Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 64.71 Billion |

| Market Size (2031) | USD 81.29 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

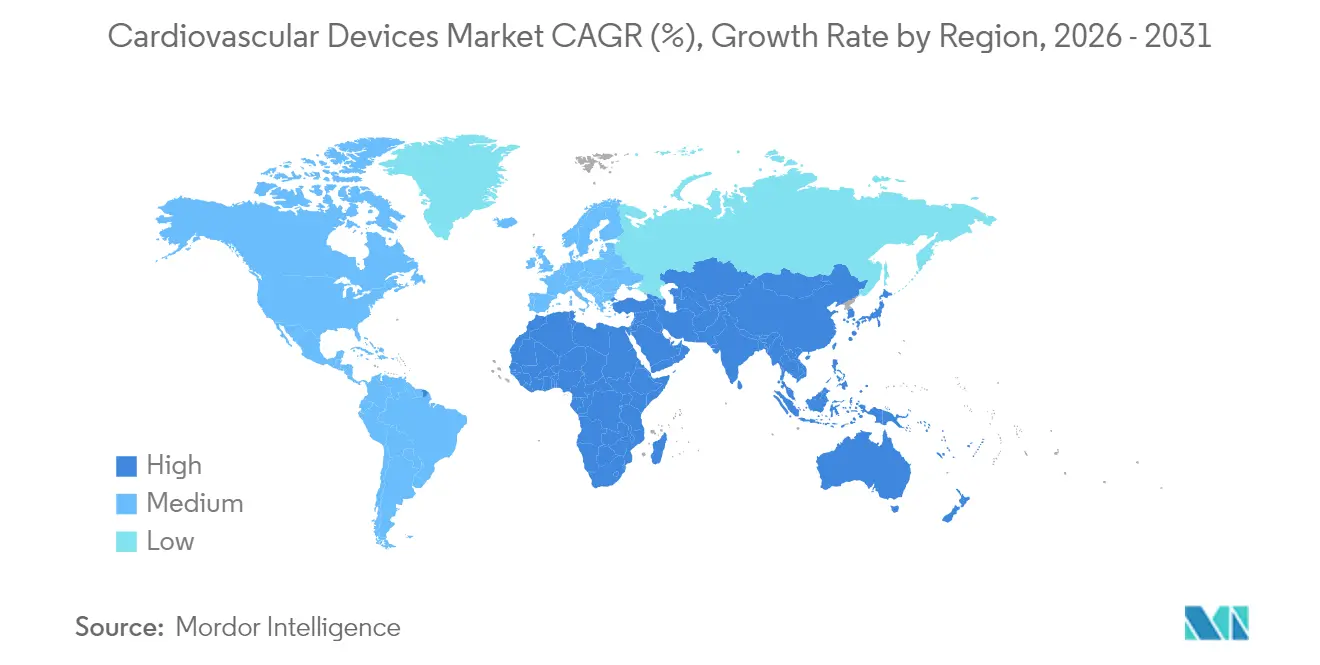

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

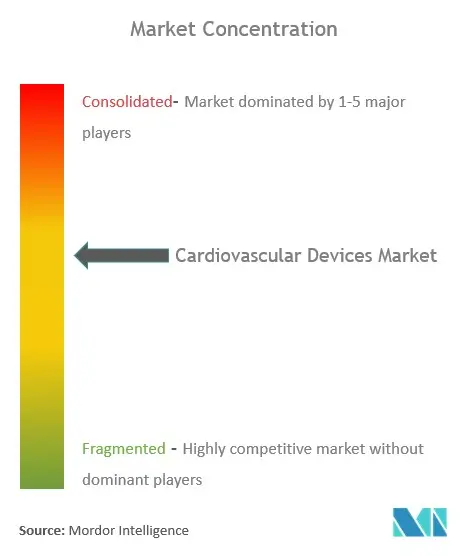

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiovascular Devices Market Analysis by Mordor Intelligence

The Cardiovascular Devices Market size was valued at USD 61.82 billion in 2025 and estimated to grow from USD 64.71 billion in 2026 to reach USD 81.29 billion by 2031, at a CAGR of 4.67% during the forecast period (2026-2031).

Demand accelerates as artificial intelligence enhances device functionality, making early detection more reliable and facilitating targeted therapies. The prevalence of minimally invasive procedures continues to grow, supported by expanded indications for transcatheter valve replacement and the increasing role of ambulatory surgical centers (ASCs). Strategic acquisitions among leading manufacturers are streamlining end-to-end treatment portfolios, while new FDA clearances for leadless pacemakers and renal denervation systems open fresh avenues for underserved patient groups. Heightened regulatory scrutiny and the high cost of advanced technology, however, remain barriers to adoption in price-sensitive regions.

Key Report Takeaways

- By device type, diagnostic and monitoring devices held 71.62% of the cardiovascular devices market share in 2025, whereas therapeutic devices posted the fastest segment CAGR at 6.74% through 2031.

- By application, coronary artery disease commanded 44.55% of the cardiovascular devices market size in 2025; structural heart disease is projected to expand at 7.42% CAGR to 2031.

- By end-user, hospitals and cardiac centers led with 58.67% revenue share in 2025, while ASCs logged the highest expected CAGR at 9.41% between 2026 and 2031.

- By geography, North America accounted for 44.78% of the cardiovascular devices market in 2025; Asia-Pacific is advancing at an 8.44% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased preference for minimally invasive procedures | 1.90% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Increasing burden of cardiovascular diseases | 1.60% | Global, highest in Asia-Pacific | Long term (≥ 4 years) |

| Rapid technological advancements | 1.40% | United States, Europe, Japan | Medium term (2-4 years) |

| Integration of AI-enabled diagnostic algorithms | 1.30% | United States, European Union | Medium term (2-4 years) |

| Proliferation of remote cardiac-monitoring reimbursement codes (CMS-2023) | 1.20% | United States | Short term (≤ 2 years) |

| China’s volume-based procurement for coronary stents | 0.90% | China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Minimally Invasive Procedures

Minimally invasive techniques are reshaping cardiovascular care by lowering complication rates and shortening hospital stays. Transcatheter tricuspid valve repair expanded market volume by more than 50% since Q2 2024. At the same time, pulsed-field ablation systems from Medtronic and Boston Scientific received FDA approvals during 2023-2024, bringing a safer approach to atrial fibrillation treatment. Investor interest mirrors these clinical shifts, as reflected in 342 cardiology clinic acquisitions from 2021 through September 2023. Johnson & Johnson’s USD 13.1 billion purchase of Shockwave Medical underscores confidence in intravascular lithotripsy, already used in 400,000 procedures worldwide [1]Source: Johnson & Johnson, “Johnson & Johnson to Acquire Shockwave Medical,” jnjmedtech.com.

Increasing Burden of Cardiovascular Diseases

Heart and circulatory diseases cause 170,000 deaths a year in the United Kingdom and affect 7.6 million people, adding urgency to advanced diagnostics [2]Source: British Heart Foundation, “Facts and Figures,” bhf.org.uk. Direct costs are steep in Asia-Pacific, reaching USD 21.7 billion in China alone. Eighty percent of disease burden links to modifiable risk factors, heightening interest in early-warning devices. Multimorbidity—diabetes coupled with cardiovascular conditions—accelerates mortality, making integrated solutions indispensable Journal of Clinical Medicine.

Rapid Technological Advancements

Breakthrough products illustrate the pace of innovation. Abbott’s AVEIR DR, the first dual-chamber leadless pacemaker, gained CE Mark in June 2024 with 98.3% implant success and >97% atrio-ventricular synchrony. Edwards Lifesciences’ SAPIEN M3 became the initial transcatheter mitral valve replacement to secure CE Mark in April 2025, widening options for inoperable patients. Both advances support sustained growth in the cardiovascular devices market.

Integration of AI-Enabled Diagnostic Algorithms

Artificial intelligence now augments electrocardiogram interpretation, identifying subtle waveform patterns that precede detectable symptoms. AI-enhanced ECG can spot left-ventricular dysfunction at an AUC of 0.95, far surpassing traditional thresholds. Medtronic’s AccuRhythm AI algorithms have cut false atrial fibrillation alerts by 88.2%, while preserving up to 100% of genuine alerts. FDA-cleared models like Implicity’s SignalHF give clinicians a two-week heads-up on heart-failure deterioration, enabling timely intervention. Together, these advances spur further demand in the cardiovascular devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory policies and product recalls | −1.1% | Europe, United States | Medium term (2-4 years) |

| High cost of instruments and procedures | −1.0% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Shortage of heparin-coated raw materials due to swine fever in China | −0.8% | China; global stent supply chain | Short term (≤ 2 years) |

| Reimbursement cap on TAVR implants by Indian NPPA | −0.7% | India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Policies and Product Recalls

Europe’s Medical Device Regulation raised evidence standards, raising costs for mid-sized manufacturers European Heart Journal. A comparative analysis found 3- to 7-year delays between CE Mark and FDA approval for many devices, with only 7 of 27 products earning dual clearances. While these rules improve safety, they slow market entry and could reduce short-term device availability, tempering growth in the cardiovascular devices market.

High Cost of Instruments and Procedures

In Canada, transcatheter aortic valve implantation (TAVI) outlays exceeded surgical replacement costs but proved cost-effective once reduced ICU and complication costs were considered. In the United States, peripheral vascular disease admissions averaged USD 33,700 per discharge, and heart-failure admissions totaled USD 19.5 billion annually. Such expenses hamper adoption in cost-sensitive settings, especially where reimbursement is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostic Dominance and Rising Therapeutics

Diagnostic and monitoring products led with 71.62% of the cardiovascular devices market share in 2025, underscoring the importance of early screening for risk management. Continuous ECG platforms, such as the BodyGuardian MINI, provide up to 15 days of Holter data, enriched by BeatLogic AI that refines rhythm classification. Vivalink’s water-resistant wearable extends monitoring to 30 days, adding comfort for long-term observation. Artificial intelligence boosts diagnostic accuracy further, as CarDS-Plus can interpret single-lead smartwatch ECGs in roughly 35 seconds, creating actionable.

Therapeutic categories are advancing quickly. Leadless pacemakers limit infection risks linked to transvenous leads, and dual-chamber models like AVEIR DR now synchronize atrio-ventricular pacing. Breakthrough devices, including Abbott’s dissolving stent for below-knee arteries, address chronic limb-threatening ischemia, expanding the cardiovascular devices market. AI-guided cardiac ablation posted 88% arrhythmia-free survival at 12 months versus 70% for pulmonary-vein-isolation alone, highlighting potential for superior outcomes. The cardiovascular devices market size attributed to advanced therapeutics is set to climb alongside these innovations.

By Application: Structural Heart Disease Gains Momentum

Coronary artery disease remained dominant at 44.55% of the cardiovascular devices market in 2025. Interventions such as intravascular lithotripsy widen treatment to severely calcified lesions. Yet structural heart applications are growing fastest at 7.42% CAGR, propelled by transcatheter mitral and tricuspid repair. Edwards Lifesciences’ SAPIEN M3 offers catheter-based mitral replacement for high-risk patients, while ongoing TAVR studies show expanded safety for low-risk cohorts.

Heart-failure technologies add to momentum. Johnson & Johnson’s acquisition of V-Wave highlighted the USD 1.7 billion potential for shunt systems alleviating pulmonary congestion. Hypertension therapies progressed in November 2023 when Medtronic’s Symplicity Spyral won FDA approval, cementing renal denervation as a viable option for drug-resistant hypertension. The cardiovascular devices market size for renal denervation is poised for multi-year double-digit expansion under these dynamics.

By End-User: ASCs Accelerate Service Shift

Hospitals and cardiac centers held 58.67% of 2025 revenue, retaining complex case referrals and advanced imaging infrastructure. Nonetheless, ASCs are growing fastest at 9.41% CAGR thanks to cost savings and shorter stays. Medicare payments to ASCs rose 2.6% in 2024, encouraging site neutrality and bringing cardiovascular interventions into community settings. Analyst projections show the U.S. ASC market climbing toward USD 59 billion by 2028, with procedure volumes set to climb 25% this decade.

Remote-care models follow the same decentralization trend. Endotronix’s Cordella pulmonary-artery sensor enables proactive heart-failure management at home, combining invasive pressure readings with non-invasive vitals. Such technology blurs traditional site boundaries, promising volume growth beyond hospital walls. Each shift supports sustained expansion in the cardiovascular devices market.

Geography Analysis

North America anchored 44.78% of the cardiovascular devices market in 2025, leveraging high per-capita healthcare spending and broad insurance coverage. Medicare reimbursement for ASCs reached USD 6.1 billion in 2022, illustrating public-payer traction for outpatient care medpac.gov. Robust regulatory frameworks allow rapid adoption of AI-enabled devices, as shown by multiple FDA clearances for leadless pacemakers and ablation systems during 2024. Supply-side strength stems from R&D hubs in Minnesota, California, and Massachusetts, where device firms co-locate with research universities.

Europe ranks second in revenue, supported by a tradition of clinical innovation. The European MDR’s stricter scrutiny, however, may defer approvals and tighten post-market surveillance, temporarily constraining supply. Even so, CE Mark nods for the AVEIR DR pacemaker and M3 mitral valve system confirm continued innovation under the new rules abbott.mediaroom.com. Adoption of pulsed-field ablation and intravascular lithotripsy further underlines regional commitment to minimally invasive care.

Asia-Pacific is the fastest-growing region at an 8.44% CAGR through 2031. Aging populations and rising lifestyle-related risk factors create a large patient pool, with China alone counting 290 million cardiovascular disease patients biospectrumasia.com. Public-private partnerships improve infrastructure, and policy initiatives in India and China encourage domestic manufacturing. Despite heterogeneous regulatory pathways, local firms collaborate with global leaders for technology transfers, accelerating acceptance of novel implants. Collectively, these elements build momentum for the cardiovascular devices market across diverse economies.

Competitive Landscape

Moderate concentration prevails, with Medtronic, Abbott, Boston Scientific, Edwards Lifesciences, and Johnson & Johnson accounting for the majority of global sales. Johnson & Johnson’s USD 13.1 billion purchase of Shockwave Medical in April 2024 boosts its technology in intravascular lithotripsy, while the subsequent V-Wave acquisition deepens exposure to heart-failure therapy. Boston Scientific broadened its intravascular lithotripsy reach by taking over Bolt Medical for up to USD 664 million in January 2025.

Product pipelines show parallel advancement. Medtronic’s AccuRhythm AI reduced false implantable monitor alerts by up to 88.2%, improving clinician efficiency. Abbott’s software-guided balloon-expandable TAVI integrates procedural algorithms that enhance valve deployment accuracy. Edwards Lifesciences focuses on next-generation transcatheter systems, aiming to capture incremental growth in mitral and tricuspid repair.

Partnerships with digital-health startups extend analytics capabilities. Medtronic collaborates with AI firms for arrhythmia prediction, and Boston Scientific invests in cloud-based rhythm-management platforms. These strategies target improved outcomes and lower readmission rates, supporting sustained demand across the cardiovascular devices market.

Portfolio Orchestration: Beyond Simple Scale vs. Specialization

The cardiovascular market is seeing a shift in how companies position themselves—moving past the old choice between being either big or specialized. The most successful players in the cardiovascular devices market are building strategic networks of complementary products that strengthen their main value offerings. This approach is clear in partnerships like the one between UK-based Anumana and Mayo Clinic, which led to FDA clearance for their ECG-AI LEF device that detects potential heart failure. These collaborations let companies access specialized expertise without having to develop everything in-house. Within the Therapeutic and Surgical Devices segment, which makes up 75.3% of the market, companies now focus on creating interconnected product systems rather than standalone devices. They recognize that winning now depends on offering complete solutions rather than just individual product features. This strategy works particularly well in North America, which represents about 51.1% of the global cardiovascular device market, where healthcare providers increasingly prefer vendors that offer comprehensive, compatible solutions.

Regulatory Capital: Turning Compliance into Competitive Advantage

Smart companies in the cardiovascular devices sector are transforming their regulatory capabilities from basic compliance functions into strategic assets that create real competitive advantages. The ability to navigate complex regulations efficiently has become a valuable skill that affects product launch timing, costs, and market position. Companies with strong regulatory expertise gain 6-12 month advantages in bringing products to market, especially noticeable in the interventional cardiology devices market where being first translates directly to market share. Anumana's successful FDA 510(k) clearance for its ECG-AI LEF device with the Mayo Clinic shows how regulatory milestones have become key events that investors and analysts watch closely. This expertise is particularly valuable in the growing Asia-Pacific region, where companies must navigate different regulations across multiple countries. Firms that invest in regulatory knowledge, maintain good relationships with regulatory authorities, and include regulatory planning early in product development are creating advantages that competitors struggle to match without significant time investment.

Cardiovascular Devices Industry Leaders

Boston Scientific Corporation

Abbott

Medtronic

Edwards Lifesciences Corporation

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Boston Scientific entered the intravascular lithotripsy arms race by acquiring Bolt Medical for up to USD 664 million

- October 2024: Medtronic received FDA clearance for the Affera Mapping and Ablation System with dual-energy capabilities for atrial fibrillation

- October 2024: Johnson & Johnson finalized its V-Wave acquisition, potentially worth USD 1.7 billion

- September 2024: Johnson & Johnson rebranded its cardiovascular subsidiaries under Johnson & Johnson MedTech

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cardiovascular devices market as the value of new diagnostic, monitoring, therapeutic, and surgical hardware, including electrocardiographs, mobile telemetry units, stents, catheters, heart valves, pacemakers, ventricular assist devices, and related capital equipment, sold to detect, repair, or sustain cardiac function across hospital, ambulatory, specialty-clinic, and regulated home-care settings.

Scope Exclusions: implantable biosensors, single-use disposables, and stand-alone cardiology software platforms are outside the frame.

Segmentation Overview

- By Device Type

- Diagnostic and Monitoring Devices

- Electrocardiogram (ECG)

- Remote Cardiac Monitoring

- Other Diagnostic and Monitoring Devices

- Therapeutic and Surgical Devices

- Cardiac Assist Devices

- Cardiac Rhythm Management Devices

- Catheters

- Grafts

- Heart Valves

- Stents

- Other Therapeutic and Surgical Devices

- Diagnostic and Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia

- Heart Failure

- Structural Heart Disease

- Hypertension

- Others

- By End-User

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Home-Care Settings

- Specialty Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview cardiologists, biomedical engineers, procurement heads, and regional distributors in North America, Europe, Asia-Pacific, and the Gulf to fine-tune typical selling prices, utilization patterns, and technology adoption curves, ensuring assumptions mirror on-ground realities.

Desk Research

Mordor analysts first map the universe through open datasets such as WHO mortality dashboards, OECD Health Statistics, Eurostat production files, U.S. FDA 510(k) clearances, and AdvaMed or Eucomed yearbooks. Company 10-Ks, clinical-trial registries, customs shipment logs, and reputable press deepen price and volume insight, while paid libraries like D&B Hoovers and Dow Jones Factiva add financial color. The sources cited illustrate the breadth; many additional references inform our desk work.

Market-Sizing & Forecasting

A top-down construct scales global procedure volumes and implant penetration rates to expenditure pools, which are then balanced with selective bottom-up supplier revenue rolls and sampled ASP × unit checks. Key drivers, including aging population share, elective-surgery backlog clearance, median stent pricing, fast-track approvals, and hospital capital budgets, feed a multivariate regression that projects demand; scenario analysis cushions sudden reimbursement or guideline shifts. Channel checks and import proxies bridge gaps where supplier splits remain opaque.

Data Validation & Update Cycle

Outputs pass variance scans against historical sales, trade data, and independent signals. Senior reviewers sign off only after anomalies are resolved. Reports refresh annually, with interim revisions when major recalls, regulatory shifts, or landmark trials materially move the market.

Why Mordor's Cardiovascular Devices Baseline Stands Firm

Published estimates often diverge because firms apply dissimilar device baskets, exchange rates, and update speeds.

Key gap drivers include narrower therapeutic scope, aggressive uptake assumptions for emerging technologies, or reliance on unverified price curves. By anchoring every variable to transparent sources and dual-track validation, Mordor Intelligence delivers steadier baselines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 61.82 B (2025) | Mordor Intelligence | - |

| USD 77.71 B (2024) | Global Consultancy A | Includes software platforms and maintenance revenue; assumes uniform five-year replacement cycle |

| USD 57.60 B (2025) | Industry Portal B | Excludes cardiac assist devices; uses list prices without regional discounts |

| USD 65.53 B (2024) | Trade Journal C | Linear extrapolation of 2020-23 sales; procedure volumes unchecked |

Taken together, the comparison shows that when scope clarity, pricing realism, and refresh cadence are harmonized, Mordor's disciplined approach offers decision-makers the most dependable reference point.

Key Questions Answered in the Report

How big is the Cardiovascular Devices Market?

The Cardiovascular Devices Market size is expected to reach USD 64.71 billion in 2026 and grow at a CAGR of 4.67% to reach USD 81.29 billion by 2031.

Which device category holds the largest share today?

Diagnostic and monitoring devices account for 71.62% of 2025 revenue, driven by broad adoption of AI-enabled ECG and remote monitoring solutions.

Why are structural heart devices attracting attention?

Structural heart disease shows the fastest application growth at 7.42% CAGR thanks to transcatheter valve innovations such as Edwards Lifesciences’ SAPIEN M3.

How are ambulatory surgical centers influencing market dynamics?

ASCs offer lower procedure costs and shorter recovery times, resulting in a 9.41% CAGR that outpaces hospital volumes and supports outpatient expansion.

What regions will lead future growth?

North America maintains the largest share at 44.78%, but Asia-Pacific posts the highest growth rate at 8.44% CAGR, fueled by rising disease prevalence and healthcare investment.

How important is artificial intelligence in this market?

AI dramatically improves diagnostic accuracy, reduces false alerts, and enables earlier intervention, making it a critical driver of future device adoption worldwide.

Page last updated on: