Pediatric Interventional Cardiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 9.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

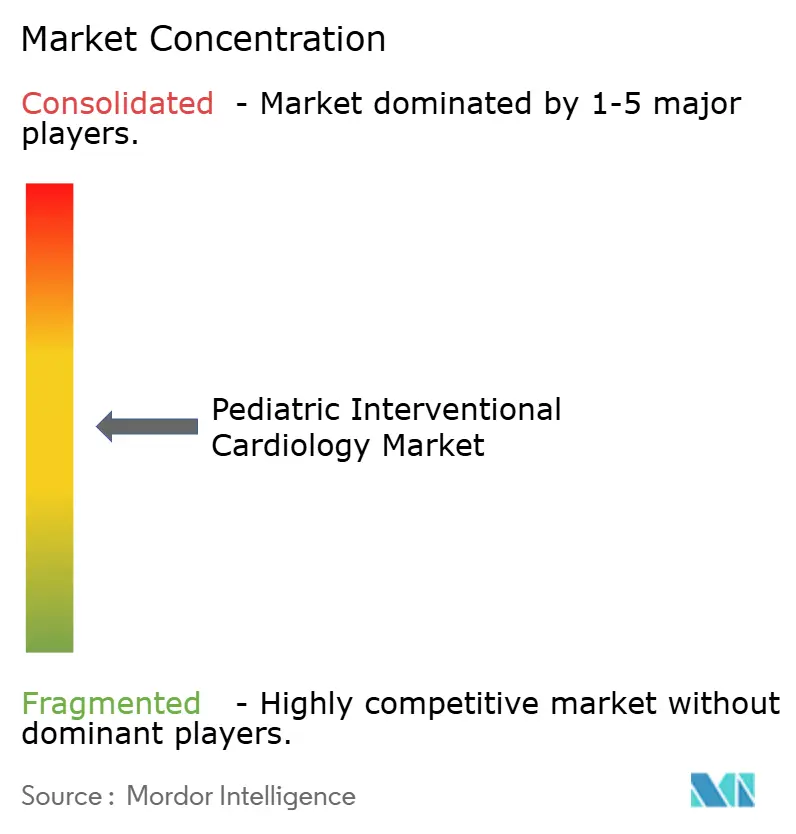

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Interventional Cardiology Market Analysis by Mordor Intelligence

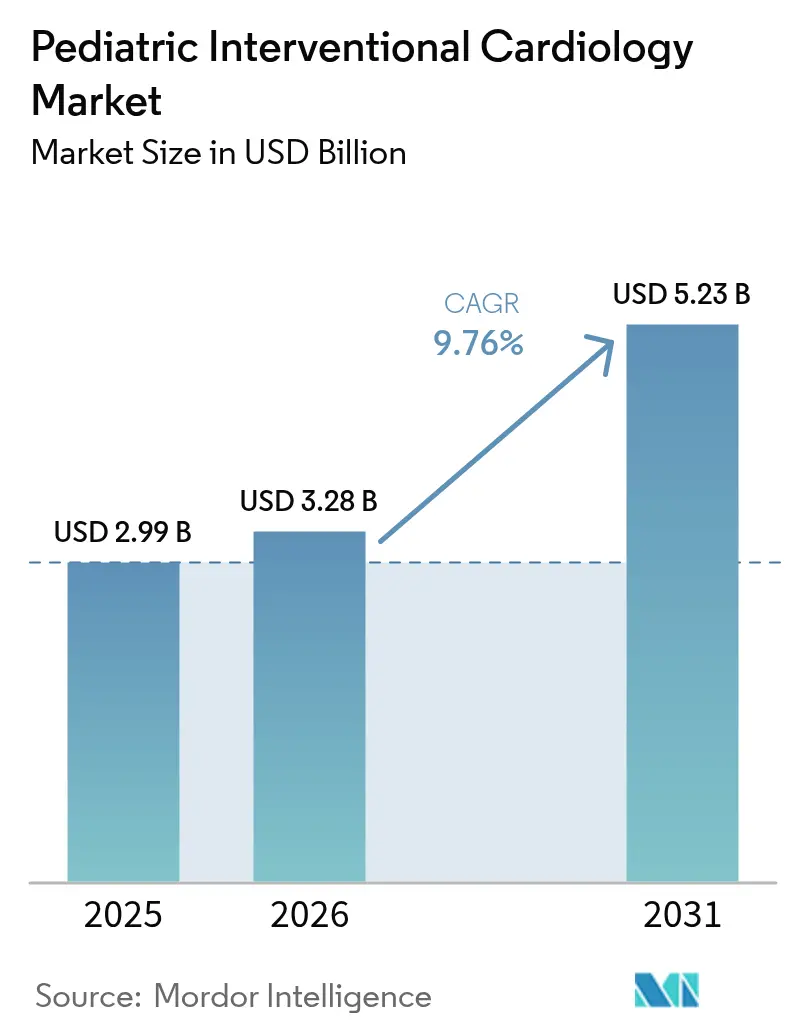

The Pediatric Interventional Cardiology market size is expected to grow from USD 2.99 billion in 2025 to USD 3.28 billion in 2026 and is forecast to reach USD 5.23 billion by 2031 at 9.76% CAGR over 2026-2031.

Rapid acceptance of minimally invasive techniques for congenital heart defect (CHD) management, steady regulatory approvals, and the shift toward AI-enhanced imaging are propelling growth. North America remains the largest regional base, yet Asia-Pacific is expanding fastest as hospitals acquire hybrid cath-lab suites and local manufacturers introduce lower-cost pediatric devices. Clinical demand is reinforced by rising CHD prevalence estimated at 1.95% of all births in new U.S. insurance datasets and by a continuing move from episodic surgery to lifelong catheter-based care models. Breakthrough products such as the FDA-cleared Minima Stent System, designed to expand with the child, signal a new era of size-appropriate implants. AI-powered cath-lab software that detects rheumatic heart disease with 90% accuracy further boosts procedural confidence.

Key Report Takeaways

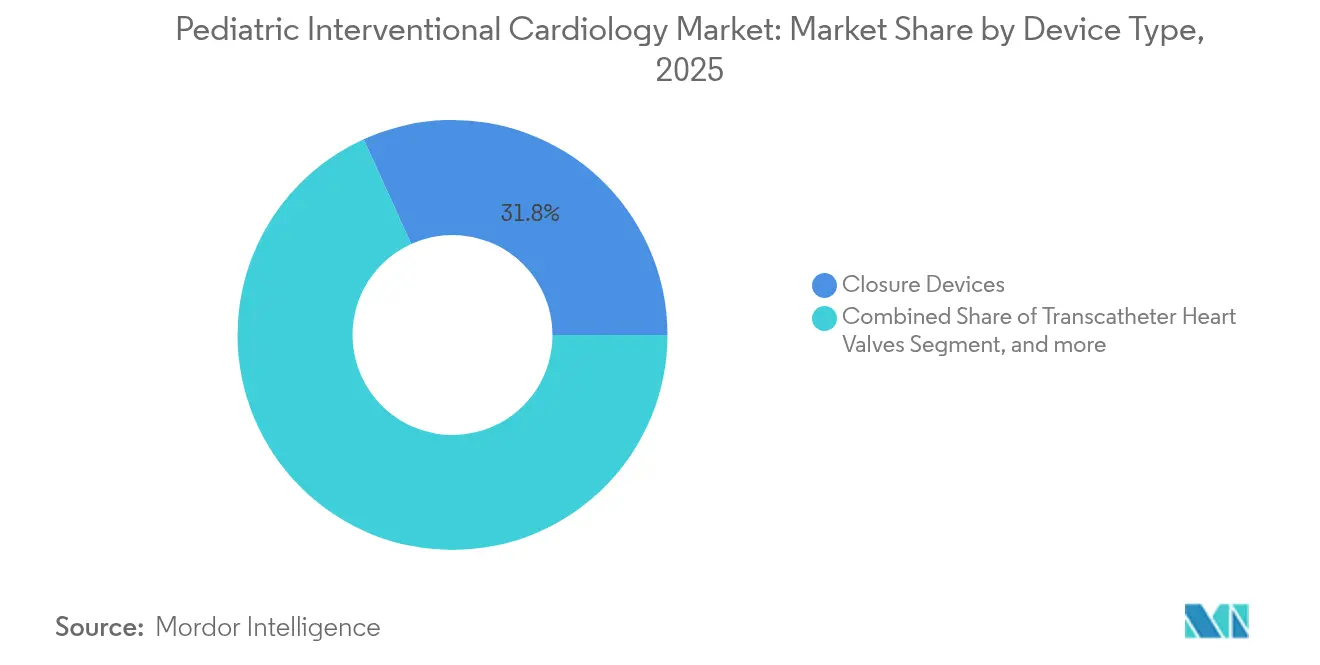

- By device type, closure devices led with 31.78% of pediatric interventional cardiology market share in 2025, while transcatheter heart valves are forecast to rise at a 13.75% CAGR through 2031.

- By procedure, congenital defect correction accounted for 27.35% of 2025 procedures, whereas catheter-based valve implantation is projected to expand at a 14.62% CAGR to 2031.

- By end user, children’s hospitals held 43.64% revenue share in 2025; ambulatory surgical centers are advancing at an 11.08% CAGR through 2031.

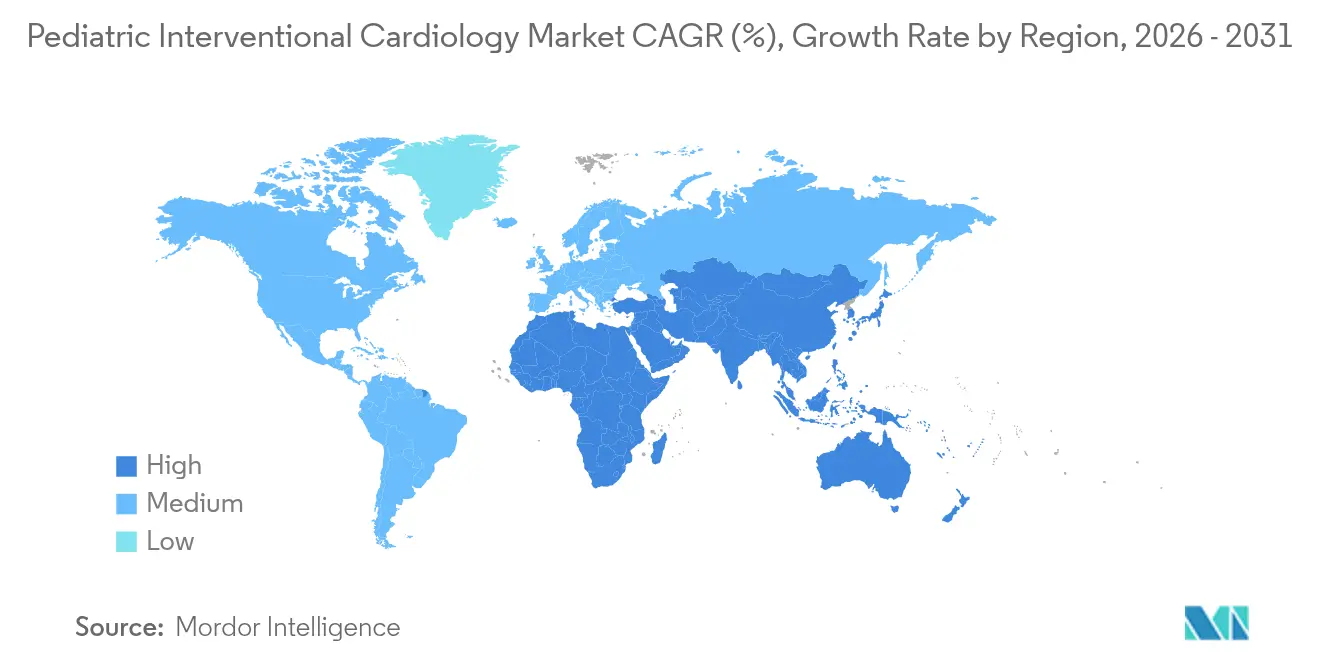

- By geography, North America dominated with 41.20% share in 2025, but Asia-Pacific is set to grow at a 12.31% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Interventional Cardiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Congenital Heart Diseases (CHDs) | +2.1% | Global, with higher rates in developing countries | Long term (≥ 4 years) |

| Advancements in Miniaturized Interventional Devices | +1.8% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Expanding R&D Pipeline for Pediatric-Specific Implants | +1.4% | Global, concentrated in major medical device hubs | Medium term (2-4 years) |

| Regulatory Incentives and Support Programs | +1.3% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Venture Capital Investment in Pediatric Med-Tech Startups | +1.1% | North America & EU primarily, emerging in APAC | Short term (≤ 2 years) |

| Integration of AI in Cath-Lab Imaging | +1.2% | North America & EU early adoption, global expansion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Congenital Heart Diseases

Newborn screening and insurance databases show CHD prevalence nearing 2% of pediatric populations, far higher than historic estimates. Enhanced prenatal echocardiography and dual-index pulse-oximetry programs have lifted early-detection sensitivity to 100% in Shanghai pilots.[1]MDPI, “Dual-Index Screening for Critical Congenital Heart Disease,” mdpi.com Earlier diagnosis extends survival, creating larger cohorts of adolescents and adults who continue to require catheter-based interventions across their lifespans.

Advancements in Miniaturized Interventional Devices

Advances in materials and engineering have cut device diameters to as little as 1.6 mm, exemplified by Medtronic’s 4.7 French OmniaSecure ICD lead, which demonstrated 100% defibrillation success in trials. The balloon-expandable Minima Stent adapts to vessel growth, achieving 97.6% procedural success without major adverse events. Absorbable metal stents and RESILIA tissue valves, which showed 99.3% freedom from deterioration at eight years, aim to minimize re-intervention risk. Such technology directly targets historic shortages of child-sized hardware.

Expanding R&D Pipeline for Pediatric-Specific Implants

Grant funding and FDA Pediatric Device Consortia programs are accelerating device concepts tailored for children. Children’s National and Additional Ventures awarded USD 300,000 for remote monitoring prototypes and mini sensors. Trials such as COMPASS, which evaluates shunt versus stent approaches for pulmonary blood-flow augmentation, are redefining long-term palliation strategies.[2]PubMed, “COMPASS Trial Protocol—Pulmonary Blood Flow Augmentation,” pubmed.ncbi.nlm.nih.gov 3D-printed auxetic stents and modified vascular plugs further widen the innovation funnel.

Regulatory Incentives and Support Programs

Regulators are actively carving pediatric pathways: the FDA’s Breakthrough Devices Program fast-tracked the Tendyne transcatheter mitral valve for severe calcification cases, clearing it in 2025.[3]Center for Devices and Radiological Health, “Minima Stent System Premarket Approval,” fda.gov Europe’s Medical Device Regulation embeds orphan-device provisions, while Japan’s Pharmaceuticals and Medical Devices Agency grants conditional approvals tied to post-market registries, collectively lowering time to market for child-focused tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedural and Device Costs | -1.9% | Global, Acute in Emerging Markets | Long term (≥ 4 years) |

| Workforce Shortages | -1.3% | Global, Critical in Rural Zones | Long term (≥ 4 years) |

| Reimbursement Hurdles | -1.5% | APAC, MEA, South America | Long term (≥ 4 years) |

| Limited Pediatric-sized Inventory | -1.4% | Global, more Severe in Developing Areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Procedures and Devices

Hospital expenditures for CHD care surpass USD 9.8 billion annually in the United States. Pregnancy costs for women with CHD average USD 24,290 per case, a material burden versus routine obstetrics. Although CMS boosted 2025 CT angiography payments from USD 178.02 to USD 357.13, out-of-pocket exposure in emerging economies remains high, slowing adoption.

Shortage of Trained Pediatric Interventional Cardiologists

Only 1,553 pediatric cardiologists practice in the United States, and the specialty’s average age is 59 years, portending an 8,650-physician deficit by 2037. Fellowship seats in pediatric cardiac intensive care historically fill at 50%, and gender disparities persist with women occupying just one-third of roles. Such scarcity limits cath-lab throughput and delays care in rural regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Closure Devices Lead While Valve Technologies Accelerate

Closure devices captured 31.78% of pediatric interventional cardiology market share in 2025 thanks to their versatility in sealing atrial and ventricular septal defects. Their usage underpins a sizeable slice of pediatric interventional cardiology market volume, buoyed by products such as the Occlutech Atrial Flow Regulator, which posted 100% implant success. Balloon catheters keep evolving toward 1.2 mm profiles that cross tight lesions with faster deflation, while next-generation atherectomy tools remove calcium with minimal vessel trauma.

Transcatheter heart valves represent the fastest-growing segment, climbing at a 13.75% CAGR. Devices including Edwards’ EVOQUE tricuspid valve and Abbott’s Tendyne system now address regurgitation and calcification without sternotomy, expanding the pediatric interventional cardiology market size for valve solutions by double digits. Absorbable metal stents aim to obviate future re-interventions as children grow, and imaging consoles integrating AI and MRI guidance are cutting radiation exposure to zero for eligible cases. Collectively, these advances draw new hospitals and ambulatory centers into complex structural heart programs.

By Procedure: Congenital Defect Correction Dominates as Valve Interventions Surge

Congenital defect corrections contributed 27.35% of 2025 procedural volume, securing the biggest slice of the pediatric interventional cardiology market. Simple occlusions of patent ductus arteriosus coexist with intricate single-ventricle palliation, and the COMPASS trial’s findings on stent-based pulmonary flow augmentation may further cement catheter dominance for neonatal circulation support.

Catheter-based valve implantation, however, is advancing most rapidly at a 14.62% CAGR, adding meaningful incremental revenue to the pediatric interventional cardiology market size. Early mitral, tricuspid, and pulmonary devices have shown procedural success above 90%. Coronary thrombectomy technology, including milli-scale spinner robots, lifts reperfusion rates to 90%, whereas hybrid surgery-assisted palliation records zero surgical mortality in resource-limited settings. The pipeline is broadening to include radiation-free MRI-guided niche interventions that appeal to parents and payers alike.

By End User: Children’s Hospitals Dominate While ASCs Gain Momentum

Children’s hospitals held 43.64% revenue owing to multidisciplinary teams, advanced imaging, and pediatric-specific anesthesia protocols. Their commanding position anchors the pediatric interventional cardiology market, reinforced by alliances such as UW Health Kids and Children’s Wisconsin, which pool faculty expertise and training resources.

Ambulatory surgical centers (ASCs), growing at 11.08% CAGR, are shifting less complex cases into the outpatient sphere. Same-day discharge is rising as closure device puncture sizes fall and vascular sealants shorten recovery, spreading the pediatric interventional cardiology market footprint across community facilities. Academic institutes continue to earn NIH and charity grants for first-in-child devices, acting as the early-adopter test bed before wider commercial rollout.

Geography Analysis

North America accounted for 41.20% of 2025 revenue, propelled by FDA leadership in clearing pediatric devices, mature reimbursement, and substantial philanthropic funding for congenital programs. The pediatric interventional cardiology market size in the region expands steadily as private insurers accept AI-guided procedures and as regulatory pathways such as Breakthrough Device Designation trim approval times. Canada complements U.S. capacity through referral networks that funnel complex neonates to tertiary centers, while Mexico draws cross-border patients with lower procedural tariffs.

Europe commands a sizeable share due to cohesive public healthcare and concentrated surgical expertise in Germany, France, and the United Kingdom. Early adoption of miniaturized heart valves and routine newborn pulse-oximetry screening boost the pediatric interventional cardiology market across EU member states. Joint clinical registries accelerate real-world data generation, helping manufacturers secure post-market authorizations.

Asia-Pacific is the fastest grower at 12.31% CAGR. China’s newborn screening programs have achieved 100% sensitivity for critical CHDs and lifted operative volumes, while Japan leads in transcatheter pulmonary valve replacements. Indian cardiac centers face cost constraints yet double pediatric cath-lab cases annually, supported by domestic production of lower-price closure devices. Government insurance expansions in Indonesia, Vietnam, and Thailand are unlocking procedure demand.

Middle East & Africa and South America trail but show momentum. Gulf nations invest heavily in specialty hospitals, and South Africa’s dedicated pediatric cardiac units serve as regional referral hubs. Brazil and Argentina widen pediatric cath-lab access under public-private insurance models, though currency volatility tempers immediate scale. Across emerging regions, portable echocardiography and tele-consult platforms extend specialist expertise to remote clinics.

Competitive Landscape

The global field is moderately fragmented. Abbott, Medtronic, and Edwards Lifesciences leverage large R&D budgets, regulatory muscle, and broad product portfolios to anchor the pediatric interventional cardiology market. Abbott’s TriClip reduced tricuspid regurgitation to moderate or less in 84% of two-year follow-ups, while its AVEIR leadless pacemaker pioneered dual-chamber functionality. Medtronic’s OmniaSecure introduced the smallest commercially available ICD lead, and the company continues work on absorbable stents. Edwards’ RESILIA tissue extends valve durability, delaying re-operation timelines.

M&A activity intensifies: Boston Scientific paid up to USD 664 million for Bolt Medical to secure intravascular lithotripsy technology and closed the Silk Road Medical takeover to strengthen neurovascular lines. Private-equity consolidation of 342 outpatient cardiology clinics between 2013 and 2023 is centralizing referral networks, influencing device vendor selection and contracting power.

AI and imaging startups, often spun out of academic labs, target smart guidance and radiation-free catheterization. Intellectual-property filings cluster around absorbable alloys, 3D-printed scaffolds, and machine-learning algorithms that derive fractional flow reserve from angiography alone. Suppliers that align technology breadth with pediatric-specific evidence are best positioned to capture incremental shares as the market matures.

Pediatric Interventional Cardiology Industry Leaders

Cardinal Health

Medtronic

GE Healthcare

NuMED Inc.

Abbott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Canid raised USD 10 million in Series A funding to enhance its pediatric vaccine management platform, demonstrating continued investor confidence in pediatric healthcare technology solutions that streamline clinical workflows and improve patient outcomes.

- April 2025: Abbott received FDA approval for the Tendyne transcatheter mitral valve replacement system, representing the first-of-its-kind device for replacing mitral valves without open-heart surgery, particularly benefiting patients with severe mitral annular calcification.

- January 2025: Boston Scientific completed its acquisition of Bolt Medical for up to USD 664 million, expanding capabilities in intravascular lithotripsy technology for treating complex calcified arterial disease in pediatric and adult populations.

- December 2024: Johnson & Johnson received FDA approval to expand Impella heart pump indications for pediatric patients with symptomatic acute decompensated heart failure and cardiogenic shock, marking a significant advancement in pediatric mechanical circulatory support.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pediatric interventional cardiology market as all catheter-based diagnostic and therapeutic procedures, together with the single-use and implantable devices that enable them, performed on infants, children, and adolescents up to 18 years of age to treat congenital or acquired cardiac defects. According to Mordor Intelligence, this universe generated USD 2.99 billion in revenue during 2025.

Scope exclusion: fetal cardiology interventions conducted in utero and open-surgery implantables are out of scope.

Segmentation Overview

- By Device Type

- Closure Devices

- Transcatheter Heart Valves

- Atherectomy Devices

- Catheters

- Balloons

- Stents

- Imaging & Guidance Systems

- Other Device Types

- By Procedure

- Catheter-Based Valve Implantation

- Congenital Heart Defect Correction

- Angioplasty

- Coronary Thrombectomy

- Hybrid Surgery-Assisted Interventions

- Other Procedures

- By End User

- Paediatric Catheterisation Laboratories

- Children’s Hospitals & Specialty Centres

- Ambulatory Surgical Centres

- Research & Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with pediatric cardiologists, cath-lab managers, procurement heads, and regulatory reviewers across North America, Europe, Asia-Pacific, and the Gulf region allowed us to validate annual procedure counts, average device mix per case, and expected pricing shifts. Surveys with parent support groups clarified adoption barriers and payer authorizations in emerging markets.

Desk Research

We began by compiling incidence and procedure volumes from public-domain cornerstones such as the CDC's Congenital Heart Defect registry, Eurostat hospital discharge files, and Japan's MHLW surgery database. Trade groups, including the American College of Cardiology and the European Association for Cardio-Thoracic Surgery, helped us benchmark evolving clinical guidelines. Device shipment clues were extracted from FDA 510(k) summaries, EUDAMED notifications, and quarterly 10-K filings. To size revenues, our analysts tapped D&B Hoovers for company financial splits, while Dow Jones Factiva tracked ASP trends in distributor disclosures. This list is illustrative; many other sources were reviewed for corroboration and gap filling.

Market-Sizing & Forecasting

A top-down incidence-to-procedure model converts live-birth CHD prevalence into treatable pools, factors age-specific intervention rates, and applies weighted ASPs to derive baseline revenue. Select bottom-up checks, supplier roll-ups of closure-device and transcatheter valve shipments, test the totals before adjustments. Key variables include: CHD incidence drift, cath-lab expansion, transcatheter valve approvals, disposable-to-reusable kit ratios, and regional reimbursement ceilings. Forecasts through 2030 rest on multivariate regression that links these drivers to historical revenue; expert panels establish scenario bounds and stress-test the equation when guideline changes or currency moves surface.

Data Validation & Update Cycle

Outputs pass three analyst reviews, variance thresholds trigger source re-checks, and models are refreshed each year or sooner if material recalls, landmark trials, or reimbursement shifts occur. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Our Pediatric Interventional Cardiology Baseline Commands Reliability

Published values often diverge because firms track different age bands, bundle peripheral devices, or refresh irregularly.

Key gap drivers include: 1) inclusion of fetal and adult congenital cases by some publishers, 2) aggressive ASP escalation assumptions, and 3) reliance on dated 2013 procedure benchmarks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.99 bn (2025) | Mordor Intelligence | - |

| USD 3.00 bn (2024) | Global Consultancy A | blends fetal plus adult interventions, uplifted ASPs |

| USD 1.16 bn (2023) | Trade Journal B | excludes Asia-Pacific volumes and hybrid cath-OR procedures |

These contrasts show that Mordor's disciplined scope, annually updated incidence data, and dual-track validation deliver a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the pediatric interventional cardiology market?

The market generated USD 3.28 billion in 2026 and is forecast to reach USD 5.23 billion by 2031.

Which device segment leads revenue?

Closure devices held 31.78% revenue share in 2025, the largest among all device categories.

Which region is growing fastest?

Asia-Pacific is projected to expand at a 12.31% CAGR, outpacing all other regions.

Why are ambulatory surgical centers gaining share?

Same-day discharge protocols and ultra-low-profile devices let less complex cases move from children’s hospitals to ASCs, which are growing at 11.08% CAGR.

How severe is the workforce shortage in pediatric cardiology?

Only 1,553 pediatric cardiologists practice in the United States, and projections indicate a shortfall of 8,650 cardiologists by 2037.

What innovation trend is most transformative today?

AI-enabled imaging that can replace invasive pressure wires or X-ray guidance is dramatically improving diagnostic precision while reducing radiation exposure.

Page last updated on: