Cloud Managed Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

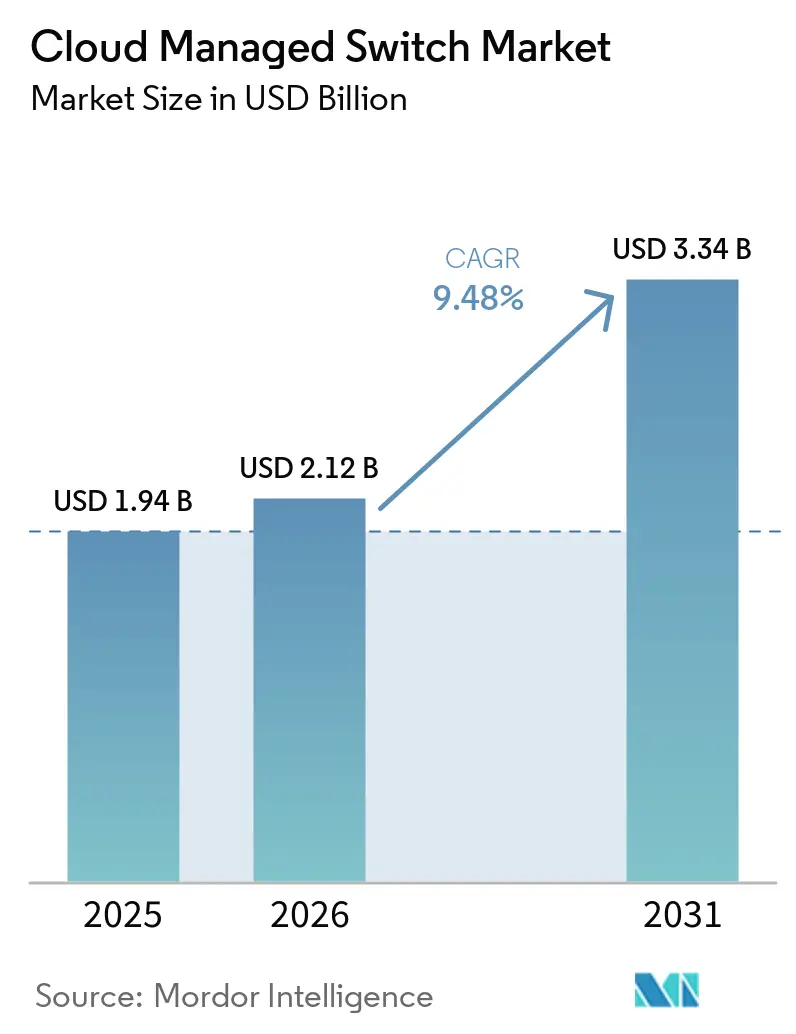

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 9.48% CAGR |

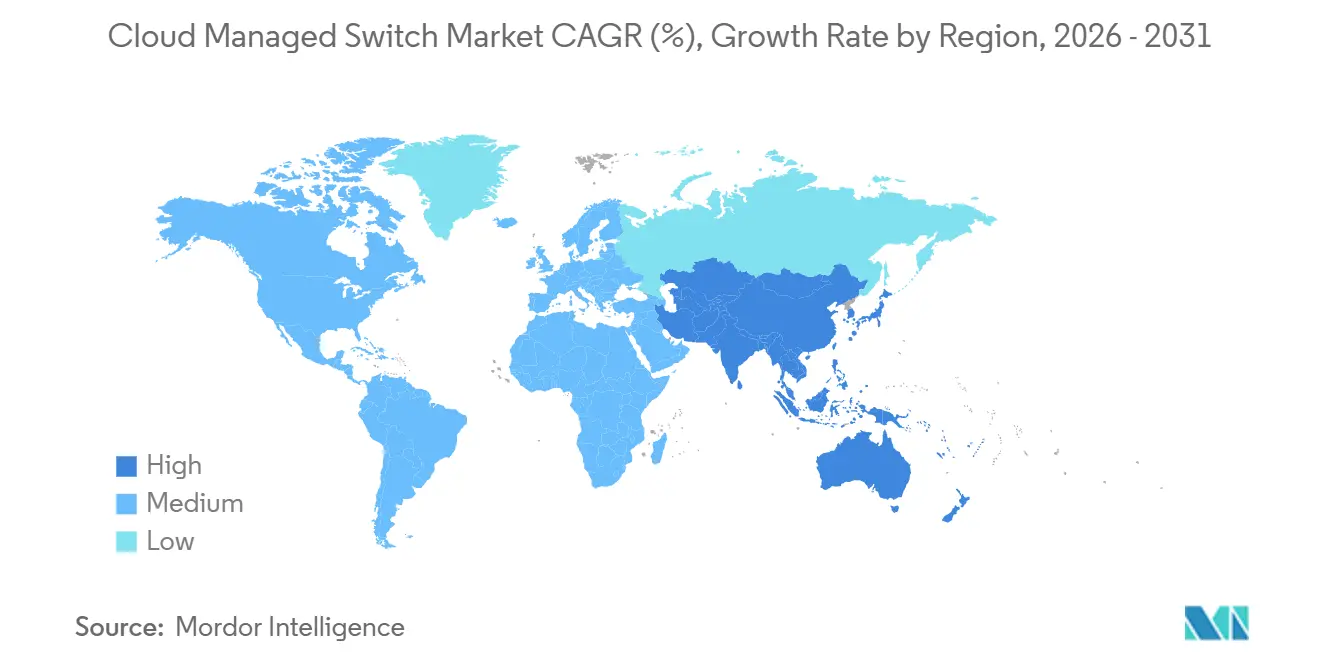

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

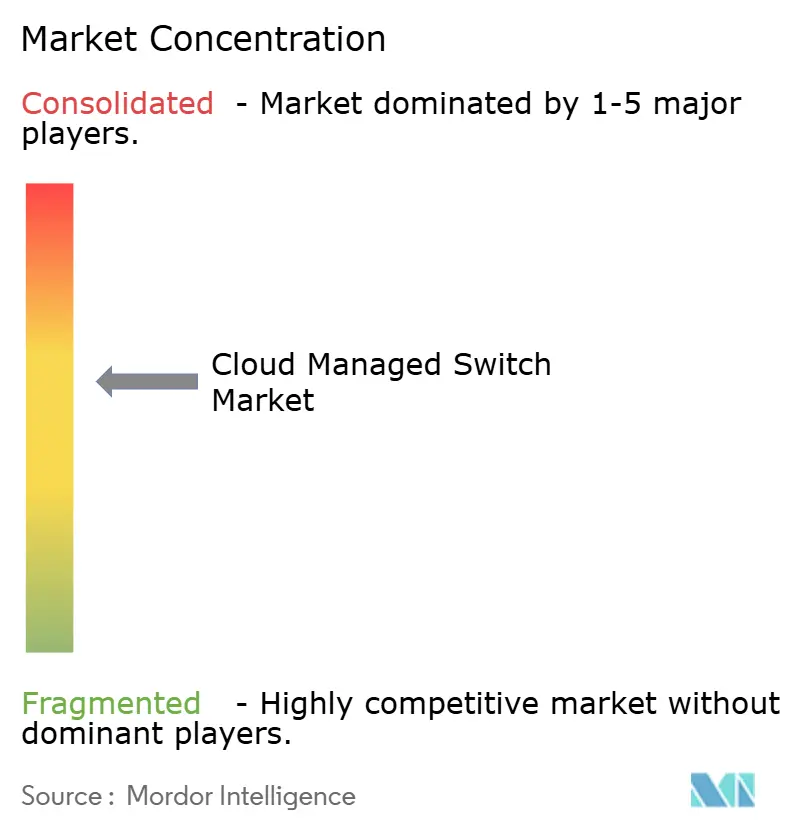

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Managed Switch Market Analysis by Mordor Intelligence

The cloud managed switch market size is projected to expand from USD 1.94 billion in 2025 and USD 2.12 billion in 2026 to USD 3.34 billion by 2031, registering a CAGR of 9.48% between 2026 and 2031. Heightened Wi-Fi 6 and Wi-Fi 6E back-haul demand, a steady migration by small and medium enterprises (SMEs) toward subscription-based operational-expenditure models, and the rise of edge compute architectures that require zero-touch provisioning are accelerating refresh cycles. Campus networks are also embracing power-efficient IEEE 802.3bt PoE standards, aligning infrastructure upgrades with corporate carbon-reduction targets. In parallel, hyperscale cloud and artificial-intelligence training fabrics are scaling switch density beyond 100 gigabit Ethernet, amplifying demand for liquid-cooled chassis and programmable silicon. Vendors continue to differentiate through AI-driven telemetry, zero-trust access, and flexible licensing that lets customers toggle between cloud, private-cloud, or on-premises controllers without replacing hardware.

Key Report Takeaways

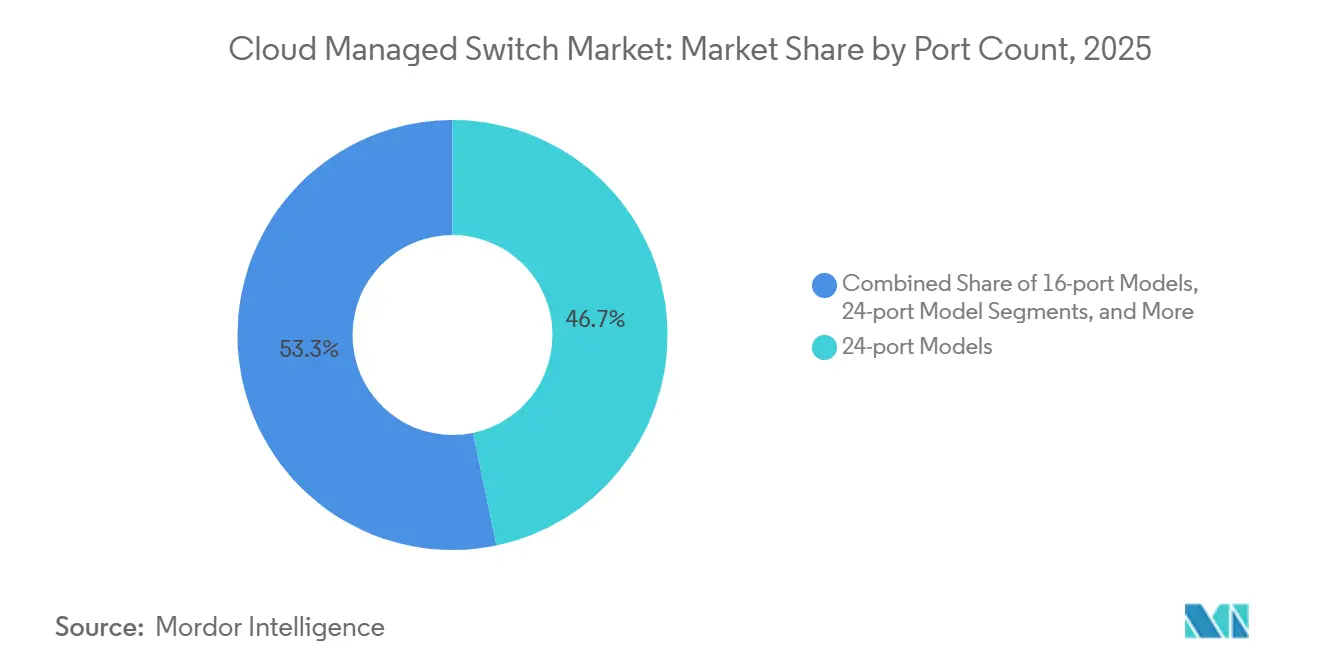

- By port count, 24-port models led with 46.72% of the cloud managed switch market share in 2025. The 96-port and chassis-based category is forecast to grow at an 18.43% CAGR between 2026 and 2031.

- By switch-capacity terms, 10 gigabit ethernet held 36.77% revenue share in 2025, while 25/40 gigabit ethernet is advancing at a 13.26% CAGR through 2031.

- By enterprise size, large enterprises accounted for 41.23% of the 2025 cloud managed switch market, yet the SME segment is growing at a 11.21% CAGR for 2026-2031.

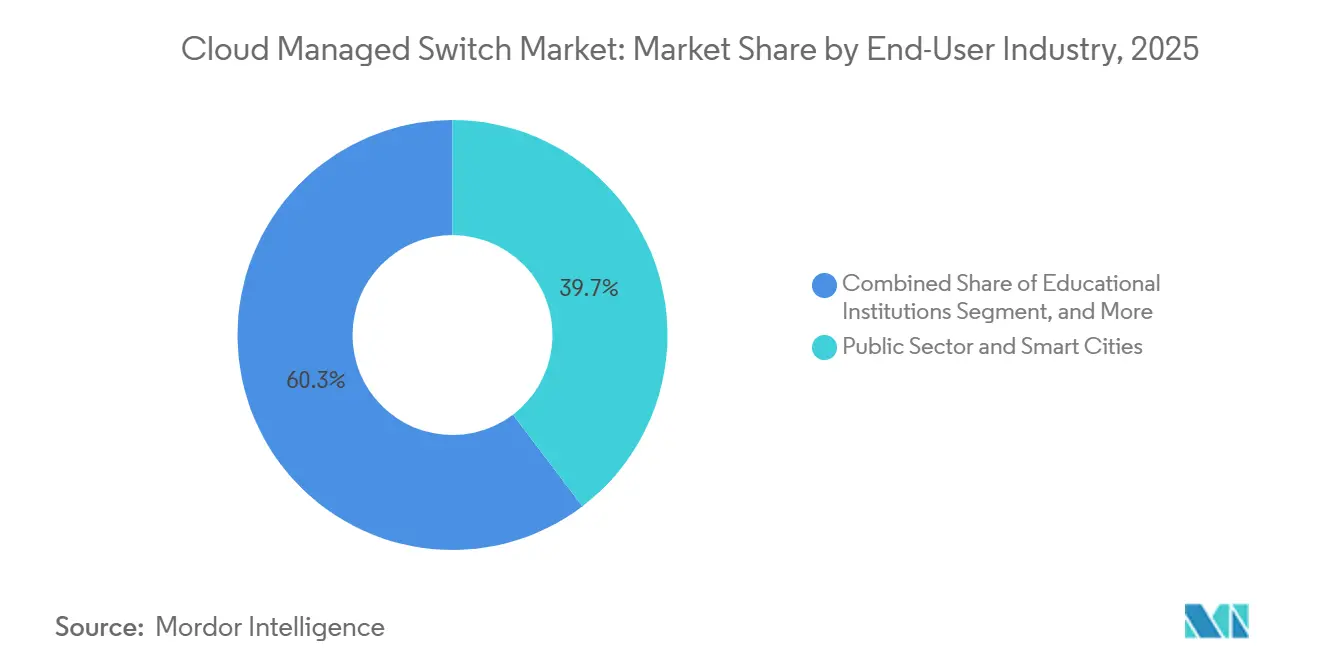

- By end-user industry, the public sector and smart cities accounted for 39,67% of the 2025 cloud managed switch market. The healthcare facilities are the fastest-growing vertical, expanding at a 16.62% CAGR to 2031.

- By deployment model, the public-cloud managed models accounted for 43.82% of the 2025 cloud managed switch market; further, the segment is growing at a 11.92% CAGR for 2026-2031.

- By geography, North America dominated with 36.77% revenue share in 2025, whereas Asia-Pacific is set to expand at a 15.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud Managed Switch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in Multi‑Gigabit Wi‑Fi 6/6E Back‑Haul Demand | +2.8% | Global, early adoption in North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Rise of SMEs Adopting OPEX Models | +2.1% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Edge and IoT Proliferation Needing Remote Switch Management | +1.9% | Global, concentrated in Asia-Pacific smart cities and North America industrial IoT | Medium term (2-4 years) |

| Sustainability‑Focused PoE+ Power Optimization | +1.2% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Open-RAN Transport Network Build-outs | +0.9% | Asia-Pacific (China, India, Japan), Europe, select North America carriers | Long term (≥ 4 years) |

| AI-driven Network Analytics in Cloud Dashboards | +0.6% | North America, Europe, Asia-Pacific tier-1 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Multi-Gigabit Wi-Fi 6/6E Back-Haul Demand

Enterprises are densifying Wi-Fi radio deployments, and each new Wi-Fi 6E access point typically requires 2.5 gigabit or 5 gigabit uplinks to avoid congestion. Cloud-managed switches equipped with multi-rate 1/2.5/5/10-gigabit BASE-T ports therefore replace legacy 1-gigabit models in education, healthcare, and large corporate campuses. Vendors have validated multi-gigabit deployments that reuse existing Category 6A cabling, avoiding disruptive rewiring.[1]Cisco Systems, “Cisco Catalyst 9300 Series Data Sheet,” cisco.com Early adopters in the United States and parts of Western Europe benefited from 6 gigahertz spectrum clearance 12-18 months ahead of Asia-Pacific, but spectrum auctions across India, Japan, and ASEAN economies are now triggering synchronized refresh cycles. As channel partners bundle switches, access points, and license subscriptions under a single contract, CFOs perceive multi-gigabit back-haul upgrades as an operational rather than capital event, smoothing budget approvals and sustaining volume shipments over the next three years.

Rise of Small and Medium Enterprises Adopting OPEX Models

SMEs lack dedicated network engineers and favor solutions that arrive pre-provisioned, self-update, and deliver natural-language troubleshooting from the cloud. Subscription-first pricing turns hardware, firmware, and support into one predictable monthly fee, freeing cash for growth initiatives. Managed-service providers (MSPs) capitalize by packaging connectivity, security, and collaboration into turnkey offerings, expanding addressable demand beyond enterprises with in-house IT staff. Competitive intensity at the lower end of the market sustains aggressive price points, while AI-driven dashboards reduce MSP overhead and let a single operator manage hundreds of sites concurrently. Because contract lengths typically span three years, the OPEX model locks in revenue visibility for vendors and partners, further reinforcing ecosystem momentum.

Edge and IoT Proliferation Needing Remote Switch Management

The shift toward distributed computing pulls servers, storage, and networking into retail outlets, factory floors, and roadside cabinets. Each remote node may only host a handful of servers, yet it must be monitored, patched, and secured to the same standard as a core data center. Cloud-managed switches with zero-touch provisioning, RESTful APIs, and secure boot allow operators to deploy hardware in unmanned locations and bring it online in minutes. Time-sensitive networking support keeps packet jitter within industrial automation thresholds, while integrated telemetry feeds AI engines that pre-empt failures. Smart-city programs across Southeast Asia and the Middle East increasingly specify remote-management functionality in procurement templates, translating policy requirements into immediate hardware demand.

Sustainability-Focused PoE+ Power Optimization

Updated PoE standards inject up to 90 watts per port, enabling LED lighting, security cameras, and building controls to draw power directly from the switch. European directives that cap building-energy intensity push facility managers toward unified power and data architectures, and cloud-managed switches expose native dashboards that profile per-port consumption. Automated power-shed policies turn off idle ports overnight, contributing to corporate emissions-reduction targets. Suppliers highlight lifecycle carbon disclosures in public tenders, so switches with efficiency certifications gain scoring advantages during competitive bidding, especially in the European Union and progressively in North America.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Migration Complexity and Cost Barriers | -1.8% | Global, higher in Europe and North America | Medium term (2-4 years) |

| Data‑Sovereignty‑Driven On‑Prem Mandates | -1.3% | Europe, China, India | Long term (≥ 4 years) |

| Semiconductor Supply‑Chain Volatility | -0.9% | Global, supply concentrated in Taiwan and South Korea | Short term (≤ 2 years) |

| Vendor Lock‑in to Proprietary Clouds | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Migration Complexity and Cost Barriers

Moving from on-premises controllers to cloud management often incurs data-egress fees, re-architecting efforts, and new licensing commitments that collectively inflate project budgets by 15-25%. Proprietary APIs and unique identity stores further complicate dual-vendor environments, while end-of-life announcements for older hardware force accelerated decision making. Enterprises that keep latency-sensitive workloads on-site risk tool fragmentation, as two control planes must co-exist until full migration completes. The resulting operational overhead extends payback periods out to two years or more, deterring conservative buyers.

Data-Sovereignty-Driven On-Prem Mandates

Regulations such as GDPR, the European Union Cloud Sovereignty Framework, and India’s Digital Personal Data Protection Act require certain data categories to remain within national borders. Buyers in healthcare, finance, and public administration increasingly demand vendor-hosted private-cloud or self-hosted virtual controllers deployed in local data centers. Providers must prove that support personnel, telemetry pipelines, and redundancy sites all sit within approved jurisdictions. Compliance documentation adds cost and complexity, and in countries with limited hyperscale footprint, it can limit the attainable subscriber base for public-cloud-managed offerings.[2]European Commission, “Cloud Sovereignty Framework,” commission.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Port Count: Density Shifts Toward Modular Platforms

The 24-port category captured 46.72% of 2025 revenue because it fits most branch and midsize campus closets, where power budgets and rack space are limited. These fixed-configuration switches will continue to ship in volume, but growth skews toward 96-port and chassis platforms that anchor spine layers in distributed data centers. The cloud managed switch market for high-density chassis is projected to expand at a 18.43% CAGR, driven by hyperscaler and AI inference cluster demand. AI training racks now draw over 30 kilowatts, and centralized cooling favors modular backplanes that consolidate multiple line cards under one management plane. Vendors offer field-replaceable fans, power supplies, and fabric modules, driving mean-time-between-failure metrics that surpass fixed-form-factor devices and appeal to operators who cannot tolerate downtime during model training.

Furthermore, Dell's PowerSwitch Z9664F-ON, a 64-port 400-gigabit Ethernet switch in 2-rack-unit form factor, supports disaggregated hardware and software via Enterprise SONiC Distribution and Dell SmartFabric OS10, enabling zero-touch installation and autonomous fabric deployment through SmartFabric Services.[3]Dell Inc., “PowerSwitch Z9664F-ON Specification Sheet,” delltechnologies.com Furthermore, branch deployments continue to deploy 8-port and 16-port switches where space is tight, such as retail kiosks or remote healthcare pods. Education and hospitality buyers favor 48-port models that balance port density with acceptable upfront cost, and PoE budgets reach the 740-watt threshold required for modern access points. While the relative share of 24-port units will slip, absolute shipments remain healthy because new IoT endpoints, badge readers, and sensors replenish access-layer demand.

By Switch Capacity: Multi-Gigabit Interfaces Bridge Campus and Edge

The mature 10 gigabit Ethernet segment dominated 2025 at 36.77% share due to broad transceiver availability and favorable cost per bit. Still, the 25/40 gigabit cohort is set to grow 13.26% annually as Wi-Fi 6E access points migrate to 2.5/5 gigabit uplinks and edge servers standardize on 25 gigabit network interface cards. This transition preserves the installed copper plant while unlocking higher throughput, making it a low-friction upgrade path for campuses. At the top end, hyperscale clouds already deploy 400 gigabit and 800 gigabit fabrics to feed AI accelerators. Although volumes are small, outsized average selling prices lift revenue contribution, and early adopters validate liquid-cooling designs that will trickle down to enterprise variants.

The 1 gigabit tier remains meaningful in emerging markets and brown-field retrofits where budget limitations or legacy controllers cap link speeds. Nevertheless, growth concentrates in multi-rate switches that auto-negotiate 1/2.5/5/10 gigabit, offering future readiness without a port-by-port forklift. By 2031, multi-rate silicon will permeate even entry-level lines, displacing static 1 gigabit chips except in ultra-low-cost models.

By Enterprise Size: Subscription Uptake Accelerates Among SMEs

In 2025, large enterprises accounted for 41.23% of spending in the cloud managed switch market. This dominance is attributed to their complex multi-site architectures and dedicated teams that prioritize advanced telemetry solutions. These enterprises continue to hold a significant position in the market due to their ability to invest in sophisticated technologies and leverage economies of scale. However, SMEs are emerging as the faster-growing segment, with a strong CAGR of 11.21% projected through 2031. Their constrained resources align seamlessly with the benefits of cloud-hosted dashboards and flexible pay-as-you-grow licensing models. For example, a restaurant chain opening multiple outlets each quarter can efficiently deploy new sites using a smartphone app, eliminating the need for on-site technical interventions. Additionally, the MSP channel enhances value for SMEs by offering bundled networking and cybersecurity solutions under a single, streamlined invoice.

While large enterprises have historically enjoyed a size advantage in the cloud managed switch market, the gap is narrowing as SMEs increasingly adopt advanced features previously exclusive to Fortune 500 companies. These include AI-powered troubleshooting and zero-trust segmentation. Vendors are addressing SME needs by introducing simplified onboarding processes and natural-language query capabilities, enabling store managers to interpret alerts without requiring formal networking expertise. As these quality-of-experience metrics improve, SME churn rates are declining, fostering a sustainable cycle of renewals and opportunities for add-on services. This shift underscores the growing importance of SMEs in shaping the future dynamics of the cloud managed switch market.

By End-User Industry: Healthcare Surges on IoT and Compliance Pressures

Public sector and smart-city projects accounted for 39.67% of 2025 installations as governments digitized transportation, utilities, and education. Healthcare is now the standout growth vertical, forecast at 16.62% CAGR, because electronic medical records, connected diagnostics, and real-time telemetry load networks are more heavily used than traditional voice and data. Compliance requirements under HIPAA and analogous regulations abroad stipulate rigorous audit trails, making cloud-provided logs attractive. Hospitals also exploit 90-watt PoE to power lighting and imaging carts, yielding tangible operating-expense reductions that fund further upgrades.

Retail and hospitality rollouts remain brisk as self-checkout, digital signage, and guest Wi-Fi become core to customer experience. Educational institutions defend budget allocations by citing hybrid learning needs and energy-saving retrofits. In every vertical, granular network segmentation that isolates IoT devices minimizes lateral-movement risk, a capability more readily configured in cloud portals than in standalone command-line sessions.

By Deployment Model: Public Cloud Leads, Hybrid Gains Ground

In 2025, public cloud platforms held a significant position in the cloud managed switch market, capturing a substantial 43.82% market share. This dominance is attributed to their ability to eliminate the need for controller hardware while providing instant global accessibility. However, the increasing enforcement of data-sovereignty regulations has driven demand for vendor-hosted private clouds and self-hosted virtual controllers, which ensure data remains within specified jurisdictions. The introduction of unified licensing has further strengthened this segment by enabling customers to transfer entitlements seamlessly between hosting modes, allowing businesses to adapt quickly to evolving compliance and latency requirements.

Hybrid models are also emerging as a critical segment, combining public cloud management for branch locations with on-premises controllers at headquarters. This configuration addresses specific use cases where sensitive workloads must remain within company premises. As APIs continue to mature, bidirectional policy synchronization has become more robust, ensuring that security groups consistently follow users, regardless of the controller's location. Analysts project that hybrid deployments will account for nearly one-third of the market by 2031, highlighting the growing importance of flexible and scalable software architectures in the cloud managed switch market.

Geography Analysis

North America held 36.77% of 2025 revenue, buoyed by early Wi-Fi 6E spectrum clearance, multi-year education grants, and accelerating AI infrastructure investment. Cloud managed switch refresh cycles align with broader shifts toward subscription software across the United States and Canada, and vendors report mid-teens data-center switch order growth for six consecutive quarters. Although the installed base is maturing, demand persists for power-efficient replacements and sustained cybersecurity visibility, keeping the regional CAGR near 8% through 2031.

Asia-Pacific is the fastest-growing territory, forecast to expand at 15.32% annually as China, India, and ASEAN members pour funding into smart-city grids, sovereign clouds, and 5G transport networks. Regional data-center capacity is on track to exceed 17 gigawatts by 2026, and rack power densities now breach 30 kilowatts, pushing operators toward liquid-cooled chassis and 400/800 gigabit fabrics. Sovereign procurement frameworks often bundle networking, compute, and financing, favoring domestic champions but still leaving room for foreign suppliers that localize management plans.

Europe’s trajectory is shaped by stringent privacy and sustainability frameworks that constrain public-cloud adoption but incentivize feature-rich private-cloud controllers. Certifications such as SecNumCloud in France and C5 in Germany require documented processing locations and transparent supply chains, and bidders with carbon-neutral roadmaps secure bonus scoring. As member states modernize campus and metropolitan transport networks, Europe’s CAGR should rise to roughly 7.8% through 2031, underpinned by sovereign-cloud mandates that force refresh projects ahead of support sunsets.[4]European Commission, “Cloud Sovereignty Framework,” commission.europa.eu

Competitive Landscape

The top five vendors, Cisco, HPE Aruba, Juniper Networks, Extreme Networks, and Huawei, collectively capture a significant portion of cloud-managed switch revenue, indicating moderate concentration. Cisco commands the broadest portfolio, spanning Meraki cloud-native platforms, Catalyst campus products, and Nexus data-center systems, and has kicked off a multi-year campus refresh anchored on Silicon One ASICs that promise 70% energy savings. HPE completed its Juniper acquisition in 2025, combining Aruba’s wireless and CX switching with Mist AI analytics, enabling customers to toggle between control planes with no hardware swaps. Extreme Networks differentiates through universal licensing that transfers across public, private, and edge clouds, while an overhauled partner program accelerates deal registration to 48 hours, helping specialist resellers counter heavyweight incumbents.

Arista widens its scope beyond hyperscale data centers into enterprise AI clusters by shipping an 800-gigabit HyperPort that claims 44% faster job completion. Ubiquiti, Cambium Networks, and Ruijie Networks address cost-sensitive SMEs and outdoor deployments, offering simplified dashboards and aggressive price-performance ratios. Semiconductor supply tightness remains an industry-wide pain point; memory shortages in early 2026 forced vendors to enter long-term purchase agreements that raised component costs and lengthened lead times. To mitigate risk, suppliers diversify assembly beyond Taiwan and invest in software features that extend product life, such as in-service OS downgrades when chips are back-ordered.

White-space niches still exist in ruggedized and industrial categories. NETGEAR’s 2026 rugged launch includes Neutrik locking connectors for audiovisual over IP, and Fortinet fuses switching with real-time threat intelligence to collapse network and security layers. Chinese vendors retain strength across Asia-Pacific smart-city projects, despite geopolitical headwinds in the United States and Europe. Overall, portfolio convergence, AI-infused operations, and flexible licensing dominate strategic roadmaps, pushing differentiation beyond raw port counts toward lifecycle experience.

Cloud Managed Switch Industry Leaders

Cisco Systems, Inc.

Extreme Networks, Inc.

Huawei Technologies Co., Ltd.

D-Link Corporation

HPE (Aruba)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cisco announced Silicon One G300 102.4 terabits-per-second silicon and G300-based Nexus systems with liquid-cooling options, citing a 70% energy-efficiency boost and 28% faster AI job completion.

- January 2026: NETGEAR introduced M4350 ruggedized switches for audiovisual over IP, incorporating 1,130-watt PoE budgets, Neutrik locking connectors, and offline provisioning through Engage Controller 2.4.

- January 2026: Hewlett Packard Enterprise expanded Aruba CX 6000 with new 8-port PoE and non-PoE compact models, integrating Juniper Mist Marvis into Aruba Central and offering GreenLake subscription terms.

- October 2025: Arista unveiled the 7800R4 modular switch supporting 576 800 gigabit ports and 3.2 terabit HyperPort interfaces, plus 7280R4 and 7020R4 fixed platforms with wire-speed TunnelSec encryption.

Global Cloud Managed Switch Market Report Scope

The Cloud Managed Switch Market refers to the industry focused on network switches that are managed, configured, and monitored through cloud-based platforms. These solutions enable centralized management, enhanced scalability, and streamlined operations, catering to the needs of enterprises, data centers, and service providers. By leveraging cloud technology, these switches simplify network management, reduce operational complexity, and support the growing demand for flexible, efficient networking solutions.

The Cloud Managed Switch Market Report is Segmented by Port Count (8-port and below, 16-port Models, 24-port Models, 48-port Models, 96-port and Chassis-based), Switch Capacity (1 GbE, 2.5/5 GbE Multigig, 10 GbE, 25/40 GbE, and 100 GbE and above), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Educational Institutions, Healthcare Facilities, Hospitality and Retail Locations, Public Sector and Smart Cities, and Other End user Industries), Deployment Model (Public-cloud managed, Vendor-hosted private cloud, and Self-hosted virtual controller), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 8-port and below |

| 16-port Models |

| 24-port Models |

| 48-port Models |

| 96-port and Chassis-based |

| 1 GbE |

| 2.5/5 GbE (Multigig) |

| 10 GbE |

| 25/40 GbE |

| 100 GbE and above |

| Large Enterprises |

| Small and Medium Enterprises |

| Educational Institutions |

| Healthcare Facilities |

| Hospitality and Retail Locations |

| Public Sector and Smart Cities |

| Other End user Industries |

| Public-cloud managed |

| Vendor-hosted private cloud |

| Self-hosted virtual controller (on-prem IaaS) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of the Asia-Pacific | ||

| Middle East and Africa | Middle East | UAE |

| Saudi Arabia | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Port Count | 8-port and below | ||

| 16-port Models | |||

| 24-port Models | |||

| 48-port Models | |||

| 96-port and Chassis-based | |||

| By Switch Capacity (Data-rate) | 1 GbE | ||

| 2.5/5 GbE (Multigig) | |||

| 10 GbE | |||

| 25/40 GbE | |||

| 100 GbE and above | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | Educational Institutions | ||

| Healthcare Facilities | |||

| Hospitality and Retail Locations | |||

| Public Sector and Smart Cities | |||

| Other End user Industries | |||

| By Deployment Model | Public-cloud managed | ||

| Vendor-hosted private cloud | |||

| Self-hosted virtual controller (on-prem IaaS) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of the Asia-Pacific | |||

| Middle East and Africa | Middle East | UAE | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the cloud managed switch market expected to grow through 2031?

The cloud managed switch market size stood at USD 1.94 billion, reached USD 2.12 billion in 2026 and is forecast to reach USD 3.34 billion by 2031, equating to a 9.48% CAGR over the period, according to Mordor Intelligence.

Which port count segment will expand the quickest?

Chassis-based and 96-port platforms show the fastest trajectory, advancing at an 18.43% CAGR as AI inference clusters and spine-leaf fabrics demand higher density, per Mordor Intelligence.

Why are healthcare networks upgrading at a higher rate than other industries?

Medical IoT growth and stricter privacy mandates push hospitals to cloud managed switches that offer segment isolation and compliant logging, driving a 16.62% CAGR for the healthcare segment.

What share of deployments relies on public-cloud controllers today?

Public-cloud-managed models represented 43.82% of installations in 2025, with hybrid approaches gaining ground where data-sovereignty rules apply, based on Mordor Intelligence data.

Which region will contribute the most incremental revenue by 2031?

Asia-Pacific is projected to deliver the largest incremental gain, expanding at a 15.32% CAGR due to smart-city investment and sovereign-cloud programs across China, India, and ASEAN.

How concentrated is vendor competition?

The top five suppliers account for roughly 60% of revenue, so while leadership is clear, ample room remains for challengers to win share through specialized hardware or flexible licensing.

Page last updated on: