Galactooligosaccharides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

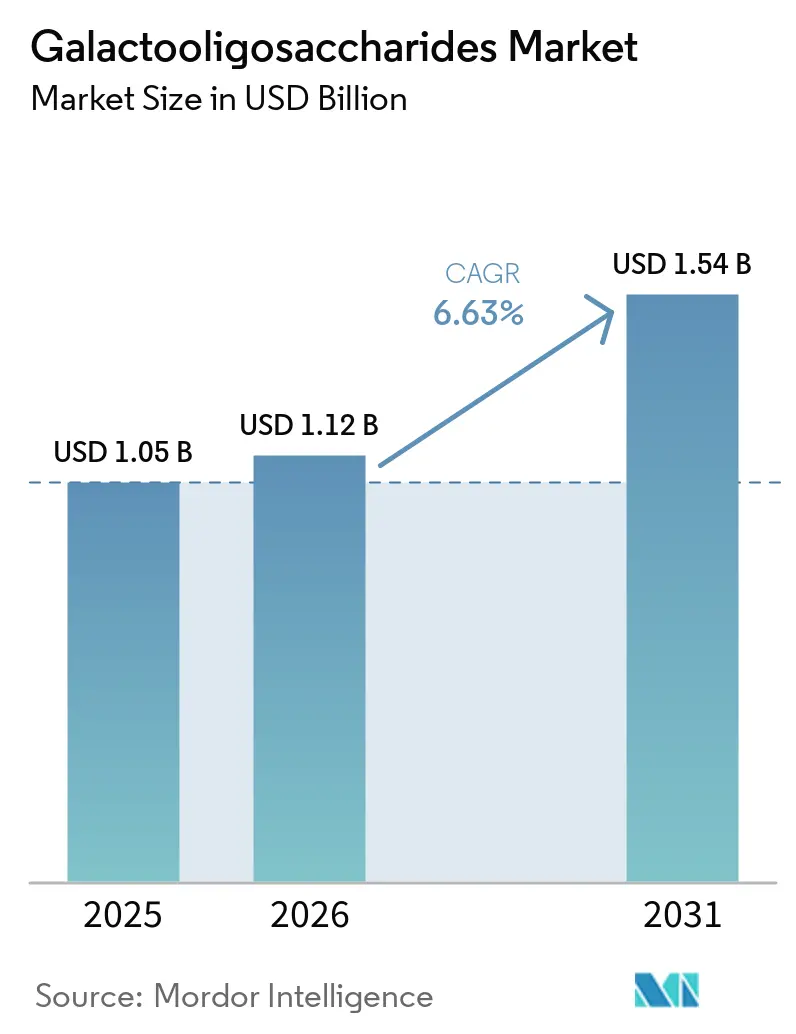

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Galactooligosaccharides Market Analysis by Mordor Intelligence

The galactooligosaccharides market, valued at USD 1.05 billion in 2025, is projected to grow to USD 1.12 billion in 2026 and reach USD 1.54 billion by 2031, with a CAGR of 6.63% from 2026 to 2031. Once a dairy co-product, GOS has become a key functional ingredient due to its proven prebiotic benefits, such as selective fermentation in the lower gastrointestinal tract and support for bifidobacteria growth. Its demand spans applications like infant nutrition, adult gut health, clinical nutrition, and pharmaceuticals, reducing dependency on any single end-use segment. Process advancements, including one-pot enzymatic methods producing GOS and antioxidant peptides simultaneously, are boosting efficiency and whey stream output value. Investments in enzyme production, such as Kerry Group’s expanded biotechnology hub in Ireland for industrial lactase production, are enhancing cost advantages for large producers. Consolidation among major ingredient groups is intensifying competition by increasing scale, patents, and supply reach, favoring well-capitalized suppliers in the galactooligosaccharides market.

Key Report Takeaways

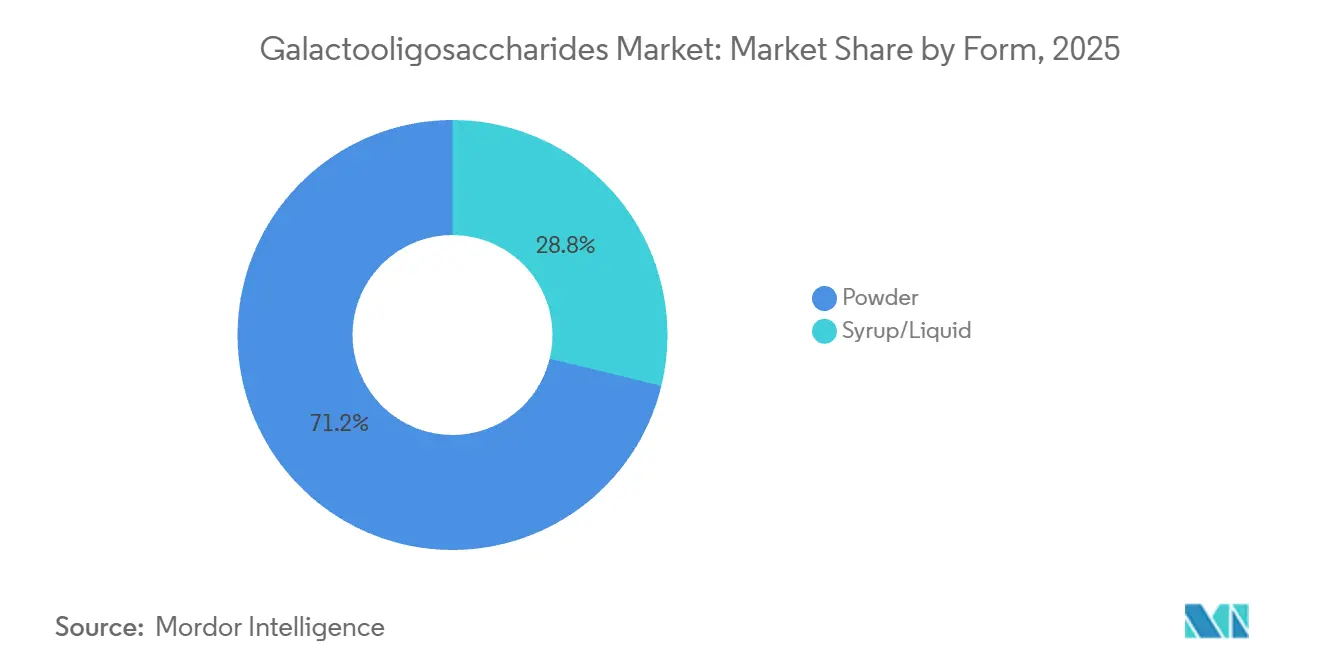

- By form, powder led with 71.2% share in 2025, while syrup/liquid is projected to grow at a 7.8% CAGR through 2031.

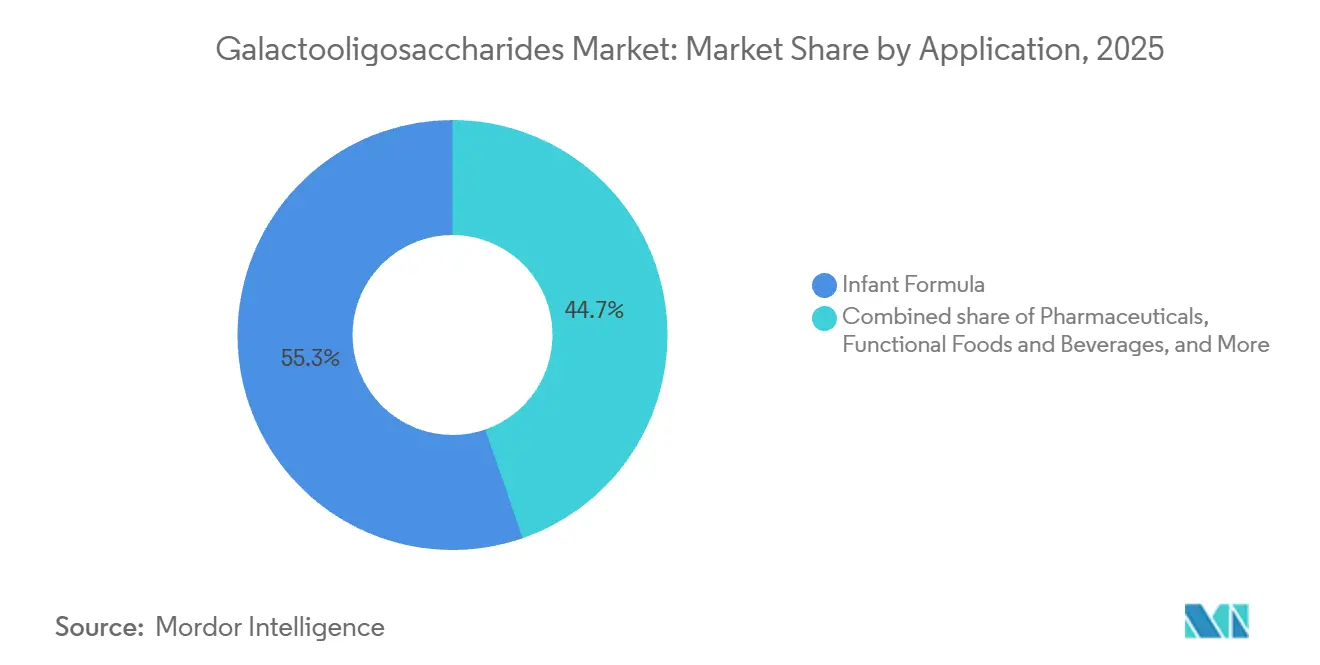

- By application, infant formula accounted for 55.3% share in 2025, while pharmaceuticals is forecast to expand at a 7.3% CAGR through 2031.

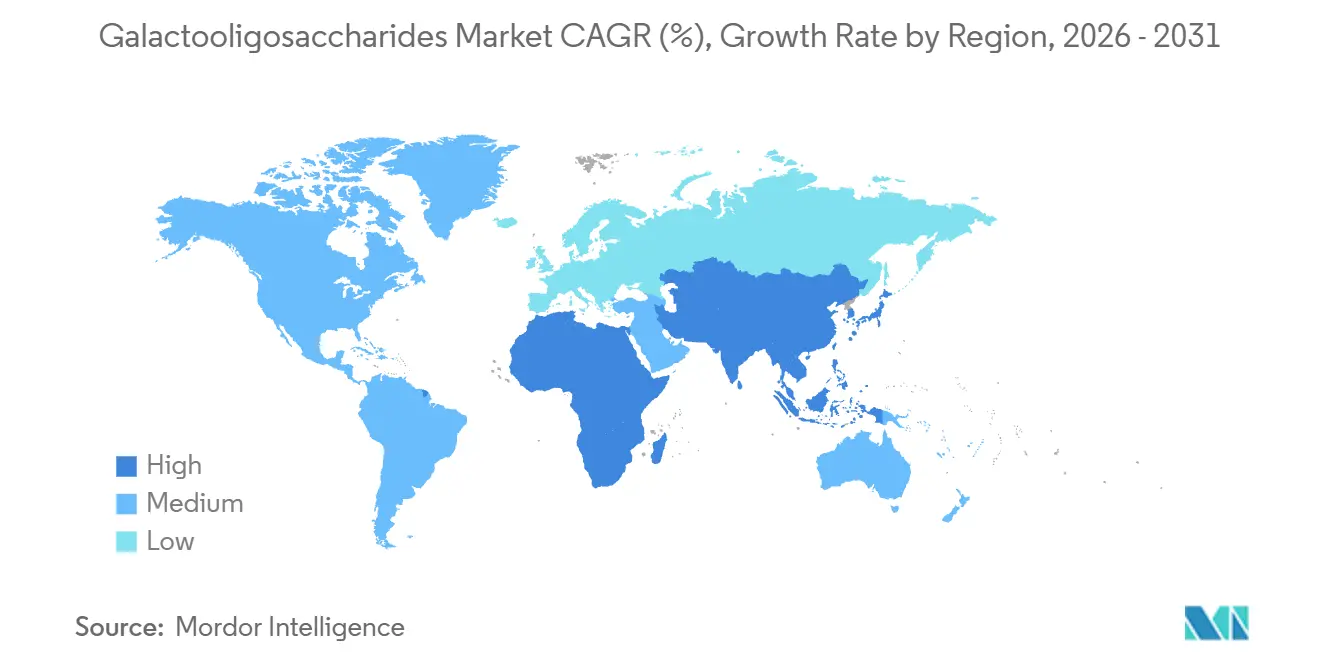

- By geography, Europe held 43.92% of revenue in 2025, while the Middle East and Africa is set to record the fastest CAGR at 8.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Galactooligosaccharides Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Awareness About Gut Health And Prebiotic Benefits | +1.8% | Global, with highest intensity in North America, Europe, and APAC | Short term (≤ 2 years) |

| Expansion Of Functional Food And Beverage Markets | +1.2% | North America, Europe, APAC, especially China and Japan | Medium term (2-4 years) |

| Clean-Label And Natural Ingredient Preferences | +0.5% | North America, Western Europe | Medium term (2-4 years) |

| Technological Advancements In Enzymatic Synthesis And Bioprocessing | +0.9% | Global, led by China, the EU, and Japan | Long term (≥ 4 years) |

| Growing Plant-Based And Vegan Product Portfolios | +0.4% | North America, the EU, and Australasia | Medium term (2-4 years) |

| Expanding Dietary Supplements And Clinical Nutrition Uses | +0.6% | North America, the EU, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Awareness About Gut Health and Prebiotic Benefits

The galactooligosaccharides market is gaining from stronger public familiarity with gut microbiome science and from the fact that GOS has an established clinical profile rather than a newly emerging one. The Global Prebiotic Association states that GOS selectively ferments in the lower gastrointestinal tract and supports the production of short-chain fatty acids and bifidobacteria, which keeps the ingredient closely linked to well-understood digestive health benefits. In the galactooligosaccharides market, this matters because brand owners usually prefer ingredients that already fit existing consumer understanding and formulation language. The same pattern also helps GOS travel across infant, adult, and therapeutic products without requiring a new education cycle for each format. That broad recognition gives the galactooligosaccharides market a more stable demand base than many newer prebiotic candidates that still need to prove both efficacy and commercial fit.

Expansion of Functional Food and Beverage Markets

The galactooligosaccharides market is also supported by steady expansion in functional food and beverage development, where product teams want ingredients that combine digestive relevance with workable formulation behavior. A 2026 review in 3 Biotech reported that GOS showed consistent beneficial effects on gut microbiota across in vitro, animal, and clinical work in functional food and therapeutic settings. In the galactooligosaccharides market, that body of evidence gives manufacturers a more practical basis for inclusion in beverages, fortified foods, and daily wellness products. The commercial effect is stronger in categories where repeat use depends on both consumer acceptance and scientific support. This keeps functional food and beverage demand relevant to long-term volume growth even when infant nutrition remains the largest application.

Technological Advancements in Enzymatic Synthesis and Bioprocessing

The galactooligosaccharides market is being reshaped by production systems that improve output value from the same lactose stream and reduce waste at the plant level. A 2025 study published through PMC showed a one-pot enzymatic process that produced GOS and antioxidant peptides simultaneously from native whey concentrate, which improved the economic logic of whey conversion[1]Source: Global Prebiotic Association, “Prebiotic Type Spotlight, Galactooligosaccharides (GOS)”, prebioticassociation.org. In the galactooligosaccharides market, this changes the discussion from simple yield improvement to broader return per unit of feedstock. Large suppliers are also strengthening their enzyme base, and Kerry’s expanded biotechnology manufacturing hub in Ireland is designed to scale industrial lactase production that supports downstream GOS synthesis. These changes favor scaled manufacturers in the galactooligosaccharides market because they can absorb capital spending faster and use process gains across larger commercial volumes.

Growing Plant-Based and Vegan Product Portfolios

The galactooligosaccharides market is also finding room in plant-forward product development, even though GOS itself is dairy-derived through lactose conversion. The ingredient does not usually carry the sensory profile of dairy in finished applications, which allows formulators to use it in products positioned around digestive health and broader lifestyle preferences. The 2026 3 Biotech review supports this direction by showing that GOS maintained consistent prebiotic effects across diverse dietary contexts, which helps its use beyond traditional dairy-centered categories. In the galactooligosaccharides market, this means one production platform can serve both conventional nutrition and newer plant-forward supplement and beverage launches. That flexibility improves asset utilization and reduces the need for separate ingredient systems as consumer portfolios widen.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Raw Material Availability And Supply Chain Vulnerability | -0.6% | Global, with acute pressure in Asia where lactose import dependency is highest | Medium term (2-4 years) |

| Strict Regulatory Requirements And Compliance Hurdles | -0.4% | The EU, APAC, and North America | Long term (≥ 4 years) |

| Competition From Alternative Prebiotics | -0.5% | Global, particularly in premium infant formula | Short term (≤ 2 years) |

| Low Enzymatic Yield Limiting Production Efficiency | -0.3% | Global, especially for sub-scale and emerging producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Raw Material Availability and Supply Chain Vulnerability

The galactooligosaccharides market remains exposed to lactose availability because lactose is still the main feedstock for enzymatic GOS production. This creates a supply risk that is difficult for producers to control on their own because major lactose output is concentrated in a relatively small number of dairy processing regions. The issue is especially important in the galactooligosaccharides market in Asia, where capacity growth can increase reliance on imported lactose and add freight cost and lead-time pressure. Shandong Bailong Chuangyuan’s December 2025 strategic agreement with Golden Corn shows how producers are trying to strengthen raw material access, even though that does not fully solve structural dependence on dairy-linked feedstock. If supply disruption affects key lactose-producing regions, the galactooligosaccharides market could face broader cost pressure at the same time that infant nutrition buyers still need secure delivery.

Competition from Alternative Prebiotics

The galactooligosaccharides market is also under pressure from other prebiotics that compete on price, familiarity, or biological similarity to human milk structures. FOS usually competes more directly in cost-sensitive applications, while inulin benefits from an agricultural-source profile and broad regulatory familiarity. In premium infant nutrition, the sharper challenge comes from HMOs, and the June 2025 global launch of HMO 2'-fucosyllactose by BENEO and Wacker added more commercial HMO availability to the category. The galactooligosaccharides market still holds advantages in regulatory familiarity across several major jurisdictions, a lower price point than HMOs, and a deeper history in mass-market formulation. Even so, the galactooligosaccharides market faces the strongest substitution risk in premium formula, where product narratives are shifting toward HMO-rich positioning and where suppliers need to keep improving their functional story.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Maintains Volume Dominance as Liquid Applications Accelerate

Powder held 71.2% of galactooligosaccharides market share in 2025, which shows how strongly the format fits existing infant formula, supplement, and dry food manufacturing systems. The galactooligosaccharides market still favors powder because it is ambient-stable, easier to transport through long supply chains, and compatible with common dry blending lines used by food manufacturers. Shandong Bailong Chuangyuan offers 70% and 90% purity powder grades and commissioned a 30,000-ton combined soluble dietary fiber production line in 2024, which supports continued confidence in powder-led output growth. In the galactooligosaccharides industry, that installed base matters because buyers usually value handling consistency as much as headline functionality when they are sourcing ingredients for repeat production.

The galactooligosaccharides market size for the syrup/liquid segment is projected to grow at 7.8% CAGR through 2031, making it the faster-moving form within the category. The galactooligosaccharides market is seeing this shift because beverage fortification, liquid infant formula, and some dairy applications can use direct liquid dosing more easily than powder dispersion. Kerry’s enzyme investment is relevant here because higher lactase capacity supports more efficient downstream synthesis and can help improve commercial availability for producers serving liquid applications. The practical benefit is a shorter path from ingredient tank to finished product in applications where solubility and handling speed matter. Within the galactooligosaccharides industry, that makes syrup and liquid formats more attractive in ready-to-drink and other water-based systems where formulation simplicity carries real value.

By Application: Infant Formula Sustains Structural Primacy as Pharmaceuticals Emerge as a High-Growth Niche

In 2025, infant formula dominated the galactooligosaccharides market, capturing a 55.3% share. This stronghold underscores the ingredient's entrenched role in formulations, bolstered by a proven safety and efficacy record. Buyers in infant nutrition tend to resist sudden shifts, favoring ingredients that have become commercial staples. Leading suppliers, like FrieslandCampina Ingredients, are not just defending this position but also enhancing it. Their Vivinal® GOS-SL product melds standard GOS with sialylated structures from bovine milk, a move secured through a patent-pending process. This evolution not only solidifies the infant formula's centrality in demand but also pivots the competition towards advanced ingredient design.

Pharmaceuticals, with a projected CAGR of 7.3% through 2031, is emerging as the fastest-growing application in the galactooligosaccharides market. A 2024 randomized clinical trial in Food & Function highlighted GOS's efficacy and safety in treating functional constipation, bolstering its appeal in therapeutic and drug-adjacent products. Further backing comes from a 2025 study in Metabolites, as referenced in the provided material, which demonstrated bifidogenic activity at minimal, capsule-compatible doses. Such dose efficiency is crucial, given the precise inclusion levels required by pharmaceutical and supplement manufacturers in solid oral products. Consequently, the galactooligosaccharides market is expanding its footprint, venturing into microbiome-focused therapy and clinical nutrition, rather than being confined to food and infant applications.

Geography Analysis

In 2025, Europe dominated the galactooligosaccharides market, accounting for 43.92% of the market size. Europe's stronghold in the galactooligosaccharides market is bolstered by its longstanding acceptance of functional foods and the presence of established suppliers like FrieslandCampina Ingredients in the Netherlands and Clasado Biosciences in the UK. Germany stands out as a significant player, boasting a well-developed food processing base and robust packaged nutrition channels. Meanwhile, North America, a mature player in the galactooligosaccharides arena, still showcases potential for growth, as evidenced by Saputo Dairy UK's GRAS Notice GRN 1216, submitted to the US FDA in August 2024[2]Source: U.S. Food and Drug Administration, “GRAS Notice GRN 1216, Saputo Dairy UK Galacto-Oligosaccharides (SDUK-GOS)”, downloads.regulations.gov.

Asia-Pacific ranks as the second-largest market for galactooligosaccharides and is a pivotal production hub. The region's robust domestic demand pairs seamlessly with its expansive manufacturing base, particularly in China. Here, suppliers like Quantum Hi-Tech and Shandong Bailong Chuangyuan cater to both local and export markets. Notably, Quantum Hi-Tech claims a commanding 50% share of China's domestic prebiotic market, underscoring the dominance of local producers in this crucial supply region. Japan's longstanding use of GOS in dairy and beverages lends stability to the market, ensuring consistent volume demand.

The Middle East and Africa lead the pack with the fastest growth rate in the galactooligosaccharides market, boasting an 8.01% CAGR projected through 2031. Further emphasizing the region's burgeoning significance, Mordor Intelligence forecasts GOS to expand at a notable 9.98% CAGR within the broader prebiotic ingredients market in the Middle East and Africa. This growth trajectory is largely fueled by high birth rates in GCC nations and Sub-Saharan Africa, sustaining a robust demand for infant formulas. Among African nations, South Africa stands out as the most developed market, driven by the rapid expansion of modern retail and functional food formats.

Competitive Landscape

The galactooligosaccharides market is moderately consolidated at the higher-value tier, where a few suppliers compete using proprietary processes, regulatory expertise, and clinical support. In contrast, the middle and lower tiers are fragmented, with Chinese producers, regional dairy suppliers, and specialty distributors competing across purity grades and contract supply. FrieslandCampina Ingredients, Clasado Biosciences, and Kerry Group lead the premium segment by combining product development with technical and commercial support, meeting large buyers' demand for supply assurance and application support alongside ingredient performance.

Strategic developments are reshaping the premium galactooligosaccharides market. FrieslandCampina Ingredients launched Vivinal® GOS-SL, adding sialylated milk oligosaccharides to its GOS platform, offering infant formula makers a high-function ingredient. In April 2026, Kerry Group expanded enzyme capacity to improve lactase availability and GOS production economics. Clasado Biosciences extended its reach in May 2026 by appointing Prokopton SAS as the exclusive French distributor for Bimuno® GOS across supplements, food, beverage, and pet nutrition. These moves emphasize product innovation and channel expansion over price competition.

In 2026, Ingredion Incorporated proposed acquiring Tate & Lyle PLC for GBP 3.7 billion (USD 5.0 billion). With Tate & Lyle already owning Quantum Hi-Tech, the merger combines Chinese production capabilities with global distribution and customer access. This raises the bar for smaller suppliers, as few can match the geographic reach and innovation scale of the combined entity. The result is likely stronger pricing discipline and increased pressure on smaller producers with limited markets or customer bases.

Galactooligosaccharides Industry Leaders

FrieslandCampina

Yakult Honsha Co., Ltd.

Kerry Group plc

Nissin Sugar Co., Ltd.

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Ingredion Incorporated announced a recommended all-cash acquisition of Tate & Lyle PLC for a total enterprise value of approximately USD 5.0 billion, representing a 59% premium to Tate & Lyle's May 2026 closing share price. The deal, which is expected to close in the second half of 2027, combines Ingredion's global specialty ingredient platform with Tate & Lyle's GOS and FOS capabilities, including its Quantum Hi-Tech integration in China, creating a combined business with approximately 65 manufacturing plants and 2,700 patents granted or pending.

- April 2026: Kerry Group opened its expanded biotechnology manufacturing hub in Carrigaline, County Cork, Ireland, significantly scaling industrial lactase enzyme production capacity and linking advanced enzyme engineering directly to large-scale commercial manufacturing. The hub connects Kerry's Global Innovation Centre with its Leipzig enzyme engineering facility and Carrigaline production, shortening the pathway from lab-scale discovery to commercial application for enzyme-enabled ingredients including those used in GOS synthesis.

- September 2025: FrieslandCampina Ingredients announced Vivinal® GOS-SL, a next-generation GOS ingredient combining standard Vivinal® GOS with sialylated HMO structures, 3'-sialyllactose (3'-SL) and 6'-sialyllactose (6'-SL), retained from bovine milk via a patent-pending production process, offering infant formula manufacturers a single ingredient that delivers GOS prebiotic function alongside additional oligosaccharide diversity without the cost overhead of separately synthesised HMOs.

Global Galactooligosaccharides Market Report Scope

| Syrup/Liquid |

| Powder |

| Infant Formula |

| Functional Foods and Beverages |

| Dietary Supplements |

| Pharmaceuticals |

| Animal Feed |

| Cosmetics |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Form | Syrup/Liquid | |

| Powder | ||

| By Application | Infant Formula | |

| Functional Foods and Beverages | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for galactooligosaccharides?

The category is forecast to reach USD 1.54 billion by 2031 from USD 1.12 billion in 2026, with a 6.63% CAGR over 2026-2031.

Which form leads demand for galactooligosaccharides?

Powder led with 71.2% share in 2025 because it fits dry blending, storage, and long-distance transport requirements across infant formula and supplements.

Which application is growing fastest through 2031?

Pharmaceuticals is the fastest-growing application, with a projected 7.32% CAGR through 2031, helped by rising use in constipation management and microbiome-focused therapy.

Which region is expanding fastest for GOS sales?

The Middle East and Africa is expected to post the fastest regional growth at 8.01% CAGR through 2031, supported by infant nutrition demand and developing retail channels.

Page last updated on: