Gastrointestinal Stent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

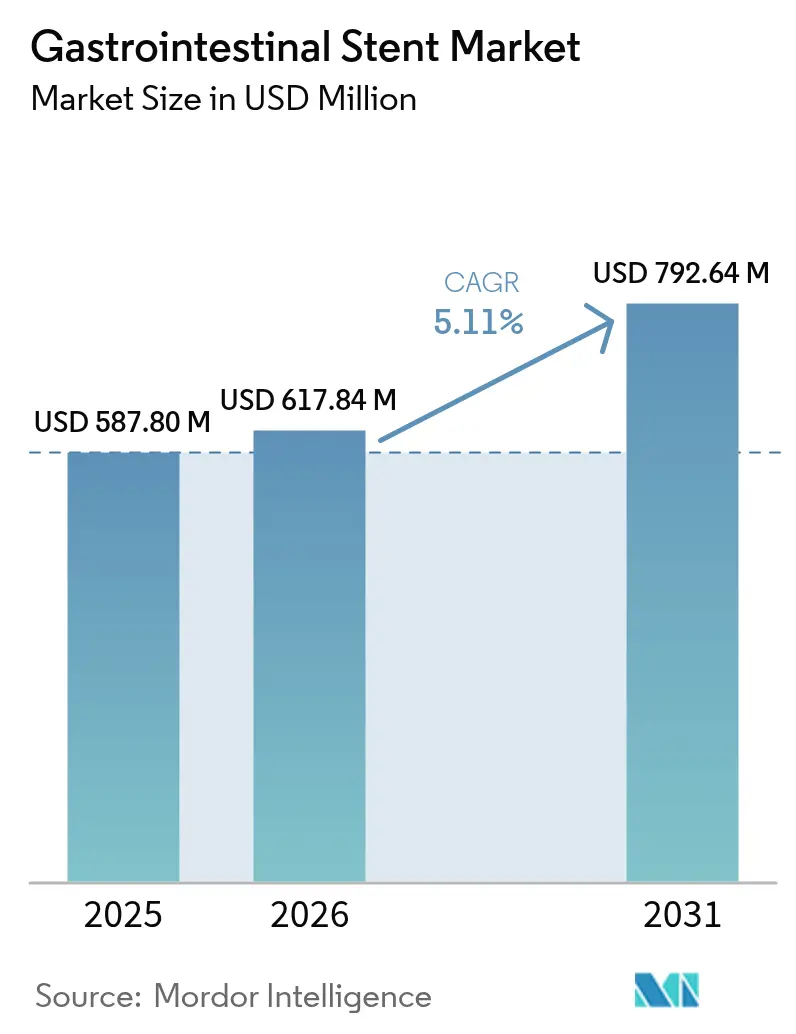

| Market Size (2026) | USD 617.84 Million |

| Market Size (2031) | USD 792.64 Million |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastrointestinal Stent Market Analysis by Mordor Intelligence

The gastrointestinal stent market size was valued at USD 587.80 million in 2025 and estimated to grow from USD 617.84 million in 2026 to reach USD 792.64 million by 2031, at a CAGR of 5.11% during the forecast period (2026-2031). Rising gastrointestinal (GI) cancer prevalence, a decisive clinical pivot toward minimally invasive endoscopy, and sustained advances in stent design—especially biodegradable and drug-eluting formats—anchor this expansion. Broader use of endoscopic ultrasound (EUS) and artificial-intelligence–guided planning has lowered technical barriers, improved patient-specific customization, and widened procedural suitability, especially for complex pancreaticobiliary disease. North America maintains volume leadership, yet high incidence of colorectal cancer and rapidly modernizing hospital networks position Asia-Pacific as the fastest-advancing region. Robust clinical evidence highlighting cost savings, shorter recovery times, and high patency levels reinforces payer acceptance and accelerates adoption across both malignant and benign indications.

Key Report Takeaways

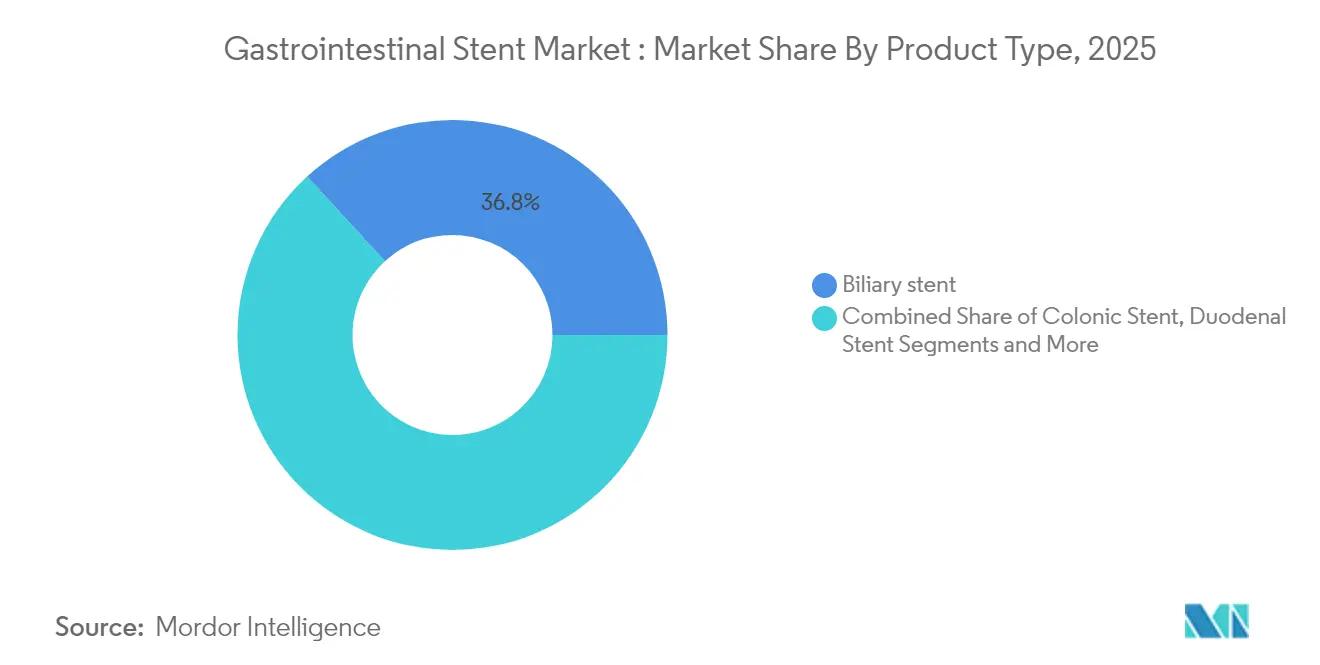

- By product type, biliary stents led with 36.82% revenue share in 2025; colonic stents are forecast to expand at an 8.67% CAGR through 2031.

- By material, self-expanding metal stents accounted for 61.05% of the gastrointestinal stent market size in 2025, while biodegradable and drug-eluting stents are projected to grow at an 8.41% CAGR to 2031.

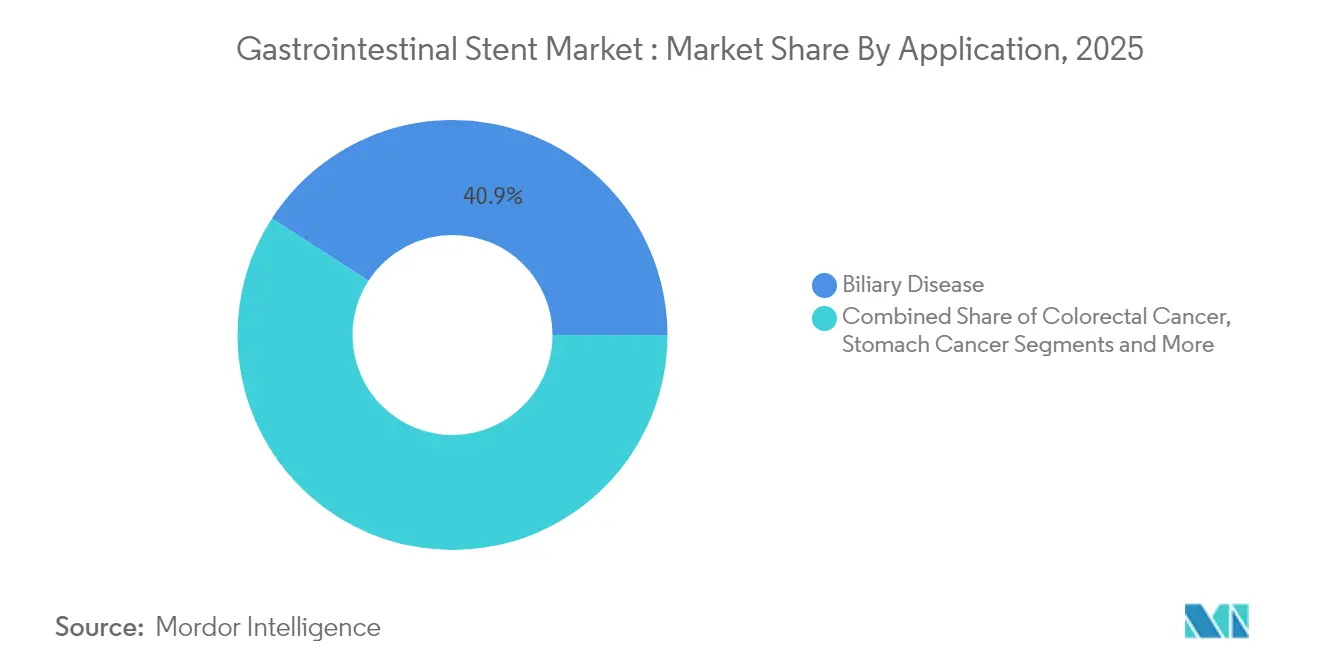

- By application, biliary disease captured 40.88% of the gastrointestinal stent market size in 2025, and colorectal cancer applications are advancing at a 8.92% CAGR through 2031.

- By end user, hospitals held 63.78% of the gastrointestinal stent market share in 2025; ambulatory surgical centers are set to rise at a 7.56% CAGR over the forecast period.

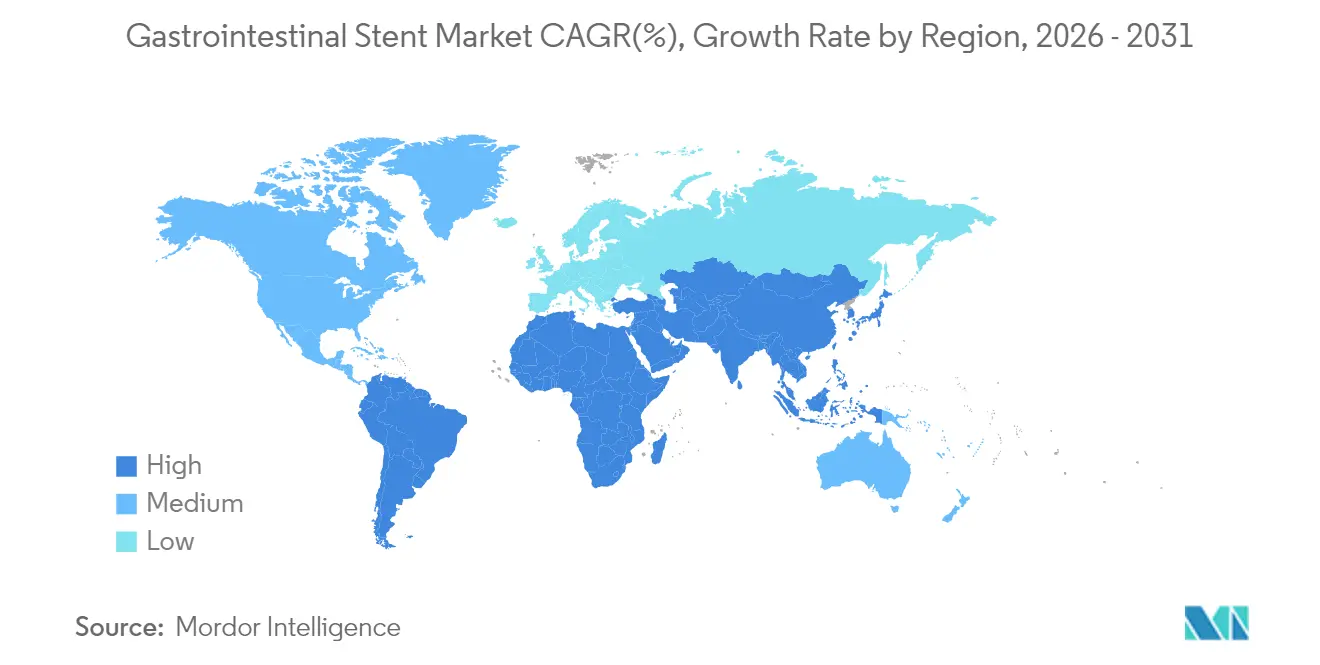

- By geography, North America dominated with 35.12% of 2025 revenues, while Asia-Pacific is poised for the fastest 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastrointestinal Stent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of GI cancers | +1.2% | Global, highest in APAC | Long term (≥ 4 years) |

| Ageing population & comorbid GI disorders | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Shift toward minimally invasive endoscopy | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| Rapid adoption of EUS-guided stenting | +0.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| AI-driven stent design & customization | +0.6% | North America & EU core markets | Long term (≥ 4 years) |

| Technological advancement in biodegradable stents | +0.7% | Global, early uptake in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of GI Cancers

Colorectal cancer incidence in Asia climbed to 23.88 per 100,000 population in 2024, overtaking stomach cancer as the dominant GI malignancy and creating sustained demand for colonic stents as bridge-to-surgery aids. Self-expandable metal stents now achieve 89.7% clinical success for malignant gastric outlet obstruction, delivering durable patency and fewer emergency surgeries.[1]Mark Gromski et al., “Endoscopic Stenting for Palliation of Intra-Abdominal Gastrointestinal Malignant Obstruction,” European Journal of Gastroenterology & Hepatology, journals.lww.comIntegration of neoadjuvant chemotherapy with stent placement optimizes tumor shrinkage and surgical outcomes, further strengthening procedure volumes. Broadening cancer screening initiatives coupled with improved survival rates sustains procedure frequency into follow-up and palliative contexts.

Ageing Population & Comorbid GI Disorders

Demographic ageing increases benign biliary strictures and pancreatitis-related complications, conditions often unsuitable for open surgery. Short fully covered metal stents resolve 99% of benign strictures in older cohorts, while lowering procedural risk and hospital stay relative to surgery.[2]Zhi Li et al., “A Short Fully Covered Self-Expandable Metal Stent for Management of Benign Biliary Stricture,” Journal of Clinical Medicine, mdpi.comEnhanced anti-migration features address fragile tissue architecture common in geriatric patients. Health systems seeking value-based care favor these minimally invasive routes, reinforcing long-term utilization across mature markets.

Shift Toward Minimally Invasive Endoscopy

Cost-effectiveness, faster recovery, and broader patient eligibility underpin the move from open surgery to endoscopic alternatives. Boston Scientific’s WallFlex and Epic platforms showcase delivery-system refinements that simplify navigation of tortuous anatomy, heightening procedural safety. Guideline-based training from the European Society of Gastrointestinal Endoscopy standardizes competencies and accelerates technology diffusion.

Rapid Adoption of EUS-Guided Stenting

EUS-guided biliary drainage yields 90% success when conventional ERCP fails, broadening options for patients with surgically altered anatomy.[3]Mohamed Abdel-Wahab et al., “The Role of Endoscopic Ultrasound in Detecting Common Bile Duct Stones,” Egyptian Journal of Internal Medicine, ejim.springeropen.com Purpose-built lumen-apposing metal stents achieve 100% technical success for pancreatic fluid collections, slashing morbidity and hospital days. Investments in simulation-based curricula shorten learning curves and hasten clinical deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related adverse events & re-interventions | −0.7% | Global, higher impact in emerging markets | Short term (≤ 2 years) |

| Stringent multi-region regulatory pathways | −0.5% | Global, affects new entrants | Medium term (2-4 years) |

| Reimbursement gaps in emerging markets | −0.9% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Nitinol supply-chain volatility & price spikes | −0.6% | Global manufacturing impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-Related Adverse Events & Re-Interventions

FDA reports list stent positioning issues (35.6%) and migration events (12.4%) as leading device complaints, with hemorrhage and perforation topping patient-related events. Migration rates can approach 40%, raising cost and patient-safety concerns. Forgotten plastic biliary stents increase cholangitis risk and clogging incidents, prompting calls for automated retrieval reminders. Next-generation anti-migration fins and biodegradable formats aim to cut secondary procedures and enhance quality metrics.

Stringent Multi-Region Regulatory Pathways

Manufacturers face divergent evidence standards across the United States, European Union, and major Asian markets, lengthening approval timelines and escalating trial costs. Harmonization efforts such as EU Medical Device Regulation (MDR) raise documentation requirements, challenging small entrants without extensive compliance infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biliary Stents Lead Clinical Applications

Biliary stents held 36.82% share of 2025 revenues in the gastrointestinal stent market, reflecting their entrenched role in malignant and benign biliary obstructions. Laser-cut geometries, hydrophilic coatings, and low-profile delivery catheters foster accurate placement in narrowed ducts and complex hilar lesions. Esophageal and duodenal stents follow in volume, benefitting from improved anti-reflux valves that enhance dysphagia relief.

Colonic stents supply the fastest 8.67% CAGR through 2031. Comparative studies show self-expandable metal stents deliver survival and quality-of-life outcomes on par with emergent surgery while avoiding colostomy formation. Pancreatic designs without internal flaps record 80.7% spontaneous migration, sparing retrieval procedures and aligning with outpatient protocols. Drug-eluting refinements now target tissue in-growth inhibition, signaling new value propositions across all product classes.

By Material: Self-Expanding Metal Dominance Challenged by Innovation

Self-expanding metal devices captured 61.05% of 2025 revenue, underlining their balance of radial strength and flexibility. Clinical trials confirm 100% technical success for ileocecal obstruction and 92.3% clinical success, validating adaptability outside the traditional left-sided colon. Advanced nitinol processing, including laser-cut micro-mesh patterns, improves conformability across tortuous anatomy.

Biodegradable and drug-eluting formats, posting an 8.41% CAGR, answer the call for temporary scaffolding without removal. Iron-based prototypes enhance mechanical reserve while enabling radiopacity tracking. Hybrid constructs bring metallic backbone reliability alongside timed degradation, promising to shift indication boundaries for benign disease management. Plastic remains relevant for short-term drainage when retrieval is planned early, preserving a niche position in the gastrointestinal stent market.

By Application: Biliary Disease Leadership Amid Colorectal Growth

Biliary disease represented 40.88% of 2025 value, supported by strong guideline endorsement and abundant physician experience. Anti-migration flares, enhanced radiopacity, and fully covered designs reduce tumor in-growth and ease subsequent interventions. Italian consensus recommendations underscore precise sizing and stent selection as outcome determinants.

Colorectal cancer indications accelerate at a 8.92% CAGR through 2031 as bridge-to-surgery protocols gain oncologic acceptance. Multidisciplinary boards integrate stents with neoadjuvant regimens, improving resection margins and lowering temporary stoma rates. Emerging research into inflammatory bowel disease strictures sparks demand for tailored diameters and softer radial force profiles, hinting at future micro-niche growth.

By End User: Hospital Dominance Challenged by Ambulatory Growth

Hospitals controlled 63.78% of 2025 spending, benefiting from anesthesiology, radiology, and critical-care backup fundamental to complex GI interventions. Integrated digital platforms link imaging, AI planning, and post-procedure tracking, reinforcing hospital centrality in high-acuity cases.

Ambulatory surgical centers advance at 7.56% CAGR, aided by slimline delivery systems and conscious-sedation protocols that shorten stays. Specialty clinics flourish in tertiary hubs, offering pancreaticobiliary expertise and high-throughput scheduling. Portable X-ray and intra-procedure ultrasound options expand point-of-care viability, though stringent patient selection remains essential for safe migration away from inpatient settings.

Geography Analysis

North America generated 35.12% of 2025 turnover, buoyed by established reimbursement pathways and deep procedural expertise. Medicare’s defined coverage for GI stenting underpins predictable payment cycles, while manufacturer-driven registries furnish real-world evidence that speeds payer updates. United States centers emphasize multidisciplinary tumor boards integrating stenting, chemotherapy, and surgery, sustaining mature demand. Canada’s universal insurance similarly ensures equitable access, fostering stable baseline volumes.

Asia-Pacific delivers the fastest 7.88% CAGR through 2031, propelled by aging demographics, growing colorectal cancer incidence, and expanded public insurance. China’s hospital upgrade program and regional CRC screening widen procedural addressability. Japan’s super-aged population mandates minimally invasive approaches, while India’s device-marketing code of conduct seeks to balance commercial incentives with ethical outreach. Reimbursement variability and price caps, however, remain decisive adoption throttles, compelling tiered product portfolios targeting affordability.

Europe displays steady mid-single-digit growth underpinned by harmonized MDR frameworks and robust clinical networks. ESGE-standardized training expands operator proficiency, while cross-border data sharing accelerates technology assessment cycles. Latin America and Middle East & Africa constitute emerging arenas; infrastructure expansion and private-sector hospital investment create runway for advanced endoscopy, yet currency volatility and fragmented insurance dampen immediate penetration.

Competitive Landscape

Market structure skews toward moderate concentration, with Boston Scientific, Cook Medical, and Olympus leveraging broad GI portfolios, extensive service networks, and acquisition-driven scale. Boston Scientific’s USD 1.26 billion Silk Road Medical deal expands neurovascular crossover know-how into GI delivery-system innovations. Teleflex’s €760 million purchase of Biotronik’s vascular unit signals intent to deepen material science capabilities and adjacent access technology.

Innovation wars dominate strategic focus. Merit Medical’s WRAPSODY cell-impermeable endoprosthesis achieved 70.1% patency versus 41.6% standard of care, underlining performance-driven product differentiation. Start-ups commercializing 3D-printed personalized stents promise anatomically exact flare diameters and optimized radial force, though scalability and regulatory evidence remain hurdles.

Supply security and price pressures spur vertical collaboration. OEMs cultivate secondary nitinol sources and adopt laser sintering to internalize component builds, buffering geopolitical supply shocks. Digital service layers—cloud-based planning software, remote proctoring, and AI-driven sizing engines—emerge as stickiness levers, complementing hardware margins and entrenching vendor–provider ecosystems within the gastrointestinal stent industry.

Gastrointestinal Stent Industry Leaders

Boston Scientific Corporation

Becton Dickinson and Company

Cook Medical

Abbott

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: SafeGuard Surgical received FDA breakthrough designation for its LeakGuard biodegradable stent.

- January 2024: Olympus completed the acquisition of Taewoong Medical, adding metallic GI stents to its EndoTherapy line.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the gastrointestinal stent market as the worldwide revenue generated from new, single-use tubular devices placed endoscopically or fluoroscopically to reopen blocked sections of the esophagus, stomach, duodenum, biliary tree, colon, or pancreas.

Scope exclusion: We do not cover vascular, airway, or urological stents.

Segmentation Overview

- By Product Type

- Biliary Stent

- Esophageal Stent

- Duodenal Stent

- Colonic Stent

- Pancreatic Stent

- By Material

- Self-Expanding Metal Stent (SEMS)

- Plastic Stent

- Biodegradable / Drug-eluting Stent

- By Application

- Biliary Disease

- Colorectal Cancer

- Stomach Cancer

- Inflammatory Bowel Disease

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed gastroenterologists, interventional radiologists, supply-chain managers, and regional distributors across North America, Europe, and Asia-Pacific. Their feedback on stent length preferences, metal-to-plastic conversions, and reimbursement hurdles allowed us to refine adoption rates and challenge desk assumptions.

Desk Research

Our analysts first mapped the demand landscape using open datasets from the World Health Organization, the National Cancer Institute, the Centers for Disease Control and Prevention, and the European Society of Gastrointestinal Endoscopy, which together detail cancer incidence, treatment rates, and device approvals. We reinforced these figures with customs shipment logs on Volza, FDA PMA filings, and procedure statistics released by large public hospitals.

Next, company 10-Ks, investor presentations, clinical papers, and price lists helped us capture average selling prices and material shifts. Paid platforms such as D&B Hoovers supplied revenue splits for privately held suppliers, tightening our value estimates. The sources listed illustrate the breadth of work; many additional publications and databases were also reviewed.

Market-Sizing & Forecasting

We began our model with a top-down reconstruction that links diagnosed obstruction cases to procedure penetration, multiplies by typical stents per patient, and adjusts for regional reimbursement ceilings before translating units into revenue. Select bottom-up checks, including manufacturer shipment samples, channel inventory audits, and clinic stocking patterns, validated the totals, and this is where Mordor Intelligence differentiates itself. Core variables include cancer incidence trends, elective versus palliative case mix, metal price spreads, re-intervention rates, and import tariffs. Five-year forecasts rely on ARIMA time-series models enriched with scenario weights agreed upon by clinical experts.

Data Validation & Update Cycle

We layer anomaly checks, peer reviews, and variance triggers onto every draft; only when all flags clear do we sign off. Reports refresh annually, with interim updates when regulations, major recalls, or mergers materially shift the market.

Why Our Gastrointestinal Stent Baseline Inspires Confidence

Published estimates often diverge because each publisher chooses different base years, device mixes, and inflation converters.

By anchoring our 2025 figure to live hospital usage data and refreshing every twelve months, Mordor Intelligence delivers a dependable reference point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 587.8 M (2025) | Mordor Intelligence | - |

| USD 457 M (2021) | Global Consultancy A | Older base year, excludes plastic variants |

| USD 429 M (2023) | Industry Journal B | Manufacturer revenue only, limited country set |

| USD 465.2 M (2022) | Research Publisher C | Uses list prices, no channel discounts |

These comparisons show that our disciplined scope selection, timely data checks, and transparent calculations give decision-makers a clear, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the gastrointestinal stent market?

The market generated USD 617.84 million in 2026 and is forecast to climb to USD 792.64 million by 2031 at a 5.11% CAGR.

Which product category holds the largest share?

Biliary stents lead with 36.82% revenue share due to their central role in managing malignant and benign biliary obstructions.

Why are biodegradable stents gaining traction?

Biodegradable designs eliminate retrieval procedures, reduce long-term adverse events, and are projected to grow at an 8.41% CAGR, the fastest among material

Which region is expanding the fastest?

Asia-Pacific shows the highest 7.88% CAGR, driven by rising colorectal cancer incidence, healthcare infrastructure upgrades, and broader insurance coverage.

What are the main clinical drivers for market growth?

Key growth factors include increasing GI cancer prevalence, ageing populations with comorbidities, rapid uptake of EUS-guided techniques, and ongoing shifts toward minimally invasive endoscopy.

Page last updated on: