Australia IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

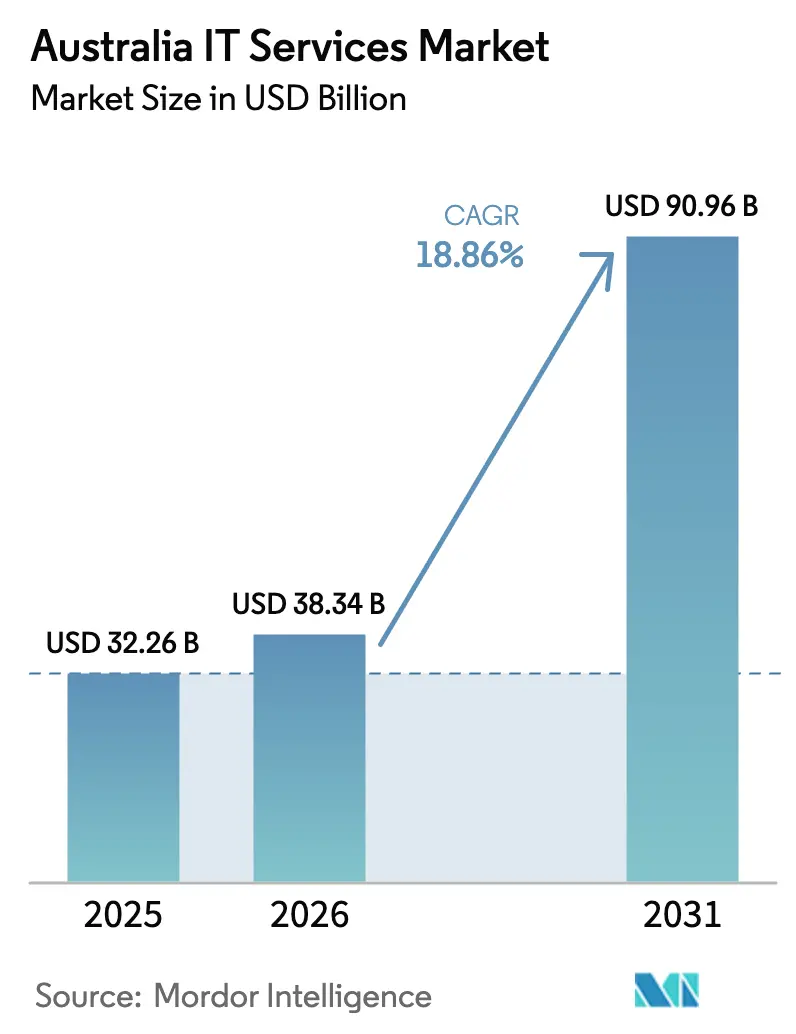

| Base Year Market Size (2025) | USD 32.26 Billion |

| Market Size (2026) | USD 38.34 Billion |

| Market Size (2031) | USD 90.96 Billion |

| Growth Rate (2026 - 2031) | 18.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia IT Services Market Analysis by Mordor Intelligence

The Australia IT services market size is expected to grow from USD 32.26 billion in 2025 to USD 38.34 billion in 2026 and is forecast to reach USD 90.96 billion by 2031 at 18.86% CAGR over 2026-2031. Robust public-sector digital programs, rapid enterprise cloud migration, and persistent cybersecurity mandates are the primary catalysts. Federal technology allocations of USD 2.8 billion for 2024-25, together with 110 active projects worth USD 12.9 billion, continue to anchor predictable systems-integration demand. Parallel hyperscale commitments, such as AWS’s USD 13.2 billion build-out through 2027 and Microsoft’s new Western Australia region, are reshaping infrastructure choices.[1]Amazon Web Services, “AWS Investment in Australia Grows,” amazon.com The Essential Eight framework and Security of Critical Infrastructure Act elevate spending on managed security services, while persistent skills shortages intensify outsourcing activity. Indigenous procurement quotas and mid-tier firm gains after Big Four contract declines also influence competitive dynamics.

Key Report Takeaways

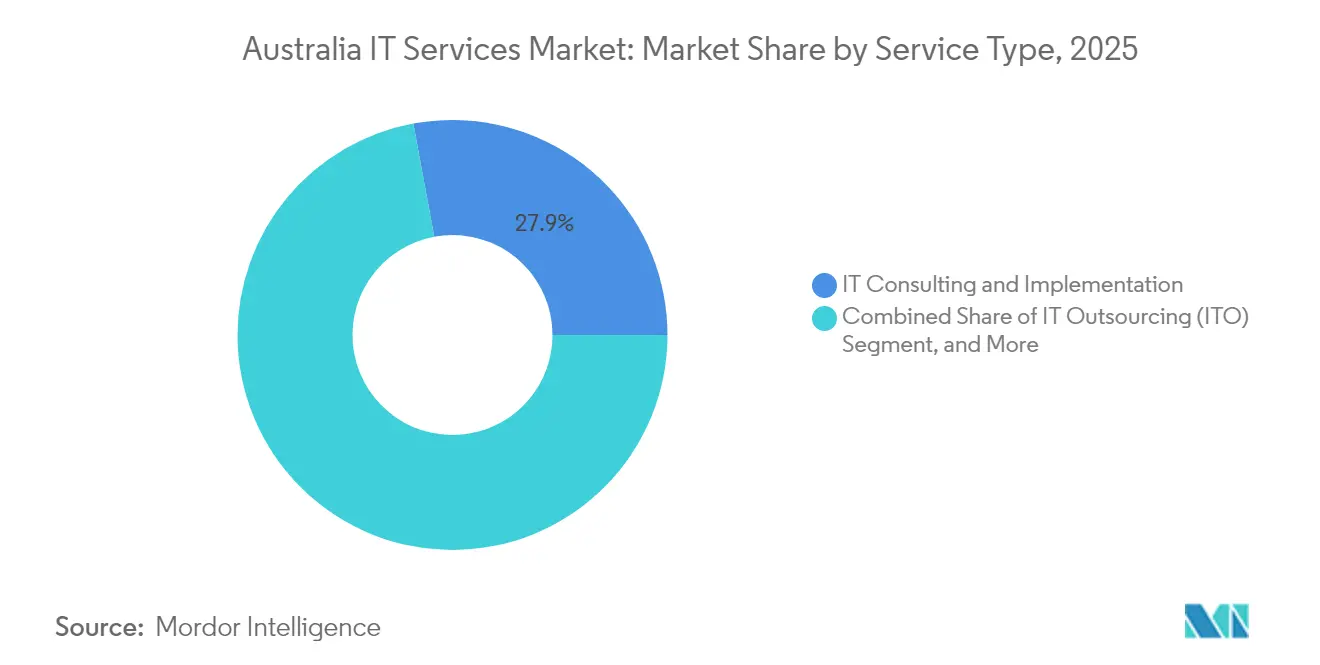

- By service type, IT consulting and implementation captured 27.92% of Australia IT services market share in 2025; cloud and platform services are advancing at a 23.64% CAGR through 2031.

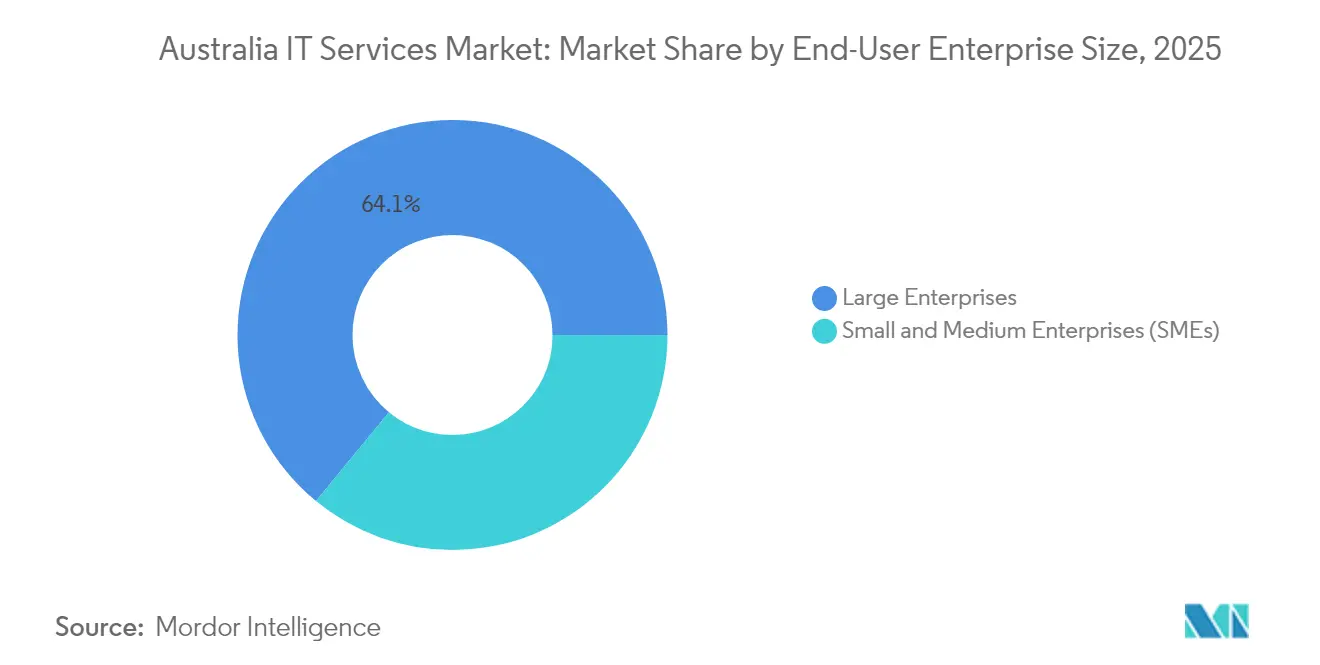

- By enterprise size, large enterprises held 64.05% share of the Australia IT services market size in 2025, while SMEs are expanding at a 22.74% CAGR to 2031.

- By end-user vertical, the BFSI segment led with 17.85% revenue share in 2025; healthcare and life-sciences are forecast to grow at a 21.95% CAGR to 2031.

- By geography, Sydney and Melbourne together accounted for more than half of the Australia IT services market in 2025; Perth is the fastest-growing metro with double-digit CAGR driven by new data-center capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital-transformation spending surge | +4.20% | National, concentrated in Canberra and state capitals | Medium term (2-4 years) |

| Pandemic-accelerated SME cloud migration | +3.80% | National, with higher adoption in urban centers | Short term (≤ 2 years) |

| Cyber-security compliance (Essential Eight, SOCI) | +3.10% | National, critical infrastructure sectors | Long term (≥ 4 years) |

| IT-skills scarcity elevates outsourcing demand | +2.90% | National, acute in Sydney and Melbourne | Medium term (2-4 years) |

| Hyperscale cloud-region build-out | +2.70% | Sydney, Melbourne, Perth data center hubs | Long term (≥ 4 years) |

| Indigenous procurement quotas boosting niche IT firms | +1.80% | National, remote area focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital-Transformation Spending Surge

Federal agencies account for more than half of the projected USD 19 billion public IT spend for 2024, reflecting the government’s goal to rank among the top three digital governments globally by 2025.[2]Digital Transformation Agency, “Australian Government Digital Strategy,” dta.gov.au The Digital Transformation Agency lists 110 active programs worth USD 12.9 billion, 80.3% of which achieved high delivery confidence in 2025. Notable allocations include USD 288 million for a digital ID platform, USD 466 million for quantum-computing infrastructure, and USD 448 million for the Landsat Next satellite. Continuous legacy-system upgrades and myGov enhancements of USD 580 million sustain demand for consulting, migration, and integration workstreams.

Pandemic-Accelerated SME Cloud Migration

Australian SMEs now favour multi-cloud strategies, with 90% using at least two cloud providers to modernize operations.[3]NBN Co., “Cloud Computing Tips for Small Businesses,” nbnco.com.au Despite higher operating costs and softer revenue, technology adoption remains a top budget line as firms seek efficiency improvements. SaaS penetration is widespread; Microsoft 365 commands 73% usage across small businesses. These patterns translate into recurring demand for cloud assessment, migration, and managed-services engagements targeting cost containment and agility gains.

Cybersecurity Compliance Mandates (Essential Eight, SOCI)

The Essential Eight guides baseline cyber hygiene across public and private sectors, while the SOCI Act forces critical-sector entities to adopt advanced maturity profiles. Agencies must demonstrate at least Level 1 compliance, and high-risk environments are migrating toward Level 3. The mandated controls—spanning application allow-listing, patch frequency, privileged-access limitations, and multi-factor authentication—stretch in-house resources and accelerate the managed security-services pipeline.

IT-Skills Scarcity Elevates Outsourcing Demand

Australia needs 1 million tech workers by 2025 but faces a shortage of 260,000 skilled professionals. The scarcity is most acute in cybersecurity, AI engineering, and cloud architecture. More than half of specialists are considering contract roles, prompting enterprises to supplement project teams with external talent. Outsourcing mitigates wage inflation and helps maintain delivery timelines, especially for regulated industries that cannot delay transformation programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour cost inflation | -2.80% | National, acute in Sydney and Melbourne | Short term (≤ 2 years) |

| Data-sovereignty barriers to off-shoring | -1.90% | National, government and critical sectors | Long term (≥ 4 years) |

| Data-centre energy-price volatility | -1.40% | Sydney, Melbourne, Perth data center hubs | Medium term (2-4 years) |

| Sub-sea cable concentration risk | -0.90% | National, international connectivity dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Cost Inflation

The salary premium for senior cybersecurity architects and AI engineers exceeds 20% year on year, squeezing provider margins. Shorter government contract tenures increase revenue volatility, compelling firms to optimize utilization and invest in up-skilling initiatives. Rising construction wages for electricians and HVAC experts further inflate data-center build-out costs, indirectly pressuring service pricing.

Data-Sovereignty Barriers to Off-Shoring

The SOCI Act mandates that sensitive workloads remain in Australia, limiting offshore delivery models and curtailing cost-arbitrage strategies. Federal buy-local rules, including the Buy Australian Plan’s USD 18.1 million allocation for supplier development, reinforce onshore preference. Domestic providers gain a protected revenue stream but must absorb higher operating expense, prompting selective automation to sustain competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type - Cloud Platforms Drive Digital Acceleration

IT consulting and implementation services controlled 27.92% of Australia IT services market share in 2025, confirming the continued need for strategic guidance and systems integration. The cloud and platform services segment are forecast to post a 23.64% CAGR, aided by hyperscale region launches and enterprise modernization agendas. Managed security services follow closely as organizations pursue Essential Eight certification paths. In contrast, business process outsourcing grows slowly as process-automation software displaces traditional manual tasks.

Demand patterns reveal a pivot from stand-alone projects toward outcome-based engagements that combine advisory, migration, and ongoing optimization. AWS’s USD 13.2 billion regional expansion and Microsoft’s Perth stack strengthen supply-side ecosystems, giving service partners targeted workload-migration incentives. Telstra’s USD 700 million AI venture with Accenture showcases convergence of telecom assets and advanced analytics, signalling new hybrid categories that fuse connectivity with platform-centric managed services.

By Enterprise Size - SME Growth Outpaces Corporate Expansion

Large enterprises accounted for 64.05% of the Australia IT services market size in 2025, reflecting deep technology budgets across banking, mining, and public agencies. Nevertheless, SMEs are projected to grow at 22.74% CAGR through 2031 as subscription-based models lower entry barriers. Commonwealth Bank’s 95% compute migration to public cloud illustrates the scale benefits accessible to large organizations. Macquarie Bank’s SAP workload cut end-of-day processing time by 20%, underlining tangible efficiency gains.

SMEs prefer bundled offerings that package security, collaboration, and analytics on a pay-as-you-go basis. Surveys show 68% of small firms rank operational efficiency as a top objective, while 71% prioritize profit improvement. The Buy Australian Plan’s supplier inclusion initiatives widen public-sector opportunities, enabling small integrators to secure multiyear contracts without competing against global primes.

By End-User Vertical - Healthcare Leads Digital Health Revolution

BFSI led the vertical mix with 17.85% share in 2025, driven by stringent risk and compliance mandates. Healthcare and life-sciences, however, is set to register a 21.95% CAGR, fuelled by government spending exceeding USD 1.1 billion to achieve full interoperability by 2027. The My Health Record platform already supports 24.1 million citizens, demanding continuous integration and cybersecurity oversight. Oracle Health and Telstra Health dominate electronic-records rollouts, using FHIR standards to streamline data exchanges.

Manufacturing and government segments adopt steady modernization plans, while retail, telecom, and logistics invest selectively to combat cost pressures. Energy-sector examples like Endeavour Energy’s SAP deployment, which trimmed reporting from hours to minutes, prove the ROI of real-time analytics. Such successes reinforce cross-industry interest in cloud-native and edge solutions.

Geography Analysis

Australia IT services market activity concentrates in eastern seaboard metros. Sydney ranks third and Melbourne eighth in Asia-Pacific data-center capacity, jointly hosting the bulk of hyperscale nodes. Competitive power rates, renewable-energy projects, and 17 subsea cables position both cities as preferred aggregation points. Canberra specializes in secure federal workloads that require security-cleared personnel, sustaining premium consulting rates.

Perth emerges as the fastest-growing metro following Microsoft’s Azure region and GreenSquareDC’s AI-optimized facility. The western capital supports mining-sector digitization and under-sea cable redundancy to Africa and the Middle East. Brisbane and the Gold Coast leverage proximity to Asian markets and enjoy modestly lower labour costs, attracting mid-market shared-services projects.

Policy instruments widen geographic spread. Indigenous procurement rules direct telecommunications and IT services dollars to remote communities, generating cybersecurity and Wi-Fi deployment contracts in Northern Territory homelands. While remote demand remains smaller in absolute terms, high service premiums offset scale limitations and incentivize providers to build local presence.

Competitive Landscape

The Australia IT services market remains moderately fragmented, with the top five providers holding an estimated 40% combined share. Big Four consulting firms historically dominated government advisory, but scandals caused a 40% revenue contraction in FY24, opening lanes for mid-tier specialists. Deloitte Australia reported USD 2.55 billion revenue in FY25, signalling stabilization after an 8.3% slide. Mid-tier firms collectively captured USD 3.5 billion, boosted by procurement diversification.

Strategic consolidation accelerates. CSO Group merged with xAmplify, forming a USD 100 million cybersecurity and AI consultancy. Logicalis integrated its Asia and Australia operations to create a USD 350 million APAC entity with 1,600 employees. Distributors Dicker Data and Data#3, posting USD 3.4 billion and USD 2.8 billion in sales respectively, broaden managed-services portfolios to counter hardware margin compression.

Innovation themes concentrate on AI-enabled service delivery, edge computing, and sovereign-cloud packaging. Telstra’s Microsoft 365 Copilot roll-out covering 21,000 seats exemplifies large-scale generative-AI adoption. Providers able to certify Essential Eight Level 3 controls and offer data-residency assurances secure premium prices, while smaller firms carve niches in Indigenous procurement plans or regional rollout contracts.

Australia IT Services Industry Leaders

Accenture Australia Pty Ltd

IBM Australia Ltd

Telstra Corporation Ltd (Telstra Purple)

DXC Technology Australia Pty Ltd

Tata Consultancy Services Limited (Australia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AWS launched a second Australian region in Melbourne backed by USD 4.5 billion capital through 2037, forecast to add USD 10.6 billion to GDP.

- May 2025: Telstra purchased 21,000 Microsoft 365 Copilot licenses in the largest national generative-AI deployment.

- January 2025: Telstra and Accenture formed a USD 700 million AI joint venture with a 60-40 equity split.

- December 2024: Microsoft activated its Perth data-center region, strengthening western-seaboard latency profiles.

Australia IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals |

Key Questions Answered in the Report

What is the projected value of the Australia IT services market in 2031?

It is forecast to reach USD 90.96 billion by 2031, reflecting a 18.86% CAGR.

Which service line is growing the fastest?

Cloud and platform services are advancing at a 23.64% CAGR through 2031.

Which customer segment shows the strongest momentum?

Small and medium enterprises are expanding at a 22.74% CAGR as cloud adoption accelerates.

Which vertical is set to post the highest CAGR?

Healthcare and life-sciences is projected to grow at a 21.95% CAGR because of digital-health investments.

How do data-sovereignty rules influence delivery models?

SOCI Act mandates keep sensitive workloads onshore, limiting off-shoring and boosting demand for domestic providers.

Why are managed security services in high demand?

Essential Eight compliance requirements are prompting organizations to outsource cybersecurity operations to certified experts.

Page last updated on: