Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

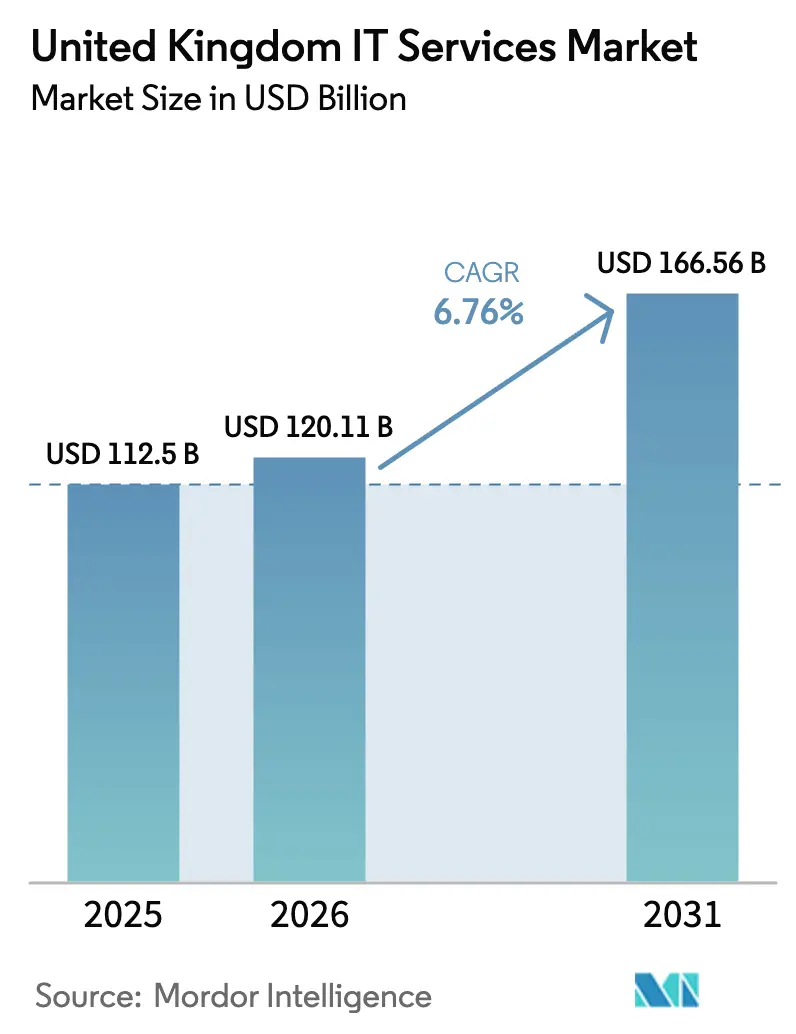

| Base Year Market Size (2025) | USD 112.5 Billion |

| Market Size (2026) | USD 120.11 Billion |

| Market Size (2031) | USD 166.56 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom IT Services Market Analysis by Mordor Intelligence

The UK IT services market size was valued at USD 112.5 billion in 2025 and estimated to grow from USD 120.11 billion in 2026 to reach USD 166.56 billion by 2031, at a CAGR of 6.76% during the forecast period (2026-2031). This trajectory underscores the resilience of the UK IT services market, powered by accelerating digital transformation in both public and private sectors, sustained public investment in AI infrastructure, and expanding compliance mandates in cybersecurity. Public-sector cloud frameworks, record generative-AI contract bookings, and growing regional tech hubs continue to stimulate demand, while wage inflation and macro-economic caution remain moderating influences. Global consulting firms are reinforcing their AI credentials to secure large multi-year deals, whereas mid-tier providers are targeting specialized niches such as managed security and Industry 4.0 integration. Nearshore delivery adoption is rising in response to tight local talent supply, yet the UK IT services market still favors on-premises proximity for high-regulation verticals such as finance and government.

Key Report Takeaways

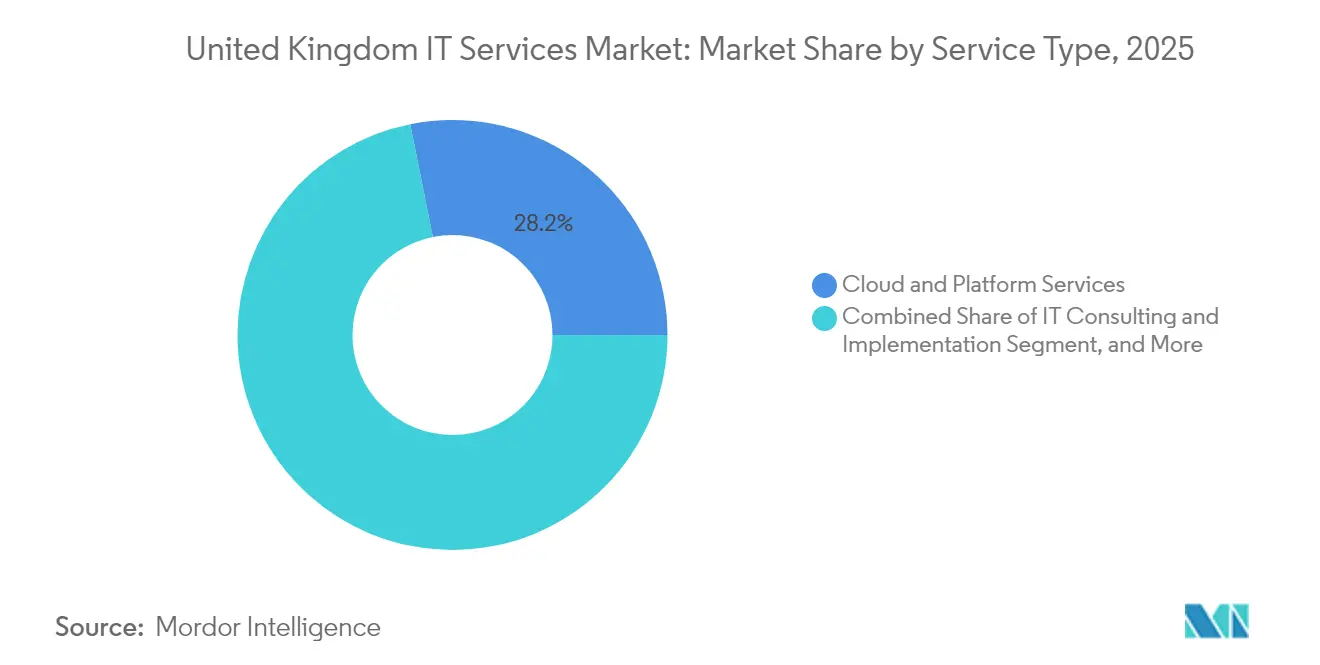

- By service type, cloud and platform services captured 28.15% of the UK IT services market share in 2025; managed security services are projected to expand at a 9.38% CAGR through 2031.

- By enterprise size, large enterprises held a 64.25% share of the UK IT services market in 2025, while the SME segment is projected to grow at a 8.98% CAGR to 2031.

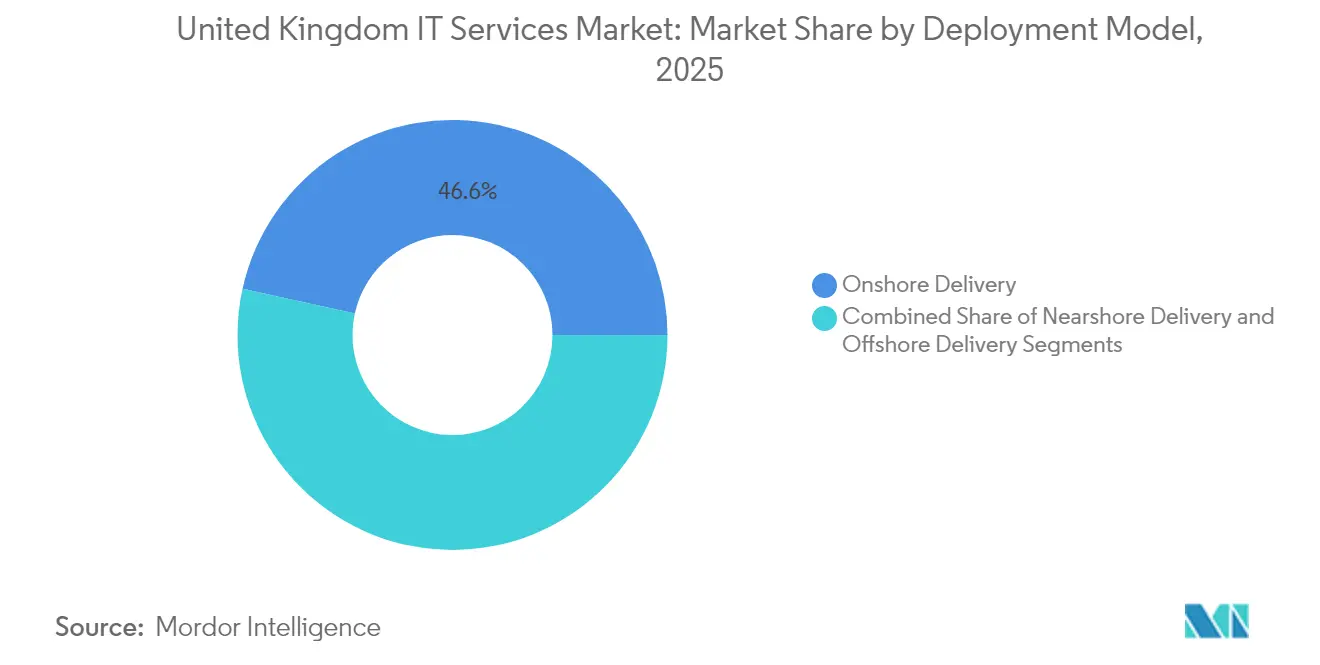

- By deployment model, onshore delivery accounted for 46.55% of the UK IT services market size in 2025, and nearshore delivery is advancing at a 9.51% CAGR through 2031.

- By end-user vertical, financial services led with 20.35% revenue share in 2025; healthcare and life sciences are forecast to expand at a 9.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-led Digital Transformation Wave | +2.1% | Global, with concentration in the London-Oxford-Cambridge triangle | Medium term (2-4 years) |

| Cloud-first Government Procurement Policies | +1.8% | National, with early gains in the Central Government departments | Short term (≤ 2 years) |

| Acute Cyber-threat Environment | +1.5% | Global, with particular focus on Financial Services and Critical Infrastructure | Short term (≤ 2 years) |

| Convergence of OT-IT in UK Manufacturing | +0.9% | National, concentrated in the West Midlands and Northern England | Medium term (2-4 years) |

| Rise of Green-IT Mandates (Sustainability Targets) | +0.6% | National, driven by government procurement requirements | Long term (≥ 4 years) |

| Brexit-Driven Regulatory Complexity | +0.4% | National, with spillover effects to EU operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-led Digital Transformation Wave

The United Kingdom now ranks as the world’s third-largest AI economy and is targeting annual productivity gains of 1.5% through AI deployment. [1]Department for Science, Innovation and Technology, “Prime Minister sets out blueprint to turbocharge AI,” GOV.UK Despite enthusiasm, only 16% of manufacturers report adequate AI knowledge, opening consultative opportunities for service providers. Public investment of USD 4 billion and USD 14 billion in private commitments form a durable pipeline for AI-centric engagements. Accenture alone secured USD 1.4 billion in generative-AI bookings during Q2 FY25, signaling robust enterprise appetite. Government-designated AI Growth Zones—beginning with Culham, Oxfordshire—will require extensive systems integration and cloud capacity. Together, these factors generate a sustained uplift in the UK IT services market.

Cloud-first Government Procurement Policies

The cloud-first mandate, highlighted by G-Cloud 14’s catalog of 46,000 services from 4,000 suppliers, is reshaping public-sector procurement. Framework savings of USD 2.3 billion since 2012 validate economic benefits and stimulate SME participation. The forthcoming USD 16 billion Technology Services 4 competition represents the largest single opportunity for vendors. Cloud uptake extends into strategic partnerships under the Digital and Technologies Sector Plan, blurring lines between procurement and innovation. Private-sector spillovers are visible as regulated industries replicate public-sector standards, reinforcing double-digit growth in platform services across the UK IT services market.

Acute Cyber-threat Environment

The Cyber Security and Resilience Bill expands oversight to 900-1,100 managed service providers and recognizes data centers as critical national infrastructure. With 58% of large financial firms reporting third-party attacks in 2024, cybersecurity spending is shifting from discretionary to mandatory. Industry growth of 13.2% suggests sustained demand amid imminent consolidation, as larger firms acquire niche specialists to satisfy regulatory scope. Alignment with EU-level rules such as DORA fosters continuous investment, propelling managed security services to become the fastest-growing category in the UK IT services market.

Convergence of OT-IT in UK Manufacturing

Valued at USD 9.5 billion in 2023, the domestic Industry 4.0 segment is forecast to hit USD 30.6 billion by 2030, demanding integration of operational and information technologies. The Made Smarter Programme’s USD 53 million fund speeds adoption, yet capability gaps drive manufacturers toward external partners for cloud migration and data analytics. West Midlands’ 5G coverage above 80% positions the region as a digitization hub demanding specialized services. Environmental compliance, including carbon border adjustment mechanisms, introduces sustainability analytics into OT-IT engagements. Such multi-disciplinary needs keep the UK IT services market on a steep growth curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Wage Inflation in Tech Talent Pool | -1.2% | National, with acute pressure in London and Southeast England | Short term (≤ 2 years) |

| Near-term Macroeconomic Slowdown | -0.8% | National, with regional variations in impact severity | Short term (≤ 2 years) |

| Data-Sovereignty Concerns with Offshore Delivery | -0.5% | National, affecting cross-border service delivery models | Medium term (2-4 years) |

| Fragmented SME Adoption Outside London | -0.3% | Regional, concentrated in Northern England, Wales, and Scotland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Wage Inflation in Tech Talent Pool

Tech salaries escalated 7-10% in 2024, with 76% of employers citing acute skill shortages. [2]Tech Nomads, “Salary Trends in the UK 2024,” technomads.io The April 2025 National Insurance hike from 13.8% to 15% inflate employer costs. Post-Brexit workforce attrition of 300,000 EU professionals leaves 600,000 vacancies that cost the economy USD 63 billion annually. Firms offset gaps by expanding nearshore and automation strategies, yet elevated labor costs compress margins and temper growth in the UK IT services market.

Near-term Macroeconomic Slowdown

Inflation uncertainty delays procurement decisions, as illustrated by Computacenter’s observation of elongated sales cycles. GenAI enthusiasm depresses other ICT transformation projects, causing real-terms contraction in 2023. Central government spending defends baseline demand, but private-sector caution prompts prioritization of ROI-proven initiatives. While AI’s measurable productivity gains help justify investments, macro sentiment remains a short-term drag on the UK IT services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Dominance Drives Security Surge

Cloud and platform services represented 28.15% of the UK IT services market share in 2025, a leadership position supported by G-Cloud 14’s widened catalog and ongoing migration of legacy estates to the public cloud. The UK IT services market size for this segment is projected to compound steadily on the back of the USD 16 billion Technology Services 4 framework. Simultaneously, managed security services are forecast to post a 9.38% CAGR to 2031, reflecting mandatory compliance under the Cyber Security and Resilience Bill. IT consulting remains resilient thanks to enterprise AI programs, while IT outsourcing and BPO experience balanced growth amid automation.

Cross-pollination between cloud migration and security hardening underpins provider revenue expansion. As agencies replace on-premise systems, bundled managed-security contracts accompany platform deals, magnifying wallet share. NHS tenders worth USD 1.4 billion illustrate how sector-specific frameworks pull along ecosystem suppliers. The UK IT services market, therefore, rewards vendors that combine hyperscale know-how with zero-trust architectures.

By End-User Enterprise Size: SME Acceleration Challenges Large-Enterprise Dominance

Large enterprises controlled 64.25% of the UK IT services market size in 2025, leveraging substantial budgets for multi-cloud rollouts, generative-AI pilots, and regulatory modernization. Despite dominance, their growth rate moderates as transformation roadmaps mature. In contrast, the SME cohort is projected to expand at a 8.98% CAGR to 2031, propelled by the SME Digital Adoption Taskforce’s 10-step action plan. UK IT services market share among SMEs remains modest, yet the economic value potential—USD 78.1 billion in AI-enabled productivity gains—creates a fertile addressable base.

Service models must adjust to shorter sales cycles and outcome-based pricing preferred by smaller firms. Regional AI innovation hubs, tax credits, and cloud marketplaces lower entry barriers, allowing providers to develop repeatable packages. Accordingly, the UK IT services market is witnessing a rise in subscription-oriented solutions tailored to micro-enterprises outside London.

By Deployment Model: Nearshore Momentum Challenges Onshore Preference

Onshore delivery captured 46.55% of the UK IT services market share in 2025 as clients prioritized data residency and close collaboration. However, wage inflation and talent scarcity push enterprises toward nearshore centers in Eastern Europe, projected to clock a 9.51% CAGR by 2031. The UK IT services market size for nearshore engagements will rise as hybrid models blend local consulting with overseas agile squads. Offshore delivery remains relevant for commodity tasks, but heightened compliance obligations cap its velocity.

Providers refine governance structures to coordinate cross-border delivery without breaching UK GDPR. Adoption of generative-AI coding assistants accelerates productivity, yet firms must navigate regulatory clarity on AI accountability, reinforcing demand for UK-based oversight.

By End-User Vertical: Healthcare Surge Challenges Financial-Services Leadership

Financial services held 20.35% of the UK IT services market size in 2025, anchored by strict regulatory imperatives and cyber-resilience mandates. Operational resilience and DORA compliance keep spending elevated, but growth is leveling off as core modernization programs mature. Healthcare and life sciences are predicted to grow 9.44% CAGR through 2031, buoyed by NHS England’s USD 1.4 billion digital framework expansion. The UK IT services market share for healthcare is set to climb as electronic-patient-record upgrades and AI-driven diagnostics roll out nationwide.

Manufacturing continues steady uptake thanks to Industry 4.0 incentives, while government agencies sustain cloud-migration momentum through large procurement vehicles. Retail, telecom, and energy verticals focus on customer experience and smart-grid projects, creating balanced opportunity lanes across the UK IT services market.

Geography Analysis

Regional clustering defines growth dynamics within the UK IT services market. London commands the highest digital sector GVA at USD 9,083 per capita, reflecting the concentration of venture funding and headquarters functions. The “golden triangle” of London, Oxford, and Cambridge attracts a disproportionate share of AI investment, risking divergence from levelling-up goals.

Government intervention via AI Growth Zones aims to seed large-scale data-center campuses outside traditional hubs, beginning with Culham, Oxfordshire. Simultaneously, tax reliefs and digital-skills funds target devolved administrations to correct labor imbalances that leave 10 million workers without essential digital capabilities.

Regional opportunities manifest in targeted cloud and managed-services packages for SMEs reluctant to adopt AI. Economic-impact studies suggest potential uplifts of USD 4.6 billion for West Yorkshire, USD 2.8 billion for Liverpool City Region, and USD 2.4 billion for Cardiff through AI integration. Such figures demonstrate geographically distributed upside for the UK IT services market when infrastructure and skills converge.

Competitive Landscape

Competition within the UK IT services market is intense but moderately fragmented. Accenture illustrates first-mover advantage in AI, leading with USD 1.4 billion in generative-AI bookings during Q2 FY25. [4]Accenture Plc, “8-K Material Event,” last10k.com By comparison, Indian majors TCS and Infosys trail significantly in project volume. M&A activity remains brisk: IBM’s acquisition of Advanced Computer Software Group’s modernization assets adds hybrid-cloud capability and exemplifies ecosystem consolidation.

White-space segments such as SME digital enablement and regional sustainability consulting entice emerging specialists. Meanwhile, compliance-driven niches in cybersecurity and AI assurance generate demand for boutique expertise capable of navigating the evolving regulatory landscape. Large framework wins, including NHS England’s USD 440 million cloud-service contract awarded to Softcat, underscore the importance of outcome-based and consumption pricing.

Providers differentiating on cloud-native delivery, AI accelerators, and zero-trust architectures will improve wallet share. The UK IT services market, therefore, favors firms capable of combining global scale with sector-specific depth, while mid-market players carve value in specialized domains.

United Kingdom IT Services Industry Leaders

Accenture plc

IBM UK Ltd.

Capgemini SE

Tata Consultancy Services (TCS) UK

Cognizant Technology Solutions UK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Accenture reported Q2 FY25 revenue of USD 16.66 billion and secured USD 1.4 billion in generative-AI bookings.

- March 2025: NHS England awarded Softcat a USD 440 million cloud-service contract for five years.

- February 2025: The UK government opened applications for AI Growth Zones, starting with Culham, Oxfordshire.

- January 2025: The Government released the AI Opportunities Action Plan, securing USD 14 billion in private investment pledges.

United Kingdom IT Services Market Report Scope

IT services allow organizations to access the technical tools and information they need to carry out their daily operations and duties. These services are frequently managed by teams with experience in IT or computer science for enterprises across a wide range of industries. Numerous IT services can assist firms and aid their smooth and efficient operation. Many of these services enable employees to interface with technology that helps them perform their daily tasks or communicate with coworkers.

The UK IT services market is segmented by type (IT outsourcing, IT consulting & implementation, and business process) and end user (IT and telecommunication, government, BFSI, energy & utilities, consumer goods & retail, and other end users).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Deployment Model

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

By End-user Vertical

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery | |

| By End-user Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-user Verticals |

Key Questions Answered in the Report

What is the projected value of the UK IT services market in 2031?

The market is expected to reach USD 166.56 billion by 2031, reflecting a 6.76% CAGR.

Which service category is growing fastest?

Managed security services are projected to expand at a 9.38% CAGR through 2031 as compliance mandates tighten.

How will nearshore delivery models evolve post-Brexit?

Nearshore engagements to Eastern Europe are forecast to rise at a 9.51% CAGR as firms offset domestic talent shortages while maintaining time-zone alignment.

Where do SMEs stand on digital adoption?

Although SMEs currently lag, government programs aim to unlock USD 78.1 billion in productivity gains by 2035 through accelerated AI and cloud uptake.

Which region outside London shows the highest growth potential?

West Yorkshire could generate USD 4.6 billion in economic uplift from AI adoption, supported by emerging AI innovation hubs and regional skills funds.

What factors most influence vendor selection today?

Clients increasingly prioritize demonstrated AI capability, strong cyber-security credentials, and the ability to deliver hybrid onshore-nearshore models compliant with UK GDPR.

Page last updated on: