TCFD Climate Disclosure Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 4.21 Billion |

| Growth Rate (2026 - 2031) | 15.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

TCFD Climate Disclosure Software Market Analysis by Mordor Intelligence

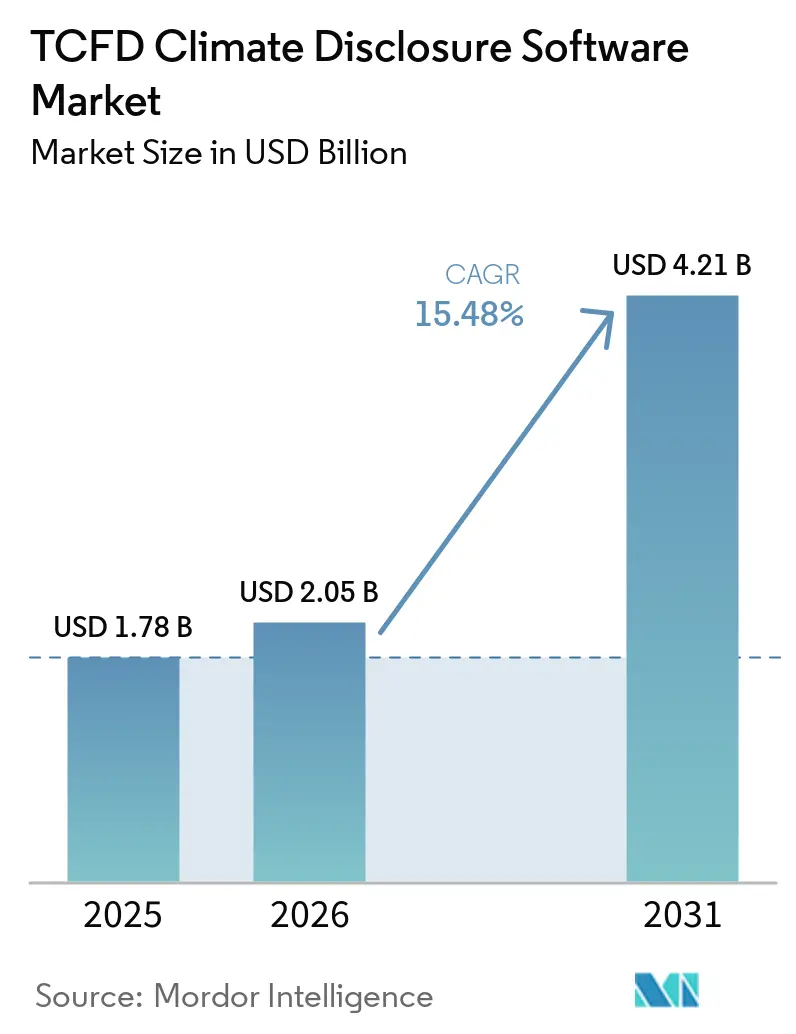

The TCFD climate disclosure software market size is projected to be USD 1.78 billion in 2025, USD 2.05 billion in 2026, and reach USD 4.21 billion by 2031, growing at a CAGR of 15.48% from 2026 to 2031. Regulatory alignment across the European Union, the ISSB framework, and major U.S. disclosure rules has moved TCFD climate disclosure software from a narrow reporting tool into a core enterprise system. Buying decisions are also being pulled forward because many reporting deadlines now sit close together across 2025-2027, which shortens vendor review cycles and favors platforms with broader prebuilt coverage. A second replacement wave is taking shape as companies that adopted earlier ESG tools between 2019 and 2022 shift toward audit-ready systems with stronger data controls, automation, and ongoing assurance support. Demand is also holding up beyond the mandatory reporting scope because investors, lenders, and large customers still expect consistent and traceable climate data even when formal rules are narrowed. Competition is now shaped by a clear divide between large software vendors that bring deep ERP connectivity and specialized providers that focus on disclosure templates, audit trails, and AI-assisted workflows.

Key Report Takeaways

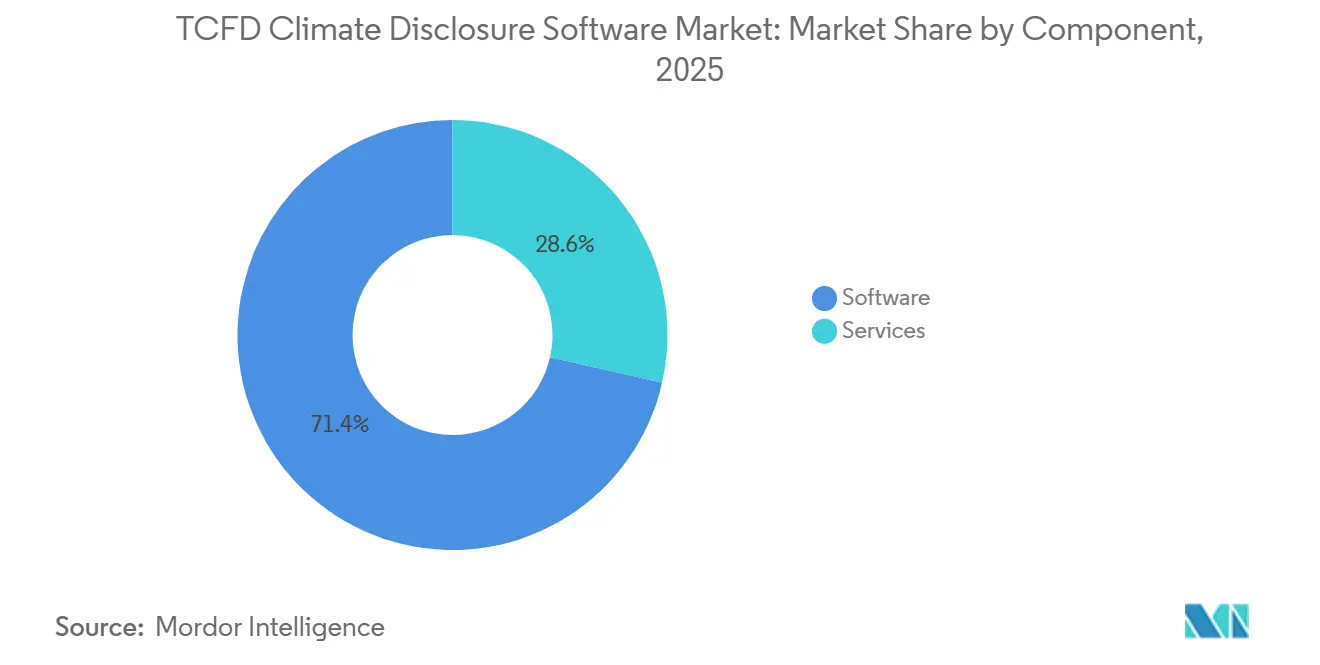

- By component, software accounted for 71.43% of revenue in 2025, while services are projected to expand at a 17.67% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 66.28% of the market in 2025, while hybrid deployment is expected to grow at a 17.21% CAGR through 2031.

- By enterprise size, large enterprises held 62.96% of the TCFD climate disclosure software market in 2025, while SMEs are projected to grow at an 18.46% CAGR through 2031.

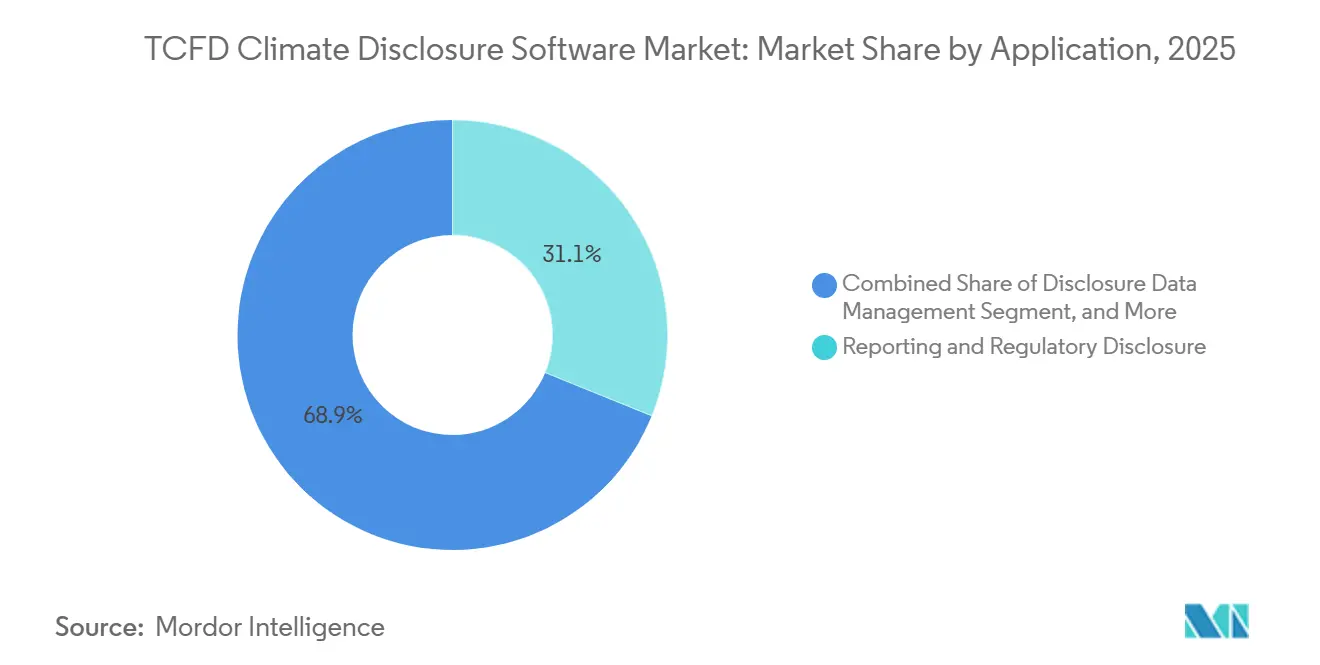

- By application, reporting and regulatory disclosure captured 31.13% of the market in 2025, while climate risk and scenario analysis is projected to grow at a 19.45% CAGR through 2031.

- By end user industry, banking, financial services, and insurance (BFSI) accounted for 34.14% share in 2025, while the government and public sector are expected to expand at a 19.12% CAGR through 2031.

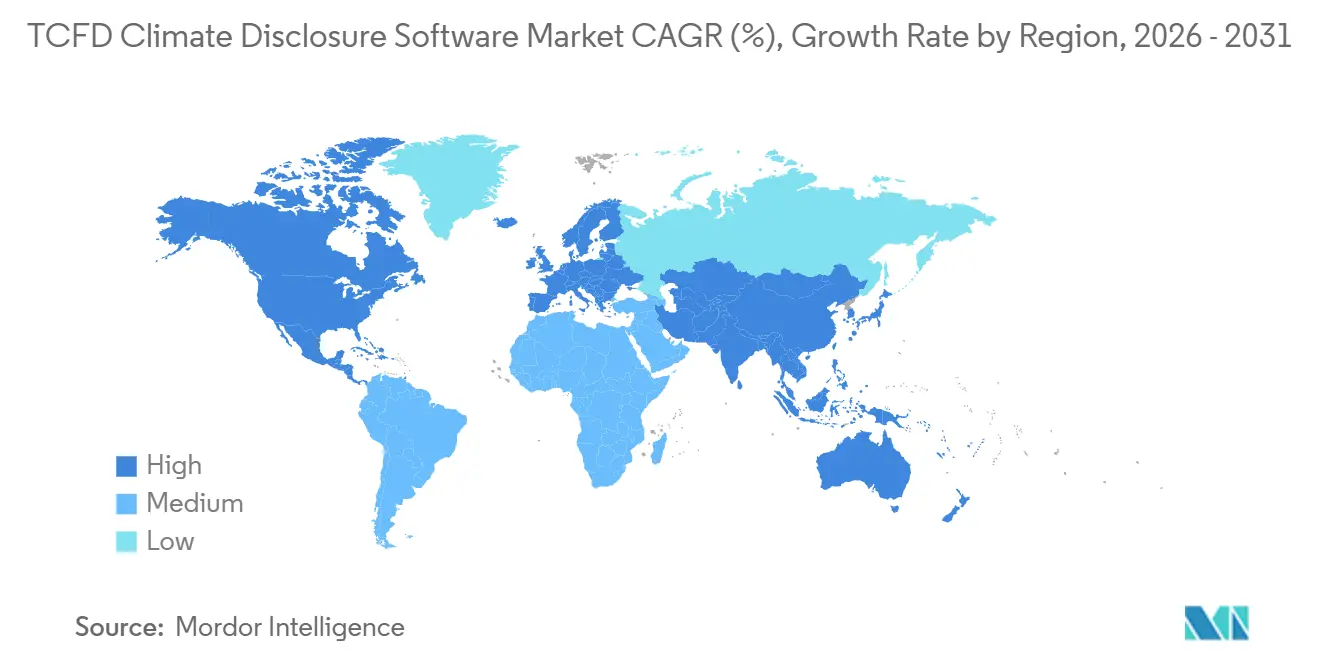

- By geography, North America held 36.14% of the climate disclosure software market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 19.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global TCFD Climate Disclosure Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Mandatory Climate Disclosure Compliance Across Capital Markets | +4.5% | Global | Short term (≤ 2 years) |

| Audit-Ready Data Trails for Investor and Regulator Scrutiny | +3.2% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| Shift From Annual Reporting to Continuous Climate Data Monitoring | +2.4% | North America, Europe, APAC | Medium term (2-4 years) |

| Scoping Pressure From Scope 3 Value Chain Data Requirements | +2.1% | Global | Medium term (2-4 years) |

| AI-Assisted Scenario Analysis for Transition Risk Planning | +1.8% | APAC, North America, Europe | Medium term (2-4 years) |

| Integration Demand With ERP, EHS, and GRC Systems | +1.3% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Mandatory Climate Disclosure Compliance Across Capital Markets

The TCFD climate disclosure software market is being pushed most directly by the spread of mandatory reporting rules across major capital markets. The CSRD brought the largest EU public-interest entities into ESRS-aligned reporting for fiscal year 2024, and the revised 2026 threshold changes are now concentrating spending among the largest companies that remain in scope. California SB 253 added another domestic demand layer in the United States, requiring companies operating in the state with more than USD 1 billion in annual revenue to publicly disclose Scope 1 and Scope 2 emissions. CARB identified around 2,600 entities on its preliminary list in September 2025. The TCFD climate disclosure software market is also seeing shorter buying windows because many filing deadlines now cluster within a narrow period, which leaves enterprises less time to wait for product maturity before committing to a platform. This has given the TCFD climate disclosure software market a clear preference for vendors that already support CSRD, ESRS, ISSB S1 and S2, GRI, TCFD, and SASB mappings in native form rather than through manual configuration. As a result, broad framework coverage has become a near-term buying factor, not just a product feature.

Audit-Ready Data Trails For Investor and Regulator Scrutiny

The TCFD climate disclosure software market is also being reshaped by the move from narrative sustainability reporting to structured and assured disclosure. SEC climate rules linked Scope 1 and Scope 2 emissions reporting for large accelerated filers to third-party attestation from fiscal year 2025, which makes data lineage and evidence control central to software selection. The Bank of England and the Prudential Regulation Authority moved in the same direction in 2025 by raising supervisory expectations for quantified climate-related financial impacts in banks and insurers, which increases the need for traceable and version-controlled data flows. In the TCFD climate disclosure software market, this changes the buying case because platforms are now evaluated on how well they reduce assurance friction rather than only on how well they collect ESG data. Companies that store evidence in a structured, role-based system can lower the burden on external attestors, which supports lower audit effort after deployment. That has made premium pricing easier to defend in the TCFD climate disclosure software market because software design now affects compliance cost, not just reporting convenience.

Shift From Annual Reporting to Continuous Climate Data Monitoring

The TCFD climate disclosure software market is moving away from annual data collection and toward continuous monitoring because reporting rules now require more frequent and more granular validation. The GHG Protocol Scope 3 Standard Phase 1 revision process in March 2026 called for companies to disaggregate Scope 3 emissions by data quality tier, which turns a once-a-year aggregation exercise into an ongoing monitoring requirement.[1]GHG Protocol, “Scope 3 Standard Revisions Phase 1 Progress Update,” GHG Protocol, ghgprotoco SAP’s Q2 2026 update to Sustainability Control Tower added monthly, quarterly, and yearly period support for greenhouse gas data imports, which reflects how the TCFD climate disclosure software market is adapting product design to continuous workflows. Watershed reported that its data cleaning agents reduced time to actionable data by 80% across test customers, and NEC reported a 93% reduction in man-hours for AI-assisted climate disclosure preparation under Japan’s SSBJ standards.[2]NEC Corporation, “NEC Streamlines and Advances Climate-Related Disclosure Processes in Securities Reports Using AI,” NEC Corporation, nec.com These examples show why the TCFD climate disclosure software market is gaining support from finance leaders who want shorter reporting cycles and cleaner data flows. They also show that workflow automation is now tied to control quality, which strengthens the business case beyond simple labor savings.

Scoping Pressure From Scope 3 Value Chain Data Requirements

Scope 3 is creating one of the strongest medium-term growth drivers for the TCFD climate disclosure software market because it extends disclosure obligations beyond the reporting company itself. The GHG Protocol revision process stated that no more than 5% of total Scope 3 emissions may remain unquantified without documented category-level justification, which limits the use of unsupported estimates and raises the standard for supplier data collection. EcoVadis launched a Product Carbon Footprint Calculator in 2026 across 12 industrial sectors and 13 languages, and it grades supplier-reported metrics across 4 Carbon Data Reliability Levels, which supports more structured downstream disclosure. The WBCSD PACT methodology and its technical specifications also give the TCFD climate disclosure software market a more standardized route for exchanging machine-readable product carbon data across trading partners. This matters because the climate disclosure software market is no longer serving only corporate reporting teams; it is increasingly sitting between large enterprises and supplier networks that must exchange usable carbon data. Vendors that can aggregate, validate, and relay supplier information at scale are therefore positioned more strongly than tools built around internal reporting only.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Climate Data Across Supplier and Portfolio Networks | -2.8% | Global | Medium term (2-4 years) |

| High Implementation and Integration Complexity | -2.1% | APAC, MEA, South America | Medium term (2-4 years) |

| Inconsistent Framework Harmonization Across Jurisdictions | -1.4% | Global | Long term (≥ 4 years) |

| Model Risk and Liability Concerns in Forward-Looking Disclosures | -0.9% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Climate Data Across Supplier and Portfolio Networks

The TCFD climate disclosure software market still faces a fundamental limitation: the weakest data often sits outside the reporting enterprise. Sphera found in 2025 that 57% of companies reporting on Scope 3 used supplier-specific data only as a partial source and filled many gaps with industry-average factors, which limits precision even when reporting platforms are sophisticated. This means the TCFD climate disclosure software market can automate workflows, calculations, and validation layers, but it cannot, on its own, fully address poor upstream measurement quality. The result is a ceiling on disclosure quality because downstream reports remain dependent on suppliers that still estimate emissions rather than measure them directly. Interoperability efforts from the GHG Protocol and WBCSD are improving the technical basis for exchange, but the underlying availability of primary supplier data remains a longer-term transition. This keeps data credibility as a restraint on the TCFD climate disclosure software market, even as product capabilities continue to improve.

High Implementation and Integration Complexity

Implementation complexity remains a meaningful brake on the TCFD climate disclosure software market because deployments often reach across finance, operations, risk, and supplier systems at the same time. SAP’s Q2 2026 documentation showed that organizations may need to align S/4HANA compatibility, configure interface extensibility with up to 20 custom dimensions, and reconcile fiscal year structures between sustainability and financial reporting systems. In the TCFD climate disclosure software market, this burden is especially heavy in the Asia-Pacific, South America, the Middle East, and Africa, where multi-vendor ERP environments are common and internal sustainability IT resources are often more limited. Quentic also highlighted how climate reporting requirements in Germany sit alongside data governance obligations, which helps explain why buyers may choose more complex hybrid setups instead of faster pure cloud deployments. Security and control requirements add another layer because regulated buyers often need more validation before full rollout, which can lengthen onboarding even after procurement is complete. This slows deployment speed in the TCFD climate disclosure software market and can push some organizations toward phased adoption rather than broad implementation from day 1.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reflects Post-Deployment Advisory Demand

Software dominated the TCFD climate disclosure software market with a 71.43% revenue share in 2025, which confirms that platform licensing remains the core commercial model. The largest providers in the TCFD climate disclosure software market continue to rely on SaaS subscription structures that are tied to data volume, entity count, and active reporting frameworks. This model works well because enterprises that connect climate data to finance and risk processes tend to stay on the same system once controls, workflows, and internal approvals are built around it. The strength of the software layer also reflects the need for recurring template updates, data ingestion, permissions management, and disclosure mapping across multiple standards. In practical terms, software remains the center of the value proposition because it creates the operating environment where reporting, validation, and audit preparation come together.

Services is still the faster-moving part of the TCFD climate disclosure software market, with a projected CAGR of 17.67% through 2031. Demand is rising because buyers need implementation support, emissions data integration, workflow design, assurance preparation, and recurring configuration changes as standards evolve. The GHG Protocol Scope 3 revision process adds to that need because companies must revisit how emissions data is classified and supported across quality tiers. This keeps post-deployment work active long after the first go-live date, especially for large reporting groups with multiple entities and disclosure frameworks. The climate disclosure software industry is therefore seeing a closer link between software sales and expert services, and that is pushing vendors toward bundled offerings rather than stand-alone licenses.

By Deployment Mode: Hybrid Architectures Support Control at the Regulatory Boundary

Cloud-based deployment led the TCFD climate disclosure software market with a 66.28% share in 2025, reflecting strong buyer preference for scalability and faster content updates. Cloud delivery has become the default path in the TCFD climate disclosure software market because vendors can update disclosure templates and regulatory mappings without waiting for client-side IT cycles. This matters in a rule environment that keeps changing, since buyers need current CSRD, ISSB, and ESRS content in working systems instead of manual workarounds. The cloud model also reduces infrastructure burden for companies that want centralized reporting across multiple business units and jurisdictions. It has therefore stayed ahead as the most practical option for organizations that value speed, standardization, and lower maintenance effort.

Hybrid deployment is projected to expand at a 17.21% CAGR through 2031, which shows that control concerns remain important even as cloud adoption rises. Buyers are using hybrid designs to keep sensitive financial records and some Scope 3 calculations inside controlled environments while still using cloud layers for collaboration and disclosure workflows. Quentic highlighted how German data governance expectations can raise the appeal of this approach for companies that must balance reporting transparency with localization and control needs. On-premises deployment still has a role in the TCFD climate disclosure software market, mainly in government and highly regulated financial settings where data sovereignty carries extra weight. SAP’s product path shows the same pattern because it continues to support enterprise integration choices instead of forcing all customers into a single architecture.

By Enterprise Size: SME Expansion Broadens the Addressable Base

Large Enterprises held 62.96% share of the TCFD climate disclosure software market size in 2025, which reflects their early entry into mandatory reporting and assurance-heavy workflows. Large organizations were the first to commit meaningfully to the TCFD climate disclosure software market because they faced the earliest obligations under CSRD, SEC rules, and ISSB-linked disclosure regimes. Their buying behavior also favors broad systems that can connect climate data to financial reporting, internal controls, and risk management in one evidence layer. This group has the staff, systems, and reporting complexity that make premium platforms easier to justify. It also has the greatest exposure to external assurance, which supports demand for stronger governance features and deeper integration.

SMEs are projected to record the fastest enterprise-size CAGR at 18.46% through 2031, and this is the largest expansion opportunity now opening in the TCFD climate disclosure software market. Growth is being pushed by value chain disclosure demands, California SB 253 coverage at the larger revenue threshold, and EBA climate disclosure expectations that encourage banks to gather better portfolio-level information from smaller borrowers.[3]European Banking Authority, “Pillar 3 Data Hub,” European Banking Authority, eba.europa.eu The VSME standard adopted in July 2025 provides a simpler reporting route for SMEs, which gives the TCFD climate disclosure software market a clearer path below the large-enterprise licensing tier. The TCFD climate disclosure software industry is therefore moving into a broader buyer base that values easier onboarding, lower complexity, and supplier-facing collaboration tools.

By Application: Climate Risk and Scenario Analysis Moves Closer to Finance

Reporting and Regulatory Disclosure captured 31.13% share in 2025, making it the largest application in the TCFD climate disclosure software market. That position reflects the volume of recurring filing activity now moving through CSRD, SEC climate rules, and ISSB-aligned disclosure regimes. Companies entering mandatory cycles need repeatable workflow control, framework mapping, and documentation support, and that keeps reporting use cases at the center of the climate disclosure software market. The application also tends to retain users because once a company configures reporting entities, controls, and templates, switching becomes more disruptive. This makes disclosure reporting the largest installed workflow base, even as adjacent use cases continue to rise.

Climate Risk and Scenario Analysis is projected to expand at a 19.45% CAGR through 2031, which shows how the TCFD climate disclosure software market is moving beyond compliance and closer to capital planning. ISSB S2 and ESRS-linked requirements pull physical and transition risk into quantified financial analysis, which means scenario tools are becoming part of CFO decision-making rather than a stand-alone sustainability exercise.[4]IFRS Foundation, “International Sustainability Standards Board,” IFRS Foundation, ifrs.org Ortec Finance’s 2026 climate scenario suite illustrates this shift because its outputs are designed to connect with broader portfolio and economic scenario tools instead of sitting in isolated reports. Disclosure Data Management and Disclosure Analytics and Performance Insights support the earlier and later stages of the same workflow, while Assurance, Verification, and Audit Readiness is gaining traction as attestation requirements widen. This mix shows that the TCFD climate disclosure software market is becoming more process-linked, with applications increasingly tied together across data capture, analysis, disclosure, and assurance.

By End User Industry: BFSI Leads Current Demand While Public Entities Accelerate

Banking, Financial Services, and Insurance led the TCFD climate disclosure software market with a 34.14% share in 2025, reflecting the sector’s unusually heavy reporting burden. BFSI firms must address financed emissions, counterparty exposure, climate stress testing, and sustainability-linked disclosure expectations across lending, insurance, and asset management functions. This creates a high-volume use case because the data burden extends far beyond internal operations and reaches portfolio, client, and funded emissions. The sector also tends to need stronger governance and audit controls because climate metrics increasingly feed regulated risk and disclosure processes. That combination has kept BFSI at the front of the climate disclosure software market even as other sectors scale their programs.

The Government and Public Sector is projected to grow at a 19.12% CAGR through 2031, making it the fastest-rising end-user group. IPSASB’s SRS 1 framework gives public entities a more structured route for climate-related financial disclosure, which is helping public sector adoption move from exploratory work toward formal process building. Industrial Manufacturing, Energy and Utilities, and Information Technology and Telecom remain important because product carbon footprint rules and Scope 3 category requirements often need specialized configuration. Healthcare and Life Sciences, Retail and Consumer Goods, and Transportation and Logistics sit in a later but still active adoption stage, with lenders and large customers increasing the cost of non-disclosure. Together, these patterns show that the TCFD climate disclosure software market is broadening by end use, but sectors with greater regulated data intensity still adopt faster and spend more deeply.

Geography Analysis

North America held 36.14% of the TCFD climate disclosure software market share in 2025, making it the largest regional contributor. The regional TCFD climate disclosure software market is led by the United States, where SEC climate rules brought large accelerated filers into emissions disclosure and attestation requirements from the fiscal year 2025. California SB 253 and SB 261 widened the addressable buyer base beyond SEC registrants, which created a two-layer compliance environment that rewards platforms with flexible template libraries and strong multi-framework mapping. The North American TCFD climate disclosure software market also benefits from investor pressure that remains active even when regulation shifts, which gives adoption a more durable base than a rule-only demand pattern.

Europe remains a major center for the TCFD climate disclosure software market even after the 2026 CSRD scope revision. The February 2026 directive narrowed the mandatory perimeter to companies with more than 1,000 employees and net turnover above EUR 450 million, or approximately USD 486 million, but it also concentrated compliance spending among the largest remaining in-scope entities. The regional climate disclosure software market still benefits from investor due diligence, bank covenant requirements, public procurement pressure, and VSME-related supplier data requests, which keep software investment active beyond the reduced statutory boundary.[5]Mouvement des Entreprises de France, “CSRD, Market Study of Software Solutions for Sustainability Reporting,” MEDEF, medef.com European vendors such as Quentic, Greenomy, and Emitwise continue to compete on ESRS-native depth and localization, while GDPR and supervisory frameworks support a stronger interest in hybrid and controlled deployment models.

Asia-Pacific is projected to record the fastest regional CAGR at 19.32% through 2031 in the TCFD climate disclosure software market. The regional TCFD climate disclosure software market is being lifted by rapid movement from voluntary sustainability reporting toward mandatory and standards-based disclosure. Japan’s SSBJ framework is a major part of that shift, and NEC reported in April 2026 that AI-assisted disclosure preparation cut man-hours by 93% compared with manual processes. Singapore moved listed issuers into ISSB-aligned reporting from 2025, and China’s CSDS trial standards brought the first reports by April 2026 for more than 300 listed companies, which expands the region’s formal buyer base. South America and Middle East, and Africa remain earlier-stage parts of the climate disclosure software market, but Brazil’s ISSB alignment efforts, Saudi Arabia’s ESG direction under Vision 2030, and the UAE net-zero related reporting activity are building the foundation for later procurement. The result is a region where present demand is uneven by country, but the forward pipeline is strengthening quickly.

Competitive Landscape

The TCFD climate disclosure software market remains moderately fragmented, with large enterprise vendors and specialized providers competing from very different starting points. SAP, IBM, Oracle, Salesforce, and Microsoft approach the TCFD climate disclosure software market through integration depth, enterprise security, and existing software relationships. SAP’s Q2 2026 update to Sustainability Control Tower, including more than 200 quantitative ESRS metrics and a broader reporting workflow, reflects that enterprise-suite strategy clearly. Workiva, Persefoni, and Watershed compete more directly on audit-ready lineage, disclosure workflow depth, and AI-supported productivity, which gives buyers a clearer alternative when disclosure control matters more than ERP proximity.[6]Workiva Inc., “Sustainability Reporting, AI-Powered Platform for Trust, Transparency, and Accountability,” Workiva, workiva.com

A third layer is taking shape around supplier data connectivity, which is changing how the TCFD climate disclosure software market handles Scope 3 at scale. EcoVadis has positioned its carbon data tools as an input layer that can feed broader disclosure environments, and its 2026 partnership with Workiva shows how supplier emissions data is being linked more directly into finance-oriented reporting systems. The same pattern appeared in EcoVadis’ partnership with Watershed, which was designed to close the primary data gap in supplier emissions and improve the quality of downstream reporting workflows. This means competition in the TCFD climate disclosure software market is no longer limited to front-end disclosure platforms, because control over supplier data channels is also becoming strategic. Vendors that can combine disclosure workflows with more reliable partner data are likely to gain an advantage as Scope 3 reporting matures.

Strategic moves in the TCFD climate disclosure software market increasingly favor partnership and ecosystem design over full in-house development. The October 2025 Diligent and Persefoni partnership is a strong example because Diligent moved its carbon accounting clients to Persefoni and took an equity position instead of building the capability itself. Workiva’s Sustainability Disclosure Agent also shows how vendors are using AI inside existing governance layers to identify present, partial, and missing disclosures before executive or assurance review. Emerging providers such as Greenomy, Emitwise, and Nasdaq’s Metrio are targeting the space between full enterprise deployments and simpler SME-oriented tools, which has become more defined since the VSME standard was adopted in 2025. At the same time, conformance requirements tied to standards and technical specifications can raise the bar for smaller entrants, which tends to favor better-funded vendors that can keep products current across jurisdictions. Overall, the TCFD climate disclosure software market is competitive, but the strongest players are increasingly the ones that pair disclosure depth with system integration and ecosystem reach.

TCFD Climate Disclosure Software Industry Leaders

Workiva Inc.

Salesforce, Inc.

International Business Machines Corporation

SAP SE

Diligent Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EcoVadis and Workiva Inc. announced a strategic partnership to expand the EcoVadis Carbon Data Network, connecting primary supplier carbon data with Workiva's AI-powered platform. The integration enables mutual customers to replace industry-average Scope 3 estimates with granular, audit-ready supplier emissions data directly within Workiva's finance-integrated disclosure environment.

- April 2026: NEC Corporation (Japan) announced the launch of an AI-powered business support service for climate-related disclosure in securities reports under Japan's SSBJ standards, scheduled for fiscal year 2026. Internal trials demonstrated a 93% reduction in man-hours compared to manual processes, addressing SSBJ S2 climate disclosure requirements mandatory from the fiscal year ending March 2027.

- February 2026: The European Parliament and Council published the CSRD Content Directive (EU 2026/470) in the Official Journal, narrowing mandatory CSRD obligations to companies with more than 1,000 employees and net turnover exceeding EUR 450 million (USD 486 million), materially concentrating compliance investment among the largest remaining in-scope enterprises.

- October 2025: Diligent Corporation and Persefoni AI Inc. announced a strategic partnership in which Diligent transitioned its carbon accounting client base to Persefoni's platform and acquired an equity stake in Persefoni, validating the platform as the preferred climate accounting layer for governance-led enterprise clients.

Global TCFD Climate Disclosure Software Market Report Scope

TCFD Climate Disclosure Software refers to digital platforms specifically designed to assist organizations in adhering to the Task Force on Climate‑related Financial Disclosures (TCFD) framework. These solutions enable businesses to efficiently collect, manage, and report climate-related data such as emissions, risks, and scenario analyses while aligning with investor and regulatory requirements. By integrating carbon accounting, sustainability data management, and audit-ready reporting, these tools facilitate transparent disclosure of climate risks and opportunities across financial, operational, and governance dimensions.

The TCFD Climate Disclosure Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Disclosure Data Management, Reporting and Regulatory Disclosure, Assurance, Verification, and Audit Readiness, Disclosure Analytics and Performance Insights, and Climate Risk and Scenario Analysis), End User Industry (Industrial Manufacturing, Energy and Utilities, Banking, Financial Services, and Insurance, Retail and Consumer Goods, Information Technology and Telecom, Healthcare and Life Sciences, Government and Public Sector, Transportation and Logistics, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Disclosure Data Management |

| Reporting and Regulatory Disclosure |

| Assurance, Verification, and Audit Readiness |

| Disclosure Analytics and Performance Insights |

| Climate Risk and Scenario Analysis |

| Industrial Manufacturing |

| Energy and Utilities |

| Banking, Financial Services, and Insurance |

| Retail and Consumer Goods |

| Information Technology and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Transportation and Logistics |

| Other End User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Disclosure Data Management | ||

| Reporting and Regulatory Disclosure | |||

| Assurance, Verification, and Audit Readiness | |||

| Disclosure Analytics and Performance Insights | |||

| Climate Risk and Scenario Analysis | |||

| By End User Industry | Industrial Manufacturing | ||

| Energy and Utilities | |||

| Banking, Financial Services, and Insurance | |||

| Retail and Consumer Goods | |||

| Information Technology and Telecom | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Transportation and Logistics | |||

| Other End User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the TCFD climate disclosure software market size in 2026 and how large will it be by 2031?

The TCFD climate disclosure software market is valued at USD 2.05 billion in 2026 and is forecast to reach USD 4.21 billion by 2031, growing at a 15.48% CAGR over 2026-2031.

What is driving demand for climate disclosure software the most?

The strongest demand driver is the spread of mandatory disclosure rules across the EU, the United States, and ISSB-aligned jurisdictions, which is pushing companies to adopt systems with audit trails, framework mapping, and assurance support.

Which application area is expanding the fastest?

Climate Risk and Scenario Analysis is the fastest-growing application, with a projected 19.45% CAGR through 2031, because climate risk is moving closer to finance and capital planning workflows.

Which customer group is opening the largest new opportunity?

SMEs are the fastest-growing enterprise-size segment at 18.46% CAGR, supported by value chain disclosure requests, bank data needs, and simplified reporting pathways under the VSME framework.

Why does BFSI lead spending in this space?

BFSI led with 34.14% share in 2025 because banks, insurers, and asset managers face financed-emissions disclosure, climate risk reporting, and portfolio-level data requirements that are wider than internal operational reporting alone.

Which region is growing the fastest and why?

Asia-Pacific is projected to expand at a 19.32% CAGR through 2031 as Japan, Singapore, China, and other regional markets move from voluntary reporting toward formal disclosure frameworks.

Page last updated on: