Market Overview

| Study Period | 2021 - 2031 |

|---|---|

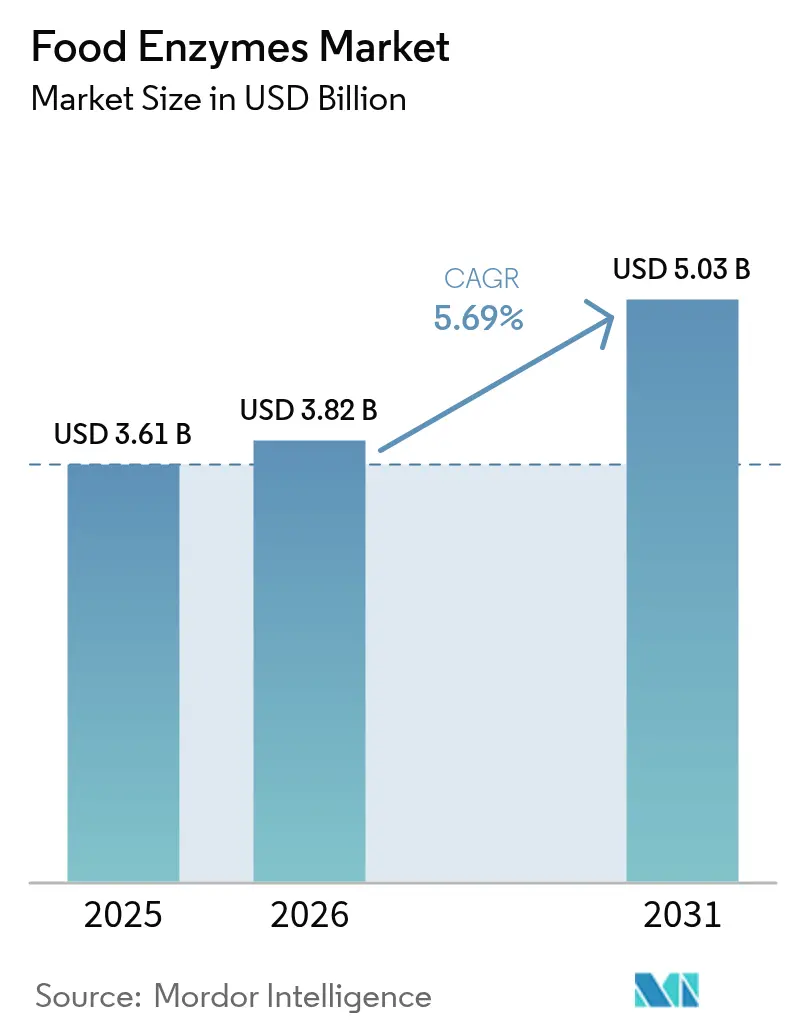

| Market Size (2026) | USD 3.82 Billion |

| Market Size (2031) | USD 5.03 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

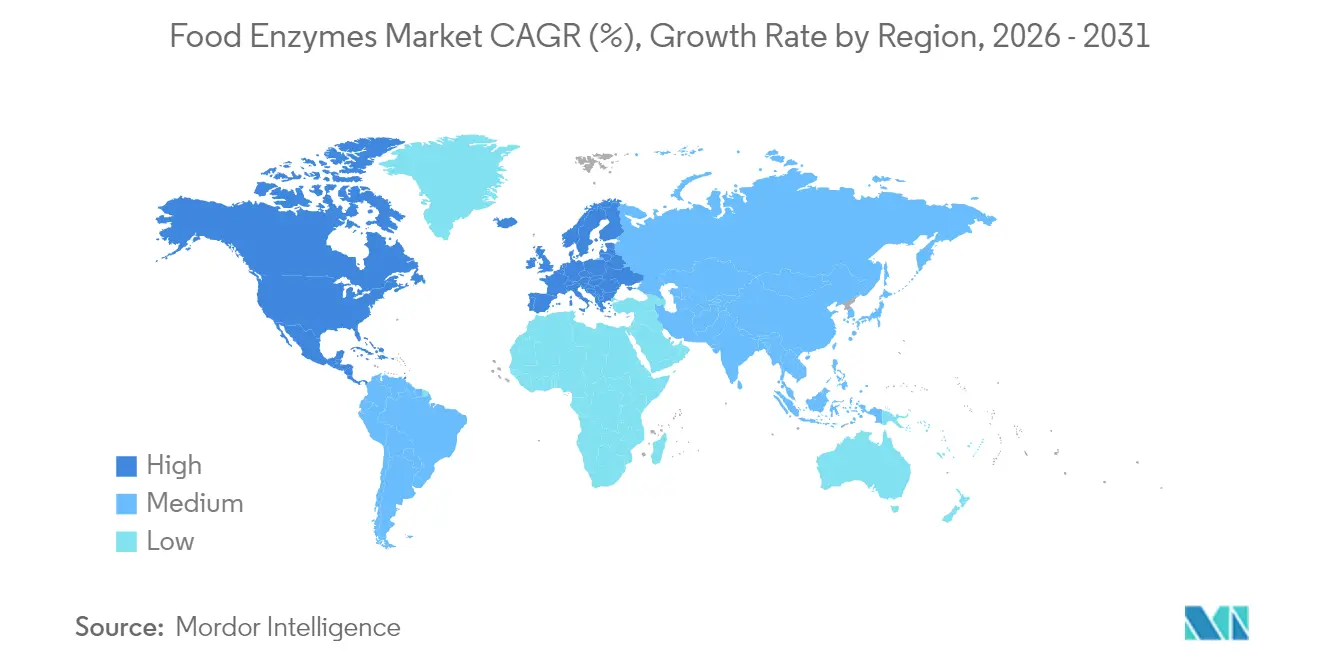

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Enzymes Market Analysis by Mordor Intelligence

The food enzymes market size is expected to grow from USD 3.61 billion in 2025 to USD 3.82 billion in 2026 and is forecast to reach USD 5.03 billion by 2031 at 5.69% CAGR over 2026-2031. This growth highlights the increasing importance of biotechnology solutions in mainstream food manufacturing processes. The rising demand for clean-label products, the growing adoption of sustainable processing technologies, and a stronger focus on extending the shelf life of food products have made enzyme systems essential rather than optional. These systems are now widely used across various food categories, including bakery, dairy, beverages, and plant-based foods. Regionally, North America continues to dominate in terms of revenue, driven by established food processing industries and consumer preferences. Meanwhile, the Asia-Pacific region is experiencing the fastest growth, supported by rapid urbanization, an expanding middle class with higher disposable incomes, and ongoing investments in food processing infrastructure. Additionally, the industry is witnessing consolidation as major players focus on achieving economies of scale, enhancing their research and development capabilities, and adopting digital manufacturing technologies. These efforts aim to address increasingly stringent regulatory requirements and meet sustainability goals effectively.

Key Report Takeaways

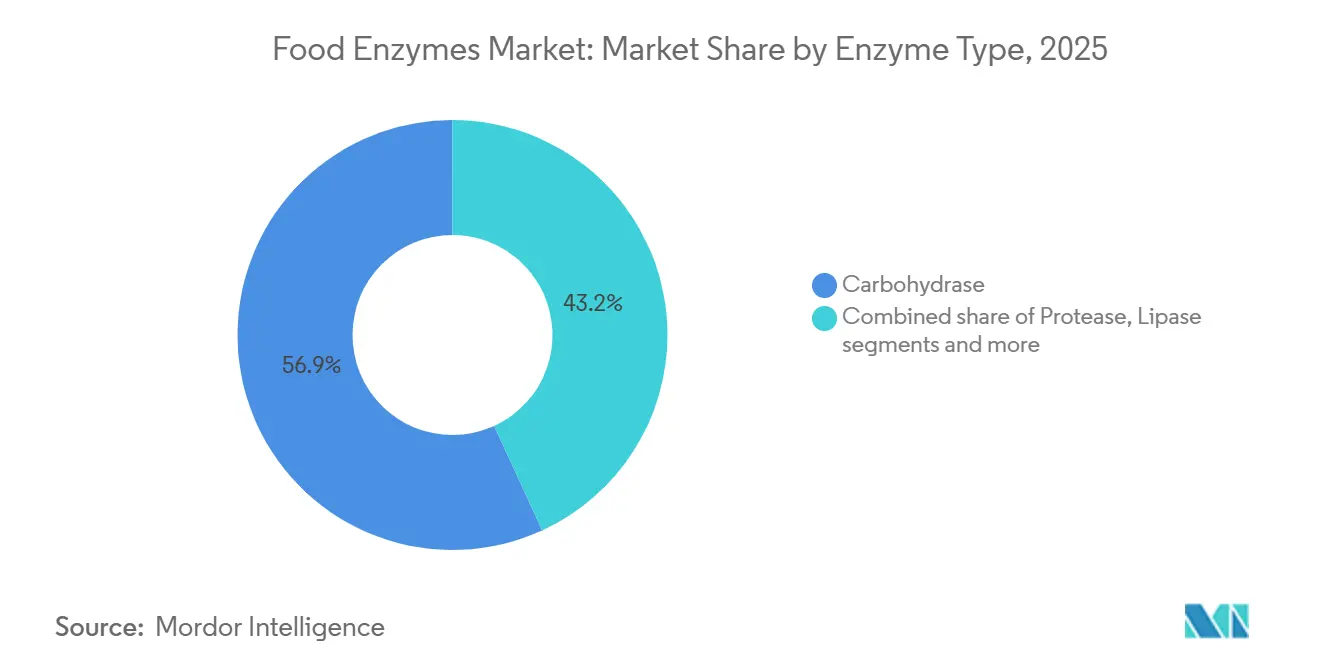

- By type, carbohydrase enzymes led with 56.85% of food enzymes market share in 2025, while lipase posted the fastest 6.72% CAGR to 2031.

- By form, powder formulations commanded 67.72% share of the food enzymes market size in 2025 and are projected to expand at 6.18% CAGR between 2026 and 2031.

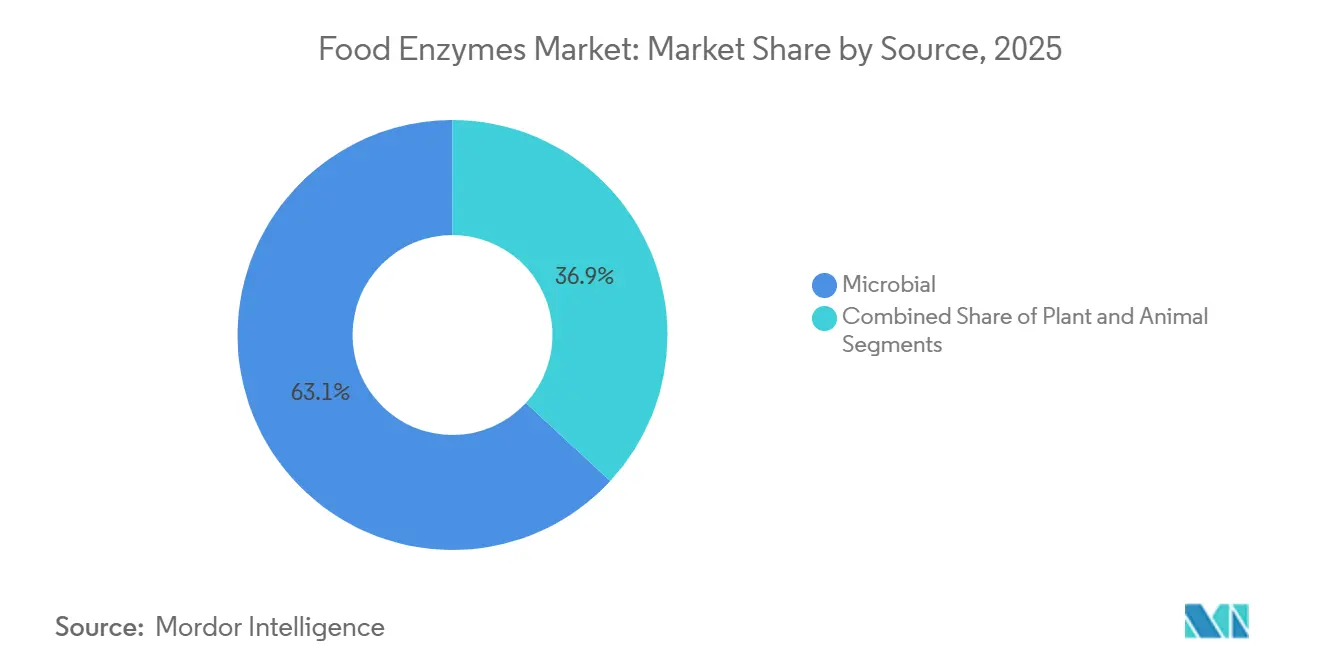

- By source, microbial production held 63.12% of the food enzymes market share in 2025; plant-based sources exhibit a 6.55% CAGR outlook through 2031.

- By application, bakery and confectionery accounted for 28.55% of the food enzymes market size in 2025, whereas dairy and desserts are advancing at a 7.02% CAGR.

- By geography, North America retained 33.25% market share in 2025; Asia-Pacific is set to grow at a 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Food Enzymes Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increased enzyme use in bakery industry for dough conditioning and shelf-life extension | +1.20% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Enhanced efficiency and yield in food manufacturing using enzymes | +1.00% | Global, particularly Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Accelerated demand for gluten-free and plant-based products driving enzyme use | +0.90% | North America and Europe primary, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Surging demand for carbohydrase in sugar syrup and beverage production | +0.80% | Global, with strong growth in Asia-Pacific beverage markets | Medium term (2-4 years) |

| Use of enzymes for improving food texture and palatability | +0.70% | Global, led by North America premium food segments | Medium term (2-4 years) |

| Consumer shift towards lactose-free and digestive health products | +0.70% | North America and Europe mature markets, Asia-Pacific emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased enzyme use in bakery industry for dough conditioning and shelf-life extension

The increasing use of enzymes in the bakery industry is a key driver of the market. Enzymes, such as amylases and proteases, are widely utilized for dough conditioning, improving texture, and extending the shelf life of baked goods. According to the United States Department of Agriculture (USDA), the global demand for processed and packaged bakery products has been steadily rising, driven by changing consumer preferences and the need for convenience. Additionally, the American Bakers Association highlights that enzymes play a crucial role in reducing production costs and enhancing product quality, making them indispensable for modern bakery operations. This trend is expected to continue during the forecast period, as manufacturers increasingly adopt enzyme-based solutions to meet consumer demands for high-quality and longer-lasting bakery products.

Enhanced efficiency and yield in food manufacturing using enzymes

The use of enzymes in food manufacturing has emerged as a significant driver in the Global Food Enzymes Market. Enzymes enhance production efficiency and improve yield, enabling manufacturers to optimize processes and reduce waste. According to the Food and Agriculture Organization, the global food production system faces increasing pressure to meet the demands of a growing population, making efficiency improvements critical. The U.S. Department of Agriculture (USDA) has also emphasized the role of enzymes in improving food quality and shelf life, which is crucial for reducing food loss across supply chains. These advancements not only support cost reduction but also align with environmental sustainability objectives, further driving the adoption of enzymes in the food industry. Furthermore, the European Food Safety Authority has approved several enzyme applications, reflecting the growing regulatory support for their use in food processing [1]European Food Safet Authority, "Food Enzymes-January 2025", www.efsa.europa.eu. This regulatory backing, combined with the increasing focus on sustainable and efficient production, is expected to propel the growth of the food enzymes market during the forecast period.

Accelerated demand for gluten-free and plant-based products driving enzyme use

Plant-based food formulations increasingly rely on sophisticated enzyme systems to overcome inherent limitations in texture, flavor, and nutritional profiles that historically hindered consumer acceptance. Enzymatic modification of pea and chickpea proteins through targeted protease treatments enhances functionality and reduces off-flavors, addressing key barriers to mainstream adoption of plant-based alternatives. AI-driven prediction models for plant protein flavor biotransformation enable manufacturers to optimize fermentation processes using specific enzyme combinations, significantly improving sensory attributes of plant-based products. The development of precision fermentation techniques for producing animal-free proteins demonstrates enzymes' critical role in creating dairy and meat alternatives that closely replicate traditional products' functional properties. Novonesis's launch of Vertera® Umami MG in 2024 exemplifies this trend, as the enzyme specifically enhances umami flavors in plant-based foods, addressing taste challenges that previously limited market penetration.

Surging demand for carbohydrase in sugar syrup and beverage production

The increasing demand for carbohydrase in sugar syrup and beverage production is a significant driver of the Global Food Enzymes Market. Carbohydrase enzymes play a crucial role in breaking down carbohydrates into simpler sugars, which are essential in the production of syrups and beverages. According to the United States Department of Agriculture (USDA), the global consumption of sugar-based products has been steadily increasing, driven by the growing demand for processed foods and beverages [3]U.S. Department of Agriculture, "Sugar and Sweeteners", www.ers.usda.gov. International Food Additives Council, emphasize the importance of enzymes like carbohydrase in enhancing production efficiency and product quality. The adoption of carbohydrase is also supported by its ability to meet the rising consumer preference for natural and clean-label products. This trend aligns with the broader shift in the food and beverage industry toward sustainable and health-conscious production practices. As a result, the carbohydrase segment is expected to witness robust growth during the forecast period, driven by its critical applications in sugar syrup and beverage manufacturing.

Restraints Impact Analysis of Food Enzymes Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent regulatory approvals and labeling restrictions | -0.70% | Global, particularly stringent in Europe and North America | Long term (≥ 4 years) |

| Sensitivity of enzymes to temperature, pH, and processing conditions | -0.50% | Global manufacturing operations | Medium term (2-4 years) |

| Inconsistent performance across different substrate sources | -0.50% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Intellectual property and patent-related disputes in enzyme technology | -0.30% | North America and Europe primary litigation markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory approvals and labeling restrictions

Regulatory complexity intensifies as authorities implement more rigorous safety assessments for enzyme applications, creating significant barriers for market entry and product innovation timelines. The European Union's enhanced transparency requirements under Regulation 2020/1823 mandate public disclosure of scientific data supporting enzyme applications [2]European Union, "COMMISSION IMPLEMENTING REGULATION (EU) 2020/1823" , www.eur-lex.europa.eu , extending approval processes and increasing compliance costs for manufacturers. FDA GRAS notifications declined in 2024, with only 13 substances approved from 57 submissions, reflecting stricter review requirements that particularly impact enzyme preparations and microbial-related products. The requirement for comprehensive safety dossiers, including characterization of production microorganisms and detailed exposure assessments, creates substantial financial and technical barriers for smaller enzyme manufacturers. China's updated GB 2760-2024 standard, effective February 2025, introduces new use principles for food additives and processing aids, requiring manufacturers to navigate evolving regulatory frameworks across major markets. These regulatory developments, while ensuring safety, create market access challenges that particularly affect innovative enzyme applications and emerging biotechnology companies.

Sensitivity of enzymes to temperature, pH, and processing conditions

Enzyme stability limitations under industrial processing conditions constrain application scope and require sophisticated formulation strategies that increase production complexity and costs. The inherent sensitivity of enzymes to thermal processing, pH variations, and mechanical stress during food manufacturing necessitates protective formulation techniques and controlled storage conditions that add operational overhead. Research demonstrates that while enzymatic tenderization effectively improves meat texture, treatments can lead to increased cooking loss and require careful optimization to maintain product quality. The development of enzyme immobilization technologies and protective coating systems addresses some stability concerns but introduces additional manufacturing steps and cost considerations. Advanced biotechnology approaches, including strain mutagenesis and genome editing, show promise for enhancing enzyme stability and activity, though these solutions require significant research and development investment and regulatory approval. The challenge becomes particularly acute in high-temperature processing applications where enzyme deactivation can occur, limiting their effectiveness in certain food manufacturing processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Food Enzymes Market Segment Analysis

By Enzyme Type:

Carbohydrase Dominance Drives Processing InnovationCarbohydrase enzymes retained 56.85% of food enzymes market share in 2025, cementing their status as workhorses for starch hydrolysis, sugar conversion, and texture modulation. Within this cluster, amylase dominates bakery and brewing, while pectinase and cellulase gain visibility in fruit and plant-protein streams. Lipase, though smaller, is projected to rise at 6.72% CAGR, reflecting its expanding role in dairy fat modification and vegan flavor-release solutions. Multi-enzyme cocktails that blend carbohydrase with protease or lipase streamline complex recipes, reducing SKUs and optimizing plant efficiencies.

The food enzymes market size attached to carbohydrase applications continues to swell as beverage producers scale high-fructose syrup alternatives and confectioners target sugar-reduction mandates. Simultaneously, protein-rich snacks and sports drinks incorporate protease-aided hydrolysates for digestibility and mouthfeel gains. Innovation clusters around hybrid enzymatic routes that unlock novel textures, filling gaps previously addressed by synthetic additives.

By Form:

Powder Formulations Lead Market AdoptionPowder variants dominated the food enzymes market in 2025, securing 67.72% of the market share and charting a steady 6.18% CAGR trajectory. Their low moisture content and extended shelf life, combined with seamless compatibility with automated feeders, bestow powders with distinct logistical advantages. Techniques like advanced spray-drying and encapsulation ensure activity is preserved during storage. These methods protect the enzymes from environmental factors such as humidity and temperature fluctuations, maintaining their efficacy over time. Moreover, controlled-release coatings activate the enzymes only under specific pH or temperature conditions, ensuring precision and efficiency in various food processing applications.

While liquid enzymes play a crucial role in beverage and dairy lines, where instant dispersion is paramount, powders are poised to extend their dominance, especially as cold-chain expenses escalate. The global pivot towards smart factories further bolsters the case for dry formulations, which not only reduce contamination risks but also enhance closed-loop material handling. Smart factories increasingly rely on automation and advanced technologies, making powders an ideal choice due to their compatibility with such systems. As a result, powder-based solutions are set to play a pivotal role in the food enzymes market's future growth, driving innovation and efficiency in food production processes.

By Source:

Microbial Production Scales with Sustainability FocusIn 2025, microbial fermentation dominated the food enzymes market, capturing a 63.12% share. This dominance is attributed to established production platforms, scalable yields, and a straightforward regulatory classification, which collectively make microbial fermentation a preferred choice for enzyme production. Breakthroughs in synthetic biology empower producers to refine microbial strains, achieving higher titers, a wider pH range, and independence from co-factors. These advancements enable manufacturers to optimize production efficiency and cater to diverse industrial applications. While plant-based enzymes start from a smaller base, they're growing at a robust 6.55% CAGR, driven by brands pursuing vegan, kosher, and halal certifications to meet the rising demand for ethically and religiously compliant products.

Precision fermentation, which produces animal-identical enzymes without relying on livestock, not only fills functional gaps but also meets ethical sourcing standards. This innovative approach allows manufacturers to replicate the functionality of animal-derived enzymes while addressing sustainability concerns. Investments, such as BASF’s Kundl expansion, underscore the industry's confidence in scaling up the microbial route. This momentum not only aligns with corporate net-zero commitments but also resonates with a climate-conscious consumer base, ensuring the food enzymes market remains pertinent. Additionally, such developments highlight the industry's proactive approach to addressing environmental challenges while maintaining product quality and functionality.

By Application:

Bakery Leadership Faces Dairy DisruptionIn 2025, bakery and confectionery sectors command a significant 28.55% share of the food enzymes market, buoyed by consistent bread consumption and a swift rise in gluten-free products. The demand for gluten-free options continues to grow as consumers increasingly prioritize health and dietary preferences, further solidifying this segment's dominance. However, the dairy and dessert segment is projected to lead all categories with a robust 7.02% CAGR. This growth is largely attributed to lactase conversions, paving the way for lactose-free milks, yogurts, and ice creams. The rising prevalence of lactose intolerance and the growing consumer preference for lactose-free alternatives are key drivers of this trend. Notably, Kerry Group's EUR 150 million acquisition of lactase highlights the burgeoning commercial interest and the strategic focus on expanding capabilities in this area.

Beverages are riding the wave, with craft brewers, juice brands, and new low-sugar soda entrants turning to specialized carbohydrase portfolios. The increasing demand for innovative and healthier beverage options has prompted manufacturers to adopt tailored enzyme solutions to enhance product quality and meet consumer expectations. Meanwhile, meat processors are harnessing protease and transglutaminase not just to tenderize cuts but also to enhance their plant-protein hybrid offerings. This dual application addresses the growing demand for both traditional meat products and plant-based alternatives. Additionally, emerging niches like soups, sauces, and dressings are tapping into enzyme capabilities for flavor enhancement and viscosity management, presenting new opportunities in the food enzymes market. These applications cater to evolving consumer tastes and the need for improved product functionality, further driving market growth.

Geography Analysis

North America's 33.25% market share in 2025 reflects the region's advanced food processing infrastructure and established regulatory frameworks that facilitate enzyme adoption across multiple applications. The United States leads regional demand, driven by large-scale food manufacturing operations and consumer preferences for clean-label products that rely on enzyme technology. Canada contributes significantly through its grain processing and dairy industries, while Mexico's growing food processing sector creates expansion opportunities. The region's emphasis on food safety and quality standards creates favorable conditions for enzyme adoption, though regulatory complexity can extend product development timelines.

Asia-Pacific emerges as the fastest-growing region with 6.84% CAGR through 2031, propelled by rapid urbanization and expanding processed food consumption across major economies, including China, India, and Japan. China's food enzyme market benefits from government support for biotechnology development and updated regulatory standards that streamline market access for innovative products. India's growing food processing sector and increasing consumer awareness of health and nutrition drive enzyme adoption in traditional and modern food applications. Japan's advanced food technology sector leads innovation in specialized enzyme applications, particularly in fermented foods and functional ingredients. The region's demographic trends, including aging populations and rising health consciousness, create sustained demand for enzyme-enhanced foods that address specific nutritional and digestive needs.

Europe maintains steady growth supported by stringent quality standards and sustainability initiatives that favor enzyme-based processing solutions over chemical alternatives. The European Food Safety Authority's introduction of the Food Enzyme Intake Model (FEIM) in 2024 streamlines dietary exposure assessments while maintaining rigorous safety standards. Germany and France lead regional enzyme consumption through their advanced food processing industries, while the United Kingdom's focus on food innovation creates opportunities for specialized enzyme applications. The region's emphasis on sustainability and environmental protection drives adoption of enzyme technologies that reduce energy consumption and chemical usage in food manufacturing. South America and Middle East and Africa represent emerging markets with significant long-term potential, though current growth remains constrained by infrastructure development and regulatory framework establishment.

Competitive Landscape

The food enzymes market exhibits moderate concentration, indicating significant consolidation opportunities amid ongoing industry transformation. The competitive landscape is characterized by the presence of a mix of global leaders and regional players, including Novozymes A/S, BASF SE, Kerry Group PLC, DSM-Firmenich, and International Flavors & Fragrances Inc., each adopting distinct strategies to strengthen their market position. Market leaders focus on vertical integration and geographic expansion to harness value throughout the enzyme supply chain. These companies invest heavily in research and development to innovate and introduce advanced enzyme solutions, catering to a wide range of applications in the food and beverage sector. Additionally, partnerships, mergers, and acquisitions are common strategies employed by these players to expand their product portfolios and enhance their global reach.

Mid-tier players, on the other hand, concentrate on specialized applications and regional market penetration. These companies often target niche segments, offering tailored enzyme solutions to meet specific customer requirements. By leveraging their understanding of local markets, they aim to establish a strong foothold and compete effectively with larger players. Furthermore, collaborations with local distributors and food manufacturers enable mid-tier companies to expand their customer base and enhance their market presence.

Strategic trends spotlight technology-led differentiation and tailored solutions, catering to the shifting demands of customers prioritizing clean-label and sustainable food processing. A growing number of companies are harnessing artificial intelligence and automated enzyme engineering, not just to hasten product development but also to fine-tune performance traits for distinct applications. The adoption of these advanced technologies allows companies to optimize enzyme functionality, improve production efficiency, and reduce costs, thereby gaining a competitive edge in the market.

Food Enzymes Industry Leaders

-

Novozymes A/S

-

International Flavors & Fragrances Inc.

-

DSM-Firmenich

-

BASF SE

-

Kerry Group PLC

- *Disclaimer: Major Players sorted in no particular order

Food Enzymes Market Companies Covered in this Report

- Novozymes A/S

- International Flavors & Fragrances Inc.

- BASF SE

- Associated British Foods plc

- Kerry Group plc

- DSM-Firmenich AG

- Advanced Enzyme Technologies Ltd.

- Amano Enzyme Inc.

- Enzyme Development Corporation

- Archer Daniels Midland Company

- Biocatalysts Ltd.

- Corbion N.V.

- Lumis Biotech Pvt. Ltd.

- Aumgene Biosciences.

- Jiangsu Boli Bioproducts Co., Ltd.

- Bioseutica B.V.

- Maps Enzymes Ltd.

- Sunson Industry Group Co., Ltd.

- SternEnzym GmbH & Co. KG

- VEMO 99 Ltd.

Recent Industry Developments in Food Enzymes Market

- February 2025: Novonesis sealed a deal to purchase DSM-Firmenich’s stake in the Feed Enzyme Alliance for a whopping EUR 1.5 billion (USD 1.6 billion).

- November 2024: International Flavors & Fragrances launched TEXSTAR™, a pioneering enzyme set designed to transform fresh fermented food textures, targeting premium applications in dairy and fermented food categories

- October 2024: Biocatalysts Ltd. unveiled an enzymatic solution tailored to elevate flavour profiles in enzyme-modified dairy ingredients. This innovative enzyme is crafted to enhance the inherent flavour traits of dairy components. With this distinct solution, manufacturers can accentuate savoury, umami-rich nuances in their dairy products, aligning with contemporary consumer preferences for pronounced tastes and transparent, cleaner labels.

- September 2024: IFF introduced DIAZYME® NOLO, a revolutionary enzyme crafted to boost the taste, efficiency, and output of no- and low-alcohol (NOLO) drinks, all without hefty capital expenditures. This advancement is poised to cater to the rising appetite for NOLO beverages.

Global Food Enzymes Market Report Scope

Food enzymes are often used for food processing owing to their multiple benefits, which include enhancement of texture, flavor & fragrance, preservation, coagulation, and tenderization. The global food enzymes market is segmented by type, application, and geography. By type, the market is segmented into carbohydrase, protease, lipase, and others. Based on the application, the market is divided into bakery, confectionery, dairy and frozen desserts, meat, poultry, seafood products, beverages, and other applications. The study also covers the global level analysis of the major regions of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD Million).

Segmentation Overview

By Type

| Carbohydrase | Amylases |

| Pectinases | |

| Cellulases | |

| Other | |

| Protease | |

| Lipase | |

| Other Enzymes |

By Form

| Powder |

| Liquid |

By Source

| Plant |

| Microbial |

| Animal |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Columbia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Carbohydrase | Amylases |

| Pectinases | ||

| Cellulases | ||

| Other | ||

| Protease | ||

| Lipase | ||

| Other Enzymes | ||

| By Form | Powder | |

| Liquid | ||

| By Source | Plant | |

| Microbial | ||

| Animal | ||

| By Application | Bakery and Confectionery | |

| Dairy and Desserts | ||

| Beverages | ||

| Meat and Meat Products | ||

| Soups, Sauces, and Dressings | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Columbia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the food enzymes market?

The market was valued at USD 3.82 billion in 2026 and is projected to reach USD 5.03 billion by 2031.

Which region is growing fastest in the food enzymes market?

Asia-Pacific is forecast to expand at 6.84% CAGR, driven by urbanization and rising processed-food demand.

Which enzyme type dominates global revenue?

Carbohydrase enzymes hold 56.85% of food enzymes market share, thanks to widespread use in bakery, beverage, and confectionery processing.

Why are powder formulations preferred?

Powders offer superior shelf life, easier handling, and compatibility with automated feeders, securing 67.72% of market revenue in 2025.

Page last updated on: