Canada Dairy Alternatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

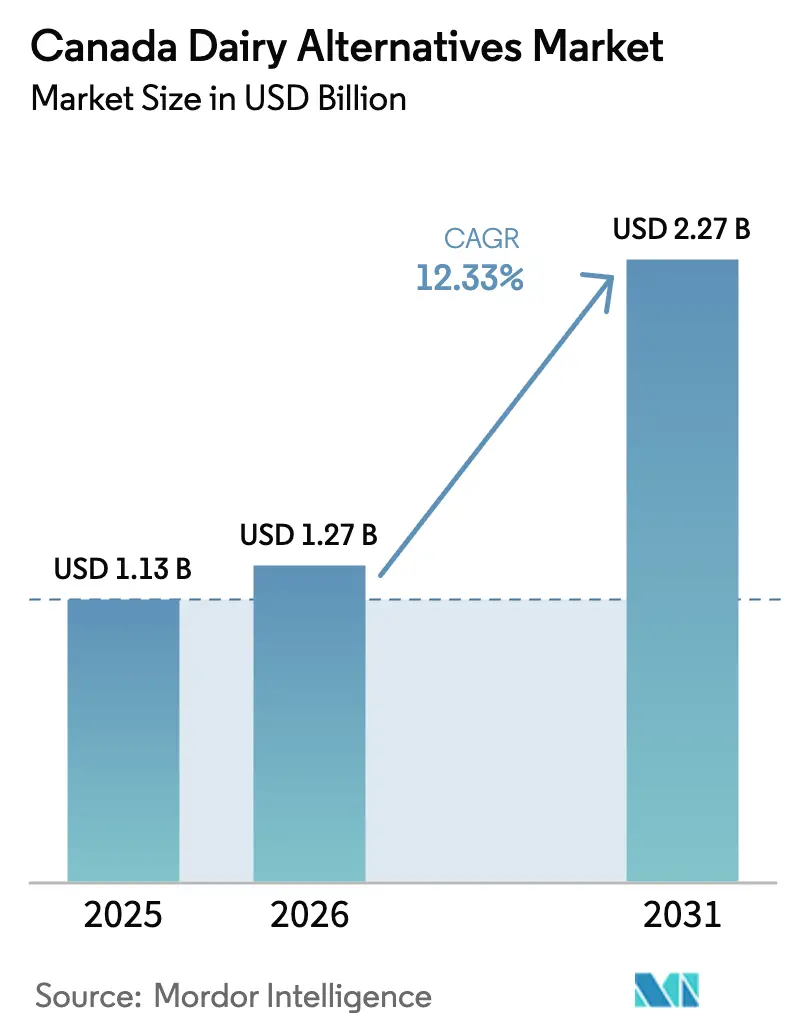

| Base Year Market Size (2025) | USD 1.13 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Dairy Alternatives Market Analysis by Mordor Intelligence

The Canada dairy alternatives market size was valued at USD 1.13 billion in 2025 and estimated to grow from USD 1.27 billion in 2026 to reach USD 2.27 billion by 2031, at a CAGR of 12.33% during the forecast period (2026-2031). This expansion is primarily fueled by Canada's large lactose-intolerant population, increasing adoption of flexitarian diets, and rapid advancements in oat- and pea-based beverages and cultured products. Growing awareness of the health benefits of plant-based ingredients, such as lower fat content, fewer calories, and improved digestion, further drives market growth. Functional products enriched with protein, calcium, and vitamin D are gaining significant traction. Manufacturers are utilizing government food-security grants to enhance local production capacities, while established dairy processors are shifting toward plant-based product lines to maintain their shelf presence. Although challenges like raw material price volatility and sensory limitations in cheese and yogurt alternatives persist, continuous research and development efforts and premiumization are expanding the consumer base. Improved distribution networks, along with the growth of organized retail and e-commerce, are ensuring broader product availability across Canada. Heightened competition among multinationals, traditional dairies, and domestic start-ups is intensifying price competition, spurring packaging redesigns, and driving channel diversification.

Key Report Takeaways

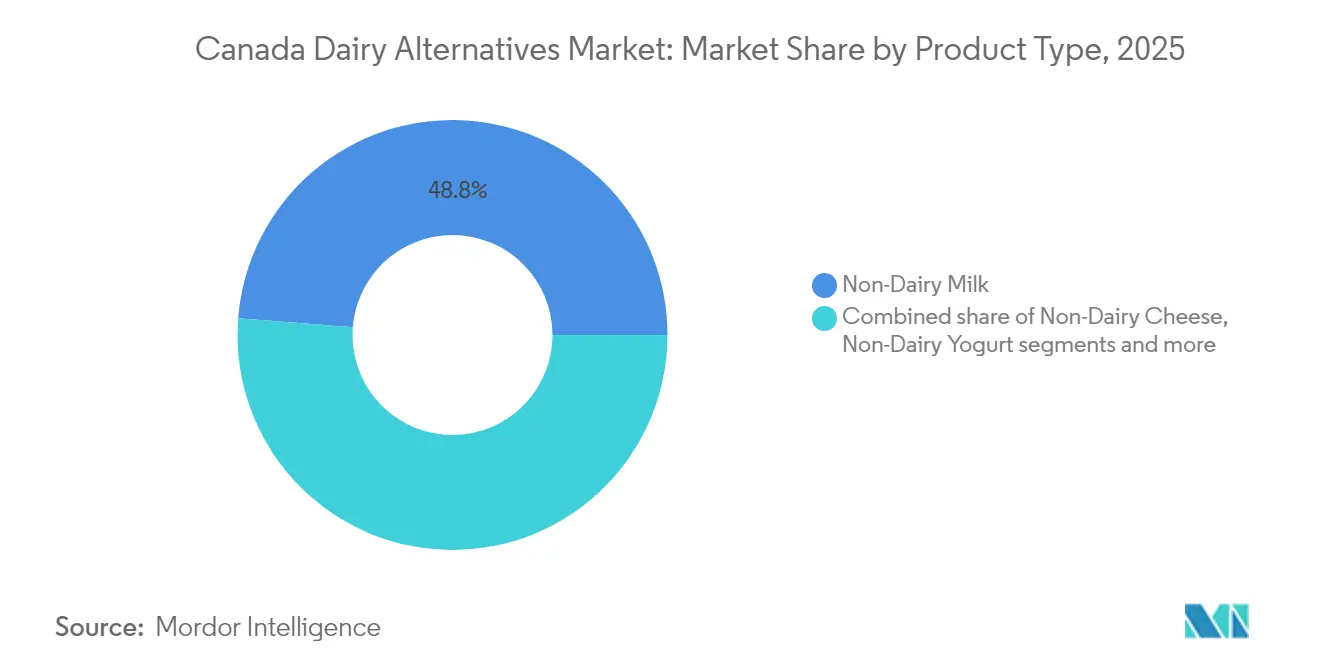

- By product type, non-dairy milk led with 48.76% revenue share in 2025, whereas non-dairy cheese is projected to expand at a 14.28% CAGR through 2031.

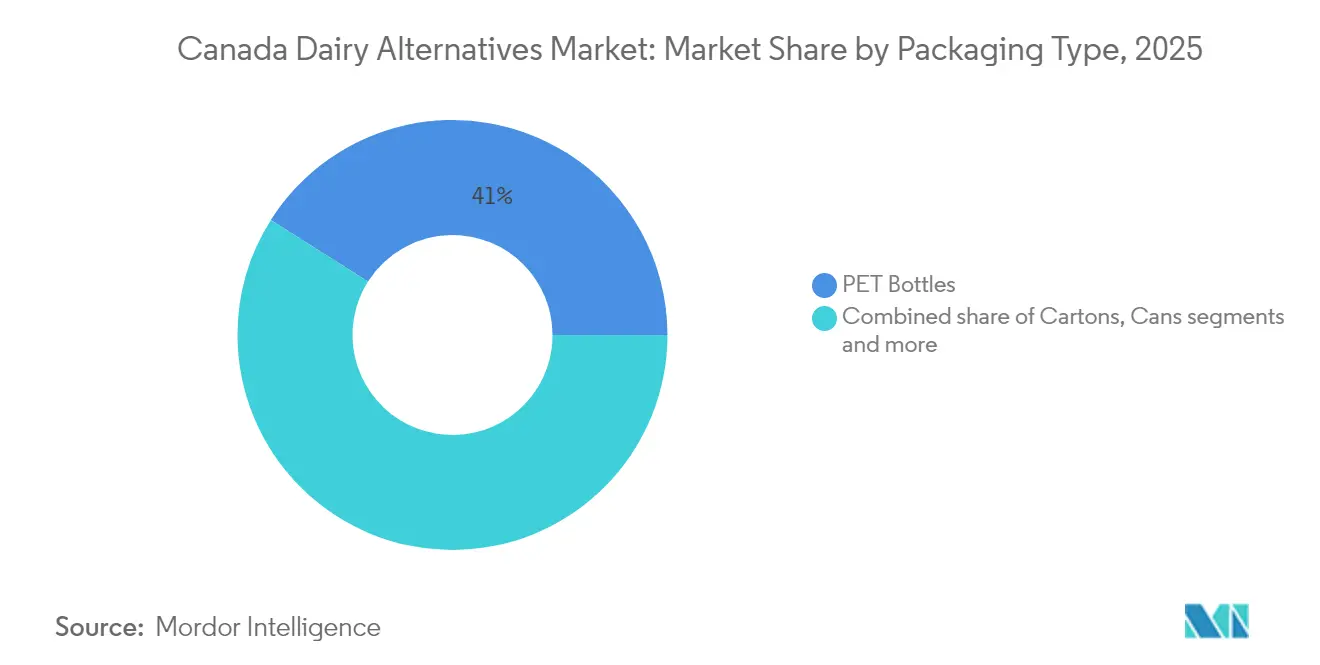

- By packaging type, PET bottles captured 41.02% of the 2025 Canada dairy alternatives market share, while cartons are forecast to grow at a 13.05% CAGR to 2031.

- By distribution channel, off-trade accounted for 78.12% of 2025 revenue, and on-trade is expected to post the fastest 13.88% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Dairy Alternatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High lactose-intolerance prevalence drives structural demand | +2.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Rising health-conscious and flexitarian lifestyles | +3.1% | National, strongest in BC and Ontario | Medium term (2-4 years) |

| High-protein oat and pea-based innovations | +2.4% | National, manufacturing hubs in Ontario and Quebec | Medium term (2-4 years) |

| Fortification of products with essential nutrients | +1.9% | National, premium retail channels | Short term (≤ 2 years) |

| Government food-security grants enabling local alt-dairy plants | +1.7% | Provincial, focused on Ontario and Quebec | Long term (≥ 4 years) |

| Growing consumer preference for natural and organic products | +2.2% | National, concentrated in metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High lactose-intolerance prevalence drives structural demand

Lactose intolerance, a digestive disorder, occurs when individuals cannot digest lactose in dairy products due to insufficient production of the lactase enzyme. In Canada, it is one of the most common food intolerances. Research published in the Journal of the Canadian Association of Gastroenterology indicates that by 2025, nearly 44% of Canadians experiences lactose intolerance[1]Source: Canadian Association of Gastroenterology, "How to Test for Lactose Intolerance", cdhf.ca. This highlights a significant market for dairy alternatives, driven by necessity rather than choice. Unlike preference-based segments, this physiological need creates a consumer base that remains stable even during economic downturns. The prevalence of lactose intolerance varies across demographics, with higher rates among Indigenous populations and recent immigrants from Asia and Africa. This demographic variation offers targeted marketing opportunities for brands that cater to these specific consumer groups. Additionally, Health Canada's recognition of lactose intolerance as a medical condition has enabled insurance coverage for specialized products in certain provinces, reducing cost barriers for consumers. Since lactose intolerance is a lifelong condition, demand for alternatives is expected to grow, particularly as immigration patterns shift the demographic composition toward populations with higher rates of intolerance.

Rising health-conscious and flexitarian lifestyles reshape consumption patterns

In Canada, the increasing focus on health and the adoption of flexitarian lifestyles are significantly transforming consumption patterns. Canadians are progressively gravitating towards food choices that are not only nutritious but also plant-based and sustainable. However, this transition is measured, as consumers carefully weigh factors such as cost and convenience. This trend is particularly evident in urban centers across the country, where dietary habits are evolving. Rather than adhering to rigid dietary frameworks, consumers are embracing a more flexible approach, seamlessly incorporating both dairy and plant-based products into their diets. These choices are often guided by specific occasions, personal health objectives, and environmental considerations. Millennials and Gen Z consumers are leading this shift, viewing plant-based alternatives as premium wellness products rather than restrictive dietary substitutes. This demographic plays a pivotal role in driving the market, accounting for 70% of category trials and repeat purchases. Their adoption of a flexitarian approach reduces the barriers to entry for plant-based products, as it eliminates the need for a complete dietary overhaul. This gradual transition fosters sustained market growth and supports the long-term expansion of the sector.

High-protein oat and pea-based innovations unlock new applications

Protein enhancement has emerged as a pivotal factor in differentiating plant-based dairy alternatives. A notable example is Danone's Silk Protein, which delivers an impressive eight times the protein content of traditional Silk Almondmilk, setting a new benchmark in the category. Similarly, Burcon NutraScience has revolutionized the industry with its proprietary pea protein extraction technologies. These innovations enable Canadian manufacturers to achieve protein profiles comparable to dairy products while adhering to clean label formulations, which are increasingly demanded by health-conscious consumers. Canada's abundant pea production further supports this growth, ensuring a reliable supply of raw materials for manufacturers. In 2024, pea production in Canada reached 3.0 million tonnes, reflecting a significant 14.9% increase compared to 2023, as per data from the Canadian Grain Commission[2]Source: Canadian Grain Commission, "Quality of western Canadian peas 2024", grainscanada.gc.ca. The game-changing advancement lies in enzymatic processing techniques, which effectively remove off-flavors, particularly the beany notes that have historically limited the adoption of pea protein in beverages. This technological progress has been exemplified by SunOpta's investment in proprietary enzymatic oat extraction processes, showcasing how innovation can enhance both functional performance and cost efficiency. These developments position Canadian manufacturers as global leaders in plant-based protein technology, enabling them to capitalize on export opportunities while driving growth beyond the domestic market.

Fortification with essential nutrients addresses nutritional gaps

Nutrient fortification has advanced significantly, transitioning from simple calcium and vitamin D supplementation to the development of intricate micronutrient profiles that either match or surpass the nutritional density of dairy products. Silk Kids' formulation exemplifies this progress by combining oat and pea proteins with DHA omega-3, choline, and prebiotics, effectively addressing parental concerns regarding the adequacy of children's diets. Health Canada's updated Food and Drug Regulations, set to take effect on December 31, 2025, will introduce enhanced nutritional labeling requirements. These changes aim to improve transparency in nutritional comparisons, thereby favoring fortified products and offering consumers clearer insights. This regulatory update provides a strategic advantage to brands that prioritize comprehensive fortification programs. Furthermore, advancements in precision fermentation technologies now enable the production of bioactive compounds, such as lactoferrin and immunoglobulins, which are identical to those found in dairy but are created without the involvement of animals. This technological innovation, combined with robust fortification efforts, positions plant-based products as nutritionally superior alternatives rather than merely serving as substitutes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus subsidised dairy | -2.1% | National, most acute in rural areas | Medium term (2-4 years) |

| Taste/texture gap in cheese and yogurt analogues | -1.8% | National, affecting all demographics | Long term (≥ 4 years) |

| Raw-material price volatility (almond, oats) | -1.2% | National | Medium term (2-4 years) |

| Heightened food-safety scrutiny post-Listeria recall | -1.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium pricing versus subsidized dairy constrains mass market penetration

Although the pricing gaps have narrowed, price parity challenges remain significant. In Canada, the supply management system enforces artificial price floors for conventional milk, ensuring higher prices for these products. On the other hand, plant-based alternatives are subjected to full market pricing pressures, creating a structural disadvantage that is further reinforced by existing government policies. This disparity is even more evident in rural markets, where conventional dairy benefits from lower distribution costs and stronger consumer loyalty, widening the pricing gap. Furthermore, private label products in the plant-based alternatives segment have limited market penetration compared to conventional dairy, reducing the competitive pressure on branded products in this category. Adding to these challenges, the raw material costs for key plant-based inputs such as almonds, oats, and other ingredients are highly volatile. This cost unpredictability complicates manufacturers' efforts to plan for long-term price parity, making it difficult to achieve consistent pricing strategies in the market.

Taste and texture gaps in cheese and yogurt analogues limit category expansion

Plant-based cheese and yogurt products continue to face significant challenges in overcoming sensory performance deficits, which remain a major obstacle to driving repeat purchases. Taste and texture are the primary barriers preventing broader consumer adoption, particularly when compared to the success of plant-based milk alternatives. Reproducing the functional properties of dairy, such as the melting characteristics of cheese and the creamy mouthfeel of yogurt, requires the use of highly advanced ingredient systems. These systems, while effective, substantially increase formulation costs, making it difficult to achieve both sensory appeal and affordability. Fermentation technologies, which have the potential to deliver authentic dairy flavors without the use of animal-derived ingredients, are still in the early stages of commercialization. As a result, immediate solutions to address taste and flavor gaps remain limited. Decades of dairy consumption have shaped consumer expectations, setting high sensory benchmarks that plant-based alternatives often struggle to meet consistently across various applications and preparation methods. Additionally, the 2024 Listeria outbreak has intensified the need for stringent quality control measures, further complicating manufacturing processes and increasing production costs. This heightened scrutiny has also made consumers more sensitive to any perceived quality deviations, adding another layer of complexity for manufacturers in this market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Dairy Milk Dominates Despite Cheese Acceleration

Non-dairy milk holds a leading 48.76% market share in 2025, reinforcing its position as the primary product for consumers transitioning to plant-based alternatives. As the segment matures, manufacturers are focusing on advanced differentiation strategies, including protein fortification, flavor innovations, and functional benefits tailored to diverse applications such as coffee and children's nutrition. Non-dairy cheese is the fastest-growing segment, with a strong 14.28% CAGR projected through 2031. This growth is fueled by technological improvements in melting properties and flavor profiles, addressing previous performance limitations. Additionally, Health Canada's approval of Remilk's lab-grown milk proteins marks a significant milestone that could transform cheese analogue functionality.

Non-dairy desserts and yogurt face more complex formulation challenges but benefit from premium positioning and the rising demand for health-conscious products. The "Others" category, which includes creamers, butter alternatives, and specialty products, presents substantial innovation opportunities as manufacturers expand beyond traditional offerings. Oat milk has become the preferred choice for barista applications due to its superior frothing capabilities, with Mintel reporting a fourfold increase in Canadian purchases. Almond milk remains popular for direct consumption, while coconut milk caters to specialized culinary uses, showcasing how different plant bases are optimized for specific consumer needs and applications.

By Packaging Type: Sustainability Drives Carton Growth

Cartons are poised to lead the packaging market, achieving a strong 13.05% CAGR through 2031. This growth is primarily fueled by increasing consumer demand for sustainable solutions and advancements in plant-based packaging technologies. In 2024, a survey by Agriculture and Agri-Food Canada highlighted that 80% of Canadians prioritize a sustainable lifestyle, reflecting the nation's environmental concerns. Tetra Pak is at the forefront, integrating significant paperboard content into its latest packaging solutions. The adoption of cartons not only facilitates ambient storage for shelf-stable products but also reduces dependence on cold chains. This transition enhances distribution capabilities, extending reach to smaller retailers and rural markets.

In 2025, PET bottles hold a dominant 41.02% market share. Their appeal lies in premium positioning and visual attractiveness, particularly for refrigerated products where transparency emphasizes quality and freshness. Cans cater to niche markets, primarily in foodservice and specialty retail, while other formats such as pouches and glass containers address the needs of consumers prioritizing convenience or sustainability. This shift in packaging trends reflects growing environmental awareness among Canadians, with recyclability becoming a critical factor in purchasing decisions. Tetra Laval's focus on plant-based products, accounting for 8.2% of its net sales, highlights how packaging innovation drives category growth by addressing sustainability concerns aligned with plant-based product positioning.

By Distribution Channel: On-Trade Acceleration Signals Mainstream Adoption

Off-trade channels hold a dominant 78.12% market share in 2025, highlighting a retail-focused growth path and a strong consumer inclination toward home consumption. These channels provide easier product comparisons, label reviews, and access to a wide variety of brands and product types, including almond, oat, soy, and various non-dairy yogurts, cheeses, and desserts. However, on-trade channels are experiencing faster growth, with a notable 13.88% CAGR projected through 2031, reflecting mainstream foodservice adoption and the category's progression toward maturity. SunOpta's strategic collaboration to expand Dream Oatmilk into 6,700 additional stores through a partnership with a leading coffee chain exemplifies how foodservice adoption fosters consumer trials and enhances brand recognition.

Supermarkets and hypermarkets remain the leading players within off-trade channels. Meanwhile, online retail is rapidly expanding, driven by subscription models and the growth of direct-to-consumer brands. Convenience stores are emerging as a key opportunity, benefiting from the grab-and-go trend that supports portable plant-based beverages. This channel evolution reflects shifting consumer shopping habits, accelerated by digital adoption and a focus on convenience. Additionally, Compass Group's institutional adoption strategies illustrate how major foodservice operators are driving category validation and scaling adoption beyond individual consumer preferences. On-trade growth is further supported by barista training programs and equipment improvements, ensuring consistent product quality in professional preparation settings.

Geography Analysis

Canada's dairy alternatives market is experiencing significant growth, with regional differences influenced by demographics, urbanization, and local food preferences. British Columbia and Ontario are leading the market, driven by a higher concentration of health-conscious consumers, diverse ethnic populations with varying lactose tolerances, and a well-developed retail infrastructure for natural products. Quebec stands out with its strong preference for local brands, as seen in Natura's 30-year history in soy beverages and its recent introduction of Celiac Canada-certified oat products. The province's distinct culinary traditions and regulatory environment create opportunities for brands that cater to local tastes and distribution networks.

In the Prairie provinces, traditional dairy consumption remains dominant, but demographic changes and urbanization are driving increased adoption of dairy alternatives. The region's proximity to oat production provides a supply chain advantage for oat-based products and potential for local processing investments. Atlantic Canada, while slower in adoption, shows growth potential as distribution networks improve and product availability increases in smaller markets. Agriculture and Agri-Food Canada's CAD 150 million investment in alternative proteins aims to enhance national infrastructure while addressing regional implementation priorities.

Manufacturing capacity is playing a growing role in shaping market dynamics. Lactalis Canada's conversion of its Sudbury facility to plant-based production is providing Northern Ontario with a supply advantage. Similarly, SunOpta's operations in Ontario are strengthening domestic production, reducing reliance on imports, and supporting local sourcing initiatives. Retailers are also emphasizing Canadian-made products. Loblaw's PC Optimum app highlights Canadian dairy alternatives, while Sobeys is increasing its focus on domestic products. These initiatives enhance the competitiveness of Canadian-produced dairy alternatives, especially as rising transportation costs and sustainability concerns make local production and shorter supply chains more appealing.

Competitive Landscape

The Canadian dairy alternatives market is moderately fragmented, with multinational corporations, established dairy companies, and specialized plant-based brands competing across various strategic dimensions. Market concentration has risen due to significant capacity investments and facility conversions. Established dairy processors like Lactalis Canada are leveraging their distribution networks and manufacturing expertise to penetrate plant-based segments through dedicated facilities and new brand launches. Companies are focusing on proprietary extraction processes, protein enhancement, and sensory optimization. For example, SunOpta is investing in enzymatic oat processing to improve functionality and cost efficiency.

Vertical integration is becoming a key strategy, as manufacturers increasingly manage ingredient supply chains to ensure consistent quality and control costs. The Canadian dairy alternatives market is marked by ongoing product innovations and strategic expansions by major players. Leading companies in the market include Danone SA, Earth’s Own Food Co., SunOpta Inc., Blue Diamond Growers, and Groupe Lactalis. These companies are developing new plant-based formulations, particularly in milk alternatives such as oat, almond, and soy, while also expanding into dairy-free cheese, yogurt, and ice cream. They are demonstrating operational agility by investing in modern production facilities and adopting sustainable manufacturing practices. Strategic initiatives include forming partnerships with retailers and foodservice operators to strengthen distribution networks. Market leaders are increasing production capacities by establishing new facilities and upgrading existing plants with advanced technology. Companies are also focusing on quality certifications, organic ingredients, and non-GMO verification to meet evolving consumer demands and regulatory standards.

Opportunities exist in specialized applications such as infant nutrition, sports nutrition, and culinary ingredients, where advanced formulation capabilities are essential. Emerging disruptors are utilizing precision fermentation and cellular agriculture technologies to produce dairy compounds without animal involvement. For instance, Remilk has received Health Canada approval for its lab-grown milk proteins. Many established food companies are entering the market by acquiring or investing in plant-based specialists rather than developing capabilities internally. The Canadian Food Inspection Agency has increased quality control requirements following the 2024 Listeria outbreak, creating challenges for smaller players while benefiting companies with strong food safety systems and regulatory compliance capabilities.

Canada Dairy Alternatives Industry Leaders

-

Blue Diamond Growers

-

Danone SA

-

Groupe Lactalis

-

Earth’s Own Food Co.

-

SunOpta Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Danone North America has strengthened its plant-based portfolio by acquiring Lifeway Foods, bringing expertise in probiotic kefir and cultured dairy. This acquisition enhances Danone's technological capabilities for developing fermented plant-based products and reinforces its position in the growing functional dairy alternatives segment.

- October 2024: SunOpta introduced its Dream Oatmilk Barista to an additional 6,700 locations, following a partnership with a prominent North American coffee chain. This initiative expanded SunOpta's distribution network, enhanced brand recognition, and reinforced its presence in the institutional foodservice sector through a specialized formulation crafted for professional coffee applications.

- May 2024: Lactalis Canada introduced ‘Enjoy!’, a plant-based brand designed for Canadians. The range includes six SKUs: Unsweetened Oat, Unsweetened Oat Vanilla, Unsweetened Almond, Unsweetened Almond Vanilla, Unsweetened Hazelnut, and Unsweetened Hazelnut and Oat.

- January 2024: Oatly has introduced Unsweetened Oatmilk and Super Basic Oatmilk in North America, marking the company's first significant beverage innovation in half a decade. Aimed at health-conscious consumers who prefer minimal ingredient formulations, these products position Oatly to entice traditional dairy drinkers to make the switch to oat milk alternatives.

Canada Dairy Alternatives Market Report Scope

Non-Dairy Butter, Non-Dairy Cheese, Non-Dairy Ice Cream, Non-Dairy Milk, Non-Dairy Yogurt are covered as segments by Category. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Non-Dairy Milk | Oat Milk |

| Hemp Milk | |

| Hazelnut Milk | |

| Soy Milk | |

| Almond Milk | |

| Coconut Milk | |

| Cashew Milk | |

| Non-Dairy Cheese | |

| Non-Dairy Desserts | |

| Non-Dairy Yogurt | |

| Others |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-trade | |

| Off-trade | Convenience Stores |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

| By Product Type | Non-Dairy Milk | Oat Milk |

| Hemp Milk | ||

| Hazelnut Milk | ||

| Soy Milk | ||

| Almond Milk | ||

| Coconut Milk | ||

| Cashew Milk | ||

| Non-Dairy Cheese | ||

| Non-Dairy Desserts | ||

| Non-Dairy Yogurt | ||

| Others | ||

| Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms