Carotenoids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

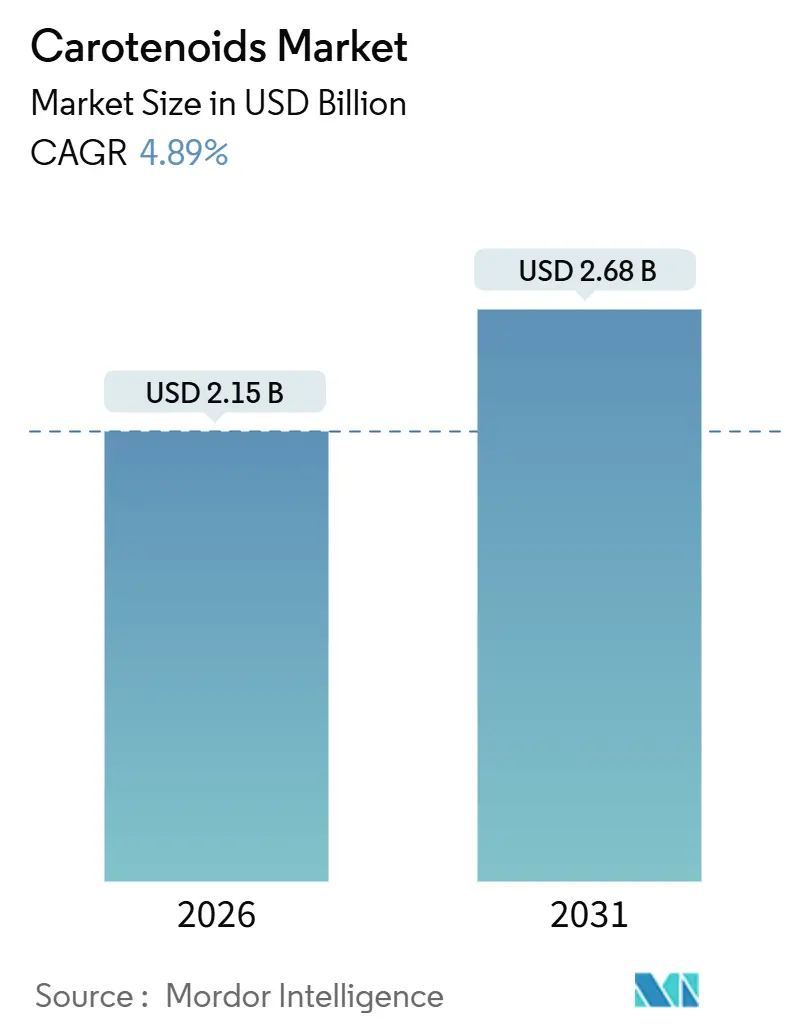

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

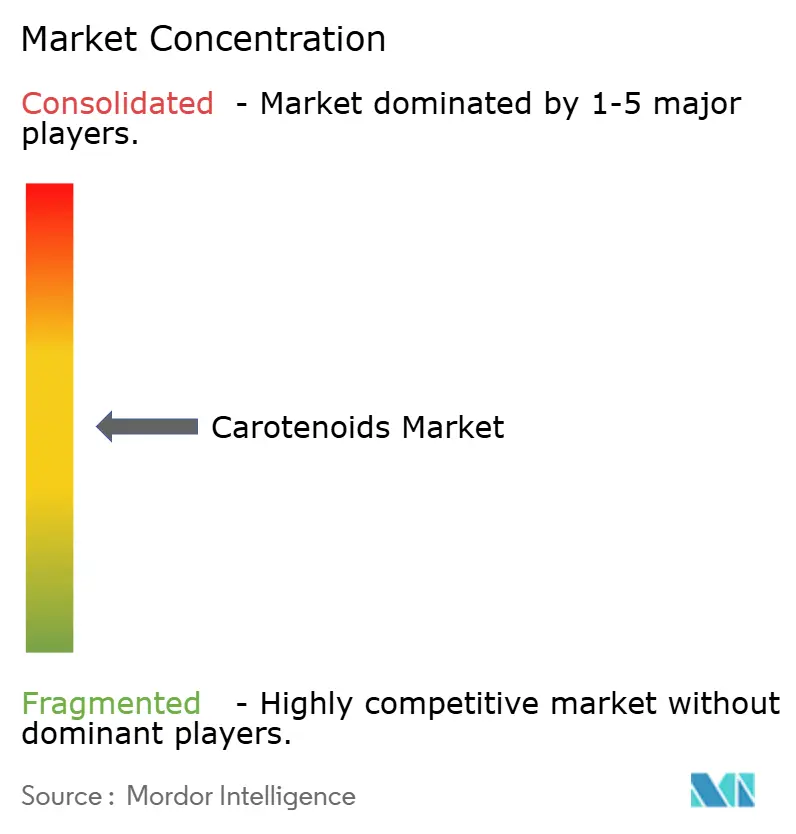

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Carotenoids Market Analysis by Mordor Intelligence

The carotenoids market size is valued at USD 2.15 billion in 2026 and is projected to reach USD 2.68 billion by 2031, growing at a 4.89% CAGR over the forecast period. Demand pivots toward fermentation and algae-derived pigments as European clean-label rules tighten and Southeast Asian aquaculture expands, reshaping the cost–performance equation for suppliers. Astaxanthin’s dual role in premium salmon feed and sports-nutrition supplements underpins its 7.28% CAGR, while powder beadlets dominate distribution channels thanks to 24-month stability in ambient storage. Natural-source variants trail synthetics in volume but outpace them in growth, driven by retailer mandates for “no artificial colors” labeling in North America and the European Union. Asia-Pacific emerges as the fastest-growing region as China and Indonesia scale shrimp and tilapia output, lifting pigment inclusion rates in compound feed.

Key Report Takeaways

- By type, astaxanthin led with 28.31% revenue share in 2025; it is projected to expand at a 7.28% CAGR through 2031.

- By source, synthetic carotenoids accounted for 57.68% of 2025 sales; natural variants register the highest forecast growth at 6.58% CAGR to 2031.

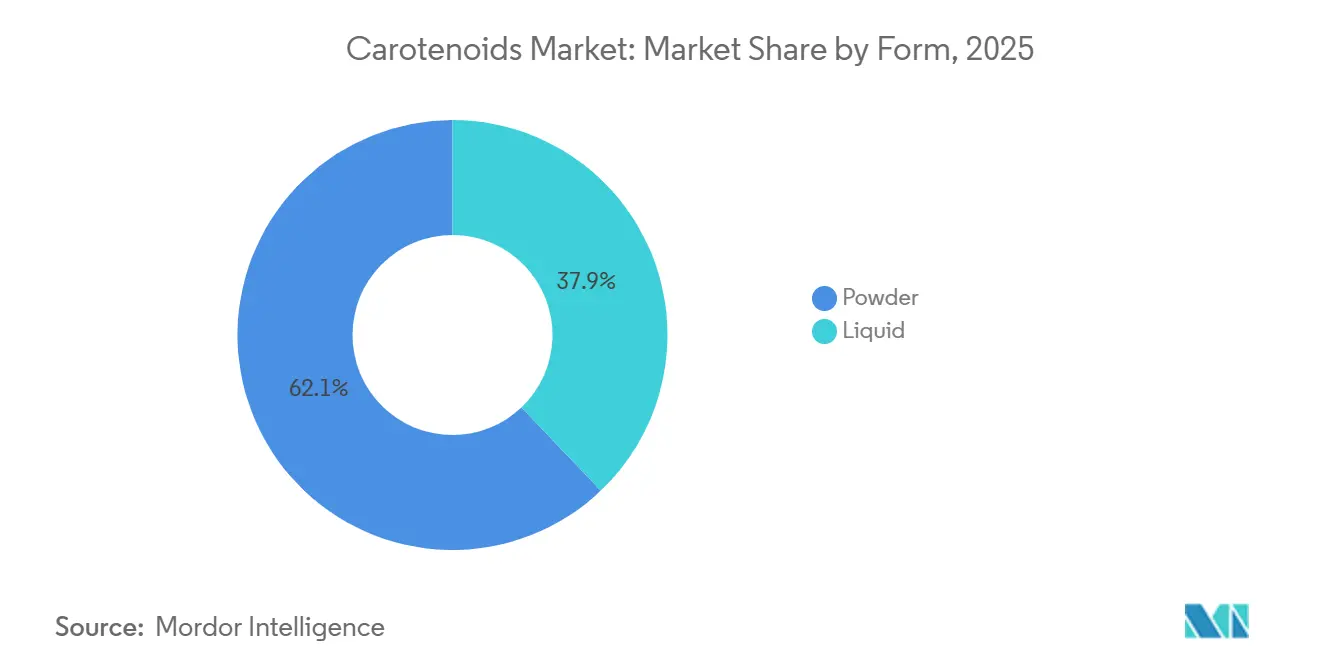

- By form, powder formats captured 62.12% revenue share in 2025; the segment is expected to post a 6.51% CAGR over the outlook period.

- By application, animal feed dominated with 41.52% of the 2025 value; dietary supplements recorded the strongest 6.35% CAGR through 2031.

- By region, Europe commanded 32.11% of the carotenoids market share in 2025, while Asia-Pacific is poised to grow at a CAGR of 6.92% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carotenoids Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Awareness of Carotenoids' Antioxidant and Eye Health Benefits | +1.0% | Global, with strong growth in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Demand in Food and Beverage for Natural Colorants and Fortification | +0.8% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Increasing Aquaculture and Animal Feed Applications for Pigmentation and Immunity | +1.3% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Popularity in Personal Care and Cosmetics for Skincare Benefits | +0.3% | Global, with early gains in developed markets | Long term (≥ 4 years) |

| Government Regulations Promoting Natural Ingredients in Food and Feed | +0.7% | Global, with strong demand in Asia-Pacific aquaculture | Short term (≤ 2 years) |

| Advancements in Sustainable Sourcing and Production Technologies | +0.6% | Global, led by North America and Europe innovation hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Carotenoids' Antioxidant and Eye Health Benefits

Lutein and zeaxanthin have become the primary components in age-related eye-health formulations, following the National Eye Institute's AREDS2 trial, which demonstrated a 25% reduction in the progression to advanced macular degeneration when 10 milligrams of lutein and 2 milligrams of zeaxanthin replaced beta-carotene[1]Source: National Eye Institute, “Age-Related Eye Disease Studies (AREDS/AREDS2),” nei.nih.gov. Formulators are now combining these xanthophylls with omega-3 fatty acids in soft-gel capsules, targeting the 196 million adults worldwide diagnosed with early-stage AMD, according to the World Health Organization. Astaxanthin, previously associated with ophthalmology, has gained traction in sports nutrition. A 2024 double-blind trial published in the Journal of the International Society of Sports Nutrition reported that a daily dose of 12 milligrams improved time-to-exhaustion by 8.2% in trained cyclists. Retail data from the United States shows that eye-health supplements experienced an 11% year-over-year growth in 2025, surpassing the broader vitamin category. This growth is partly driven by optometrists prescribing "nutraceuticals" during routine exams. Such clinical validation is expanding carotenoid demand from traditional multivitamins to condition-specific SKUs, which offer higher margins and foster repeat purchases.

Rising Demand in Food and Beverage for Natural Colorants and Fortification

The European Commission has banned titanium dioxide (E171) in food applications to enhance food safety[2]Source: European Food Safety Authority, “Food Colors,” efsa.europa.eu. This regulation has driven confectionery and bakery manufacturers to adopt natural alternatives, such as yellow-orange hues sourced from beta-carotene, annatto, or paprika extract. In 2025, Nestlé responded to this regulatory change by reformulating 47 product lines in its European portfolio. The company replaced synthetic colorants with carotenoid blends, a move that increased raw-material costs by approximately USD 0.02 per unit but met retailer clean-label requirements. Beverage brands are utilizing lycopene from tomato oleoresin to achieve red tones in functional drinks without triggering allergen concerns. Additionally, beta-carotene is being used to fortify plant-based dairy alternatives, ensuring they match the vitamin A content of cow's milk. Regulatory frameworks, such as the EU's Novel Food Regulation and the FDA's color-additive petitions, have created a two-tier market. Established carotenoids like beta-carotene benefit from GRAS status and faster approvals, while newer fermentation-derived variants face lengthy multi-year dossiers and toxicology studies. This regulatory environment favors experienced suppliers with existing petitions and regulatory expertise, while posing significant challenges for algae-based entrants that often lack the financial resources to fund pre-market safety assessments.

Increasing Aquaculture and Animal Feed Applications for Pigmentation and Immunity

Farmed salmon and shrimp require dietary astaxanthin to develop the pink-to-red flesh color that consumers commonly associate with wild-caught seafood. Without this supplementation, farmed fish remain gray, resulting in a 30% to 40% price discount at wholesale, according to the Norwegian Seafood Council[3]Source: Norwegian Seafood Council. "Astaxanthin Pigmentation Standards in Aquaculture." en.seafood.no. In 2024, global aquaculture production reached 124.2 million metric tons, with China, Indonesia, and Vietnam accounting for 68% of the output. Feed manufacturers in these regions now include 50 to 100 milligrams of astaxanthin per kilogram of pellet to meet export-market color requirements, as reported by the FAO. Beyond pigmentation, recent research links carotenoid supplementation to improved immune responses and reduced mortality during disease outbreaks. For example, a 2025 study published in the Aquaculture journal reported a 19% decrease in white-spot syndrome virus prevalence among shrimp fed canthaxanthin-enriched diets. In the poultry industry, integrators add lutein and zeaxanthin to laying hens' diets to enhance egg-yolk color. This deeper color is associated with perceived freshness and commands higher prices in markets such as Japan and South Korea. In the EU and U.S., feed-additive approvals specify maximum inclusion rates and withdrawal periods. This regulatory framework creates a compliance advantage for suppliers with established dossiers and quality-assurance protocols adhering to ISO 22000 and FAMI-QS standards.

Advancements in Sustainable Sourcing and Production Technologies

Precision fermentation is quickly establishing itself as a scalable alternative to conventional agricultural extraction. Companies are leveraging yeast and bacteria to biosynthesize compounds such as beta-carotene, astaxanthin, and lycopene, achieving yields comparable to petrochemical methods. DSM-Firmenich operates a 10,000-metric-ton fermentation facility in Switzerland, where beta-carotene is produced using genetically modified Escherichia coli, resulting in a carbon footprint 40% lower than that of solvent extraction from carrots. In 2024, BASF entered into a joint venture with a Singapore-based synthetic-biology firm to commercialize astaxanthin derived from Corynebacterium glutamicum, with a target production cost of less than USD 1,000 per kilogram by 2027. Achieving this cost threshold could make natural astaxanthin economically viable in the mainstream aquafeed market, as noted in a BASF press release. Algae cultivation in closed photobioreactors eliminates contamination risks and enables year-round production, unaffected by seasonal weather. However, the capital expenditure for a 100-ton-per-year facility exceeds USD 50 million, limiting participation to well-capitalized companies. Additionally, solvent-free supercritical CO₂ extraction is gaining popularity for lutein recovery from marigold flowers. This method ensures higher purity and avoids hexane residues, which can jeopardize non-GMO and organic certifications. These technological advancements are reducing the cost disparity between natural and synthetic carotenoids, driving the market toward bio-based supply chains that align with corporate sustainability objectives and Scope 3 emissions-reduction goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Analysis |

|---|---|---|---|

| High Production Costs of Natural Carotenoids | -0.6% | Global, particularly affecting Asia-Pacific producers | Short term (≤ 2 years) |

| Supply Variability from Climate-Sensitive Natural Sources | -0.5% | Global, with particular impact on cross-border trade | Medium term (2-4 years) |

| Stringent Regulatory Scrutiny on Synthetic Variants and Labeling | -0.4% | Global, particularly affecting food and beverage applications | Short term (≤ 2 years) |

| Complex Extraction and Purification Processes for Natural Sources | -0.3% | Global, with higher impact in processed food sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs of Natural Carotenoids

Natural astaxanthin, derived from Haematococcus pluvialis algae, is priced between USD 2,500 and USD 7,000 per kilogram. In comparison, synthetic astaxanthin, produced using petrochemical intermediates, costs USD 500 to USD 1,000 per kilogram. This creates a 3-to-7-fold price premium for the natural variant, limiting its use mainly to the nutraceutical and cosmetic markets, where consumers are more willing to pay higher prices. Producing natural astaxanthin requires controlled photobioreactors with precise monitoring of temperature, pH, and nutrients. Furthermore, energy-intensive harvesting and drying processes account for 60% of the total production cost. Similarly, lutein extraction from marigold flowers involves multiple steps, including saponification and chromatography, to remove chlorophyll and achieve the 80% purity needed for dietary supplements. This complex process raises costs to USD 150 to USD 200 per kilogram, compared to USD 40 to USD 60 for synthetic beta-carotene. In the Asia-Pacific, feed manufacturers prioritize cost over origin, favoring synthetic blends of canthaxanthin and astaxanthin that provide adequate pigmentation at one-third the cost of natural alternatives. Despite scale-up efforts, this cost gap persists. Biological systems face limitations due to photosynthetic efficiency and cell density constraints, while chemical synthesis benefits from continuous process improvements and economies of scale within the existing petrochemical infrastructure.

Supply Variability from Climate-Sensitive Natural Sources

In India, marigold flower cultivation, responsible for nearly 70% of the global lutein supply, is increasingly affected by unpredictable monsoon patterns. In 2024, delayed rains caused a 22% production shortfall in Karnataka and Andhra Pradesh, driving spot prices to USD 220 per kilogram, up from USD 160 the previous year. Similarly, paprika pepper harvests in Spain and Peru have faced volatility; in 2025, heat waves reduced capsanthin yields by 18%, prompting European food manufacturers to switch to synthetic alternatives to avoid supply disruptions. Although algae cultivation is theoretically shielded from climate variability in closed systems, it remains susceptible to power outages and equipment failures. For example, Cyanotech's Hawaii facility experienced a 9-day production halt in August 2024 due to a transformer failure that disrupted photobioreactor circulation, resulting in a USD 1.2 million revenue loss. To mitigate such risks, buyers often adopt dual-source contracts that combine natural and synthetic inventories. However, this strategy compromises the "100% natural" claims that typically justify premium pricing in consumer markets. Addressing climate challenges—such as relocating marigold cultivation to higher latitudes or developing drought-resistant cultivars—requires extensive agronomic trials and multi-year lead times. This leaves the supply chain exposed to immediate weather shocks, compressing margins and forcing formulators to maintain larger safety stocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Astaxanthin Captures Dual-Market Momentum

Astaxanthin, recognized for its role as both a premium aquafeed pigment and a powerful antioxidant for human nutrition, is expected to grow at a 7.28% CAGR through 2031. This dual functionality allows suppliers to leverage two distinct profit margins from a single production asset. In 2025, astaxanthin accounted for 28.31% of the market share, primarily driven by Norwegian and Chilean salmon farmers. These farmers administer feed doses of 50 to 80 milligrams per kilogram, ensuring their salmon achieve SalmoFan color scores above 25, the standard for premium retail placement. At the same time, sports-nutrition brands promote astaxanthin as a mitochondrial antioxidant capable of crossing the blood-brain barrier. They cite clinical trials demonstrating its effectiveness in improving endurance and reducing muscle soreness. Beta-carotene remains a staple in food fortification and animal feed, particularly in poultry and dairy applications for its provitamin A properties. However, its growth is limited to approximately a 4% CAGR due to market saturation and competition from synthetic retinyl esters.

Lutein and zeaxanthin are gaining traction in dietary supplements, driven by aging populations in North America, Europe, and Japan. In these regions, more than 8% of adults aged 65 and older are affected by age-related macular degeneration. Lycopene, extracted from tomatoes, serves niche markets in prostate-health supplements and as a natural red colorant in beverages. Canthaxanthin is preferred by poultry integrators seeking egg-yolk pigmentation while avoiding the regulatory challenges faced by synthetic alternatives in the European Union. Zeaxanthin is most commonly paired with lutein in a 5:1 ratio to replicate macular pigment composition, though emerging research on its cognitive benefits may create opportunities for standalone supplements. The "Others" category, which includes fucoxanthin, capsanthin, and bixin, is experiencing modest growth. However, its adoption is constrained by limited clinical evidence and high extraction costs, restricting its use to specialized cosmetic and pharmaceutical applications.

By Source: Natural Variants Gain Despite Cost Premium

Natural carotenoids are expected to grow at a 6.58% CAGR through 2031, surpassing synthetic carotenoids by 0.89 percentage points. This growth is primarily driven by clean-label mandates in North America and the European Union, which are encouraging food and beverage manufacturers to shift towards plant-derived or fermentation-based ingredients. In 2025, synthetic carotenoids accounted for 57.68% of the market share, largely due to their cost-effectiveness in animal-feed applications, where pigmentation performance outweighs ingredient origin. For instance, petrochemical-derived astaxanthin costs only one-third of algae-based alternatives. However, regulatory changes are influencing the market. In 2025, the European Union revised its feed-additive regulations, reducing the maximum residue limits for synthetic canthaxanthin by 15%. This regulatory shift is prompting poultry integrators to explore natural sources, despite the associated margin pressures. Precision fermentation is emerging as a solution to bridge the cost-performance gap. DSM-Firmenich has developed beta-carotene using engineered E. coli, achieving "nature-identical" status that complies with clean-label requirements while offering production costs closer to synthetic methods.

Consumer willingness to pay a premium for natural carotenoids varies significantly by application and region. A 2025 Nielsen survey in the United States revealed that 64% of supplement buyers were willing to pay a 20% premium for "plant-derived" lutein, whereas only 31% were willing to do so for food colorants, which are not visible to end users. In the nutraceutical sector, algae-based astaxanthin is priced between USD 4,000 and USD 7,000 per kilogram, while synthetic astaxanthin used in aquafeed is priced between USD 500 and USD 1,000 per kilogram. This price gap has created a bifurcated market, forcing suppliers to either maintain dual production lines or accept reduced margins in one segment to scale the other. Marigold-derived lutein faces competition from synthetic lutein esters, but the latter requires additional saponification steps, which reduce their cost advantage and complicate regulatory approvals in markets with strict natural-definition standards. As fermentation technology progresses and capital costs decline, the price gap between natural and synthetic carotenoids is expected to narrow. This development will accelerate the shift towards bio-based supply chains, aligning with corporate sustainability objectives and Scope 3 emissions-reduction targets.

By Form: Powder Dominates on Stability and Handling

In 2025, powder formulations accounted for 62.12% of the market share and are expected to sustain a 6.51% CAGR through 2031. Their widespread adoption is attributed to benefits such as extended shelf life, ease of transport, and compatibility with dry-blend premixes, making them ideal for use in animal feed, dietary supplements, and bakery applications. Carotenoid powders typically use spray-dried or beadlet encapsulation matrices, such as gelatin, starch, or modified cellulose. These matrices protect the pigment from oxidation and light degradation, enhancing stability from just 6 months in liquid suspensions to over 24 months in sealed powder formats. Feed manufacturers in the Asia-Pacific prefer powder blends due to their seamless integration into pelleting lines. This eliminates the need for additional emulsification equipment, reducing capital expenditure and simplifying quality control processes.

Liquid carotenoid emulsions cater to niche applications requiring instant dispersion, such as functional beverages, dairy analogs, and cosmetic serums. However, their shorter shelf life and higher freight costs limit their use to premium segments. Beverage formulators utilize water-dispersible liquid beta-carotene to fortify plant-based milks and sports drinks, achieving uniform color without the sedimentation issues associated with powder suspensions. Cosmetic brands incorporate liquid astaxanthin into anti-aging serums and sunscreens, highlighting its antioxidant properties and red-orange hue as a natural alternative to synthetic actives. However, regulatory frameworks in the European Union and United States classify carotenoids as colorants rather than active ingredients, restricting certain marketing claims. Advancements in microencapsulation technologies, such as spray-chilling and coacervation, are combining the benefits of powders and liquids. These technologies produce free-flowing granules that disperse quickly in aqueous systems while maintaining the oxidative stability of traditional powders. Nevertheless, the higher processing costs limit their adoption to high-margin sectors like nutraceuticals and personal care.

By Application: Dietary Supplements Overtake Mature Feed Segment

In 2025, animal feed accounted for 41.52% of the market share, supported by regulatory requirements in aquaculture mandating astaxanthin and canthaxanthin supplementation to meet export-market color standards for salmon, shrimp, and trout. Norwegian salmon farmers include 50 to 80 milligrams of astaxanthin per kilogram of feed to achieve SalmoFan scores above 25, the threshold for premium retail placement in Japan and the U.S. In South Korea and Japan, poultry integrators add lutein and canthaxanthin to layer diets to enhance egg-yolk color, a characteristic associated with freshness that commands a 10% to 15% price premium. However, feed applications face margin pressures as aquaculture production consolidates, with buyers negotiating volume contracts that reduce supplier pricing power, limiting the segment's growth to low-single-digit CAGRs.

Dietary supplements are experiencing the fastest application growth, with a projected CAGR of 6.35% through 2031. This growth is driven by clinical evidence linking lutein and zeaxanthin to macular degeneration prevention and astaxanthin to sports recovery benefits. The National Eye Institute's AREDS2 trial identified 10 milligrams of lutein and 2 milligrams of zeaxanthin as the recommended doses for eye health, leading to a standardized formulation that optometrists frequently recommend during routine exams. In sports nutrition, brands market astaxanthin as a mitochondrial antioxidant that enhances endurance and reduces muscle soreness, citing double-blind trials showing an 8.2% improvement in time-to-exhaustion among trained cyclists. Food and beverage applications are growing at a slower pace, constrained by the European Union's ban on titanium dioxide, which has led to a search for natural yellow-orange colorants. However, beta-carotene and annatto face challenges with stability in low-pH beverages and high-temperature baking. In personal care, astaxanthin's antioxidant properties are utilized in anti-aging serums and sunscreens. Meanwhile, pharmaceutical applications remain niche, focusing on ophthalmic drug delivery systems and investigational therapies for non-alcoholic steatohepatitis.

Geography Analysis

In 2025, Europe accounted for 32.11% of the market share, driven by strict clean-label regulations and a rapid transition to natural food colorants. This shift followed the European Union's 2022 ban on titanium dioxide in food applications. The European Food Safety Authority revised its guidelines on synthetic food additives in 2025, lowering acceptable daily intake levels for several azo dyes. This prompted confectionery, bakery, and beverage manufacturers to accelerate reformulation efforts, replacing synthetic additives with beta-carotene, paprika extract, and annatto. Germany and the Netherlands dominate demand for natural astaxanthin in dietary supplements, with consumers willing to pay a premium for algae-derived ingredients certified as organic and non-GMO. In aquaculture, Norway and Scotland drive astaxanthin usage in salmon feed, with producers meeting Japanese import standards by dosing 60 to 80 milligrams per kilogram to achieve the required SalmoFan color scores. However, Europe's well-established regulatory framework and slower population growth limit the region's CAGR to approximately 3.8% through 2031, below the global average. Growth in the region primarily stems from the substitution of synthetic ingredients with natural alternatives rather than overall market expansion.

Asia-Pacific is projected to achieve the fastest regional growth, with a CAGR of 6.92% through 2031. This growth is supported by the expansion of aquaculture in China, Indonesia, Thailand, and Vietnam. In 2024, these countries collectively produced 47.3 million metric tons of shrimp and tilapia, reflecting a 9.1% year-over-year increase. Chinese feed manufacturers use a blend of synthetic astaxanthin and canthaxanthin to achieve cost-effective pigmentation. Domestic suppliers such as Zhejiang NHU and Guangzhou Leader Bio-Technology dominate the market, offering prices 20% to 30% lower than European imports. In India, marigold cultivation in Karnataka and Andhra Pradesh, which supplies about 70% of the global lutein feedstock, experienced a 22% yield reduction in 2024 due to erratic monsoon patterns. This led to spot prices rising to USD 220 per kilogram and encouraged buyers to diversify sourcing to Peru and Mexico. In Japan and South Korea, an aging population and increased awareness of macular degeneration are driving demand for dietary supplements. Retail sales of lutein and zeaxanthin products grew by 13% year-over-year in 2025. Additionally, Southeast Asian governments are offering tax incentives and subsidized land leases to attract carotenoid manufacturers, positioning the region as a cost-efficient production hub that could challenge Europe's traditional dominance in natural-extract supply chains.

North America, South America, and the Middle East and Africa collectively represent the remaining market share. In the United States, dietary supplement consumption is supported by optometrists recommending AREDS2-formula eye-health products containing lutein and zeaxanthin. Brazil and Chile contribute to aquaculture demand, particularly for astaxanthin used in salmon and trout feed. Meanwhile, Mexico and Peru cultivate paprika peppers for capsanthin extraction, which is used in poultry feed and as a natural colorant. In the Middle East, multinational brands are expanding the distribution of food colorants, but regulatory inconsistencies across Gulf Cooperation Council states delay approval processes for new carotenoid sources, such as fermentation-derived beta-carotene. Africa remains an emerging market, with South Africa and Nigeria importing carotenoid premixes for poultry and aquaculture. However, infrastructure challenges and limited cold-chain logistics hinder the adoption of premium natural variants that require refrigerated storage.

Regulatory Landscape

Regulation is a key demand shaper in carotenoids because many end uses are governed as additives rather than conventional ingredients. In the United States, the FDA regulates carotenoids used for coloring under Title 21 of the Code of Federal Regulations, with beta-carotene listed under 21 CFR 73.95 as a color additive exempt from batch certification. Separate listings and use limitations apply for certain carotenoids used in animal food. This framework creates different compliance pathways across food, dietary supplements, and feed, so petition and labeling capabilities become a differentiator for suppliers.

In the European Union, carotenoids used as food additives must be authorized and included on the Union List (Annex II to Regulation (EC) No 1333/2008). Specifications are defined under Commission Regulation (EU) No 231/2012, with safety assessments handled through EFSA evaluations and re-evaluations. The EU system also evolves through technical updates to additive entries, including changes to annatto-related listings (E 160b) to reflect differing safety profiles. For manufacturers serving European retail and export markets, these updates can shift formulation choices and documentation requirements.

Value Chain Analysis

The carotenoids value chain starts with upstream feedstocks and biosynthesis inputs, such as marigold for lutein, paprika or chili peppers for capsanthin/capsorubin-type pigments, and microalgae such as Dunaliella salina for beta-carotene. It then moves through extraction or fermentation, purification, and downstream formulation into standardized formats like beadlets, powders, and emulsions. Large integrated producers, including BASF and DSM-Firmenich, combine chemical or fermentation production with stabilization and encapsulation to meet handling requirements across food, feed, and supplements. Specialist natural-ingredient suppliers and regional extractors focus on crop- and algae-derived sources.

Two bottlenecks tend to dominate. First, agricultural variability in natural sources (for example, monsoon-driven swings affecting marigold output) can flow through to oleoresin availability and pricing. Second, manufacturing concentration risk for synthetic and fermentation-derived carotenoids can tighten supply if production is disrupted. A recent example is BASF signaling further delays in restarting carotenoid (and vitamin) production at its Ludwigshafen site after a plant incident, highlighting how a disruption at a single large facility can tighten supply for downstream users that rely on long qualification cycles. To manage timing risk, buyers increasingly qualify dual-source supply and favor longer-stability formats, especially powder beadlets, to reduce spoilage and inventory write-offs during interruptions.

Competitive Landscape

The carotenoids market, with a moderate concentration, demonstrates moderate fragmentation. Multinational ingredient suppliers operate alongside specialized algae cultivators, fermentation start-ups, and regional extract producers. BASF, DSM-Firmenich, and Kemin Industries dominate the synthetic and fermentation-derived carotenoids segment. They utilize established regulatory dossiers and global distribution networks, supported by vertically integrated production processes that include chemical synthesis, precision fermentation, and spray-drying encapsulation.

DSM-Firmenich's 10,000-metric-ton beta-carotene facility in Switzerland runs at 92% capacity, serving food fortification and animal feed clients through multi-year contracts that ensure volume commitments and pricing stability. Meanwhile, smaller players like Cyanotech Corporation and Solabia-Algatech focus on premium natural astaxanthin derived from Haematococcus algae. They cater to nutraceutical and cosmetic brands, commanding prices between USD 4,000 and USD 7,000 per kilogram. These prices are justified by "100% natural" claims, enabling higher retail pricing. Strategic initiatives increasingly emphasize backward integration into fermentation and algae cultivation to secure supply and mitigate raw-material price volatility. In 2024, BASF announced a joint venture with a synthetic-biology firm in Singapore to commercialize astaxanthin derived from Corynebacterium glutamicum. The partnership aims to reduce production costs below USD 1,000 per kilogram by 2027, making natural astaxanthin a viable option for mainstream aquafeed.

Kemin Industries expanded its supercritical CO₂ extraction capacity in Iowa, removing hexane solvents from lutein production to meet organic and non-GMO certification standards. Opportunities also exist in pharmaceutical applications, where carotenoids are used as excipients in ophthalmic drug delivery and investigational therapies for metabolic disorders. However, regulatory pathways remain undefined, and clinical-trial costs exceed USD 50 million per indication. Emerging disruptors include precision-fermentation start-ups that license microbial strains to contract manufacturers, bypassing the need for capital-intensive cultivation infrastructure and accelerating the time-to-market for novel carotenoid variants such as fucoxanthin and astaxanthin diesters.

Carotenoids Industry Leaders

-

Givaudan SA

-

Döhler Group SE

-

BASF SE

-

Sensient Technologies Co.

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Fermentation and biotech-enabled supply looks like a key whitespace where suppliers are investing to improve consistency and support clean-label positioning, while reducing reliance on climate-sensitive crops. In 2026, GRA Nutra introduced AuraBC, positioned as a non-GMO fermentation-derived beta-carotene food color for yellow-to-orange applications. HSF Biotech also highlighted a microbial fermentation platform using a Blakeslea trispora strain for carotenoids. Together, these moves point to continued commercial momentum around “nature-identical” and fermentation-derived carotenoids that can work in reformulation programs for food, beverage, and supplements without the seasonality and traceability constraints tied to some agricultural extracts.

Aquaculture and animal nutrition remain a high-volume outlet where cost, regulatory authorization, and supply reliability guide purchasing decisions, supporting opportunity for scaled manufacturing and partnership-led supply. In May 2026, the EU adopted Implementing Regulation (EU) 2026/1148 renewing authorization for synthetic beta-carotene as a feed additive for all animal species for 10 years, sustaining a large compliant addressable base for established suppliers. On the natural side, Kuehnle AgroSystems announced Series B financing in July 2026 to scale dark-fermentation astaxanthin production, alongside a collaboration with Corbion, which underscores active capital formation aimed at expanding natural astaxanthin access beyond premium nutraceutical channels. At the same time, regulatory actions continue to open adjacent colorant options, such as the FDA final rule effective March 23, 2026 authorizing beetroot red for human foods. This increases competitive pressure on carotenoids in certain red-shade applications and raises the value of performance-in-use advantages like stability in processing and standardized dosing in premixes.

Recent Industry Developments

- July 2026: Kuehnle AgroSystems announced the closing of a Series B financing round to scale commercial production of natural astaxanthin using its dark-fermentation approach and to support a strategic collaboration with Corbion. The funding supports capacity scale-up and process industrialization, key constraints for expanding natural astaxanthin beyond premium nutraceutical and cosmetics channels. It also signals continued partnering between biotech developers and established ingredient companies to accelerate commercialization and downstream market access.

- July 2025: BASF outlined plans to restart carotenoid production at its Ludwigshafen site following the 2024 incident that disrupted output. The restart timeline and subsequent ramp-up period shaped supply assurance planning for customers in food fortification and animal nutrition, where ingredient qualification cycles are long. The update also reinforced the role of large integrated sites in global carotenoid availability, along with the need for inventory recovery after disruptions.

- May 2024: Cepham launched Luteye, an eye-health formulation combining lutein and zeaxanthin with extra virgin olive oil enriched with oleocanthal. The product targets age-related eye-health positioning, aligning with supplement category demand tied to macular pigment formulations. It also reflects continued innovation in delivery matrices and combination concepts designed to differentiate carotenoid-based SKUs in a crowded nutraceutical shelf.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the carotenoids market is defined as the value of carotenoid ingredients sold into downstream uses, covering both natural and synthetic carotenoids used mainly for coloring and functional benefits across key end-use industries.

Scope exclusions: We exclude crude oleoresin type extracts and carotenoid-rich whole biomass sold as a food ingredient rather than a defined carotenoid ingredient.

Segmentation Overview

-

By Type

- Astaxanthin

- Beta-carotene

- Canthaxanthin

- Lutein

- Lycopene

- Zeaxanthin

- Others

-

By Form

- Powder

- Liquid

-

By Source

- Synthetic

- Natural

-

By Application

- Food and Beverage

- Dietary Supplement

- Animal Feed

- Personal Care and Cosmetics

- Pharmaceuticals

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research sets the ground rules for what is counted and helps build the first view of demand and supply signals by application. We referred to public sources such as Food and Agriculture Organization statistics, UN Comtrade trade data, USDA and EU food and feed market publications, and FDA and European Commission regulatory pages for additives and labeling.

To make the numbers usable in a model, we also reviewed company annual reports, investor presentations, and product specification documents that describe typical grades and use cases. When needed, we checked patent databases to track where production routes and formulations are shifting. For commercial sanity checks, we used a paid subscription for company financials and for import-export shipment level checks to cross-check volumes and the direction of pricing by grade. The sources listed above are illustrative, and many other public and paid references were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to test the desk assumptions that most often move the market value, especially application mix, typical inclusion rates, and pricing by grade (natural versus synthetic). We spoke with stakeholders across ingredient manufacturing, distributors, and downstream buyers in food, supplements, and feed, then compared the inputs across major consuming regions to keep the final view consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | APAC: 46% |

| Mid tier: 55% | Functional/Unit leaders: 25% | EMEA: 31% |

| Smaller Players: 16% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where consumption pools are reconstructed by end-use industries and then converted into carotenoid demand using typical dosage and formulation shares. We used market fingerprints such as production and trade indicators for key raw materials, food and beverage output trends, animal feed production volumes, and supplement category growth, which are then mapped to carotenoid usage intensity and price bands.

To keep totals realistic, we ran selective bottom-up approximations in parallel. These included sampled supplier revenue roll-ups, channel checks for average selling prices by type, and volume times price builds for a few high-usage applications. We then adjusted where coverage gaps existed. Forecasts were developed using scenario analysis supported by expert views on natural share shifts, pricing pressure, regulatory acceptance, and demand growth in supplements and aquaculture feed. The model was re-run under each scenario to keep the CAGR and yearly steps aligned to the drivers.

Data Validation & Update Cycle

Outputs are validated through a set of checks that compare the model to independent signals, including trade direction, reported capacity movements, and application demand proxies, so large jumps are questioned before sign-off. If a variance looks unusual, assumptions are reviewed again, and targeted re-contacts are triggered to retest the specific input that caused the swing.

Each report is refreshed annually. Interim updates are made when a material event changes supply, pricing, or regulatory access. Before delivery, a final analyst review is completed to ensure recent developments are reflected and the latest year values are internally consistent across regions and applications.

Mordor Intelligence's Carotenoids Market Market Size Versus Other Published Estimates

Published market sizes for carotenoids can differ widely because the same term is used for different product forms, and then pricing and application boundaries get mixed together. Differences typically come from whether studies include crude extracts, whole-biomass products, or only refined carotenoid ingredients, and whether they treat natural and synthetic grades using the same pricing logic.

The benchmark table shows a wide spread, and in Mordor Intelligence's model, totals stay tied to ingredient-level carotenoids sold into food, supplements, feed, personal care, and pharma, while excluding crude oleoresins and whole biomass that can inflate value when counted as carotenoids.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.15 B (2026) | |

| Industry Research Publisher A | USD 3.26 B (2024) | Uses a broader definition that appears to roll up more adjacent categories and applies a different base year, which can lift totals when natural and synthetic mixes and their price points are assumed differently. |

| Global Publisher B | USD 1.72 B (2025) | Uses a narrower value base and a different forecast window, and the lower figure can result when application coverage and year-average pricing assumptions are more conservative or not fully aligned to ingredient grade splits. |

Taken together, the range is mainly explained by scope cut lines and how prices are carried across grades and applications year to year. Our approach keeps the value traceable to a defined ingredient basket, with demand pools and price bands that can be rechecked and updated as new signals emerge.

Key Questions Answered in the Report

How large is the carotenoids market in 2026?

The carotenoids market size stands at USD 2.15 billion in 2026 and is projected to reach USD 2.68 billion by 2031.

Which carotenoid type holds the largest share?

Astaxanthin leads, accounting for 28.31% of 2025 revenue due to its dual use in salmon feed and sports-nutrition supplements.

What drives the fastest growth within applications?

Dietary supplements are the fastest-growing application, advancing at a 6.35% CAGR through 2031 on the back of eye-health and performance-nutrition demand.

Which region is expected to grow most rapidly?

Asia Pacific is forecast to post a 6.92% CAGR through 2031, propelled by expanding aquaculture in China and Southeast Asia.

Page last updated on: