Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

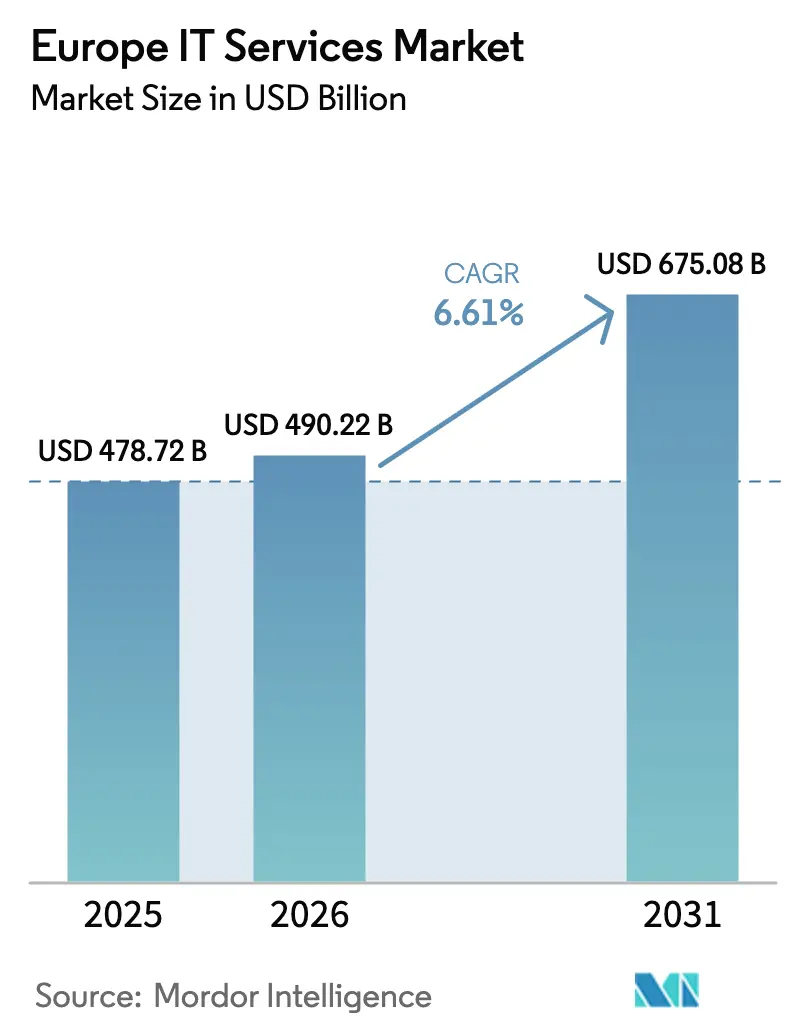

| Base Year Market Size (2025) | USD 478.72 Billion |

| Market Size (2026) | USD 490.22 Billion |

| Market Size (2031) | USD 675.08 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe IT Services Market Analysis by Mordor Intelligence

The Europe IT services market size is projected to be USD 478.72 billion in 2025, USD 490.22 billion in 2026 and reach USD 675.08 billion by 2031, growing at a CAGR of 6.61% from 2026 to 2031. Mandatory cybersecurity, sustainability reporting, and ERP modernization deadlines, rather than discretionary digital pilots, now set the rhythm for spending. Enterprises are reallocating budgets away from small proofs of concept toward large, compliance-driven outsourcing deals, especially in managed security and SAP S/4HANA migration. Delivery-model selection is fragmenting along data-sovereignty lines, giving cost-competitive nearshore hubs in Poland and Romania a pricing premium over India for sensitive workloads. At the same time, green-energy surcharges under the EU Emissions Trading System are pressuring hyperscalers to optimize data-center footprints rather than offer blanket price cuts. These structural shifts explain why the Europe IT services market trails faster-growing North American peers despite robust demand.

Key Report Takeaways

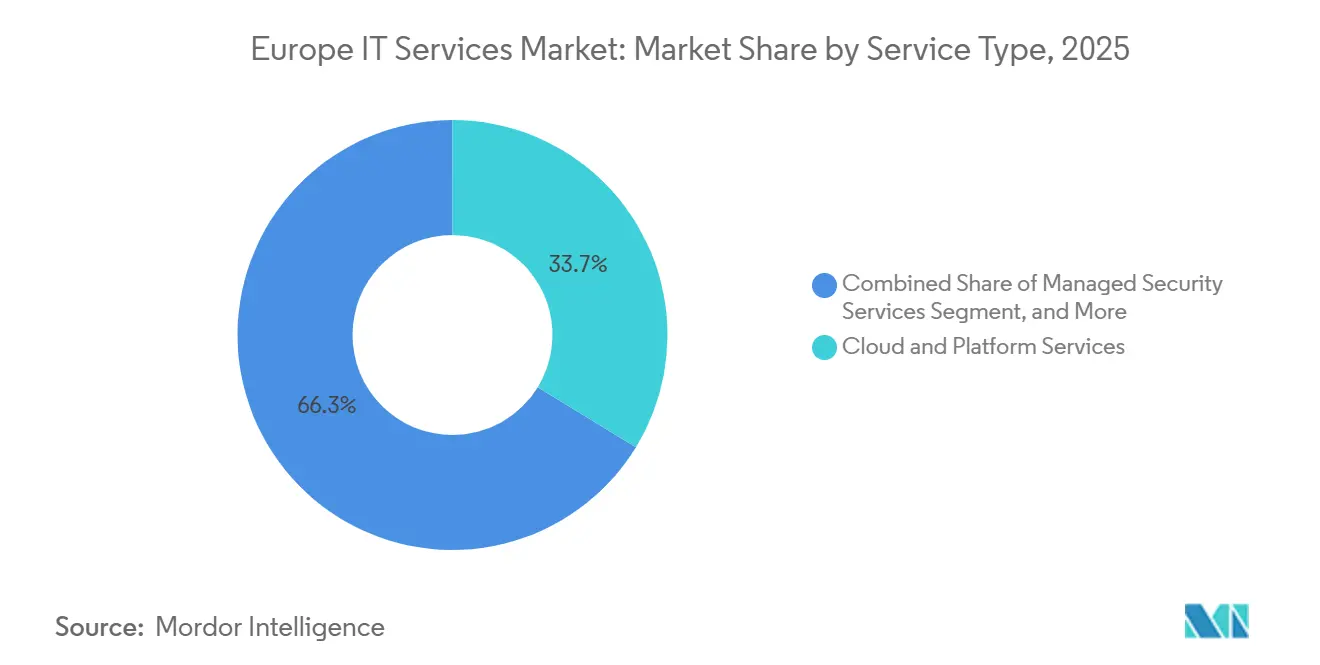

- By service type, Cloud and Platform Services led with 33.74% of Europe IT services market share in 2025, while Managed Security Services is advancing at a 6.72% CAGR through 2031.

- By enterprise size, Large Enterprises accounted for 60.36% of the Europe IT services market size in 2025; Small and Medium Enterprises are expanding at a 6.96% CAGR to 2031.

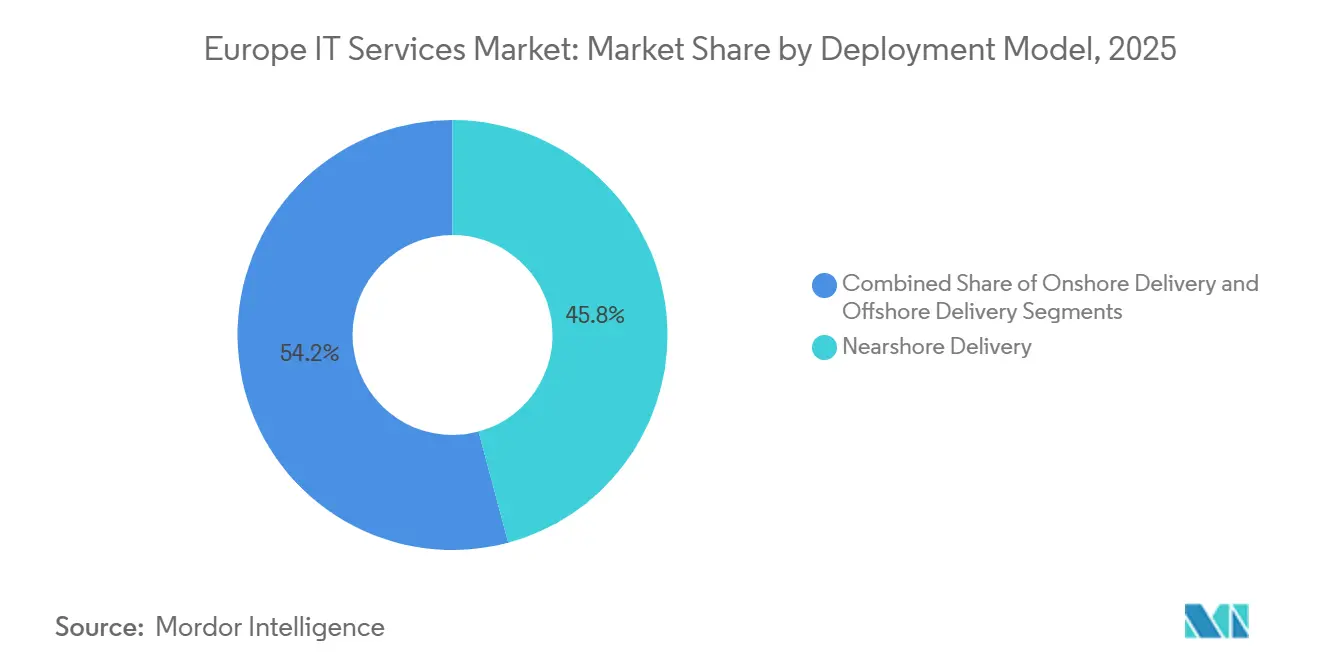

- By deployment model, Nearshore Delivery contributed 45.83% revenue in 2025, but Offshore Delivery is projected to climb at a 7.02% CAGR from 2026-2031.

- By end-user vertical, BFSI captured 20.93% share in 2025; Healthcare and Life-Sciences is forecast to post the fastest 6.88% CAGR to 2031.

- By Country, United Kingdom commanded a 26.64% share of the Europe IT services market in 2025, while Spain is expected to post a 7.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging enterprise-wide cloud migration | +1.2% | Global, with highest intensity in UK, Germany, Nordics | Medium term (2-4 years) |

| Demand for cost-optimized ITO and BPO contracts | +0.9% | Global, spill-over from UK and Germany to Southern Europe | Short term (≤ 2 years) |

| Shift to managed security amid EU-wide cyber-threat directives | +1.1% | EU-27, with early adoption in France, Netherlands, Belgium | Short term (≤ 2 years) |

| AI-driven vendor-selection platforms accelerating outsourcing | +0.7% | Global, early gains in UK, Germany, Nordics | Medium term (2-4 years) |

| Corporate urgency to modernize SAP and legacy ERP before 2027 support sunset | +1.0% | Germany, UK, France, Italy, Spain | Short term (≤ 2 years) |

| EU CSRD-linked ESG-reporting services boosting consulting demand | +0.8% | EU-27, strongest in Germany, France, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Enterprise-Wide Cloud Migration

Cloud adoption jumped after the NIS2 Directive obliged essential entities to maintain alternate processing sites, making multi-cloud redundancy a legal necessity rather than a best practice.[1]European Commission, “NIS2 Directive,” EUROPA.EU German industrial firms are moving sensitive workloads to Gaia-X-aligned sovereign clouds while keeping non-critical data on global hyperscalers. The Digital Decade program targets 75% cloud usage among European companies by 2030, sustaining a pipeline of lift-and-shift and modernization projects. Vendors able to combine SAP expertise with container-based microservices are winning large transformation mandates. Multi-cloud complexity also unlocks follow-on demand for FinOps, observability, and inter-cloud security gateways, strengthening long-term managed-services revenues.

Shift to Managed Security Amid EU-Wide Cyber-Threat Directives

The NIS2 Directive expanded the scope of regulated entities from roughly 2,000 to more than 160,000 organizations in January 2025. Mandatory 24-hour breach reporting and supply-chain risk mapping overloaded in-house security teams, pushing buyers toward Managed Security Service Providers that can deliver round-the-clock SOC monitoring and zero-trust design. Sector guides from France’s ANSSI and Germany’s BSI standardized tender specifications, cutting procurement ambiguity and accelerating deal closure. Fixed-fee “compliance-as-a-service” bundles appeal to mid-market firms that lack chief information-security officers, converting ad-hoc audits into predictable subscriptions.

Corporate Urgency to Modernize SAP and Legacy ERP Before 2027 Support Sunset

SAP will end mainstream support for ECC 6.0 in December 2027, exposing nearly 15,000 European installations to security and compliance risks unless they migrate to S/4HANA. Brownfield conversions dominate in Germany’s manufacturing belt because custom ABAP code must be preserved to protect just-in-time production. Selective data-transition approaches, moving only high-value processes, promise license savings but heighten integration risk, driving demand for specialist integrators. Oracle and Microsoft are courting laggards with migration incentives, fragmenting the ERP services arena into vendor-specific skill pools and intensifying competition for scarce functional consultants.

EU CSRD-Linked ESG-Reporting Services Boosting Consulting Demand

The Corporate Sustainability Reporting Directive applies to all large undertakings by 2025 and to 50,000 companies by 2028, mandating double-materiality assessments and auditable Scope 3 emissions disclosures.[2]European Commission, “Corporate Sustainability Reporting Directive,” EUROPA.EU Most firms lack systems to aggregate supplier-level data, opening a sustained consulting revenue stream around ESG data platforms, IoT-enabled carbon metering and blockchain-based provenance tracking. Technology-plus-sustainability practices enjoy higher win rates than pure-play ESG advisories because they automate reporting and assurance in one stack, locking clients into multi-year managed-service extensions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent scarcity and wage inflation in key delivery hubs | -0.6% | Germany, UK, Nordics, Poland, Romania | Short term (≤ 2 years) |

| Geopolitical data-sovereignty barriers (Schrems II, AI Act) | -0.5% | EU-27, with acute impact on UK post-Brexit | Long term (≥ 4 years) |

| Prolonged client-decision cycles owing to macro-uncertainty | -0.4% | Global, highest in manufacturing-heavy Germany, Italy | Short term (≤ 2 years) |

| Rising carbon-footprint penalties on energy-intensive data centers | -0.3% | EU-27, particularly Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Scarcity and Wage Inflation in Key Delivery Hubs

Eurostat recorded 500,000 unfilled ICT posts in 2025 and median developer pay in Germany rose 8.2% year-on-year, eroding nearshore cost advantages.[3]Eurostat, “ICT Specialists—Hard-to-Fill Vacancies,” EUROSTAT.EC.EUROPA.EU Wage spikes of 9% in Poland and Romania squeezed vendors locked into fixed-price contracts signed during the low-inflation era. Brain drain toward North America compounds shortages, forcing providers to automate tier-1 support through generative-AI chatbots and prioritize high-margin advisory work. These stopgaps, however, only partly offset the structural talent gap, trimming Europe IT services market growth potential.

Geopolitical Data-Sovereignty Barriers (Schrems II, AI Act)

The Schrems II judgment voided the Privacy Shield and left trans-Atlantic data transfers exposed to future legal contests despite the 2023 adequacy decision. The AI Act’s extraterritorial rules require CE-marking and conformity assessments for high-risk systems delivered from offshore centers, pushing sensitive workloads to onshore or nearshore locations. Fragmented data-residency regimes prevent universal labor-arbitrage strategies and keep the Europe IT services market segmented into three non-fungible price tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Compliance Mandates Elevate Security Spend

Managed Security Services sits atop growth rankings with a 6.72% CAGR to 2031 even though Cloud and Platform Services controlled a 33.74% Europe IT services market share in 2025. Mandatory threat-monitoring duties under NIS2 and DORA make 24x7 SOC coverage a board-level concern, converting discretionary security pilots into non-negotiable opex. Vendors that embed continuous compliance checks into ERP rollouts and cloud migrations capture incremental wallet share.

Consulting and Implementation revenue is buoyed by SAP S/4HANA conversions, CSRD-linked ESG platform buildouts, and European Health Data Space integrations. ITO and BPO lines are converging as robotic process automation and AI-driven document extraction reshape back-office deals, while Extended Detection and Response platforms push security spending from perimeter defense into predictive threat hunting.

By Enterprise Size: SME Digitalization Accelerates

Large Enterprises generated 60.36% of 2025 revenue thanks to multi-year global support deals, yet Small and Medium Enterprises are on course for a 6.96% CAGR through 2031. EU Digital Decade funds and Germany’s Digital Now grants cover up to 50% of eligible cloud costs, lowering adoption hurdles. Pre-configured SaaS bundles shorten deployment cycles, but integrations, data migration and cyber-posture assessments still require external expertise, expanding opportunity for modular service catalogs.

A secondary growth lever is consultancy-led “digital maturity” diagnostics, which unlock public subsidies and channel spend toward solution providers already accredited under national voucher schemes. This creates recurring advisory assignments alongside initial implementation work.

By Deployment Model: Offshore Gains Despite Data-Sovereignty Friction

Nearshore Delivery retained 45.83% share in 2025 owing to GDPR-native Polish and Romanian centers that bridge cost and compliance. Offshore Delivery nevertheless leads growth at 7.02% because AI-fueled collaboration tools mitigate time-zone and communication barriers. Clients segment workloads, sensitive data resides onshore or nearshore, while commodity maintenance flows to India, with a three-tier tariff, onshore at 2× nearshore, nearshore at 1.5× offshore.

Follow-the-sun models rotate L1 support across geographies, freeing European experts for high-value tasks. However, Schrems II and AI Act restrictions inhibit wholesale workload re-location, ensuring demand persists for every tier.

By End-User Vertical: Healthcare Surges on EHDS Mandates

BFSI held 20.93% of 2025 revenue after the Digital Operational Resilience Act required banks to audit third-party ICT risk. Healthcare and Life Sciences is the fastest-growing vertical at 6.88% through 2031 because the European Health Data Space compels cross-border EHR interoperability. Manufacturing demand is tempered by interest-rate uncertainty, which delays Industry 4.0 capex, yet EU Recovery funds sustain baseline digital spending. Public-sector modernization benefits from the EUR 134 billion Recovery and Resilience Facility, although procurement cycles remain lengthy.

The EHDS regulation's requirement for a European Health Data Space infrastructure-enabling patients to access their health data across borders and researchers to access anonymized datasets for secondary use-is creating a multi-billion-euro opportunity in health IT services, spanning EHR system upgrades, consent-management platforms, and federated-learning architectures that preserve privacy while enabling AI model training

Geography Analysis

The United Kingdom maintained a 26.64% revenue share in 2025 but faces headwinds from Brexit-induced talent outflows and data-adequacy ambiguities that complicate cross-border contracting. Germany and France enjoy robust pipelines under the Digital Now and France 2030 programs, respectively, though wage inflation erodes margin headroom. Italy’s National Recovery and Resilience Plan allocates EUR 40.7 billion for digital transition yet is slowed by administrative bottlenecks.

Spain is the growth standout, with a 7.11% CAGR to 2031, powered by the Digital 2030 Agenda’s EUR 20 billion cloud and smart-city stimulus and a tax regime that courts nearshore centers. Elsewhere, the Nordics lead in AI and green-tech uptake, Benelux focuses on fintech and logistics digitalization, while Eastern Europe benefits from rising nearshore demand but wrestles with wage pressures.

Pricing spreads reflect regulatory friction, onshore UK and German rates average 2 × Polish nearshore tariffs, which in turn exceed Indian offshore by roughly 50%. Currency-hedging costs and energy-surcharge pass-throughs under the EU ETS introduce additional regional differentiation.

Competitive Landscape

The Europe IT services market remains moderately fragmented, the top five suppliers together hold only 28% share, leaving plentiful room for vertical specialists and delivery-model innovators. Accenture and Capgemini are expanding sovereign-cloud offerings to counter data-residency barriers, IBM Consulting opened a Warsaw SOC to capture NIS2-driven security spend, and Tata Consultancy Services won a five-year NHS deal that cements its European healthcare credentials. Atos divested non-core voice assets to fund cybersecurity expansion.

Indian integrators leverage AI-powered vendor-matching engines that halve RFP cycles, eroding incumbents’ relationship moat. Smaller contenders such as Reply, GFT Technologies, and Endava win on domain depth in fintech, healthtech, and AI Act compliance audits. Growing demand for outcome-based pricing compels legacy firms to tie fees to resilience metrics or carbon-emission reductions, shifting risk-reward profiles across contracts.

White-space opportunity clusters around sovereign-cloud orchestration and CSRD-compliant ESG automation, both of which are underserved by hyperscalers. Providers offering university upskilling pipelines and immigration sponsorship secure scarce talent faster, gaining a margin edge as wage inflation bites.

Europe IT Services Industry Leaders

Accenture plc

Capgemini SE

Tata Consultancy Services Limited

IBM Consulting

Atos SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Tata Consultancy Services secured a 5-year, GBP 200 million (USD 254 million) contract with the UK National Health Service to modernize electronic health record systems across 42 hospital trusts, integrating cloud-based data lakes, AI-powered diagnostic support, and patient-facing mobile applications.

- November 2025: IBM Consulting won a EUR 180 million, 7-year contract with Deutsche Bahn to implement an AI-driven predictive maintenance platform across Germany's rail network, leveraging IBM Watson IoT and Red Hat OpenShift to analyze sensor data from 33,000 rail cars and reduce unplanned downtime by an estimated 25%.

- October 2025: Infosys announced a EUR 200 million investment to expand its delivery center in Brno, Czech Republic, adding 1,500 jobs focused on cloud engineering, AI model training, SAP S/4HANA migration services, and cybersecurity operations.

- September 2025: Cognizant Technology Solutions acquired Lev, a Netherlands-based Salesforce consulting firm with 400 employees and strong presence in Benelux and Nordics, for USD 150 million.

Europe IT Services Market Report Scope

Europe IT services leverage technology and business expertise to help organizations create, manage, and optimize information and business processes.

The Europe IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, Cloud and Platform Services), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (Onshore, Nearshore, and Offshore), End-User Vertical (BFSI, Manufacturing, Government, Healthcare, Retail, Telecom, Logistics, Energy, and Other End-Use Verticals), and Geography (UK, Germany, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Deployment Model

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

By End-User Vertical

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe IT services market in 2031?

Forecasts indicate the market will reach USD 675.08 billion by 2031.

How fast is managed security spending growing in Europe?

Managed Security Services is projected to rise at a 6.72% CAGR from 2026-2031, outpacing all other service types.

Why are SMEs accelerating IT outsourcing adoption?

EU Digital Decade incentives subsidize up to half of qualified cloud costs, enabling SMEs to adopt SaaS and managed services without heavy upfront investment.

Which European country is expected to post the fastest IT services growth?

Spain is forecast to record a 7.11% CAGR through 2031, propelled by EUR 20 billion in public digital-infrastructure programs.

How will SAP’s 2027 support sunset affect service providers?

Roughly 15,000 European ECC 6.0 users must migrate to S/4HANA or risk compliance gaps, fueling multi-year consulting and implementation demand.

Page last updated on: