Smart Managed Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

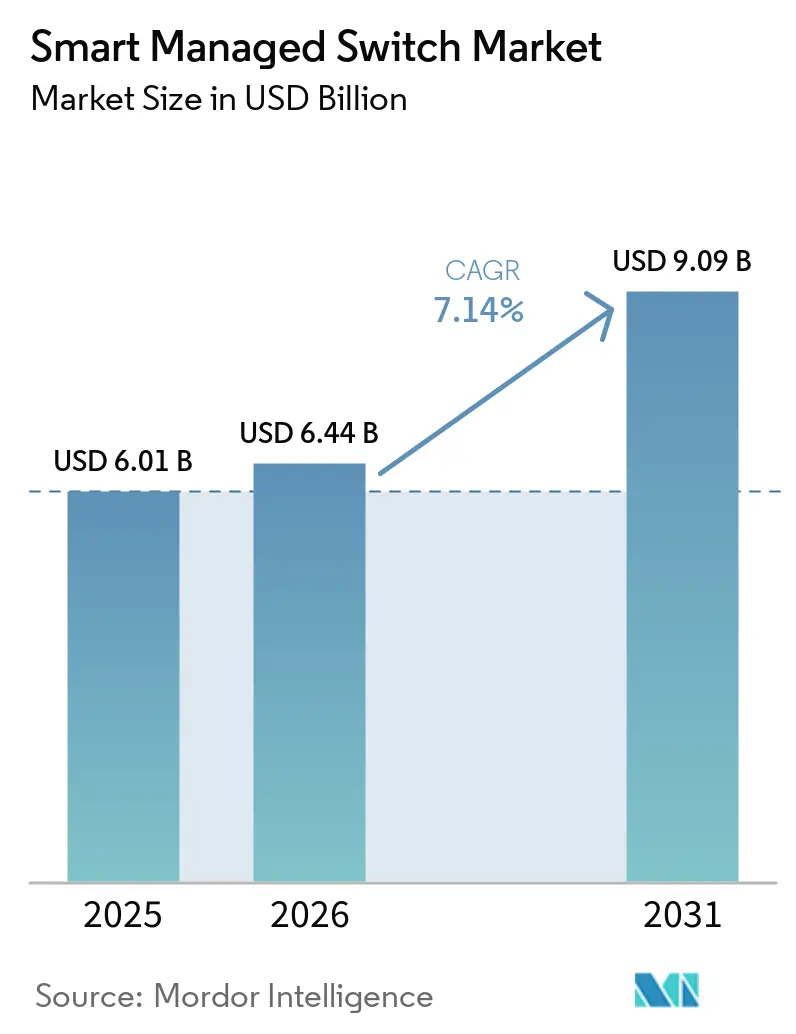

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 9.09 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

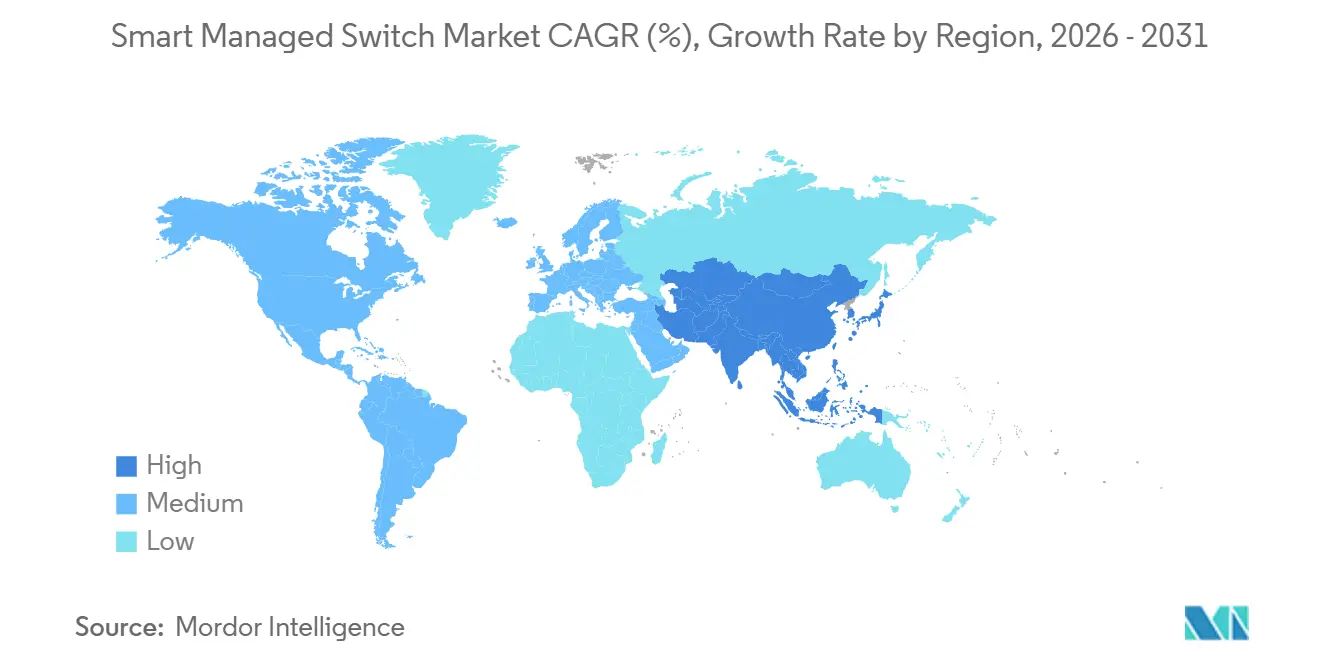

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Managed Switch Market Analysis by Mordor Intelligence

The Smart Managed Switch market size is expected to increase from USD 6.01 billion in 2025 to USD 6.44 billion in 2026 and reach USD 9.09 billion by 2031, growing at a CAGR of 7.14% over 2026-2031. Enterprises modernize edge and core networks to accommodate AI workloads, cloud-native orchestration, and converged OT-IT traffic. Power over Ethernet (PoE++) adoption, Wi-Fi 7 multi-gigabit uplinks, and regulatory energy-efficiency mandates accelerate replacement cycles, while AI-driven network operations tools lower the skill threshold for day-to-day management. Hyperscalers ignite demand for 800 Gigabit fabrics, and industrial users seek IEC-certified designs that tolerate harsh environments. However, semiconductor supply volatility and the high capital cost premium over unmanaged alternatives temper near-term uptake.

Key Report Takeaways

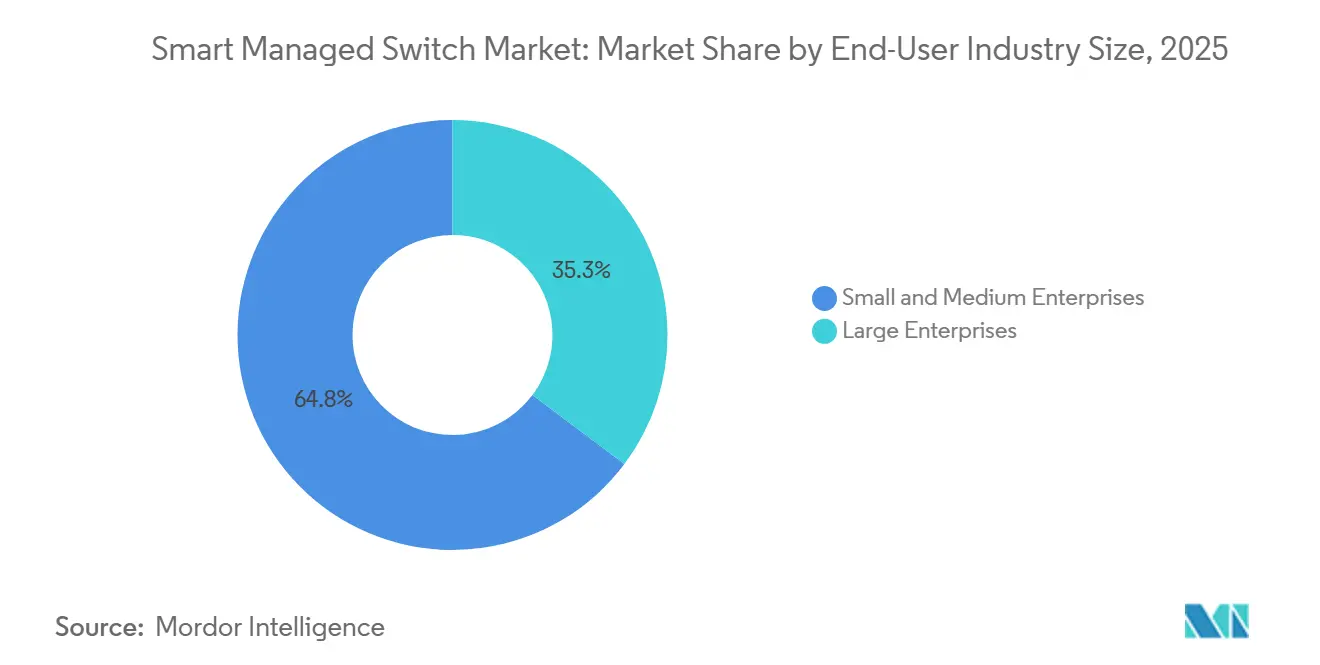

- By end-user industry size, small and medium enterprises held 64.75% revenue share in 2025 and are projected to expand at an 11.55% CAGR through 2031 as cloud-managed switching converts capital expense into subscription-based operating costs.

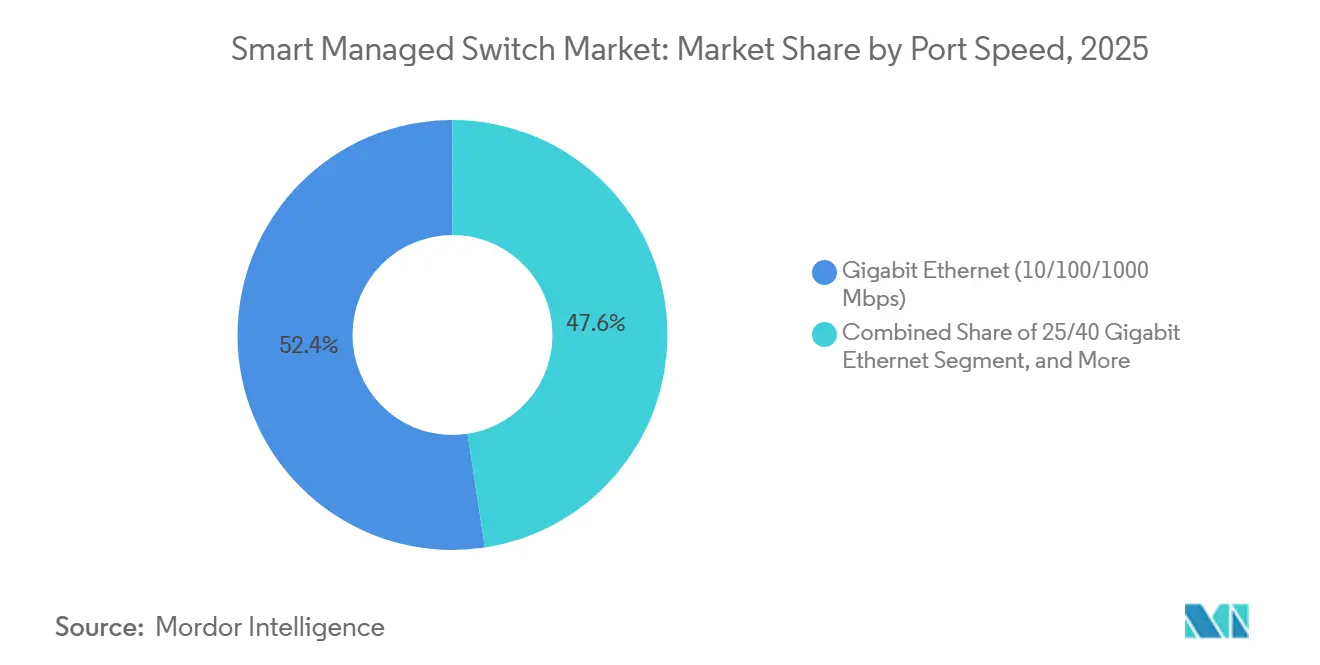

- By port speed, Gigabit Ethernet dominated with 52.41% of Smart Managed Switch market share in 2025, yet 25/40 Gigabit variants will register the fastest growth at a 10.21% CAGR on the back of AI inference servers and flash storage clusters.

- By geography, Asia-Pacific accounted for 35.41% of 2025 revenue and will lead growth at a 9.75% CAGR, buoyed by India’s electronics manufacturing incentives and smart factory rollouts.

- By port count, 9-24-port models commanded 38.65% share in 2025, while 25-48-port switches will outpace all others with a 10.64% CAGR as enterprises densify wiring closets to support Wi-Fi 7 access layers.

- By management method, hybrid approaches captured 41.33% of 2025 spending, yet cloud-native architectures will post a 10.90% CAGR to 2031 as vendors embed AI-powered anomaly detection and intent-based policy engines into SaaS portals.

- By end-user industry, IT and telecom led with 28.92% of 2025 revenue, whereas healthcare is forecast to rise at a 9.12% CAGR as hospitals pursue 99.9% uptime for real-time patient monitoring.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Managed Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 Adoption in Discrete and Process Industries | +1.8% | Global; clusters in Germany, Japan, China, India, United States | Medium term (2-4 years) |

| Proliferation of PoE-Enabled Edge Devices | +1.5% | North America and Europe lead; Asia-Pacific catching up | Short term (≤ 2 years) |

| Rapid Expansion of Cloud-Managed Networking Platforms | +1.3% | North America and Europe dominate; Asia-Pacific SMEs rising | Medium term (2-4 years) |

| AI-Driven Intent-Based Switching for SMB Networks | +1.1% | Strongest in North America and Western Europe | Medium term (2-4 years) |

| Wi-Fi 7 Multi-Gigabit Access Layer Upgrades | +0.9% | Urban centers across North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Energy-Efficiency Mandates for ICT Equipment | +0.6% | Europe, California, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 Adoption in Discrete and Process Industries

Manufacturers embracing digital twins and predictive maintenance push network designers to enforce deterministic traffic segregation without sacrificing microsecond-level synchronization. India’s Production-Linked Incentive program earmarked INR 1.46 trillion (USD 19.7 billion) to electronics manufacturing, catalyzing factory investments that mandate managed switches with native PROFINET, EtherNet/IP, and OPC UA support. Rockwell Automation’s Stratix series blends Cisco IOS with Device Level Ring redundancy, showing how industrial vendors meld enterprise switching with plant-floor resilience. Phoenix Contact’s Ethernet-APL switch, certified to IEC TS 60079-47, extends managed Ethernet 1 km into explosive zones, eliminating legacy fieldbus gateways. As factories migrate from reactive to condition-based maintenance, unmanaged devices fail to meet the throughput and segmentation demands of high-frequency sensor telemetry.

Proliferation of PoE-Enabled Edge Devices

Wi-Fi 7 access points consume 47-51 watts per port, forcing upgrades from PoE+ to IEEE 802.3bt hardware. Wi-Fi 7 accounted for 31.1% of enterprise AP shipments in Q3 2025 and will surpass 90% by 2028. TP-Link’s Omada SG3218XP-M2 provides 16 ports of 2.5 Gigabit Ethernet and a 240-watt budget, showing how mid-market buyers secure multi-gigabit uplinks without premium pricing. Beyond wireless, IP surveillance cameras and edge AI boxes consolidate power and data over Ethernet, reducing cabling yet concentrating thermal load at the switch. Labor savings from avoiding separate injectors offset the 15-20% hardware premium once deployments exceed 12 endpoints.

Rapid Expansion of Cloud-Managed Networking Platforms

UK enterprise adoption of cloud-managed switching reached 78% by late 2025, a market now valued at GBP 4.2 billion (USD 5.3 billion).[1]UK Department for Science, Innovation and Technology, “Cloud-Managed Networking Adoption in UK Enterprises,” GOV.UK, gov.uk Extreme Networks’ Platform ONE couples conversational AI with zero-touch provisioning, cutting manual configuration by 90% and slashing incident resolution times by 98% among early adopters. Cisco previewed AI-native switching in February 2026, embedding machine-learning models into firmware to predict congestion and surface security threats in real time. Although SaaS delivery lowers management overhead, dependence on vendor cloud uptime introduces new operational risk, which hybrid designs mitigate through local fall-back control.

AI-Driven Intent-Based Switching for SMB Networks

Intent-based networking translates business outcomes into device policies, letting staff without CLI expertise enforce complex rules. RUCKUS Networks’ IntentAI applies reinforcement learning to Wi-Fi optimization, reducing support tickets 60% in pilots. Cisco’s upcoming AI-native portfolio extends intent across wired layers, detecting drift and recommending fixes automatically. Gluware 5.8 adds multi-vendor compliance checks and rollbacks, shrinking human-error windows during upgrades. These capabilities let SMBs redirect scarce capital from network staffing to revenue initiatives, though opaque algorithms raise audit challenges in regulated verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial CapEx Versus Unmanaged Alternatives | -1.2% | Price-sensitive SMBs in Asia-Pacific, South America, Africa | Short term (≤ 2 years) |

| Skilled Workforce Shortage for Advanced Network Management | -0.9% | Global; pronounced in Asia-Pacific and Middle East emerging markets | Medium term (2-4 years) |

| Semiconductor Supply-Chain Volatility | -0.7% | Global | Short term (≤ 2 years) |

| Vendor Lock-in from Proprietary Cloud Portals | -0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial CapEx Versus Unmanaged Alternatives

Managed switches cost 40-60% more than unmanaged equivalents. For example, NETGEAR’s GS728TXUP lists at GBP 1,552.49 (USD 1,970) versus sub-USD 800 unmanaged peers, extending payback beyond 36 months for single-site users. Component shortages and expedited sourcing premiums inflate bills further as AI accelerator demand diverts wafer capacity. Price-sensitive buyers in emerging regions often deploy unmanaged hardware plus software overlays, trading hardware-level QoS for lower capital outlays.

Skilled Workforce Shortage for Advanced Network Management

The United Kingdom reported a 15% YoY shortfall in network engineering roles during 2025. Extreme Networks’ Partner First program couples certifications with an AI Sales Assistant to speed partner enablement, acknowledging widespread skills gaps. In Asia-Pacific and the Middle East, rapid infrastructure growth outpaces trained personnel supply, nudging organizations toward vendor consolidation and AI-assisted operations. Regulatory accountability questions linger when autonomous agents make production changes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Port Speed: Shift Toward 25/40 Gigabit Upgrades

The Smart Managed Switch market size for Gigabit Ethernet led overall demand, yet 25/40 Gigabit options are accelerating at a double-digit clip. Hyperscalers gravitate to Arista’s 7800R4 chassis, packing 576 ports of 800 Gigabit Ethernet in one frame. Huawei’s liquid-cooled 51.2 Tbps switch halves thermal overhead, enabling eight units per cabinet.[2]Huawei Technologies, “Huawei Unveils the Upgraded Xinghe AI Fabric 2.0 Solution for the AI Era,” Huawei, huawei.com While 10 Gigabit remains prevalent in mid-tier data centers, price-parity 25 Gigabit NICs shrink oversubscription headaches. The Smart Managed Switch market share of 100 Gigabit and above platforms is rising as GPU workloads require low-latency fabrics, a trend underscored by shipments tripling in Q2 2025.

Refresh cycles compress because incremental bandwidth bumps can no longer match application growth. The Ultra Ethernet Consortium’s lossless enhancements may splinter standards, but they underline demand for deterministic performance in AI clusters. Vendors differentiate through programmable ASIC telemetry pipelines that expose microburst visibility without external taps.

By Port Count: Edge Density Lifts 25-48 Port Demand

Fixed 9-24-port models satisfy branch offices, yet the Smart Managed Switch market size for 25-48-port devices is climbing fastest as Wi-Fi 7 mandates one switch port per access point. Extreme Networks’ 4000 Series bundles Universal ZTNA at the port level, letting hospitals and banks micro-segment traffic on the switch itself.

Ruggedized 2-8-port units such as Phoenix Contact’s FL SWITCH 2608 address tight industrial enclosures, commanding 50-80% price premiums. Above 48 ports, modular chassis prevail where in-service line-card upgrades justify higher cost. Instant stacking that collapses multiple units into one management domain reduces firmware touchpoints, a compelling benefit when IT teams supervise hundreds of closets.

By Management Method: Cloud-Native Gains Momentum

Hybrid management controlled the largest Smart Managed Switch market share in 2025, balancing local autonomy with SaaS convenience. Cloud-native growth outpaces all others as SMEs favor zero-touch onboarding and AI-driven troubleshooting. An outage in 2025 that froze a leading vendor’s portal for six hours exposed centralization risk.

Hybrid designs buffer that exposure by caching policies locally, albeit at the cost of real-time analytics. Subscription economics amplify lock-in; migrating away demands parallel operation and dual fees, stretching budgets. Despite these frictions, AI operations baked into cloud dashboards are becoming table stakes, tilting the long-term balance toward pure SaaS control planes.

By End-User Industry Size: SMEs Propel Volume

SMEs accounted for nearly two-thirds of 2025 revenue as cloud platforms democratize enterprise-grade features. Extreme Platform ONE allowed SMB customers to reduce manual tasks by 90%, eliminating the need for CCNP-level talent. TP-Link’s fee-free Omada SDN undercuts recurring-license rivals, boosting adoption in price-sensitive markets.

Large enterprises grow more slowly, focusing on optimization rather than greenfield rollout, yet still demand unified stacks across switching, routing, and wireless, a driver behind HPE’s USD 14 billion Juniper acquisition.

By End-User Industry: Healthcare Leads CAGR

IT and telecom remain the revenue anchor, yet growth moderates as installed bases mature. Hospitals require 99.9% uptime to support real-time patient monitoring, spurring a Smart Managed Switch market size expansion in healthcare. Verizon’s reference architecture isolates medical devices via VLANs to reduce ransomware exposure.

Manufacturing, energy, and transport accelerate managed switch adoption to enable predictive maintenance and industrial IoT. Moxa’s 2026 portfolio showcases extended-temperature designs with PROFINET redundancy to prevent process downtime.

Geography Analysis

Asia-Pacific generated over one-third of 2025 revenue and will post the fastest regional CAGR. India’s smart factory initiatives, backed by INR 1.46 trillion (USD 19.7 billion) of incentives, push demand for converged OT-IT switching. Huawei’s Xinghe AI Fabric 2.0 rollout in Shenzhen, Singapore, and Sydney underscores hyperscale momentum.

North America and Europe exhibit slower unit growth but trigger compliance-driven refreshes as EU Regulation 2023/826 caps standby power at 2-7 watts.[3]European Commission, “EU Regulation 2023/826 on Standby and Networked Standby Power,” European Commission, ec.europa.eu The Middle East and Africa ride sovereign cloud mandates, with projects such as Saudi Arabia’s HUMAIN campus specifying 400-Gigabit-ready fabrics.

South America benefits from USD 60 billion in AI data center capex, including Tecto’s BRL 200 million (USD 37.2 million) Porto Alegre build. Procurement priorities diverge: Western buyers pay premiums for multi-decade support, whereas Asian customers accept emerging-vendor risk for 40-60% price savings.

Competitive Landscape

The Smart Managed Switch market is moderately concentrated: the top five vendors Cisco, HPE, Arista, Huawei, and Dell, collectively control roughly 55-60% of global revenue. Cisco’s Silicon One G300 ASIC delivers 102.4 Tbps throughput and a programmable pipeline to defend hyperscale share.

Arista’s 800 Gigabit push narrows performance gaps, while Huawei leads in liquid-cooled designs that double rack density. Industrial specialists such as Rockwell and Siemens win where IEC 62443 certification is mandatory. Disruptors like Ubiquiti and TP-Link pressure incumbents in the SMB tier with low-cost, cloud-managed bundles.

Competitive advantage increasingly hinges on AI automation and energy telemetry; Extreme Networks and Arista filed patents covering switch-embedded inference engines that detect anomalies locally. Cloud portals deepen lock-in, but orchestration platforms like Gluware mitigate heterogeneity by abstracting vendor CLIs.

Smart Managed Switch Industry Leaders

Cisco Systems Inc.

Hewlett Packard Enterprise Company

Arista Networks Inc.

Dell Technologies Inc.

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cisco unveiled the Universal Quantum Switch supporting classical Ethernet and quantum key distribution for post-quantum security compliance.

- March 2026: Huawei introduced the CloudEngine XH9230-128DQ-LC, a 51.2 Tbps liquid-cooled fixed switch enabling eight devices per cabinet.

- March 2026: Moxa published its 2026 Solutions Brochure featuring managed switches with PROFINET-MRP redundancy for continuous-process plants.

- February 2026: Cisco launched the Silicon One G300 ASIC with 102.4 Tbps throughput and custom telemetry hooks.

- February 2026: Extreme Networks debuted the AP460C-WR Wi-Fi 6 access point featuring 2.5 Gigabit uplinks and PoE++ draw.

Global Smart Managed Switch Market Report Scope

The Smart Managed Switch Market stands as a hybrid category, blending limited management features with user-friendly configuration. Offering vital controls like VLAN setup and traffic prioritization, these switches bridge the gap between unmanaged and fully managed counterparts. Their growth is spurred by a rising appetite for cost-effective yet controllable networking solutions, especially among SMEs and lighter industrial settings.

The Smart Managed Switch Market Report is Segmented by Port Speed (Gigabit Ethernet [10/100/1000 Mbps], 10 Gigabit Ethernet, 25/40 Gigabit Ethernet, and 100 Gigabit and Above), Port Count (2-8 Ports, 9-24 Ports, 25-48 Ports, and Above 48 Ports), Management Method (Cloud-native, On-prem native, and Hybrid), End-User Industry Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, Healthcare, Retail, Government, Education, and Other End-user industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Gigabit Ethernet (10/100/1000 Mbps) |

| 10 Gigabit Ethernet |

| 25/40 Gigabit Ethernet |

| 100 Gigabit and Above |

| 2-8 Ports |

| 9-24 Ports |

| 25-48 Ports |

| Above 48 Ports |

| Cloud-native |

| On-prem native |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| IT and Telecom |

| Healthcare |

| Retail |

| Government |

| Education |

| Other End-User industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Port Speed | Gigabit Ethernet (10/100/1000 Mbps) | |

| 10 Gigabit Ethernet | ||

| 25/40 Gigabit Ethernet | ||

| 100 Gigabit and Above | ||

| By Port Count | 2-8 Ports | |

| 9-24 Ports | ||

| 25-48 Ports | ||

| Above 48 Ports | ||

| By Management Method | Cloud-native | |

| On-prem native | ||

| Hybrid | ||

| By End-User Industry Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Industry | IT and Telecom | |

| Healthcare | ||

| Retail | ||

| Government | ||

| Education | ||

| Other End-User industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current Smart Managed Switch market size and projected growth?

The Smart Managed Switch market size stands at USD 6.44 billion in 2026 and is forecast to reach USD 9.09 billion by 2031, reflecting a 7.14% CAGR (2026-2031).

Which region will lead adoption through 2031?

Asia-Pacific will register the fastest regional expansion at a 9.75% CAGR as electronics manufacturing incentives and smart factory projects multiply.

Why are SMEs investing aggressively in managed switches?

Cloud-managed platforms and subscription pricing let SMEs access enterprise-grade features without hiring dedicated network engineers, driving an 11.55% CAGR for the segment.

How is Wi-Fi 7 influencing switch specifications?

Wi-Fi 7 access points require 2.5 Gigabit uplinks and 47-51 watts of PoE, compelling enterprises to replace legacy PoE+ Gigabit switches with IEEE 802.3bt-compliant multi-gigabit models.

What role does energy regulation play in replacement cycles?

EU Regulation 2023/826 caps networked standby power at 2-7 watts from 2027, forcing organizations to swap older, less efficient switches for models with dynamic power management.

Page last updated on: