United Arab Emirates IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

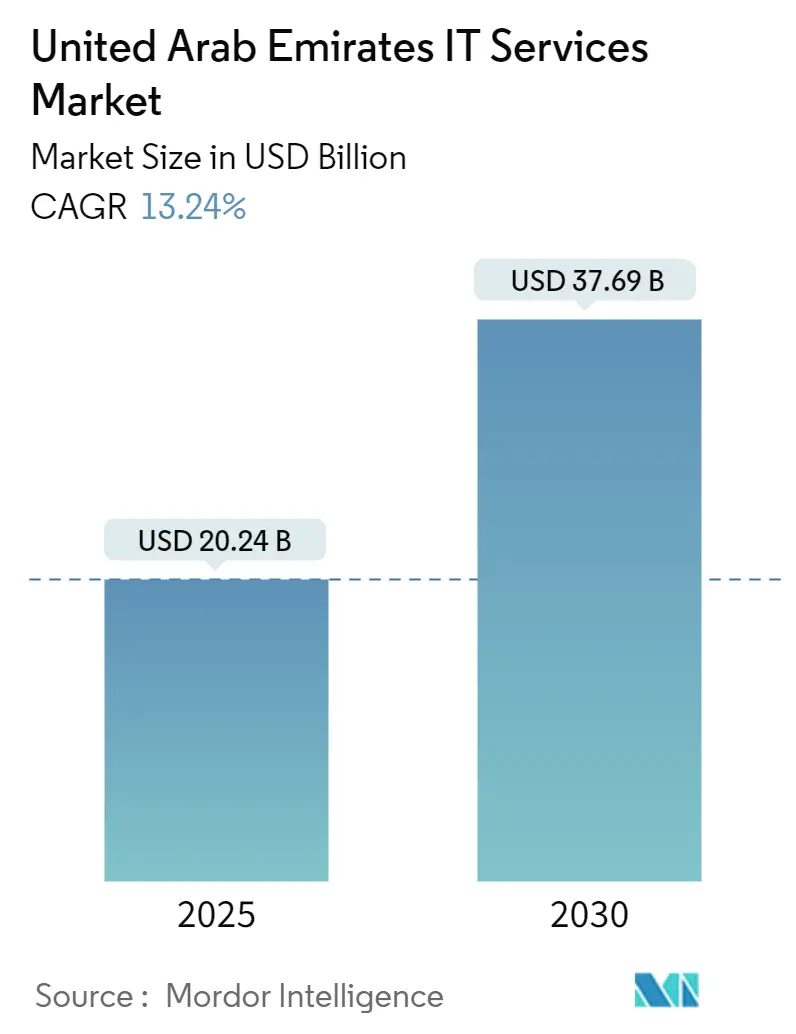

| Market Size (2025) | USD 20.24 Billion |

| Market Size (2030) | USD 37.69 Billion |

| Growth Rate (2025 - 2030) | 13.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates IT Services Market Analysis by Mordor Intelligence

The UAE IT services market size reached USD 20.24 billion in 2025 and is projected to advance to USD 37.69 billion by 2030, translating into a 13.24% CAGR over the forecast period.[1]UAE Government, “E-commerce Law in the UAE,” u.ae Growth rests on mandatory federal cloud migration timelines, sovereign data-residency rules and the National AI Strategy 2031, all of which are compelling ministries and enterprises to modernize core systems. Capital expenditure on sovereign cloud regions, AI-rich data centers and zero-trust security frameworks is widening addressable revenues for vendors that combine local hosting with advanced analytics. Consolidation among regional champions and global hyperscalers is reshaping service architectures, while government procurement quotas for citizen-owned SMEs are opening new entry points for standardized SaaS and managed-service bundles. Heightened cyber-risk-more than 50,000 daily attacks reported in 2024-keeps security operations and threat-intelligence services on executive roadmaps, encouraging bundled offerings that fuse infrastructure, AI and protection layers.

Key Report Takeaways

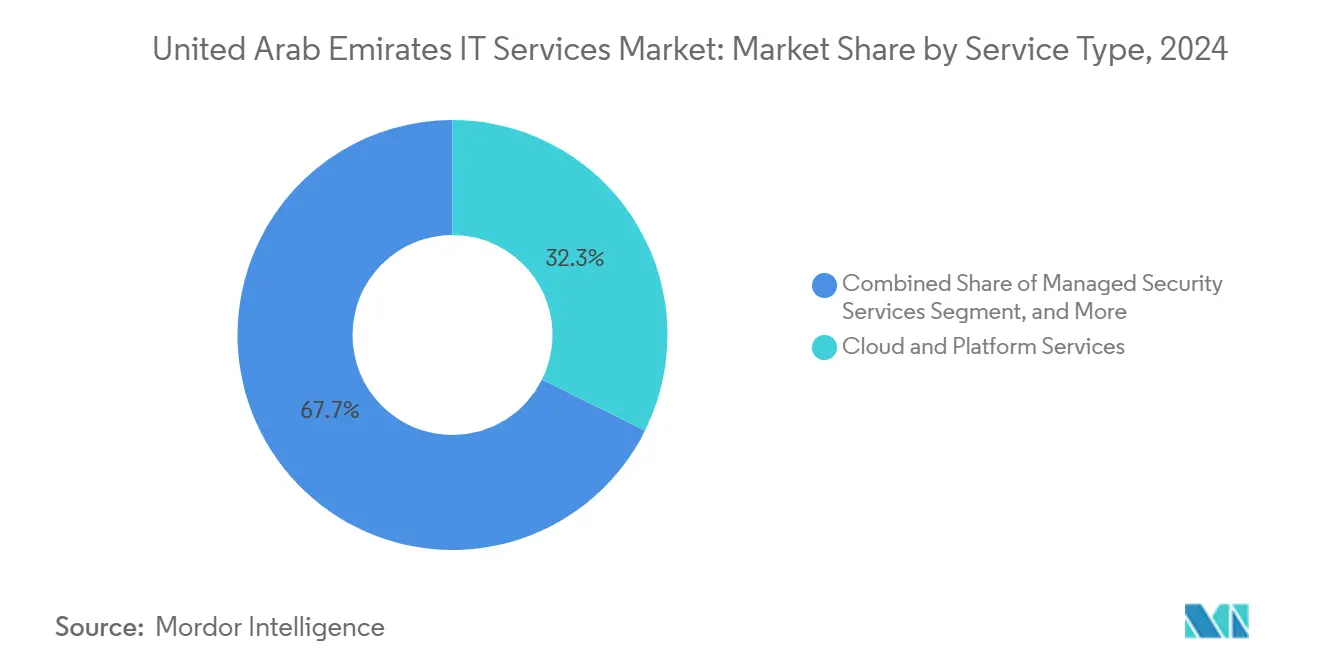

- By service type, cloud and platform services led with 32.33% of UAE IT services market share in 2024; managed security services are set to grow at an 18.70% CAGR through 2030.

- By enterprise size, large enterprises accounted for 63.04% of the UAE IT services market in 2024, whereas SMEs are forecast to expand at a 15.90% CAGR to 2030.

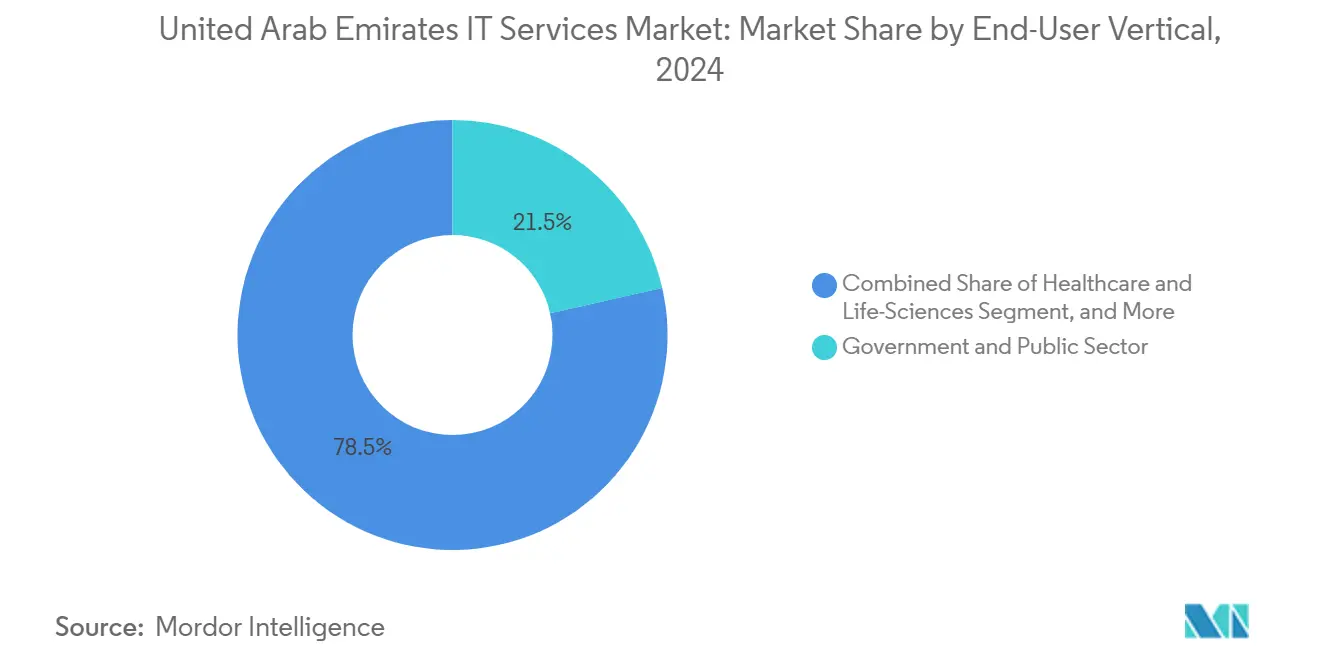

- By end-user vertical, government and public sector contributed 21.50% to 2024 revenue, while healthcare and life sciences are pacing the field at a 17.40% CAGR through 2030.

- By delivery model, onshore engagements dominated 2024 billings and are expected to retain leadership given Federal Decree-Law No. 45-2021 on data protection.

United Arab Emirates IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digital-economy targets under UAE Digital Economy Strategy | +3.20% | National, with concentrated impact in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Mandatory federal cloud migration (FEDnet/IaaS) for ministries | +2.80% | Federal government entities nationwide | Short term (≤ 2 years) |

| Surge in AI/Gen-AI pilot projects post 2023 National AI Strategy | +2.50% | National, with Abu Dhabi leading implementation | Medium term (2-4 years) |

| Mega-events (COP28 legacy, Dubai Expo City) requiring ICT over-build | +1.90% | Dubai and Abu Dhabi, spillover to Northern Emirates | Long term (≥ 4 years) |

| Skill-intensive cybersecurity demand after new TDRA Zero-Trust mandates | +1.70% | National, with higher adoption in financial and government sectors | Short term (≤ 2 years) |

| Region-wide data-residency deals positioning UAE as GCC service hub | +1.30% | UAE as regional hub, serving broader GCC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating digital-economy targets under UAE Digital Economy Strategy

The cabinet’s goal to lift digital-economy contribution to 19.4% of GDP by 2025 is fuelling a wave of multi-year transformation programs across ministries and large corporates.[2]Abu Dhabi Digital Authority, “Abu Dhabi Digital Strategy 2025-2027,” adda.gov.ae Abu Dhabi set aside AED 13 billion (USD 3.5 billion) for AI-driven government platforms, pushing demand from basic virtualization into cognitive twins and autonomous operations. Health authorities are rolling out virtual nurses and AI diagnostic engines that call for cloud APIs, HL7 integrations and always-on SOC oversight. The mix of analytics, machine-learning orchestration and citizen-facing apps is nudging buyers toward vendors that can wrap consulting, build and run under a single SLA. Consequently, the UAE IT services market is pivoting from point projects to outcome-based, end-to-end managed services that carry higher lifetime value.

Mandatory federal cloud migration (FEDnet/IaaS) for ministries

Telecommunications and Digital Government Regulatory Authority has imposed a 2026 deadline for all ministries to shift legacy workloads onto the sovereign FEDnet stack. Certified suppliers with local data centers and UAE-national clearance now enjoy a protected pipeline of lift-and-shift, refactor and platform-engineering deals valued in the hundreds of millions. Sovereign-cloud clauses exclude offshore processing for sensitive classes, forcing even global hyperscalers to partner with local firms or build in-country regions. Migration complexity varies-some entities require code refactoring, others demand pure infrastructure relocation-opening parallel revenue streams for assessment, remediation and managed hosting. The policy anchors near-term growth for the UAE IT services market while cementing long-term annuity via managed cloud operations.

Expansion of 5G private networks in industrial zones

Manufacturing parks in Abu Dhabi’s KIZAD, Dubai Industrial City and Sharjah’s SAIF Zone are issuing RFPs for end-to-end 5G private networks that connect autonomous robots, video analytics and digital twins. Telecommunications operators bundle licensed spectrum, edge computing and managed SLA dashboards, while systems integrators supply network slicing, campus orchestration and OT cybersecurity. Early pilots at Emirates Global Aluminium achieved 25% reduction in unplanned downtime and 18% uplift in asset utilization, prompting adjacent metal, chemical and food-processing plants to replicate blueprints. Because 5G cores must reside within UAE borders for compliance, demand flows directly to onshore integration and managed-service contracts. The ripple effect enlarges use cases for AI-enabled quality inspection and predictive maintenance, amplifying service bookings across consulting, deployment and lifecycle support.

Surging demand for digital payment and fintech platforms

Cashless-transaction share in the UAE surpassed 70% of retail sales in 2024, and the Central Bank’s Instant Payment Platform mandates real-time clearing for all licensed banks by 2026. Fintechs are racing to integrate open-API gateways, biometric onboarding and AI fraud analytics, while incumbent lenders replat form core systems to support embedded finance and tokenized deposits. Each initiative triggers multi-tower projects covering cloud migration, microservice refactoring, ISO 20022 messaging and zero-trust security audits. Systems integrators with PCI-DSS and SOC 2 credentials are securing multi-year managed-service agreements that bundle payment-gateway operations, DevSecOps and 24×7 threat monitoring. As digital wallets expand to fuel subsidies, transit fares and cross-border B2B settlements, the addressable spend for specialized fintech integration and compliance services continues to widen.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising price-competition from India-based offshore vendors | -2.10% | National, affecting all service segments | Short term (≤ 2 years) |

| Limited Emirati talent pool inflating wage bills | -1.80% | National, with acute impact in Abu Dhabi and Dubai | Medium term (2-4 years) |

| Delayed public-cloud certifications for sensitive workloads | -1.30% | Federal and emirate-level government entities | Medium term (2-4 years) |

| Lengthy payment cycles in government contracts | -0.90% | Government and public sector clients | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising price competition from India-based offshore vendors

Indian majors continue to quote blended rates up to 60% below onshore delivery, pressing margins for local integrators. TCS retains Top-Employer status in the UAE, signalling deeper localization that combines low-cost engineering with Emirati client-facing teams. Hybrid execution-40% on-site, 60% offshore-satisfies non-regulated workloads, leaving local firms to defend share via specialization in data-sovereign and Arabic-language AI services. The intensity of low-cost bids is expected to suppress certain commodity projects within the UAE IT services market, although data-residency clauses still shield critical-sector work.

Limited Emirati talent pool inflating wage bills.

Emiratization quotas mandate rising shares of national staff in technical roles, yet only a limited pool holds advanced cloud or cybersecurity certification. du’s Future X graduate academy aims to train fresh cohorts, but the talent pipeline will take several cycles to close gaps. Until then, firms are importing expatriate specialists on short visas, which introduces retention risk and onboarding costs, tempering profitability in the UAE IT services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud-first mandates reshape the value mix.

Cloud and platform services captured 32.33% of the UAE IT services market size in 2024 and are forecast to expand at a 13.8% CAGR through 2030 as ministries complete sovereign-cloud cutovers and enterprises pivot to hybrid landing zones. Adoption accelerates any workload that benefits from elastic scale, automated patching and regionally compliant backup, allowing vendors to embed AI APIs, edge orchestration and data-fabric connectors in one commercial stack. Mandatory encryption, key-management and zone-residency rules favour onshore hyperscale regions that rely on local partners for last-mile integration, giving rise to joint operating models in which global providers own infrastructure while domestic specialists manage tenancy design and migration. Managed security services ranked second in momentum, growing at an 18.70% CAGR, driven by TDRA zero-trust guidelines that require micro-segmentation, multifactor identity and 24×7 telemetry consolidation. Consulting and implementation revenues remain resilient because every lift-and-shift triggers a chain of assessment, target-architecture design and legacy API refactoring that neither SaaS publishers nor hyperscalers deliver directly. Business-process outsourcing is advancing more slowly but still finds niches in finance back-office, health-insurance adjudication and multilingual call-center support once data-locality guarantees are in place. IT outsourcing margins are under stress from offshore rate cards, yet complex refactor programs tied to confidential data continue to reward firms that can deploy certified Emirati architects.

The UAE IT services market share held by cloud and platform lines is expected to edge up to 35.4% by 2030 as workloads exit proprietary data centers. Service providers are monetizing adjacent analytics by layering data-mesh blueprints, real-time observability and MLOps pipelines that turn consumption-based hosting into outcome-priced managed services. Sovereign workload escalation clauses built into new master service agreements lock customers into three- to five-year minimum terms, improving revenue visibility for vendors. Meanwhile, hyperscalers are funding partner enablement grants that underwrite certification and solution-factory accelerators, narrowing capability gaps for mid-tier firms. As a result, the competitive frontier is shifting from raw infrastructure supply to domain-rich packaged platforms for healthcare, financial crime analytics and digital twin maintenance. Vendors that combine verticalized IP with certified sovereign footprints are best positioned to outpace the broader UAE IT services market.

By Enterprise Size: SME cloud uptake widens the addressable base.

Large organizations dominated spending with 63.04% of 2024 revenue, relying on multi-tower contracts that span consulting, build and run across thousands of users, petabyte-scale data sets and audited security baselines. They procure through tier-one systems integrators or global advisories that can field deep benches of architects, change-management experts and program-governance staff. Most have already rationalized core ERP and are now investing in AI copilots, predictive maintenance models and zero-trust overlays that expand wallet share for incumbent partners. Procurement sophistication, however, is forcing price compression on commodity towers, pushing vendors to automate ticket handling and apply AIOps to preserve margins.

SMEs are projected to lift the UAE IT services market size at a 15.90% CAGR, aided by federal rules reserving 10% of government spend for citizen-owned small companies. Roughly 78% now license cloud CRM, bookkeeping or productivity suites, and an additional 46% intend to migrate local file storage to SaaS within 18 months. Because SMEs rarely hire full-time IT staff, they favour subscription bundles that combine virtual helpdesk, endpoint security and compliance monitoring under a single invoice. Abu Dhabi’s Tajir license removes physical-office requirements across more than 1,000 activities, letting entrepreneurs launch online storefronts that immediately need payment gateways, order-management plugins and secure hosting. Vendors that can deploy templated storefronts, localized ERP modules and pay-as-you-grow managed services will capture rapid, low-friction revenue while building future cross-sell pipelines. The SME wave therefore serves as both a volume buffer and a sandbox for repeatable packaged IP, enriching overall profitability even though average deal value remains modest.

By End-User Vertical: Public spending anchors momentum

Government and public-sector bodies accounted for 21.50% revenue in 2024, a reflection of cabinet directives that digitize judicial services, land records, customs and social programs. Each initiative pairs sovereign-cloud tenancy with DevSecOps pipelines managed under continuous-compliance dashboards to satisfy personal-data and export-control statutes. Ministries increasingly demand outcome-based milestones-such as citizen-satisfaction scores or processing-time cuts-instead of labour-hour billing, nudging providers toward modular reference architectures that can be cloned across agencies. Healthcare and life sciences advance fastest at 17.40% CAGR as Emirates Health Services scales AI diagnostic algorithms, virtual nursing assistants and e-prescription exchanges, each of which requires HL7 mapping, image-store encryption and algorithm traceability. BFSI budgets remain sizable because 70% of GCC banks plan to shift to platform banking, embedded finance and hyper-personalized wealth tools, all of which rest on open-API frameworks and microservice gateways. Manufacturing picks up velocity thanks to Industry 4.0 lighthouse programs that integrate edge sensors, private 5G and cloud historians inside aluminium, steel and petrochemical complexes.

Retail, logistics, utilities and telecom together generate a long tail of high-volume, mid-complexity engagements suited to agile sprints and managed services. Supermarket chains prioritize computer-vision stock counts and loyalty analytics, logistics players adopt real-time fleet routing, and utilities deploy IoT-based grid optimization with digital-twin replicas. Telecom and media incumbents such as e and du are morphing into technology aggregators that resell hyperscale IaaS, private 5G slices and edge AI, positioning them simultaneously as partners and rivals to classic systems integrators. These motions keep the UAE IT services market fragmented yet dynamic, because each vertical’s roadmap spawns demand for specialized domain accelerators that smaller boutiques can still monetize.

By Delivery Model: Data regulation cements onshore preference

On-shore contracts formed the bulk of 2024 billings, underwritten by Federal Decree-Law No. 45-2021 on personal-data protection, which restricts offshore processing unless special permits exist. Ministries, financial regulators and critical-infrastructure operators must store sensitive classes inside UAE territory, steering demand to domestic data-center campuses run by G42, Moro Hub and Etisalat by e. Near-shore work-typically hosted in Bahrain, Oman or Qatar-has gained modest traction for non-regulated analytics, provided traffic stays within GCC data-residency rings. Offshore models remain useful for software development and non-identifiable test data, but buyers insist on code-escrow, geo-fencing and periodic audits, shrinking addressable volume for pure India-based time-and-material bids.

Because compliance reviews now pierce deep into subcontractor chains, prime vendors write multi-party data-processing addenda that flow down encryption, access-control and secrets-management obligations. Hybrid structures-local client engagement plus offshore delivery pods-are becoming the norm for commercial teams that must square cost optimization with statute obedience. Over time, as GCC nations align privacy codes, some sensitive workloads may gain regional-processing clearance, yet the onshore premium is unlikely to dissolve entirely, ensuring sustained revenue for UAE-hosted managed-service platforms. The policy environment therefore acts as a moat around the UAE IT services market, raising switching costs and tempering purely price-driven competition.

Geography Analysis

Dubai and Abu Dhabi account for roughly three-quarters of current contract value because they host most sovereign-cloud zones, hyperscale regions and free-zone headquarters. Dubai leverages its position as a global travel and finance node, using Expo City and DIFC roadmaps to pilot digital-identity wallets, tokenized securities and AI concierge services. Abu Dhabi, backed by deep sovereign wealth, prioritizes AI supercomputing, edge-to-core chip fabrication and cognitive-city infrastructure, illustrated by the USD 2.5 billion Aion Sentia project slated for 2027 completion.[3]Abu Dhabi Investment Office, “Aion Sentia Project Overview,” investinabudhabi.gov.ae Both emirates compete yet collaborate, creating a dual-hub model that concentrates highly skilled labour, investor attention and regulatory sandboxes, thus reinforcing their pull-on foreign systems integrators seeking regional headquarters.

The Northern Emirates-Sharjah, Ras Al Khaimah, Ajman, Fujairah and Umm Al Quwain-are entering the digital race through federal cloud mandates and spillover smart-city contracts. Sharjah rolled out an omni-channel citizen-services portal that requires SLA-based application-support, while Ras Al Khaimah’s RAK Digital Assets Oasis free zone is onboarding Web3 exchanges that opt for local blockchain audits and SOC-as-service subscriptions. Though deal sizes remain smaller than Dubai or Abu Dhabi, the growth slope is steeper because many entities are moving from paper-based workflows directly to AI-enabled mobile experiences. Vendors able to provision low-touch, template-driven cloud environments at competitive price points will capture first-mover status before regional competitors become entrenched.

The UAE’s geographic advantage also manifests in export revenue. Bilateral data-residency accords allow Emirati clouds to host workloads from Oman, Bahrain and occasionally Saudi entities awaiting local hyperscale launches. As a result, cross-border projects contribute an emerging revenue tier that partly insulates the UAE IT services market against domestic budget cycles. At the same time, rivalry with Saudi Arabia’s NEOM and Qatar’s smart-nation programs pushes Emirati providers to differentiate via faster compliance clearance, Arabic-first AI models and more mature fintech sandboxes. The feedback loop sharpens local capabilities, making UAE vendors credible bidders for pan-GCC mega deals and driving sustained geographic diversification.

Competitive Landscape

Competition remains moderately fragmented but is tightening as global giants lock equity alliances with domestic players. Microsoft invested USD 1.5 billion in G42 to build sovereign-cloud services, granting Azure workloads clearance for sensitive public-sector data while giving G42 access to proprietary foundation-model refinements. IBM entered a managed-security joint venture with Etisalat by e that bundles QRadar SIEM, 24×7 SOC and incident-response retainers purpose-built for zero-trust audits. Accenture scaled its Abu Dhabi Innovation Hub to 900 consultants specializing in data-mesh, responsible-AI playbooks and Gen-AI prompt engineering for Arabic dialects. Such moves reshape partner ecosystems, because domestic mid-tiers must either join alliance programs or become subcontractors on megadeals they once chased directly.

Consolidation accelerates. G42 folded Injazat, Inception and its cloud unit into the Core42 brand, creating a full-stack AI and cloud integrator with 8,000 staff and 15% domestic share. The purchase of CPX added 400 cybersecurity specialists, enabling cross-sell of managed-security contracts into every Core42 migration engagement.[4]G42, “Strategic Acquisition Announcement,” g42.ai Meanwhile, international firms eye bolt-on acquisitions in analytics boutiques, robotic-process-automation specialists and identity-management startups to round out zero-trust posture. Regulatory thresholds announced in March 2025 stipulate pre-clearance above AED 300 million sales or 40% share, but volumes are expected to rise, nudging the UAE IT services market toward a more concentrated profile over the forecast period.

Technology differentiation focuses squarely on AI value-chains. Vendors are embedding code copilots into DevOps, using synthetic data to boost model performance on dialectical Arabic and automating document-processing via large-language-model pipelines. Those capabilities translate into productivity gains that free up billable hours, allowing firms to reinvest in Emirati talent development and vertical IP accelerators. As telecom groups such as e and du target 40% of revenue from technology services, traditional integrators face co-opetition: partnering for last-mile implementation while contending against the operators’ own cloud and security arms. The result is an ecosystem where nimble choreography of alliances, IP ownership and compliance credibility determines share momentum more than sheer headcount.

United Arab Emirates IT Services Industry Leaders

Accenture plc

Microsoft Corporation

Amazon Web Services, Inc.

Injazat Data Systems LLC

Emirates Telecommunication Group Company PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cisco joined the Stargate UAE initiative alongside G42, OpenAI, Oracle, NVIDIA and SoftBank to build an AI data-center campus that will scale from 200 MW to 1 GW by 2026.

- May 2025: OpenAI agreed with Abu Dhabi entities to construct a 5-gigawatt compute complex, aligning with national AI self-sufficiency targets.

- March 2025: New merger-control thresholds (AED 300 million sales or 40% share) took effect, signaling stricter antitrust scrutiny.

- February 2025: G42 acquired CPX, adding 400 cybersecurity experts to strengthen AI value-chain protection.

United Arab Emirates IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| On-shore Services |

| Near-shore (GCC) Services |

| Offshore Services |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Delivery Model | On-shore Services |

| Near-shore (GCC) Services | |

| Offshore Services |

Key Questions Answered in the Report

What is the projected value of the United Arab Emirates IT services market in 2030?

The market is forecast to reach USD 37.69 billion by 2030, growing at a 13.24% CAGR.

Which service line currently holds the largest UAE IT services market share?

Cloud and platform services lead with 32.33% share in 2024.

How fast are managed security services growing in the UAE?

They are expanding at an 18.70% CAGR on the back of zero-trust mandates.

Why is onshore delivery favoured over offshore alternatives?

Federal Decree-Law No. 45-2021 enforces data-sovereignty rules that require sensitive workloads to stay within UAE borders.

Which vertical is the fastest-growing customer segment?

Healthcare and life sciences is advancing at a 17.40% CAGR as AI diagnostics and telehealth scale.

How are SMEs influencing future demand?

Government set-asides and simplified licensing enable SMEs to adopt cloud bundles, pushing SME spending to a 15.90% CAGR.

Page last updated on: