Canned Pineapple Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Pineapple Market Analysis by Mordor Intelligence

The global canned pineapple market is anticipated to grow from USD 3.79 billion in 2025 to USD 3.99 billion in 2026, reaching USD 5.17 billion by 2031, with a CAGR of 5.33% during the forecast period from 2026 to 2031. This growth is primarily driven by increasing consumer demand for convenient, ready-to-eat fruit products with long shelf lives, offering ease of storage and year-round availability. The rising preference for packaged fruit products among busy consumers seeking quick meal solutions and low-preparation food options is a key factor supporting market expansion. Advancements in canning and food preservation technology are driving market growth by enhancing product quality, extending shelf life, and maintaining the natural taste, texture, and nutritional value of pineapple. Additionally, the growing popularity of tropical fruit flavors and heightened awareness of fruit-based nutrition are contributing to the increased consumption of canned pineapple products worldwide.

Key Report Takeaways

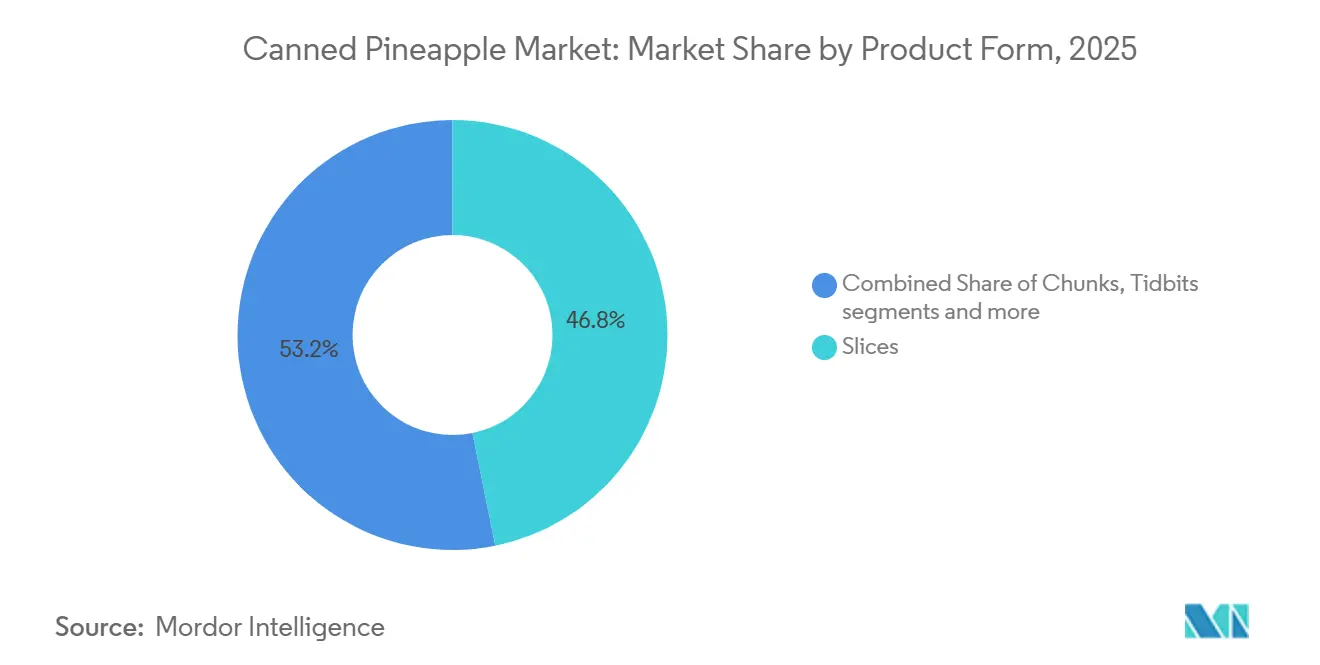

- By product form, slices led with 46.81% revenue share in 2025, while chunks are forecast to expand at a 5.42% CAGR through 2031.

- By packaging type, cans held 70.09% share in 2025, while cups and jars are projected to grow at a 6.19% CAGR through 2031.

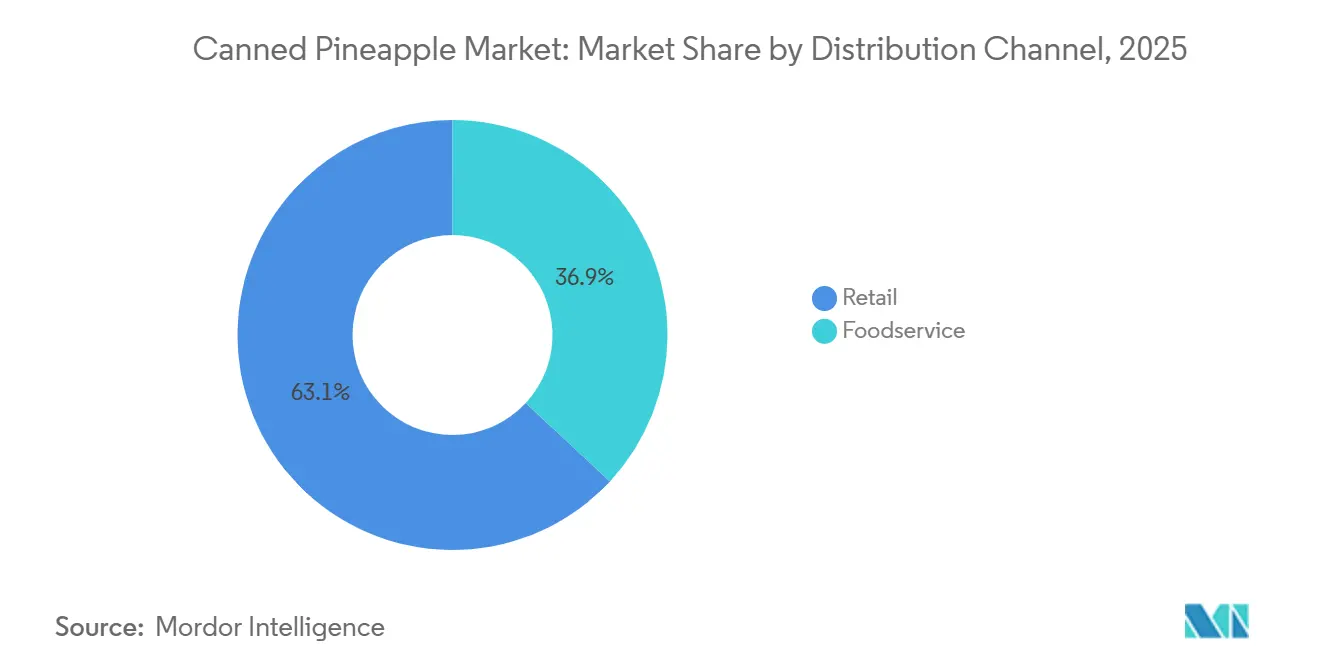

- By distribution channel, retail accounted for 63.08% share in 2025, while foodservice is projected to record the highest CAGR at 5.98% through 2031.

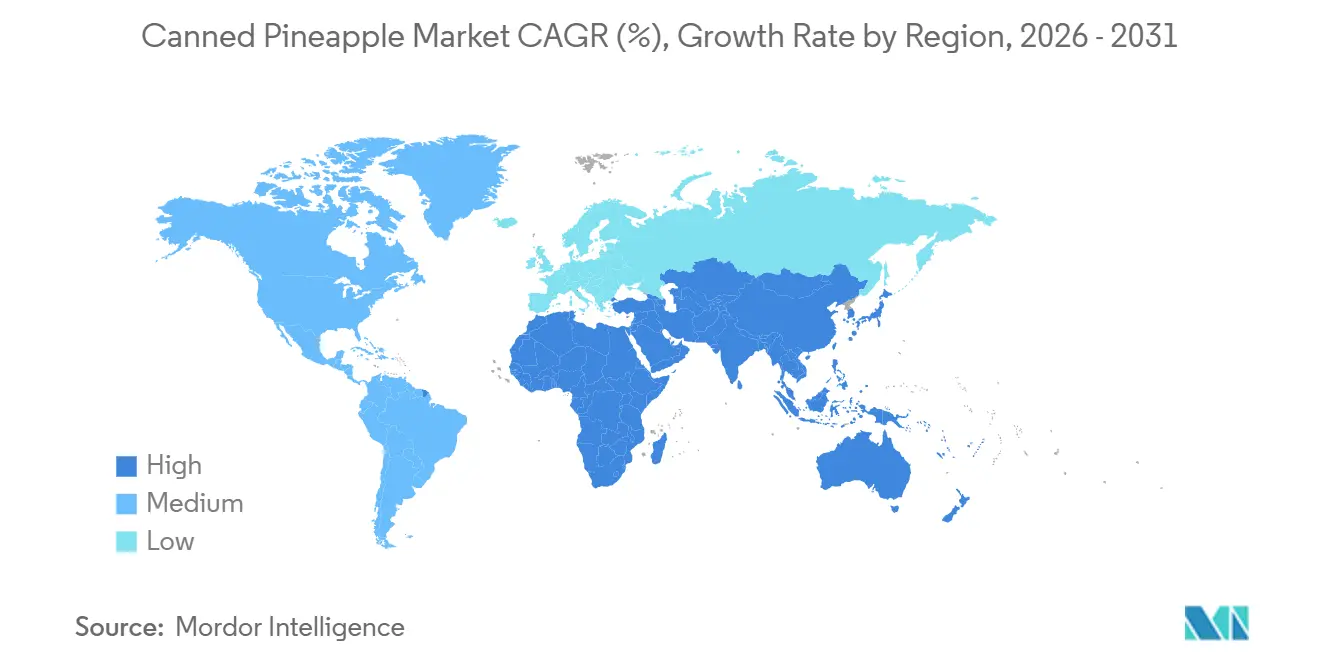

- By geography, Asia-Pacific held 33.01% share in 2025, while Middle East and Africa is forecast to expand at a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Canned Pineapple Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenient and ready-to-eat fruit products | +1.2% | Global | Short term (≤ 2 years) |

| Consumer preference for long shelf-life food products | +0.8% | Global, with accelerated uptake in Asia-Pacific and Middle-East and Africa | Medium term (2–4 years) |

| Advancements in canning and food preservation technologies | +0.7% | Global, with manufacturing intensity in Asia-Pacific | Medium term (2–4 years) |

| Product innovations including organic, no-added-sugar, and sustainably pack | +0.9% | North America and Europe, with growing uptake in urban Asia-Pacific | Medium term (2–4 years) |

| Rising consumer inclination toward healthy snacking | +0.7% | North America, Europe, and urban Asia-Pacific markets | Medium term (2–4 years) |

| Increasing demand for year-round availability of tropical fruits | +0.6% | Asia-Pacific core, spill-over to Middle-East and Africa and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for convenient and ready-to-eat fruit products

The increasing demand for convenient and ready-to-eat fruit products is driving the growth of the canned pineapple market. Consumers are prioritizing food options that require minimal preparation while offering extended shelf life, easy storage, and immediate consumption convenience. Canned pineapple aligns with these preferences by providing pre-processed, peeled, and ready-to-eat fruit products, which save preparation time and help reduce food waste. Factors such as busy lifestyles, urbanization, and a growing preference for quick meal solutions are further encouraging the adoption of packaged fruit products that can be easily integrated into daily diets. Moreover, canned pineapple ensures year-round availability and consistent quality, unaffected by seasonal variations, making it a reliable and accessible fruit option. The rising popularity of convenient pantry staples, combined with the demand for portable and easy-to-store food products, continues to support the global consumption of canned pineapple.

Consumer preference for long shelf-life food products

Increasing consumer preference for long shelf-life food products is a key factor driving the global canned pineapple market. Packaged food items that can be stored for extended periods without significant quality loss are gaining popularity, particularly due to the growing demand for convenient pantry staples and emergency food storage options. Canned pineapple provides extended usability, minimizes spoilage risk, and ensures year-round availability, making it an appealing choice for households seeking reliable fruit products with minimal storage challenges. According to Food Standards Australia New Zealand (FSANZ), canned foods with a shelf life exceeding two years do not require date marking [1]Source: Food Standards Australia New Zealand (FSANZ), "Canned foods: purchasing and storing", foodstandards.gov.au. As long as the can remains intact, these products retain their long shelf life even at room temperature, underscoring the preservation benefits of canned food products.

Advancements in canning and food preservation technologies

Modern canning technologies allow manufacturers to effectively preserve the natural flavor, texture, color, and nutritional properties of pineapple while extending shelf life for long-term storage and distribution. Advances in sterilization processes, vacuum sealing, aseptic packaging, and temperature-controlled preservation methods have improved the quality and consistency of canned pineapple products. These technologies also minimize microbial contamination and spoilage risks, enhancing consumer confidence in the safety and reliability of canned fruits. Additionally, automated processing systems and precision cutting technologies increase operational efficiency, reduce product waste, and ensure uniform product appearance and portion consistency. Manufacturers are also adopting lightweight packaging and improved lining materials to prevent flavor degradation and maintain product freshness over extended periods.

Product innovations such as organic, no-added-sugar, and sustainably packaged

Product innovation is significantly influencing the market as manufacturers introduce healthier, premium, and sustainability-focused offerings to address evolving consumer preferences. Increasing health consciousness is driving demand for canned fruit products with cleaner labels, reduced sugar content, and natural ingredient formulations. In response, companies are diversifying their portfolios with organic pineapple products, no-added-sugar options, and environmentally friendly packaging solutions that align with dietary and sustainability trends. For example, Dole plc provides canned pineapple slices with no added sugar, catering to consumers seeking healthier fruit options without additional sweeteners. These innovations enable manufacturers to attract health-conscious consumers who value convenient fruit products while preserving nutritional quality and natural flavor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns regarding added sugar and preservatives among health-conscious consumers | -0.9% | North America and Europe, with growing impact in urban Asia-Pacific | Medium term (2–4 years) |

| High competition from frozen, dried, and fresh pineapple alternatives | -0.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations affecting packaging and formulation | -0.4% | Europe, North America, and select Asia-Pacific markets | Medium term (2–4 years) |

| Risk of supply chain disruptions affecting raw material sourcing | -0.6% | Global, concentrated in Asia-Pacific supply origins | Short to medium term |

| Source: Mordor Intelligence | |||

Concerns regarding added sugar and preservatives

Concerns about added sugar and preservatives are significantly restraining the growth of the global canned pineapple market, as consumers increasingly prioritize healthier and more natural food options. Canned fruit products are often perceived as containing excessive sugar syrups, artificial preservatives, and processed ingredients, which can deter health-conscious consumers. Rising awareness of the health risks associated with high sugar consumption, such as obesity, diabetes, and other lifestyle-related conditions, further discourages the consumption of sweetened canned fruit products. The World Health Organization recommends that free sugars account for less than 10% of total daily energy intake for individuals consuming approximately 2,000 calories per day to maintain a healthy body weight. This growing emphasis on reducing sugar intake is driving consumers toward fresh fruits and minimally processed food alternatives, which are viewed as healthier and more natural options.

High competition from frozen, dried, and fresh pineapple alternatives

High competition from frozen, dried, and fresh pineapple alternatives is limiting the growth of canned pineapple products, as consumers increasingly explore diverse fruit formats that align with evolving lifestyle and dietary preferences. Fresh pineapple appeals to consumers seeking natural taste, freshness, and minimally processed options, particularly among health-conscious individuals who prioritize products perceived as natural and nutrient-rich. Meanwhile, frozen pineapple products are gaining traction due to their ability to retain flavor and nutritional quality while offering convenient storage and extended shelf life. Dried pineapple alternatives are also experiencing increased demand, driven by their portability, snack convenience, and alignment with healthy snacking trends. These alternative pineapple formats provide consumers with a broader range of product choices for various consumption occasions and storage needs, intensifying competition for canned pineapple products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Slices Dominate While Chunks Gain Culinary Traction

The slices segment accounted for a 46.81% value share of the global canned pineapple market in 2025, driven by strong consumer preference, convenience, visual appeal, and consistent product quality. Pineapple slices are popular due to their ability to retain the natural shape, texture, and recognizable appearance of the fruit, making them more appealing compared to crushed or chunk formats. Consumers increasingly favor fruit products that combine convenience with a fresh-like eating experience. Slices meet this demand through their ready-to-consume nature and ease of serving. Additionally, the segment benefits from the rising demand for portion-controlled fruit products that are easy to store and consume without further preparation.

The chunks segment is expected to be the fastest-growing category in the market, with a projected CAGR of 5.42% through 2031. This growth is attributed to increasing consumer preference for convenient, bite-sized fruit formats that offer versatility, ease of consumption, and a natural eating experience. Pineapple chunks are gaining popularity as they provide a balanced combination of texture, sweetness, and convenience. Their compact and uniform shape enhances ease of handling and portion control, appealing to modern consumers seeking practical and time-saving food options.

By Packaging Type: Cans Retain Their Grip as Alternative Formats Accelerate

The cans segment accounted for a dominant 70.09% share of the global canned pineapple market in 2025, supported by its durability, effective product protection, extended shelf life, and growing sustainability benefits. Metal cans remain a preferred choice for canned pineapple packaging due to their ability to provide strong barriers against moisture, oxygen, light, and contamination. This ensures the preservation of the fruit's taste, texture, nutritional value, and freshness over long storage periods. Additionally, the increasing emphasis on sustainable packaging has bolstered the segment's position. According to the International Aluminium Institute, aluminium can recycling reached 75% in 2025, underscoring the environmental and circularity benefits of metal packaging [2]Source: International Aluminium Institute,, "Global Aluminium Can Recycling Reaches 75% Marking-Major Step Toward Circular Economy", international-aluminium.org.

The cups and jars segment is projected to grow at a CAGR of 6.19% through 2031, driven by rising consumer demand for convenient, portable, and visually appealing packaging formats. Consumers are increasingly opting for single-serve and resealable fruit packaging solutions that offer ease of consumption, better portion control, and enhanced storage flexibility. These features are significantly contributing to the growth of cups and jars in the canned pineapple market. Such packaging formats cater to modern on-the-go lifestyles, enabling consumers to consume fruit products directly without the need for additional preparation or transferring to separate containers.

By Distribution Channel: Retail Leads While Foodservice Drives Fastest Incremental Demand

In 2025, the retail segment accounted for a dominant 63.08% share of the global canned pineapple market distribution value. This dominance is attributed to the growing consumer reliance on convenient and accessible purchasing channels for packaged food products. Retail outlets remain the primary point of purchase for canned pineapple due to their extensive product availability, organized displays, and the ability to offer a wide variety of packaging sizes, product forms, and brand options in one location. The segment's strong position is further reinforced by evolving consumer shopping behaviors that prioritize one-stop purchasing experiences and easy access to products for daily household consumption. Additionally, retail channels enhance product visibility and shelf presence, enabling consumers to efficiently compare quality, packaging, and pricing.

The foodservice segment is anticipated to be the fastest-growing distribution channel in the global canned pineapple market, with a projected CAGR of 5.98% through 2031. This growth is driven by the rising demand for convenient, consistent, and long shelf-life fruit ingredients in commercial food preparation environments. The segment's momentum is supported by the increasing preference for ready-to-use fruit products that reduce preparation time, minimize wastage, and enhance operational efficiency in large-scale food handling operations. Furthermore, the growth of fast-paced dining trends and the rising consumer demand for tropical fruit flavors are contributing to the higher adoption of canned pineapple through foodservice channels.

Geography Analysis

The Asia-Pacific region accounted for 33.01% of the global canned pineapple market value in 2025, underscoring its position as a major production hub and a rapidly growing consumption market. The region benefits from tropical climatic conditions that facilitate large-scale pineapple cultivation, ensuring a stable supply of raw materials for canning operations. Countries in Asia-Pacific have established advanced pineapple processing and preservation capabilities, enhancing supply chain efficiency and export competitiveness. According to the Food and Agriculture Organization (FAO), the Philippines, one of the largest global producers of pineapples, harvested approximately 2.9 million metric tons in 2024, demonstrating the region's agricultural strength in pineapple production [3]Source: Food and Agriculture Organization (FAO), "Leading countries in pineapple production worldwide", fao.org.

The Middle East and Africa region is expected to achieve the highest growth in the global canned pineapple market, with a projected CAGR of 6.98% through 2031. This growth is driven by increasing consumer demand for convenient, long shelf-life food products and rising awareness of fruit-based nutrition and healthy eating habits. Rapid urbanization and changing dietary patterns are fostering greater adoption of packaged fruit products that provide convenience and year-round availability. Additionally, shifting lifestyles and a growing preference for tropical fruit flavors are boosting the consumption of canned pineapple products. Expanding food distribution networks, exposure to international food trends, and rising demand for imported processed fruit products are further accelerating market growth in the region.

North America and Europe together represent the largest combined value pool for branded and premium canned pineapple products. This is supported by strong consumer preference for high-quality, convenient, and sustainably packaged fruit offerings. Consumers in these regions increasingly seek premium canned fruit products that emphasize natural ingredients, clean-label formulations, organic positioning, and superior product quality. The market is further driven by demand for convenient pantry staples that cater to busy lifestyles while offering nutritional value and tropical flavor appeal. Robust retail infrastructure, high penetration of branded packaged foods, and a growing willingness among consumers to pay for premium fruit products continue to support market value growth in both regions.

Competitive Landscape

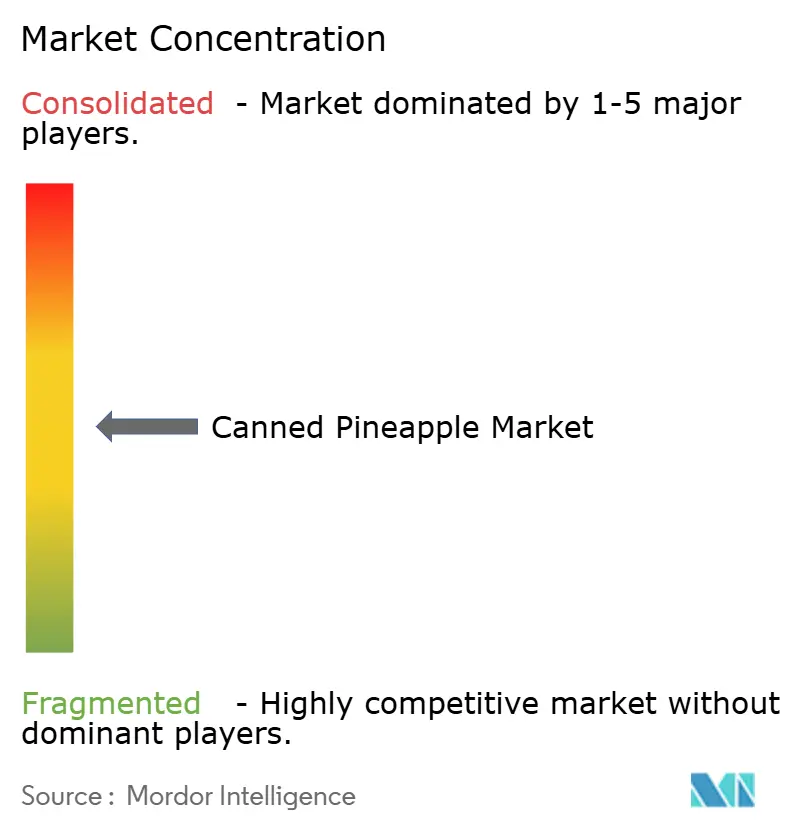

The global canned pineapple market is moderately concentrated, featuring a mix of multinational food companies and large-scale pineapple processors. These players compete based on product quality, processing efficiency, distribution capabilities, and packaging innovation. Key companies in the market include Great Giant Pineapple, Dole plc, Del Monte International GmbH, and Thai Pineapple Canning Industry. These firms maintain strong market positions through extensive pineapple sourcing, vertically integrated operations, and diverse product portfolios that address varying consumer preferences and packaging needs. Competition is increasingly focused on ensuring consistent product quality, year-round supply availability, and robust global distribution networks to meet the rising demand for convenient tropical fruit products.

Technological advancements are significantly influencing competition in the canned pineapple industry. Leading companies are investing in advanced fruit processing technologies, including automated sorting systems, precision cutting equipment, and improved sterilization and preservation methods. These innovations enhance operational efficiency while maintaining product freshness, texture, and nutritional value. Advances in canning processes are also enabling manufacturers to reduce waste, optimize production yields, and improve shelf-life stability, all while preserving the natural taste and appearance of pineapple products. Additionally, companies are adopting digital supply chain management, traceability systems, and quality control technologies to strengthen food safety standards and ensure consistent production quality.

Packaging innovation has emerged as a critical competitive factor in the global canned pineapple market. Manufacturers are focusing on improving convenience, sustainability, and product differentiation through packaging solutions. Lightweight cans, easy-open lids, resealable formats, and recyclable materials are being introduced to align with evolving consumer preferences and environmental sustainability goals. The growing demand for portion-controlled and portable packaging options is driving the development of cups, jars, and single-serve formats that enhance convenience and product appeal. Furthermore, manufacturers are prioritizing visually appealing packaging designs and transparent labeling to boost brand visibility and foster consumer trust.

Canned Pineapple Industry Leaders

-

Great Giant Pineapple (Sunpride)

-

Dole plc

-

Del Monte International GmbH

-

Thai Pineapple Canning Industry (TPC)

-

Tipco Foods PCL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Dole launched "Colada Royale," an innovative naturally bred hybrid pineapple variety specifically developed to replicate the distinctive flavors of a Piña Colada cocktail.

- October 2025: Premier Group announced plans to acquire RFG Holdings through a share-swap transaction, which will result in RFG being delisted from the JSE. Under the agreement, RFG shareholders will receive one Premier share for every seven RFG shares, giving them a collective 22.5% stake in the enlarged entity. RFG's brands include Rhodes canned vegetables and fruit juices, Pakco curry powders, and Man's Meal ready-to-eat pies.

Global Canned Pineapple Market Report Scope

Canned pineapple refers to mature, peeled, and cored pineapple that is cut into various shapes (rings, chunks, or crushed) and preserved in a liquid medium like juice or syrup. The canned pineapple market is segmented by product form, packaging type, distribution channel, and geography. Based on product form, the market is segmented into slices, chunks, tidbits, crushed, and spears and whole. Based on packaging type, the market is segmented into cans, cups and jars, and others. Based on distribution channel, the market is segmented into foodservice and retail. The retail segment is further segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Slices |

| Chunks |

| Tidbits |

| Crushed |

| Spears and Whole |

| Cans |

| Cups and Jars |

| Others |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Form | Slices | |

| Chunks | ||

| Tidbits | ||

| Crushed | ||

| Spears and Whole | ||

| By Packaging Type | Cans | |

| Cups and Jars | ||

| Others | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of canned pineapple by 2031?

The canned pineapple market is forecast to reach USD 5.17 billion by 2031, rising from USD 3.99 billion in 2026 at a 5.3% CAGR over the forecast period.

Which product form leads global demand for canned pineapple?

Slices led demand with 46.81% share in 2025 because they remain widely used in retail, pizza toppings, desserts, and foodservice garnish.

Which packaging format is growing the fastest?

Cups and jars are projected to grow at a 6.19% CAGR through 2031 as shoppers favor portion control, resealability, and visible product presentation.

Why is foodservice becoming more important for pineapple processors?

Foodservice is projected to grow at a 5.98% CAGR through 2031 because restaurants, caterers, and institutional kitchens need uniform cuts, stable Brix levels, and year-round supply.

Page last updated on: