Stackable Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

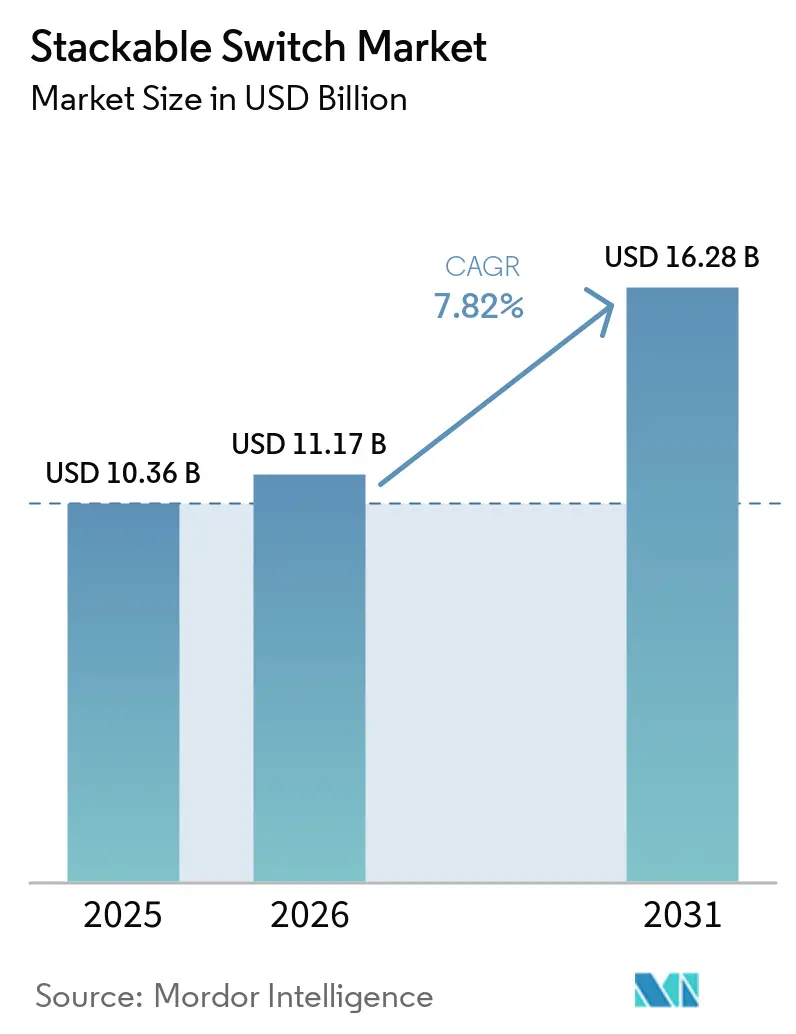

| Market Size (2026) | USD 11.17 Billion |

| Market Size (2031) | USD 16.28 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stackable Switch Market Analysis by Mordor Intelligence

The stackable switch market size was valued at USD 10.36 billion in 2025 and estimated to grow from USD 11.17 billion in 2026 to reach USD 16.28 billion by 2031, at a CAGR of 7.82% during the forecast period (2026-2031). Mid-sized enterprises are prioritizing modular hardware that scales in 24-port or 48-port increments, preventing costly forklift upgrades when cloud workloads spike. Multi-gig Ethernet ports are replacing 1 GbE uplinks in campuses where Wi-Fi 6E and Wi-Fi 7 require 2.5 Gbps or 5 Gbps backhaul. Industrial automation projects are turning to ruggedized stackables that tolerate wide temperature swings and electromagnetic noise, allowing deterministic networking on factory floors. Competitive pressure from white-box original-design manufacturers is shaving 30%-40% off average selling prices, compelling tier-one vendors to differentiate through AI-driven telemetry and cloud-managed software. Supply-chain volatility for merchant-silicon ASICs continues to elongate lead times, forcing many IT departments to stagger refresh cycles or extend support contracts on end-of-sale gear.

Key Report Takeaways

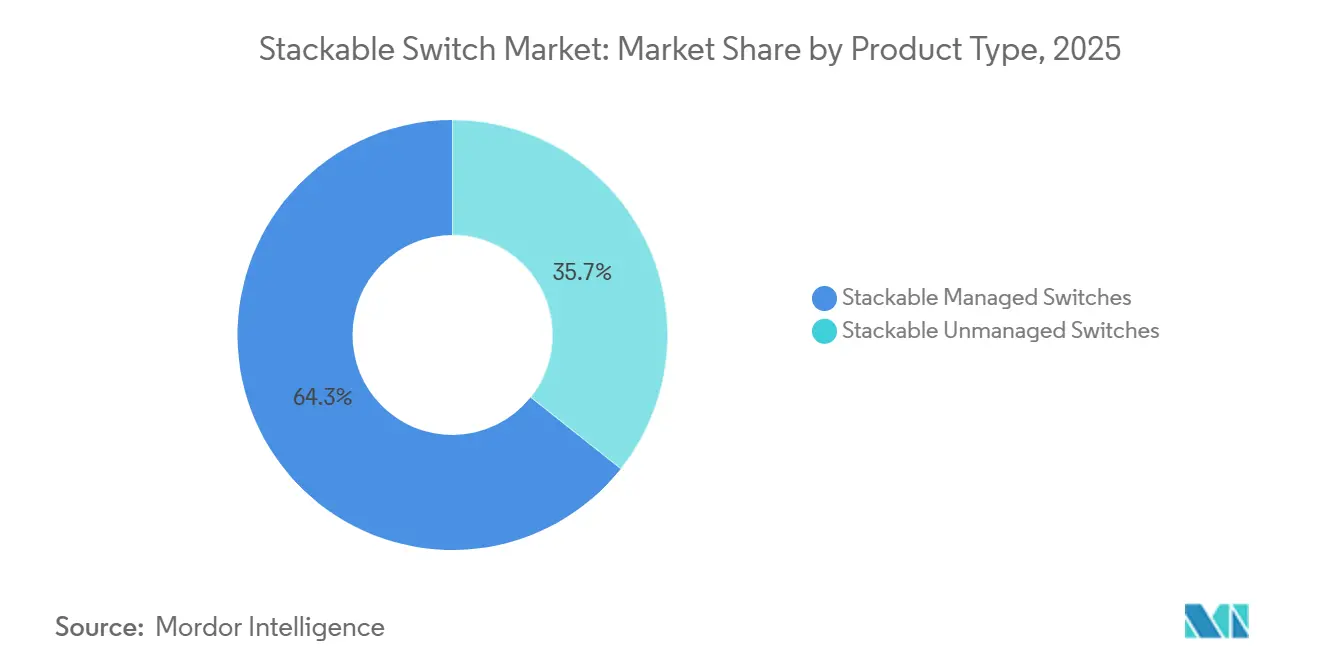

- By product type, stackable managed switches led with 64.32% revenue share in 2025, while industrial stackable variants are advancing at a 12.52% CAGR through 2031.

- By port speeds, ≤1 GbE ports accounted for 51.28% of shipments in 2025, whereas multi-gig ports are expanding at an 18.33% CAGR to 2031.

- By port counts, 48-port models captured 46.73% of installations in 2025, while switches with ≤24 ports are growing at a 10.71% CAGR over the same horizon.

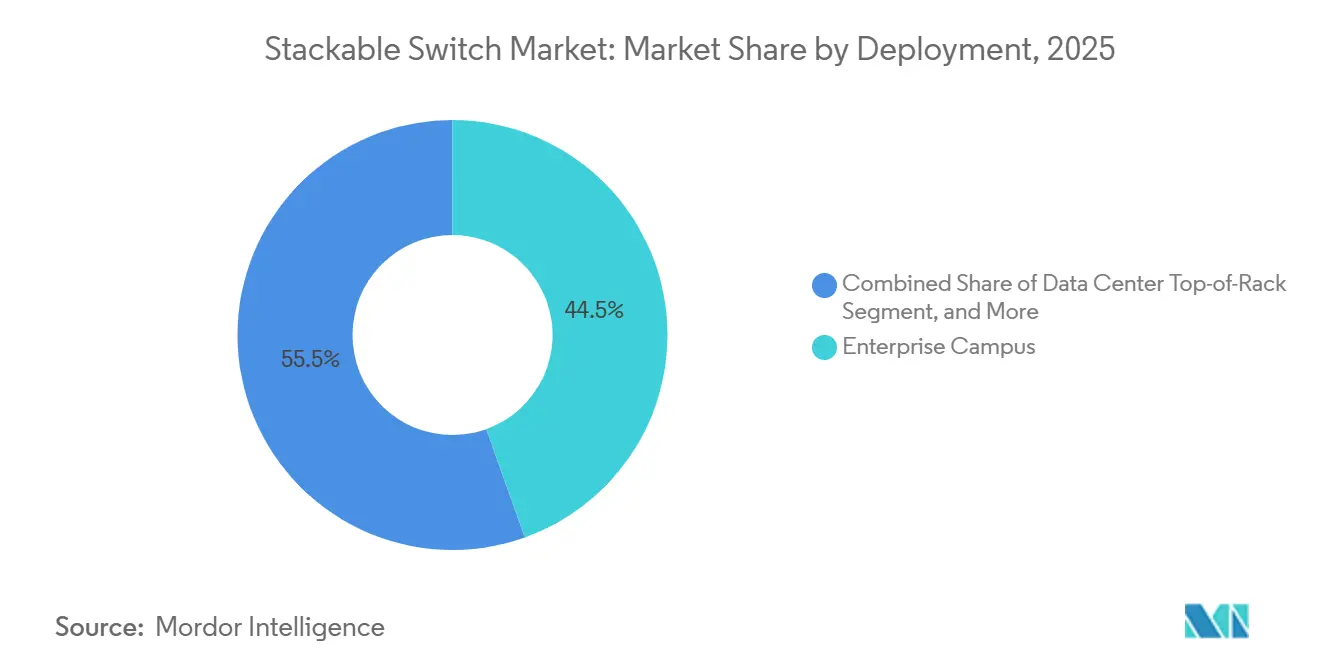

- By deployment, enterprise campus networks represented 44.52% of unit shipments in 2025, whereas industrial networks are expanding at a 14.26% CAGR through 2031.

- By end-user industry, education represented 41.43% of unit shipments in 2025, whereas government and defence industries are expanding at a 7.83% CAGR through 2031.

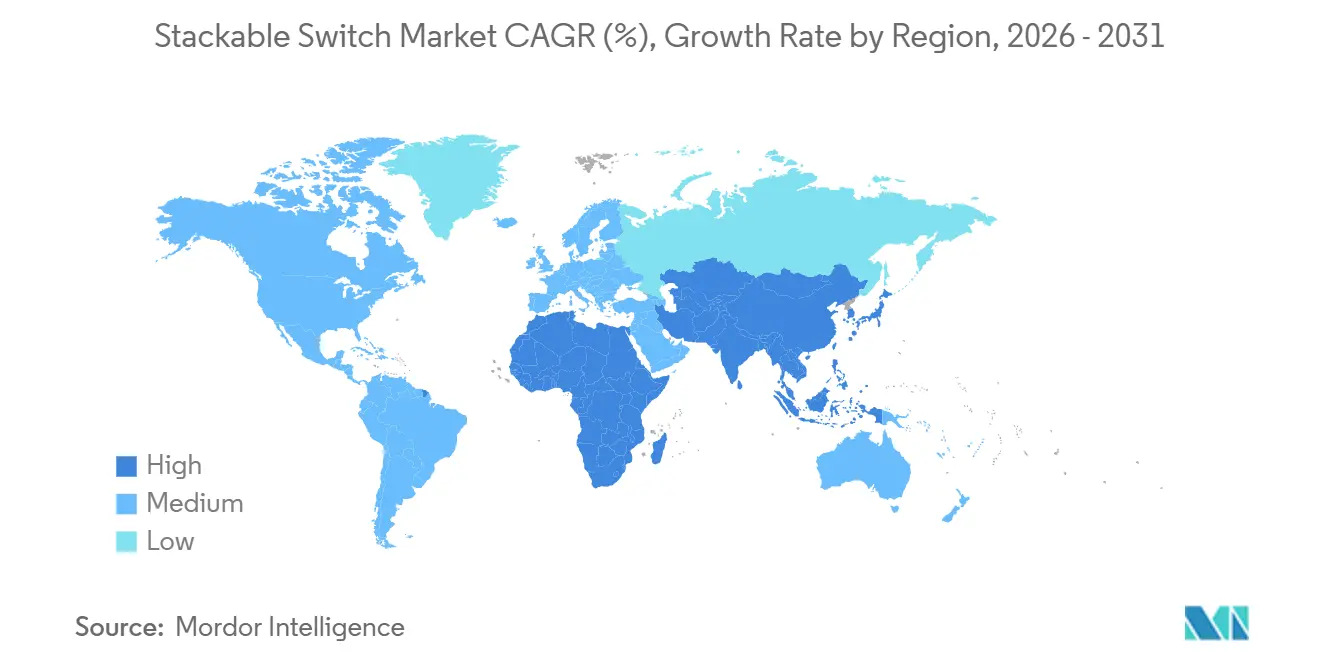

- By geography, North America held 37.83% revenue share in 2025, and the Asia Pacific is accelerating at a 17.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stackable Switch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Enterprise Network Expansion Via Cloud and Iot Adoption | +2.3% | Global, focus on North America and Asia Pacific | Medium term (2-4 years) |

| Multi-gig (2.5/5 Gbe) Ports for Wi-fi 6 Backhaul | +1.7% | North America and Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| Rising Poe Demand for IoT/VoIP Endpoints | +1.4% | Global, smart-building retrofits in tier-2/3 cities | Medium term (2-4 years) |

| Campus Upgrades to 10/25/40 Gb Ethernet | +1.1% | North America and Europe campuses, Asia Pacific data centers | Long term (≥ 4 years) |

| Need For Simplified Scalability and Management | +0.7% | Global, emphasis on mid-market enterprises | Medium term (2-4 years) |

| Smart-building Retrofits in Tier-2/3 Cities | +0.4% | Asia Pacific core with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Network Expansion Via Cloud And IoT Adoption

Hybrid-cloud architectures are flooding campus cores with east-west traffic, prompting enterprises to specify 10 Gbps or 25 Gbps uplinks in new switch stacks. Containerized workloads moving between on-premises Kubernetes clusters and public-cloud regions demand latency under 5 ms, a target met by HPE’s CX 6000 launch in 2026 that embeds AMD DPUs for inline telemetry. IoT device density in manufacturing hit 47 endpoints per 1,000 sq ft in 2025, up from 31 in 2023, forcing network planners to deploy additional stackables to preserve sub-millisecond jitter.[1]IEEE Standards Association, “IEEE 802.3bt-2018,” ieee.org Converged IT-OT fabrics now carry video surveillance, access control, and building-automation traffic, raising segmentation complexity that managed stackables solve through hardware-enforced VLANs. Vendors embedding AI inference engines for anomaly detection further reduce operational burden in lean IT teams.

Multi-Gig (2.5/5 GbE) Ports For Wi-Fi 6 Backhaul

Wi-Fi 6E access points exceed 2 Gbps throughput, yet legacy 1 GbE uplinks throttle user experience in lecture halls and stadiums. IEEE 802.3bz multi-gig ports deliver 2.5 Gbps or 5 Gbps over existing Cat5e/Cat6, avoiding costly re-cabling. Cisco Catalyst 9200 and HPE Aruba CX 6300 shipped multi-gig variants in 2025, accelerating adoption in education and hospitality. Late-2025 interoperability tests confirmed bit-error rates below 10-12 across 100 m Cat6 runs, addressing early signal-integrity concerns. Integrating PoE Type 3 and Type 4 over multi-gig lines introduces thermal constraints, driving switch makers to redesign airflow paths and heatsinks. Demand is strongest where Wi-Fi 7 pilots are underway and bandwidth ceilings near 5 Gbps per AP.

Rising PoE Demand For IoT/VoIP Endpoints

Power-over-Ethernet evolved from a convenience feature for VoIP to a cornerstone of smart-building design, energizing cameras, sensors, and Wi-Fi 6E radios. IEEE 802.3bt introduced 60 W and 100 W classes, but adoption surged only after vendors improved switch power supplies in 2024-2025. Aruba’s CX 6000 provides 2,880 W across 48 ports, enabling simultaneous PTZ camera and Wi-Fi backhaul power budgets.[2]Aruba Networks, “Aruba CX 6000 Switch Series,” arubanetworks.com Centralized power distribution trims AC outlet counts yet concentrates thermal load in wiring closets, nudging facilities teams to upgrade HVAC systems. Regulatory audits under NEC Article 840 and IEC 60950-1 scrutinize PoE safety, steering hospitals and government sites toward switches with certified fault-protection circuits. PoE adoption aligns with sustainability goals by consolidating uninterruptible power supplies.

Campus Upgrades To 10/25/40 Gb Ethernet

Video-conferencing, VDI, and high-definition lecture capture are saturating 1 Gbps aggregation layers. Texas A&M University cut peak-hour packet loss from 1.2% to <0.1% after deploying Juniper EX4650 stackables with 10 Gbps uplinks in 2025. Data-center top-of-rack designs are leaping directly to 25 Gbps or 40 Gbps, fueled by hyperconverged nodes and NVMe-oF storage. Emerging AI clusters use NVIDIA Spectrum-X 400 Gbps stackables to hold latency under 10 µs during collective operations. Although 1 Gbps hardware still dominates installed bases, refresh cycles are compressing from seven to four years as OS vendors retire support for older NICs. Upgraded switch stacks increasingly feature modular uplink bays that future-proof bandwidth planning.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| ASIC Supply-chain Volatility Delaying Roll-outs | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Price Pressure From White-box Vendors | -0.6% | Global, price-sensitive segments | Medium term (2-4 years) |

| Cannibalization by Chassis-based Switches | -0.4% | North America and Europe large enterprises | Long term (≥ 4 years) |

| SD-WAN Edge Lowering Campus Switch Density | -0.3% | North America and Europe distributed enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ASIC Supply-Chain Volatility Delaying Roll-Outs

Broadcom and Marvell lead times stretched to 52 weeks in late 2025, stalling campus refresh projects and inflating vendor backlogs. Cisco cited an 8% revenue dip in campus switching during its fiscal Q3 2025 earnings, attributing the slide to silicon shortages. Concentration of production at a handful of Asian foundries injects geopolitical risk, prompting Arista and Juniper to dual-source select models. Enterprises are countering by ordering hardware nine months ahead of deployment, tying up capital and skewing quarterly shipment data. Persistent scarcity could redirect some refresh budgets toward subscription-based managed services rather than outright hardware purchases.

Price Pressure From White-Box Vendors

Edgecore, Delta, and Accton ship IEEE 802.3-compliant stackables at discounts up to 40%, bundling SONiC or Cumulus Linux to eliminate per-port software fees. The Open Compute Project accepted stackable switch specifications in early 2025, validating open networking in the enterprise. Hyperscale operators and budget-constrained universities gravitate toward these platforms, eroding tier-one vendor margins. Incumbents respond with AI-driven assurance and cloud-hosted dashboards, but the widening feature gap may not offset aggressive pricing for mid-market customers. ODM momentum is strongest in regions where on-site vendor support lags, further undercutting branded equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Managed Variants Dominate, Industrial Surge Ahead

Stackable managed switches generated 64.32% of 2025 revenue, underscoring enterprise reliance on centralized configuration and SNMP-based monitoring. This category anchors the stackable switch market size narrative by offering lifecycle automation and firmware orchestration that unmanaged gear lacks. Industrial stackables, fortified with conformal coatings and DIN-rail mounts, are forecast to expand at a 12.52% CAGR through 2031, reflecting intensified Industry 4.0 rollouts.

Managed models now embed on-chip AI engines that flag anomalous traffic spikes and predict port failures, streamlining operations for lean IT staffs. Industrial variants converge PROFINET, EtherNet/IP, and TSN on a single platform, trimming cabinet footprint on factory floors. Unmanaged units linger in small offices and retail POS lanes but their slice of the stackable switch market is shrinking as cloud-managed offerings approach similar pricing.

By Port Speeds: Multi-Gig Ascent Reshapes Access Layer

In 2025, ports with speeds of ≤1 GbE held a significant position in the stackable switch market, accounting for 51.28% of the shipment share. This segment continues to play a crucial role due to its widespread adoption and compatibility with existing network infrastructure. However, as Wi-Fi 7 pilots highlight gigabit bottlenecks, multi-gig interfaces are experiencing robust growth, with a remarkable CAGR of 18.33%. This speed tier has emerged as the fastest-growing segment in the market, driven by decreasing transceiver costs and the benefit of backward-compatible cabling, which facilitates seamless integration into current systems.

HPE Aruba CX 6300 and Cisco Catalyst 9200 provide 24- and 48-port multi-gig SKUs that slot seamlessly into existing racks.[3]Cisco Systems, “Catalyst 9200 Series Switches Data Sheet,” cisco.com Data-center leaf layers are jumping to 25 Gbps and 40 Gbps to feed NVMe-oF throughput demands, while NVIDIA’s Spectrum-X demonstrates 400 Gbps stackables for AI fabrics. Auto-negotiation keeps multi-gig ports interoperable with legacy devices, enabling phased upgrades aligned with depreciation schedules.

By Port Counts: Density Trade-Offs Drive Form-Factor Splits

In 2025, 48-port frames accounted for 46.73% of installations, offering an optimal combination of rack efficiency and scalability. The port count segment plays a significant role in the stackable switch market, as businesses prioritize configurations that align with their operational needs. Switches with 24 or fewer ports are experiencing a 10.71% CAGR, fueled by the growing adoption of micro-data centers and branch offices with constrained power budgets. These compact switches often feature fanless cooling systems, making them particularly suitable for applications in retail kiosks and transportation hubs.

Uplink modularity blurs traditional counts; a 48-port chassis with four QSFP28 bays can effectively scale to 56 ports as bandwidth upgrades dictate. Full 802.3bt Type 4 power across 48 ports necessitates power supplies exceeding 2,500 W, often demanding dual-feed AC circuits. Rising energy densities are nudging vendors toward more efficient DC power shelves and advanced airflow designs.

By Deployment: Campus Leads, Industrial Gains Momentum

In 2025, enterprise campus networks accounted for 42.44% of shipments, underscoring their pivotal role in the stackable switch market. This segment's dominance is driven by the increasing demand for scalable, high-performance networking solutions that support modern enterprise operations. The adoption of advanced cloud-based management platforms, such as DNA Center, Mist AI, and Aruba Central, further strengthens its position by enabling seamless network management and enhanced operational efficiency. These features make enterprise campus networks a cornerstone for organizations aiming to optimize connectivity and streamline IT infrastructure.

Meanwhile, industrial deployments, growing at a robust 14.26% CAGR, are adopting TSN to ensure microsecond-level precision in robotics and process control. Data centers are opting for top-of-rack designs, utilizing stackables in compact footprints where chassis-based equipment would be excessive. On the other hand, the service-provider edge remains a niche segment, requiring MPLS and SyncE features that are rare in campus SKUs. Furthermore, the merging of Ethernet and fieldbus traffic is streamlining operations by removing the need for protocol gateways, making troubleshooting easier for plant engineers.

By End-user Industry: Government And Education Lead, Others Diversify

Government and defense entities drove significant refresh activity in 2025, aided by zero-trust mandates that require hardware-enforced VLAN isolation. The defense sector's procurement policies, which prioritize Common Criteria EAL4+ certified stackable switches, have significantly limited the pool of eligible suppliers to a select few. Concurrently, educational institutions have modernized their Wi-Fi backhaul and lecture-capture infrastructure, effectively extending refresh cycles to seven years to achieve improved total cost of ownership.

The stackable switch market is witnessing varied requirements across the healthcare, retail, and hospitality industries. Healthcare facilities are focusing on Power over Ethernet (PoE) budgets to support nurse-call system deployments. Retail chains are increasingly adopting cloud-managed, plug-and-play provisioning solutions to streamline operations. In the hospitality sector, the emphasis is on guest-network isolation and high-density Wi-Fi capabilities, prompting vendors to introduce subscription-based pricing models that align with occupancy levels. These evolving demands are shaping the competitive landscape and driving innovation within the market.

Geography Analysis

North America accounted for 37.83% of global revenues in 2025, driven by government cybersecurity mandates and higher-education modernization efforts. The aging Cat5e cabling, approaching its end-of-life, has prompted organizations to synchronize re-cabling efforts with multi-gig switch upgrades. Additionally, vendor consolidation, following HPE's acquisition of Juniper, has strengthened the market position of the top three vendors, who now account for approximately 60% of total shipments.

Asia Pacific is the fastest-growing territory, projected at a 17.67% CAGR to 2031. China’s USD 1.4 trillion digital-infrastructure investment and India’s USD 30 billion electronics incentive scheme are catalyzing hyperscale data centers and smart-factory build-outs.[4]Government of India, “Production-Linked Incentive Scheme for Electronics Manufacturing,” meity.gov.in In ASEAN, cities are increasingly adopting PoE-powered surveillance systems and environmental sensors, which has spurred demand for rugged stackable switches with high power budgets to support these applications. This trend reflects the region's focus on enhancing urban infrastructure and smart city initiatives.

Europe's stackable switch market is shaped by regulatory compliance, including GDPR and new sustainability reporting standards that emphasize vendor carbon footprints. Germany, France, and the United Kingdom are at the forefront of deployments, particularly in the automotive and financial sectors, where sub-10 µs latency is a critical requirement. These countries are leveraging advanced network infrastructure to meet the stringent demands of these industries. In contrast, South America and the Middle East and Africa lag in overall spending on stackable switches. However, isolated smart city projects and data center developments in countries like Brazil, the UAE, and South Africa indicate potential growth opportunities. As macroeconomic volatility subsides, these regions could witness increased investments in network infrastructure, further driving market expansion.

Competitive Landscape

Cisco, HPE Juniper, and Arista together accounted for significant global revenue in 2025, indicating moderate concentration in the stackable switch market. Cisco continues to leverage its well-established Catalyst product line and the automation capabilities of its DNA Center. However, the company faces increasing competition in the data-center segment from Arista and NVIDIA, particularly with NVIDIA's AI-optimized Spectrum-X line. The merger between HPE and Juniper in July 2025 marked a pivotal development, combining Mist AI with Aruba's campus switching solutions. This integration is expected to deliver a unified cloud dashboard, aimed at reducing operational complexities and enhancing efficiency for enterprise customers.

White-box ODMs such as Edgecore, Delta, and Accton have gained traction by offering solutions that integrate SONiC NOS with IEEE-compliant hardware at 30%-40% lower costs compared to traditional vendors. This value proposition has resonated strongly with cost-sensitive segments like universities and cloud service providers. Additionally, Fortinet has emerged as a disruptive player by bundling security and switching functionalities, targeting branch offices that prioritize integrated and streamlined solutions. The Ultra Ethernet Consortium's upcoming 2026 transport-layer specification is anticipated to commoditize certain switch features, compelling vendors to differentiate through advanced software overlays and AI-driven performance optimization.

Technological advancements in the market are underscored by patent filings for innovations such as 800 Gbps Ethernet, liquid-cooled optics, and co-packaged photonics. These developments signal an industry-wide race to enhance stackable throughput capabilities without reverting to traditional chassis-based designs. On the regulatory side, frameworks like NIST 800-171 and IEC 62443 are influencing industrial buyers to adopt platforms with secure-boot capabilities, effectively sidelining legacy unmanaged switches that lack encryption and other advanced security features. This evolving regulatory and technological environment is shaping the competitive dynamics of the stackable switch market.

Stackable Switch Industry Leaders

Cisco Systems Inc.

Hewlett Packard Enterprise (Aruba)

Huawei Technologies Co. Ltd.

Arista Networks Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cisco unveiled a Universal Quantum Switch prototype aimed at ultra-low-latency trading and scientific workloads.

- March 2026: Arista Networks announced the 12.8 Tbps liquid-cooled XPO optics multi-source agreement for 800 Gbps and 1.6 Tbps Ethernet.

- March 2026: HPE launched the AI Grid architecture, merging Aruba campus fabric with Juniper’s AI-native platform.

- February 2026: MTN and Huawei completed Ghana’s first large-scale Alpha Antenna rollout using stackable switches for integrated 5G backhaul.

Global Stackable Switch Market Report Scope

Stackable Switches are Ethernet switches engineered to be physically interconnected, enabling multiple units to operate as a single logical switch. This functionality allows businesses to increase port capacity, simplify network management, and enhance redundancy without replacing existing hardware. By enabling the stacking of multiple switches for unified management, these switches deliver scalable and modular networking solutions.

The Stackable Switch Market Report is Segmented by Product Type (Stackable Managed Switches, and Stackable Unmanaged Switches), Port Speeds (≤1 GbE, 2.5/5 GbE, 10 GbE, 25-40 GbE, and ≥100 GbE), Port Counts (≤24 Ports, 48 Ports, and >48 Ports), Deployment (Enterprise Campus, Data Center Top-of-Rack, Service Provider Edge, and Industrial Networks), End-user Industry (Government and Defence, Education, and Other End-user Industries), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Stackable Managed Switches |

| Stackable Unmanaged Switches |

| ≤1 GbE (10/100/1000) |

| 2.5/5 GbE (Multi-Gig) |

| 10 GbE |

| 25-40 GbE |

| ≥100 GbE |

| ≤24 Ports |

| 48 Ports |

| More than 48 Ports |

| Enterprise Campus |

| Data Center Top-of-Rack |

| Service Provider Edge |

| Industrial Networks |

| Government and Defence |

| Education |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Stackable Managed Switches | ||

| Stackable Unmanaged Switches | |||

| By Port Speeds | ≤1 GbE (10/100/1000) | ||

| 2.5/5 GbE (Multi-Gig) | |||

| 10 GbE | |||

| 25-40 GbE | |||

| ≥100 GbE | |||

| By Port Counts | ≤24 Ports | ||

| 48 Ports | |||

| More than 48 Ports | |||

| By Deployment | Enterprise Campus | ||

| Data Center Top-of-Rack | |||

| Service Provider Edge | |||

| Industrial Networks | |||

| By End-user Industry | Government and Defence | ||

| Education | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast will the stackable switch market grow through 2031?

Mordor Intelligence projects a 7.82% CAGR, taking revenue from USD 11.17 billion in 2026 to USD 16.28 billion by 2031.

Which product type dominates spending today?

Managed variants led with 64.32% revenue in 2025, reflecting enterprise appetite for centralized control.

What share did 48-port models hold in 2025?

The 48-port form factor captured 46.73% of installations, the largest slice of the stackable switch market share.

Why are multi-gig ports important for upcoming Wi-Fi upgrades?

Wi-Fi 6E and Wi-Fi 7 access points exceed 2 Gbps, making 2.5 Gbps and 5 Gbps uplinks essential to avoid backhaul bottlenecks.

Which region is expanding the fastest?

Asia Pacific is forecast to grow at 17.67% CAGR, buoyed by hyperscale data centers and smart-city investments.

Page last updated on: