Industrial Alcohol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 132.06 Billion |

| Market Size (2031) | USD 170.09 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Alcohol Market Analysis by Mordor Intelligence

The industrial alcohol market size is projected to grow from USD 128.34 billion in 2025 to USD 132.06 billion in 2026, reaching USD 170.09 billion by 2031, with a CAGR of 5.19% during the forecast period of 2026-2031. Growth is driven by the convergence of low-carbon fuel regulations in North America and Brazil with increasing demand for premium-grade solvents in the pharmaceutical and cosmetics industries. On the supply side, feedstock flexibility plays a critical role, with corn being predominant in the United States, sugarcane in Brazil, and molasses in India. Additionally, carbon-capture credits under the US 45Z Clean Fuel Production Tax Credit enhance margins for facilities capable of reducing life-cycle emissions below 50 g CO₂e/MJ. The industrial alcohol market is moderately concentrated, with the top five U.S. producers accounting for approximately 45% of production capacity. However, the presence of numerous mid-sized distillers globally leads to regional price competition, limiting global pricing power. Furthermore, corporate sustainability initiatives in the beauty and personal care industry are driving increased demand for bio-based preservatives, boosting the need for high-purity ethanols.

Key Report Takeaways

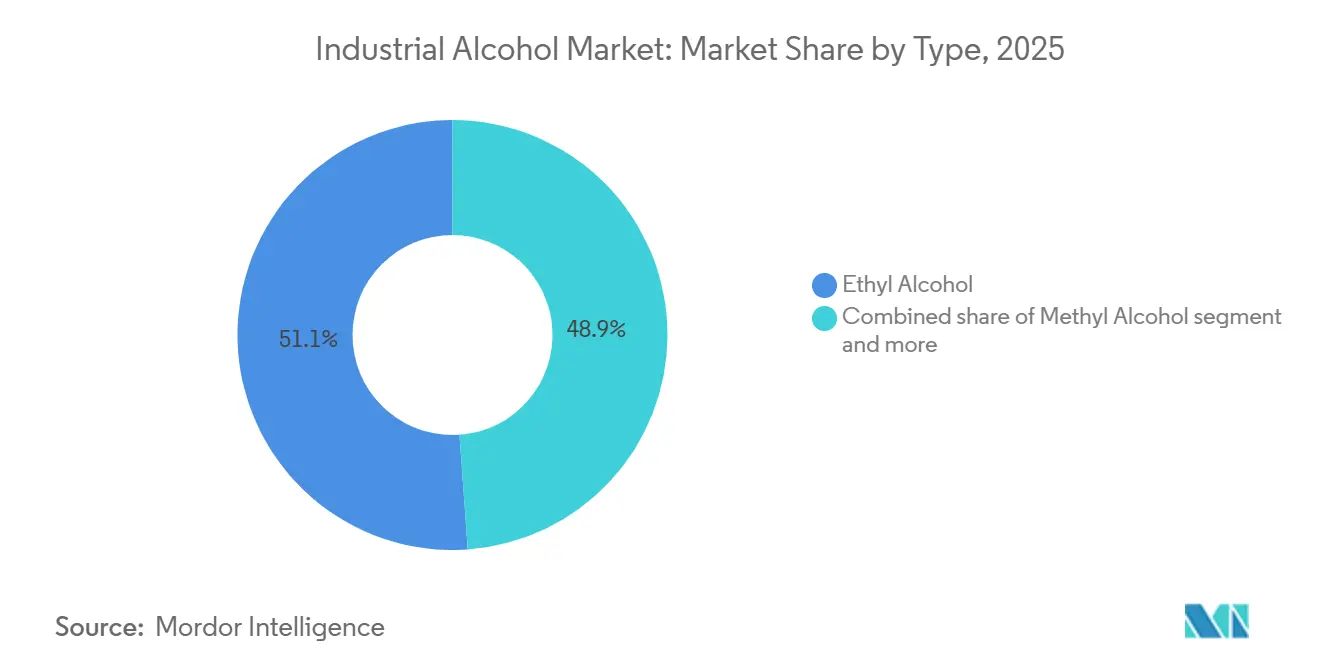

- By type, ethyl alcohol held 51.13% of the industrial alcohol market share in 2025 and is projected to post a 5.56% CAGR to 2031.

- By source, sugar and molasses feedstocks led with a 37.17% share in 2025, while grains are set to expand at a 6.12% CAGR between 2026 and 2031.

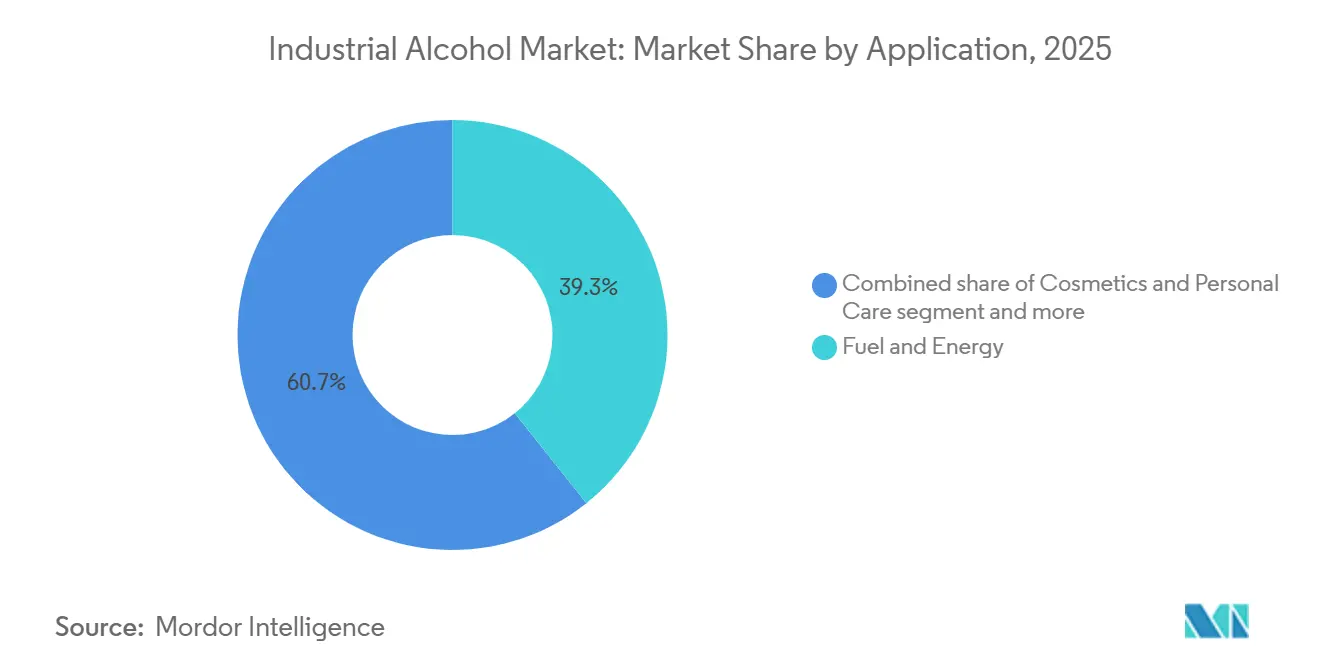

- By application, the fuel and energy segment dominated with 39.29% market share in 2025; cosmetics and personal care applications are poised for a 6.81% CAGR.

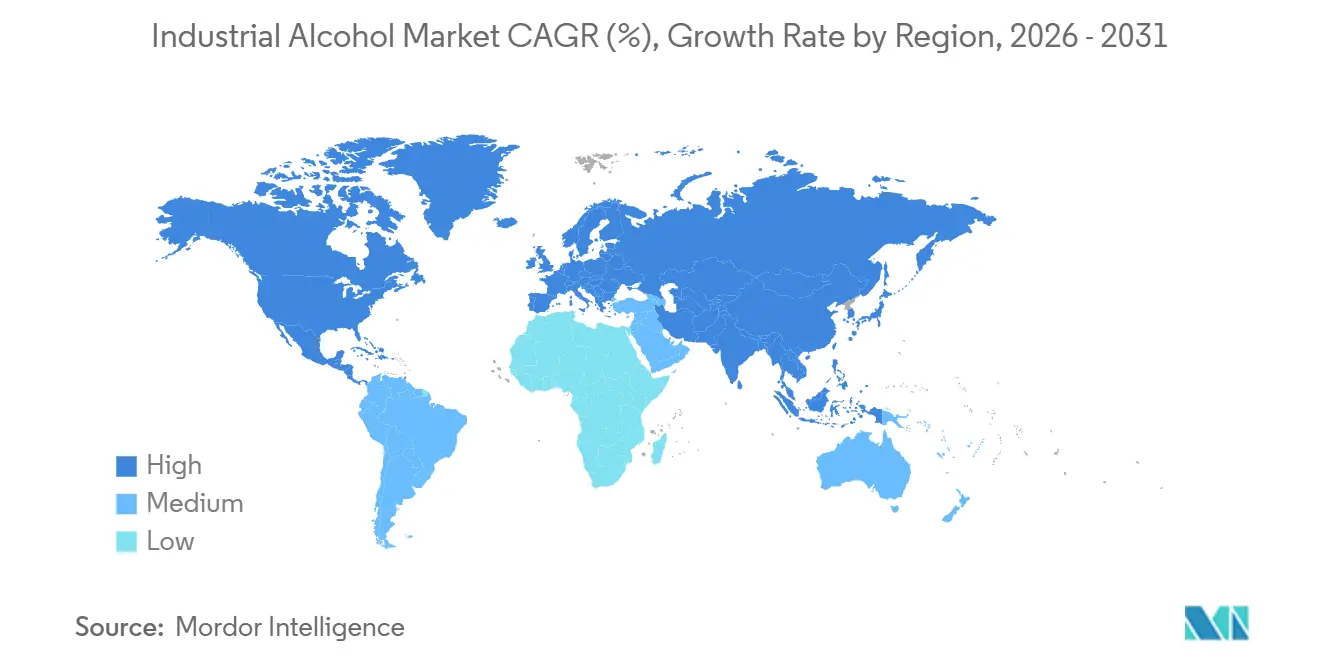

- By geography, Asia-Pacific contributed 40.41% of the 2025 market share, and North America is on track for the quickest regional upswing at a 5.58% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Alcohol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for industrial alcohol in biofuels | +1.8% | Global, with concentration in North America, Brazil, India, and ASEAN | Medium term (2-4 years) |

| Rising technological innovations in extraction processes | +0.9% | North America, Europe, Asia-Pacific (India, China) | Long term (≥ 4 years) |

| Abundant raw material availability | +0.7% | North America (corn belt), South America (sugarcane), Asia-Pacific (molasses, cassava) | Short term (≤ 2 years) |

| Government policies and incentives | +1.3% | Global, strongest in United States, Europe, India, Brazil, ASEAN | Medium term (2-4 years) |

| Emerging market expansions | +0.6% | Asia-Pacific (Southeast Asia, India), Middle East, Africa | Long term (≥ 4 years) |

| Increasing demand for sustainable and renewable products | +0.8% | Global, led by Europe, North America, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for industrial alcohol in biofuels

The biofuels market is driving increased demand for industrial alcohol due to mandatory blending requirements and carbon reduction targets in key economies. According to the U.S. Energy Information Administration, fuel ethanol production is projected to reach 1.05 million barrels per day by 2025 [1]Source: International Energy Agency, “Renewables 2024", IEA, iea.org. In the European Union, the ReFuelEU Aviation mandate requires a 2% sustainable aviation fuel (SAF) blending by 2025, with a target of 70% by 2050. Similarly, India's goal of achieving 20% ethanol blending by 2025 is expected to generate an annual demand of 240 billion liters, significantly impacting global supply chains. The alcohol-to-jet fuel pathway is also advancing, with LanzaJet's Freedom Pines facility set to produce 10 million gallons of sustainable aviation fuel annually starting in 2025. This rising demand is leading to supply constraints, particularly in corn-based ethanol production, as feedstock costs increase due to competition between food and fuel uses. To address regulatory requirements and access low-carbon fuel markets, ethanol producers are adopting carbon capture technologies, such as Green Plains' project to sequester 800,000 tons of CO2 annually.

Rising technological innovations in extraction processes

Advancements in extraction and purification technologies are enhancing the efficiency of industrial alcohol production while minimizing environmental impact and operational costs. In March 2025, ExxonMobil announced a USD 100 million investment in ultra-pure isopropyl alcohol production at its Baton Rouge facility, aiming for 99.999% purity levels to meet the demands of semiconductor manufacturing. Researchers at the Gwangju Institute of Science and Technology have improved the efficiency of converting CO2 into allyl alcohol using electrochemical processes, setting new performance benchmarks for large-scale production. The integration of artificial intelligence and machine learning in fermentation control systems is optimizing yield rates and reducing processing times, with RCM Technologies introducing capacity enhancement solutions for ethanol plants. Methanol-to-jet technology is emerging as an alternative to traditional Fischer-Tropsch processes, with ExxonMobil developing methods to convert alternative feedstocks into synthetic jet fuel components. These technological advancements are enabling producers to access higher-margin applications while improving resource utilization.

Abundant raw material availability

The growth in global agricultural productivity and the diversification of feedstock sources are creating favorable supply conditions for industrial alcohol production, despite regional disparities and climate-related challenges. For instnace, during the period, 2023-2024, Brazil processed 713 million tons of sugarcane, producing 35.3 billion liters of ethanol. Additionally, corn-based ethanol production reached 5.8 billion liters, highlighting successful feedstock diversification, as reported by the Energy Research Office [2]Source: Energy Research Office, "Analysis of Current Biofuels Outlook-Year 2023", www.epe.gov.br. The adoption of second-generation feedstocks, such as lignocellulosic biomass and agricultural waste, is increasing the availability of raw materials. Research on co-fermentation of waste tissue paper and food waste has shown a 46.5% ethanol yield, demonstrating the potential of municipal waste as a viable feedstock. Advances in synthetic biology and engineered microorganisms are enabling the use of non-agricultural feedstocks, reducing dependence on traditional crop-based inputs. In India, the establishment of nine new ethanol plants in Bihar is expected to create 50,000 jobs and reduce reliance on sugar mills by directly procuring crops from farmers.

Government policies and incentives

Policy frameworks are transitioning from mandate-driven approaches to carbon intensity-based incentives, emphasizing process innovation over compliance with volume targets. The US 45Z Clean Fuel Production tax credit, set to take effect on January 1, 2025, offers per-gallon credits based on lifecycle emissions reductions. Corn ethanol producers with carbon intensity scores below 50 grams CO2-equivalent per megajoule will qualify for the maximum credits. In the European Union, the RED III directive requires 42.5% renewable energy by 2030, including a transport sector sub-target of 29% renewable fuel intensity. This framework excludes food-crop ethanol from double-counting but allows advanced biofuels and recycled carbon fuels to benefit from multipliers. Moreover, for producers, the fluidity of policiesm, such as the timing of 45Z guidance in the US, can impact margins by 10-15 cents per gallon, highlighting the importance of regulatory monitoring alongside feedstock procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing and energy costs | -0.9% | Global, acute in Europe and energy-import-dependent Asia-Pacific | Short term (≤ 2 years) |

| Supply chain disruptions | -0.6% | Global, with elevated risk in single-feedstock regions (Argentina corn, Thailand molasses) | Short term (≤ 2 years) |

| Market fragmentation and intense competition | -0.4% | North America, Europe, India | Medium term (2-4 years) |

| Taxation and price controls | -0.5% | Emerging markets (India, Southeast Asia, Africa), selective EU states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High manufacturing and energy costs

Energy accounts for 25-35% of ethanol production cash costs, making distilleries highly sensitive to fluctuations in natural gas and electricity prices. European producers face electricity costs that are 2-3 times higher than those of their U.S. counterparts, creating a structural disadvantage that has led several facilities to reduce or idle capacity during periods of peak winter pricing. Strategic responses to this challenge vary: large integrated producers are co-locating with renewable natural gas sources or installing on-site solar energy systems, while smaller distillers are either exiting the market or consolidating operations. The volatility in energy costs poses a significant risk, as it can quickly turn a profitable quarter into a loss, especially for producers without long-term utility contracts, where adjustments to feedstock hedges may not be sufficient to offset the impact.

Supply chain disruptions

Feedstock logistics present significant challenges for just-in-time distillery operations. The 2024 low-water conditions on the Mississippi River caused barge shipment delays of 10-14 days, compelling Midwest ethanol plants to procure corn via rail at a premium of USD 0.30-0.40 per bushel. This additional cost reduced margins by 8-10 cents per gallon for producers lacking on-site storage. In 2025, Thailand's drought reduced molasses production by 18%, leading to increased imports from India and Pakistan, both of which faced export restrictions due to domestic sugar policy measures. The USMCA trade framework supports ethanol trade across North America; however, periodic disputes over country-of-origin labeling for blended fuels create regulatory uncertainty, discouraging cross-border investments. Producers with multi-feedstock facilities (corn, sorghum, wheat) or access to both rail and barge logistics experience 15-20% lower earnings volatility compared to those relying on single feedstocks or transport modes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ethyl Alcohol Drives Market Leadership

Ethyl alcohol accounted for a significant market share of 51.13% in 2025 and is projected to grow at a CAGR of 5.56% through 2031. This growth is attributed to its extensive use in fuel, pharmaceutical, and industrial applications. The segment's development is further supported by regulations promoting sustainable aviation fuel and rising demand for pharmaceutical manufacturing. Companies such as LanzaJet are advancing alcohol-to-jet technologies to convert ethanol into aviation fuel. Meanwhile, isobutyl alcohol and other specialty alcohols continue to cater to niche applications in the solvents, adhesives, and chemical intermediates markets.

The planned opening of European Energy's Kassø e-methanol facility in May 2025 highlights progress in methanol production through the integration of renewable energy and carbon capture technologies. Additionally, Korean researchers have made notable advancements in CO2-to-alcohol conversion efficiency, introducing innovative production methods that could impact the manufacturing costs of methanol and ethanol. Market competition has intensified as producers adopt carbon capture technologies and prioritize high-purity products for premium markets, while also striving to remain competitive in traditional fuel and solvent segments.

By Source: Sugar Feedstocks Lead Despite Grain Acceleration

Sugar and molasses maintained a 37.17% market share in 2025, supported by established processing infrastructure and efficient conversion economics. The grains segment demonstrates the highest growth potential, with a compound annual growth rate (CAGR) of 6.12% through 2031. In 2023, Brazil processed 713 million tons of sugarcane, producing 29.5 billion liters of ethanol, underscoring the efficiency of sugar-based feedstocks. Additionally, Brazil's corn-based ethanol production reached 5.8 billion liters, while U.S. facilities maintained an annual capacity of 18 billion gallons, with a 2% growth rate in 2023. Lignocellulosic biomass offers new opportunities through second-generation conversion technologies, with research indicating enhanced alcohol solubility via modified hydrothermal pretreatment processes.

Efforts to diversify feedstocks include Cargill's collaboration with the University of Minnesota on winter camelina and pennycress research, aimed at developing oilseed crops for renewable fuel production. Additionally, the company's partnership with Virent focuses on utilizing corn dextrose as a feedstock for BioForming technology, enabling the conversion of plant sugars into renewable gasoline, jet fuel, and biochemicals. However, European producers face rising feedstock costs due to adverse harvest conditions. For instance, Ukraine's wheat production decreased to 22.3 million tons, and its corn supply declined to 22.9 million tons, highlighting significant supply chain risks.

By Application: Fuel Dominance Amid Cosmetics Growth

The fuel and energy segment accounted for a 39.29% market share in 2025, driven by biofuel mandates and sustainable aviation fuel (SAF) requirements. The cosmetics and personal care segment is expected to grow at a compound annual growth rate (CAGR) of 6.81% through 2031, reflecting expanding applications beyond traditional energy uses. Summit Next Gen's USD 1.6 billion ethanol-to-SAF facility in Texas, utilizing Honeywell's conversion technology, is North America's largest ethanol-to-jet fuel production plant. The pharmaceuticals segment is witnessing growth due to rising demand for high-purity alcohols in drug manufacturing and sanitization.

Alto Ingredients has increased its specialty alcohol production by 4 million gallons year-over-year. In the food and beverage industry, ethanol is used for flavor extraction and preservation, while the solvents and chemicals segment supports industrial cleaning and manufacturing processes. Praj Industries has initiated jet fuel production from alcohol, highlighting the intersection of traditional alcohol applications and the SAF market. The adoption of carbon capture technologies at production facilities enables access to premium low-carbon markets across various applications, as demonstrated by Green Plains' project to sequester 800,000 tons of CO2 annually.

Geography Analysis

Asia-Pacific held a 40.41% share of the industrial alcohol market in 2025, driven by the availability of agricultural feedstock, government biofuel mandates, and robust manufacturing capabilities in countries like China, India, and Southeast Asia. India's ethanol production reached 6.35 billion liters in 2024, leading the region's growth in ethanol production through the utilization of sugarcane and grain. The region benefits from competitive advantages such as lower production costs, supportive regulations, and proximity to end-use markets, solidifying its role as a global production hub for industrial alcohol applications.

North America is projected to exhibit the fastest regional growth, with a CAGR of 5.58% through 2031, supported by advancements in carbon capture technologies, sustainable aviation fuel mandates, and premium application development. In 2023, the U.S. biofuels production capacity increased by 7% to 24 billion gallons annually, with renewable diesel and other biofuels rising by 44%, while fuel ethanol capacity reached 18 billion gallons, according to the U.S. Energy Information Administration. ExxonMobil's USD 100 million investment in ultra-pure isopropyl alcohol production at Baton Rouge aims to support semiconductor manufacturing applications. According to Government of Canada data, the excise duty adjustments in Canada, effective April 2025, will limit rate increases to a maximum of 2% for an additional two years, offering regulatory stability for producers [3]Source: Government of Canada, EDN100 Adjusted rates of excise duty on spirits and wines", www.canada.ca.

Europe faces challenges related to feedstock cost pressures and regulatory compliance while advancing sustainable production processes and carbon management systems. The European Union's ReFuelEU Aviation mandate requires sustainable aviation fuel blending, starting at 2% in 2025 and increasing to 70% by 2050, driving demand for alcohol-to-jet conversion technologies. Suntory's collaboration with Tokyo Gas achieved 99.5% CO2 recovery purity during distillation processes at its Hakushu Distillery, showcasing the integration of carbon capture in alcohol production. The region's market position is supported by technological innovation, environmental compliance capabilities, and access to premium markets that prioritize sustainability credentials.

Competitive Landscape

The industrial alcohol market is moderately fragmented, with the top dozen producers holding significant but not dominant shares. Green Plains is targeting USD 50 million in annual savings and implementing an 800,000-ton CO₂ capture system in Nebraska, highlighting the growing importance of operational efficiency and carbon management for competitiveness. Cargill's strategy, which includes crop innovation, a renewable BDO joint venture with HELM, and BioForming trials with Virent, demonstrates a shift toward vertical expansion into higher-margin biochemicals beyond bulk ethanol production.

Technological advancements play a critical role in gaining a competitive edge. ExxonMobil's proprietary Methanol-to-Jet technology, RCM Technologies' fermentation yield optimization solutions, and Korean academic innovations in CO₂-to-alcohol conversion are raising the bar for industry competition. Smaller companies are focusing on feedstock proximity and specialty purity niches to differentiate themselves, while financiers increasingly prioritize carbon intensity performance as a key criterion for project funding.

Merger and acquisition activity remains strong as companies seek to enhance their capabilities. For example, Tate & Lyle's planned USD 1.8 billion acquisition of CP Kelco aims to expand into specialty hydrocolloids, aligning with growing demand for natural and clean-label ingredients that complement bio-derived alcohol solvents. Overall, the industrial alcohol market favors companies that effectively integrate technology, feedstock flexibility, and carbon scoring into a cohesive market strategy.

Industrial Alcohol Industry Leaders

-

Archer Daniels Midland Company

-

Cargill Inc.

-

Valero Energy Corporation

-

Green Plains Inc.

-

Tereos S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Insempra introduced its range of bio-based, 100% natural ingredients, including Superior Phenyl Ethyl Alcohol (Superior PEA), a high-purity fragrance ingredient developed through precision fermentation.

- March 2025: KAPSOM established the first industrial-scale E-methanol production facility globally in Denmark. E-methanol is a green methanol variant produced using renewable energy sources such as wind and solar power.

- November 2024: NTPC, India's largest power producer, inaugurated the world's first CO₂-to-methanol conversion plant at its Vindhyachal facility. Methanol is a clear, colorless, flammable liquid with an odor similar to ethanol.

- January 2024: LanzaJet has established the first commercial production facility for ethanol-based sustainable aviation fuel (SAF) in Soperton, Georgia. This facility allows LanzaTech, its subsidiary LanzaJet, Inc., and their partners to refine the manufacturing process and reduce production costs for converting renewable ethanol into aviation fuel.

Global Industrial Alcohol Market Report Scope

| Ethyl Alcohol |

| Methyl Alcohol |

| Isopropyl Alcohol |

| Isobutyl Alcohol |

| Others |

| Corn |

| Sugar and Molases |

| Grains |

| Lignocellulosic Biomass |

| Industrial Gas and Waste Streams |

| Cosmetics and Personal Care |

| Food and Beverages |

| Fuel and Energy |

| Pharmaceuticals |

| Others (Solvents and Chemicals, Laboratory, Adhesives) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Ethyl Alcohol | |

| Methyl Alcohol | ||

| Isopropyl Alcohol | ||

| Isobutyl Alcohol | ||

| Others | ||

| By Source | Corn | |

| Sugar and Molases | ||

| Grains | ||

| Lignocellulosic Biomass | ||

| Industrial Gas and Waste Streams | ||

| By Application | Cosmetics and Personal Care | |

| Food and Beverages | ||

| Fuel and Energy | ||

| Pharmaceuticals | ||

| Others (Solvents and Chemicals, Laboratory, Adhesives) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Industrial alcohol market in 2031?

It is forecast to reach USD 170.09 billion by 2031, rising from USD 132.06 billion in 2026.

Which product type holds the largest share?

Ethyl alcohol dominates with 51.13% of 2025 revenue and is growing at a 5.56% CAGR.

Why are cosmetics driving new demand?

EU preservative rules favor bio-based ingredients, lifting cosmetic-grade ethanol volumes at a 6.81% CAGR through 2031.

Which region is expanding the fastest?

North America is projected to grow at a 5.58% CAGR because of higher E15 adoption and new EPA mandates.

Page last updated on: