Canada ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

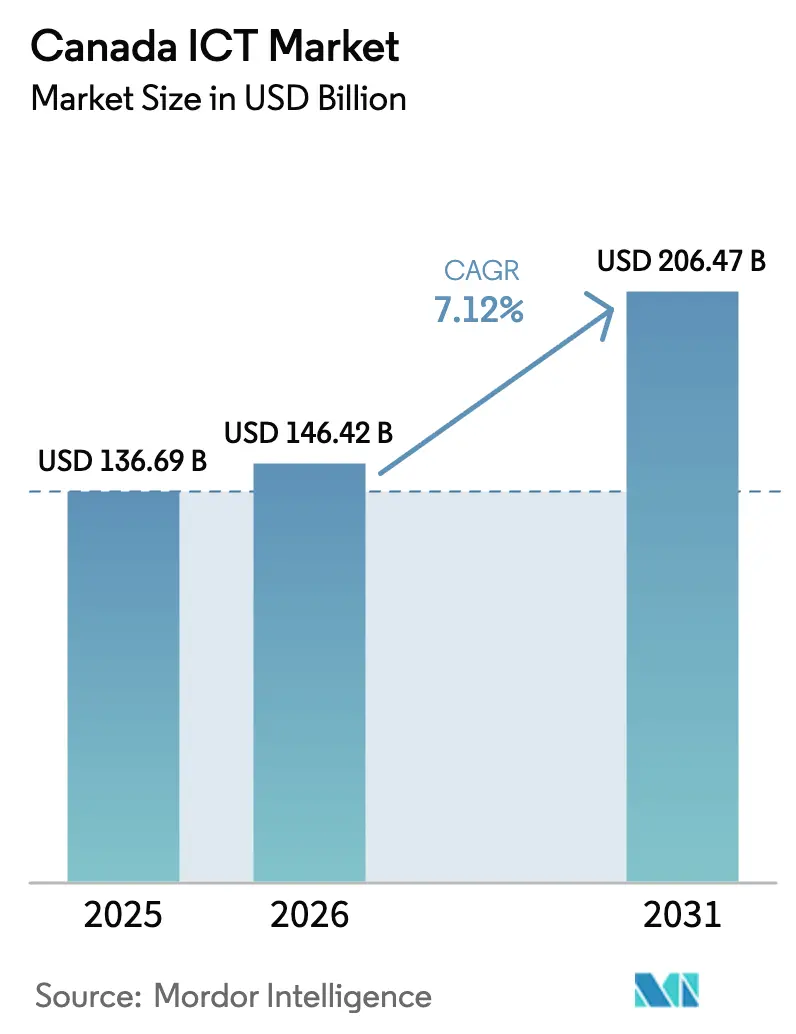

| Base Year Market Size (2025) | USD 136.69 Billion |

| Market Size (2026) | USD 146.42 Billion |

| Market Size (2031) | USD 206.47 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

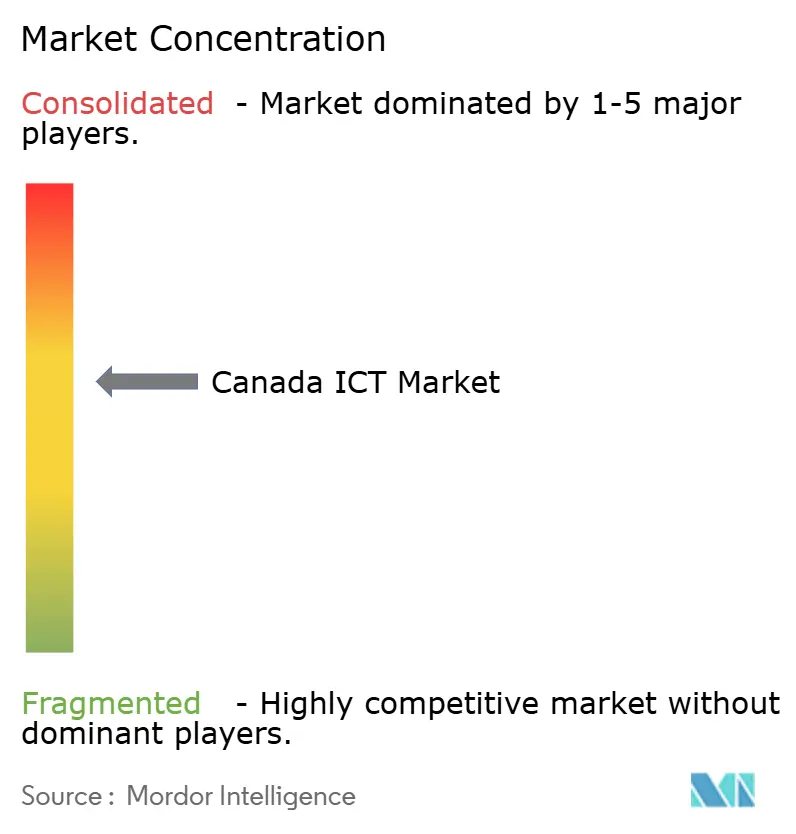

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada ICT Market Analysis by Mordor Intelligence

The Canada ICT market size is expected to grow from USD 136.69 billion in 2025 to USD 146.42 billion in 2026 and is forecast to reach USD 206.47 billion by 2031 at 7.12% CAGR over 2026-2031. This solid trajectory rests on sustained federal funding for artificial intelligence, rapid enterprise digitization, hyperscaler data-center build-outs and a nationwide broadband upgrade program that is closing historic connectivity gaps. Growing provincial incentives, clean-energy availability and data-sovereignty rules continue to attract global cloud providers, while subscription-based software and managed services help firms shift capital spending to operating budgets. Escalating cybersecurity threats, especially in finance and healthcare, underpin double-digit spending on protective solutions even as telecom pricing pressures spur demand for more cost-efficient voice and data alternatives. Skills shortages remain a headwind, yet they are simultaneously catalyzing investment in automation, low-code platforms and targeted reskilling partnerships that improve long-run productivity across the Canada ICT market.

Key Report Takeaways

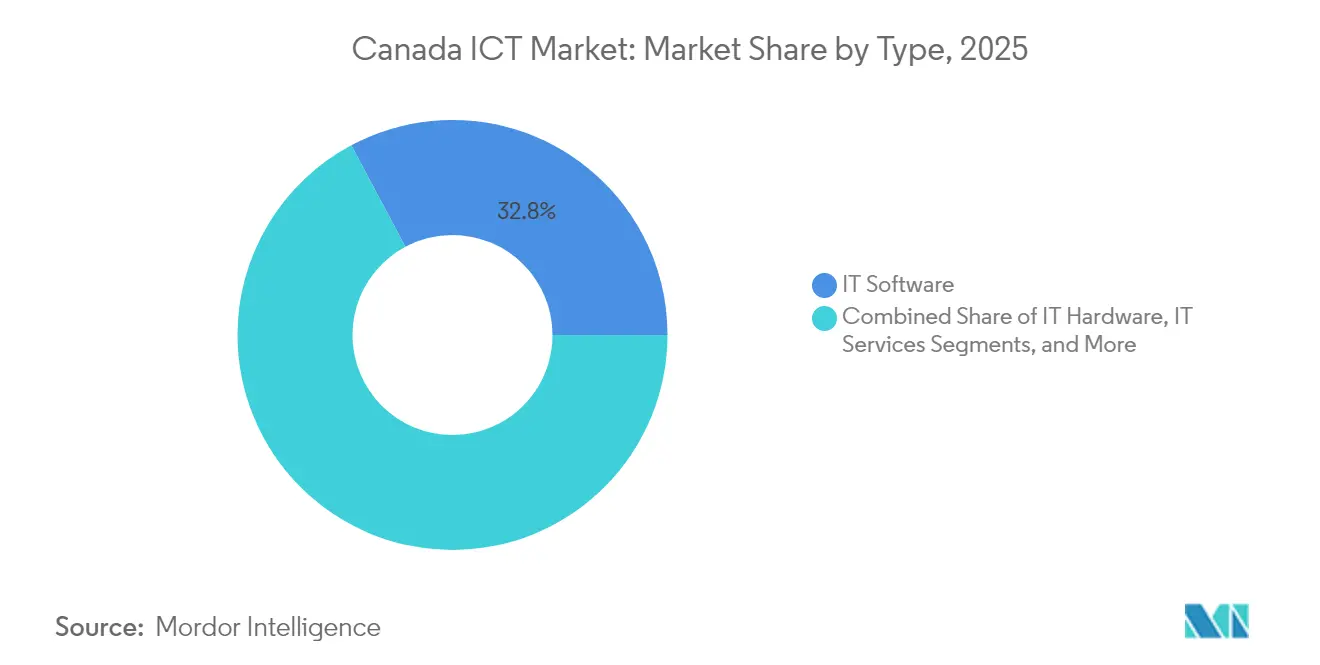

- By type, IT Software led with a 32.80% revenue share in 2025, while IT Security/Cybersecurity is on track for the fastest 10.85% CAGR through 2031.

- By end-user enterprise size, Large Enterprises held 59.90% of the Canada ICT market share in 2025; Small and Medium Enterprises are set to post a 10.14% CAGR to 2031.

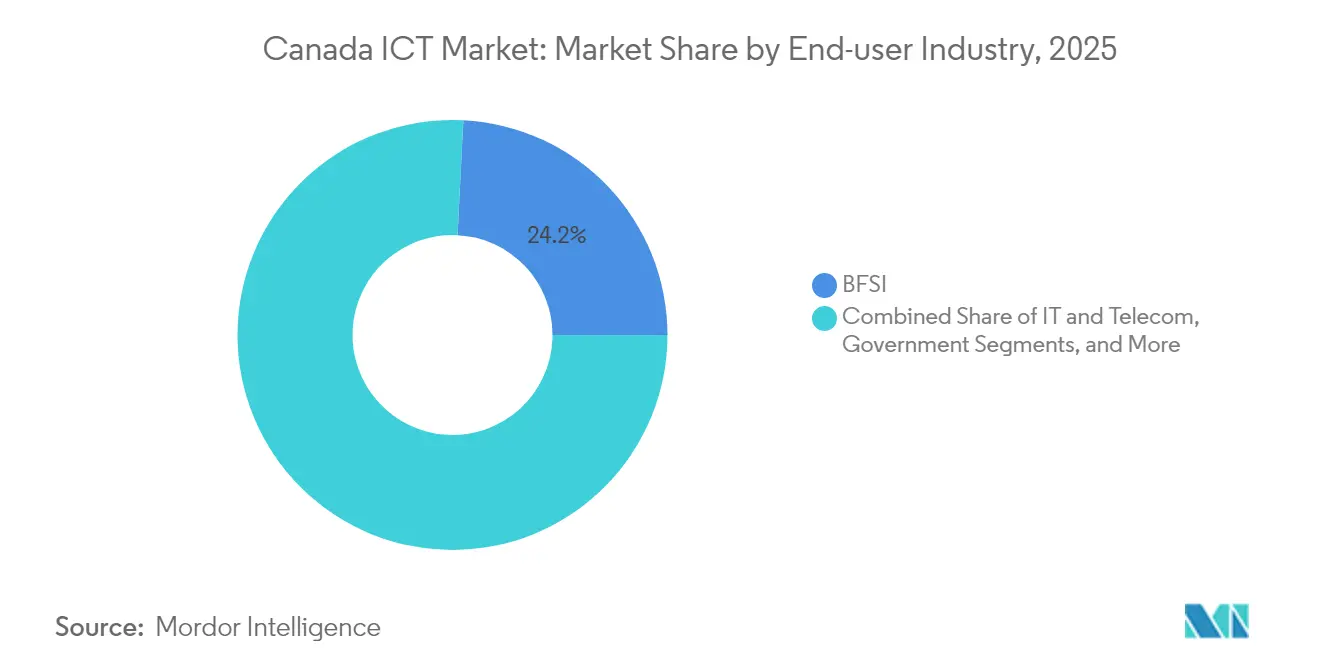

- By end-user industry, BFSI accounted for 24.20% of the Canada ICT market size in 2025, whereas Healthcare is projected to advance at a 11.55% CAGR through 2031.

- By deployment mode, Cloud deployments captured 56.10% of 2025 revenue and are expanding at a 10.42% CAGR, outpacing on-premise solutions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI-focused federal investment boom | +1.8% | National, concentrated in Toronto, Montréal, Vancouver | Medium term (2-4 years) |

| Universal Broadband Fund accelerating rural connectivity | +1.2% | Rural Canada, northern territories, Atlantic provinces | Long term (≥4 years) |

| Rapid cloud-first migration among SMEs | +2.1% | National, higher in urban centers | Short term (≤2 years) |

| Data-center expansions by hyperscalers in Ontario and Québec | +1.5% | Ontario and Quebec core, spillover to adjacent provinces | Medium term (2-4 years) |

| Electrification and carbon pricing pushing smart-grid IT spend | +0.9% | National, early gains in Alberta, Ontario, British Columbia | Long term (≥4 years) |

| Province-level digital-ID programs triggering cybersecurity upgrades | +1.1% | Alberta and Québec leading implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative AI federal investment boom drives market transformation

A USD 2.4 billion federal package has positioned Canada among the world’s three strongest AI ecosystems; yet only 26% of domestic enterprises have adopted AI tools versus 34% worldwide, leaving ample runway for diffusion [1]Innovation, Science and Economic Development Canada, “Budget 2025: AI Investments,” ic.gc.ca. Microsoft’s planned USD 80 billion AI-enabled region is estimated to generate USD 187 billion in economic output by 2030, cementing hyperscale capacity in Toronto. Complementing the federal push, Québec earmarked USD 11 million for 15 sector-focused AI projects and launched innovation zones such as DistriQ for quantum technologies that connect academia, startups and incumbents. Vendors like Vooban aim for 30-40% productivity uplifts through tailored implementations, illustrating how AI budgets are migrating beyond pure-tech firms into healthcare, manufacturing and public services. These converging initiatives accelerate solution maturity, enrich local data sets and anchor long-term demand for high-performance compute, thereby lifting the Canada ICT market.

Universal Broadband Fund transforms rural digital infrastructure

The USD 3.2 billion Universal Broadband Fund targets 98% national coverage by 2026, prioritizing fiber rather than stop-gap wireless links, which unlocks low-latency connectivity vital for telehealth, online learning and cloud-based commerce in underserved communities [2]Government of Ontario, “Ontario’s Digital Strategy,” ontario.ca. Reliable links in Indigenous and northern areas enable digital government transactions and remote work participation, shrinking the urban-rural digital divide. As newly connected households adopt e-services, local SMEs gain cloud access, raising demand for cybersecurity, managed networks and SaaS billing solutions. In turn, this translates into steady incremental revenue streams that enlarge the Canada ICT market over the long term.

Rapid SME cloud migration accelerates digital transformation

Cloud subscriptions now account for 55.6% of total deployments and grow at 10.9% annually, propelled by programs such as the national Canada Digital Adoption Program and Québec’s grant that covers up to USD 1.5 million per project. Shopify’s merchant platform illustrates tangible benefits, posting 27% revenue growth to USD 2.36 billion in Q1 2025 as more Canadian sellers embrace embedded commerce tools. Pay-as-you-go models reduce capital outlay, letting SMEs deploy ERP, CRM and cybersecurity services within weeks and scale usage with sales cycles. The result is a broader customer base and recurring revenues that reinforce the Canada ICT market’s expansion momentum.

Data-center investments reshape regional economics

Ontario and Québec together attracted over USD 7 billion in hyperscale capital from operators such as Cologix and eStruxture owing to abundant hydroelectric power and supportive incentive schemes. These facilities drive demand for optical networking, power-management software and specialist security services. Enterprises benefit from lower latency and sovereign data storage, encouraging repatriation of sensitive workloads that were previously hosted abroad. Edge computing nodes are emerging around Montréal and Toronto, providing distributed processing for IoT, gaming and streaming applications that further deepen the Canada ICT market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute tech-talent shortage and wage inflation | −1.9% | National, highest in Toronto, Vancouver, Montréal | Short term (≤2 years) |

| Slow capital-equipment refresh outside Tier-1 metros | −0.8% | Rural and secondary urban centers | Medium term (2-4 years) |

| Legacy telecom duopoly limiting price competition | −1.2% | National, with regional variations | Long term (≥4 years) |

| Data-sovereignty concerns delaying cross-border cloud workloads | −0.7% | Financial services and government users nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tech-talent shortage constrains growth despite strong demand

Sixty-eight percent of employers report hiring difficulties and the national unemployment rate for digital roles sits below 3.3%. Cybersecurity alone needs 26,000 additional professionals by 2025, inflating wages and squeezing SME budgets. Provinces respond with intensive bootcamps and micro-credential programs, yet mismatches persist between academic curricula and enterprise toolchains. The gap accelerates automation adoption but can lengthen project delivery times, trimming the Canada ICT market’s near-term growth trajectory.

Telecom duopoly pricing pressures limit market expansion

Rogers, Bell and Telus control close to 85% of retail telecom revenue, resulting in some of the G7’s highest data prices despite wholesale access mandates by the CRTC. The recent Rogers–Shaw merger and Bell’s USD 3.47 billion Ziply Fiber purchase strengthened their regional footholds, complicating price competition for smaller ISPs. Enterprises, especially cost-sensitive SMEs, defer bandwidth-intensive solutions when connectivity fees remain elevated, dampening potential spending on adjacent cloud and managed services inside the Canada ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Software leadership shapes market evolution

IT Software captured 32.80% of 2025 revenue, giving it the largest slice of the Canada ICT market. Platform-as-a-service, low-code suites and vertical SaaS bundles help firms digitize workflows without heavy infrastructure. In parallel, IT Security/Cybersecurity posts the fastest 10.85% CAGR as privacy mandates, breach insurance clauses and ransomware activity force upgrades. The Canada ICT market size for cybersecurity reached USD 14.12 billion in 2025 and should climb steadily as zero-trust and extended-detection technologies roll out. Hardware demand is mixed: networking equipment benefits from 5G and data-center scale-outs while client devices face price erosion. Services revenue remains resilient because managed service providers bridge skills shortages and integrate multicloud estates.

Cross-segment AI infusion is now routine. OpenText’s USD 5.77 billion turnover demonstrates appetite for unified information-management stacks that span content, process and security. As vendors bundle analytics and observability with core products, enterprises consolidate suppliers, enhancing recurring billings and strengthening the Canada ICT market.

By End-user Enterprise Size – SME growth accelerates digital democratization

Large Enterprises held 59.90% of 2025 spending thanks to complex, multi-year modernization roadmaps and in-house IT teams. However, SMEs are advancing at a 10.14% CAGR, outpacing broader growth as affordable SaaS licenses, business-process automation and provincial subsidies reduce adoption risk. The Canada ICT market size captured by SMEs is forecast to exceed USD 73.6 billion by 2031, translating into an expanding addressable base for cloud security and fintech payment platforms.

SME cloud uptake also fuels demand for API-first accounting, point-of-sale and marketing applications that integrate with Shopify’s merchant ecosystem, highlighting product-led expansion paths. Meanwhile, large enterprises experiment with generative AI copilots for code, finance and customer support, a trend that raises security and governance requirements, thus creating services revenue for integrators across the Canada ICT market.

By End-user Industry – Healthcare leads transformation

BFSI maintained a 24.20% share of 2025 revenue by upgrading mobile banking and fraud-prevention systems, underscoring its status as the single largest vertical inside the Canada ICT market. Healthcare’s 11.55% forecast CAGR makes it the fastest mover, aided by 93% adoption of electronic medical records among family physicians and ongoing telehealth reimbursement policies. As hospitals deploy AI-enabled imaging and remote patient monitoring, data-integration and identity-management tools rise in tandem.

Government spending follows close behind, with Ottawa and provinces digitizing licensing, tax and benefits services, boosting demand for content-management systems and citizen-facing mobile apps. Energy and manufacturing drive smart-grid and predictive-maintenance spending, supporting IoT gateways and analytics platforms. Retail trails yet shows healthy upside through immersive commerce, computer-vision checkout and supply-chain visibility, widening the solution canvas for the Canada ICT industry.

By Deployment Mode – Cloud dominance underpins hybrid strategies

Cloud deployments represented 56.10% of revenue in 2025 and continue to lead at a 10.42% CAGR, confirming their pivotal role in the Canada ICT market. Yet hybrid models persist because finance, public sector and critical infrastructure operators require on-prem control for sensitive workloads subject to residency mandates. The Canada ICT market share for cloud is projected to exceed 65.30% by 2031 as data-center availability zones multiply and providers certify industry-specific compliance.

Microsoft’s forthcoming AI region, paired with partnerships that ensure Canadian data residency, exemplifies continental cloud expansion aligned with local rules. OpenText generated USD 1.82 billion in cloud revenue last fiscal year, illustrating robust demand for SaaS versions of document and workflow suites. Over the forecast horizon, workload portability, container orchestration and FinOps tooling will draw incremental spending, sustaining hybrid adoption across the Canada ICT market.

Geography Analysis

Ontario remains the largest provincial contributor, adding over USD 41 billion to GDP and hosting the country’s densest cluster of software firms, banks and hyperscaler campuses. The province’s Digital Strategy, backed by a USD 500 million acceleration fund, aims to digitize public services and grow high-tech employment, reinforcing local demand for AI platforms, cybersecurity and managed networks. Hundreds of start-ups leverage Toronto’s innovation corridors, feeding AI, fintech and health-tech use cases that anchor venture capital flows and deepen the Canada ICT market.

Quebec delivers the fastest growth through 2031 as its USD 125 million AI budget, quantum innovation zones and digital-ID roadmap stimulate spending on data governance, identity management and sovereign cloud. Montréal’s bilingual talent pool and abundant renewable energy attract data-center builders, while regional tax credits support video-game and VFX studios, extending the technology ecosystem. The provincial government targets complete digital-ID rollout by 2028, which requires robust security architectures, driving incremental software and services consumption within the Canada ICT market.

British Columbia and Alberta round out the top four regions. Vancouver’s clean-tech cluster nurtures cloud gaming, digital-media and cybersecurity firms, whereas Calgary harnesses oil-and-gas expertise to upscale industrial IoT and smart-grid solutions. Alberta’s Oliu digital-ID platform already serves 2.1 million verified users, demonstrating public-sector adoption at scale. Atlantic Canada and the northern territories benefit from broadband grants that convert connectivity into e-commerce and telehealth gains, fostering inclusive growth across the wider Canada ICT market.

Competitive Landscape

Competition in the Canada ICT market is intense yet moderately concentrated. Rogers, Bell and Telus dominate network access, but global cloud hyperscalers, domestic software champions and hundreds of specialist integrators vie for share in adjacent layers. Microsoft’s commitment to a USD 80 billion AI-optimized region signals escalating hyperscale rivalry, while Amazon Web Services adds new availability zones to address local compliance demands. These capacity investments promote multicloud adoption, boosting demand for orchestration, FinOps and security managed services.

Consolidation shapes the services tier. World Wide Technology closed a USD 1.249 billion purchase of Softchoice, aligning hardware resale with cloud transformation consulting [3]Channel Futures, “WWT closes Softchoice acquisition,” channelfutures.com. CGI expanded its data-analytics bench by acquiring Momentum Technologies, adding 250 professionals who specialize in business intelligence. Meanwhile, Bell snapped up Ziply Fiber for USD 3.47 billion to extend fiber reach across the Pacific Northwest. Such moves improve geographic coverage and solution breadth, raising the bar for smaller rivals within the Canada ICT market.

Innovation continues from home-grown leaders. Shopify generated USD 2.36 billion in Q1 2025 by expanding payment, fulfillment and B2B marketplaces, and it invests heavily in AI-driven merchant tooling. OpenText integrates security, content and analytics in a unified cloud platform, translating to USD 5.77 billion in revenue for fiscal 2025. Constellation Software pursues a buy-and-build playbook across niche vertical software, accumulating USD 2.468 billion in Q2 2024 sales. Such diversified strategies ensure that no single vendor controls the broader Canada ICT market, thereby sustaining healthy service innovation and pricing dynamics.

Canada ICT Industry Leaders

Amazon Web Services, Inc

CGI Inc.

Rogers Communications Inc.

Bell Canada

Telus Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: H.I.G. Capital acquired Converge Technology Solutions and merged it with Mainline Information Systems, forming Pellera Technologies to enhance multi-vendor delivery.

- March 2025: CGI acquired Momentum Technologies, bringing 250 analytics specialists and deepening its presence in Québec’s public and insurance segments.

- January 2025: World Wide Technology completed its USD 1.249 billion acquisition of Canadian VAR Softchoice, expanding software, cloud and AI capabilities.

- November 2024: Bell Canada announced a USD 3.47 billion acquisition of Ziply Fiber to broaden fiber coverage in the Pacific Northwest.

Canada ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

The Canadian ICT market is segmented by type (hardware, software, IT services, and telecommunication services), by the size of the enterprise (small and medium enterprise and large enterprise), by industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, and energy and utilities). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| IT Hardware | Computer Hardware | |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure / Data Centers | ||

| IT Security / Cybersecurity | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| Communication Services | ||

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| IT and Telecom |

| Government |

| Retail and E-commerce |

| Manufacturing |

| Healthcare |

| Energy and Utilities |

| Others |

| On-premise |

| Cloud |

| By Type | IT Hardware | Computer Hardware | |

| Networking Equipment | |||

| Peripherals | |||

| IT Software | |||

| IT Services | Managed Services | ||

| Business Process Services | |||

| Business Consulting Services | |||

| Cloud Services | |||

| IT Infrastructure / Data Centers | |||

| IT Security / Cybersecurity | Solutions | Application Security | |

| Cloud Security | |||

| Data Security | |||

| Identity and Access Management | |||

| Infrastructure Protection | |||

| Integrated Risk Management | |||

| Network Security Equipment | |||

| Other Solutions | |||

| Services | Professional Services | ||

| Managed Services | |||

| Communication Services | |||

| By End-user Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Government | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Healthcare | |||

| Energy and Utilities | |||

| Others | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

Key Questions Answered in the Report

What is the current size of the Canada ICT market?

The market is valued at USD 146.42 billion in 2026 and is on course to reach USD 206.47 billion by 2031.

Which segment grows fastest in the Canada ICT market?

IT Security/Cybersecurity shows the highest projected growth at an 10.85% CAGR through 2031, driven by escalating threat levels and compliance mandates.

How significant is cloud adoption in Canada?

Cloud deployments account for 56.10% of total ICT spending and are expanding at a 10.42% CAGR as enterprises favor scalable, subscription-based models.

Why is Quebec considered the fastest-growing regional market?

Quebec combines substantial AI funding, renewable energy and digital-ID programs, translating into above-average ICT spending momentum.

Page last updated on: