Carbohydrase Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 3.04 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

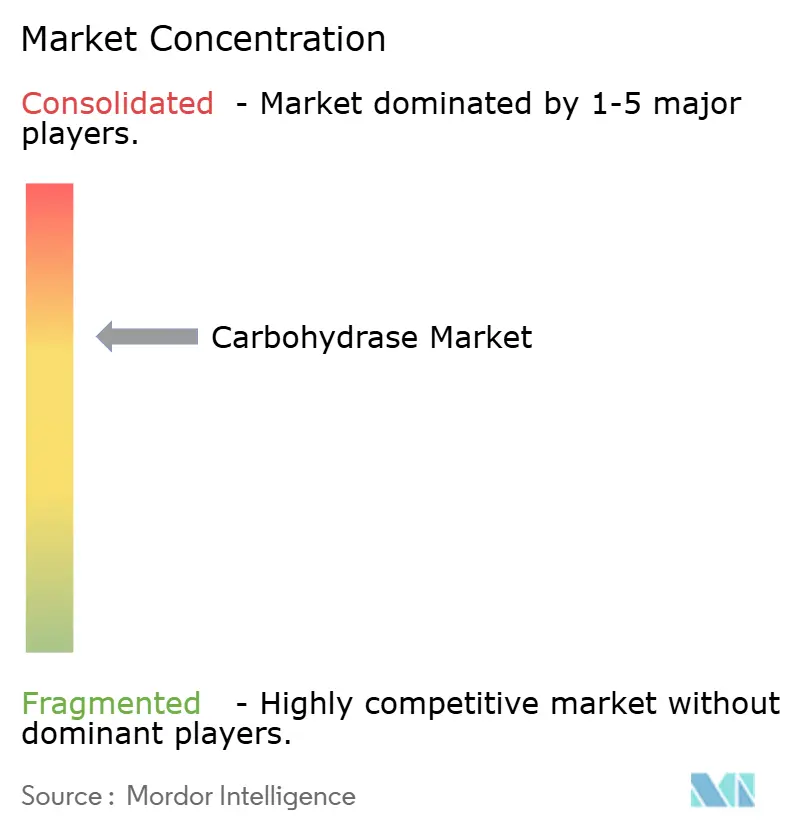

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbohydrase Market Analysis by Mordor Intelligence

The Carbohydrase market size is projected to be USD 2.02 billion in 2025, USD 2.22 billion in 2026, and reach USD 3.04 billion by 2031, growing at a CAGR of 5.57% from 2026 to 2031. Growth in the Carbohydrase market is tied to the food sector’s steady move away from chemical processing aids and toward enzyme-based solutions that support cleaner labels and lower processing intensity. The Carbohydrase market is also benefiting from faster industrialization of food and feed supply chains in developing economies, while mature markets are creating more value through multi-enzyme blends that improve consistency, yield, and formulation control. Another change shaping the Carbohydrase market is the growing overlap between food-grade and therapeutic-grade production, as digestive enzyme applications require stronger compliance systems and raise the entry threshold for smaller manufacturers. Product development speed is also improving, with AI-supported protein design helping major suppliers shorten research cycles and bring more thermostable and application-specific variants to market. Competition remains moderately concentrated, with large integrated biosolutions companies strengthening their reach through distribution control, while input-cost pressure and long approval timelines remain the main limits on expansion

Key Report Takeaways

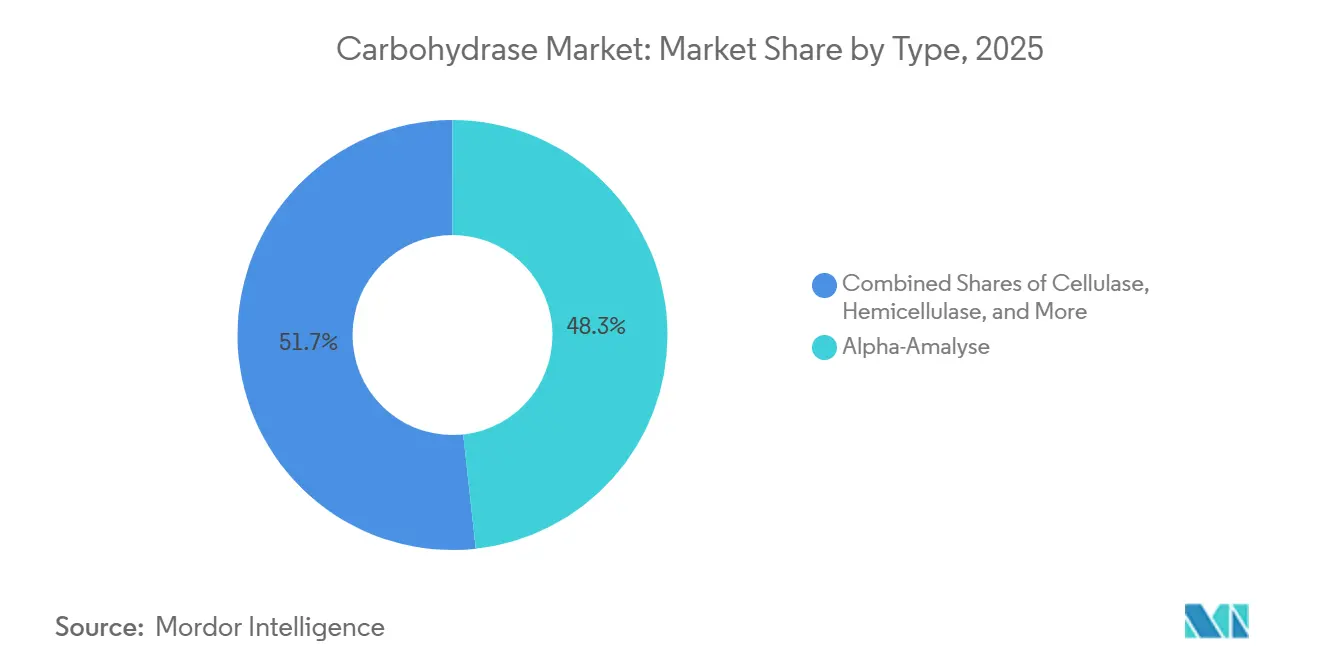

- By type, Alpha Amylase led with a 48.28% share in 2025, while Cellulase was the fastest-growing type through 2031, and Cellulase recorded the highest CAGR at 6.73%.

- By form, Powder held a 51.41% share in 2025, while Liquid recorded the highest projected CAGR at 7.02% through 2031.

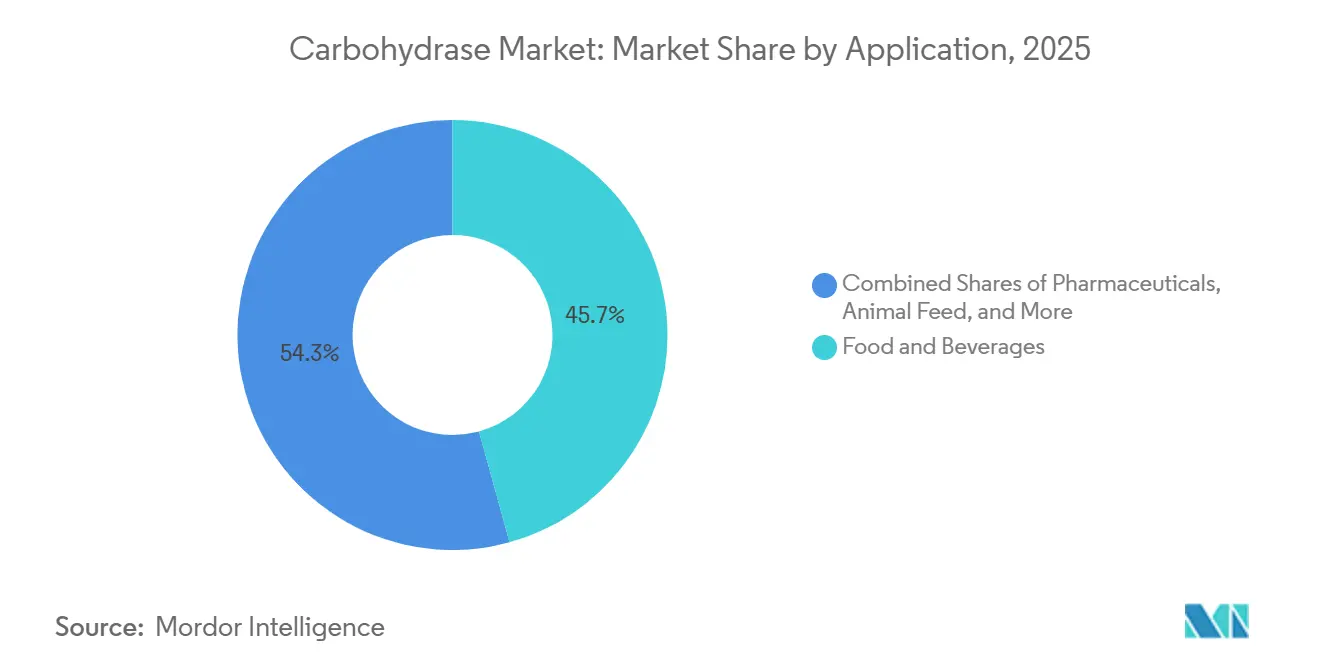

- By application, Food and Beverages accounted for a 45.73% share in 2025, while Pharmaceuticals was the fastest-growing application through 2031, recording a CAGR of 6.45%.

- By geography, North America held a 38.42% share in 2025, while Asia-Pacific recorded the highest projected CAGR at 6.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carbohydrase Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Processed and Convenience Foods | +1.4% | Global, with APAC and South America as primary demand centers | Medium term (2–4 years) |

| Expansion of the Bakery Industry | +1.1% | North America & Europe (mature), APAC (nascent) | Short term (≤ 2 years) |

| Rising Demand for Functional and Specialty Ingredients | +0.8% | North America, Europe | Medium term (2–4 years) |

| Increasing Adoption in Animal Feed Applications | +0.7% | Global, concentrated in APAC and South America | Short term (≤ 2 years) |

| Growing Industrial Applications Beyond Food Processing | +0.5% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Technological Advancements in Enzyme Engineering | +0.7% | North America & Europe (R&D), Global (deployment) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Processed and Convenience Foods

The Carbohydrase market is closely tied to processed food demand because packaged and shelf-stable products require more precise texture control, flavor stability, and shelf-life management. The Carbohydrase market also gains from the continued rise in cereal processing, since starch conversion remains a core step in glucose syrup, sweetener, and related production chains. Global cereal grain output has remained above 2.8 billion tonnes in recent years, providing a large and steady base for starch-processing enzymes such as alpha-amylase and glucoamylase [1]Source: Food and Agriculture Organization of the United Nations, “Cereal Supply and Demand Brief,” fao.org . Processed dairy is adding another layer of demand, especially where lactose-reduced and probiotic-oriented products require more precise enzymatic handling during reformulation. The Carbohydrase market still has room to deepen in Asia-Pacific and Latin America, where food processing systems are formalizing, and enzyme intensity remains below North American and European levels. Large manufacturers are also using optimized enzyme blends to ease input-cost pressure without weakening product quality, which strengthens the economic case for broader adoption.

Expansion of the Bakery Industry

The Carbohydrase market has a strong link to bakery production because alpha-amylase and xylanase remain basic processing tools for dough conditioning, loaf volume improvement, and anti-staling performance. The Carbohydrase market is therefore supported whenever industrial bakeries add capacity or replace chemical improvers with cleaner processing systems. A 2025 review in Foods showed that protein-engineered alpha-amylases are improving thermostability, catalytic efficiency, and reuse potential across bakery and sugar-refining applications. That change matters in North America and Europe, where clean-label reformulation has pushed enzyme blends into roles once held by emulsifiers and chemical dough conditioners. Advanced Enzyme Technologies identified baking solutions as a priority growth area in its FY26 presentation and linked that plan to expansion across Europe, the Americas, and other international markets. The Carbohydrase market also has a longer runway in countries such as India and Vietnam, where industrial bakery capacity is rising, and enzyme penetration is still developing.

Increasing Adoption in Animal Feed Applications

The Carbohydrase market is gaining support from feed applications because xylanase-amylase blends and cellulase preparations help release more usable energy from wheat, corn, and soy-based diets. That makes the Carbohydrase market relevant not only to feed cost control, but also to digestion efficiency and gut-health management in poultry and swine systems. Novonesis placed a EUR 1.5 billion value on acquiring dsm-firmenich’s share of the Feed Enzyme Alliance in 2025, which showed how important scale and direct market access have become in feed enzymes. Thermostable enzyme systems have also improved the practical fit of carbohydrases in pelleted feed, since higher heat tolerance allows inclusion earlier in the process and reduces handling complexity. The Carbohydrase market is seeing especially firm feed demand in Asia-Pacific and South America, where poultry production is large and pressure to reduce antibiotic use is expanding the role of nutritional enzymes. This broadens demand beyond simple energy release and gives suppliers more room to position feed carbohydrases as performance tools.

Technological Advancements in Enzyme Engineering

The Carbohydrase market is changing as enzyme engineering shortens the path from lab design to commercial launch. The Carbohydrase market is also becoming more differentiated because suppliers can now tune pH range, activity profile, and heat tolerance more closely to specific industrial needs. Novonesis reported that AI reduced protein shape prediction time from nearly 1 year to less than 1 minute, helping support 33 new biosolution launches in 2025, with 25% of annual revenue coming from products developed within the previous 5 years. A 2025 study in Polymers showed that directed evolution improved xylanase activity, which has clear relevance for bakery, fiber processing, and biofuel uses. Another 2025 study found that catalytic tunnel engineering improved the rate performance of a thermostable GH7 endoglucanase while preserving operation above 75°C, which supports harder-use industrial settings. A separate 2025 paper identified a glucoamylase that can hydrolyze raw starch at moderate temperatures without gelatinization, which could lower energy demand in starch conversion and improve the cost case for wider adoption in the Carbohydrase market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Development Costs | -0.5% | Global | Medium term (2-4 years) |

| Stringent Regulatory Requirements | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Availability of Alternative Processing Technologies | -0.2% | North America and Europe | Long term (≥ 4 years) |

| Price Sensitivity Among End Users | -0.2% | APAC core, Middle East and Africa, South America | Medium term (2-4 |

| Source: Mordor Intelligence | |||

High Production and Development Costs

The Carbohydrase market remains cost-sensitive because commercial fermentation needs controlled bioreactors, sterile operations, and continuous downstream purification. The Carbohydrase market is also affected by the high share of substrate inputs in operating costs, since glucose syrups, nitrogen sources, and mineral salts can represent 40% to 60% of production expense. That structure favors large manufacturers with fermentation capacity above the scale where unit costs become more competitive with leading market prices. Development costs add another burden because new enzyme preparations require application testing, safety work, and commercial validation before they can earn a place in regulated end uses. Pharmaceutical and digestive supplement channels raise the bar further, since those applications need stronger quality systems than standard food-grade output. The result is a narrower field in higher-value niches, where only a limited group of vertically integrated suppliers can support both compliance and scale.

Stringent Regulatory Requirements

The Carbohydrase market faces slower expansion when suppliers try to launch the same enzyme preparation across food, feed, and therapeutic channels in multiple regions. The Carbohydrase market is especially exposed in Europe, where food enzymes need a positive EFSA opinion before they can move onto the Union List, and that path can take several years. Advanced Enzyme Technologies reported that it had filed 15 enzyme dossiers with EFSA by March 2025, with 9 receiving positive R&D opinions and 6 still under review, which shows how long even established companies must wait. The United States offers a faster route in some cases, but the FDA GRAS process still requires large toxicological and compositional data packages, as seen in the March 2025 closure for AB Enzymes’ fructanase notice[2]Source: U.S. Food and Drug Administration, “GRAS Notice No. GRN 1197, Fructanase Enzyme Preparation, AB Enzymes Inc.,” fda.gov. Different approval speeds across major regions give an advantage to suppliers with dedicated regulatory teams and local infrastructure. That slows the spread of newer performance-improved variants in the Carbohydrase market and raises the burden on mid-sized competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Alpha Amylase Anchors a Diversifying Enzyme Portfolio

Alpha Amylase held 48.28% of the carbohydrase market share in 2025, reflecting its central role in starch liquefaction across bakery, brewing, glucose-syrup production, and biofuel feedstock processing. The Carbohydrase market continues to lean on this enzyme type because those end uses sit at the core of global food and industrial carbohydrate conversion. A 2025 review in Foods described how directed evolution, semi-rational design, and immobilization methods are improving alpha-amylase stability and efficiency in food processing. A 2024 review published through PMC showed that xylanase reduces arabinoxylan viscosity in poultry diets and also supports juice clarification, which explains its broad commercial relevance. Pectinase kept its place through juice clarification and wine processing, with adoption growing in fruit-processing markets across Asia and South America. Hemicellulase also gained importance in multi-enzyme bakery blends where it works with alpha-amylase and xylanase to improve dough behavior and crumb structure. Disaccharidase preparations, including lactase and sucrase, added relevance in dairy and confectionery processing as lactose-free and specialized nutrition formats expanded. The broader Carbohydrase market therefore remains anchored by high-volume starch enzymes, but it is steadily diversifying into more application-specific portfolios. That shift makes the type mix more balanced over time without weakening alpha-amylase’s lead position.

Cellulase was the fastest-growing type through 2031, recording a CAGR of 6.73%. The Carbohydrase market is drawing more cellulase demand from renewable fuels because lignocellulosic feedstocks need effective saccharification before conversion. The U.S. Energy Information Administration reported in 2024 that U.S. biofuel production capacity rose by 7% to nearly 24 billion gallons per year, which supports the need for biomass-conversion enzymes[3]Source: U.S. Energy Information Administration, “U.S. Biofuel Production Capacity Report,” eia.gov.. In digestive health, cellulase-containing formulations are appearing more often in over-the-counter enzyme products, where value per unit is higher than in bulk industrial use. This gives the Carbohydrase industry another path to growth beyond large-volume food conversion. It also means that future type expansion will depend not only on scale, but also on how well suppliers can meet different quality and application standards. The Carbohydrase market is therefore seeing faster growth in types that connect industrial processing with health-oriented end uses.

By Form: Powder Commands Volume as Liquid Grows Fastest

Powder accounted for 51.41% of the global Carbohydrase market in 2025, showing its continued strength in bakery premixes, compound feed blending, and supply chains that need stable dry formulations. The Carbohydrase market still depends heavily on powder because dry formats are easier to store, transport, and dose in large batch operations. Spray-dried and lyophilized powders support precise activity levels in flour milling and feed manufacturing, where consistent enzyme performance per kilogram of substrate matters. Granules serve a more specialized role in the Carbohydrase market, especially in feed pelleting, where dust control, release behavior, and workplace handling standards matter more. Powder and granule forms also keep a cost edge in large-scale starch and sweetener processing when liquid precision is not essential. That cost advantage helps protect the installed base of dry forms even as processing lines become more automated. The Carbohydrase market therefore keeps powder at the center of volume demand, while granules support targeted operating needs in selected applications. This balance reflects the fact that form choice is usually driven by plant workflow and storage conditions rather than enzyme type alone. It also explains why dry products remain deeply embedded in long-haul and high-throughput industrial systems.

Liquid is projected to record the fastest growth at 7.02% CAGR through 2031 in the Carbohydrase market size mix by form. The Carbohydrase market is pulling more liquid demand from continuous baking, brewing, and starch-processing systems because automated dosing improves control and reduces variability. Liquid formulations remove the dust-handling and dispersion steps needed with powders, which makes them easier to integrate into real-time process management. Pharmaceutical and digestive supplement channels reinforce this trend because liquid enzyme formats are often preferred where fast dissolution and easier oral delivery matter. As a result, the Carbohydrase market is likely to see liquids gain share fastest in facilities that prioritize automation, dosing accuracy, and formulation responsiveness. Even so, liquid growth does not displace powders across the board, because many bulk users still prefer the lower handling complexity of dry supply. That leaves the form mix of the Carbohydrase market split between volume efficiency in powder and process precision in liquid. The outcome is a more application-led form structure rather than a simple shift from one format to another.

By Application: Food and Beverages Lead as Pharmaceutical Pull Strengthens

Food and Beverages accounted for 45.7% of the carbohydrase market size in 2025. The Carbohydrase market depends on this segment because bakery, starch processing, brewing, and juice clarification represent the broadest and most established demand base. Bakery remains the single most important pull within this group, especially as producers in Europe and North America replace chemical dough conditioners with enzyme-led clean-label systems. That scale shows how deeply the Carbohydrase market is tied to everyday food production rather than a narrow specialty niche. Animal Feed remained an adjacent demand center, where xylanase-amylase blends improve digestibility and gut-health outcomes in commercial livestock systems. Biofuel and biorefinery use added another structural support line because cellulase remains central to cellulosic ethanol processing from residues and energy crops. The Carbohydrase market therefore continues to draw most of its revenue from food-linked uses, even as adjacent sectors expand. This gives the application a mix of stability and room for gradual diversification.

Pharmaceuticals was the fastest-growing application through 2031, recording a CAGR of 6.45%. The Carbohydrase market is entering a higher-value channel here because prescription and health-focused applications carry tighter compliance requirements and stronger unit economics than bulk processing uses. Pancreatic Enzyme Replacement Therapy includes amylase as a core component, and growing diagnosis of exocrine pancreatic insufficiency is supporting prescription demand in North America and Europe. Beyond prescription use, over-the-counter products containing alpha-galactosidase, lactase, and fructanase are moving further into mainstream retail, supported in part by Health Canada’s updated digestive enzyme monograph in December 2025. This is changing the Carbohydrase market by creating a split between large-volume industrial demand and smaller but more valuable therapeutic-grade demand. Suppliers that can serve both channels are better placed to widen margins and defend product differentiation. Suppliers focused only on low-cost bulk output may find it harder to participate in this faster-growing application path. The Carbohydrase market is therefore becoming more layered by application quality standards as much as by end-use volume. That shift is one of the clearest reasons pharmaceuticals is gaining attention within the broader growth story.

Geography Analysis

North America held 38.42% of the carbohydrase market share in 2025. The Carbohydrase market in North America is supported by a large industrial bakery base, a mature starch-sweetener sector, and an FDA GRAS framework that gives suppliers a workable path for novel enzyme commercialization. Recent FDA closures for AB Enzymes’ fructanase preparation in March 2025 and BASF’s beta-mannanase notice for swine feed in July 2025 show that the region is still active in product approvals. The Carbohydrase market also benefits from close working links between enzyme manufacturers and large food producers, which helps speed commercial deployment after approval. South America remained smaller in revenue, but the market pointed to stronger biofuel-linked demand through Brazil’s renewable fuel push and to growing food-processing investment in Chile, Colombia, and Peru. That combination gives the Carbohydrase market in South America a useful mix of fuel, beverage, fruit-processing, and animal nutrition demand. Even so, enzyme intensity per person still trails North America, which leaves room for future adoption gains as local processing scales up.

Europe remained a core revenue region in the Carbohydrase market, but its pace is shaped by strict authorization rules and long review timelines. The Carbohydrase market in Europe therefore rewards suppliers that can sustain larger regulatory investments over several years. The region also benefits from policy support for bio-based production and for lower reliance on chemical food additives, which strengthens the case for enzyme alternatives in bakery, juice, and dairy processing. Advanced Enzyme Technologies reported 15 EFSA filings by early 2026, with 9 positive R&D opinions, which highlights the level of commitment required to stay active in Europe. The Carbohydrase market in smaller European countries such as Poland and Belgium is also moving forward as bakery and flour-milling systems modernize. This means Europe remains important not because it is easy to enter, but because it sets high standards that can favor established and technically capable suppliers.

Asia-Pacific is projected to expand at 6.65% CAGR through 2031, making it the fastest-growing regional block in the Carbohydrase market size outlook. The Carbohydrase market in this region is being driven by rapid industrialization of food and feed supply chains in China, India, Vietnam, and wider Southeast Asia. It also noted that Advanced Enzyme Technologies recorded a 22% year-on-year rise in Animal Nutrition revenue and a 16% increase in food bio-processing revenue in Q3 FY26, reflecting stronger demand across South Asian markets. The Carbohydrase market in the Middle East and Africa remained the smallest by revenue, yet food-processing investment in the UAE, Saudi Arabia, and South Africa is creating a broader base for starch and bakery enzymes. North African countries such as Morocco and Egypt were described as early-stage adopters, with growth linked to flour-milling expansion and local processing by international food manufacturers. This leaves the Carbohydrase market with its fastest growth profile in Asia-Pacific, while the Middle East and Africa develops from a smaller base through capacity-building in food manufacturing.

Competitive Landscape

The Carbohydrase market shows moderate-to-high concentration, with Novonesis A/S, IFF, and BASF holding strong positions in large-volume starch, bakery, and feed enzyme segments. The Carbohydrase market is not fully consolidated, though, because specialist suppliers such as AB Enzymes, Advanced Enzyme Technologies, and SUNSON Industry Group still compete through product focus, regional cost advantages, and selected regulatory coverage. Novonesis strengthened its position in 2025 by completing the acquisition of dsm-firmenich’s share of the Feed Enzyme Alliance, taking over full sales and distribution responsibility for that portfolio. That move showed that control over commercial channels now matters as much as manufacturing scale in feed enzymes. The Carbohydrase market is also creating space in higher-value areas, especially where digestive applications and more heat-stable industrial uses require stronger technical performance than standard fermentation output can deliver.

Competitive behavior in the Carbohydrase market is increasingly centered on portfolio breadth, regulatory depth, and the ability to combine enzyme performance with downstream application support. IFF and BASF moved in that direction in October 2025 through a strategic collaboration that joined IFF’s Designed Enzymatic Biomaterials platform with BASF’s polymer and chemistry capabilities. That partnership suggests the Carbohydrase market is shifting from competition based on single preparations toward competition based on broader systems and use-case performance. Advanced Enzyme Technologies also expanded its quality and testing base through Staria Labs under its U.S. subsidiary, supporting more analytical infrastructure for enzyme and probiotic products. These moves show that suppliers are investing not only in production, but also in validation, customer support, and technical differentiation.

Asian manufacturers are adding pressure in the Carbohydrase market, especially where cost-competitive fermentation and region-specific commercial strategies can win business in volume applications. SUNSON Industry Group described its approach in 2025 through a “Four-New” strategy focused on new enzymes, new applications, new market segments, and new geographies. The Carbohydrase market is therefore seeing stronger competition from producers that are no longer limited to commodity supply and are instead building broader global positions. At the same time, the suppliers best placed for the next phase are those that can combine large fermentation systems, downstream purification, and credible regulatory execution across regions. This keeps the Carbohydrase market open enough for regional challengers to grow, but still tilted toward integrated players in the most valuable segments. Companies with only single-site production and narrow portfolios may face margin pressure as bulk pricing tightens. The result is a market where scale still matters, but scale alone is no longer enough without technical and regulatory depth.

Carbohydrase Industry Leaders

Novonesis A/S

BASF SE

International Flavors and Fragrances Inc.

Archer Daniels Midland Company

Advanced Enzyme Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Novonesis received full EU label registration for its next-generation phytase HiPhorius, expanding authorization to all monogastric species, including laying hens, breeding poultry, piglets, and fattening pigs, beyond the prior restricted authorization. The expansion enables feed producers to deploy a single, high-efficiency phytase solution across multi-species operations, improving feed conversion ratios and reducing inorganic phosphorus supplementation across the feed value chain.

- October 2025: IFF and BASF announced a strategic collaboration to develop next-generation enzyme technologies, combining IFF's Designed Enzymatic Biomaterials™ platform — which includes carbohydrases for animal nutrition and food processing — with BASF's chemistry and polymer engineering expertise. The partnership targets performance-superior enzyme systems and biobased polymers for fabric, dish, personal care, industrial cleaning, and animal nutrition applications.

- June 2025: Novonesis completed the acquisition of dsm-firmenich's share of the Feed Enzyme Alliance following all regulatory approvals, assuming full sales and distribution responsibilities for the alliance's animal feed and gut health enzyme portfolio globally. The transaction, valued at EUR 1.5 billion (approximately USD 1.61 billion at the 2025 average EUR/USD rate of 1.07), substantially extends Novonesis's direct-to-market reach in carbohydrase-heavy animal nutrition.

Global Carbohydrase Market Report Scope

| Alpha Amalyse |

| Xylanases |

| Pectinase |

| Hemicellulase |

| Cellulase |

| Disaccharidase |

| Others |

| Liquid |

| Powder |

| Granuels |

| Food and Beverages |

| Pharmaceuticals |

| Animal Feed |

| Bifuel and Biorefinaries |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Alpha Amalyse | |

| Xylanases | ||

| Pectinase | ||

| Hemicellulase | ||

| Cellulase | ||

| Disaccharidase | ||

| Others | ||

| By Form | Liquid | |

| Powder | ||

| Granuels | ||

| By Application | Food and Beverages | |

| Pharmaceuticals | ||

| Animal Feed | ||

| Bifuel and Biorefinaries | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for the Carbohydrase market?

The Carbohydrase market is projected at USD 2.22 billion in 2026 and is expected to reach USD 3.04 billion by 2031, growing at a 5.57% CAGR over 2026 to 2031.

Which enzyme type leads global demand in carbohydrases?

Alpha Amylase led demand with 48.28% share in 2025 because it is widely used in starch liquefaction, bakery, brewing, and glucose-syrup processing.

Why is Asia-Pacific gaining attention in carbohydrases?

Asia-Pacific is the fastest-growing region with a 6.65% CAGR through 2031, supported by food and feed processing expansion across China, India, Vietnam, and Southeast Asia.

What is driving pharmaceutical use of carbohydrases?

Pharmaceutical demand is rising because digestive enzyme therapies and retail supplement products are expanding, and regulators such as Health Canada updated guidance in 2025 that supports commercialization.

Page last updated on: