India IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

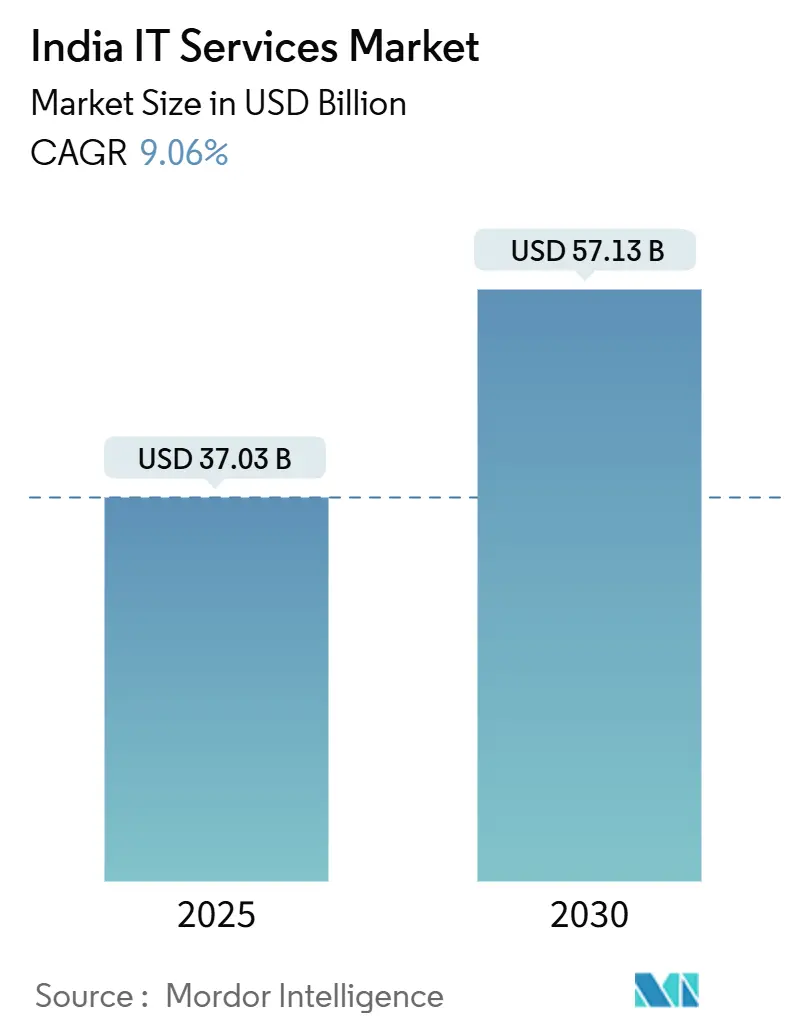

| Market Size (2025) | USD 37.03 Billion |

| Market Size (2030) | USD 57.13 Billion |

| Growth Rate (2025 - 2030) | 9.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India IT Services Market Analysis by Mordor Intelligence

The India IT Services market size stood at USD 37.03 billion in 2025 and is forecast to expand at a 9.06% CAGR to USD 57.13 billion by 2030. Demand is accelerating as enterprises channel more than 4% of revenue into technology modernization, outpacing global peers. Cloud-first projects, the rise of Global Capability Centers, and government digital-infrastructure spending collectively bolster the India IT Services market, even amid global economic uncertainty.[1]Inductus GCC, “GCC Industry Brief,” nasscom.in Cybersecurity, AI-led transformation, and hybrid delivery models are opening new value pools and sparking intense competition among service providers and emerging niche specialists. Structural headwinds—talent attrition, wage inflation, and evolving data-sovereignty mandates—are prompting firms to recalibrate pricing models and reskill workforces.

Key Report Takeaways

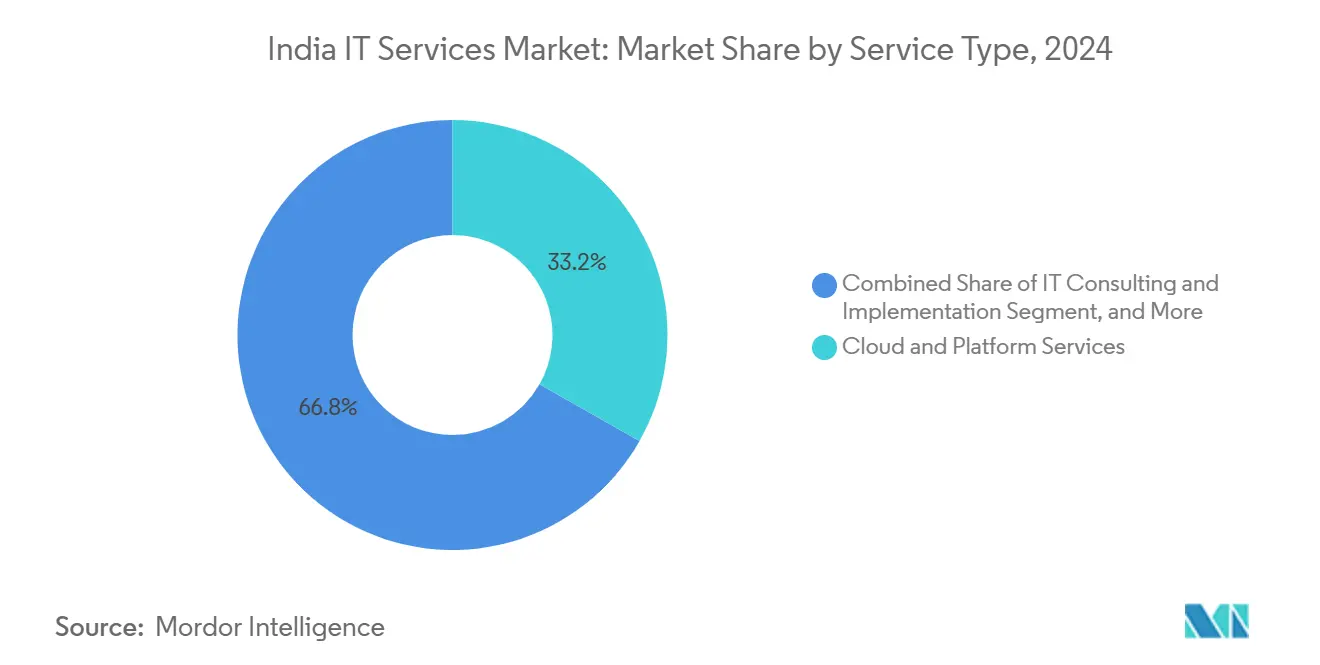

- By service type, Cloud and Platform Services led with 33.2% revenue share in 2024; Managed Security Services is projected to grow at a 10.8% CAGR through 2030.

- By enterprise size, Large Enterprises held 64.3% of the India IT Services market share in 2024, while SMEs are advancing at a 10.1% CAGR.

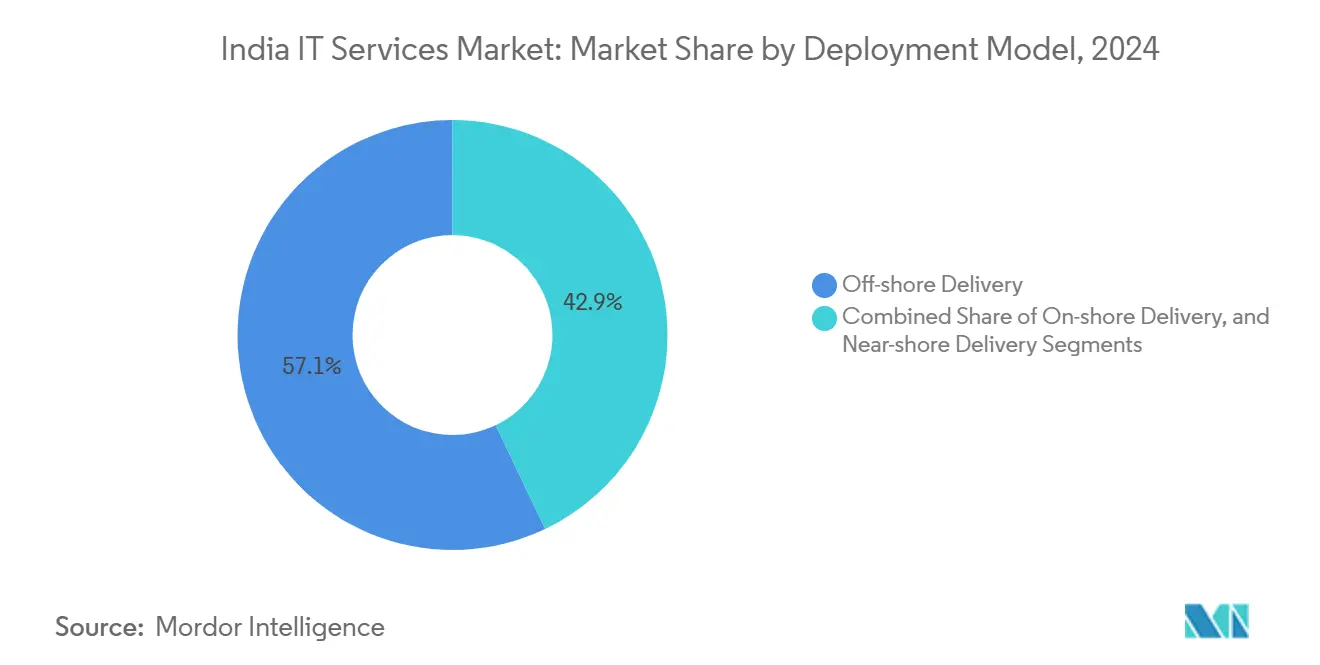

- By deployment model, Offshore Delivery accounted for a 57.1% share of the India IT Services market size in 2024; Nearshore Delivery is forecast to expand at an 11.7% CAGR to 2030.

- By end-user vertical, BFSI captured a 22.5% share in 2024, whereas Healthcare and Life-Sciences are set to climb at an 11.5% CAGR.

India IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated digital-transformation spend in BFSI and retail | +2.1% | Global; early gains in Mumbai, Bangalore, Chennai | Medium term (2-4 years) |

| Surge in public-cloud adoption and spending | +1.8% | Global | Medium term (2-4 years) |

| Government Digital India / Smart-Cities initiatives | +1.5% | National; early gains in tier-2 cities | Long term (≥ 4 years) |

| Rising demand for managed security services | +1.4% | Global | Short term (≤ 2 years) |

| Expansion of GCCs is driving high-value engineering work | +1.2% | Asia-Pacific core; spill-over to North America and the EU | Medium term (2-4 years) |

| Indigenous GenAI frameworks lowering TCO for SMEs | +1.0% | National; early gains in Hyderabad, Pune, Gurugram | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated digital-transformation spend in BFSI and retail

Banks are spearheading demand for India's IT Services market engagements as digital-banking maturity reached 59% in 2024, eclipsing global norms. Global financial institutions lifted tech budgets by 10% to USD 716 billion, while Indian lenders raised spending by 12.2% to USD 13.2 billion. Unified Payments Interface volumes are projected to touch USD 7 trillion by 2030, compounding the need for real-time payment-processing platforms. Retailers mirror this momentum, prioritizing omnichannel experiences that hinge on cloud scalability and AI-driven customer analytics. Cost savings of up to 30% from AI, blockchain, and RPA adoption in banking free budgets for new transformation projects.

Surge in public-cloud adoption and spending

Comprehensive cloud strategies now cover 78% of Indian enterprises, making cloud migration the linchpin of modernization road maps. The domestic cloud-services arena is set to post a 24% CAGR through 2028, fueled by platform-as-a-service uptake. Enterprise spend reached USD 15 billion in 2023 and is expected to quintuple its share of software budgets within a few years. Talent shortages plague 75% of adopters, intensifying demand for managed services and training programs. Strategic alliances, such as TCS and AWS, upskilling 25,000 professionals, embed India's IT Services market expertise into global cloud ecosystems.

Rising demand for managed security services

India’s cybersecurity segment hit USD 6.06 billion in 2023 and is advancing at 32% annually. BFSI and IT/ITeS together command more than half of the spending as cyber attacks rose 71% year on year. Generative-AI tools are sharpening threat-detection accuracy and cutting response time, enabling providers to differentiate on proactive defense. Skills shortages drive enterprises toward outsourced 24/7 monitoring models that guarantee compliance with stringent regulations. India IT Services market participants now package AI-driven security analytics, compliance automation, and IoT protection into subscription offerings that cater to both large enterprises and SMEs.

Government Digital India / Smart-Cities initiatives

Public-sector tech procurement has shifted decisively online, with GeM processing INR 2 trillion in transactions across 70,000 agencies. The India AI Mission earmarks INR 10,372 crore (USD 1.19 billion) for GPU infrastructure, creating an onshore demand surge for AI-enablement services.[2]PSU Watch, “India AI Mission GPU Procurement,” psuwatch.com Optical fiber investments exceeded USD 13 billion, widening broadband access in tier-2 clusters that now supply 6% of national data-center capacity. Smart-city programs catalyze projects in IoT-based surveillance and traffic management, opening local delivery opportunities for mid-tier providers. Preference for India-incorporated vendors in AI tenders underlines a policy tilt that secures domestic market share for compliant firms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global macro-economic uncertainty and IT-budget cuts | −1.8% | Global | Short term (≤ 2 years) |

| Talent attrition and wage inflation | −1.5% | National; early gains in Bangalore, Hyderabad, Chennai | Medium term (2-4 years) |

| Power-cost volatility for hyperscale data centers | −0.8% | National; early gains in Mumbai, Chennai, Bangalore | Medium term (2-4 years) |

| Emerging data-sovereignty clauses complicate delivery | −0.6% | Global; early gains in the EU, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global macro-economic uncertainty and IT-budget cuts

Revenue growth for the India IT Services market decelerated from 7.4% in 2022 to 6.1% in 2023 as clients deferred discretionary projects. Major firms responded with workforce rationalization; TCS announced a 2% headcount reduction and halted experienced-hire intake to save USD 300–400 million annually. Budget caution is most pronounced in communications and hi-tech segments pressed by weak demand. Yet analysts expect spending to rebound by late 2025, driven by the pent-up need for AI, cloud, and security solutions once macro risk subsides. Providers that reposition offerings around cost-efficiency and rapid ROI gain traction even under constrained budgets.

Talent attrition and wage inflation

Rising GCC salaries—15–20% above traditional rates—fuel attrition and lift median wages across the India IT Services industry. More than 150 new GCCs have been launched over 30 months, intensifying competition for cloud, AI, and security specialists. Fiscal 2025 salary increments are forecast at 4–8.5%, but niche skills in AI and cyber command outsized premiums. Entry-level hiring for legacy roles may contract 15–20%, while demand for advanced profiles rises 25–30% by 2025. Firms invest in reskilling programs and flexible work models to retain talent, but wage pressures persist as long as GCC expansion continues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Digital Acceleration

Cloud and Platform Services captured 33.2% of 2024 revenue, reaffirming their role as the cornerstone of enterprise modernization. This dominance translates into a USD 12.3 billion slice of the India IT Services market size in 2025. Managed Security Services, growing at a 10.8% CAGR, is rapidly closing the gap as cyber resilience becomes non-negotiable for regulated sectors. The India IT Services market share of traditional IT Outsourcing continues to erode under automation, yet consulting demand picks up as clients seek AI integration road maps.

Platform-native solutions reduce migration cycles by up to 40% and free budgets for innovation projects. Regulatory compliance mandates—from the Digital Personal Data Protection Act to sector-specific norms—spur governance-as-a-service offerings bundled with cloud and security. Providers that combine hyperscaler partnerships with industry templates are well placed to secure multi-year transformation deals. Conversely, standalone ITO contracts face pricing pressure as outcome-based models take hold.

By End-User Enterprise Size: SME Digitization Accelerates Growth

Large Enterprises drove 64.3% of 2024 spending, equal to USD 23.8 billion of the India IT Services market size. Their focus remains on multi-cloud orchestration, AI Centers of Excellence, and zero-trust security architectures. SMEs, however, are the fastest-growing cohort at 10.1% CAGR, scaling adoption through subscription-priced GenAI and low-code platforms.

Government incentives and preferential procurement policies for MSMEs tilt demand toward localized solution bundles. As cost barriers fall, SME projects increasingly mirror enterprise complexity, spanning predictive analytics and automated compliance reporting. Providers target this pool with templated offerings that balance affordability and rapid deployment, often delivered via partner ecosystems that combine financing, training, and managed services.

By Deployment Model: Nearshore Gains Momentum Amid Changing Preferences

Offshore Delivery retained 57.1% of 2024 revenue, underscoring India’s entrenched position in global sourcing networks. Yet Nearshore Delivery is riding an 11.7% CAGR wave as clients seek tighter collaboration and data-sovereignty assurance. Blended-shore contracts now stipulate up to 30% near-time-zone engagement for AI projects requiring daily iteration cycles.

Data-localization statutes in the EU, Australia, and parts of Asia prompt providers to expand regional centers that replicate offshore efficiencies while satisfying local oversight. Onshore Delivery remains indispensable in government, defense, and healthcare contracts demanding physical presence certifications. Firms such as TCS exhibit a balanced model, mixing on-, near-, and offshore capacity to mitigate geopolitical and regulatory risk.

By End-User Vertical: Healthcare Digitization Drives Sectoral Transformation

BFSI generated 22.5% of 2024 revenue on the back of digital-payments proliferation and open-banking adoption. The India IT Services market share of Healthcare and Life-Sciences, while smaller, is expanding quickly at 11.5% CAGR as telehealth, electronic health records, and AI-assisted diagnostics scale.

Manufacturers pursue Industry 4.0 road maps, pushing IoT and predictive-maintenance deployments toward 40–50% plant penetration by 2025. Public-sector smart-city initiatives boost demand for IoT integration, analytics platforms, and citizen-service apps. Telecom providers, motivated by 5G monetization, invest in network-API platforms that invite ecosystem innovation. Cross-vertical convergence around AI and cloud fosters reusable solution stacks that shorten go-to-market timelines for providers.

Geography Analysis

Metropolitan hubs—Bangalore, Hyderabad, Chennai, and Mumbai—continue to anchor 2025 delivery capacity, housing the bulk of the India IT Services market talent pool. These cities benefit from mature ecosystems, international connectivity, and policy support that sustain double-digit growth despite rising costs. Tier-2 and tier-3 centers such as Kochi, Mohali, and Jaipur, presently contributing 6% of national data-center capacity, are projected to absorb a larger share of growth as fiber and power infrastructure improve.[3]ET CIO, “Tier 2 Cities Becoming Digital Powerhouses,” cio.economictimes.indiatimes.com

Global revenue distribution remains North America-centric, but Europe’s appetite for AI-driven engineering services is climbing. Infosys’s EUR 450 million (USD 525.74 million) purchase of in-tech underscores the strategic imperative to deepen continental presence. Asia-Pacific opportunities surface in markets with rapid digitization agendas and favorable trade pacts, while data-sovereignty considerations compel providers to adopt region-specific compliance blueprints.

Competitive intensity varies by locale. In mature regions, incumbents guard share through long-term managed-services contracts and local delivery hubs. Emerging geographies invite challenger firms that leverage India’s cost-quality balance to capture first-mover advantage. Visa policies, tax incentives, and geopolitical alignments will remain decisive in shaping the overseas expansion paths of Indian providers.

Competitive Landscape

India's IT Services market competition is moderate-to-high, with top players leveraging scale, domain expertise, and AI investments to fend off GCCs and specialist challengers. TCS, Infosys, Wipro, and HCLTech collectively command a significant revenue share, yet face erosion risks as GCCs lure talent with higher pay and niche firms exploit agility advantages. Strategic acquisitions dominate growth playbooks—Infosys’s AUD 158 million (USD 102.40 million) Versent stake targets the Australian cloud segment, while HCLTech’s TIBCO pact adds integration depth.

Mid-tier companies like Persistent Systems have compounded revenue at a 28% CAGR by importing leadership talent and focusing on vertical IP. Partnership ecosystems with hyperscalers and chipmakers, exemplified by Nvidia alliances, accelerate go-to-market for AI solutions.[4]Business Standard, “Partnership with Nvidia,” business-standard.comCompliance credentials—ISO, SOC 2, sector-specific certifications—have evolved into critical differentiators when courting regulated clients.

White-space remains in edge-computing, AI-first managed services, and outcome-based pricing models. Firms capable of marrying domain consulting with platform engineering and managed operations stand to carve out a premium share. Consolidation is poised to continue as larger entities acquire domain specialists to plug capability gaps and expand geographic coverage.

India IT Services Industry Leaders

Tata Consultancy Services Ltd.

Infosys Ltd.

Wipro Ltd.

HCL Technologies Ltd.

Tech Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Infosys acquired a 75% stake in Telstra’s Versent Group for AUD 233.25 million (USD 158 million) to launch an AI-led cloud joint venture targeting Australia.

- August 2025: HCLTech entered an exclusive agreement with Cloud Software Group to bolster global TIBCO services, onboarding 400 specialists.

- July 2025: TCS disclosed a 12,200-employee reduction and a freeze on experienced hiring, aiming for USD 300–400 million in annual savings.

- June 2025: Tech Mahindra and Wipro joined the Aduna consortium to accelerate network-API adoption in telecom.

India IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| On-shore Delivery |

| Near-shore Delivery |

| Off-shore Delivery |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Model | On-shore Delivery |

| Near-shore Delivery | |

| Off-shore Delivery | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-user Verticals |

Key Questions Answered in the Report

What is the current value of the India IT Services market?

The market is valued at USD 37.03 billion in 2025 and is projected to reach USD 57.13 billion by 2030.

How fast is cloud adoption growing among Indian enterprises?

Cloud services revenue is advancing at a 24% CAGR through 2028 as 78% of organizations pursue comprehensive cloud strategies.

Which segment is expanding the quickest in IT services?

Managed Security Services is the fastest-growing service type, posting a 10.8% CAGR between 2025 and 2030.

Why are SMEs important to service providers?

SMEs are logging 10.1% CAGR in IT spend, driven by affordable GenAI frameworks and government digitization incentives.

How are talent challenges affecting providers?

GCC wage premiums and skill shortages push attrition higher, prompting IT firms to invest heavily in reskilling and flexible workforce models.

Page last updated on: