Cardiac Resynchronization Therapy (CRT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

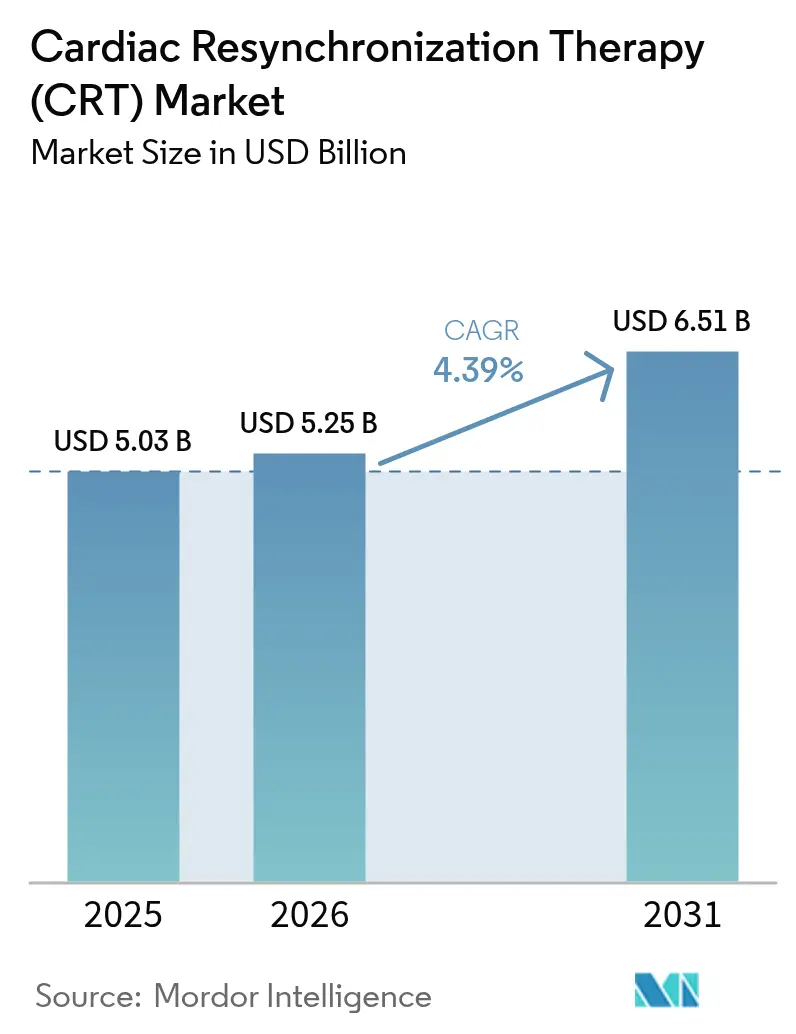

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 6.51 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

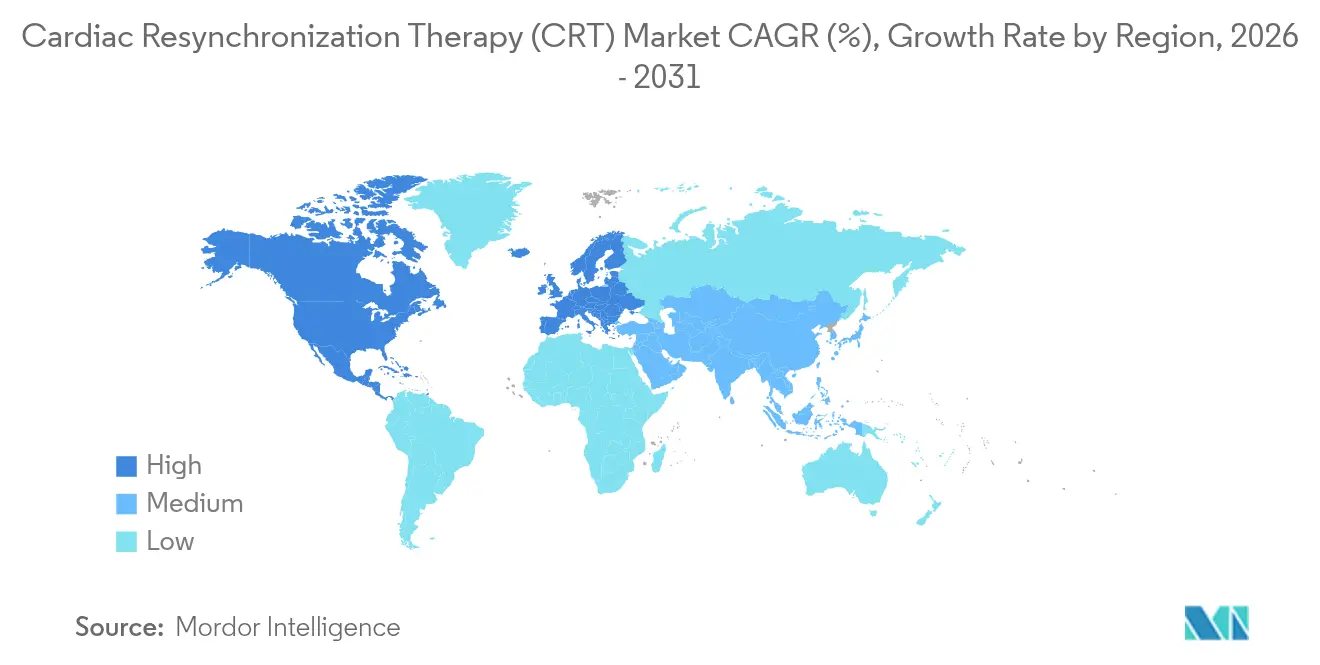

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

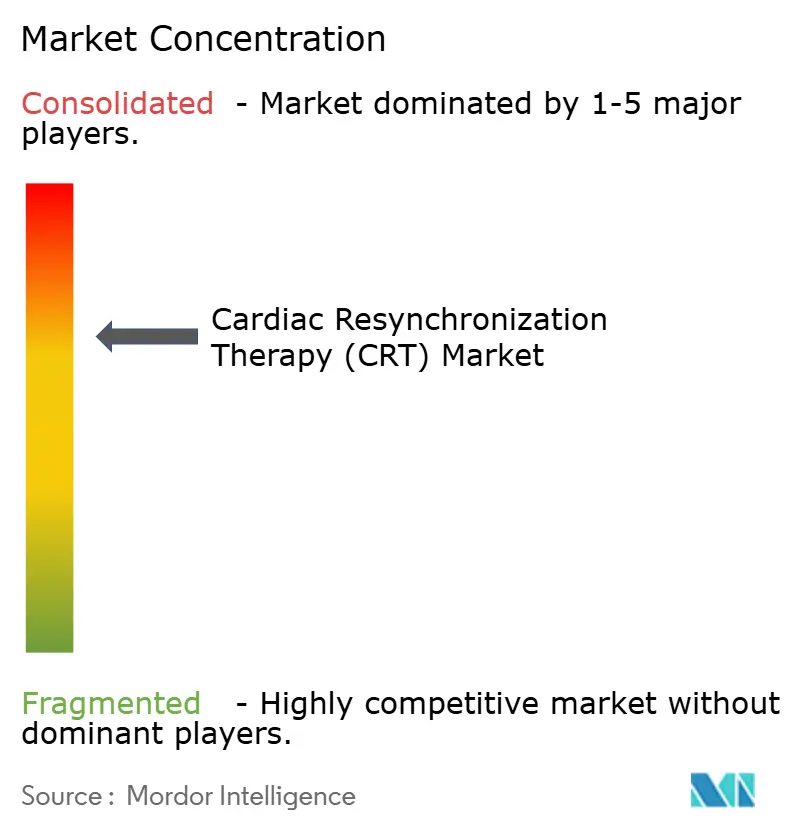

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Resynchronization Therapy (CRT) Market Analysis by Mordor Intelligence

The cardiac resynchronization therapy market size was valued at USD 5.03 billion in 2025 and estimated to grow from USD 5.25 billion in 2026 to reach USD 6.51 billion by 2031, at a CAGR of 4.39% during the forecast period (2026-2031). Demand is pivoting from pure procedure volume to value-based care, where AI-driven patient stratification, leadless systems, and modular upgrades determine purchasing decisions. Aging populations, a persistent heart-failure burden, and faster approvals for minimally invasive hardware sustain unit growth, while His-bundle and left-bundle branch area pacing are reshaping clinical guidelines. North America’s supportive reimbursement, Asia-Pacific’s capacity expansion, and Europe’s emphasis on outcome-based procurement together keep the cardiac resynchronization therapy market on a steady global uptrend. Manufacturers are mitigating raw-material risks by dual-sourcing rare-earth magnets and by adding fabless semiconductor partnerships, securing supply resilience and protecting margins.

Key Report Takeaways

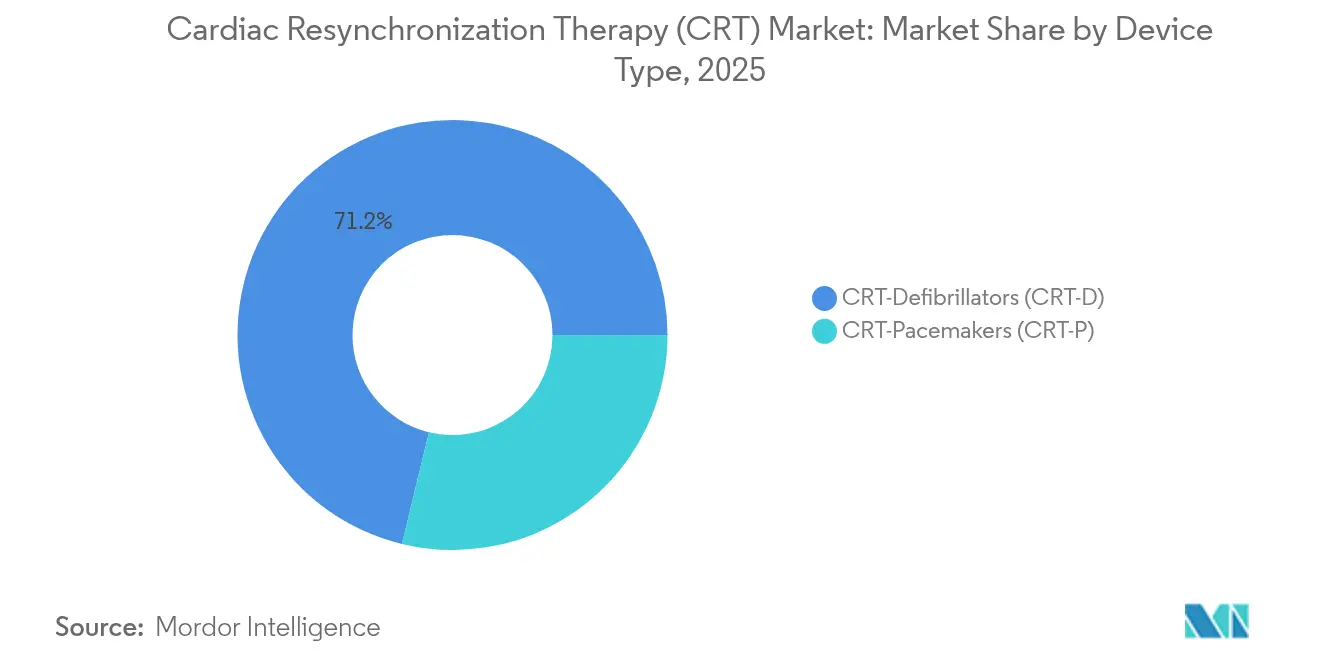

- By device type, CRT-Defibrillators led with 71.22% revenue share in 2025; CRT-Pacemakers are forecast to expand at a 4.96% CAGR through 2031.

- By end user, Hospitals & Cardiac Centers held 69.78% of the cardiac resynchronization therapy market share in 2025, while Ambulatory Surgical Centers record the highest projected CAGR at 5.44% to 2031.

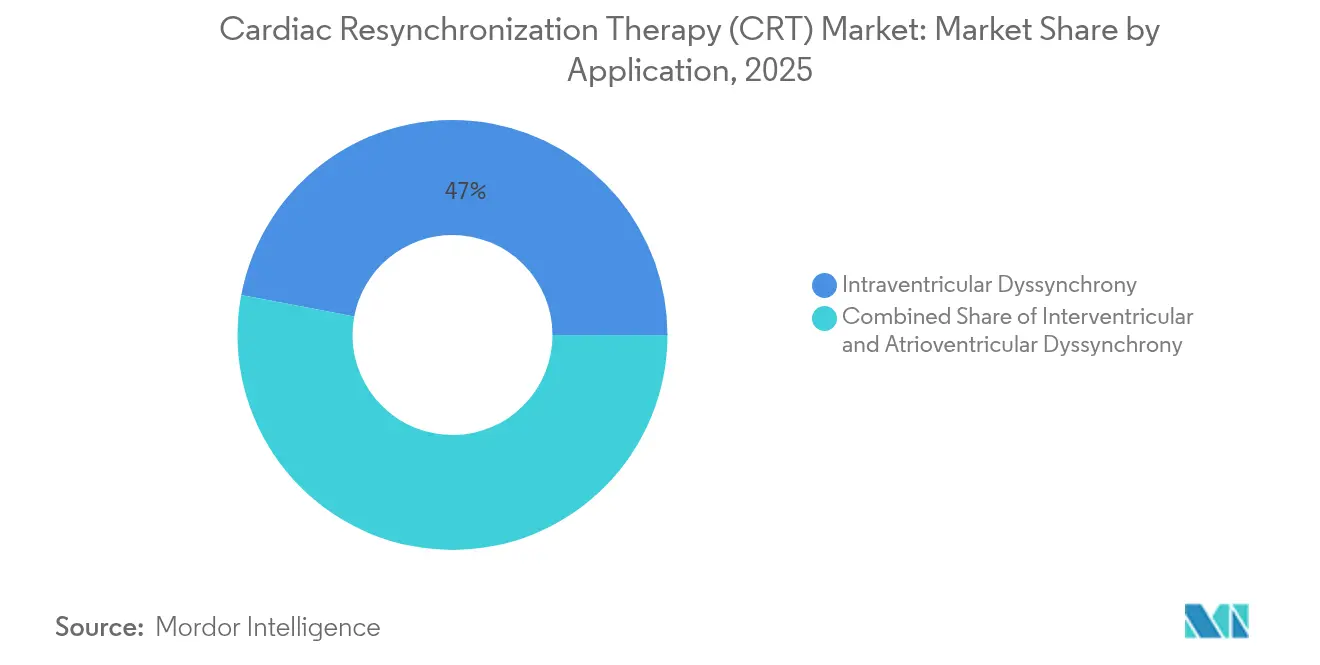

- By application, Intraventricular Dyssynchrony accounted for 47.02% share of the cardiac resynchronization therapy market size in 2025 and Interventricular Dyssynchrony is advancing at a 5.01% CAGR through 2031.

- By technology, Conventional Bi-ventricular Pacing commanded 87.62% share in 2025; His-Bundle Pacing is set to grow the fastest at 5.56% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Resynchronization Therapy (CRT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of heart failure & other cardiac disorders | +1.5% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Rapidly expanding geriatric population and sedentary lifestyles | +0.8% | Global; Asia-Pacific and North America | Long term (≥ 4 years) |

| Break-through product innovations | +0.6% | North America & Europe, then Asia-Pacific | Medium term (2-4 years) |

| Favourable reimbursement & HF mandates in OECD nations | +0.4% | OECD countries; spillover to emerging markets | Medium term (2-4 years) |

| AI-driven CRT optimisation & predictive analytics | +0.3% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Commercialisation of leadless & modular CRT in emerging markets | +0.2% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Heart Failure & Other Cardiac Disorders

Cardiovascular disease now causes 20.5 million deaths each year, and more than 80% occur in low- and middle-income countries. The widening prevalence of reduced ejection-fraction heart failure enlarges the cardiac resynchronization therapy market by continually adding eligible candidates. Asia-Pacific cities show increasing heart-failure incidence among adults in their 40s, triggered by urban diets and limited exercise. CRT lowers heart-failure-related admissions by 30-40%, making it a first-line device therapy in international guidelines. Enhanced echocardiography and AI-enabled biomarker screening uncover latent conduction delays, expanding the treatable cohort and underpinning sustained device demand.

Rapidly Expanding Geriatric Population and Sedentary Lifestyles

Every region is ageing, yet Asia-Pacific adds the largest absolute number of elders annually. Concomitant sedentary behaviour in younger demographics intensifies lifetime cardiovascular risk. Governments in China and India are scaling public insurance that covers CRT because long-term modelling shows a 40% drop in five-year management costs when CRT replaces repeated hospitalizations [1]Journal of the American Heart Association Staff, “Health-Economics of CRT,” jaha.ahajournals.org. The cardiac resynchronization therapy market thereby gains both volume and policy support, especially as outpatient implant pathways shorten stay lengths and free capacity for older complex cases.

Break-through Product Innovations

Leadless platforms such as Abbott’s AVEIR DR and EBR Systems’ WiSE CRT eliminate transvenous leads, lowering infection rates and enabling implantation in challenging anatomies. Artificial-intelligence software now optimises atrioventricular delays in real time, pushing responder rates above 80% in single-centre trials [2]Circulation Editorial Team, “Physiologic Pacing Advances,” circulationaha.org . Left Bundle Branch Area Pacing offers a physiologic alternative to bi-ventricular pacing and shows superior synchrony in septal fibrosis subgroups. Modular CRT lets physicians upgrade from single-chamber pacing to full CRT-D without generator replacement, extending device life and reducing revision costs, which keeps the cardiac resynchronization therapy market attractive for payers.

Favourable Reimbursement & Heart-Failure Mandates in OECD Nations

Policy makers in the United States, Germany, and Japan have widened CRT eligibility to include atrial fibrillation and New York Heart Association class II patients. Bundled-payment pilots prove that hospital systems recover CRT costs within three years through fewer readmissions, securing ongoing budget allocation. Harmonising coverage definitions across OECD states accelerates simultaneous launches of new pulse generators. This alignment shortens payback periods for R&D and sustains pipeline investment, buffering the cardiac resynchronization therapy market against macroeconomic cycles.

AI-Driven CRT Optimisation & Predictive Analytics Platforms

Algorithms analysing electrogram data detect impending decompensation weeks earlier than traditional follow-up visits, prompting timely medication titration and forestalling shocks. Clinics using remote analytics document 25% lower unplanned visits within one year, strengthening physician loyalty to vendors that bundle software with hardware. Early adoption is highest in the United States, but cloud infrastructures in India and Brazil are already onboarding these services, shifting revenue from one-time device sales toward recurring digital subscriptions.

Commercialisation of Leadless & Modular CRT Systems in Emerging Markets

Manufacturers assemble final devices in Malaysia and Costa Rica to avoid import tariffs and cut logistics time for Latin America and Middle East distributors. Tiered pricing strategies shave 20% off list price in lower-income nations, unlocking incremental volume without eroding margins in developed regions. Local regulatory agencies accept OECD clinical dossiers, trimming approval to nine months and speeding market entry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region regulatory requirements and lengthy approval cycles | –0.7% | Global; hits new entrants hardest | Medium term (2-4 years) |

| High procedure/device cost & limited implanter skill base | –0.5% | Emerging markets; rural developed regions | Long term (≥ 4 years) |

| Supply-chain vulnerability for rare-earth magnets and semiconductor ICs | –0.4% | Global; Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Rising clinical scrutiny of non-responder rates spurring CSP substitutes | –0.3% | North America & Europe; spreading to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Regulatory Requirements and Lengthy Approval Cycles

The United States FDA demands 12-18 months for novel CRT clearances, while Europe’s MDR adds post-market surveillance costs exceeding USD 10 million for a global filing [3]MDPI Devices Division, “Regulatory Pathways for Implantable Cardiac Devices,” mdpi.com . These investments deter start-ups and delay diffusion of cost-saving innovations. Variations in battery longevity mandates or lead insulation test protocols force region-specific SKUs, ballooning inventory complexity. Consequently, first launches concentrate in high-margin territories, slowing cardiac resynchronization therapy market expansion into lower-income countries.

High Procedure/Device Cost & Limited Implanter Skill Base

Implant charges range from USD 25,000 to USD 50,000. In economies where per-capita health spend is below USD 800, such costs are prohibitive. Kenya’s registry shows only 33.5% of indicated patients receive any implantable rhythm device, underscoring access gaps. Training pipelines are thin; electrophysiology fellowships number under 1 per 7 million population in many African and Southeast Asian countries. Without concerted education financing, procedure backlogs curb the cardiac resynchronization therapy market’s attainable volume.

Supply-Chain Vulnerability for Rare-Earth Magnets and Semiconductor ICs

Neodymium pricing spiked 45% in 2024 after geopolitical friction disrupted Chinese exports, inflating pulse-generator costs. Chip-foundry lead times lengthened to 40 weeks, forcing strategic stockpiling that ties up working capital. Vendors now dual-source magnets from Australia and chips from Taiwan, but any renewed supply shock could squeeze gross margins and delay device shipments.

Rising Clinical Scrutiny of Non-Responder Rates Spurring Conduction-System Pacing Substitutes

One in five CRT recipients shows minimal functional improvement, prompting payers to withhold reimbursement for repeat upgrades. Physicians increasingly direct borderline QRS-duration patients toward His-bundle pacing, bypassing conventional CRT. If large-scale trials confirm superior outcomes, substitution risk could dampen the cardiac resynchronization therapy market’s long-term growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: CRT-D Dominance Faces Pacemaker Innovation

CRT-Defibrillators generated 71.22% of 2025 global revenue, reflecting their dual role in halting arrhythmic death and resynchronising ventricles. Their comprehensive protection cements physician preference for high-risk heart-failure patients. Nevertheless, CRT-Pacemakers are rising at a 4.96% CAGR as guidelines broaden to milder ejection-fraction impairment. Leadless CRT-P devices shorten theatre time and cut infection risk, giving ambulatory centres a safer outpatient path. AI-driven optimisation firmware bundled into both categories is enlarging perceived clinical value and justifying price premiums. CRT-D adoption may plateau past 2028 as comorbidity profiles shift toward lower arrhythmia risk, prompting device-selection algorithms to propose pacemakers instead.

In monetary terms, the CRT-Pacemaker sub-segment is forecast to add USD 455 million by 2031, capturing users unsuitable for ICD shocks yet benefiting from ventricular resynchronisation. Advanced single-chamber CRT-P systems tailored to atrioventricular node ablation recipients highlight personalised therapy. Remote-monitoring connectivity features, once premium, are now standard, equalising differentiation and pushing the cardiac resynchronization therapy market toward service-based competition. Vendor strategies increasingly pair devices with subscription analytics, converting episodic hardware sales into annuity revenue.

By End User: Ambulatory Centers Challenge Hospital Dominance

Hospitals & Cardiac Centers held 69.78% of global procedures in 2025 because complex implants still need advanced imaging, anaesthesia, and intensive monitoring. They dominate upgrades and generator replacements, which account for one-third of annual volume. However, the 5.44% CAGR in Ambulatory Surgical Centers shows payer appetite for lower facility fees. Simplified CRT-P implants with conscious sedation allow same-day discharge, freeing inpatient beds for acuity-heavy cases. Hospitals respond by setting up on-site outpatient wings to retain referrals.

Home & Remote Monitoring Settings form a nascent but strategic channel. Cloud dashboards alert clinicians to threshold changes, enabling drug titration or firmware tweaks without clinic visits. Over time, remote adjustments could cut in-person follow-ups by 40%, easing workforce constraints while solidifying vendor-provider relationships. Research & Academic Institutes, though small in volume, shape future practice through first-in-human trials of conduction-system pacing, influencing longer-term product roadmaps and indirectly steering the cardiac resynchronization therapy industry toward physiologic pacing norms.

By Application: Dyssynchrony Treatment Patterns Evolve

Intraventricular Dyssynchrony retained 47.02% share in 2025, as prolonged left-bundle branch block remains the archetypal CRT indication. Its extensive evidence base simplifies payer approvals and clinician uptake. Interventricular Dyssynchrony therapy, expanding at 5.01% CAGR, benefits from 3-D strain-imaging that reveals right-to-left delay candidates previously misclassified. Application-specific algorithms now adjust interventricular pacing intervals every 60 seconds, lifting stroke volume and elevating responder fractions.

Atrioventricular Dyssynchrony, although smaller, gains relevance when atrial fibrillation ablation creates pacing dependency. Adaptive CRT modes restore atrial contribution and improve exercise capacity. Linking application analytics to device memory cards enhances decision support. As imaging AI distinguishes mechanical versus electrical dyssynchrony, treatment paradigms become more granular, enlarging the cardiac resynchronization therapy market size for precision-guided solutions while reducing non-responders.

By Technology: Physiological Pacing Disrupts Conventional Approaches

Conventional Bi-ventricular Pacing dominates with 87.62% share, underpinned by decades of surgical familiarity and robust leads. Yet His-Bundle Pacing surges at 5.56% CAGR as studies show better synchrony in septal scar, chronic kidney disease, and chemotherapy cardiomyopathy cohorts. The learning curve is steep, but sheath guides and fluoroscopy overlays shorten procedure time to near bi-ventricular norms. Left Bundle Branch Area Pacing offers a middle ground: distal conduction capture with higher success than His-bundle fixation.

Advanced technologies create a stratified product menu. Prudent hospitals standardise on bi-ventricular backups while specialist centres pioneer physiologic modes. By 2031, physiologic pacing could account for 19% of all implants, shaving the non-responder rate below 15% and cementing AI-directed lead placement as a routine adjunct. Such shifts keep the cardiac resynchronization therapy market competitive and innovative, challenging incumbents to refresh platforms rather than rely on incremental battery improvements.

Geography Analysis

North America commanded 45.02% of 2025 revenue because public and private payers reimburse CRT without volume caps, and more than 1,500 implants centres operate across the United States. Medicare covers device and implantation fees, ensuring broad access for seniors, while Veterans Affairs facilities adopt new algorithms rapidly through centralised procurements. Canadian provinces fund CRT under single-payer plans, though device selection committees negotiate aggressive discounts. Mexico’s growing middle class uses private hospitals where leadless CRT-P launches at a 15% price premium, yet faces no waiting lists.

Europe delivered steady growth under mature conditions. Germany leads procedure counts, aided by DRG incentives that reward shorter stays when remote monitoring replaces in-person checks. The United Kingdom’s NHS centralised tendering lowers per-unit costs but guarantees high vendor volumes. France pilots bundled payments linking hospital bonuses to six-month readmission rates, nudging adoption of predictive-analytics platforms. Eastern European nations are upgrading catheter labs with EU cohesion funds, expanding the reachable cardiac resynchronization therapy market.

Asia-Pacific posts the fastest trajectory, 6.03% CAGR through 2031. China’s device tenders specify domestic content thresholds, encouraging multinationals to co-manufacture with local firms. India’s Ayushman Bharat scheme reimburses CRT-P at tier-II city hospitals, enlarging rural reach. Japan adopts physiologic pacing early thanks to experienced electrophysiologists and an ageing demographic profile. South Korea’s national insurance approves AI-optimised CRT adjustments, speeding market penetration of software modules. Vietnam, Indonesia, and the Philippines witness double-digit growth from rising per-capita incomes and government insurance expansions that include high-value cardiac implants.

The Middle East & Africa region records moderate uptake. Gulf Cooperation Council states import premium CRT-D models for tertiary centres in Riyadh, Abu Dhabi, and Doha. South Africa’s private insurers cover CRT selectively, while public hospitals rely on donor programmes. Supply-chain constraints and limited implanter availability cap volume growth elsewhere on the continent. South America sees Brazil leading adoption as ANVISA accelerates approvals for locally-assembled pulse generators, while Argentina’s import-licence delays lengthen waiting lists.

Regulatory Landscape

Regulation for CRT systems remains anchored in high-risk active implantable device controls across major markets. In the European Union, Regulation (EU) 2017/745 (MDR) continues to govern conformity assessment and clinical evaluation for Class III/active implantable devices, with manufacturers increasingly using structured clinical-development planning and post-market evidence to support notified-body reviews.

In 2026, clinical-evidence requirements tightened further through standards and policy updates relevant to implantable device investigations. ISO 14155:2026 introduced updated expectations for clinical investigation governance (including clearer roles for Clinical Events Committees and Data Monitoring Committees) and documentation rigor, shaping how CRT trials and registries are designed and audited across jurisdictions that reference ISO-aligned practices. In Europe, Commission Delegated Regulation (EU) 2026/1451 amended provisions tied to clinical-investigation exemptions, prompting manufacturers to reassess whether specific implant configurations and modifications qualify for exemptions or require additional clinical work. In the United States, CRT pathways remain PMA-centered for many components and systems, and professional guidance such as the American College of Cardiology 2025 Appropriate Use Criteria for ICD and CRT continues to influence utilization and payer scrutiny around patient selection.

Value Chain Analysis

The CRT value chain spans specialized upstream materials, regulated manufacturing, and channel execution inside hospital purchasing ecosystems. Key inputs include pacing and sensing ASICs, lithium-iodine battery cells, platinum-iridium electrode alloys, and medical-grade silicone and polymers for lead insulation. Electronics and semiconductor dependencies are concentrated, with pacing ASIC capacity linked to foundry ecosystems in Taiwan and South Korea, while magnet and capacitor availability can add cost volatility for pulse generators.

Manufacturing and final assembly operate under stringent quality and biocompatibility regimes (commonly ISO 13485 quality systems and ISO 10993 biological evaluation), and are tightly coupled to regulatory documentation for Class III life-sustaining devices. The midstream layer includes device OEMs that integrate generators, leads, delivery tools, and software, increasingly bundling remote monitoring and analytics subscriptions alongside hardware. Downstream distribution runs through direct sales teams and regional distributors to electrophysiology labs and cardiac centers, where procurement decisions are influenced by reimbursement structures, outcome-based purchasing, and total cost of ownership, including service, remote monitoring infrastructure, and replacement-cycle economics.

Competitive Landscape

The cardiac resynchronization therapy market exhibits moderate consolidation. Abbott, Medtronic, and Boston Scientific collectively hold about 70% of global sales, benefiting from deep portfolios spanning CRT-D, CRT-P, leads, and analytics platforms. They invest heavily in battery chemistries exceeding 15-year longevity, cutting replacement frequency and lowering lifetime therapy cost. Each leverages cloud telemetry ecosystems that feed dashboards into hospital electronic records, embedding switching costs.

Challengers focus on niche technologies. EBR Systems pioneered the WiSE leadless left-ventricular electrode, gaining FDA approval in April 2025. Impulse Dynamics markets cardiac contractility modulation; while not CRT, it competes for the same patient budgets, pressuring incumbents to defend share with broader evidence. Zoll and MicroPort expand in price-sensitive nations by repurposing regional service networks from ICD businesses, offering bundled training that alleviates workforce shortages.

Supply resilience and intellectual property are critical battlefronts. Manufacturers dual-source capacitors and magnets, while patent estates on sheath geometry and AI algorithms prolong exclusivity. Vertical integration deepens: in July 2025 Teleflex acquired BIOTRONIK’s vascular intervention unit for EUR 760 million to strengthen distribution heft in electrophysiology. Johnson & Johnson’s USD 16.6 billion Abiomed buyout underscores cardiology as a strategic pillar, encouraging cross-divisional device-drug solutions that could reshape procurement contracts. Moderate but rising M&A keeps competitive tension high, fostering innovation yet keeping barriers formidable for start-ups.

Cardiac Resynchronization Therapy (CRT) Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic Plc

BIOTRONIK

Lepu Medical Technology(Beijing)Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity area is the product and workflow shift from conventional coronary-sinus lead placement toward conduction system pacing (CSP), particularly left bundle branch area pacing (LBBAP), supported by concrete regulatory actions in 2026. In March 2026, Medtronic received US FDA approval for an expanded indication for its OmniaSecure defibrillation lead to support LBBAP placement for CSP, and in April 2026 BIOTRONIK expanded access with FDA approval for Acticor Sky and Rivacor Sky ICD and CRT-D systems after launching CE-approved LBBAP high-voltage systems earlier in 2026. These actions widen the commercially available toolset for physiologic pacing strategies that address non-responder concerns and support differentiated premium system positioning.

Leadless and modular CRT remains a second whitespace, particularly for anatomies that complicate conventional LV lead delivery and for patients needing upgrade paths. EBR Systems WiSE CRT, already FDA-approved in April 2025, moved into a reimbursement-decision phase in June 2026 when CMS initiated a national coverage analysis under the Transitional Coverage for Emerging Technologies (TCET) pathway, setting a defined policy milestone that can broaden provider adoption once coverage terms are established. Device simplification that reduces implant time and lead-related complications also creates operational headroom for hospitals and ambulatory settings, aligning with the market pivot toward value-based care and software-led optimization reflected in current purchasing behavior.

Recent Industry Developments

- June 2026: CMS initiated a national coverage analysis (NCA) for EBR Systems WiSE CRT under the Transitional Coverage for Emerging Technologies (TCET) pathway. The analysis increases reimbursement visibility for leadless LV endocardial pacing and may reduce adoption friction for hospitals evaluating non-traditional CRT configurations while the review proceeds.

- July 2025: Teleflex completed its acquisition of BIOTRONIK’s Vascular Intervention business for EUR 760 million. The transaction strengthens Teleflex’s interventional cardiology platform and distribution leverage, which can influence adjacent electrophysiology and implant procedure ecosystems that interface with CRT implantation workflows.

- April 2025: EBR Systems secured US FDA approval for the WiSE CRT System, enabling fully leadless left-ventricular endocardial pacing. This approval expanded the competitive set beyond transvenous LV leads and accelerated industry focus on leadless and modular CRT architectures aimed at lowering infection risk and addressing difficult anatomies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from cardiac resynchronization therapy devices used to improve ventricular coordination in eligible heart failure and rhythm disorder patients, including the core implantable systems and related procedure driven device demand across major regions.

Scope exclusions: We exclude general heart failure drugs, diagnostic imaging, remote monitoring software sold as stand-alone, and non-CRT pacing or defibrillation devices that are not used for resynchronization.

Segmentation Overview

- By Device Type

- CRT-Defibrillators (CRT-D)

- Transvenous CRT-D

- Sub-cutaneous CRT-D (S-ICD)

- CRT-Pacemakers (CRT-P)

- Single-chamber CRT-P

- Dual/Biventricular CRT-P

- CRT-Defibrillators (CRT-D)

- By End User

- Hospitals & Cardiac Centres

- Ambulatory Surgical Centres

- Home & Remote Monitoring Settings

- Research & Academic Institutes

- By Application

- Intraventricular Dyssynchrony

- Interventricular Dyssynchrony

- Atrioventricular Dyssynchrony

- By Technology

- Conventional Bi-ventricular Pacing

- His-Bundle Pacing (HBP)

- Left Bundle Branch Area Pacing (LBBAP)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a consistent clinical and regulatory view of who is eligible for CRT and how therapy is delivered across care settings. We refer to public sources such as the US FDA device databases, US CDC and WHO cardiovascular statistics, OECD health expenditure indicators, and national health ministries for population and treatment context. Procedure and utilization direction is also cross-checked using sources such as CMS utilization and payment files, peer-reviewed cardiology journals, and publications from heart and rhythm associations.

On the commercial side, we review annual reports, investor presentations, and press releases to understand product mix shifts between CRT-P and CRT-D, as well as regional demand signals. A paid subscription for company financials and news is used to track reporting periods and segment disclosures, and a paid patent database is referenced to understand innovation cadence around leads and device longevity. The sources listed here are illustrative only, and many other public references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs are gathered from cardiologists and electrophysiology specialists, hospital procurement teams, distributors, and device service partners so we can pressure-test utilization assumptions and pricing ranges. Since demand is global, feedback is intentionally balanced across APAC, EMEA, and the Americas, and it is used to confirm eligible patient funnels, replacement cycles, and how quickly newer features are adopted in routine practice.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 38% |

| Mid tier: 58% | Functional/Unit leaders: 42% | EMEA: 37% |

| Smaller Players: 15% | Managers: 43% | Americas: 25% |

Market-Sizing & Forecasting

Sizing uses top-down and bottom-up logic together, where the top-down build reconstructs demand from the treated heart failure pool and CRT eligibility, and then converts that into device demand by applying implant and replacement rates. To keep the totals realistic, results are corroborated with selective bottom-up approximations such as sampled ASP times unit volumes by device type, channel checks on tender activity, and a sanity roll-up from disclosed revenue bands.

Key inputs include the heart failure prevalence trend, the share of patients with conduction abnormalities aligned with guideline indications, implant rates by care setting, replacement cycles linked to battery longevity, and the price mix between CRT-P and CRT-D. Where country level data is sparse, we fill gaps with proxy utilization rates from comparable health systems and then adjust based on local reimbursement and physician feedback. For forecasting, we rely on scenario analysis supported by expert views on diagnosis rates, therapy adoption, and pricing progression, and then the model is re-run under conservative and base case assumptions before final selection.

Data Validation & Update Cycle

Outputs are validated through triangulation across epidemiology signals, procedure direction, and supplier disclosures, and then checked for variances that do not match known reimbursement or access constraints. When an outlier is seen, the assumption is revisited and, if needed, follow-up calls are triggered to confirm whether it is a true shift or a data artifact. A second analyst review is completed before sign-off so calculation logic and unit consistency are verified.

Reports are refreshed annually, and interim updates are performed when material events occur, such as major regulatory actions, reimbursement changes, or sharp pricing moves in a large market. Before delivery, we do a fresh pass of key variables and currency conversions so clients receive the latest updated view.

Mordor Intelligence's Cardiac Resynchronization Therapy Market Estimate Compared With Other Published Estimates

Published CRT market values often differ because studies do not always count the same device scope, patient pool, and pricing basis, and the timing of currency conversion can also shift the final number. We try to keep assumptions traceable, so a reader can follow how demand and pricing were built and then validated.

The main gap comes from whether the estimate includes only implantable CRT systems versus folding in adjacent rhythm management revenues and broader service lines, and Mordor Intelligence keeps the model tied to CRT-P and CRT-D device demand linked to eligibility and replacement cycles rather than wider arrhythmia device spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.25 B (2026) | |

| Industry Publisher A | USD 6.96 B (2025) | Uses a different base year and may apply a broader revenue perimeter across end users and applications, which can lift totals when pricing and mix are not normalized to a common year. |

| Global Consultancy B | USD 5.05 B (2024) | Anchors on an earlier year and can reflect a narrower device only snapshot with limited adjustment for subsequent adoption changes, replacement timing, and ASP progression by device type. |

The spread across sources is mainly explained by year alignment and what gets counted around the core CRT device scope. By keeping inputs anchored to eligibility, implant and replacement rates, and device type pricing, the model stays easy to audit and repeat when new utilization or reimbursement signals emerge.

Key Questions Answered in the Report

What is the current Cardiac Resynchronization Therapy (CRT) Market size?

It stands at USD 5.25 billion in 2026 and is expected to reach USD 6.51 billion by 2031.

Who are the key players in Cardiac Resynchronization Therapy (CRT) Market?

Abbott Laboratories, Boston Scientific Corporation, Medtronic Plc, BIOTRONIK and Lepu Medical Technology(Beijing)Co.,Ltd. are the major companies operating in the Cardiac Resynchronization Therapy (CRT) Market.

Which is the fastest growing region in Cardiac Resynchronization Therapy (CRT) Market?

Asia-Pacific, at a 6.03% CAGR, driven by infrastructure upgrades and rising insurance coverage.

Which device type leads global revenue?

CRT-Defibrillators hold 71.22% share due to their dual arrhythmia and heart-failure benefits.

Page last updated on: