Unmanaged Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.5 Billion |

| Market Size (2031) | USD 20.5 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unmanaged Switch Market Analysis by Mordor Intelligence

The unmanaged switch market size was valued at USD 12.50 billion in 2025 and is estimated to grow from USD 13.50 billion in 2026 to reach USD 20.50 billion by 2031, at a CAGR of 6.39% during the forecast period (2026-2031). Continual demand for plug-and-play connectivity among small and medium businesses, residential offices, and edge-industrial sites sustains steady unit volumes even as managed alternatives gain traction in enterprise cores. Multi-gigabit broadband roll-outs, expanding Power over Ethernet requirements for high-wattage cameras and access points, and regulatory pre-cabling mandates for smart buildings anchor medium-term growth. Price visibility on entry-level smart-managed models compresses margins, yet cost-sensitive buyers still favor zero-configuration hardware in the 5- to 8-port class. Supply-chain redesigns that relocate manufacturing to Southeast Asia temper component lead-times and help vendors hedge against tariff exposures, while gallium-nitride power technology improves thermal performance in emerging PoE++ designs.

Key Report Takeaways

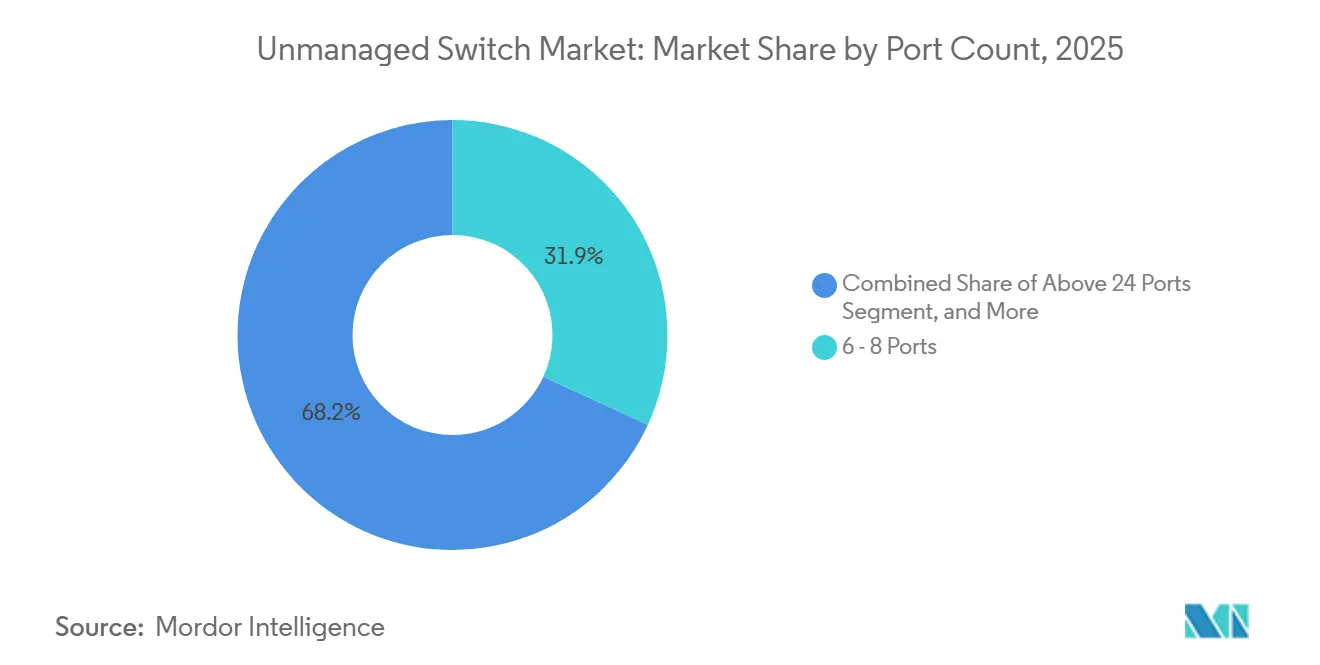

- By port count, the 6-8 port segment led with 31.85% of unmanaged switch market share in 2025, whereas the above-24-port class is projected to expand at an 8.62% CAGR through 2031.

- By PoE capability, non-PoE models accounted for 48.90% revenue in 2025, while PoE++ devices are forecast as the fastest-growing sub-category with a 9.41% CAGR to 2031.

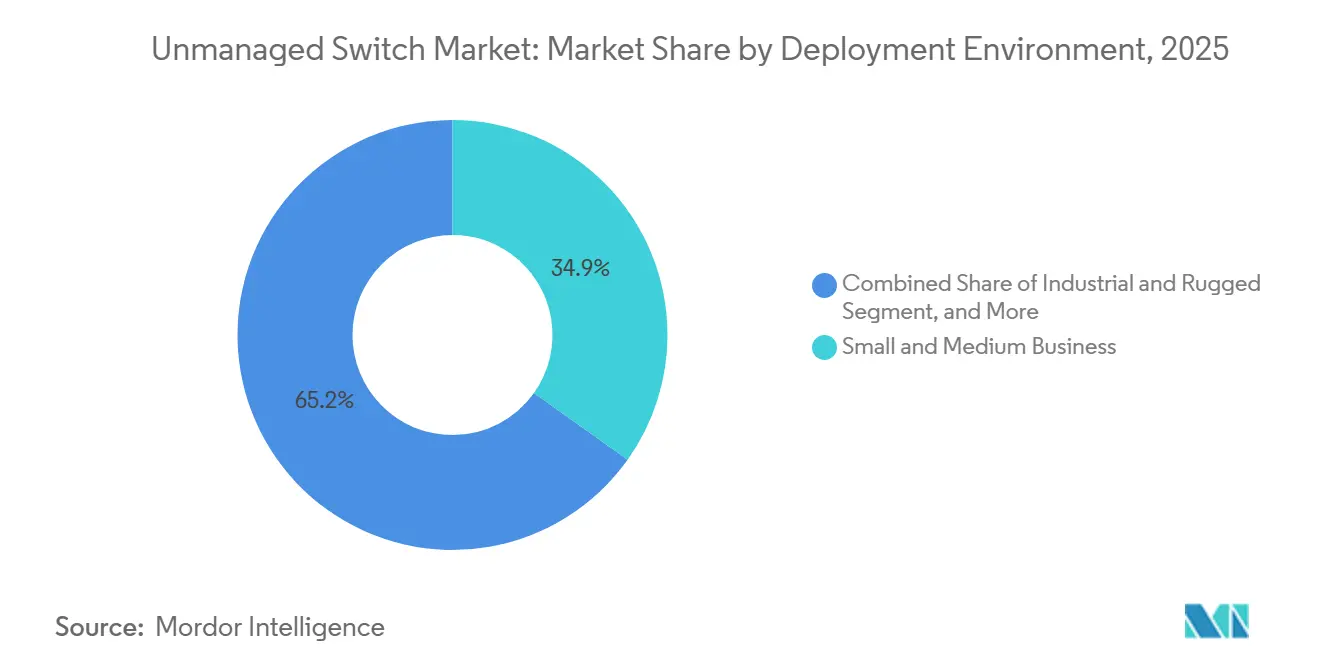

- By deployment environment, small and medium businesses held 34.85% of the unmanaged switch market size in 2025, whereas the industrial and rugged segment is set to advance at an 8.11% CAGR between 2026-2031.

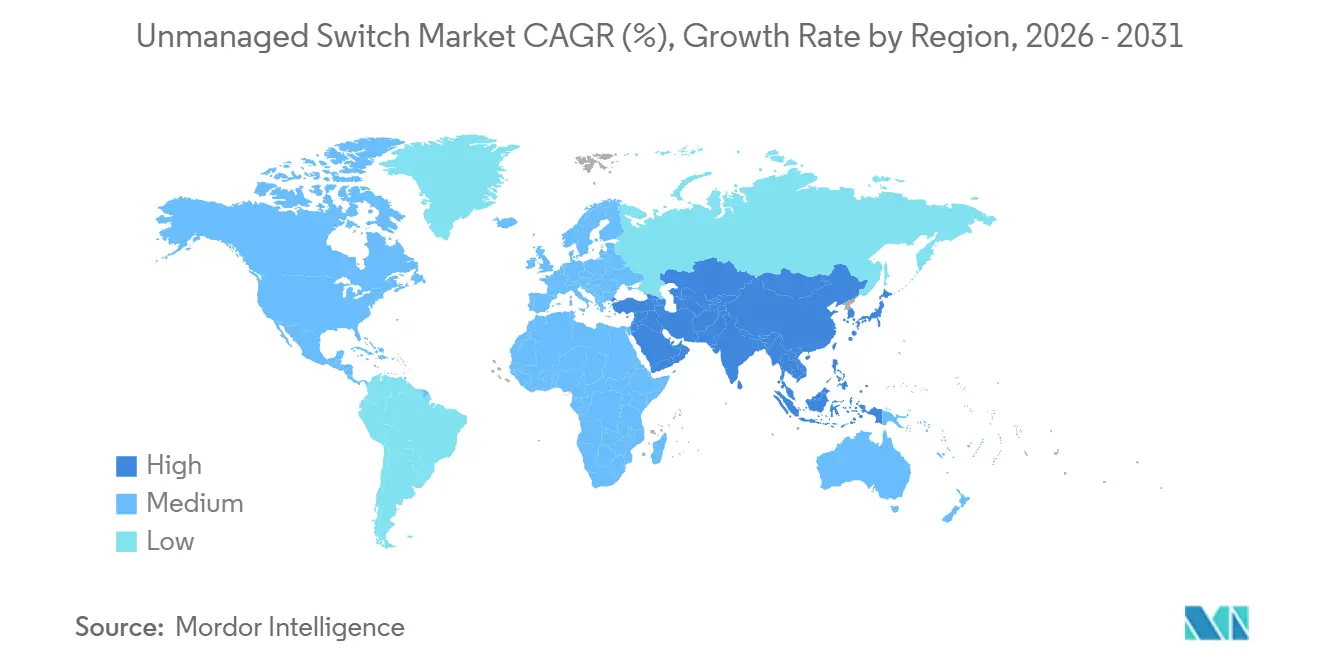

- By geography, Asia-Pacific captured 33.85% of 2025 revenue and is positioned to grow at a 7.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unmanaged Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging SMB Demand For Cost-Effective Plug-And-Play Networking | +1.8% | Global with strength in Asia-Pacific and North America | Medium term (2–4 years) |

| Expansion Of Video-Centric Surveillance Infrastructure Requiring PoE | +1.5% | Global, led by Asia-Pacific commercial and government sectors | Long term (≥4 years) |

| Home-Office Upgrades Driven By Hybrid Work Trends | +0.9% | North America and Europe, urban Asia-Pacific spillover | Short term (≤2 years) |

| Industrial Ethernet Migration In Mid-Tier Automation Lines | +1.2% | Asia-Pacific manufacturing hubs, Europe automotive and process industries | Medium term (2–4 years) |

| Government Smart-Building Mandates Embracing Low-Power Wired Backbones | +0.8% | Europe, North America, emerging Middle East | Long term (≥4 years) |

| Accelerated Fiber-To-The-Room Deployments Creating Edge Switch Refresh | +0.6% | Enterprise campuses in North America, Europe, tier-1 Asia-Pacific cities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging SMB Demand For Cost-Effective Plug-And-Play Networking

Price-sensitive small firms rarely allocate dedicated IT staff, so they adopt unmanaged devices that negotiate port speeds automatically and require no configuration. Typical 8-port Gigabit models retail well under USD 100, a figure that remains compelling even as devices per user rise to three endpoints on average. Zero-touch installation supports pop-up retail kiosks and coworking floors where cabling must be re-routed frequently. In Southeast Asian export hubs, local value-added resellers bundle low-cost switches with cloud routers to accelerate digital onboarding for first-time e-commerce merchants. Hybrid work routines further elevate branch connectivity needs as employees rotate between home and office desks, sustaining replenishment cycles for compact form factors.

Expansion Of Video-Centric Surveillance Infrastructure Requiring PoE

The global shift from analog CCTV to high-resolution IP cameras ties directly to Power over Ethernet budgets because every camera needs both data and power over the same cable. New industrial PoE++ switches now deliver up to 90 watts per port, supporting infrared-equipped PTZ units on highways and critical infrastructure. For small installations such as convenience stores or municipal parking lots, 4- and 8-port unmanaged PoE models remain adequate, enabling electricians, not IT engineers, to hang cameras quickly. As analytics migrate onto cameras themselves, higher processor loads raise wattage draw, which in turn accelerates refresh from legacy 802.3af platforms toward 802.3bt hardware.

Home-Office Upgrades Driven By Hybrid Work Trends

Part-time remote staff expect enterprise-grade video calls and low-latency file sync, pushing many to hard-wire laptops, phones, and network-attached storage. Unmanaged desktop switches fit under a standing desk and use energy-efficient Ethernet to cut idle power by up to 70% compared with earlier chipsets. Growing interest in do-it-yourself security encourages consumers to power indoor cameras over Cat6, increasing attach rates for 4-port PoE variants. Nonetheless, accelerating Wi-Fi 6E and Wi-Fi 7 adoption in North America tempers port growth as single-radio routers deliver multi-gigabit wireless throughput.[1]Cisco Systems, “Wi-Fi 7 And The Growing Future Of Wireless Design Guide,” cisco.com

Industrial Ethernet Migration In Mid-Tier Automation Lines

Automakers, electronics subcontractors, and food processors are phasing out fieldbus links in favor of deterministic Ethernet protocols such as PROFINET and EtherNet/IP. Unmanaged DIN-rail switches with IP30 housings, redundant 24 V DC inputs, and -40 °C to +75 °C ratings align with panel-level budgets where configuration is unnecessary. Vendors including Fiberroad and Phoenix Contact reinforce broadcast-storm protection at silicon level to maintain determinism. Asia-Pacific’s China-Plus-One factory wave adds thousands of machine-level nodes in Vietnam, Malaysia, and India, magnifying demand for inexpensive, rugged eight-port units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feature Creep Of Low-Cost Managed Switches Cannibalizing Unmanaged Sales | -1.1% | Global, most visible in North America and Europe enterprises | Short term (≤2 years) |

| Security Vulnerabilities From Lack Of Traffic Segmentation | -0.7% | Global, heightened in regulated industries | Medium term (2–4 years) |

| Wi-Fi 6E And 7 Reducing Edge Port Growth In SOHO | -0.5% | North America and Europe residential and small offices | Short term (≤2 years) |

| Semiconductor Supply Disruptions Elevating BOM Costs | -0.4% | Global, acute for commodity vendors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Feature Creep Of Low-Cost Managed Switches Cannibalizing Unmanaged Sales

Smart-managed models dipped below USD 300 for 48 ports in 2025, bundling VLAN tagging, SNMP monitoring, and cloud dashboards that once carried enterprise-grade premiums. Zyxel’s XMG2230 series, released in 2026, layers multi-gigabit speeds and 2,400-watt PoE budgets onto SMB offerings while retaining intuitive app-based setup.[2]Zyxel Networks, “Zyxel Networks Launches New Era Of Multi-Gig High-Power PoE Connectivity With XMG2230 Series,” zyxel.com Buyers in 16- to 24-port bands increasingly perceive minimal savings when foregoing management, eroding unmanaged volumes in mainstream offices. Vendors answer with hybrid profiles configured by rotary switches, yet this middle ground risks cannibalizing both sides of the portfolio.

Security Vulnerabilities From Lack Of Traffic Segmentation

Flat Layer 2 domains allow any compromised endpoint to laterally probe every other device, violating zero-trust mandates. The April 2026 disclosure of CVE-2026-6988 on an unmanaged edge model underscores real-world exploitability, scoring 8.8 on the CVSS scale with public proof-of-concept code. Financial services and healthcare audits now require VLANs or ACLs even at wiring-closet edges, pushing regulated workloads toward managed hardware. European NIS2 and IEC 62443 impose segmentation and logging obligations on industrial sites, accelerating retrofit programs that displace legacy unmanaged backbones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Port Count: High-Density Edge Aggregation Gains Traction

The unmanaged switch market size for 6-8 port models remained dominant in 2025 as shops, clinics, and home offices typically require fewer than ten wired devices. Compact plastics enclosures and wall-wart power designs keep acquisition costs low, reinforcing volume leadership. Conversely, above-24-port chassis class products, often rack-mounted, benefit from data-center edge and industrial control-panel rollouts that aggregate dozens of sensors per rack. Multi-gigabit uplinks and SFP+ cages are entering this tier, enabling seamless spine connections without stepping up to managed software stacks.

Demand in 9- to 24-port bands faces stiff headwinds from feature-rich smart-managed alternatives that now retail only slightly higher, yet buyers focused purely on bandwidth, not segmentation, may consider D-Link’s newly released 2.5-gigabit unmanaged lines. Manufacturers strive to retain share by offering fanless thermal designs, integrated power supplies, and front-panel DIP control of energy-saving modes. Consequently, the unmanaged switch market share for ultra-dense categories is projected to climb fastest through 2031 as building-side edge aggregation embraces zero-touch provisioning in smart campuses.

By PoE Capability: High-Power Standards Drive Fastest Growth

Non-PoE units represented nearly half of 2025 revenue, reflecting legacy environments where endpoints source local power. Nevertheless, the unmanaged switch market size tied to PoE++ is expanding the quickest as Wi-Fi 6E access points and 4K PTZ cameras push per-port budgets toward 90 watts. Gallium-nitride transistors, showcased by TRENDnet, shrink power-supply footprints by roughly 40% and lower thermal resistance, enabling fanless eight-port models that still deliver 480 watts aggregate.

PoE and PoE+ devices maintain moderate growth as VoIP handsets and fixed-lens cameras keep cycling out 100 Mb s hardware. EU building codes that require networked EV chargers and energy-meter sensors validate Cat6A cabling for both data and power, sustaining refresh in commercial real estate. For unmanaged brands, differentiation now leans on total power budget, surge protection, and automatic port classification rather than traditional packet features.

By Deployment Environment: Industrial Segment Outpaces Traditional SMB

While SMB offices contributed over one-third of unmanaged switch market share in 2025, volume expansion slows as branch IT teams pivot toward entry-level cloud-managed gear for visibility. In contrast, factories, substations, and transport systems tap rugged DIN-rail models certified for -40 °C to +75 °C operation, sealed housings, and redundant 24 V DC feeds. Industrial Ethernet’s advance in mid-tier automation lines, particularly across Vietnam and India, underpins an 8.11% CAGR to 2031.

Residential and home offices form a stable but substitution-prone base as Wi-Fi bandwidth milestones reduce wired drops. Data-center edge closets add incremental demand for 24- and 48-port variants with fiber uplinks that aggregate IoT sensors and building-automation devices. Across every environment, unmanaged switch market size gains hinge on balancing minimal touch deployment with environmental ruggedization or high-power PoE capability rather than classic Layer 2 features.

Geography Analysis

Asia-Pacific led unmanaged switch market share at 33.85% in 2025 and continues to outpace global averages at a 7.56% CAGR as manufacturers diversify beyond mainland China. Vietnam’s north-south industrial corridor, India’s production-linked incentive districts, and Malaysia’s Johor electronics clusters collectively commission thousands of machine-level Ethernet nodes each quarter. In parallel, smart-city pilots in Seoul and Singapore install unmanaged PoE junction boxes at lamp posts and traffic signals, boosting port densities despite rising wireless penetration.

North America remains a sizeable contributor yet confronts cannibalization from low-cost managed entrants in open-plan offices and co-working venues. Still, hybrid-work home upgrades support ongoing refresh cycles for five- and eight-port desktop units, while private-sector spending on PoE++ access-point refresh sustains demand in the education vertical. Enterprise campuses that adopt fiber-to-the-room laminates deploy above-24-port rack-mount chassis at floor aggregation closets to terminate copper runs.

Europe’s market reflects regulatory pull as the recast Energy Performance of Buildings Directive prescribes structured cabling for EV charging, meters, and sensors.[3]European Commission, “Providing Guidance On New Or Substantially Modified Provisions Of The Recast Energy Performance Of Buildings Directive (EU) 2024/1275,” Official Journal Of The European Union, europa.eu Cost-effective unmanaged switch market deployments satisfy per-floor consolidation needs in commercial retrofits where centralized building-management software already resides in cloud services. Middle East and Africa growth gravitates toward utility substations, CCTV-heavy public-safety grids, and oilfield telemetry huts, all environments that require IP67 casings and extended temperature operations. South America, led by Brazil’s retail chains and Mexico’s maquiladora factories, gradually embraces unmanaged PoE refresh as supply constraints ease and currency headwinds stabilize.

Competitive Landscape

Competition remains moderately fragmented. Netgear, TP-Link, D-Link, and Zyxel dominate the consumer and SMB tiers through retail shelves and e-commerce bundles, while Belden, Phoenix Contact, Siemens, Moxa, and Rockwell Automation address industrial buyers via system integrators. Price tension escalated in 2025 when smart-managed units dropped below USD 300, encouraging SMBs to reserve unmanaged purchases for ultra-compact or harsh-environment use cases. Vendors emphasize three vectors of differentiation: first, multi-gigabit unmanaged devices with 2.5 Gb s copper and 10 Gb s SFP+ uplinks that satisfy creator studios and edge-compute closets; second, PoE++ platforms leveraging gallium-nitride power modules for 90-watt per-port delivery with fanless acoustics; and third, rugged DIN-rail options that merge shock resistance with compliance to PROFINET conformance class A.

Chinese challengers such as Ruijie and Kyland press aggressive pricing in emerging markets, while Ubiquiti’s simplified UniFi consoles blur category lines by offering lightweight management through a smartphone app. Belden’s demonstration of a 5G-enabled switch prototype at Hannover Messe hints at future convergence where private-5G backhauls share enclosures with Ethernet aggregation. Semiconductor tightness, particularly for PHYs and magnetics, plus copper and bromine price spikes, squeeze gross margins on commodity 8-port units, reinforcing vendor interest in higher-value industrial and PoE++ niches where ASPs remain resilient.

Unmanaged Switch Industry Leaders

Netgear Inc.

TP-Link Corporation Limited

D-Link Corporation

Zyxel Communications Corporation

Shenzhen Tenda Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: D-Link introduced 16-port and 24-port 2.5-gigabit unmanaged switches in Australia and New Zealand, positioning the range for bandwidth-intensive creative studios and hybrid-work offices.

- April 2026: Belden unveiled the BRS-5G prototype at Hannover Messe, integrating a Snapdragon X72 modem to enable Ethernet switching with native private-5G backhaul for factory automation.

- April 2026: Versitron released two compact copper-to-fiber unmanaged models with industrial-grade housings, expanding options for surveillance and transportation deployments.

- February 2026: Zyxel rolled out XMG2230 multi-gigabit Layer 3 PoE access switches targeting SMBs upgrading to Wi-Fi 7, offering up to 2,400-watt power budgets and Nebula Cloud management.

- June 2025: Phoenix Contact debuted DIN-rail REG switches optimized for building-automation cabinets, featuring automatic PoE detection and tool-free busbar mounting.

Global Unmanaged Switch Market Report Scope

The Unmanaged Switch Market features plug-and-play Ethernet switches that function without user intervention. Offering fundamental connectivity for smaller networks, these switches are budget-friendly, straightforward to deploy, and demand minimal technical know-how. Their appeal is particularly strong among small businesses, limited-scale industrial setups, and cost-sensitive network applications.

The Unmanaged Switch Market Report is Segmented by Port Count (5 Ports and Below, 6-8 Ports, 9-16 Ports, 17-24 Ports, and Above 24 Ports), PoE Capability (Non-PoE, PoE [802.3af], PoE+ [802.3at], and PoE++ [802.3bt]), Deployment Environment (Residential and Home Office, Small and Medium Business, Enterprise and Campus, Industrial and Rugged, and Data Center Edge), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 5 Ports and Below |

| 6 - 8 Ports |

| 9 - 16 Ports |

| 17 - 24 Ports |

| Above 24 Ports |

| Non-PoE |

| PoE (802.3af) |

| PoE+ (802.3at) |

| PoE++ (802.3bt) |

| Residential and Home Office |

| Small and Medium Business |

| Enterprise and Campus |

| Industrial and Rugged |

| Data Center Edge |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Port Count | 5 Ports and Below | |

| 6 - 8 Ports | ||

| 9 - 16 Ports | ||

| 17 - 24 Ports | ||

| Above 24 Ports | ||

| By PoE Capability | Non-PoE | |

| PoE (802.3af) | ||

| PoE+ (802.3at) | ||

| PoE++ (802.3bt) | ||

| By Deployment Environment | Residential and Home Office | |

| Small and Medium Business | ||

| Enterprise and Campus | ||

| Industrial and Rugged | ||

| Data Center Edge | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the unmanaged switch market size in 2026?

The unmanaged switch market size is projected at USD 13.50 billion in 2026.

Which port-count category grows fastest through 2031?

Above-24-port unmanaged switches register the highest forecast CAGR at 8.62%, fueled by data-center edge and industrial aggregation needs.

How does PoE++ adoption influence vendor strategies?

PoE++ switches that deliver up to 90 watts per port enable high-power cameras and Wi-Fi 7 access points, prompting suppliers to integrate gallium-nitride power stages for compact fanless designs.

Why are unmanaged switches still popular in Asia-Pacific factories?

Rapid factory expansions in Vietnam, Malaysia, and India favor low-complexity, rugged DIN-rail devices that technicians can install without network configuration training.

What security risks are associated with unmanaged switches?

Lack of VLAN segmentation creates flat networks vulnerable to lateral movement, a concern underscored by the high-severity CVE-2026-6988 buffer-overflow disclosure on an edge model.

Page last updated on: