Saudi Arabia IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

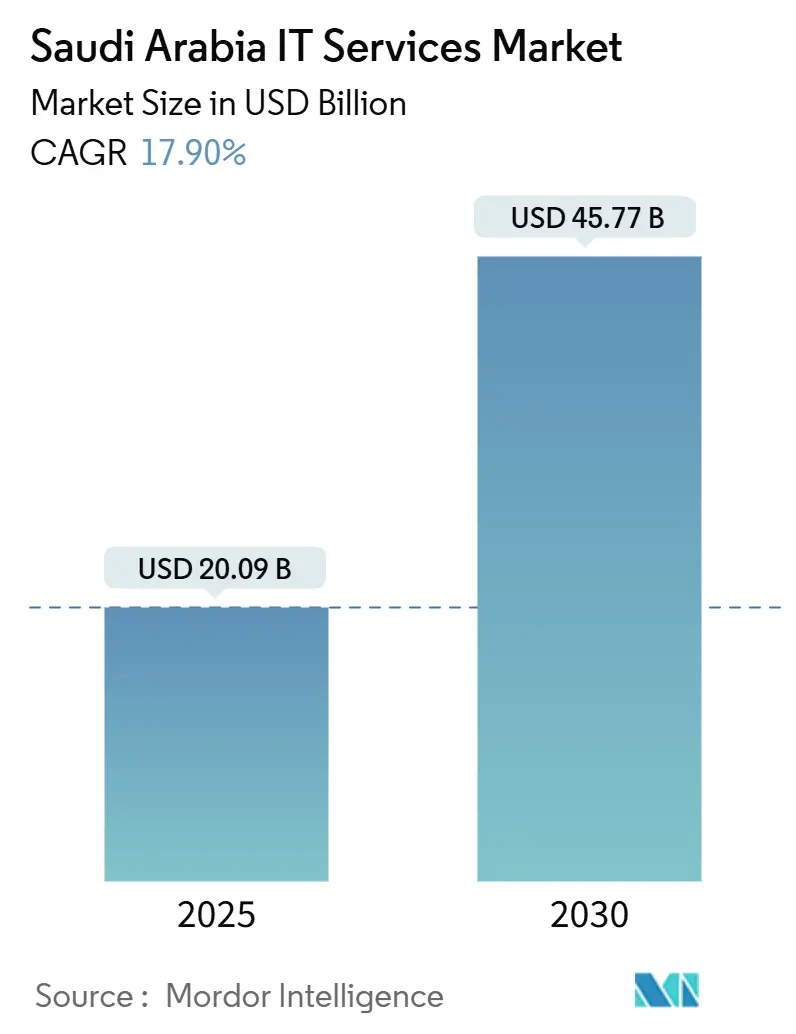

| Market Size (2025) | USD 20.09 Billion |

| Market Size (2030) | USD 45.77 Billion |

| Growth Rate (2025 - 2030) | 17.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia IT Services Market Analysis by Mordor Intelligence

The Saudi Arabia IT services market size stands at USD 20.09 billion in 2025 and is projected to reach USD 45.77 billion by 2030, reflecting a 17.9% CAGR. The expansion is propelled by Vision 2030 mandates that prioritize digitization of public services, sustained hyperscale data-center investments, and sovereign AI programs that demand Arabic language processing and local data residency. Government entities have shifted to outcome-based contracts that encourage large, multi-year consulting engagements, while enterprises accelerate hybrid-cloud adoption following the operational launch of AWS’s Saudi region. Managed security services gain momentum as cyber threats rise and the Essential Cybersecurity Controls framework becomes mandatory. Growing compliance costs linked to the Personal Data Protection Law fuel demand for specialized services but compress provider margins. International integrators, regional champions, and niche specialists compete vigorously, with consolidation intensifying after high-profile acquisitions such as SAMI’s takeover of Advanced Electronics Company. [1]Saudi Data & AI Authority, “HUMAIN Program Launch,” SDAIA.GOV.SA

Key Report Takeaways

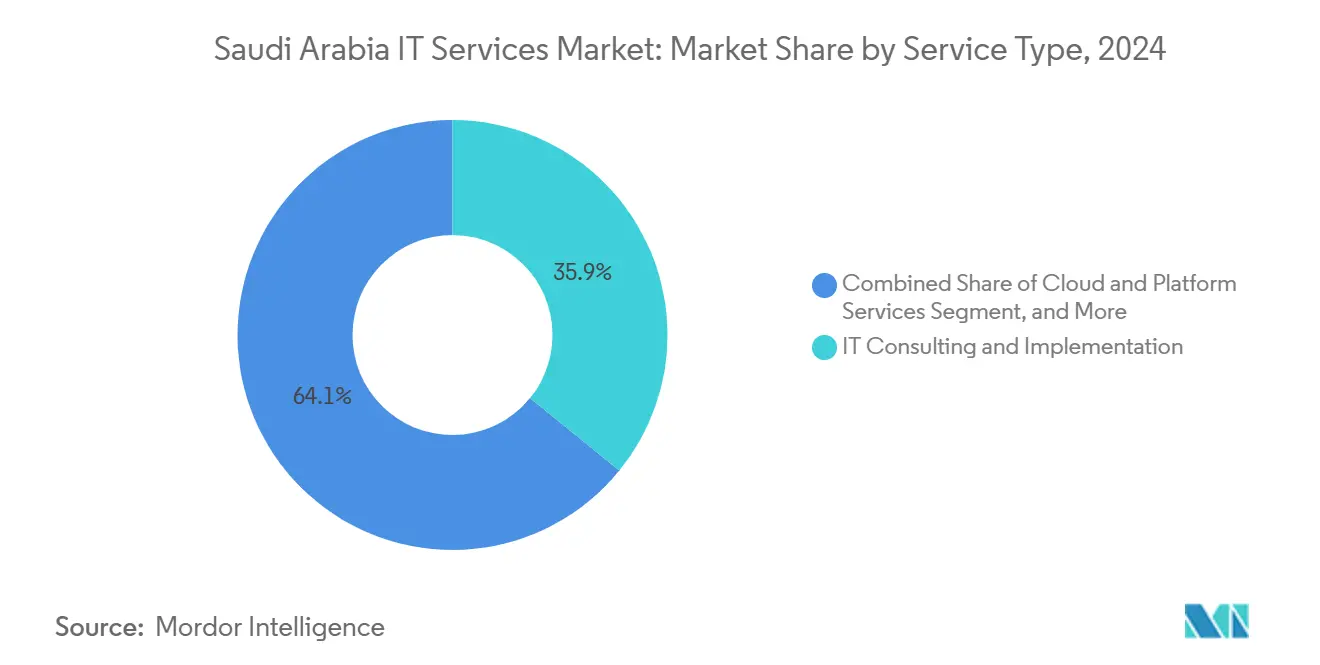

- By service type, IT Consulting and Implementation led with 35.86% revenue share of the Saudi Arabia IT services market in 2024, whereas Cloud and Platform Services are advancing at a 19.5% CAGR through 2030.

- By end-user enterprise size, Large Enterprises accounted for 68.41% of the Saudi Arabia IT services market share in 2024, while SMEs are forecast to expand at a 19% CAGR to 2030.

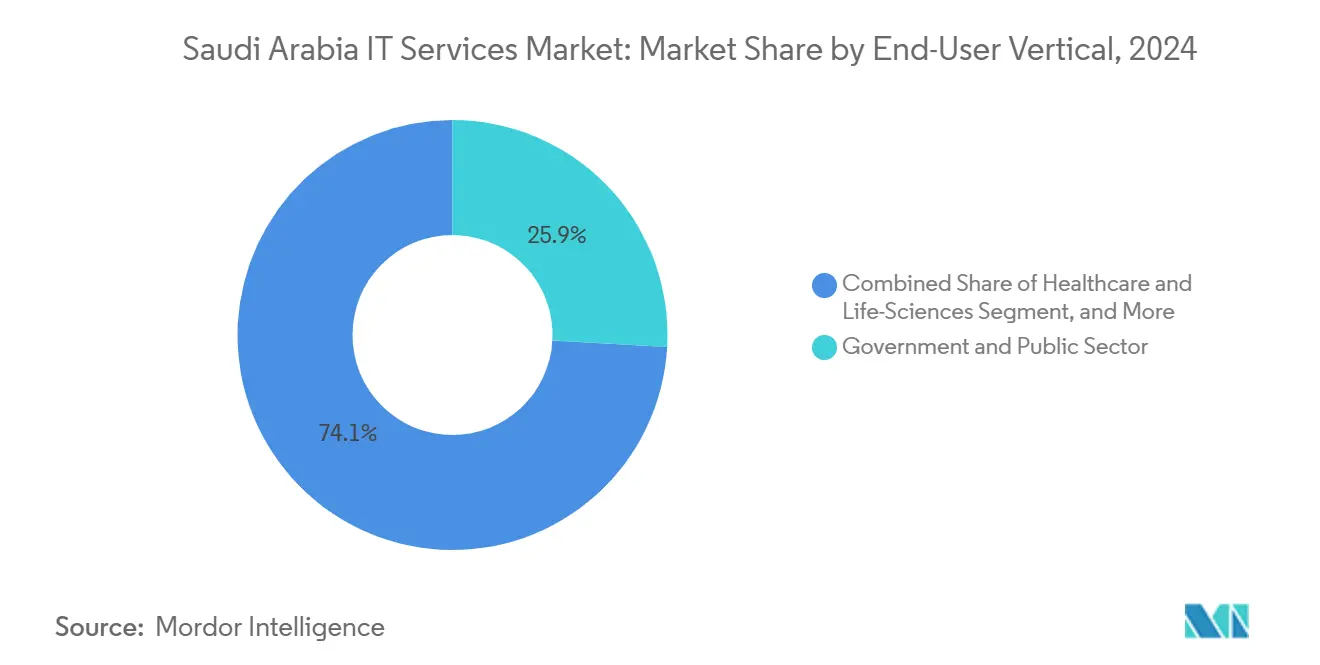

- By end-user vertical, the Government and Public Sector captured a 25.88% share of the Saudi Arabia IT services market size in 2024, and Healthcare and Life Sciences are expanding at a 19.3% CAGR through 2030.

- By deployment model, Onshore Delivery held 48.77% share of the Saudi Arabia IT services market size in 2024, whereas Offshore Delivery records the highest projected CAGR at 19.2% to 2030.

Saudi Arabia IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030-driven public-sector digital spending boom | +4.2% | National, concentrated in Riyadh and Eastern Province | Long term (≥ 4 years) |

| Accelerating enterprise cloud-migration wave | +3.8% | National, with early adoption in BFSI and manufacturing | Medium term (2-4 years) |

| Escalating cyber-threat landscape boosts managed security uptake | +2.9% | National, critical infrastructure focus | Short term (≤ 2 years) |

| Rapid build-out of hyperscale and colocation data-centre capacity | +3.1% | Regional, NEOM and Eastern Province leadership | Long term (≥ 4 years) |

| Sovereign-AI (HUMAIN) programs spur Arabic LLM services demand | +2.6% | National, government and education sectors priority | Medium term (2-4 years) |

| Mandatory e-invoicing (FATOORA) compliance fuels SME IT/BPO spend | +1.4% | National, SME sector concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030-driven Public-Sector Digital Spending Boom

The Ministry of Communications and Information Technology allocated SAR 15 billion (USD 4 billion) for IT modernization in 2024, a 340% rise over pre-Vision 2030 baselines. [2]Ministry of Communications and Information Technology, “Digital Government Strategy 2024,” MCIT.GOV.SA Outcome-based contracting now dominates, raising average deal sizes and drawing tier-1 global integrators that partner with local firms to meet Saudization rules. Agencies favor vendors with Arabic AI and sovereign-cloud capabilities, shifting competition away from price toward compliance differentiators. Semi-government entities add USD 2.3 billion in annual spend, cushioning market growth during economic swings. Procurement urgency created by Vision 2030 bypasses previous bureaucratic delays and sustains a multi-year pipeline.

Accelerating Enterprise Cloud-Migration Wave

Cloud adoption among Saudi enterprises reached 78% in 2024, up from 45% in 2022, after regulations permitted specific government workloads in locally operated facilities. AWS’s USD 5.3 billion regional launch resolved latency and compliance concerns, while sovereign clouds from STC and Mobily expanded mid-market access. BFSI leads with 89% penetration, followed by manufacturing at 72%. Edge-computing demand linked to NEOM’s smart-city projects stimulates hybrid architectures that blend public cloud scale with local processing, boosting specialized integration revenues.

Escalating Cyber-Threat Landscape Boosts Managed Security Uptake

Sophisticated attacks on critical infrastructure jumped 67% in 2024, with an average breach cost of USD 4.88 million. Managed security uptake rose to 43% among large enterprises as talent shortages made in-house defense untenable. New Essential Cybersecurity Controls give providers a standardized blueprint, pushing contract values up 34%. Global firms opened Security Operations Centers in Riyadh and Dammam, while Elm expanded its cybersecurity workforce by 89% in 2024 to capture demand.

Rapid Build-Out of Hyperscale and Colocation Data-Center Capacity

Data-center investment surged USD 21 billion in 2024, led by DataVolt’s USD 20 billion partnership with Supermicro that will create multiple hyperscale AI campuses. NEOM’s USD 5 billion allocation is the Kingdom’s largest single commitment and will serve one million residents by 2030. Capacity spreads across Riyadh, Jeddah, Dammam, and NEOM, lowering latency and fostering redundancy. International colocation operators consider entry while local providers grow capacity 127%, spurring demand for facility management, network optimization, and disaster-recovery services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortfall of advanced IT and cybersecurity talent | -2.8% | National, acute in Riyadh and Eastern Province | Long term (≥ 4 years) |

| Complex data-residency and compliance cost burdens | -1.9% | National, multinational corporations most affected | Medium term (2-4 years) |

| Margin erosion from fierce price competition | -1.6% | National, commodity services segments | Short term (≤ 2 years) |

| Lengthy government procurement and payment cycles | -1.2% | National, government sector focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortfall of Advanced IT and Cybersecurity Talent

The market lacks over 15,000 skilled professionals, even after NITA programs trained 50,000 individuals in 2024. [3]National Information Technology Academy, “Annual Training Report 2024,” NITA.GOV.SA Salary premiums exceed regional norms by 45-60% and lengthen project timelines. Skills gaps are most acute where Arabic AI and compliance intersect. International firms build academies with local universities, but expert development cycles of 18-24 months lag immediate demand. Premium Residency visas attract limited IT talent, as many recipients favor oil and gas.

Complex Data-Residency and Compliance Cost Burdens

Full enforcement of the Personal Data Protection Law in September 2024 raised compliance costs to 3-5% of Saudi IT budgets, with localization adding 2-3% for infrastructure duplication. SDAIA risk-assessment guidelines issued in February 2025 require detailed flow-by-flow evaluations, demanding specialized legal and technical expertise. Providers must price in audit overhead and potential SAR 5 million penalties, squeezing margins and extending sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consulting Dominance Amid Cloud Acceleration

IT Consulting and Implementation holds 35.86% of the Saudi Arabia IT services market share in 2024, reflecting sustained demand for strategic guidance on large Vision 2030 projects. The average engagement value reached USD 2.3 million, nearly triple regional norms. Cloud and Platform Services, powered by local hyperscale launches, register the fastest 19.5% CAGR.

Managed Security Services outpace other subsegments as organizations comply with Essential Cybersecurity Controls, lifting average contract values 34% in 2024. Integration across consulting, cloud, and security now features in 67% of large deals, demonstrating buyer preference for comprehensive partnerships that support sovereign-cloud, Arabic AI, and zero-trust postures.

By End-User Enterprise Size: Large Enterprise Stability Versus SME Dynamism

Large Enterprises contribute 68.41% to the Saudi Arabia IT services market size, often signing multi-domain contracts worth USD 15-25 million per year. They leverage outcome-based clauses that shift performance risk to vendors.

SMEs, stimulated by FATOORA, post a 19% CAGR. Average engagement values climbed to USD 78,000 in 2024 as compliance drove holistic demand. Government incentives for cloud credits and cybersecurity training lower adoption barriers, enabling providers to deliver standardized offerings that fit SME budgets.

By End-User Vertical: Government Leadership Drives Healthcare Innovation

Government and Public Sector commands 25.88% of the Saudi Arabia IT services market size, anchored by multi-year contracts worth USD 50-100 million for citizen platforms and agency integration.

Healthcare and Life Sciences grow at 19.3% CAGR under the Ministry of Health’s digital agenda. Requirements for electronic health records, telemedicine, and AI diagnostics create high-value projects. BFSI maintains strong cybersecurity demand after the pending Google Pay launch. Manufacturing, Energy, Retail, and Logistics each add steady pipelines linked to industrial digitization and e-commerce growth.

By Deployment Model: Onshore Preference Amid Offshore Growth

Onshore Delivery held a 48.77% share in 2024 as clients sought local presence, Arabic capability, and compliance assurance. Onshore teams command premium pricing but satisfy Saudization quotas.

Offshore Delivery posts a 19.2% CAGR as cost pressures persist and remote collaboration matures. Providers split project phases across locations, achieving follow-the-sun efficiency while respecting SDAIA safeguards for sensitive workloads. Nearshore hubs in the UAE and Egypt offer balanced cost and cultural alignment.

Geography Analysis

Saudi Arabia accounted for roughly 45% of the GCC IT services market in 2025, dwarfing its UAE and Qatar counterparts. Riyadh and Eastern Province represent 65% of national spending due to government headquarters and oil-and-gas majors.

NEOM’s USD 5 billion data-center program will redistribute demand toward the northwest by 2028. The Western Province shows robust retail and logistics projects tied to Jeddah’s commercial hub, while southern regions grow on tourism and cross-border trade digitalization.

Data-residency laws foster Saudi-based delivery centers that also serve GCC clients with similar sovereignty concerns. Dedicated clusters in Dammam focus on industrial IoT, whereas Jeddah emphasizes trade-tech. This distributed strategy nurtures specialized expertise while easing pressure on Riyadh talent pools.

Competitive Landscape

The market is moderately fragmented but trending toward consolidation. Global integrators such as IBM, Accenture, and TCS scale local operations through workforce programs and strategic alliances. Regional champions STC Solutions and Elm leverage regulatory insight and Arabic AI investments.

SAMI’s USD 500 million acquisition of Advanced Electronics Company in 2024 created a formidable defense technology competitor. [4]SAMI Advanced Electronics, “SAMI Acquires Advanced Electronics Company,” AECL.COM Outcome-based contracts gain popularity, rewarding firms with the financial capacity to absorb delivery risk. Providers differentiate through sovereign-compliant clouds, localized AI, and automated compliance toolkits.

Patent filings for Arabic language AI rose 127% in 2024, evidencing heavy R&D investment. International and local providers alike vie to secure intellectual property that can anchor future smart-city and public-sector tenders.

Saudi Arabia IT Services Industry Leaders

solutions by stc Company

Devoteam Arabia Company Limited

MDS for Computer Systems Co. Ltd. (MDS SI Saudi Arabia)

Ejada Systems Ltd.

Elm Company (Al Elm Information Security Co.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The 19th wave of FATOORA e-invoicing implementation impacted over 400,000 SMEs, triggering USD 800 million in new IT demand.

- June 2025: Wipro Arabia Limited opened a Riyadh HQ, tripling local staff for AI and cybersecurity projects.

- May 2025: SDAIA launched the HUMAIN sovereign AI program with USD 1 billion funding for Arabic LLMs.

- May 2025: Supermicro partnered with DataVolt to invest USD 20 billion in hyperscale AI campuses.

- April 2025: SAMI finalized its USD 500 million acquisition of Advanced Electronics Company.

- March 2025: SDAIA issued updated cross-border data transfer risk-assessment guidelines.

- February 2025: HP announced a manufacturing site in Riyadh and an AI research center in Dhahran.

- February 2025: ServiceNow revealed plans for Saudi data centers by 2026 with local partners.

- January 2025: Elm acquired Thiqah, strengthening its digital identity portfolio.

Saudi Arabia IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery |

Key Questions Answered in the Report

How large is the Saudi Arabia IT services market in 2025?

The Saudi Arabia IT services market size is USD 20.09 billion in 2025.

What is the expected growth rate through 2030?

The market is forecast to expand at a 17.9% CAGR, reaching USD 45.77 billion by 2030.

Which service segment is growing fastest?

Cloud and Platform Services lead with a 19.5% CAGR through 2030.

Why are SMEs investing heavily in IT services?

Mandatory FATOORA e-invoicing rules push SMEs to digitize finance and compliance processes, driving 19% CAGR in SME demand.

What regulatory factors influence provider selection?

Personal Data Protection Law requirements for data residency and Essential Cybersecurity Controls shape vendor choices toward firms with sovereign-cloud and Arabic AI capabilities.

Which regions inside Saudi Arabia show the strongest demand?

Riyadh and Eastern Province account for 65% of spending, while NEOM is emerging as a new growth center due to USD 5 billion data-center investments.

Page last updated on: