Campus Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.19 Billion |

| Market Size (2031) | USD 18.05 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

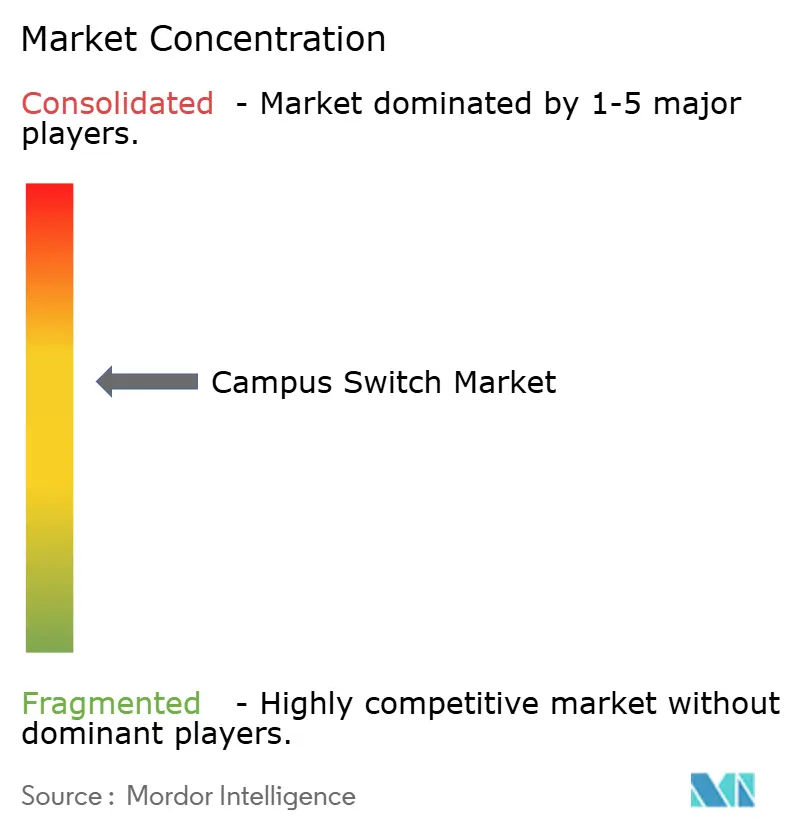

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Campus Switch Market Analysis by Mordor Intelligence

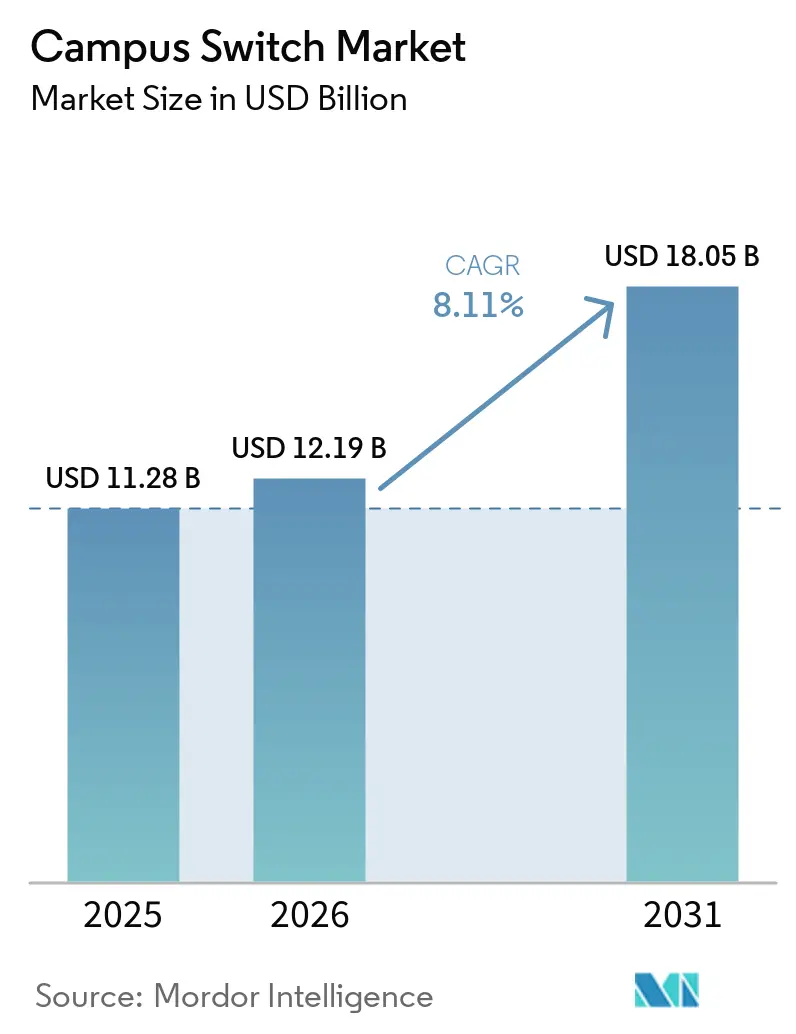

The campus switch market size is projected to grow from USD 11.28 billion in 2025 to USD 12.19 billion in 2026 and is forecast to reach USD 18.05 billion by 2031 at a CAGR of 8.1% from 2026 to 2031. Demand is accelerating as Wi-Fi 7 backhaul requirements outstrip gigabit uplinks, power-over-Ethernet (PoE++) endpoints multiply across smart campuses, and open networking software such as SONiC erodes the vendor lock-in that once prolonged refresh cycles. Vendors that embed artificial-intelligence operations into switching silicon capture margin even as average selling prices at the edge compress. Meanwhile, merger activity, most notably the USD 14 billion merger of Hewlett Packard Enterprise and Juniper Networks, is reshaping channel relationships and creating opportunities for pure-play disaggregated hardware suppliers. Against this backdrop, the campus switch market is evolving from a commodity hardware segment into a strategic platform for edge compute, security, and energy optimization.

Key Report Takeaways

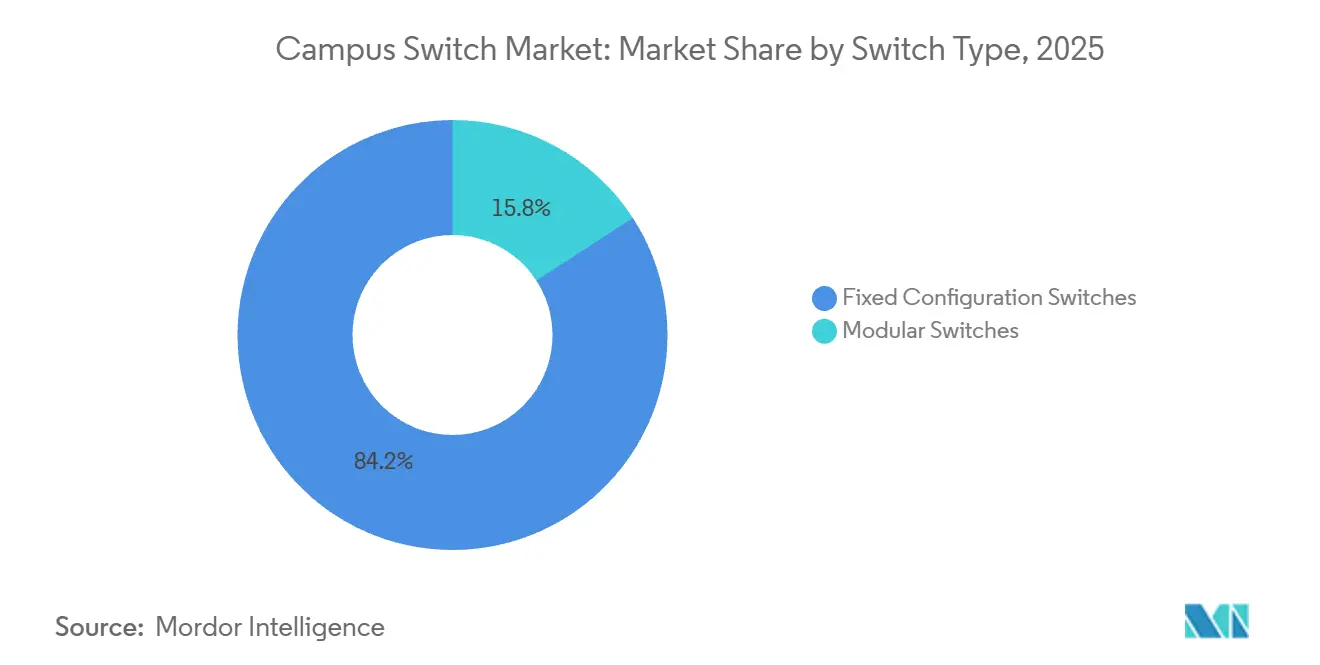

- By switch type, fixed configuration switches held 84.16% of the campus switch market revenue share in 2025, while modular systems are forecast to expand at a 9.72% CAGR through 2031.

- By port speed, 1 GbE and below retained 44.82% of campus switch market share in 2025, but 2.5/5 GbE multi-gig interfaces are projected to grow at a 12.48% CAGR, the fastest of any speed tier.

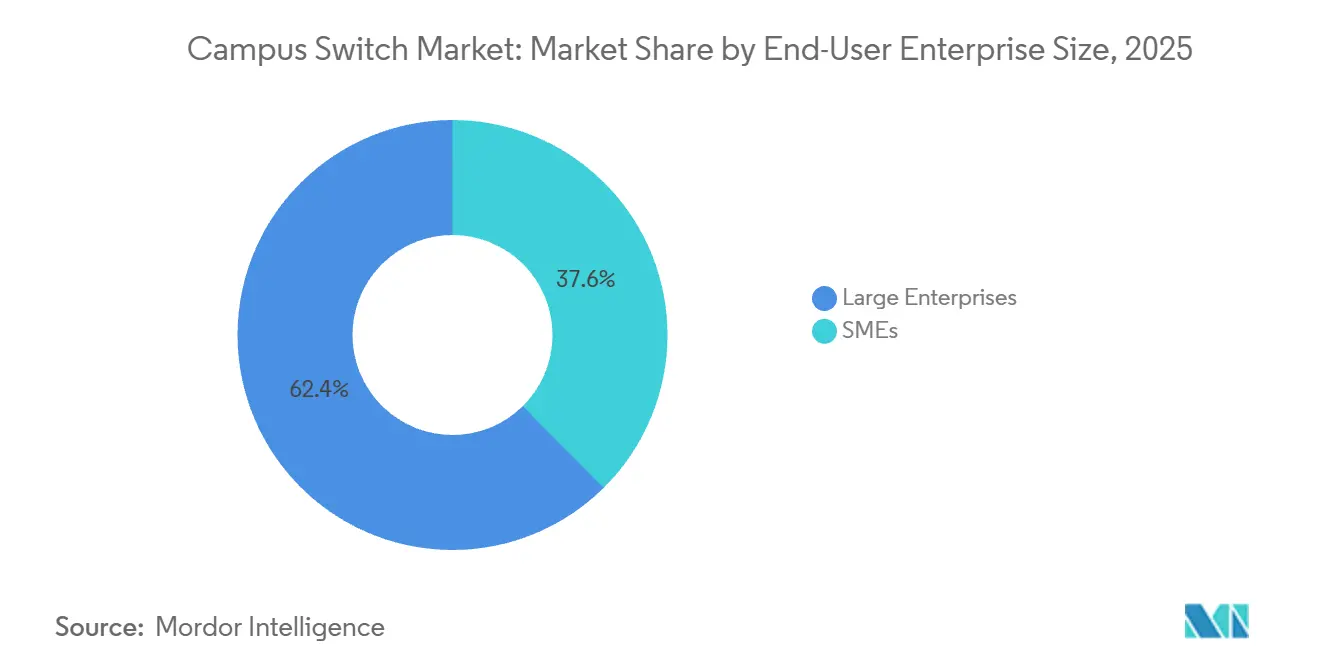

- By end-user enterprise size, large enterprises accounted for 62.40% of spending in 2025, whereas SMEs are set to grow at an 8.94% CAGR as cloud management reduces the total cost of ownership.

- By end-user industry, enterprise and corporate campuses led with 38.42% of 2025 revenue, yet education is expected to post an 8.88% CAGR under digital-equity mandates.

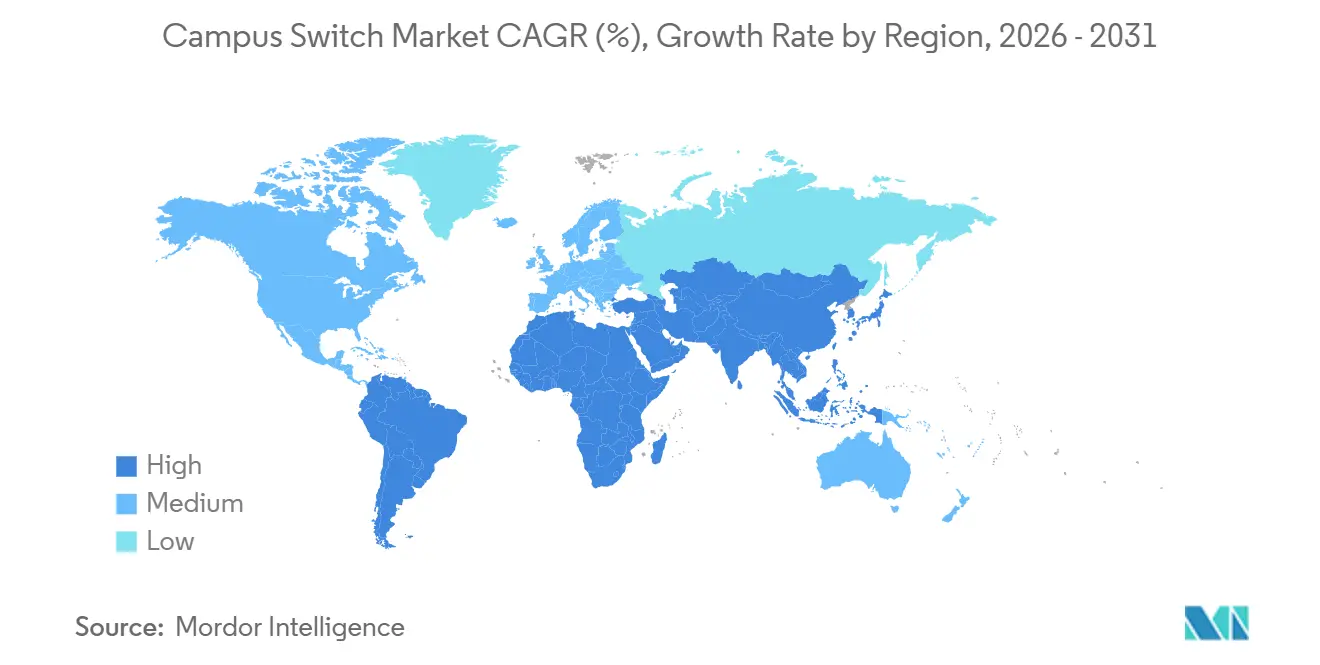

- By geography, North America contributed 37.82% of 2025 revenue, while Asia-Pacific is on track for a 9.68% CAGR, the highest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Campus Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Expansion of Wi-Fi 6/6E and Wi-Fi 7 Adoption | +2.10% | Global, with early density in North America and Asia-Pacific | Medium term (2-4 years) | |

| Growth in Smart Campus and EdTech Investments | +1.80% | North America, Europe, Asia-Pacific | Medium term (2-4 years) | |

| Rising Data Traffic per Student and Staff Device | +1.50% | Global | Long term (≥ 4 years) | |

| Surge in PoE-Powered IoT Edge Devices on Campuses | +1.30% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) | |

| Increasing Campus Cyber-Resilience Requirements | +0.90% | Global, regulatory influence in North America and Europe | Medium term (2-4 years) | |

| Vendor Neutral Open-Networking Push (SONiC, NOS Disaggregation) | +0.70% | North America, Europe, emerging in Asia-Pacific | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Expansion of Wi-Fi 6/6E and Wi-Fi 7 Adoption

Wi-Fi 7’s 320 MHz channels deliver headline throughput above 40 Gbps, exposing access-layer bottlenecks wherever legacy gigabit switching persists. Georgetown University upgraded to Catalyst 9000 switches with 2.5/5 GbE ports in 2025 to remove that choke point. Hewlett Packard Enterprise reports that 60% of new Aruba 730 series access points now ship with multi-gig switches, underscoring that the wired backhaul must keep pace with wireless capacity. Huawei’s 2025 fiber-to-the-office project at Hubei University pairs Wi-Fi 7 radios with XGS-PON Pro+ to deliver 10 Gbps of edge bandwidth.[1]Huawei, “Hubei University FTTO XGS-PON Pro+ Deployment,” carrier.huawei.com As more campuses emulate these examples, demand cascades from access-layer multi-gig ports to 400 Gbps spines that aggregate hundreds of high-speed uplinks. The campus switch market, therefore, gains a durable growth engine that extends well beyond the initial Wi-Fi 7 refresh cycle.

Growth in Smart Campus and EdTech Investments

Generative AI, immersive learning, and converged building controls all ride on wired infrastructure that can enforce quality of service and deliver PoE power budgets measured in kilowatts. University of Colorado Boulder’s ChatGPT Edu launch in 2024 drove daily peak traffic to 10 Tb across the core, forcing emergency upgrades to 400 Gbps spines.[2]University of Colorado Boulder, “CU Boulder Launches ChatGPT Edu,” colorado.edu Birmingham City University’s digital-transformation program required PoE++ to run high-definition cameras and IoT sensors in every classroom, highlighting that modern pedagogy intertwines with switching capabilities. Adelphi University’s 2025 multi-gig refresh aligns with hybrid learning models that stream 4K video to on-campus and remote students. These projects share the thesis that network fabric quality increasingly influences student experience and institutional competitiveness, which, in turn, fuels incremental switch spending even in fiscally cautious environments.

Rising Data Traffic per Student and Staff Device

SINET6 upgraded to 400 Gbps links in 2025 to serve 900 Japanese universities, following a 40% year-over-year increase in inter-campus traffic. At the University of Tokyo, telemetry from 7,600 Mist-managed access points showed median per-device upstream traffic of 12 GB per day, demanding distribution-layer upgrades to sustain line-rate throughput. Bangladesh’s BRAC University provisioned every student with 1 Gbps symmetric internet on top of a Huawei 10 Gbps backbone, illustrating that even emerging-market campuses can leap to high-capacity fabrics. As device counts and cloud sync volumes climb, oversubscription models that once amortized switch investments collapse, accelerating refresh cycles toward multi-gig and 10 Gbps access.

Surge in PoE-Powered IoT Edge Devices on Campuses

IEEE 802.3bt’s 90-watt envelope enables a new class of edge hardware, pan-tilt-zoom cameras, 8K signage, and environmental sensors that rely on the switch for both power and data. Aoyama Gakuin University’s plan to deploy 3,000 PoE-enabled access points by 2029 underscores how power budget now ranks alongside port count in procurement. Arista’s ruggedized 710HXP series extends PoE++ outdoors for stadium lighting and parking-lot surveillance. In March 2026, Hitachi and the University of Technology Sydney launched an energy-efficiency pilot using PoE-powered occupancy sensors to trim HVAC energy use by 20%. These implementations show why shipments of higher-wattage switch models are outpacing shipments of base-class PoE switches, further lifting campus switch market demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budgetary Constraints in Public Educational Institutions | -1.20% | North America, Europe, emerging in South America | Medium term (2-4 years) |

| Lengthy Cap-Ex Refresh Cycles (7-10 Years) | -0.90% | Global, pronounced in public sector | Long term (≥ 4 years) |

| Skills Shortage in Network Automation and SDN | -0.60% | Global | Medium term (2-4 years) |

| Supply-Chain Volatility for ASICs and Optics | -0.50% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Budgetary Constraints in Public Educational Institutions

OECD data show that real per-student tertiary spending fell 3% between 2023 and 2024, squeezing discretionary budgets for IT upgrades. California cut community-college funding by USD 500 million for fiscal 2025-2026, prompting districts to extend the service life of decade-old switches rather than adopt multi-gig platforms.[3]State of California, “2025-2026 State Budget,” ebudget.ca.gov World Bank figures indicate that lower-income countries now devote under 10% of education outlays to digital infrastructure. The result is a bifurcation: well-endowed private universities advance refresh cycles, while public institutions defer, dampening unit shipments even as the installed base ages.

Lengthy Cap-Ex Refresh Cycles (7-10 Years)

Campus switches funded by municipal bonds or operating grants often stay in production for a full decade. Hardware purchased in 2016, when gigabit uplinks sufficed, remains under maintenance contracts today, slowing migration to multi-gig. Institutions lacking automation skills perceive open networking as risky and instead negotiate support extensions for legacy platforms. Deferred upgrades impose hidden costs: when 400 Gbps and terabit-class ASICs become baseline after 2030, residual value on gigabit hardware will be zero, forcing a sudden, expensive cut-over rather than phased line-card swaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Type: Modular Growth Aligns with Pay-As-You-Grow Strategies

Fixed Configuration Switches held 84.16% of the campus switch market share in 2025. Fixed configuration switches will still dominate access closets through 2031 because K-12 and branch offices rarely exceed 48 ports per rack. Stacking options, such as Cisco Catalyst 9300, allow logical aggregation of up to 8 units, offering some scale without chassis complexity. However, stacking cables introduces single-point failure domains that modular backplanes avoid, a nuance increasingly acknowledged in technical evaluations. Consequently, procurement teams at flagship universities specify chassis for distribution and core layers while retaining fixed models at the edge, a hybrid approach that tempers absolute displacement but sustains modular growth momentum.

Modular switches captured a modest slice of revenue in 2025 but are forecast to grow 9.72% annually through 2031, outstripping the broader campus switch market. Institutions with tens of thousands of endpoints can install a partially populated chassis and scale line cards as enrollment or IoT density increases, thereby improving return on invested capital. Juniper’s QFX5250 delivers 102.4 Tbps in a 16-slot frame, yet administrators can light only the ports they need, reducing upfront cash outlay. Extreme Networks’ 7830 likewise supports future 800 Gbps optics without requiring a chassis replacement. In contrast, fixed configuration models remain popular in SMEs, where simplicity and rapid deployment matter more than slot flexibility.

By Port Speed: Multi-Gig Interfaces Eclipse Legacy Gigabit

In 2025, 1 GbE and slower ports held 44.82% of shipments, but their share is sliding as Wi-Fi 6E and Wi-Fi 7 saturate gigabit uplinks. The 2.5/5 GbE multi-gig tier is projected to expand 12.48% annually, the fastest of any speed class, lifting the overall campus switch market size for access-layer hardware. Juniper’s EX4000 delivers multi-gig and PoE++ across every port, enabling institutions to standardize on a single SKU from the closet to the core.[4]Juniper Networks, “EX4000 Series Switches Overview,” juniper.net Arista’s fanless 710XP caters to noise-sensitive libraries and small classrooms, underscoring that multi-gig is no longer a premium feature.

Ten-gigabit ports remain relevant for server uplinks, while 25/40 GbE remain mostly confined to data-center leaf roles. Demand for 100/400 Gbps aggregation climbs in absolute terms because spines must funnel hundreds of multi-gig flows upstream, but their share within the campus switch market remains modest. By 2028, gigabit ports are expected to serve voice handsets and legacy sensors, whereas multi-gigabit becomes the default across new construction and major renovations, changing the mix of power budgets, cooling requirements, and price bands that vendors must target.

By End-User Enterprise Size: Cloud Management Accelerates SME Adoption

Large enterprises accounted for 62.40% of 2025 revenue, reflecting their scale and compliance obligations, yet SME spending grows nearly in lockstep with the total campus switch market because cloud dashboards erase the need for on-premises controllers. Arista’s SaaS edition of CloudVision is priced at USD 10 per device per month, converting capital outlay to operating expense for organizations with limited cash reserves. Ubiquiti and TP-Link compete aggressively with subscription-free offerings that undercut enterprise-class SKUs by up to 60%, broadening access to managed switching features.

SMEs are on course for an 8.94% CAGR in the campus switch market and benefit from disaggregated hardware. This price-performance dynamic narrows the capability gap between a 200-employee firm and a Fortune 500 headquarters. Meanwhile, large enterprises continue to favor hybrid management modes that satisfy data-residency mandates, which sustains their absolute spending lead even as SME growth outpaces it.

By End-User Industry: Education Funding Propels Infrastructure Refresh

Enterprise and corporate campuses delivered 38.42% of 2025 revenue, but growth moderates as many offices completed major upgrades during the pandemic. The education vertical, by contrast, is on course for an 8.88% CAGR, energizing the campus switch market under federal digital-equity initiatives such as the USD 42.5 billion BEAD program. University of Colorado Boulder’s AI roll-out exposed capacity gaps that forced immediate switching refreshes, a pattern mirrored at institutions embracing 4K lecture capture and AR/VR labs.

Government and public-sector campuses face the lowest-price technically acceptable procurement rules that slow the adoption of AI-driven fabrics. Healthcare campuses and research parks show niche acceleration tied to latency-sensitive robotics and genomics workloads, but remain a minor slice of spending. Overall, universities that treat infrastructure as a competitive differentiator out-invest enterprises that characterize it as an operating cost, tilting vendor R&D toward education-centric features such as dormitory energy analytics and e-sports QoS profiles.

Geography Analysis

Asia-Pacific is the fastest-growing region at a projected 9.68% CAGR, fueled by national AI strategies that bankroll fiber-rich campus backbones. Japan’s SINET6 400 Gbps upgrade cascades demand across the network, prompting bulk purchases of 100 Gbps distribution switches.[5]National Institute of Informatics, “SINET6 Backbone Upgrade to 400 Gbps Completed,” nii.ac.jp China’s leapfrog to XGS-PON Pro+ in student housing eliminates copper limitations and accelerates multi-gig adoption, while India’s data-center build-out following AirTrunk’s USD 1.2 billion acquisition of Lumina CloudInfra requires 400 Gbps spines to marry compute and storage clusters.

North America held 37.82% of 2025 revenue on the strength of early Wi-Fi 7 deployments and aggressive PoE rollouts. Growth, however, decelerates as the installed base matures and refresh cycles lengthen. Federal stimulus tied to digital equity sustains near-term spending, but fiscal pressure at state and local levels tempers expansion, especially in community colleges and K-12 districts. Europe remains significant yet constrained by austerity budgets.

Institutions in the United Kingdom and Germany pursue digital-first curricula, but cross-border procurement complexity slows velocity. South America’s spending centers on Brazil and Argentina, but macroeconomic volatility hampers multi-year projects. The Middle East channels diversification funds into greenfield smart campuses, favoring the latest switching technology. Africa’s nascent adoption concentrates in South Africa and Nigeria, where power reliability and currency depreciation dictate cautious rollouts aligned with donor financing.

Competitive Landscape

Revenue concentration is moderate with the top five suppliers, Cisco, Hewlett Packard Enterprise (post-Juniper merger), Huawei, Arista, and Dell Technologies captured majority of market share in 2025. The HPE-Juniper merger closed in July 2025, creating integration challenges that invite channel migration toward white-box alternatives. Edgecore’s April 2025 decision to abandon proprietary NOS in favor of a pure SONiC stack, backed by Broadcom Tomahawk 6 silicon, positions the firm as a vendor-neutral foil to full-stack incumbents.

Arista doubled down on bundled campus-WAN orchestration by acquiring VeloCloud SD-WAN assets in July 2025 and unveiling VESPA roaming architecture in December 2025, enabling 500,000 wireless clients to traverse a campus without re-authentication. Juniper’s Mist platform continues to differentiate on reinforcement-learning-based anomaly detection that predicts access-point failures 72 hours ahead, turning AI operations into a revenue moat. Meanwhile, U.S. Department of Justice remedies require HPE to divest Aruba Instant On and certain Mist AIOps licenses by mid-2027, introducing a new competitor focused squarely on SMEs.

White-space opportunities arise in ruggedized outdoor switching, ultra-low-power fanless designs, and power-budget-optimized PoE++ models. Vendors capable of fusing open-networking hardware with AI-driven cloud services command the highest margins, while pure hardware specialists without recurring revenue streams face pricing pressure, as the former benefit from differentiated, subscription-led value propositions and stronger customer stickiness, whereas the latter are increasingly exposed to commoditization and intensified price competition from low-cost and white-box alternatives.

Campus Switch Industry Leaders

Cisco Systems, Inc.

Arista Networks, Inc.

Hewlett Packard Enterprise Company

Huawei Technologies Co., Ltd.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AirTrunk acquired Lumina CloudInfra for USD 1.2 billion, committing to 400 Gbps fabrics in Chennai and Mumbai for hybrid-cloud workloads.

- April 2026: Juniper Networks enhanced Mist AI with distributed denial-of-service (DDoS) troubleshooting and rogue DHCP detection, consolidating security into the switching layer.

- March 2026: Hitachi, University of Technology Sydney, and NTT DATA launched a green-transformation pilot using PoE-powered sensors and AI HVAC, targeting 20% energy savings.

- December 2025: Arista unveiled VESPA architecture to support 500,000 roaming wireless clients across a campus fabric.

Global Campus Switch Market Report Scope

The campus switch market is the segment of the networking equipment industry focused on switches deployed in enterprise campus environments, such as corporate offices, educational institutions, healthcare facilities, and government buildings, to enable high-speed, secure, and reliable local area network (LAN) connectivity. These switches aggregate and manage traffic between end-user devices and connect them to core or data center networks.

The Campus Switch Market Report is Segmented by Switch Type (Fixed Configuration Switches, and Modular Switches), Port Speed (1 GbE and Below, 2.5/5 GbE Multi-Gig, 10 GbE, 25/40 GbE, 100 GbE, and 400 GbE and Above), End-User Enterprise Size (Large Enterprises, and SMEs), End-User Industry (Education, Enterprise and Corporate Campuses, Government and Public Sector Campuses, and Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fixed Configuration Switches |

| Modular Switches |

| 1 GbE and Below |

| 2.5/5 GbE Multi-Gig |

| 10 GbE |

| 25/40 GbE |

| 100 GbE |

| 400 GbE and Above |

| Large Enterprises |

| SMEs |

| Education (K-12 and Higher Education) |

| Enterprise and Corporate Campuses |

| Government and Public Sector Campuses |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Switch Type | Fixed Configuration Switches | |

| Modular Switches | ||

| By Port Speed | 1 GbE and Below | |

| 2.5/5 GbE Multi-Gig | ||

| 10 GbE | ||

| 25/40 GbE | ||

| 100 GbE | ||

| 400 GbE and Above | ||

| By End-user Enterprise Size | Large Enterprises | |

| SMEs | ||

| By End-User | Education (K-12 and Higher Education) | |

| Enterprise and Corporate Campuses | ||

| Government and Public Sector Campuses | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the campus switch market be by 2031?

The campus switch market size is projected to reach USD 18.05 billion by 2031, reflecting an 8.1% CAGR over 2026-2031.

Which port-speed segment is growing the fastest?

2.5/5 GbE multi-gig ports are forecast to advance at a 12.5% CAGR through 2031 as campuses backhaul Wi-Fi 7 traffic without rewiring for fiber.

Why are modular switches gaining traction in campuses

Modular chassis allow universities to add line cards gradually, reducing upfront capital and aligning capacity with enrollment or IoT growth, which drives a 9.7% CAGR for this segment.

What is driving switch demand in the education sector?

Federal digital-equity funding and bandwidth-intensive EdTech platforms such as generative AI accelerate network refresh cycles, making education the fastest-growing end-user industry segment at an 8.9% CAGR .

Which region will contribute most to incremental growth?

Asia-Pacific leads with a 9.7% regional CAGR thanks to government-funded AI research clusters that require high-capacity campus backbones .

Page last updated on: