Canada IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

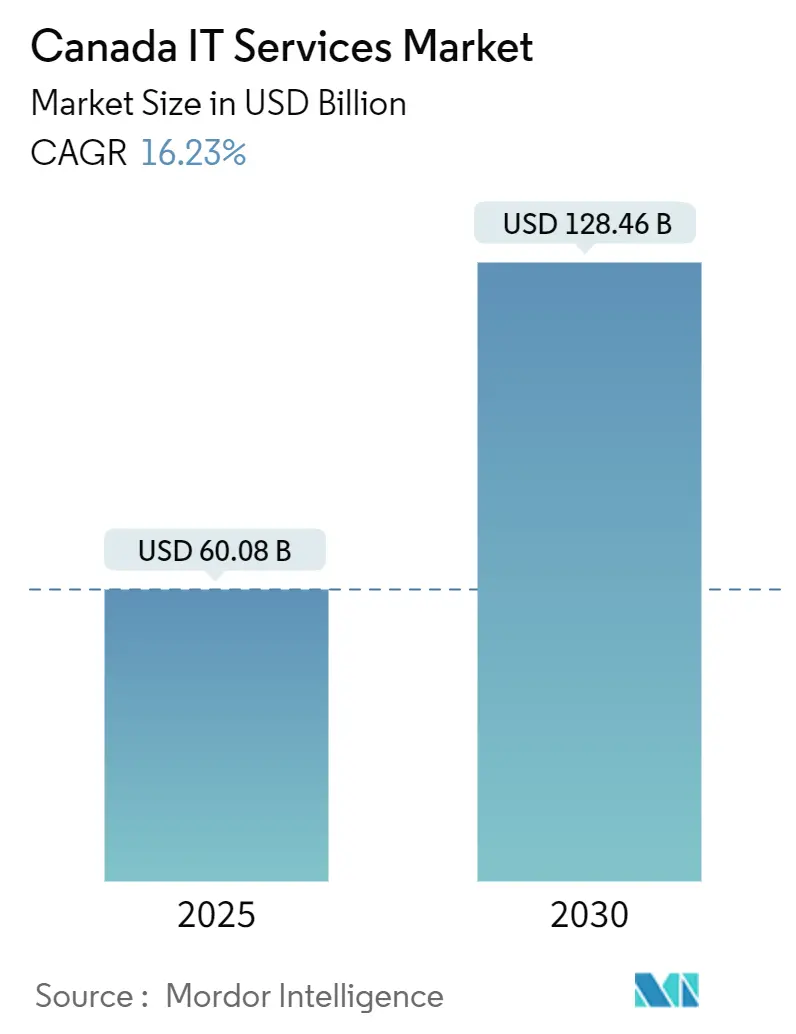

| Market Size (2025) | USD 60.08 Billion |

| Market Size (2030) | USD 128.46 Billion |

| Growth Rate (2025 - 2030) | 16.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada IT Services Market Analysis by Mordor Intelligence

The Canada IT services market size reached USD 60.08 billion in 2025 and is forecast to climb to USD 128.46 billion by 2030, representing a 16.23% CAGR.[1]Shared Services Canada, “Shared Services Canada’s 2025-26 Departmental Plan,” canada.ca Strong federal digital-modernization mandates, rapid enterprise uptake of generative AI, tougher cybersecurity insurance requirements, and new climate-disclosure rules are collectively expanding addressable demand. Cloud-first directives and a USD 2.17 billion federal IT operations budget validate public-sector migrations that influence risk-averse private buyers, while a USD 240 million government investment in sovereign AI compute capacity attracts data-intensive workloads. Meanwhile, cyber-insurance premiums that rose more than 28% year over year are compelling organizations of all sizes to outsource security operations. On the supply side, a 0.9% unemployment rate for senior cloud architects constrains delivery capacity, putting upward pressure on wages and intensifying the war for talent.[2]Government of Canada Job Bank, “Cloud Architect - Information Technology in Canada,” jobbank.gc.ca Altogether, the Canada IT services market is evolving toward outcome-based contracts in which providers assume explicit responsibility for business results rather than traditional time-and-materials engagements.

Key Report Takeaways

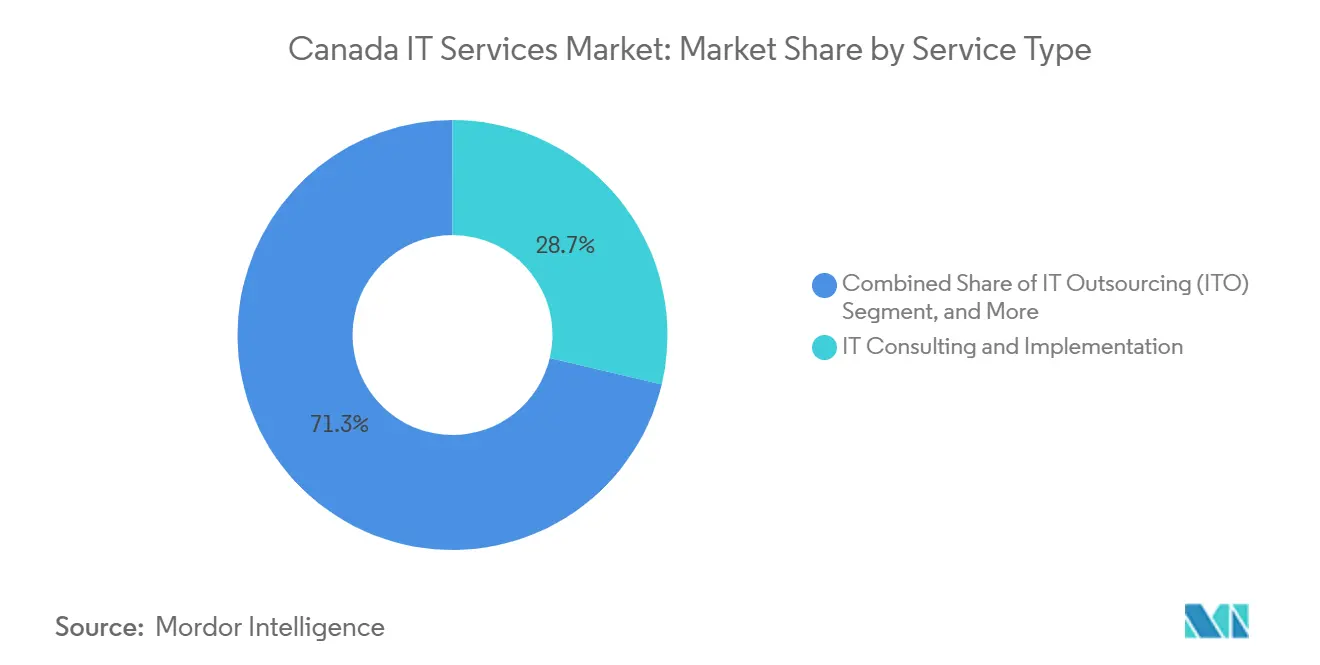

- By service type, IT consulting and implementation led with 27.80% of the Canada IT services market share in 2024, while cloud and platform services are projected to expand at a 19.21% CAGR through 2030.

- By deployment model, on-premises solutions accounted for 55.00% share of the Canada IT services market size in 2024; cloud-hosted services are advancing at a 20.01% CAGR through 2030.

- By service-delivery location, onshore work commanded 48.50% revenue share in 2024, whereas offshore delivery is growing at an 18.83% CAGR despite rising near-shore wages.

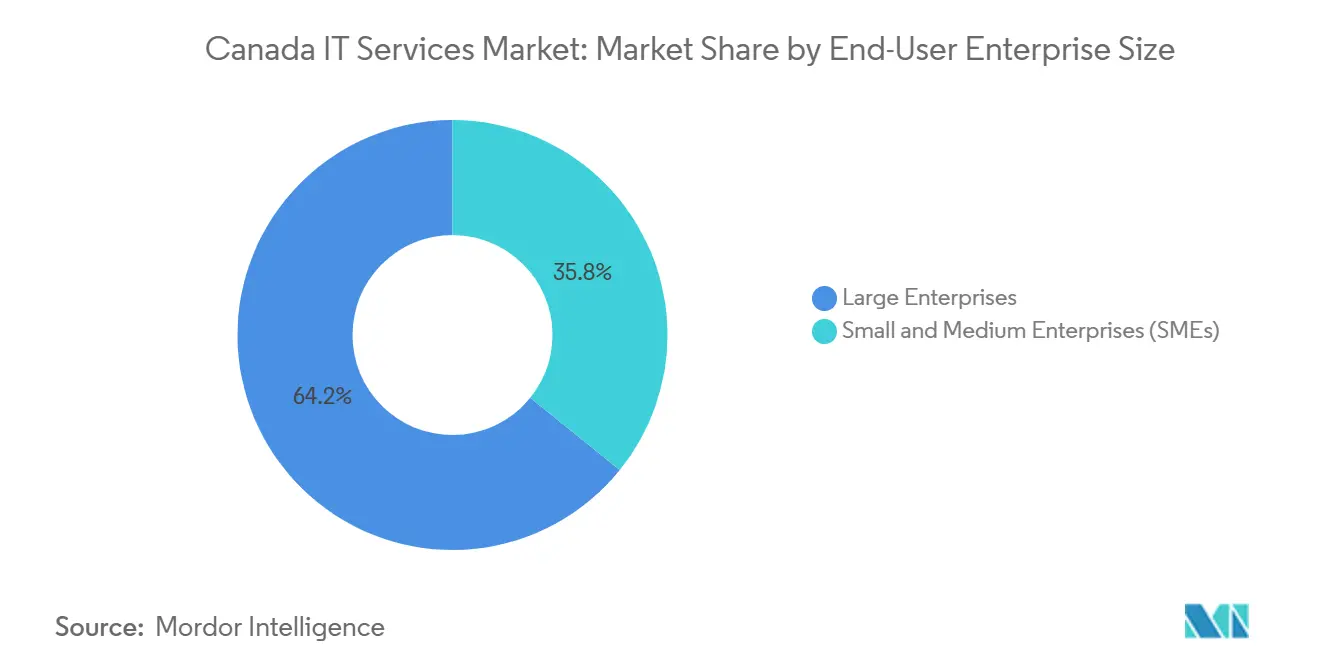

- By enterprise size, large enterprises represented 64.20% of the Canada IT services market size in 2024; small and medium enterprises are forecast to post an 18.40% CAGR to 2030.

Canada IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal "Cloud-First" Policy and Shared Services Canada modernization push | +3.20% | National, concentrated in Ottawa-Gatineau region | Medium term (2-4 years) |

| Surge in Canadian enterprise Gen-AI Proof-of-Concept spending post–2025 | +2.80% | National, with concentration in Toronto-Waterloo corridor | Short term (≤ 2 years) |

| Accelerated migration of Tier-2 banks to open-banking-ready core platforms | +2.10% | National, primarily Toronto and Montreal financial hubs | Medium term (2-4 years) |

| Cyber-insurance premium escalation (>28% YoY) forcing MSSP adoption | +1.90% | National, with higher impact in Alberta and BC | Short term (≤ 2 years) |

| Quebec's Data-Center tax-holiday extension to 2030 | +1.40% | Quebec-specific, spillover to Eastern Canada | Long term (≥ 4 years) |

| Upcoming mandatory Scope-3 audit rules driving ESG IT consulting | +1.10% | National, concentrated in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal cloud-first policy accelerates enterprise adoption

Shared Services Canada plans to retire 720 legacy data centers in favour of four secure facilities, allocate USD 2.17 billion for IT operations, and roll out zero-trust frameworks. Because federal procurement standards heavily influence regulated enterprises, large banks, insurers, and telecom carriers are mirroring this architecture through hybrid cloud roadmaps. Treasury Board guidance that enables Microsoft Copilot across departments further signals institutional readiness for AI-enabled productivity tools.[3]Shared Services Canada, “Shared Services Canada’s 2025-26 Departmental Plan,” canada.ca As reference designs mature, systems integrators focused on risk mitigation gain an advantage by codifying repeatable migration patterns that satisfy data-sovereignty requirements.

Enterprise generative-AI proof-of-concept surge transforms services demand

Scale AI disbursed more than USD 96 million to 22 projects, triggering a wave of production pilots that apply large-language models to customer support, claim processing, and content generation. Sun Life’s employee chatbot recorded a 229% usage jump in eight months, surfacing quantifiable productivity gains that justify larger AI budgets. To capture this momentum, consultancies are packaging industry-specific accelerators for regulated sectors and investing in prompt-engineering talent. Providers able to marry domain knowledge with secure model-ops platforms are winning multi-year managed-service contracts.

Banking sector core-platform modernization boosts integration services

National Bank of Canada’s partnership with CGI positions the institution for open-banking compliance slated for 2025, highlighting the urgency among tier-2 banks to re-platform before regulation takes effect. Royal Bank of Canada’s work with Cohere illustrates how AI is being embedded into core banking functions without violating risk protocols. This push drives demand for cloud-native core systems, payment-rail integrations, and data-lineage solutions that ensure transparency for forthcoming consumer-data portability laws.

Cyber-insurance inflation forces managed security adoption

With a combined ratio of 153% and breach costs averaging USD 6.9 million, Canadian cyber-insurers hiked premiums more than 28% annually, making unmanaged in-house security economically untenable for many firms. Only 5% of businesses carry coverage, creating a protection gap that managed security service providers exploit by bundling threat monitoring, incident response, and cyber-risk quantification. As underwriters begin to mandate minimum security controls for policy issuance, MSSPs that can verify compliance in real time retain a pricing edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight domestic talent pool; 0.9% unemployment for senior cloud architects | -2.30% | National, acute in Toronto and Vancouver | Short term (≤ 2 years) |

| End-user "sovereign-cloud" concerns slowing hyperscaler IaaS off-take | -1.80% | National, particularly government and regulated sectors | Medium term (2-4 years) |

| Rising near-shore wage inflation (10% CAGR) eroding outsourcing cost appeal | -1.40% | National, affecting cost-sensitive SME segment | Medium term (2-4 years) |

| 2026 Quebec Bill C-29 AI-Act compliance burden on vendors | -0.90% | Quebec-specific, with national vendor implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent shortage constrains cloud architecture capabilities

Government labour statistics show persistent vacancies for cloud architects with median wages above USD 53.85 per hour, while Experis reports a +29% net hiring outlook in 2025. TELUS Health projects technology salaries to rise 3.45%, outpacing national averages and squeezing service-provider margins. Firms respond by accelerating internal academies, partnering with polytechnics, and shifting architect-level work to lower-cost offshore centers, yet capability gaps linger, delaying project timelines and diluting revenue realization.

Sovereign-cloud concerns curb hyperscaler velocity

The Digital Governance Standards Institute’s geo-residency framework and high-profile U.S.-Canada data-privacy debates elevate scrutiny of hyperscaler jurisdictional exposure. Domestic alternatives such as ThinkOn gain traction by offering fully Canadian data sovereignty, prompting some agencies to defer hyperscaler migrations in favour of interim private-cloud deployments. Compliance audits and legal reviews prolong sales cycles, dampening near-term growth for global cloud providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: AI integration reshapes consulting demand

IT consulting and implementation retained 27.80% of the 2024 Canada IT services market share, anchored by modernization programs that embed generative AI into legacy workflows. Cloud and platform services posted the fastest 19.21% CAGR outlook as federal cloud adoption normalizes hybrid architectures and opens compliance-tested migration patterns. Business process outsourcing grew steadily as clients sought cost stability during wage inflation, while managed security services accelerated on the back of cyber-insurance mandates. IT outsourcing faced margin pressure yet continued to supply niche legacy-system expertise.

Providers are pivoting from staff-augmentation deals toward outcome-linked contracts that bundle advisory, integration, and ongoing optimization. For example, CGI’s Databricks Select designation reflects a strategic push to scale AI-centric data-platform projects at premium bill rates. Simultaneously, ESG consulting emerges as a sub-segment after the Canadian Sustainability Standards Board’s Scope 3 rules, driving specialized data-chain integrations. Early movers bundling AI accelerators with carbon-accounting toolkits are capturing cross-sell opportunities across verticals.

By Deployment Model: Hybrid architectures drive cloud growth

On-premises environments still represented 55.00% of the Canada IT services market size in 2024 because of entrenched legacy applications and strict data-residency demands. However, cloud-hosted workloads are expected to expand at a 20.01% CAGR through 2030 as Shared Services Canada’s IaaS prequalification of AWS, Google, Microsoft, and Oracle reassures compliance officers. Organizations are adopting layered architectures that keep high-risk data in provincial data centers while leveraging hyperscaler elasticity for analytics. Bell Cloud Connect facilitates this model by offering dedicated, low-latency paths from customer sites to multiple clouds.

Hybrid adoption is further catalysed by accelerators such as zero-trust blueprints and sovereign-cloud landing zones delivered as code. System integrators monetize reference patterns through managed-platform offerings that shorten deployment timelines and embed recurring revenue. Concerns over vendor lock-in are addressed via multi-cloud orchestration platforms that abstract service-specific dependencies, positioning providers as impartial operators rather than single-vendor resellers.

By Service-Delivery Location: Offshore growth despite wage pressures

On-shore services remained preferable for strategy and regulatory work, maintaining 48.50% market share in 2024. Nevertheless, offshore throughput is projected to rise at an 18.83% CAGR as providers rebalance labour pyramids in favour of lower-cost geographies to counter domestic salary inflation. Firms differentiate through follow-the-sun security operations centers and 24-hour DevSecOps pipelines rather than pure price competition.

Canadian buyers are increasingly sophisticated about global delivery risk, emphasizing contractual clauses on data handling, local privacy law adherence, and rapid remediation capabilities. As a result, providers with ISO 27001-certified facilities and Canadian data-residency gateways win preference. Near-shore teams still play a role for bilingual support and agile collaboration but are now justified on value terms rather than headline rate savings.

By Enterprise Size: AI democratization empowers SMEs

Large enterprises captured 64.20% revenue in 2024 because their complex estates demand broad service portfolios. Small and medium enterprises, however, are set to drive incremental growth at an 18.40% CAGR as no-code AI services and subscription-based security bundles reduce entry costs. Scale AI cost-sharing grants that reimburse up to 40% of project expenses materially lower adoption barriers for mid-market manufacturers and logistics firms.

Providers are packaging modular offerings-such as fixed-scope data catalogues, pre-tuned chatbots, and turnkey security monitoring-in price points aligned to SME budgets. Furthermore, the National Research Council’s AI Assist Program provides aid up to USD 66,600, expanding the investable pool of proof-of-concept projects. As SMEs graduate from pilots to production, managed-services agreements shift from per-user pricing to consumption-based models that scale with customer growth, locking in predictable revenue for vendors.

By End-User Vertical: Healthcare leads digital transformation

Banking, financial services, and insurance maintained 24.70% share of the Canada IT services market size in 2024, propelled by open-banking readiness and payment-rail modernization. Healthcare and life sciences is projected to expand at a 19.99% CAGR through 2030 as electronic health-record mandates, tele-diagnostic platforms, and precision-medicine analytics require deep regulatory knowledge.

Manufacturing pursues Industry 4.0 retrofits, while public-sector agencies embrace digital identity and citizen-services portals fuelled by federal funding. Retail and consumer goods demand centers on omnichannel orchestration and inventory intelligence, whereas telecom providers accelerate 5G-edge platform deployments. Energy and utilities customers emphasize asset-integrity analytics and grid digitization to meet decarbonization targets. Each vertical’s regulatory overlay nudges clients toward providers with domain-specific compliance accelerators and local data-residency assurances.

Geography Analysis

Ontario anchors demand, with the Toronto-Waterloo innovation corridor hosting financial-services headquarters and more than 3,500 tech startups, translating into the single largest provincial share of the Canada IT services market. Federal spending clustered in Ottawa-Gatineau injects predictable workloads for cloud transformation and secure network engineering. Quebec follows, buoyed by data-center tax incentives and a thriving AI ecosystem centered in Montreal that benefits from provincial funding and academic-industry partnerships such as TELUS-Mila.

Western Canada demonstrates above-average growth driven by energy-sector digitization in Calgary and resource-supply-chain modernization in Vancouver. British Columbia’s forecast 3.60% salary growth underscores a tight labour market that favours providers with established recruiting pipelines. The Prairies leverage agriculture-tech initiatives and rural broadband expansion to adopt cloud-based monitoring solutions, while Atlantic provinces capitalize on lower operating costs and targeted immigration programs to attract near-shore delivery centers.

Regional policy heterogeneity shapes service-mix variation. Quebec’s Law 25 privacy regulation raises demand for compliance audits and data-residency solutions, giving homegrown providers a competitive edge. Ontario’s upcoming Digital Platform Workers Rights Act influences HR-tech outsourcing requirements, whereas Alberta’s Emissions Management and Climate Resilience strategy spurs ESG data-platform demand. Consequently, providers must tailor go-to-market messages, delivery models, and regulatory toolkits to province-specific nuances to capture full opportunity potential.

Competitive Landscape

Large vendors such as CGI, IBM Canada, and Accenture combine global delivery reach with localized compliance expertise, enabling them to secure multi-year transformation contracts across federal departments, tier-1 banks, and telecom operators. Mid-tier specialists-including MNP, Softchoice, and Long View Systems-capitalize on niche expertise in Microsoft ecosystems, AI prompt engineering, and sovereign-cloud orchestration to win mid-market and public-sector deals.

Mergers and acquisitions remain a principal route to capability expansion. CGI’s acquisition of Momentum Technologies adds 250 Quebec-based analytics experts, while Bell Canada’s partnership with ServiceNow embeds IT-workflow automation into managed network offerings.[4]ServiceNow, “ServiceNow and Bell Canada Expand Partnership,” servicenow.com Accenture completed 39 buyouts in 2024, including the Canadian operations of True North Solutions to deepen energy vertical coverage. These moves intensify competition by compressing service-differentiation windows and driving pricing convergence around standardized offerings.

Sovereign-cloud compliance and AI-act readiness present new battlegrounds where domestic players can outmanoeuvre global rivals constrained by data-jurisdiction complexities. Providers controlling Canadian data centers, such as ThinkOn and OVHcloud, partner with systems integrators to deliver end-to-end stacks that meet provincial residency statutes. Meanwhile, hyperscalers expand regional zones and sign clean-energy purchase agreements to counter environmental-impact narratives, positioning themselves as sustainable options. Successful competitors will blend hyperscaler innovation, sovereign-residency guarantees, and vertical accelerators to create defensible value propositions.

Canada IT Services Industry Leaders

CGI Inc.

IBM Canada Ltd.

Accenture Inc. (Canada)

Deloitte Inc.

Tata Consultancy Services Canada Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Bell Canada and Cohere unveiled an alliance to co-sell AI tools to Canadian governments and businesses, leveraging Bell’s AI data centers and fiber network.

- March 2025: CGI finalized the acquisition of Momentum Technologies, adding 250 data-analytics professionals in Quebec City.

- March 2025: The Government of Canada closed a USD 240 million investment in Cohere to expand domestic AI compute capacity.

- February 2025: CGI attained Databricks Select partner status with more than 100 certified consultants.

Canada IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| On-Premise |

| Cloud-Hosted (Public/Private) |

| On-shore |

| Near-shore |

| Off-shore |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By Deployment Model | On-Premise |

| Cloud-Hosted (Public/Private) | |

| By Service-Delivery Location | On-shore |

| Near-shore | |

| Off-shore | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals |

Key Questions Answered in the Report

What is the current value of the Canada IT services market?

The market was valued at USD 60.08 billion in 2025 and is forecast to reach USD 128.46 billion by 2030.

How fast is spending on cloud-hosted services growing?

Cloud-hosted workloads are projected to expand at a 20.01% CAGR between 2025 and 2030.

Which vertical is expected to grow fastest through 2030?

Healthcare and life sciences is forecast to post a 19.99% CAGR as digital-health mandates and data-analytics initiatives accelerate.

What share do large enterprises hold in overall demand?

Large enterprises accounted for 64.20% of 2024 spending, driven by complex transformation agendas and compliance requirements.

Why are managed security services gaining traction?

Cyber-insurance premiums rose more than 28% year over year, making outsourced security operations more cost-effective than in-house alternatives.

How does Canadas data-sovereignty focus affect hyperscaler adoption?

Strict residency standards prolong procurement cycles and spur interest in sovereign-cloud alternatives that guarantee Canadian data location.

Page last updated on: