China Dairy Alternatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

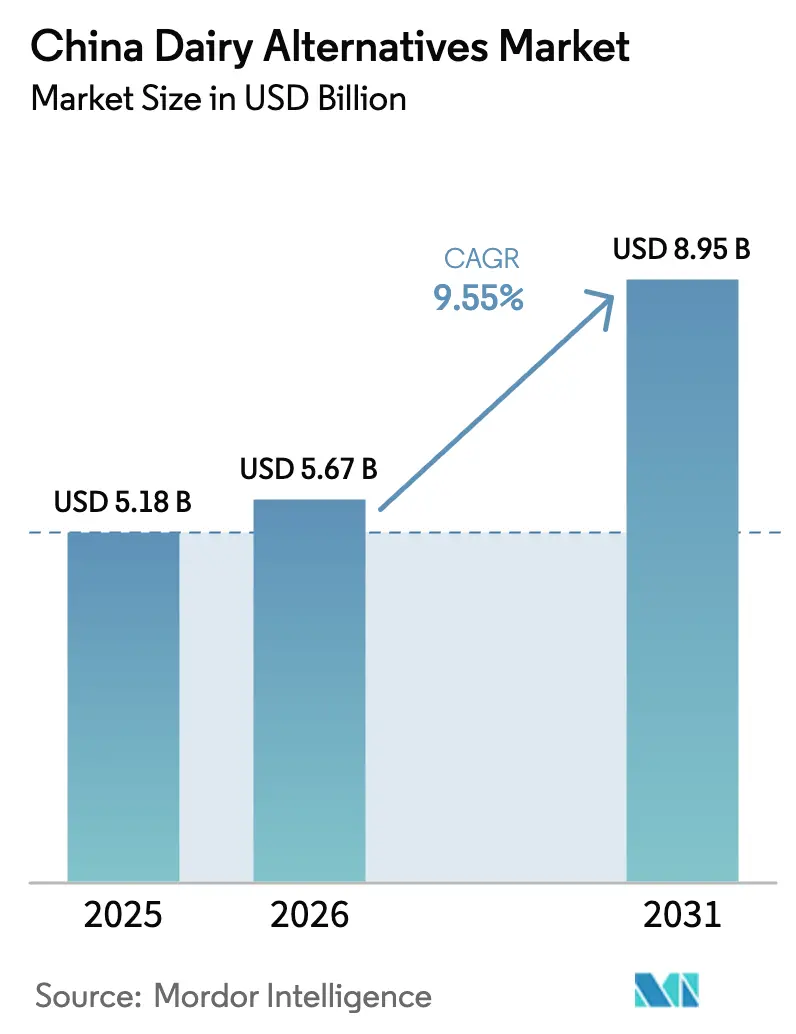

| Base Year Market Size (2025) | USD 5.18 Billion |

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 8.95 Billion |

| Growth Rate (2026 - 2031) | 9.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Dairy Alternatives Market Analysis by Mordor Intelligence

China dairy alternatives market size in 2026 is estimated at USD 5.67 billion, growing from 2025 value of USD 5.18 billion with 2031 projections showing USD 8.95 billion, growing at 9.55% CAGR over 2026-2031. Government policies actively incorporate plant-based foods into the broader "big food concept," driving sustained long-term demand. Urbanization, premiumization, and advancements in technology are actively reshaping the competitive landscape by enabling continuous product upgrades. Leading dairy companies like Yili and Mengniu are proactively expanding their brands into plant-based alternatives. However, focused innovators and new entrants are capturing market share by delivering superior taste, improved texture, and enhanced sustainability. Distribution channels are also undergoing significant transformation. Off-trade retail continues to dominate, but on-trade venues — including coffee chains and casual dining establishments — are rapidly scaling up, particularly in tier-1 cities. Younger consumers in these urban areas actively seek products that align with their lifestyle preferences, further fueling this growth.

Key Report Takeaways

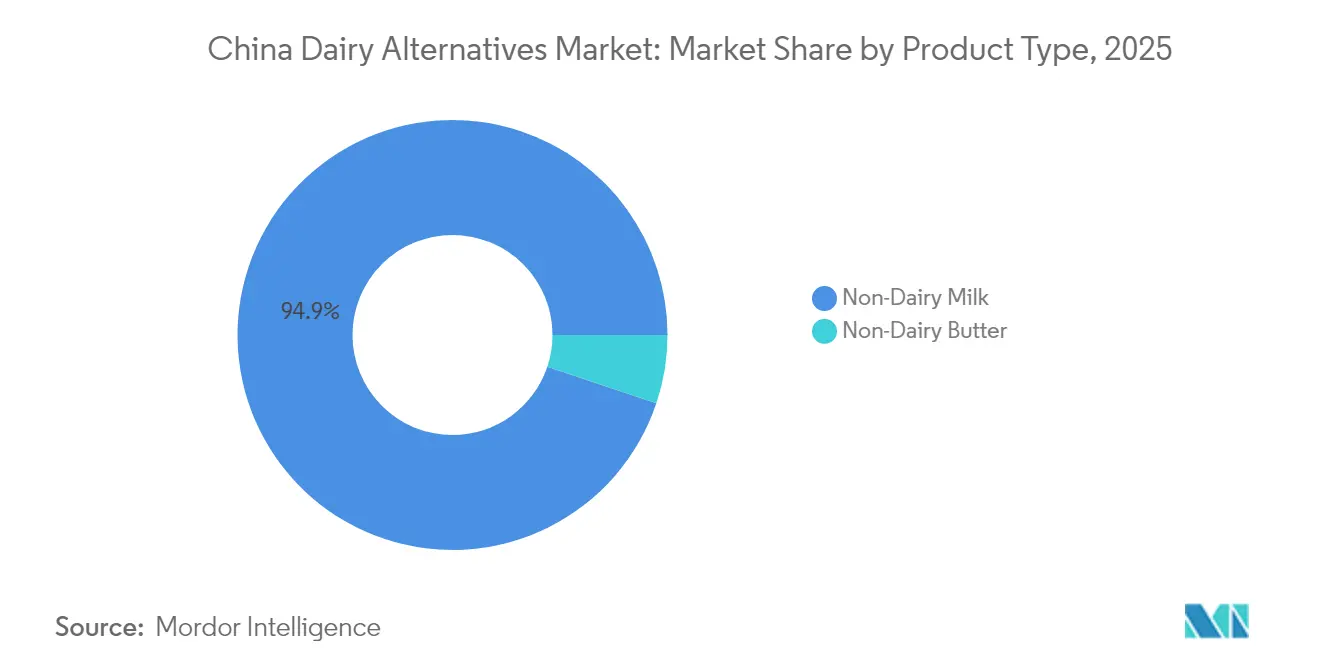

- By product type, non-dairy milk led with 94.85% revenue share of the China dairy alternatives market in 2025; non-dairy butter is projected to expand at a 10.05% CAGR to 2031.

- By source, soy commanded 60.78% share of the China dairy alternatives market size in 2025, while almond alternatives are advancing at a 9.89% CAGR through 2031.

- By packaging, cartons accounted for 56.65% share of the China dairy alternatives market size in 2025 and plastic bottles are rising at a 9.98% CAGR through 2031.

- By flavor, unflavored products captured 68.97% of China dairy alternatives market share in 2025; flavored variants are growing at an 10.72% CAGR to 2031.

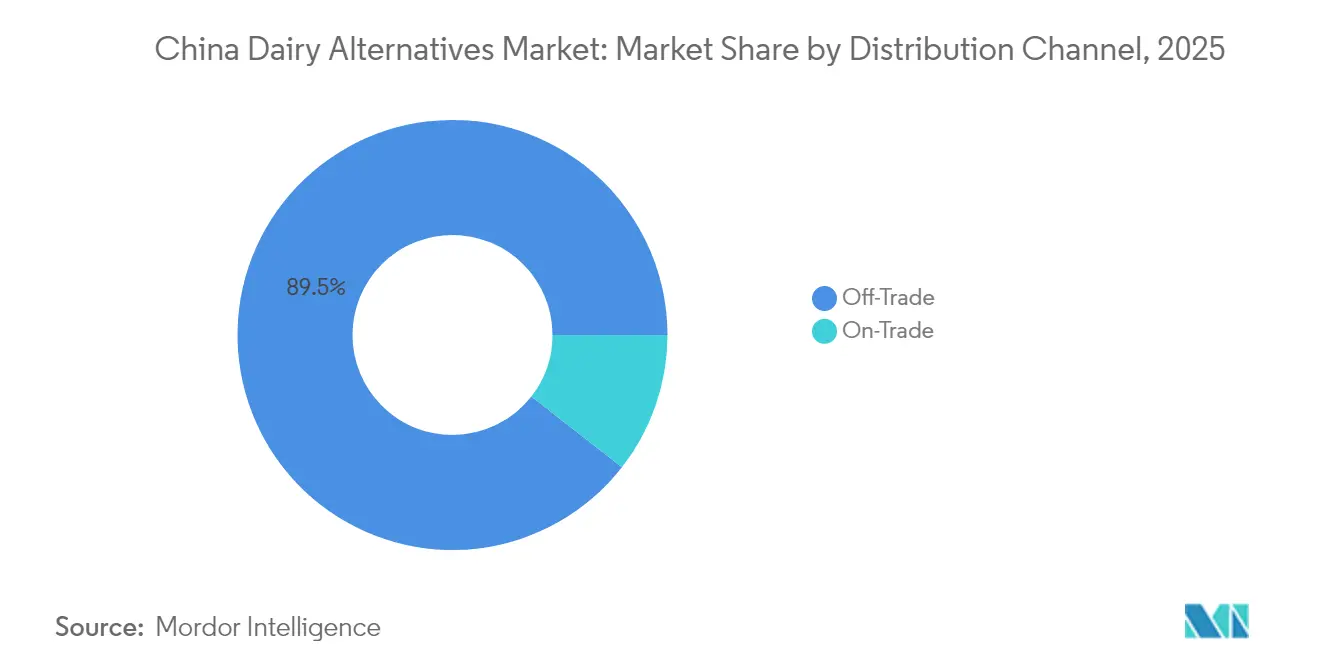

- By distribution channel, off-trade outlets held 89.45% of China dairy alternatives market share in 2025, whereas on-trade sales are climbing at a 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Dairy Alternatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of lactose intolerance among Chinese adult population | +2.8% | National, concentrated in Han-majority regions | Long term (≥ 4 years) |

| Growing health consciousness and demand for plant-based alternatives | +2.1% | Tier-1 and Tier-2 cities, expanding to lower tiers | Medium term (2-4 years) |

| Expanding vegan and vegetarian population influenced by Western culture | +1.4% | Urban coastal regions, Beijing-Shanghai-Shenzhen corridor | Medium term (2-4 years) |

| Continuous innovation improving taste, texture, and nutrition | +1.9% | National, with research and development concentrated in eastern provinces | Short term (≤ 2 years) |

| Rising consumer concerns for animal welfare and ethical consumption | +0.8% | Urban millennials and Gen-Z demographics nationwide | Long term (≥ 4 years) |

| Government initiatives promoting sustainable agriculture and food security | +1.2% | National policy implementation, regional pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High prevalence of lactose intolerance among the Chinese adult population

In China, a significant portion of the adult population grapples with lactose intolerance, propelling the country's dairy alternatives market. Many consumers, facing digestive issues with traditional dairy, are increasingly turning to plant-based alternatives like soy, oat, almond, and coconut products. A 2023 report from the National Institute of Health highlights that around 40% of neonates in China are lactose intolerant, representing 12–30% of all affected children [1]Source: National Institute of Health, "Awareness about Neonatal Lactose Intolerance among Chinese Neonatologists in Outpatient Settings: A Multi-Center Survey", www.pmc.ncbi.nlm.nih.gov. This underscores a pronounced genetic and early-life sensitivity to dairy, which persists into adulthood for many individuals. Coupled with heightened health awareness, changing dietary preferences, and advancements in product taste and nutritional profiles, this widespread intolerance is driving a swift embrace of dairy alternatives in both retail and foodservice sectors nationwide. The growing availability of these alternatives across various price points and formats further supports their adoption among diverse consumer groups.

Growing health consciousness and increasing demand for plant-based, nutritious dairy substitutes

Growing health consciousness among Chinese consumers has emerged as a key driver boosting demand for plant-based, nutritious dairy substitutes. With rising awareness of the health implications associated with excessive dairy intake, including lactose intolerance, cholesterol concerns, and digestive discomfort, consumers are increasingly seeking healthier, natural, and easily digestible alternatives. Plant-based beverages and products derived from soy, oats, almonds, and coconuts are being perceived as rich sources of fiber, protein, and essential micronutrients, aligning with the country's broader shift toward preventive health and sustainable nutrition. The popularity of vegan and flexitarian diets, amplified by social media and wellness influencers, has further accelerated the acceptance of these products. Manufacturers are also responding with innovations in taste, texture, and nutrient fortification, reinforcing consumer perception of dairy alternatives as both a health-enhancing and lifestyle-compatible choice.

Expanding vegan and vegetarian population influenced by Western culture

The expanding vegan and vegetarian population in China, strongly influenced by Western dietary trends and lifestyle habits, is a major driver of the country’s dairy alternatives market. Younger urban consumers are increasingly embracing plant-based diets inspired by global wellness movements, ethical consumption, and sustainability values. According to the World Animal Foundation, about 3.6% of the Chinese population identifies as vegetarian, reflecting a steady rise in plant-forward nutritional preferences and the growing mainstream appeal of dairy-free living [2]Source: World Animal Foundation, "Vegetarian Statistics 2025: Global Facts, Diet Trends & Market Growth", www.worldanimalfoundation.org. This shift has been fueled by exposure to Western culture through travel, digital platforms, and international brand influence, which has made plant-based milk, yogurt, and other alternatives more desirable. As cafés, restaurants, and retail chains diversify their menus and product assortments, the adoption of these plant-based substitutes continues to move beyond niche segments toward a broader health-conscious consumer base across China.

Continuous innovation in dairy alternatives improving taste, texture, and nutrition

Continuous innovation in dairy alternatives is significantly enhancing product taste, texture, and nutritional value, driving strong growth in China’s dairy alternatives market. Manufacturers are investing heavily in research and development to improve the sensory appeal of plant-based products and reduce the taste gap between traditional dairy and its substitutes. Advancements in food processing technologies, fermentation techniques, and ingredient blending are enabling the creation of smoother, creamier, and more nutrient-rich alternatives made from soy, oats, almonds, coconuts, and peas. These innovations not only cater to the increasing demand for lactose-free and vegan products but also address consumer expectations for high-quality, protein-rich, and fortified options with added vitamins and minerals. As a result, evolving product quality and diversification are attracting a wider audience—from health-conscious consumers to mainstream dairy users—fueling sustained market expansion across retail and foodservice channels in China.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price premium compared to traditional dairy products | -1.8% | National, most pronounced in lower-tier cities and rural areas | Medium term (2-4 years) |

| Taste and texture preferences inhibiting acceptance | -1.2% | National, varying by age demographics and regional preferences | Short term (≤ 2 years) |

| Regulatory uncertainties and evolving food safety standards | -0.9% | National regulatory framework, provincial implementation variations | Medium term (2-4 years) |

| Limited awareness and availability in lower-tier cities and rural areas | -1.4% | Tier-3 cities and rural regions, cold-chain infrastructure gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher price premium of dairy alternatives compared to traditional dairy products

Price premiums for dairy alternatives, averaging 50-100% above conventional dairy, pose significant adoption challenges. This is especially true in price-sensitive segments, where these alternatives vie directly with subsidized domestic milk. Costs for specialized ingredients, such as oat protein and almond processing, outstrip those of traditional dairy inputs. Furthermore, smaller production scales hinder the economies of scale that could otherwise bridge this cost gap. Manufacturers face added pricing volatility due to import dependencies on certain ingredients, making them susceptible to currency fluctuations and shifts in trade policies. This volatility complicates long-term market positioning. The pricing paradox is even more pronounced in rural markets. Here, despite constrained disposable incomes, the prevalence of high lactose intolerance makes these regions the largest untapped consumer base. Since August 2021, a domestic oversupply in conventional dairy markets has led to a 14.38% drop in raw milk prices. This decline has widened the cost gap, rendering alternatives even pricier by comparison [3]Source: United States Department of Agriculture," China: Dairy and Products Semi-annual", www.fas.usda.gov.

Taste and texture preferences inhibiting acceptance

Taste and texture preferences continue to pose a restraint to the growth of the dairy alternatives market in China. While product innovation has improved significantly, many consumers still find the flavor profiles and mouthfeel of plant-based milks and yogurts less appealing compared to traditional dairy. Variations in texture—such as a thinner consistency or slight aftertaste—often deter repeat purchases, especially among consumers who prioritize the creamy and rich characteristics of conventional dairy products. Moreover, localized taste preferences in China, where dairy is often consumed in sweetened beverages and desserts, create an additional challenge for plant-based formulations to match traditional sensory expectations. Overcoming these barriers will require sustained innovation in formulation and flavor enhancement to better align with Chinese consumer palates and build stronger long-term acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Dairy Milk Dominance Faces Butter Innovation

Non-dairy milk accounted for a substantial 94.85% market share in China’s dairy alternatives sector in 2025, positioning it as the dominant category and core driver of the market’s overall expansion. Its leadership reflects strong consumer familiarity with liquid milk formats, which easily substitute for traditional dairy in everyday applications such as breakfast beverages, coffee, and culinary uses. The seamless integration of non-dairy milk into Chinese households and foodservice menus underscores its role as the primary entry point for consumers shifting away from animal-based dairy. The segment further benefits from continuous innovation in flavor, texture, and nutritional fortification, especially in soy and oat-based variants, which enhance versatility across consumer segments. Marketing efforts emphasizing health benefits, lactose-free attributes, and environmental sustainability also reinforce consumer loyalty and repeat purchases.

Non-dairy butter represents the fastest-growing segment in China’s dairy alternatives market, projected to expand at a CAGR of 10.05% through 2031. Its rapid ascension is primarily supported by the evolving bakery, confectionery, and foodservice industries that increasingly favor plant-based formulations with reliable functional performance. Unlike liquid milk substitutes, the purchase drivers in this category center on texture, spreadability, and baking stability—criteria that align with both professional and household culinary needs. Manufacturers are innovating with coconut, cashew, and blended vegetable oil bases to deliver buttery richness and stability under varying cooking conditions. The segment’s growth also aligns with heightened awareness of cholesterol-free and vegan lifestyle trends among urban consumers seeking cleaner ingredient labels.

By Source: Soy Leadership Challenged by Almond Innovation

Soy-based products dominate China’s dairy alternatives market with a commanding 60.78% share in 2025, sustained by decades of consumer trust and strong integration into traditional dietary habits. The segment’s leadership reflects deep cultural familiarity with soy milk beverages and related applications, which have long served as staple components of Chinese breakfast and household consumption. This enduring acceptance has translated into stable demand, supported by a mature domestic supply chain that continuously ensures availability, cost efficiency, and quality consistency. Local soybean cultivation capacity provides supply assurance and contributes to price stability that reinforces its position in both mass-market and institutional channels. Moreover, extensive retail penetration and continuous innovation in flavor, packaging, and nutritional formulations have helped soy-based products maintain broad accessibility across income tiers.

Almond-based dairy alternatives form the fastest-growing category in the Chinese market, forecast to expand at a CAGR of 9.89% through 2031. This strong growth trajectory highlights evolving consumer preferences for products that convey premium quality and milder taste profiles distinct from traditional soy offerings. Almond milk resonates particularly well with younger, health-conscious, and urban demographics valuing natural ingredients and perceived digestibility advantages. Producers are leveraging imported almond sources and advanced processing technologies to enhance smoothness and richness, elevating its appeal in both retail and foodservice channels. The segment is also gaining traction through diversified flavor innovations and fortified blends targeting functional nutrition and lifestyle positioning.

By Packaging Type: Carton Convenience Meets Plastic Innovation

Carton packaging accounted for the largest share of 56.65% in China’s dairy alternatives market in 2025, supported by its strong association with convenience, reliability, and product safety. The dominance of this format stems from established distribution networks and consumer trust built around UHT-processed beverages that allow long shelf life and ambient storage. Cartons continue to be the preferred packaging solution for non-dairy milk due to their cost-effectiveness, lightweight design, and compatibility with large-scale manufacturing. Domestic producers also benefit from mature filling infrastructure and standardized supply chains that facilitate efficient nationwide logistics. The format’s eco-friendly perception and recyclability further enhance its acceptance amid growing consumer awareness of sustainable packaging.

Plastic bottles represent the fastest-growing packaging format, projected to expand at a CAGR of 9.98% through 2031, reflecting the influence of convenience and premiumization in China’s evolving beverage sector. This segment’s appeal lies in its resealability, portability, and suitability for chilled, ready-to-drink versions of dairy alternatives that fit modern, on-the-go lifestyles. Brands are increasingly using clear plastic bottles to emphasize product freshness, flavor innovations, and premium positioning through transparent presentation. The category also benefits from consumer preference for portion-controlled packaging that aligns with individual consumption habits in urban settings. Manufacturers leverage high-quality PET materials and ergonomic designs to enhance shelf visibility and functional performance while maintaining recyclability.

By Flavor: Unflavored Preference Shifts Toward Variety

Unflavored dairy alternatives held a dominant 68.97% market share in China in 2025, underscoring consumers’ strong preference for neutral-tasting products that offer broad versatility across culinary and beverage applications. This segment’s leadership is attributed to the widespread use of non-dairy milk and other substitutes in cooking, baking, and tea or coffee preparation, where added flavors could alter intended taste profiles. The appeal of unflavored options lies in their adaptability—they serve as foundational ingredients suitable for both household and foodservice consumption. Manufacturers continue to refine texture, mouthfeel, and nutritional consistency to ensure that unflavored variants perform well in recipes while meeting health expectations. The segment benefits from strong distribution presence and high repeat purchase rates due to its utility-oriented positioning.

Flavored dairy alternatives represent the fastest-growing segment in the Chinese market, projected to rise at a CAGR of 10.72% through 2031 as consumers increasingly seek variety, indulgence, and experiential taste profiles. This growth is largely driven by younger demographics and urban consumers who associate plant-based drinks with modern, lifestyle-oriented beverage choices. Flavored variants—ranging from chocolate and vanilla to regional fruit-based blends—are gaining traction in ready-to-drink and snacking formats that emphasize convenience and enjoyment. Brands are leveraging innovative formulations, reduced-sugar options, and functional fortifications to enhance appeal while differentiating themselves from traditional soy and oat benchmarks. The rise of café-inspired flavors and localized taste adaptations further accelerates expansion within on-the-go channels.

By Distribution Channel: Off-Trade Dominance Faces Foodservice Growth

Off-trade channels accounted for a commanding 89.45% market share in China’s dairy alternatives market in 2025, underscoring the central role of retail accessibility in category expansion. Supermarkets, hypermarkets, and convenience stores continue to dominate distribution as they provide visibility and availability for consumers exploring plant-based options. The extensive presence of dairy alternative products on retail shelves supports consumer education through packaging, in-store displays, and promotional sampling. Off-trade growth is further reinforced by e-commerce platforms, which enhance reach and affordability, particularly among younger consumers seeking variety and convenience. The dominance of this channel also reflects purchasing habits shaped around at-home consumption, where consumers feel more comfortable experimenting with unfamiliar dairy-free products.

On-trade channels represent the fastest-growing segment, projected to expand at a CAGR of 10.12% through 2031, as dining and beverage establishments increasingly adopt plant-based offerings. Coffee shops, cafés, and restaurants are becoming key partners in familiarizing consumers with dairy alternatives through practical, taste-driven applications. This channel plays an important educational role—allowing consumers to experience soy, oat, or almond milk in professionally prepared beverages and menu items before purchasing for home use. Premium coffee chains and quick-service restaurants are also leveraging plant-based options to signal sustainability and inclusivity, appealing to health-conscious and flexitarian consumers. The visibility of dairy alternatives in foodservice environments fosters trial, builds trust, and elevates perceived quality and taste.

Geography Analysis

China's dairy alternatives market showcases distinct regional variations, shaped by urbanization, income disparities, and infrastructure development. In tier-1 cities like Beijing, Shanghai, Guangzhou, and Shenzhen, adoption rates soar above 25% among target demographics. This surge is bolstered by advanced cold-chain networks and heightened consumer awareness. These major cities enjoy the backing of international brands and foodservice channels, seamlessly integrating plant-based options into familiar settings such as coffee shops and Western eateries. With income levels in these tier-1 markets justifying premium pricing, there's also a cultural receptiveness to foreign food concepts, easing the path for new trials.

Meanwhile, tier-2 and tier-3 cities, boasting a combined population exceeding 400 million, present a significant growth frontier. As disposable incomes in these regions inch closer to thresholds for premium food product adoption, the potential is evident. Yet, challenges loom: a nascent cold-chain infrastructure and evolving retail sophistication hinder product availability and quality assurance. In rural markets, despite a pronounced lactose intolerance prevalence, penetration remains elusive. Here, price sensitivity, limited awareness, and infrastructural shortcomings pose formidable barriers. Yet, with government-backed rural modernization and e-commerce initiatives, market access is on the rise. Coupled with an expansion in domestic production, there's potential for cost reductions, paving the way to tap into these price-sensitive segments.

Regional taste nuances play a pivotal role in shaping product development and determining market success. Northern consumers in China lean towards bolder flavors, while their southern counterparts favor subtler profiles. Coastal areas, with a heightened environmental awareness, are more inclined to pay a premium for sustainable offerings. In contrast, inland regions emphasize functional benefits and value. Brands chart their geographic expansion in tandem with established FMCG distribution routes, capitalizing on existing partnerships and logistics to navigate the diverse regional landscape efficiently.

Competitive Landscape

In the China dairy alternatives market, a concentration index of 4 out of 10 indicates a moderate level of fragmentation. This market is characterized by the presence of established dairy giants, niche plant-based entrants, and global brands, each competing for distinct strategic positions. Traditional dairy leaders such as Yili and Mengniu leverage their extensive distribution networks and strong brand recognition to secure market share. These companies focus on expanding their portfolios through line extensions and acquisitions, enabling them to diversify their offerings and cater to evolving consumer preferences. Their ability to capitalize on existing infrastructure and consumer trust provides them with a competitive edge in the market.

Pure-play alternatives companies, which are solely dedicated to plant-based products, prioritize innovation and premium positioning to differentiate themselves. These companies focus on developing unique product offerings that appeal to health-conscious and environmentally aware consumers. By emphasizing product innovation, such as introducing new flavors, improving nutritional profiles, and enhancing product quality, they aim to carve out a niche in the competitive landscape. Their strategies are designed to meet the growing demand for sustainable and plant-based alternatives, setting them apart from traditional dairy producers.

International brands like Oatly, Vitasoy, and Danone's Alpro division bring advanced technical expertise and global best practices to the Chinese market. These companies introduce innovative technologies and processes, which help elevate product quality and meet international standards. However, they face significant challenges in localization, such as adapting to local tastes and preferences, as well as managing cost pressures, which limit their ability to penetrate the mass market effectively. Additionally, leaders in the sector are driving competitive differentiation through technology adoption, investing in proprietary processing methods, flavor masking innovations, and nutritional fortification. These advancements enable them to establish sustainable advantages over traditional commodity producers and strengthen their market position.

China Dairy Alternatives Industry Leaders

-

Hebei Yangyuan Zhihui Beverage Co. Ltd

-

Vitasoy International Holdings Ltd

-

Danone S.A.

-

Mengniu Dairy Company Limited

-

Inner Mongolia Yili Industrial Group Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Mengniu has committed to reducing its environmental footprint by implementing eco-friendly practices across its supply chain, including sustainable sourcing of raw materials, water conservation, and waste management. The company aims to enhance animal welfare standards and shift towards plant-based alternatives to meet the growing consumer demand for eco-conscious products.

- July 2023: Sweden's Veg of Lund has introduced three varieties of its potato-based milk alternative, DUG, in China: Original, Unsweetened, and Barista. This launch marks the company's entry into the Chinese market, aiming to cater to the growing demand for plant-based milk alternatives.

- September 2022: Vitasoy introduced a new product line, Vitasoy Plant+, to its plant milk portfolio. The new product line comprises almond milk and oat milk made from 100% almonds and oats, respectively.

China Dairy Alternatives Market Report Scope

Non-Dairy Butter, Non-Dairy Milk are covered as segments by Category. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Non-Dairy Butter | |

| Non-Dairy Milk | Almond Milk |

| Coconut Milk | |

| Oat Milk | |

| Soy Milk |

| Soy |

| Almond |

| Oat |

| Rice |

| Others |

| Flavored |

| Unflavored |

| Cartons |

| Plastic Bottle |

| Glass Bottle |

| Others (Tetrapacks, Pouches) |

| Off-Trade | Convenience Stores |

| Online Retail | |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| Others | |

| On-Trade |

| By Product Type | Non-Dairy Butter | |

| Non-Dairy Milk | Almond Milk | |

| Coconut Milk | ||

| Oat Milk | ||

| Soy Milk | ||

| By Source | Soy | |

| Almond | ||

| Oat | ||

| Rice | ||

| Others | ||

| Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | Cartons | |

| Plastic Bottle | ||

| Glass Bottle | ||

| Others (Tetrapacks, Pouches) | ||

| By Distribution Channel | Off-Trade | Convenience Stores |

| Online Retail | ||

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| Others | ||

| On-Trade | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms