Distribution and Core Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

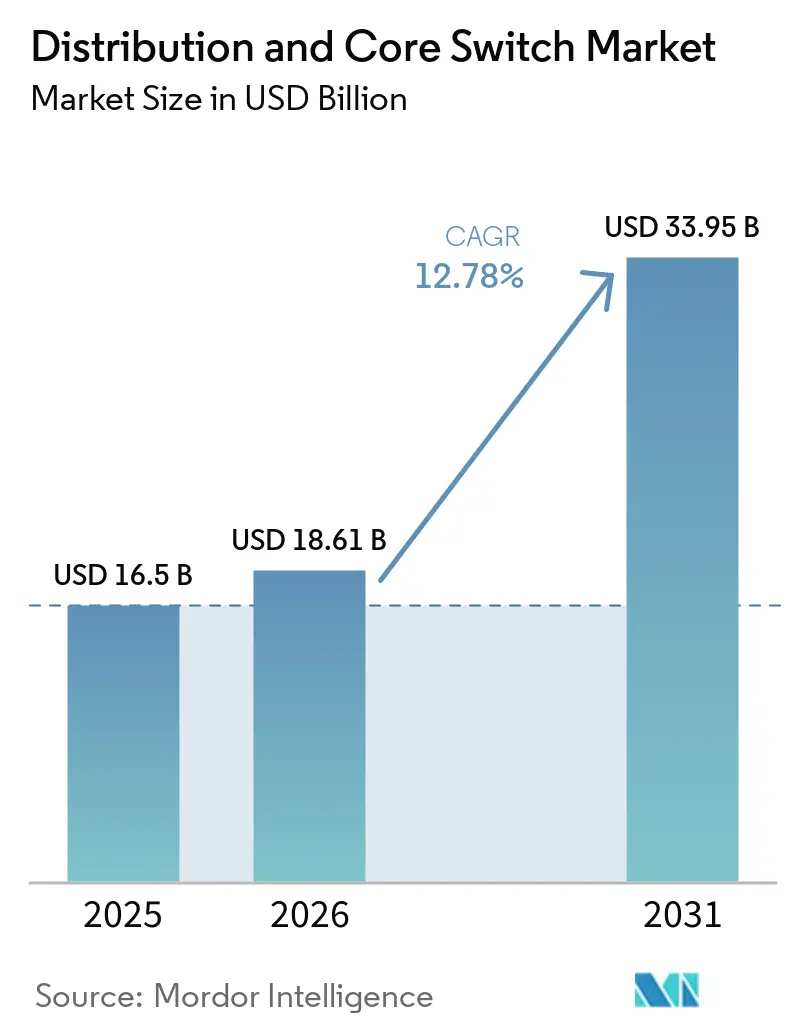

| Market Size (2026) | USD 18.61 Billion |

| Market Size (2031) | USD 33.95 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Distribution and Core Switch Market Analysis by Mordor Intelligence

The distribution and core switch market size is expected to increase from USD 18.61 billion in 2026 to USD 33.95 billion by 2031, growing at a CAGR of 12.78% over 2026-2031. Robust capital spending by hyperscale cloud providers, steady 5G backhaul modernization, and the rise of industrial Ethernet are expanding addressable demand. Operators are standardizing on 400-gigabit and 800-gigabit fabrics to ease artificial-intelligence workload congestion, which is steering spending toward high-density chassis that support non-blocking architectures. Government broadband programs in North America and Europe are adding fresh orders for gigabit-capable aggregation switches, and open-networking initiatives are lowering per-port costs, widening adoption among price-sensitive enterprises. Core switching platforms are commanding premium prices as buyers favor modularity and field-replaceable line cards that future-proof expansion.

Key Report Takeaways

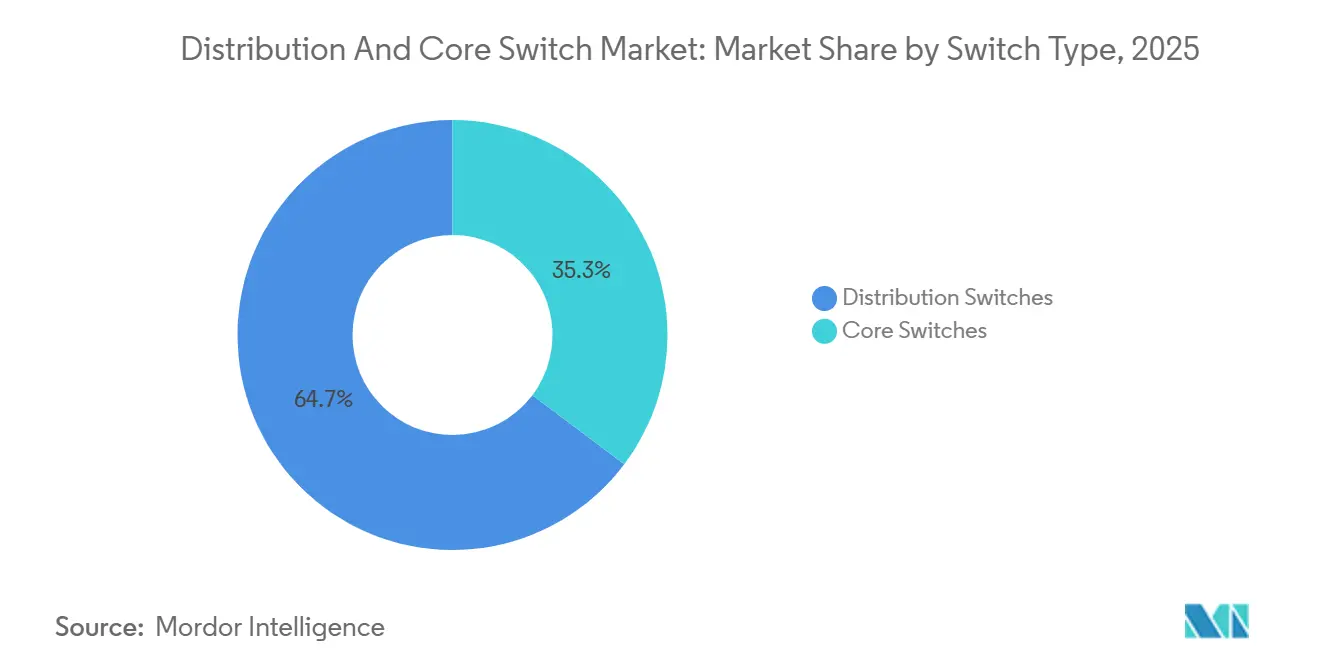

- By switch type, distribution switches led with 64.73% revenue share in 2025, while core switches are projected to grow at a 15.45% CAGR through 2031.

- By form factor, fixed-configuration units held 53.47% of the distribution and core switch market share in 2025, whereas blade switches are forecast to expand at 15.20% over 2026-2031.

- By port speed, legacy 1-gigabit to 10-gigabit links accounted for 46.60% of deployments in 2025, yet 100-gigabit uplinks are advancing at a 14.81% CAGR to 2031.

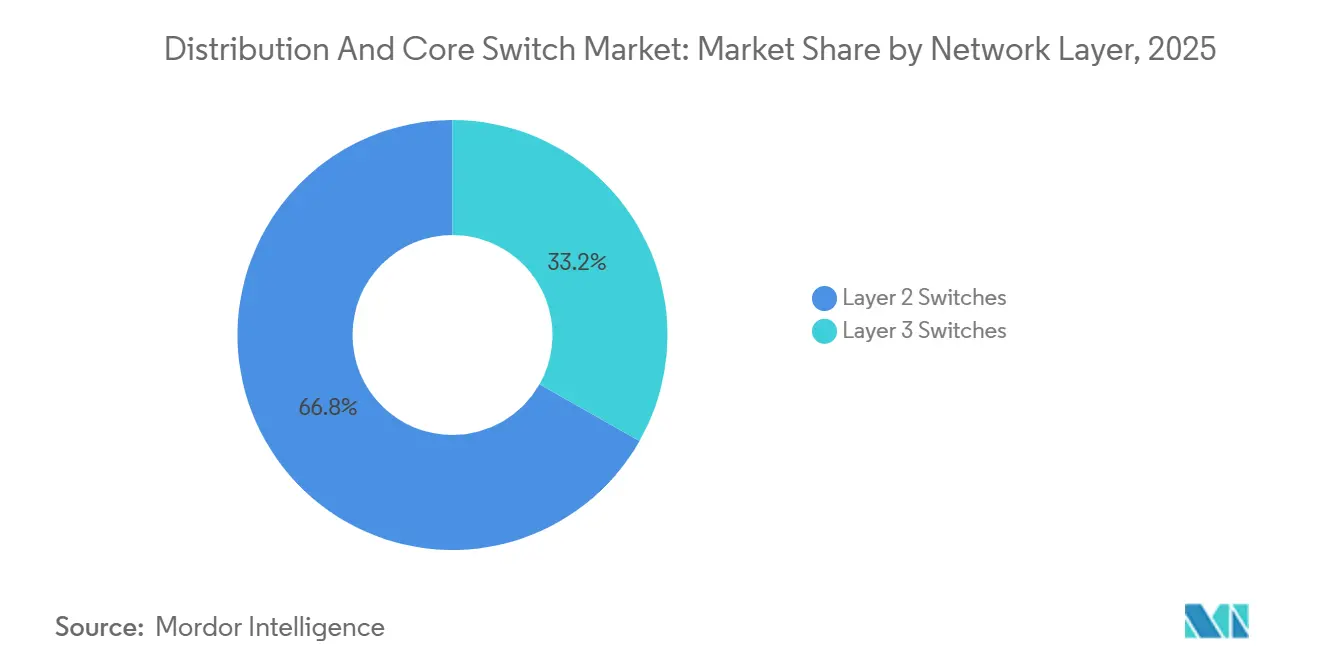

- By network layer, Layer 2 switches represented 66.80% of installations in 2025, although Layer 3 platforms are accelerating at 15.72% a year through 2031.

- By end-user industry, data centers controlled 49.50% of spending in 2025, while telecommunications operators are expected to post 14.10% CAGR during 2026-2031.

- By geography, Asia-Pacific captured 37.50% of 2025 revenue and is forecast to expand at 14.40% annually to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Distribution and Core Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cloud Service Provider Investments in Hyperscale Facilities | +3.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2–4 years) |

| Expansion of 5G Backhaul and Fronthaul Networks | +2.8% | Global, with early momentum in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Rising Adoption of 400G and 800G Ethernet to Support AI Workloads | +2.5% | North America and Asia-Pacific hyperscale clusters | Medium term (2–4 years) |

| Rapid Growth of Industrial Ethernet in Manufacturing 4.0 | +1.9% | Europe and Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Increased Government Funding for Digital Infrastructure Modernization | +1.6% | North America and Europe rural broadband zones | Medium term (2–4 years) |

| Emergence of Open Networking and Disaggregated Switching Platforms Driving Cost Efficiency | +1.4% | Global, led by hyperscalers and large service providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud Service Provider Investments in Hyperscale Facilities

Hyperscale operators commission availability zones that require thousands of spine and leaf switches, and every greenfield campus deploys 12-16 core chassis alongside 200-300 top-of-rack units to sustain east-west traffic. Google signaled USD 175 billion-USD 185 billion in 2026 capital outlays, with most of the budget earmarked for AI infrastructure connecting GPU clusters on 800-gigabit fabrics. Amazon Web Services is adding a USD 12 billion Louisiana site that will house 500,000 servers, each attaching to distribution switches through dual 100-gigabit uplinks. Alibaba Cloud is planning three new data centers near Beijing to reach one exaflop of capacity, further lifting demand for multi-terabit core platforms. Retrofit projects at colocation providers such as Equinix add another replacement cycle because tenants expect 400-gigabit connectivity for hybrid-cloud workloads.

Expansion of 5G Backhaul and Fronthaul Networks

Radio access upgrades break out new fronthaul segments that ferry digitized signals between radio heads and baseband units, shifting traffic patterns onto Ethernet and converged packet-optical gear. AT&T extended fiber paths to 14,000 towers in 2025, inserting aggregation switches at each hub to multiplex multiple sectors. Verizon directed USD 18.5 billion toward C-Band densification, placing low-latency switching at every ring to keep end-to-end delay under 5 ms. European operators follow a similar script: Deutsche Telekom allocated EUR 17 billion (USD 18.1 billion) to synchronous Ethernet-ready platforms, and Orange is investing EUR 15 billion (USD 16.0 billion) to sunset time-division multiplexing gear. These rollouts favor modular chassis that accept future 200-gigabit and 400-gigabit optics, protecting investments as traffic per site pushes past 10 Gbps.

Rising Adoption of 400G and 800G Ethernet to Support AI Workloads

Distributed AI training saturates networks with terabytes of gradient data, so operators migrate from 100-gigabit leaf-spine designs to 400-gigabit or 800-gigabit layers. NVIDIA’s Spectrum-X delivered 1.6 times higher training throughput than traditional fabrics.[1]NVIDIA Engineering, “Accelerating AI Training with NVIDIA Spectrum-X Ethernet Fabric,” nvidia.comMeta outfitted its AI Research SuperCluster with 400-gigabit back-end links to keep tail latency below one microsecond. Arista posted 180% year-over-year growth in 400-gigabit port shipments in Q4 2024, confirming hyperscale adoption momentum. IEEE 802.3df ratification jump-started 800-gigabit pilots, and LinkedIn is already testing the technology to halve spine counts, trimming capital outlays by 25%.

Rapid Growth of Industrial Ethernet in Manufacturing 4.0

Factories are abandoning proprietary fieldbuses for time-sensitive networking (TSN) over standard Ethernet, enabling deterministic communication between programmable logic controllers, robots, and vision systems. Siemens installed SCALANCE XM-400 switches with sub-microsecond synchronization across automotive plants. Cisco shipped over 100,000 rugged IE3400 units certified to IEC 61850-3 for harsh electrical environments. Moxa’s EDS-4000 series introduced recovery rings that restore connectivity within 20 ms, minimizing line stoppages. Manufacturers also demand IEC 62443-compliant firmware to harden operational technology networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility in High-Speed Switch ASICs | -1.8% | Global, acute in North America and Europe hyperscale deployments | Short term (≤ 2 years) |

| Energy Consumption Concerns of High-Density Switches | -1.5% | Global, regulatory pressure in Europe and North America | Medium term (2–4 years) |

| Escalating Cybersecurity Compliance Costs for Critical Networks | -1.2% | Europe and North America critical infrastructure sectors | Medium term (2–4 years) |

| Skills Shortage in Managing Software-Defined Networks in Emerging Markets | -0.9% | Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility in High-Speed Switch ASICs

Advanced switching silicon is fabricated on 5-nm and 3-nm nodes that remain capacity-constrained through 2027. Broadcom’s Tomahawk 5 and Jericho3-AI devices saw lead times stretch beyond six months in 2025, and Marvell’s Prestera pipeline faced similar bottlenecks as hyperscalers prepaid wafer slots 18 months ahead. Shortages also hit indium phosphide lasers for coherent 400-gigabit pluggables, while printed-circuit vendors struggle with tight impedance tolerances needed for 112-Gbps serial lanes. Several operators delayed facility openings by up to three quarters, postponing switch orders.

Energy Consumption Concerns of High-Density Switches

A fully loaded 51.2-terabit chassis can draw 8 kW, inflating power bills and carbon footprints. The U.S. Environmental Protection Agency updated ENERGY STAR specifications in 2024, demanding idle-state efficiency gains of 20% over 2020 baselines.[2]U.S. Environmental Protection Agency, “ENERGY STAR Network Equipment,” energystar.gov H3C’s liquid-cooled S12500G-AF trimmed consumption by 30% but requires specialized plumbing. Cisco introduced transceiver power control in IOS XE 17.15, saving 2 W per 400-gigabit port. U.S. tax credits for data centers achieving sub-1.2 PUE ratios are nudging operators toward energy-optimized switches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Type: Core Platforms Anchor AI Fabrics

Core switches captured smaller revenue than distribution switches in 2025 but will outstrip them with 15.45% annual growth through 2031. The distribution and core switch market size allocated to premium chassis is rising because hyperscale buyers insist on 51.2-terabit non-blocking fabrics that keep GPU clusters saturated. Arista’s 7800R4, delivering 230.4 Tbps in one frame, became the reference spine for AI back-end networks in 2025. Core configurations favor modularity, redundant supervisors, and hot-swappable line cards that allow incremental scaling without downtime. At the same time, distribution platforms remain indispensable in campus aggregation and service-provider edge roles, but price competition from white-box vendors is muting their revenue trajectory. The distribution and core switch market continues to pivot toward chassis that can migrate from 400-gigabit to 800-gigabit optics via field-upgradeable PHY mezzanines.

Growth is also linked to architectural change. Leaf-spine Clos fabrics replace three-tier hierarchies, so what once acted as a backbone router is now a latency-critical spine layer that must tolerate microbursts without head-of-line blocking. This function rewards ASIC pipelines that support deep buffer, cut-through forwarding, and high-precision telemetry. Premium chassis list between USD 500,000 and USD 800,000, lifting average selling prices and boosting the distribution and core switch market even as unit counts flatten. Open Compute Project designs, published by Meta and Google, are shifting a slice of core deployments to merchant-silicon white boxes, but enterprises still lean on integrated offerings that include orchestration, analytics, and embedded security.

By Form Factor: Blade Designs Thrive in Converged Racks

Fixed-configuration switches held 53.47% share in 2025 thanks to simplicity and lower upfront cost, yet blade switches are advancing at 15.20% as converged infrastructure proliferates. Embedding the network into compute chassis shortens cable runs, trims power draw by 15%, and saves rack space. Cisco UCS and HPE Synergy both employ internal midplane backplanes, reducing top-of-rack clutter and easing airflow. Hyperconverged vendors exploit this design to ship turnkey private-cloud nodes that can be installed in remote offices without specialized staff. Dell’s PowerEdge MX sold more than 50,000 enclosures in 2025, illustrating appetite for integrated fabrics tied to software-defined storage.

Conversely, modular chassis retain dominance in large enterprise cores and telecom aggregation because field-replaceable cards and redundant supervisors drive downtime toward zero. Fixed configurations still rule at the edge of enterprise campuses, especially where Wi-Fi 6E and Wi-Fi 7 access points attach at multi-gigabit speeds. The distribution and core switch market size attached to blade units remains modest today but will expand as container-based workloads, analytics, and virtual desktop infrastructure converge on standardized sleds.

By Port Speed: 100 Gbit/s Uplinks Bridge Two Worlds

Links operating at 1-gigabit to 10-gigabit commanded 46.60% of 2025 shipment volume, yet the 100 Gigabit tier is growing at 14.81% a year to 2031. Enterprises refreshing campus cores adopt 100 Gbit/s uplinks as QSFP28 modules slide below USD 200, delivering a cost-effective leap that preserves existing multimode fiber. In data centers, 100 Gbit/s serves as the leaf layer feeding 400 Gbit/s spines, striking a balance between performance and optics cost. Cisco’s Nexus 9300-GX2, with 48 ports of 100 Gbit/s in one rack unit, was the best-selling leaf switch in 2025.

At the top end, 400 Gigabit and 800 Gigabit segments accelerate on the back of AI fabric buildouts. Arista’s 7060X6 and Juniper’s PTX10008 integrate 400 Gbit/s line cards, while LinkedIn is testing 800 Gbit/s optics to cut spine counts by half. Component costs remain steep—an 800 Gbit/s pluggable still exceeds USD 10,000—but hyperscalers accept premiums in exchange for rack consolidation and reduced fiber runs. The distribution and core switch market share for sub-40 Gigabit uplinks is slipping as server network-interface cards settle on 25 Gigabit and 50 Gigabit lanes that map cleanly into 100 Gigabit switch ports.

By Network Layer: Routing Intelligence Moves to the Edge

Layer 2 switches held 66.80% share in 2025 because they are easy to configure and suit retail and hospitality footprints. Nonetheless, Layer 3 devices are slated to expand at 15.72% annually as enterprises push software-defined wide-area architectures into branch sites. Embedding routing in the access layer allows direct cloud breakout, cutting latency for SaaS traffic by 40%. Cisco Catalyst SD-WAN boxes shipped more than 200,000 units in 2025, proving demand for integrated routing-and-switching appliances.

Internet-of-Things proliferation is another catalyst. Smart cameras, building controls, and industrial sensors require segmentation to keep operational data isolated, which nudges buyers toward devices that support VRF-lite, policy-based routing, and secure tunnel termination. Extreme Networks, Fortinet, and Juniper are packaging firewall and routing features into switching hardware to appeal to zero-trust initiatives. The distribution and core switch market therefore tilts toward multi-layer functionality as pure L2 deployments give way to policy-driven overlay networks.

By End-User Industry: Telcos Accelerate Standalone 5G

Data centers represented 49.50% of 2025 outlays, but telecommunications carriers are the fastest riser at 14.10% CAGR through 2031. Standalone 5G cores separate control and user planes, spawning dozens of micro data centers at the network edge, each hosting a gateway stack hooked to spine-leaf fabrics. AT&T’s fiber-to-tower project and Verizon’s C-Band densification both depend on distribution switches to aggregate traffic and maintain strict latency budgets. Carrier upgrades also favor deterministic transport, synchronizing time across radio heads using precision timing extensions embedded in switch silicon.

Government, enterprise, and public-sector buyers form the balance of demand. U.S. Broadband Equity Access and Deployment funds funnel USD 42.45 billion into rural fiber builds, creating new nodes that require gigabit-capable aggregation. Enterprises redesign campuses for hybrid work, installing software-defined access fabrics built around Catalyst 9500 or Aruba CX platforms. Industrial end users in oil, gas, and transportation adopt ruggedized gear that tolerates wide temperature swings and voltage fluctuations, boosting sales of IEC-compliant models from Moxa and Hirschmann.

Geography Analysis

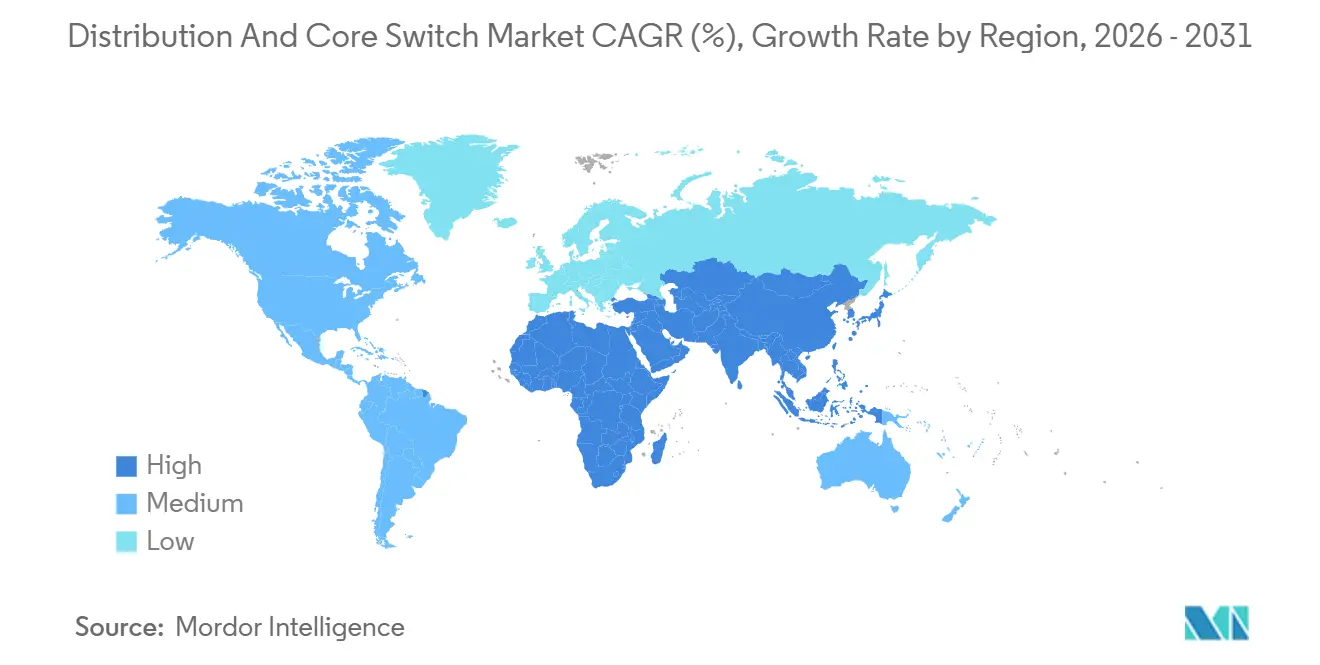

Asia-Pacific led the distribution and core switch market with 37.50% share in 2025 and is projected to expand at a 14.40% CAGR to 2031. China’s national computing-hub strategy calls for ten mega campuses that each deploy thousands of non-blocking chassis, and Alibaba Cloud is adding three Beijing-area sites targeting one exaflop of AI performance. Tencent reserved CNY 50 billion (USD 6.9 billion) for data center expansion, while India’s USD 6.36 billion BharatNet Phase III fiber project demands gigabit-capable aggregation at 250,000 rural exchanges. South Korea’s SK Telecom and Japan’s NTT are both scaling 400 Gigabit fabrics to underpin national AI clusters, driving sustained orders for high-density switches.[3]NTT Corporation, “Annual Report 2024,” group.ntt

North America maintains a substantial revenue base due to hyperscaler capital expenditures that topped USD 200 billion in 2025. Google, AWS, Microsoft, and Meta each fund new availability zones with 800 Gigabit spines, and U.S. broadband programs underwrite rural aggregation builds. Canada follows suit with fiber subsidies, whereas Mexico’s reforms encourage competitive carrier builds albeit at a slower cadence.

Europe shows steady expansion, anchored by Deutsche Telekom’s EUR 17 billion (USD 18.1 billion) and Orange’s EUR 15 billion (USD 16.0 billion) modernization programs. The EU Digital Decade mandate for universal gigabit coverage by 2030 stimulates fiber rollouts that hinge on Layer 3 aggregation. Operators must also comply with the NIS2 Directive, spurring demand for switches that embed real-time threat detection.

The Middle East and Africa and South America account for smaller slices, yet mega projects such as Saudi Arabia’s USD 20 billion data-center plan and Brazil’s rural 5G buildouts introduce fresh orders. Currency volatility and supply-chain variability moderate near-term growth, but long-term digitization agendas keep pipelines active.

Competitive Landscape

Market concentration remains moderate: the five largest vendors secured roughly 60%-65% of 2025 sales, but white-box traction is eroding incumbent share. Cisco, Arista, and Juniper defend positions by bundling telemetry, security, and orchestration with ASIC roadmaps that leapfrog to 800 Gigabit and 1.6 Terabit lanes. Microsoft pushed SONiC across more than one million servers, demonstrating that open-source NOS software can shave 30%-40% off per-port cost. Meta and Google publish Open Compute Project designs, enabling Edgecore and Delta to supply commodity hardware, intensifying price pressure.

Industrial Ethernet remains fragmented, allowing specialists such as Moxa, Phoenix Contact, and Hirschmann to win deals in manufacturing and utility sectors that demand rugged specifications. NVIDIA is an emerging disruptor: Spectrum ASICs with adaptive routing sliced tail latency in AI fabrics by half, securing contracts with Azure and Oracle Cloud.[4]NVIDIA Networking, “Spectrum-X Technical Brief,” nvidia.com Regulatory drivers also tilt the field: NIS2 pushes critical-infrastructure buyers toward integrated security, an area where Fortinet’s firewall-enabled switches compete aggressively.

Vendors respond through M&A and joint ASIC programs. HPE’s USD 14 billion purchase of Juniper merges campus wireless and data-center switching portfolios under one roof, while Dell collaborated with Broadcom on Tomahawk 6 silicon to speed enterprise platforms. Liquid-cooling innovations from H3C and Huawei attack the energy constraint, and Arista’s 7060X7 doubled port density inside the same rack envelope, landing design wins with GPU-dense clusters.

Distribution and Core Switch Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Arista Networks, Inc.

Hewlett Packard Enterprise Company

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Juniper Networks closed its USD 14 billion sale to Hewlett Packard Enterprise, forming a combined USD 40 billion entity that unifies campus and data-center fabrics.

- December 2025: Arista Networks unveiled the 7060X7, a 128-port 400 Gigabit chassis with microsecond telemetry for AI workloads.

- November 2025: Cisco earmarked USD 1 billion to expand its Bangalore silicon center, focusing on 800 Gigabit and 1.6 Terabit ASICs.

- October 2025: NVIDIA signed Spectrum-X deployment agreements with Microsoft Azure, Oracle Cloud Infrastructure, and CoreWeave.

- September 2025: Huawei introduced the CloudEngine 16800, supporting 256 ports of 400 Gigabit Ethernet and network slicing.

- August 2025: Dell and Broadcom co-developed custom Tomahawk 6 ASICs for PowerSwitch Z-series enterprise leaf switches.

- July 2025: Extreme Networks bought Aerohive’s campus switching IP for USD 120 million to add cloud-managed features.

Global Distribution and Core Switch Market Report Scope

| Distribution Switches |

| Core Switches |

| Fixed Configuration Switches |

| Modular Chassis Switches |

| Blade Switches |

| 1G–10G |

| 25G–40G |

| 100G |

| 400G and Above |

| Layer 2 Switches |

| Layer 3 Switches |

| Telecommunications Service Providers |

| Data Centers (Colocation & Hyperscale) |

| Enterprises |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Switch Type | Distribution Switches | |

| Core Switches | ||

| By Form Factor | Fixed Configuration Switches | |

| Modular Chassis Switches | ||

| Blade Switches | ||

| By Port Speed | 1G–10G | |

| 25G–40G | ||

| 100G | ||

| 400G and Above | ||

| By Network Layer | Layer 2 Switches | |

| Layer 3 Switches | ||

| By End-User Industry (Demand Side) | Telecommunications Service Providers | |

| Data Centers (Colocation & Hyperscale) | ||

| Enterprises | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the distribution and core switch market and its growth outlook?

The segment is valued at USD 18.61 billion in 2026 and is projected to reach USD 33.95 billion by 2031, reflecting a 12.78% CAGR.

Which switch type shows the fastest growth through 2031?

Core platforms are set to expand at a 15.45% CAGR as hyperscale buyers prioritize multi-terabit chassis for AI fabrics.

Why are hyperscale data centers demanding 400 G and 800 G Ethernet fabrics?

Large language-model training floods networks with gradient traffic, so operators need higher bandwidth and sub-microsecond latency to keep GPU clusters fully utilized.

How is open networking affecting vendor selection for enterprises?

Disaggregated hardware running open-source NOS software can cut per-port costs by 30%-40%, prompting price-sensitive buyers to weigh white-box options against proprietary stacks.

Page last updated on: