France IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

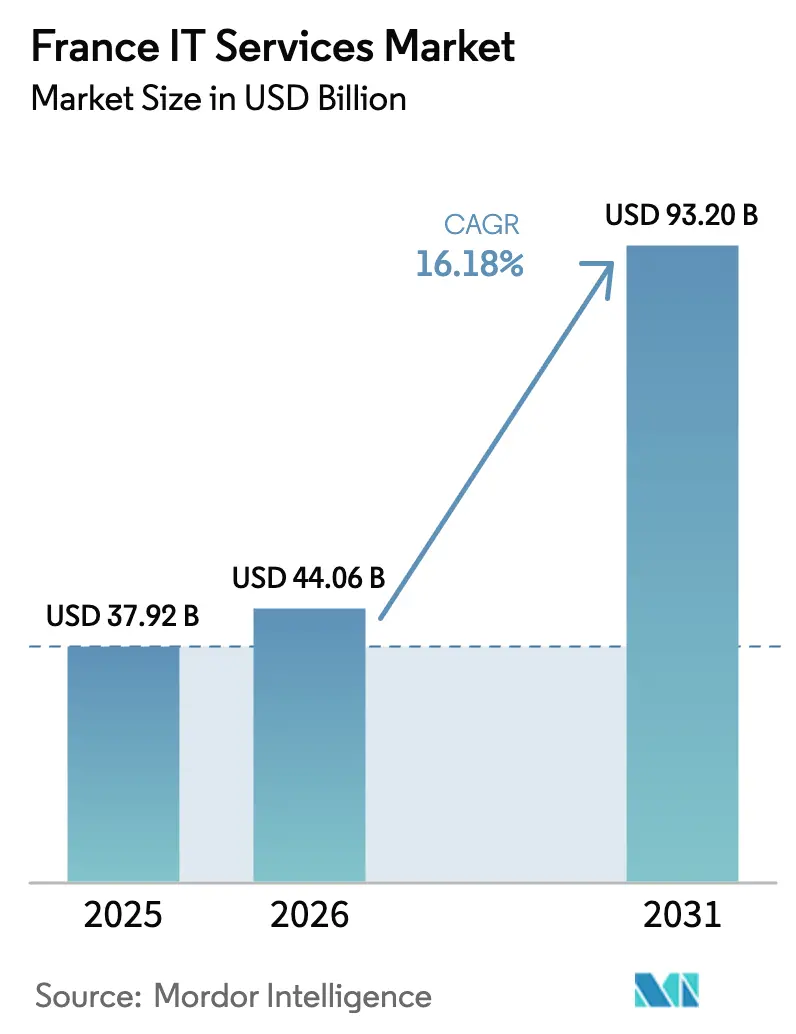

| Base Year Market Size (2025) | USD 37.92 Billion |

| Market Size (2026) | USD 44.06 Billion |

| Market Size (2031) | USD 93.2 Billion |

| Growth Rate (2026 - 2031) | 16.18% CAGR |

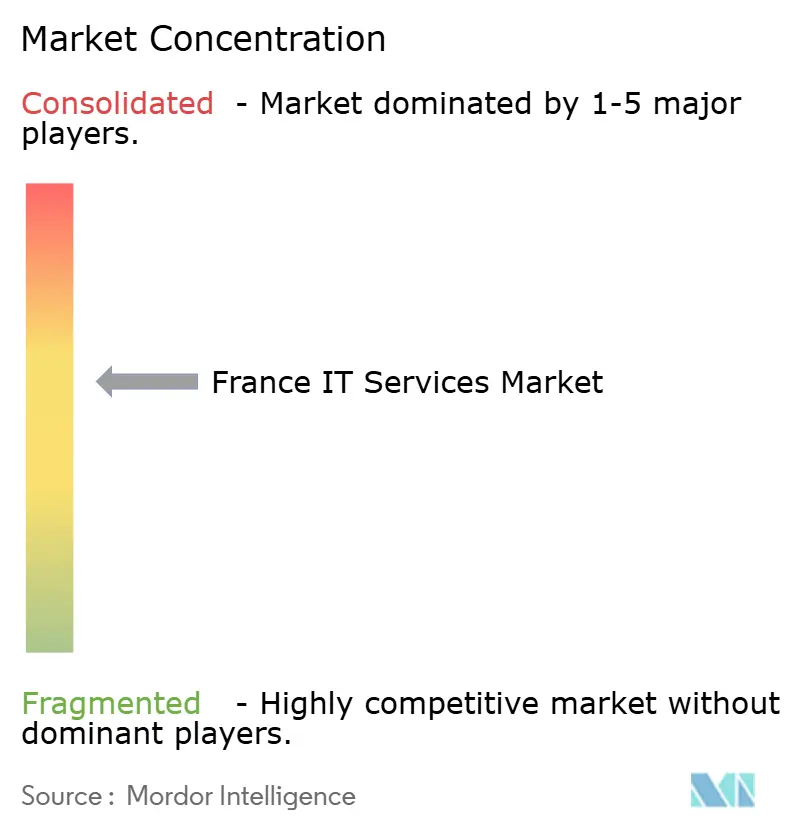

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France IT Services Market Analysis by Mordor Intelligence

The France IT services market size in 2026 is estimated at USD 44.06 billion, growing from 2025 value of USD 37.92 billion with 2031 projections showing USD 93.2 billion, growing at 16.18% CAGR over 2026-2031. This expansion stems from steady government funding, strict GDPR compliance, and rapid uptake of sovereign-cloud solutions that guarantee local data residency. Spending momentum remains strongest in cloud migration, managed security, and AI-enabled service delivery, while hybrid outsourcing models allow enterprises to align operating costs with revenue cycles. The competitive field mixes domestic champions and global consultancies, each chasing opportunities in healthcare digitalization, SME enablement, and AI-driven automation. Cost pressure persists, yet energy-tax incentives and local data-center efficiency programs help preserve margins.[1]Direction Générale des Entreprises, “France Relance—Digital Modernization Measures,” entreprises.gouv.fr

Key Report Takeaways

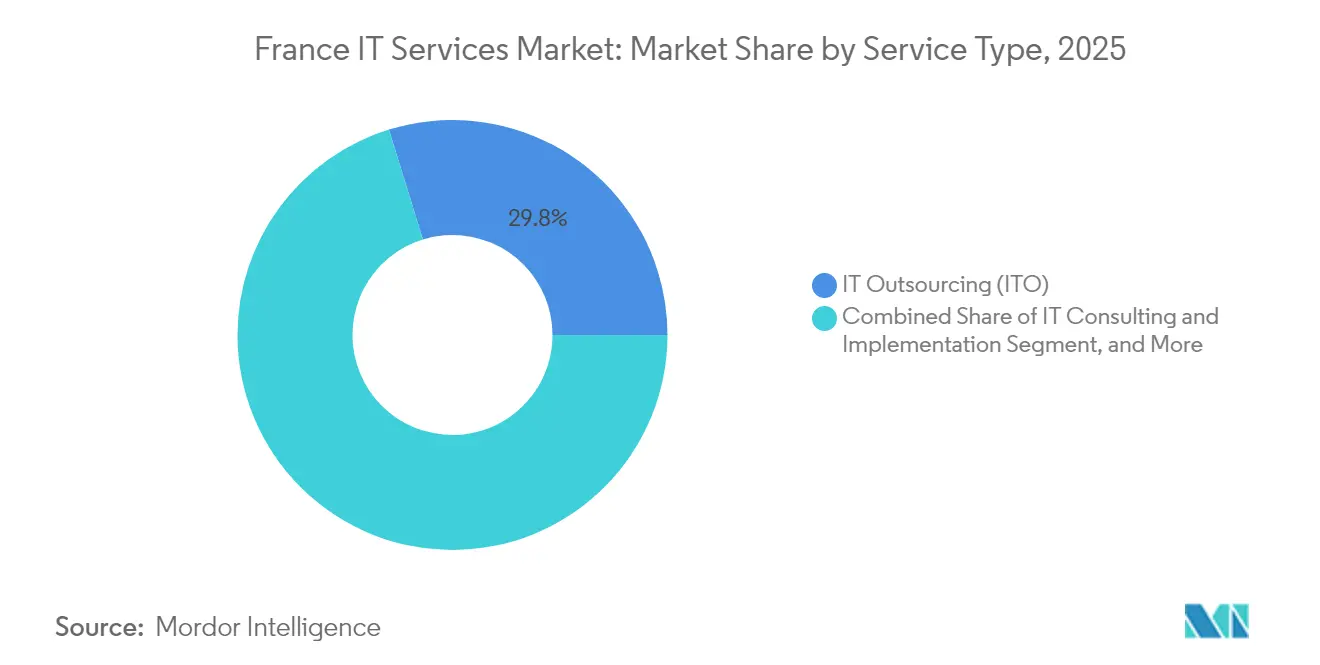

- By service type, IT Outsourcing (ITO) held 29.78% of France IT services market share in 2025, whereas Managed Security Services is projected to post a 19.05% CAGR through 2031.

- By enterprise size, Large Enterprises contributed 67.74% of 2025 spending, yet Small and Medium Enterprises are forecast to expand at an 18.12% CAGR to 2031.

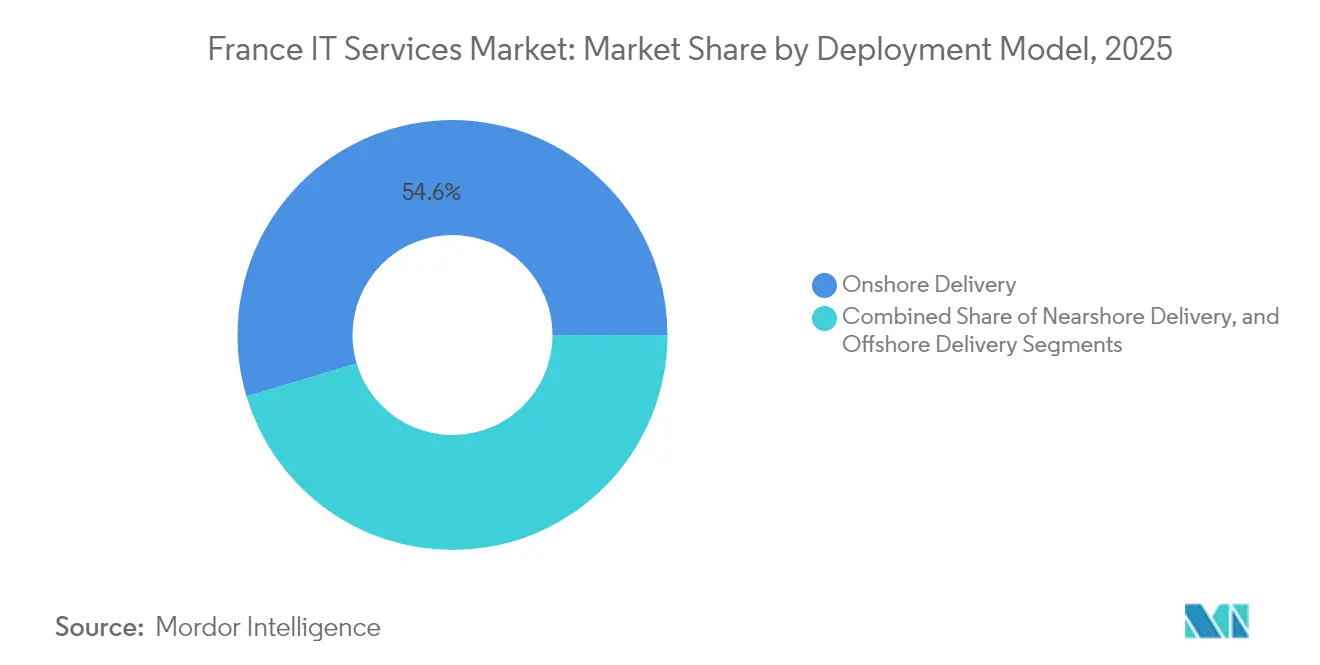

- By deployment model, Onshore Delivery commanded 54.62% of 2025 revenue, while Nearshore Delivery is advancing at an 17.94% CAGR over the forecast period.

- By end-user vertical, BFSI led with 24.28% revenue share in 2025, while Healthcare and Life-Sciences are expected to accelerate at a 18.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated cloud adoption among French enterprises | +3.2% | National, with a concentration in the Paris and Lyon metropolitan areas | Medium term (2-4 years) |

| Rising demand for managed security amid GDPR compliance | +2.8% | National, with a heightened focus on financial services and healthcare sectors | Short term (≤ 2 years) |

| Government digital-transformation funding (France Relance) | +2.1% | National, with priority allocation to the public sector and critical infrastructure | Medium term (2-4 years) |

| Growing outsourcing to optimize IT costs post-pandemic | +1.9% | National, with stronger adoption in the manufacturing and retail sectors | Short term (≤ 2 years) |

| Emergence of sovereign-cloud offerings for data residency | +1.7% | National, with emphasis on government agencies and essential services | Long term (≥ 4 years) |

| Rapid uptake of AI-driven IT operations (AIOps) in the mid-market | +1.5% | National, with early adoption in telecommunications and energy sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Adoption Among French Enterprises

Cloud-first directives and a USD 713 million public-sector cloud envelope under France 2030 have led organizations of all sizes to migrate workloads at pace. Providers report that multi-cloud orchestration services outstrip classic data-center management in new contract value. Subscription-based, outcome-linked engagements dominate tenders, signaling a structural shift from time-and-materials contracts. Mid-market firms, once wary of external hosting, now adopt sovereign-cloud environments to unlock analytics and AI functionality previously reserved for large enterprises. The ripple effect boosts demand for application refactoring, container management, and cloud FinOps advisory.

Rising Demand for Managed Security Amid GDPR Compliance

GDPR enforcement and CNIL oversight have raised cyber-risk stakes, prompting enterprises to outsource security operations in order to guarantee 24×7 monitoring and incident response. Regulated industries face steep fines for breach-notification lapses, so managed security contracts increasingly bundle regulatory expertise with technical controls. Providers that maintain SecNumCloud-certified platforms and hold trusted relationships with ANSSI gain a durable competitive edge, especially when they can demonstrate localized data handling and rapid audit support. Converged offerings that unify threat intelligence, SOC, and compliance dashboards resonate strongly with BFSI and healthcare buyers.

Government Digital-Transformation Funding (France Relance)

Public-sector modernization receives full project-cost coverage under specific France Relance sub-programs, funneling fresh demand toward French IT consultancies well-versed in procurement rules. Municipal portals, citizen-identity services, and e-invoicing upgrades dominate award lists, stimulating systems integration and low-code platform workstreams. Because the grants favor domestic suppliers, local champions obtain repeatable revenue streams and reference sites that translate into private-sector credibility. The initiative further embeds digital sovereignty by requiring that cloud workloads remain in certified data centers.[2]Direction Générale des Entreprises, “France 2030 Cloud Investment Plan,” entreprises.gouv.fr

Growing Outsourcing to Optimize IT Costs Post-Pandemic

Budget-conscious enterprises now blend onshore strategy with nearshore execution, achieving 20-30% savings versus fully domestic delivery. Outcome-based contracts underpinned by service-level dashboards tie vendor remuneration to measurable business KPIs rather than labor hours. Manufacturing and retail firms accelerate engagement handoffs, freeing capital for supply-chain resilience projects. Vendors that invest in automation, process mining, and robotic service desks can deliver productivity gains that offset wage inflation and talent scarcity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of skilled IT professionals | -2.3% | National, with particular severity in Paris, Lyon, and Toulouse tech hubs | Long term (≥ 4 years) |

| High domestic labor costs versus near/offshore options | -1.8% | National, with competitive pressure most acute in commodity IT services | Medium term (2-4 years) |

| Heightened union scrutiny of ITO/BPO offshoring | -1.2% | National, with the strongest opposition in traditional industrial regions | Short term (≤ 2 years) |

| Energy-price volatility is hitting data-center margins | -0.9% | National, with particular impact on hyperscale data center operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Skilled IT Professionals

Cloud engineers, cybersecurity analysts, and AI specialists remain in short supply, inflating salary bands and elongating project lead times. Domestic recruitment is insufficient, and graduate output lags demand, making international sourcing and automation unavoidable. Leading providers partner with engineering schools to create fast-track curricula, while also adopting low-code, no-code toolsets to curb reliance on senior developers. Over the forecast horizon, the talent deficit will temper service-delivery capacity even as demand surges.

High Domestic Labor Costs Versus Near/Off-Shore Options

Average French development rates roughly quadruple those in Eastern Europe, prompting clients to insist on blended teams that balance expertise and cost. Providers differentiate by emphasizing high-value consulting, regulatory fluency, and on-site governance—capabilities less amenable to relocation. Hybrid delivery gains acceptability because it retains strategic roles in France while transferring repetitive engineering tasks abroad, thereby reducing project cost without sacrificing compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Drive Growth

Managed Security Services is expected to deliver a 19.05% CAGR, well above the broader France IT services market growth. The segment capitalizes on rising threat complexity and mandatory breach-reporting timetables. Meanwhile, the ITO category accounted for 29.78% of France's IT services market share in 2025 as enterprises used outsourcing to pivot capital toward growth initiatives. Some clients move from staff-augmentation to managed-capacity models, prompting providers to embed self-healing AIops into service catalogs.

Cloud and Platform Services continue to benefit from the EUR 1.8 billion (USD 2.10 billion) state investment earmarked for sovereign-cloud ecosystems, with workloads shifting from private data centers to SecNumCloud-qualified platforms. Traditional BPO confronts union opposition to offshoring, yet demand persists for digital front-office solutions integrated with conversational AI. Consulting and implementation services thrive on large-scale ERP and CRM modernization funded through France Relance grants.

By End-User Enterprise Size: SME Acceleration

SMEs are forecast to post an 18.12% CAGR, outpacing the overall France IT services market and narrowing the digital gap with larger corporations. Government programs such as France Num subsidize advisory costs and training, while off-the-shelf SaaS bundles reduce complexity barriers. High adoption of collaborative suites, e-commerce plugins, and cybersecurity subscriptions underscores the democratization of advanced tools.

Large Enterprises will sustain the bulk of expenditure thanks to extensive legacy estates and global operating footprints. Their focus shifts toward generative-AI pilots, zero-trust network redesign, and green IT initiatives that lower carbon footprints. Vendors able to cross-sell strategic consulting, change-management support, and continuous engineering services maintain preferred-supplier status.

By Deployment Model: Nearshore Momentum

Nearshore centers in Poland, Romania, and Morocco attract application maintenance and QA workloads, supporting an 17.94% CAGR for this model within the French IT services market. Clients welcome overlapping time zones and cultural affinity, enabling agile ceremonies without late-night calls. Onshore resources remain indispensable for business-critical architecture and stakeholder engagement, keeping onshore delivery at 54.62% of 2025 spend and ensuring that knowledge of French regulation stays domestic.

Offshore engagement beyond Europe faces union scrutiny and data-residency limits, yet retains relevance for cost-sensitive legacy remediation. Hybrid frameworks, under which customer-facing roles stay in France and engineering pods rotate in nearshore centers, strike a workable equilibrium between price and compliance. Providers signal performance through joint KPIs that track velocity, defect rates, and customer-satisfaction scores.

By End-User Vertical: Healthcare Digitization

Healthcare and Life are projected to deliver a 18.66% CAGR as the France 2030 digital-health program funds electronic patient records, telemedicine platforms, and AI-driven diagnostics. Clinical workflow optimization and interoperability projects dominate RFP volumes, with emphasis on HIPAA-equivalent privacy guarantees and local data residency. Providers with ISO 13485 familiarity and SecNumCloud pedigrees secure multi-year managed-service deals.

BFSI continues to wield the highest absolute budget, claiming 24.28% of 2025 expenditure. Mainframes integrate with cloud-native micro-services to satisfy PSD2, DORA, and real-time payment requirements. Manufacturing accelerates Industry 4.0 investments that connect production lines to digital twins, while public-sector agencies roll out citizen portals and paperless administration funded by France Relance. Energy and Utilities buyers emphasize AIOps for grid stability and predictive maintenance.

Geography Analysis

Paris and the wider Île-de-France corridor accounted for a significant share of the 2024 France IT services market consumption, driven by the presence of corporate headquarters, financial regulators, and hyperscale data centers. Lyon’s biotech cluster and Toulouse’s aerospace ecosystem create secondary demand pockets where high-end engineering and cybersecurity services dominate engagement scopes. Nice and Sophia Antipolis contribute AI research spin-offs that feed specialized analytics projects.

Northern regions such as Hauts-de-France and Grand Est lean toward manufacturing modernization and supply-chain resilience projects, whereas Occitanie and Provence-Alpes-Côte d’Azur prioritize tourism tech and logistics optimization. Territorial digital-transformation grants totaling EUR 88 million (USD 102.75 million) subsidize infrastructure rollouts in mid-size cities, supporting local e-government portals and cloud-based ERP for municipalities. Harmonized CNIL guidelines ensure that cybersecurity and privacy controls remain consistent nationwide.

French providers increasingly tap nearshore facilities for overflow capacity while retaining design authority domestically. Cross-border projects grow as EU initiatives funnel capital into sovereign-cloud and 5G corridors, positioning France as a regional delivery hub linked by high-speed rail to Brussels, Frankfurt, and Barcelona. Post-Brexit relocation of certain banking workloads from London to Paris further deepens local demand for bilingual IT specialists conversant with both EU and UK regulation.

Competitive Landscape

Moderate concentration characterizes the France IT services market, with the top domestic players—Capgemini, Atos, and Sopra Steria—leveraging deep regulatory knowledge and longstanding government contracts. Capgemini’s 2024 revenue of EUR 22.096 billion (USD 25.80 billion) underlines scale, yet the firm pivots to margin-rich AI consulting and sustainable-IT advisory after flat growth in traditional sectors. Atos restructures around Eviden, targeting cybersecurity and advanced computing, while Sopra Steria widens financial-services consulting via the proposed Aurexia acquisition.[4]Sopra Steria, “Proposed Acquisition of Aurexia,” soprasteria.com

Global incumbents IBM and Accenture complement extensive hyperscale alliances with French data-sovereignty guarantees, while Indian heritage firms TCS and Infosys expand La Défense innovation labs focusing on human-centric AI. M&A remains a tool for fast-tracking capability gaps; targets include boutique AIops vendors, niche healthcare ISVs, and cloud-security specialists. Clients favor providers that can articulate transparent ESG roadmaps, prompting investments in green-data-center certifications and circular-IT services.

Competitive differentiation converges on three pillars: domain depth, automation maturity, and proximity. Vendors that demonstrate sector-specific solution libraries, proprietary AI accelerators, and hybrid delivery governance frameworks increasingly win multi-tower renewals. As sovereign-cloud contracts gain momentum, alliances between IT providers and national telecom operators become pivotal, co-creating secured cloud environments certified by ANSSI and SecNumCloud standards.

France IT Services Industry Leaders

Capgemini SE

Atos SE

Sopra Steria Group SA

Inetum (GFI Informatique) SA

Orange Business Services (Orange SA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Capgemini opened exclusive talks to acquire India’s WNS Holdings, aiming to deepen BPO vertical expertise and broaden global delivery reach.

- April 2025: BNP Paribas renewed a multi-year IBM Cloud partnership focused on resilience and generative-AI enablement.

- February 2025: Capgemini reported FY 2024 revenue of EUR 22.096 billion (USD 23.6 billion) and pledged sustained investment in generative-AI offerings that drove 6% of Q1 2025 bookings.

- January 2025: Sopra Steria entered exclusive negotiations to acquire Aurexia, reinforcing its French banking and insurance consulting footprint.

France IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery | |

| By End-user Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-user Verticals |

Key Questions Answered in the Report

What CAGR is projected for the France IT services market through 2031?

The market is forecast to expand at 16.18% annually from 2026 to 2031.

Which service line is growing fastest in France?

Managed Security Services is projected to record a 19.05% CAGR as organizations outsource GDPR-grade cyber defense.

Why are SMEs accelerating technology spending?

Subsidies under the France Num program and affordable SaaS bundles have reduced entry barriers, driving an 18.12% CAGR in SME uptake.

How does nearshore delivery benefit French enterprises?

Nearshore centers in Eastern Europe and North Africa offer cost savings of roughly 50-75% while maintaining cultural and time-zone alignment.

Which vertical offers the highest growth opportunity?

Healthcare and Life-Sciences leads with a 18.66% CAGR as digital health investments proliferate under France 2030.

What factors shape vendor selection in the country?

Buyers prioritize regulatory expertise, sovereign-cloud credentials, and AI-enabled automation capabilities when awarding contracts.

Page last updated on: