Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 21.88 Billion |

| Market Size (2031) | USD 27.4 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

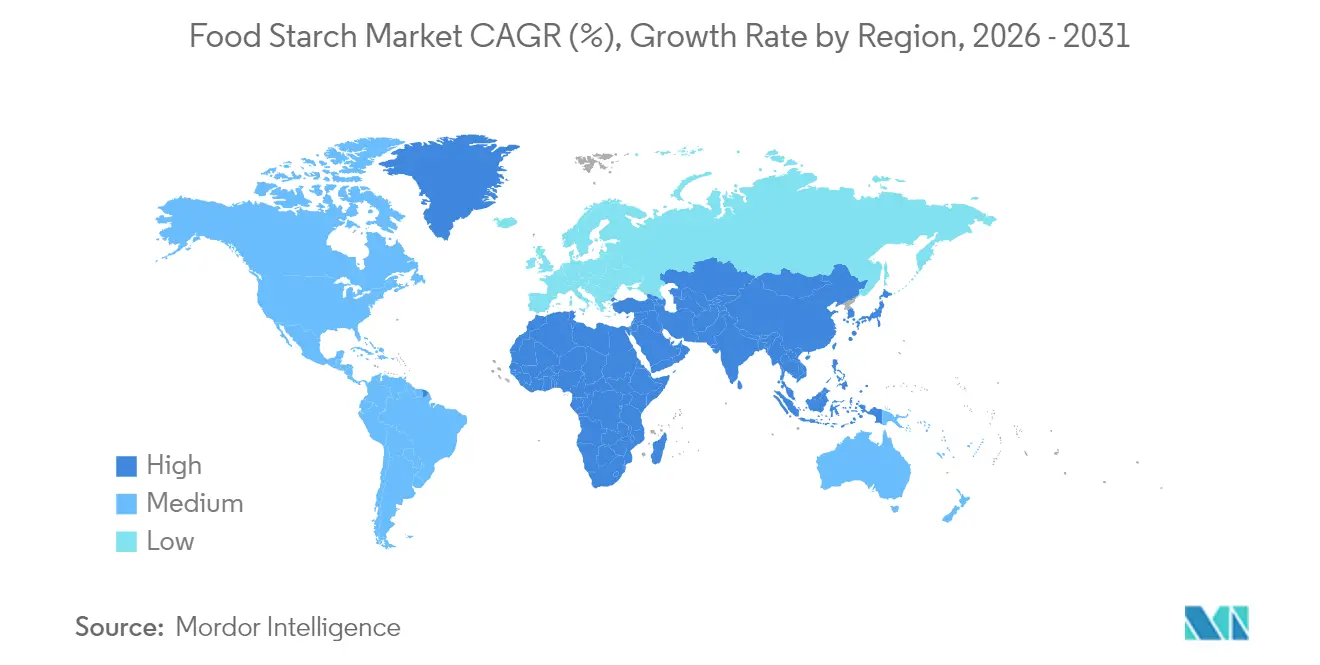

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Starch Market Analysis by Mordor Intelligence

food starch market size in 2026 is estimated at USD 21.88 billion, growing from 2025 value of USD 20.92 billion with 2031 projections showing USD 27.4 billion, growing at 4.59% CAGR over 2026-2031. The market growth is driven by consistent demand for texture-enhancing ingredients in processed foods, baked goods, and plant-based alternatives. Modified starches dominate the market due to their stability during freeze-thaw cycles, high-shear processing, and long-term storage. While North America represents the largest consumption region, the Asia-Pacific market exhibits the highest growth rate, supported by increasing urbanization and packaged food adoption. Though raw material price fluctuations pose challenges, manufacturers address these through agricultural diversification and improved processing methods that align with clean-label consumer preferences.

Key Report Takeaways

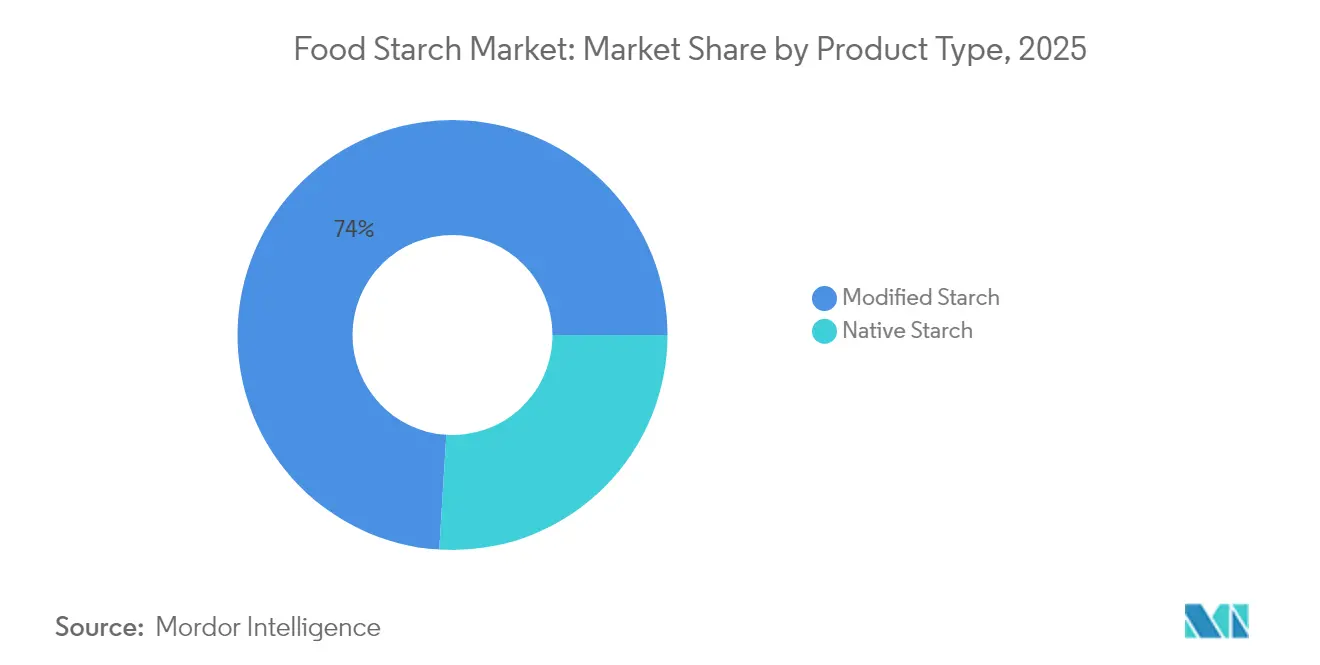

- By product type, modified starch held a 74.02% food starch market share in 2025 and is poised for the fastest 5.55% CAGR through 2031.

- By source, maize accounted for 72.30% of the food starch market size in 2025, while potato starch is projected to expand at a 5.28% CAGR.

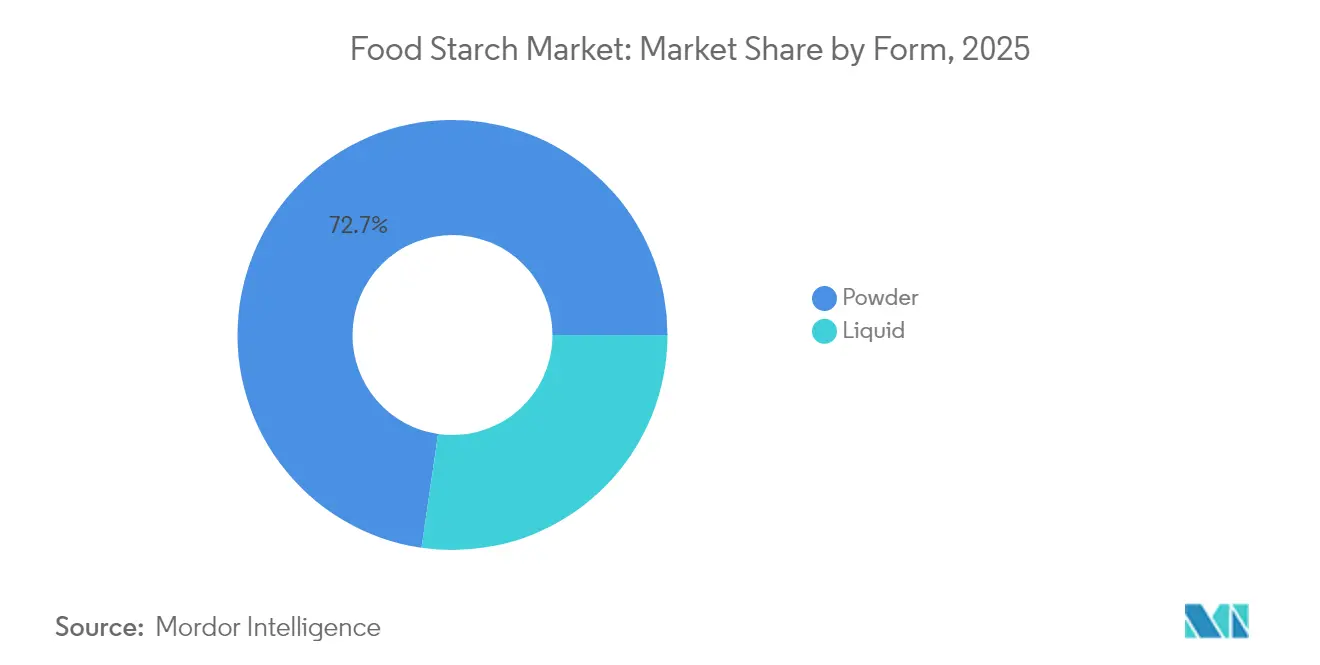

- By form, the powder segment controlled 72.70% of the 2025 food starch market, yet liquid formats will post a 5.00% CAGR to 2031.

- By application, bakery and confectionery dominated with 33.05% market share in 2025; pharmaceutical uses are set to rise at a 5.98% CAGR.

- By geography, North America commanded 31.55% of the 2025 share, whereas Asia-Pacific will record the highest 5.60% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Starch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenience and ready-to-eat food products | +0.6% | Global, with the highest impact in North America and Europe | Medium term (2-4 years) |

| Increase in demand for clean label products | +0.5% | North America and Europe, with growing influence in Asia-Pacific | Long term (≥ 4 years) |

| Surging demand for modified starch in bakery products for enhanced texture and quality | +0.4% | Global, with a concentration in Europe and North America | Medium term (2-4 years) |

| Plant-based and vegan diet trends strengthen natural starch consumption | +0.3% | North America, Europe, with emerging impact in Asia-Pacific | Long term (≥ 4 years) |

| Enhanced processing technologies enable high-performance modified starches | +0.3% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Health-focused snacking spurs uptake of functional starch ingredients | +0.2% | North America, Europe, with a growing influence in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenience and Ready-to-Eat Food Products

The accelerating pace of modern lifestyles is fundamentally reshaping food consumption patterns, with convenience foods emerging as a cornerstone of household food strategies rather than occasional indulgences. This shift is particularly evident in North America and Europe, where dual-income households now represent the majority, creating time constraints that drive demand for ready-to-eat meals and convenience foods that rely heavily on modified starches for texture stability and extended shelf life. Modified starches play a critical role in maintaining product integrity during microwave heating, freeze-thaw cycles, and extended storage capabilities that native starches cannot deliver consistently. The market is witnessing a strategic pivot toward starches that can withstand the rigorous processing conditions of convenience foods while maintaining clean label status, with companies reporting significant growth in their starch-based texturizers specifically formulated for convenience applications. The European food and drink industry, with a turnover of USD 1,379.87 billion and employing 4.7 million people, demonstrates the scale of this transformation toward convenience-oriented food production[1]Source: Food Drink Europe, “Data & Trends 2024,” fooddrinkeurope.eu.

Increase in Demand for Clean Label Products

Consumer focus on ingredient transparency has become a key factor in purchasing decisions, with buyers increasingly preferring products containing recognizable ingredients and clear sourcing information. Food manufacturers have responded to this shift by developing clean-label starches that match the performance of modified variants without chemical processing or E-number classifications. These clean-label alternatives aim to maintain the same functional properties while meeting consumer demands for simpler, more natural ingredients. For example, Tate & Lyle's CLARIA Functional Clean-Label Starch products provide similar functionality to modified starches while reducing carbon emissions by 35% and water consumption by 34% in their new CLARIA G range. The clean label trend now encompasses both ingredient simplicity and environmental sustainability, requiring starch manufacturers to address both aspects in their product development. This dual focus has led to increased investment in research and development to create innovative solutions that satisfy both consumer preferences and environmental considerations.

Surging Demand for Modified Starch in Bakery Products for Enhanced Texture and Quality

Modified starches serve as essential functional ingredients in the bakery industry, enhancing product quality and addressing operational challenges, particularly in premium offerings with extended shelf life. These ingredients improve moisture retention in baked goods, especially in gluten-free products, where they provide structural support while maintaining desired sensory characteristics. The growing gluten-free market, which now includes both celiac patients and health-conscious consumers, has increased the demand for modified starches. Modified starches offer superior stability during freezing and thawing cycles, making them valuable for frozen bakery products. Additionally, they contribute to improved dough handling properties and enhanced crumb structure in various baked goods. The development of cold-water swelling starches has simplified manufacturing processes by eliminating cooking steps while preserving product quality. These starches also help reduce production costs, minimize energy consumption, and ensure consistent product quality across different batches.

Plant-Based and Vegan Diet Trends Strengthen Natural Starch Consumption

The plant-based food revolution has created unprecedented opportunities for starch producers, as manufacturers seek plant-derived ingredients to replace animal-based components in formulations while maintaining familiar textures and mouthfeel. Starches play a pivotal role in mimicking the structural and textural properties of animal proteins in plant-based alternatives, with modified starches enabling the creation of convincing meat analogs that satisfy consumer expectations for taste and texture. The trend extends beyond meat alternatives to plant-based dairy products, where starches provide the creamy texture and stability consumers expect, with companies developing specialized formulations to enhance gelling and mouthfeel in dairy alternatives. This shift toward plant-based formulations is driving innovation in starch modification techniques that can deliver animal-product-like functionality while maintaining clean label credentials.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal dependency ofstarch corps affects availability and cost | -0.3% | Global, with the highest impact in regions with extreme weather patterns | Short term (≤ 2 years) |

| Rising popularity of low-carb and keto diets poses a major challenge | -0.2% | North America and Europe primarily | Medium term (2-4 years) |

| Consumer inclination towards whole food and fresh alternatives | -0.2% | North America and Europe, with emerging influence in Asia-Pacific | Long term (≥ 4 years) |

| Complex research and development and costly innovation deter small manufacturers | -0.1% | Global, with the highest impact on emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal Dependency of Starch Corps Affect Availability and Cost

The food starch market faces significant vulnerability to climate volatility and seasonal fluctuations that directly impact raw material availability and pricing stability The USDA projects corn prices to start at USD 3.90 per bushel in 2025, with a gradual rise to USD 4.30 by 2030, reflecting ongoing volatility in agricultural commodity markets that directly impacts starch production costs[2]Source: U.S. Department of Agriculture, “Long-Term Projections 2025-2030,” usda.gov. Climate-related disruptions are becoming more frequent, affecting crop yields and quality, which in turn impacts starch extraction efficiency and product consistency. Forward-thinking companies are addressing this constraint through geographical diversification of supply chains and investments in climate-resilient crop varieties, though these strategies require significant capital investment and multi-year implementation timelines. The European starch industry exemplifies these challenges, with processors facing rising raw material and energy costs driven by geopolitical tensions and market volatility.

Rising Popularity of Low-Carb and Keto Diets Poses a Major Challenge

The sustained momentum of ketogenic and low-carbohydrate dietary patterns represents a structural challenge for the starch market, particularly in North America and Europe, where these approaches have gained mainstream adoption beyond their initial niche status. This dietary shift has prompted starch producers to develop innovative formulations with reduced glycemic impact and enhanced nutritional profiles to maintain relevance in health-conscious market segments. Companies are increasingly investing in resistant starch variants that function as dietary fiber rather than digestible carbohydrates, allowing them to position these ingredients as compatible with lower-carbohydrate dietary approaches. The challenge for manufacturers lies in communicating these nuanced nutritional distinctions to consumers who may categorically avoid products they perceive as starch-heavy without understanding the functional and nutritional differences between starch variants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modified Starch Drives Value-Added Growth

Modified starch accounts for 74.02% of the market share in 2025, driven by its enhanced functionality and versatility across food applications compared to native starch. The segment is projected to grow at a CAGR of 5.55% from 2026-2031, surpassing the overall market growth rate. This expansion reflects manufacturers' focus on value-added starch derivatives that enable premium pricing. Modified starches provide critical functional benefits, including freeze-thaw stability, texture control, and resistance to processing conditions - capabilities that native starches cannot reliably deliver. The superior performance characteristics of modified starches make them essential ingredients in processed foods, bakery products, and convenience foods. Their ability to withstand various processing conditions while maintaining desired texture and stability properties has established them as indispensable components in modern food manufacturing.

Native starch maintains its market presence in applications requiring minimal processing, particularly in clean-label formulations that avoid chemical modifications. The segment's growth corresponds with organic food trends, as consumers favor clean-label products, with organic certification being the primary clean-label indicator. The advancement of physical modification methods, such as heat moisture treatment and cold plasma technology, is broadening native starch applications in premium food products while meeting clean label standards. The increasing consumer demand for natural and minimally processed ingredients has created opportunities for native starch in organic foods, natural beverages, and clean-label snack products. Food manufacturers are investing in research and development to enhance the functional properties of native starches through physical modifications, aiming to bridge the performance gap with modified starches while maintaining a clean label status.

By Source: Maize Dominance Meets Potato Innovation

The maize segment holds a 72.30% market share in 2025, driven by its cost-effectiveness, reliable supply, and well-established processing infrastructure. Corn starch derivatives benefit from high crop yields and efficient agricultural practices, creating economies of scale that exceed other starch sources. The segment continues to grow through technological advancements, including the development of specialized non-GMO corn starch formulations for dairy and alternative dairy products to improve texture and mouthfeel. The market players are expanding their production capacity to cater to the rising demand for corn starch.

The potato starch market is projected to grow at a CAGR of 5.28% during 2026-2031, driven by its functional properties and increasing demand for non-GMO ingredients. The functional properties of potato starch include its excellent thickening capabilities, neutral taste, and high binding strength, making it valuable in food processing applications. Wheat starch and alternative sources, such as arrowroot, cater to specific market segments, each offering distinct characteristics for various industrial applications. The development of arrowroot starch nanocrystals for edible bioplastic straws demonstrates the market's shift toward sustainable alternatives to conventional plastics, addressing growing environmental concerns and regulatory pressures on single-use plastics.

By Form: Powder Stability Versus Liquid Convenience

Powder form starch commands a market share of 72.70% in 2025, attributed to its storage stability, extended shelf life, and established handling protocols in food manufacturing facilities. The powder format enables diverse applications across processing conditions and remains the industry standard. The versatility of powder starch extends to various food applications, including bakery products, confectionery, and processed foods. Recent powder starch innovations focus on improved dispersibility and reduced dusting during handling, addressing manufacturers' operational requirements. Advancements in particle engineering have yielded powdered starches with enhanced functionality, including cold-water swelling properties that streamline production processes. These improvements have led to better process control, reduced energy consumption, and increased production efficiency in food manufacturing operations.

Liquid starch formulations are projected to grow at a CAGR of 5.00% from 2026-2031, the highest growth rate in the form segment. This expansion is driven by their efficient integration in high-throughput manufacturing environments. The adoption of automated liquid ingredient handling systems in food manufacturing facilities supports this trend, as liquid starches eliminate powder-related issues. The liquid format offers advantages in continuous processing systems, enabling precise dosing and uniform distribution in food products. Recent advances in liquid starch stabilization technology have addressed previous constraints by improving shelf life and cold temperature stability. These developments have expanded the application scope of liquid starches in ready-to-eat meals, dairy products, and beverage applications, contributing to their growing market adoption.

By Application: Bakery Leadership Amid Pharmaceutical Growth

The bakery and confectionery segment commands 33.05% of the modified starch market in 2025. Modified starch plays a crucial role in these products by improving texture, controlling moisture, and extending shelf life. In bakery applications, it enhances dough handling properties and final product quality. The ingredient is especially important in gluten-free products, where it provides necessary structure. Modified starch helps maintain product consistency, prevents staling, and improves the overall mouthfeel of baked goods. The consumption of bakery products is increasing across the region, owing to the rising innovations. According to the DEFRA data from 2023, the Average purchase per person per week of cakes, buns, and pastries in the United Kingdom was 161 grams.

The pharmaceutical segment is projected to expand at a 5.98% CAGR from 2026 to 2031, driven by the increasing adoption of modified starch in drug delivery systems and as excipients. Modified starch serves as a binding agent, disintegrant, and film-forming material in pharmaceutical formulations. It helps control drug release rates, improve tablet compression, and enhance the stability of pharmaceutical products. Modified starch also finds applications in snacks, soups, sauces, dressings, dairy products, and meat products, where it delivers specific functional benefits tailored to each product category. In these applications, it acts as a thickener, stabilizer, and texture modifier, contributing to product consistency and quality.

Geography Analysis

North America holds a 31.55% share of the Global Food Starch Market in 2025, supported by its advanced food processing infrastructure and innovation ecosystem. The region's market leadership comes from its established convenience food sector and the presence of major starch producers and food manufacturers. Clean label preferences shape product development, with companies focusing on functional native starches that provide modified starch capabilities while offering familiar ingredients. The region's agricultural framework and corn production provide a consistent raw material supply, with USDA projections indicating corn prices of USD 3.90 per bushel in 2025, increasing to USD 4.30 by 2030. The National Nanotechnology Initiative's USD 2.2 billion funding request for 2025 supports research and commercialization efforts, including food safety sensors and improved food contact materials.

Asia-Pacific demonstrates the highest growth rate with a 5.60% CAGR from 2026-2031, attributed to urbanization, expanding middle-class demographics, and changing food preferences toward processed and convenience foods. The region's food manufacturing industry continues to expand, with companies developing specialized starch formulations for local applications, including dent corn-based modified starch for sauces and pectin alternatives for gummies. Food security and nutrition initiatives increase demand for fortified products using modified starches, as seen in Senegal's fortified rice program for school meals.

Europe maintains substantial market share through its emphasis on sustainability and clean label innovations, reflecting strict regulations and consumer preferences. The region excels in organic starch production, with organic certification remaining the most recognized clean label designation. Sustainability initiatives include Tereos' commitment to net-zero greenhouse gas emissions by 2050 and sourcing deforestation-free agricultural materials by 2025. South America and the Middle East and Africa regions show growth potential as their food processing capabilities expand and consumer purchasing power increases.

Competitive Landscape

The global food starch market shows moderate fragmentation. This market structure enables regional specialists to compete effectively with multinational corporations through targeted innovation and local supply chain advantages. Major players in the market include Cargill, Incorporated, Roquette Frères, Ingredion Inc., Archer Daniels Midland Company, and Tate & Lyle Plc. Regional players leverage their understanding of local preferences and market dynamics to maintain strong market positions. Companies across the market are shifting toward clean label and functional starches, with substantial investments in acquisitions and development projects focused on texture and health-oriented solutions.

The market shows substantial growth potential in specialized applications, particularly pharmaceutical excipients and biodegradable packaging, where starch properties effectively meet emerging requirements beyond traditional food applications. Companies are expanding their research and development capabilities to capture these opportunities and develop innovative solutions. The competitive landscape is evolving through strategic partnerships and technology investments, with companies focusing on sustainability initiatives and environmental considerations as key differentiators in the market.

Companies are implementing comprehensive sustainability programs, focusing on responsible sourcing, energy-efficient production processes, and waste reduction initiatives. The integration of advanced processing technologies enables manufacturers to enhance product quality, reduce operational costs, and meet evolving consumer demands for sustainable production methods.

Food Starch Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

Ingredion Inc.

Tate & Lyle Plc

Roquette Freres

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cargill opened a new corn milling plant in Gwalior, Madhya Pradesh, operated by Indian manufacturer Saatvik Agro Processors, to meet increasing demand from India's confectionery, infant formula, and dairy industries.

- March 2025: Ingredion partnered with the Austrian company Agrana to increase starch production in Romania, expanding its manufacturing presence in Eastern Europe to address the rising regional demand for specialty starches.

- February 2025: Linqing Deneng Golden Corn Bio Limited, a subsidiary of China Starch Holding Company, expanded its operations by opening two additional starch processing facilities. The company operates two cornstarch production lines at its existing facilities, with annual production capacities of 550,000 tonnes and 450,000 tonnes, respectively.

- August 2024: Al Ghurair Foods initiated construction of its Corn Starch Manufacturing Plant at Khalifa Economic Zones Abu Dhabi (KEZAD). The facility, which is the first corn starch plant in the region, aims to increase local food production capacity and support the UAE's National Strategy for Food Security.

Global Food Starch Market Report Scope

The global food starch market is segmented by type such as native starch, modified starch, starch derivatives, and starch sweeteners. The modified starch segment is further segmented into oligosaccharides, sugar polyols, starch sugars, and others. By source, the market is segmented into corn, wheat, potato, cassava, and other sources. By application, the market is segmented into confectionery, bakery, dairy, beverages, and other food and beverage applications.

Also, the study provides an analysis of the food starch market in the emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

By Type

| Native Starch |

| Modified Starch |

By Source

| Maize |

| Wheat |

| Potato |

| Others |

By Form

| Powder |

| Liquid |

By Application

| Bakery and Confectionary |

| Snacks |

| Soup, Sauces and Dressings |

| Dairy Products |

| Meat and Meat Products |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Native Starch | |

| Modified Starch | ||

| By Source | Maize | |

| Wheat | ||

| Potato | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Bakery and Confectionary | |

| Snacks | ||

| Soup, Sauces and Dressings | ||

| Dairy Products | ||

| Meat and Meat Products | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Food Starch Market size?

The food starch market is valued at USD 21.88 billion in 2026 and is forecast to reach USD 27.4 billion by 2031, advancing at a 4.59% CAGR.

Which starch type leads the market and which is expanding the quickest?

Modified starch commands the largest 74.02% share in 2025 and is also the fastest-growing segment, advancing at a 5.55% CAGR through 2031.

Which geographic region dominates sales, and where is the highest growth expected?

North America held 31.55% of global revenue in 2025, while Asia-Pacific is forecast to record the strongest 5.60% CAGR between 2026 and 2031.

How are clean label demands influencing product formulation?

Food manufacturers are shifting toward physically or enzymatically modified native starches that match the performance of conventional modified grades while appearing as familiar, chemical-free ingredients on labels.

Page last updated on: