The Journal of Pediatrics, jpeds.comNew-generation resuscitators embed micro-sensors that track peak inspiratory pressure and PEEP in real time, issuing audible alarms when thresholds are exceeded. Research teams are coupling these sensors with skin-interfacing wearable biosensors that capture heart rate and oxygen saturation, enabling closed-loop control protocols. Contactless photoplethysmography cameras are also moving from pilot to production, showing heart-rate accuracy within −0.2 bpm, which strengthens the case for fully integrated monitoring suites. As U.S. and European hospitals add these capabilities to procurement frameworks, average selling prices rise, creating headroom for vendors to fund continuous R&D and software updates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ISO 10651 & FDA Class IIb Compliance Costs | -0.8% | Global, particularly impacting new entrants | Short term (≤ 2 years) |

| Risk Of Inadvertent PEEP With T-Piece Systems | -0.6% | Global, clinical adoption hesitancy | Medium term (2-4 years) |

| Supply-Chain Shortfalls Of Medical-Grade Silicone | -0.5% | Global manufacturing | Short term (≤ 2 years) |

| Low Clinician Training Penetration In Rural Facilities | -0.4% | LMICs, rural healthcare settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent ISO 10651 & FDA Class IIb Compliance Costs

Gaining market clearance for an infant resuscitator can cost well over USD 2 million once biocompatibility tests, bench verification and clinical validation studies are tallied. ISO 10651-4 updates added in 2024 demand tighter pressure-accuracy tolerances and more robust alarm systems, forcing design revisions even for legacy products. U.S. manufacturers must match those requirements while also filing FDA 510(k) submissions, including exhaustive material traceability that relies on supplier master files—NuSil alone maintains more than 700 silicone dossiers. These hurdles lengthen time-to-market, deter venture investment and leave price-sensitive LMIC tenders largely to incumbent multinationals that can amortize compliance overhead across broad product portfolios.

Risk of Inadvertent PEEP with T-Piece Systems

Although T-piece devices win on pressure consistency, studies show they can generate excessive PEEP, especially when gas flow rates exceed 10 L/min and expiration times shorten. Compliance-dependent delivered PEEP poses special concern in term infants with healthy lungs and in settings where operator skill varies. Clinical hesitancy is therefore highest in rural hospitals, where staff turnover undercuts continuous competency upkeep. Liability fears run high in litigious markets, and some procurement committees still purchase bag-valve-mask units as a fallback, diluting near-term demand for T-piece systems. Vendors must embed flow-limiting valves and clearer feedback displays to overcome these clinical reservations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automated Systems Challenge Manual Dominance

Self-inflating bag-valve masks held 44.23% of the infant resuscitators market in 2024 thanks to their low price and ease of use. Yet automated or mechanical resuscitators are forecast to grow at an 8.43% CAGR as hospitals standardize protocols and reduce operator-dependent variability. The infant resuscitators market size for automated systems is projected to widen sharply between 2025 and 2030 as NICUs attach premium to integrated alarms and data logging. Flow-inflating bags remain a niche choice among highly trained clinicians demanding fine pressure control, while guideline-driven preference for T-piece devices adds further pressure on manual BVM incumbents.

Clinical literature demonstrates that T-piece resuscitators deliver a mean peak inspiratory pressure of 16.5 cm H₂O versus 20.7 cm H₂O for self-inflating bags, explaining the gradual but steady shift toward devices that minimize barotrauma risk. Added electronics push average selling prices higher, allowing vendors to offset rising silicone and sensor input costs. Procurement policies in Europe increasingly limit manual ventilation to emergency backups, accelerating the product-mix swing in the infant resuscitators market.

By Modality: Disposable Dominance Accelerates Post-Pandemic

Disposable units captured 62.34% of the infant resuscitators market share in 2024 as infection-control rules tightened worldwide. The modality’s 9.05% CAGR reflects hospitals’ willingness to trade higher consumable costs for lower sterilization complexity and litigation exposure. Reusable resuscitators still appeal to high-volume public facilities, yet the FDA’s demanding guidance on reprocessing validation is nudging many toward single-use kits.

Manufacturers are innovating with lighter polymers and modular valve inserts to keep unit economics viable even in resource-constrained markets. Meanwhile, carbon-footprint concerns spur interest in recyclable materials, a factor likely to shape product-design roadmaps by the late 2020s. Because disposables remove the logistical bottleneck of autoclave scheduling, clinical teams gain faster room-turn capability, bolstering throughput in busy tertiary centers and cementing disposable leadership within the infant resuscitators market.

By Technology: Integrated Monitoring Emerges as Premium Tier

Pressure-limited devices still generate 49.77% of 2024 revenue, but integrated-monitoring systems are growing fastest at 9.23% CAGR as facilities transition from reactive to data-driven ventilation. Vendors bundle flow-sensors, oxygen analyzers and Bluetooth telemetry, enabling real-time dashboards in central nursing stations. This high-feature tier commands premium pricing, lifting the infant resuscitators market size for smart systems well above the category average.

PEEP-capable devices serve as a mid-range option, favored in settings that lack budget for full telemetry yet want more safety than basic pressure-limited kits offer. Contactless heart-rate imaging and epidermal biosensors, validated at ±0.2 bpm accuracy, are beginning to converge with these resuscitators, paving the way for unified neonatal monitoring suites. Regulatory bodies encourage built-in alarm redundancy, further differentiating integrated platforms from low-cost analog units.

By End User: EMS Settings Drive Growth Beyond Traditional NICUs

Hospitals and dedicated NICUs accounted for 56.48% of 2024 sales, reflecting the concentration of high-risk births in tertiary facilities. Yet EMS and pre-hospital services are poised for a 7.83% CAGR, fueled by regionalized perinatal networks that dispatch neonatal retrieval teams equipped with portable resuscitators. Launch-time improvements from 35.5 minutes to 17.0 minutes in urgent neonatal transfers underscore why ambulance crews now demand lightweight, battery-operated devices with automatic pressure control.

Ambulatory surgical centers and maternity clinics remain smaller segments but are steadily refreshing inventories to meet updated resuscitation guidelines. Vendors differentiate offerings by portability, battery life and ambient-temperature tolerance, tailoring SKUs to diverse care environments. These moves broaden the customer base and stabilize recurring revenue in the infant resuscitators market.

Geography Analysis

North America generated 34.23% of global revenue in 2024, benefiting from high healthcare expenditure and strict enforcement of updated neonatal resuscitation protocols. Despite a 227% rise in neonatologists and a 48% increase in NICU beds over three decades, mortality reduction has plateaued, pushing hospitals to prioritize equipment sophistication over sheer capacity. The FDA flags pediatric-device supply gaps—such as shortages of neonatal breathing tubes—as critical vulnerabilities, prompting domestic sourcing initiatives and bolstering local production of advanced resuscitators. Integrated-monitoring units therefore see strong uptake, as they align with hospital digital-strategy roadmaps and justify premium reimbursement.

Asia-Pacific is the standout growth engine at an 8.21% CAGR, propelled by large public-sector investments in maternal-and-child health infrastructure. China’s CARE-Preterm cohort underscores the scale: 60 NICUs handling more than 10,000 very-preterm infants still record 10.74% mortality, spotlighting the capability gap that modern resuscitators can close. UNICEF’s landscape analysis identifies rural shortfalls in essential newborn care, steering budget toward neonatal equipment upgrades in secondary hospitals and township health centers. Price sensitivity remains high, so suppliers offer tiered portfolios—low-cost reusable kits for district hospitals and smart systems for metropolitan centers—ensuring broad penetration across income strata in the infant resuscitators market.

Europe shows stable replacement-cycle demand, helped by CE-mark harmonization and strong academic links that drive evidence-based adoption. Studies from European neonatal units have influenced global flow-limit recommendations for T-piece devices, reinforcing regional leadership in safety-focused designs. Meanwhile, Middle East & Africa benefit from multilateral partnerships such as the COINN/NEST360 program, which deploys bundled training and equipment packages to frontline facilities. South America follows a middle path: Brazil and Argentina invest in NICU upgrades yet seek cost-effective products that balance safety with budget constraints, sustaining steady, mid-single-digit growth.

Competitive Landscape

The infant resuscitators market is moderately fragmented. Incumbents like Drägerwerk, GE HealthCare and Koninklijke Philips leverage deep regulatory expertise and multi-channel distribution to protect share. Specialty players—Laerdal Medical, Fisher & Paykel Healthcare and Ambu—focus on neonatal innovations, such as single-use valves or humidity-optimized circuits, often pairing hardware with simulation-based training modules. Rising compliance costs under ISO 10651 and FDA Class IIb rules act as defensive moats for these established vendors, while smaller firms struggle to fund multi-year validation pipelines.

Strategically, most leaders double down on disposables to capture the infection-control trend; Ambu’s neonatal portfolio exemplifies this pivot. Smart-sensor integration is another battleground: Dräger and GE embed pressure, flow and FiO₂ telemetry that feeds hospital analytics suites, differentiating on data interoperability. In LMICs, cost-optimized designs from emerging Asian manufacturers are gaining tender wins, but scale-up remains challenged by silicone shortages and fluctuating foreign-exchange rates.

M&A activity centers on platform expansion and supply-chain security. Recent examples include cross-licensing deals for miniaturized pressure sensors and localized molding partnerships designed to hedge against material shortages. As procurement criteria evolve toward outcome-based metrics, vendors that pair connected hardware with analytics dashboards are likely to widen their lead, even as ultra-low-cost challengers target the bottom of the pyramid.

Infant Resuscitators Industry Leaders

Drägerwerk AG & Co. KGaA

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Ambu A/S

Laerdal Medical AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Global Financing Facility reported that Tanzania’s Safer Births Bundle of Care cut early newborn deaths by 40%, validating large-scale roll-outs that combine training with resuscitation-device provision.

- November 2024: The Council of International Neonatal Nurses and NEST360 launched a partnership to improve care for small and sick newborns in sub-Saharan Africa, focusing on equipment deployment and clinician training.

Global Infant Resuscitators Market Report Scope

| Self-Inflating Bag Valve Mask |

| Flow-Inflating Bag |

| T-piece Resuscitator |

| Automated/Mechanical Resuscitator |

| Reusable |

| Disposable |

| Pressure-Limited |

| PEEP-Capable |

| Integrated Monitoring |

| Hospitals & NICUs |

| Ambulatory Surgical Centers |

| EMS / Pre-hospital Settings |

| Maternity Clinics & Birth Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Self-Inflating Bag Valve Mask | |

| Flow-Inflating Bag | ||

| T-piece Resuscitator | ||

| Automated/Mechanical Resuscitator | ||

| By Modality | Reusable | |

| Disposable | ||

| By Technology | Pressure-Limited | |

| PEEP-Capable | ||

| Integrated Monitoring | ||

| By End User | Hospitals & NICUs | |

| Ambulatory Surgical Centers | ||

| EMS / Pre-hospital Settings | ||

| Maternity Clinics & Birth Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current infant resuscitators market size and its expected growth?

The infant resuscitators market size stands at USD 307.3 million in 2025 and is projected to reach USD 403.91 million by 2030, implying a 5.59% CAGR.

Which product category holds the largest infant resuscitators market share?

Self-inflating bag-valve masks lead with 44.23% market share in 2024, though automated systems are growing faster.

Why are disposable resuscitators gaining traction?

Tighter infection-control guidelines and the high cost of validating reusable-device reprocessing are driving hospitals toward single-use units despite higher per-item prices.

Which region is expected to grow the fastest through 2030?

Asia-Pacific is forecast to post the quickest 8.21% CAGR, driven by sizable government investments in NICUs and rising birth volumes.

What is the biggest regulatory hurdle for new market entrants?

Meeting ISO 10651-4 and FDA Class IIb requirements can cost over USD 2 million and add multi-year approval timelines, discouraging startups.

Page last updated on: