Canada Location-Based Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

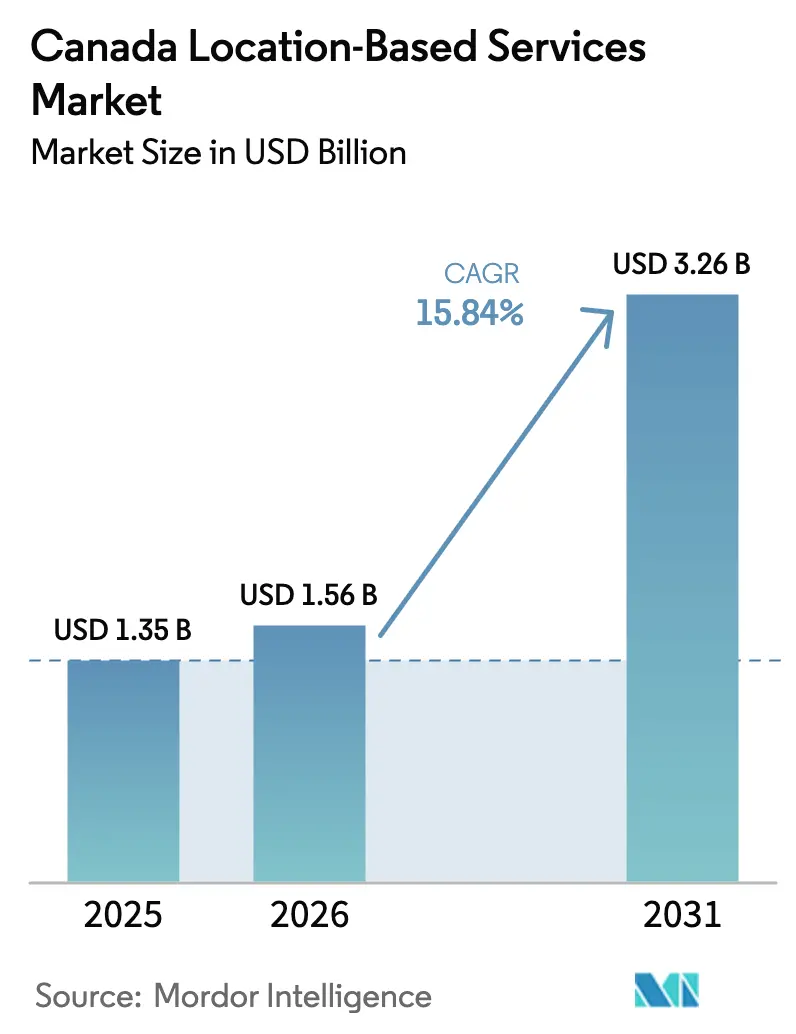

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.56 Billion |

| Market Size (2031) | USD 3.26 Billion |

| Growth Rate (2026 - 2031) | 15.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Location-Based Services Market Analysis by Mordor Intelligence

The Canada Location-Based Services Market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.56 billion in 2026 to reach USD 3.26 billion by 2031, at a CAGR of 15.84% during the forecast period (2026-2031).

Growth rests on sustained network capital expenditure by the country’s three national carriers, rapid smartphone adoption that lifts mobile data consumption, and public-sector investments in smart-city infrastructure. Indigenous data sovereignty frameworks—especially OCAP principles—shape solution design, while the delay in federal privacy reform has postponed tighter compliance costs yet heightened uncertainty. Hardware supply-chain pressures continue to elevate component prices, but they also spur service-centric business models that better absorb volatility. Competitive intensity is moderate as telcos safeguard core connectivity revenues and specialist vendors expand through vertical alliances, leaving ample opportunity for niche innovators in precision agriculture, indoor positioning, and remote healthcare applications.

Key Report Takeaways

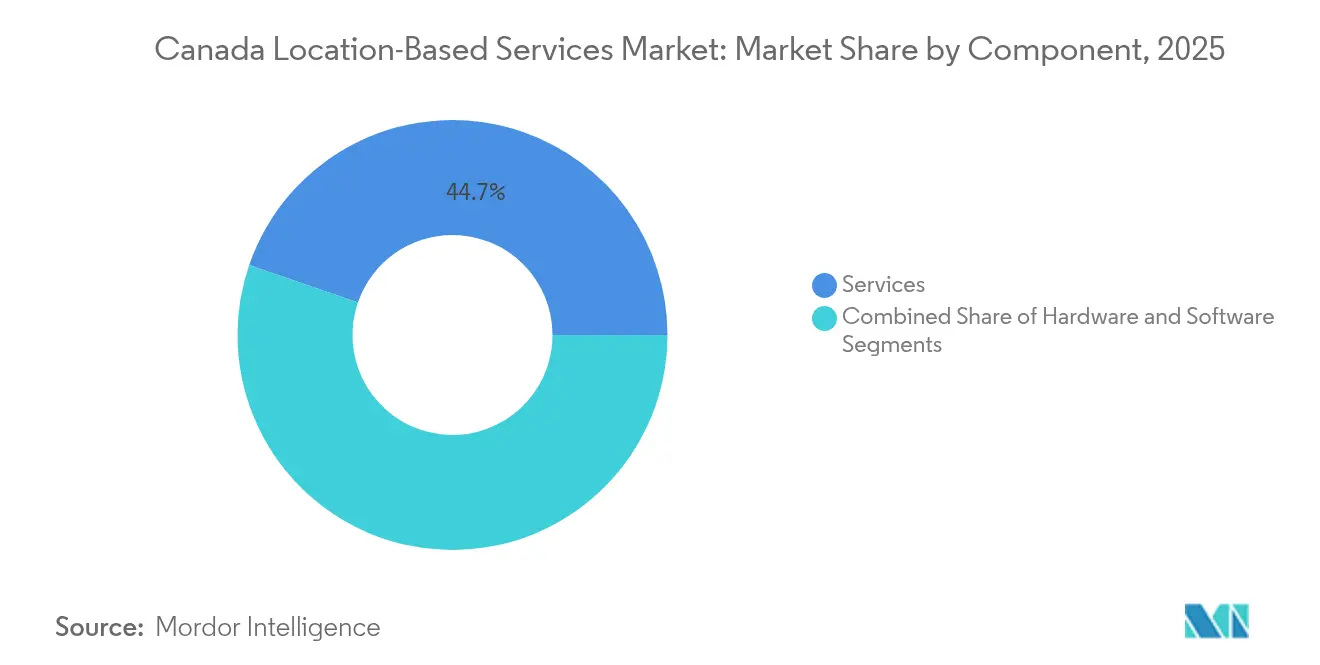

- By component, services held 44.73% of the location-based services market share in 2025; hardware is forecast to expand at a 10.12% CAGR to 2031.

- By location, outdoor deployments commanded a 62.95% share of the location-based services market size in 2025, and indoor positioning is advancing at a 11.62% CAGR through 2031.

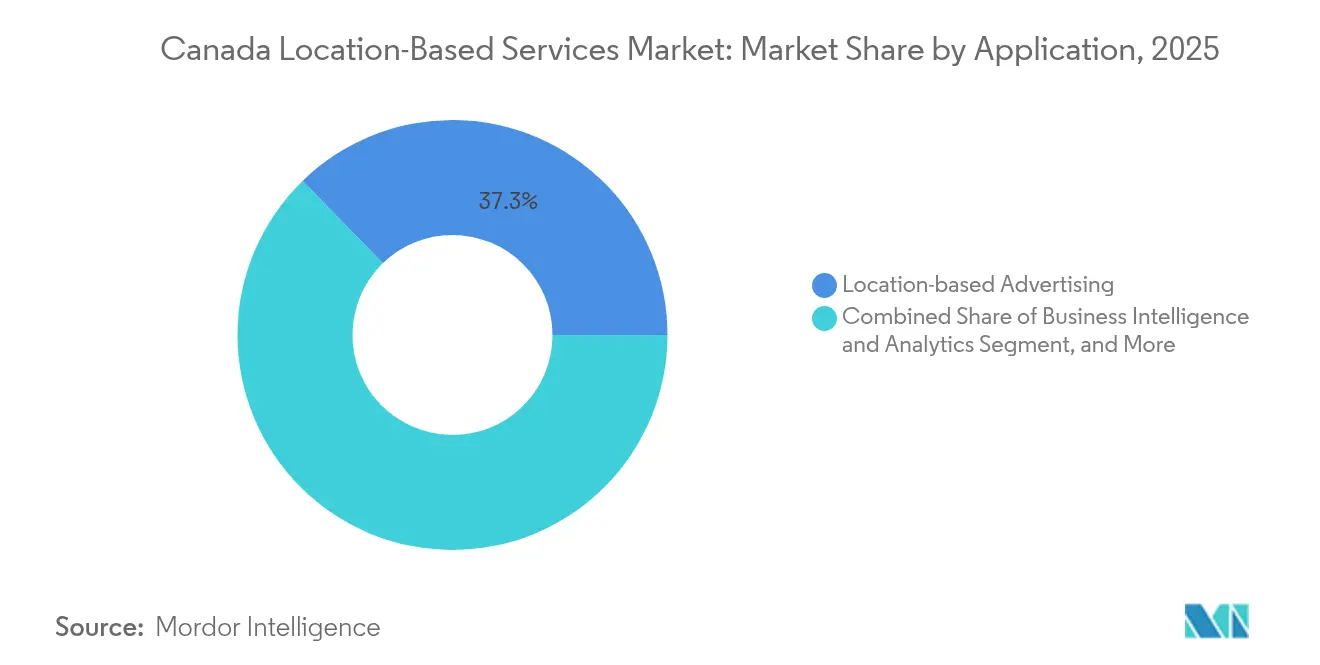

- By application, location-based advertising led with 37.28% of revenue in 2025, while social networking and entertainment applications are projected to grow at a 13.08% CAGR to 2031.

- By end-user industry, transportation and logistics accounted for 40.35% of the location-based services market size in 2025, and healthcare is progressing at a 12.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Canada includes both locally based firms and those operating across multiple regions. The market landscape in the global location based services industry research shows how these players are arranged internationally.

Canada Location-Based Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smartphone and cheap-data penetration | +3.2% | National, with urban concentration in Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| IoT uptake in transportation and logistics | +2.8% | National, with early gains in Alberta agriculture, Ontario manufacturing | Medium term (2-4 years) |

| Smart-city and public-safety mandates | +2.1% | Provincial leadership in BC, Ontario, Quebec municipalities | Medium term (2-4 years) |

| Indoor positioning tech (BLE/UWB) rollout | +1.9% | Urban centers, healthcare facilities, retail complexes | Long term (≥ 4 years) |

| Indigenous data-sovereignty push | +1.5% | Northern territories, First Nations lands, rural communities | Long term (≥ 4 years) |

| Precision-agriculture geo-fencing demand | +1.3% | Prairie provinces, agricultural regions across Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone and Cheap-Data Penetration

Mobile revenue reached CAD 59.6 billion in 2023, with retail data up 6.6%, a trajectory that underpins most consumer-facing location applications [1]Canadian Radio-Television and Telecommunications Commission, “Communications Market Report 2025,” crtc.gc.ca. Subscriber usage rose 21.3% year on year, translating into richer contextual datasets that ad-tech platforms monetize. Carrier bundles that blend connectivity with value-added location analytics lift average revenue per user and deepen customer retention. Rogers’ satellite-to-mobile pilot, already covering 5.4 million km², further enlarges the addressable base in previously dark zones. The resulting network breadth allows emergency text-to-911 and asset-tracking services to flourish where traditional towers were never economically viable.

IoT Uptake in Transportation and Logistics

Fleet managers adopt telematics to mitigate rising fuel and maintenance costs. TELUS Farm Fuel Management Solution pairs cellular IoT hubs with sensor probes so growers can locate tanks and schedule refills in real time [2]North Star Systems, “TELUS Farm Fuel Management Solution,” northstarsystems.ca. Geotab’s mixed-fleet module now integrates electric vans and heavy trucks, letting dispatchers benchmark utilization across Rivian, Volkswagen, and legacy assets. In agriculture, variable-rate seeding based on GNSS feedback reduces fertilizer waste across 160 million acres of Canadian cropland. Supply-chain chip shortages have doubled NFC lead times, but recurring software fees shield IoT platform vendors from hardware margin swings.

Smart-City and Public-Safety Mandates

Municipalities view traffic analytics as a lever to trim congestion and emissions. Edmonton’s Smart Roads project already layers sensor data onto adaptive signal cycles, improving corridor travel times. Toronto’s 5G-enabled cameras alert operators to blocked intersections, complementing pedestrian flow metrics gathered from curbside small cells. Standardized permit fees—USD 2,000 per smart-pole plus USD 250 annual upkeep—give cities predictable cost recovery. Such open data policies attract app developers that repurpose feeds for micromobility routing and accessibility mapping, reinforcing the location-based services market ecosystem.

Indoor Positioning Tech Rollout (BLE/UWB)

Mapsted’s software-only engine maps RF fingerprints across 8 million m² of Canadian real estate without extra beacons, lowering retrofit hurdles. Hospitals still favor beacon kits for sub-3 m accuracy; one Montreal facility mounted 1,200 BLE nodes over 60,000 m² and cut lost-equipment spend by digitizing asset locations. Apple’s second-generation U2 chip, fabricated on 7 nm tech, boosts UWB range and throughput, a leap that phone OEMs can exploit for centimeter-level indoor navigation. Shipments of UWB radios are on a path to 7.5 billion units by 2025, pushing venue owners to future-proof physical spaces with multi-protocol networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent privacy acts (PIPEDA, C-27) | -2.4% | National, with Quebec leading provincial regulations | Short term (≤ 2 years) |

| Indoor multipath accuracy limits | -1.8% | Urban centers, dense building environments | Medium term (2-4 years) |

| Sparse-north cartography cost burden | -1.3% | Northern territories, remote regions | Long term (≥ 4 years) |

| Carrier-billing rule changes | -0.9% | National, affecting all telecommunications providers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Privacy Acts (PIPEDA, C-27)

Bill C-27 remains in legislative limbo, yet its draft clauses on automated decision-making already influence product roadmaps. The Office of the Privacy Commissioner’s “No-Go Zones” explicitly bars location profiling that could enable discrimination, compelling providers to embed differential privacy and on-device processing. Quebec’s anonymization rule forces firms to document re-identification risk, an overhead that weighs more heavily on startups than on telcos with in-house compliance teams. Some vendors now market sovereign-cloud instances hosted within provincial borders to reassure public-sector buyers. Although compliance raises costs, vendors that master privacy-by-design gain a competitive moat as enterprises seek turnkey solutions.

Indoor Multipath Accuracy Limits

Radio reflections inside steel-reinforced buildings still hamper sub-meter precision. Controlled trials in Canadian emergency wards report a 66 cm mean deviation using BLE trilateration, a gap unacceptable for clinical asset tracking, where infusion pumps must be found within seconds. Advanced algorithms that harness non-line-of-sight paths deliver gains but demand high-density antennas and intensive calibration. The capital cost to blanket a 50,000 m² mall can exceed USD 250,000 when factoring in beacon hardware and annual battery swaps. Accuracy constraints, therefore, limit uptake in safety-critical scenarios and temper the overall growth of the location-based services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Anchor Adoption as Hardware Volatility Persists

Services held 44.73% of 2025 revenue, benefiting from predictable subscription contracts and outsized demand for integration expertise. Falling sensor prices narrow the total cost of ownership, yet chip shortages have doubled delivery times for NFC controllers and pushed some SKUs to 2,100% price hikes. Platform vendors insulate clients from these shocks by offering device-agnostic location stacks delivered via managed-service models. Hardware innovators leverage advanced foundry nodes; Apple’s 7 nm UWB die sets a benchmark that mid-tier IC houses must match to stay relevant. Software upgrades spread AI features that enrich context, such as Fraser Health’s digital-twin model that re-creates regional patient flows and guides resource allocation. With USD 100,000–200,000 required for a single 5G macro cell, enterprises prefer opex-driven service contracts, reinforcing the dominance of this component within the location-based services market.

Rising compliance spending also favors service providers able to certify privacy workflows. Many SMEs outsource data-retention audits and consent management, further baking services revenue into long-term operating budgets. Consequently, the location-based services market size for services is forecast to climb from USD 699.12 million in 2026 to USD 1.13 billion by 2031, translating into a 9.98% CAGR.

By Location: Indoor Breakout Accelerates as Use-Cases Mature

Outdoor deployments accounted for 62.95% of 2025 spending thanks to satellite and cellular coverage that now spans almost the entire populated landmass. Rogers’ satellite-to-mobile beta adds 2.5× more footprint than traditional towers, widening the public-safety and asset-tracking opportunity. Indoor positioning, however, registers the quickest climb at a 11.62% CAGR. Hospitals, airports, and retail chains pilot BLE beacons that knit wayfinding, occupancy analytics, and logistics into unified dashboards. The location-based services market share for indoor solutions is projected to surge from 37.05% in 2025 to close to parity with outdoor by 2031.

Software-only approaches lower capital barriers. Mapsted’s RF fingerprinting eliminates beacon hardware, while TDK’s geomagnetic SDK turns existing smartphone sensors into navigation beacons. Despite accuracy headwinds from multipath, emergent multi-modal fusion—combining UWB, BLE, Wi-Fi RTT, and visual odometry—promises sub-30 cm precision in dense venues. As retailers shift to phygital models that blur online and in-store journeys, footfall analytics teams increasingly rely on indoor heatmaps to optimize merchandising.

By Application: Entertainment and Social Networking Redefine Growth

Location-based advertising captured 37.28% of 2025 value, buoyed by Google Services’ USD 76.5 billion quarterly haul. Privacy shifts that limit third-party cookies pivot ad spend toward first-party location signals, keeping revenue robust. Social networking and entertainment apps are forecast to outpace advertising with a 13.08% CAGR, driven by augmented-reality games and immersive media that hinge on centimeter-level positioning. Niantic’s accelerated coordinate encoding shrinks world-scale AR map generation from hours to minutes, unlocking event-based campaigns that overlay digital quests onto real streets.

Mapping and navigation remain essential, but now emphasize live context. HERE Technologies and AWS committed USD 1 billion to stream HD maps for autonomous mobility, opening APIs that developers can embed into business-intelligence dashboards. Enterprise analytics increasingly rely on geofencing to align staffing with local demand or to time restocking cycles. Patent filings from Meta, Samsung, and Apple point to gesture-aware indicators and metaverse locators that will further blur physical-digital boundaries, broadening the application canvas inside the location-based services market.

By End-User Industry: Healthcare Outstrips Transport on Telemonitoring Boom

Transportation and logistics retained 40.35% of 2025 revenue as fleets adopted mixed-asset telematics and farmers optimized inputs across 160 million acres. Geotab’s OEM alliances with Volkswagen and Rivian facilitate standardized diagnostics, cutting maintenance downtime. The location-based services market size embedded in transport will still grow steadily but cede share to healthcare, which posts a 12.08% CAGR. Toronto Grace Health Centre already monitors 16,000 chronic-care patients remotely and plans to double coverage by 2026, leveraging GNSS tags and cellular gateways for continuous vitals streaming.

Government verticals accelerate through smart-city rollouts, while BFSI and hospitality deploy indoor positioning to sharpen customer engagement. Precision AI’s drone-sprayer reduces herbicide cost to USD 2.85 per acre, showing agriculture’s appetite for spatial analytics. Manufacturing plants adopt real-time locating systems to orchestrate just-in-time workflows, and public utilities layer asset maps onto outage-management systems to cut restoration times.

Geography Analysis

Canada’s vast 5.4 million km² landmass yields a dual market profile: dense southern corridors exhibit urban use-case saturation, while sparsely populated northwestern regions present connectivity white spaces. Carrier capex commitments—TELUS at CAD 70 billion through 2029 and Rogers at CAD 45 billion since inception—fuel a backbone that supports high-precision geolocation across provinces. Quebec sets the tone for privacy with its 2024 anonymization rules that ripple into neighboring jurisdictions. Ontario’s draft cybersecurity bill layers additional obligations on public bodies, likely prompting harmonization talks. Western provinces leverage LoRa and private-LTE networks for agriculture, while Atlantic Canada pilots maritime asset tracking on hybrid satellite-cellular links.

Indigenous territories, where only 18% have standard cellular reach, now receive attention as Rogers’ direct-to-device service extends text coverage nationwide. OCAP data principles require solution vendors to secure local consent for positional archives, fundamentally influencing architecture design. Remote healthcare programs collaborate with tribal councils to integrate geo-fencing alerts that respect cultural protocols. Northern resource projects, from hydroelectric dams to critical-mineral mines, demand ruggedized GNSS and UWB tags to monitor worker safety in extreme environments, injecting fresh demand into the location-based services market.

Urban leadership centers on Toronto, Vancouver, Montreal, and the Waterloo tech cluster. Municipal RFPs increasingly stipulate open-data access, spurring SMEs to build micro-services on traffic APIs. Startups capitalize on academic-industry links, with Waterloo turning out RF engineers who fuel indoor-mapping breakthroughs. Meanwhile, Saskatchewan farmers adopt satellite NDVI imagery to optimize crop inputs, illustrating how rural throughput upgrades unlock high-value analytics.

Mordor Intelligence tracks the location based services market across other major regions such as Middle East and Africa, with additional country-level coverage spanning United States, Brazil, United Arab Emirates, Nigeria, Spain, Italy, and South Korea, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Canada’s location-based services industry comprises a triad of dominant carriers and a constellation of specialist vendors. Rogers, TELUS, and Bell collectively spent more than CAD 120 billion on networks over the past decade, securing latent advantages in spectrum and fiber access. They defend their footprint by bundling device management, edge compute, and privacy consulting. Partnerships amplify reach: Cisco and TELUS target 1.5 million connected vehicles through a 5G mobility platform, while Rogers taps Ericsson for 5G-Advanced features that cement latency leadership.

Verticalmergers specialists drive differentiation. Mapsted delivers hardware-free indoor maps to malls, Jibestream maintains hospital and airport wayfinding suites, and Descartes Systems optimizes last-mile routing for cross-border freight. Patent activity is brisk: Meta’s UWB physical layer header now supports 124.8 Mb/s, Apple’s context-aware AR cues improve user orientation, and Google’s map-aided inertial odometry reduces battery drain during visual positioning. Investors notice: Battery Ventures acquired TrueContext to consolidate mobile field-service workflows, signaling a new phase of merger and acquisitions that could compress fragmentation.

White-space niches emerge in sovereign-cloud location analytics and agricultural drone mapping, where regulatory hurdles and domain complexity limit new entrants. AI overlays become table stakes as Bell builds a 500 MW sovereign AI fabric, offering on-shore inference for privacy-sensitive geodata. Overall, competition tilts toward collaboration: telcos lease APIs, chipmakers release reference designs, and software vendors bundle datasets, driving a layered ecosystem rather than a winner-takes-all race.

Canada Location-Based Services Industry Leaders

Cisco Systems Inc.

IBM Corporation

Ericsson Inc.

Apple Inc.

Esri Canada Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Rogers Communications launched a satellite-to-mobile text service covering 5.4 million km², offered as a free beta with text-to-911 support in partnership with SpaceX and Lynk Global.

- June 2025: TELUS pledged CAD 70 billion investment through 2029 to expand PureFibre and open two Sovereign AI Factories, strengthening rural and Indigenous connectivity.

- June 2025: Rogers deployed Ericsson 5G-Advanced features, the first Canadian rollout of the new network release.

- May 2025: Bell introduced Bell AI Fabric, a 500 MW hydro-powered compute project developed with Groq to scale domestic AI workloads.

- March 2025: Terrestar Solutions and Monogoto announced a hybrid cellular-satellite IoT service to improve national coverage.

Canada Location-Based Services Market Report Scope

Location-based services (LBSs) are computer or mobile applications that provide information based on the location of the device and the user, primarily through mobile portable devices, such as smartphones and mobile networks. The precision of the location services primarily depends on the hardware and software used in the mobile communication system, along with the positioning server.

Canada's location-based services market is segmented by component (hardware, software, and service), location (indoor and outdoor), application (mapping and navigation, business intelligence and analytics, location-based advertising, social networking and entertainment, and other applications), and end-user (transportation and logistics, it and telecom, healthcare, government, BFSI, hospitality, manufacturing, and other end-users).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Indoor |

| Outdoor |

| Mapping and Navigation |

| Business Intelligence and Analytics |

| Location-based Advertising |

| Social Networking and Entertainment |

| Other Applications |

| Transportation and Logistics |

| IT and Telecom |

| Healthcare |

| Government |

| BFSI |

| Hospitality |

| Manufacturing |

| Other End-Users |

| By Component | Hardware |

| Software | |

| Services | |

| By Location | Indoor |

| Outdoor | |

| By Application | Mapping and Navigation |

| Business Intelligence and Analytics | |

| Location-based Advertising | |

| Social Networking and Entertainment | |

| Other Applications | |

| By End-User Industry | Transportation and Logistics |

| IT and Telecom | |

| Healthcare | |

| Government | |

| BFSI | |

| Hospitality | |

| Manufacturing | |

| Other End-Users |

Key Questions Answered in the Report

What is the current value of Canada’s location-based services market?

The location-based services market size in Canada is USD 1.56 billion in 2026, with a forecast to more than double to USD 3.26 billion by 2031.

Which segment grows the fastest within the Canadian market?

Indoor positioning registers the highest growth, advancing at a 11.62% CAGR as hospitals, malls, and airports adopt BLE, UWB, and sensor-fusion solutions.

How does Indigenous data sovereignty influence solution design?

OCAP principles require vendors to secure community consent for geodata collection and storage, leading to privacy-by-design architectures and localized cloud deployments.

Why are services more dominant than hardware sales?

Service contracts shield buyers from chip shortages and large upfront 5G infrastructure outlays, making recurring integration and analytics offerings more attractive.

What regulation poses the greatest near-term risk?

The combination of PIPEDA and the stalled Bill C-27 creates uncertainty and adds compliance costs, curbing aggressive data-monetization models.

Which end-user industry is expected to outpace others by 2031?

Healthcare is projected to grow at a 12.08% CAGR, driven by remote patient monitoring and hospital asset-tracking deployments across multiple provinces.

Page last updated on: