Brazil Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

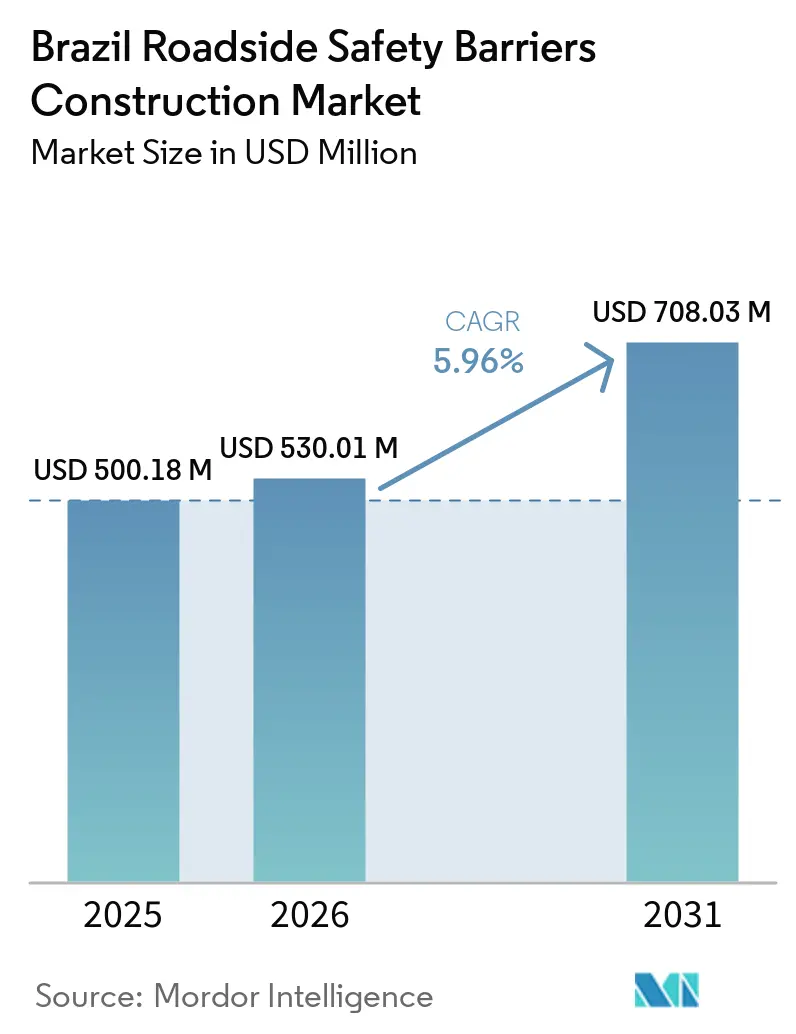

| Base Year Market Size (2025) | USD 500.18 Million |

| Market Size (2026) | USD 530.01 Million |

| Market Size (2031) | USD 708.03 Million |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

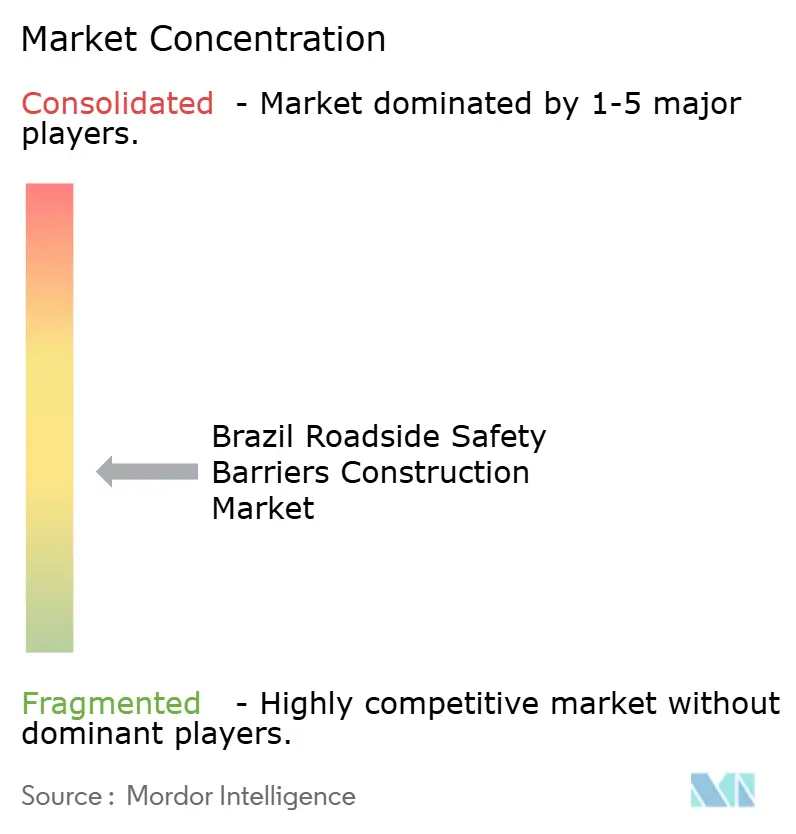

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The Brazil Roadside Safety Barriers Construction Market size is expected to grow from USD 500.18 million in 2025 to USD 530.01 million in 2026 and is forecast to reach USD 708.03 million by 2031 at 5.96% CAGR over 2026-2031. The expansion of tolled corridors, implementation of data-driven crash-reduction programs, and mandatory adherence to the 2016 edition of ABNT NBR 15486 are key factors driving demand in new federal and state highway concessions. Private operators, including VINCI, Arteris, EcoRodovias, and Motiva, fund barrier upgrades through long-term user-fee revenue streams, helping to reduce the safety disparity between concessioned and directly managed roads. São Paulo's adoption of the International Road Assessment Program (iRAP) methodology on a statewide level, along with DNIT's coding of 54,500 km of federal highways, ensures that limited public funds are allocated to segments where median and roadside barriers can achieve the greatest reduction in crash severity. Advances in materials, such as tire-rubber concrete and energy-absorbing crash cushions, are expanding the supplier base and introducing circular-economy benefits. These developments come at a time when Brazil's import-dependent steel value chain is experiencing currency and price volatility.

Key Report Takeaways

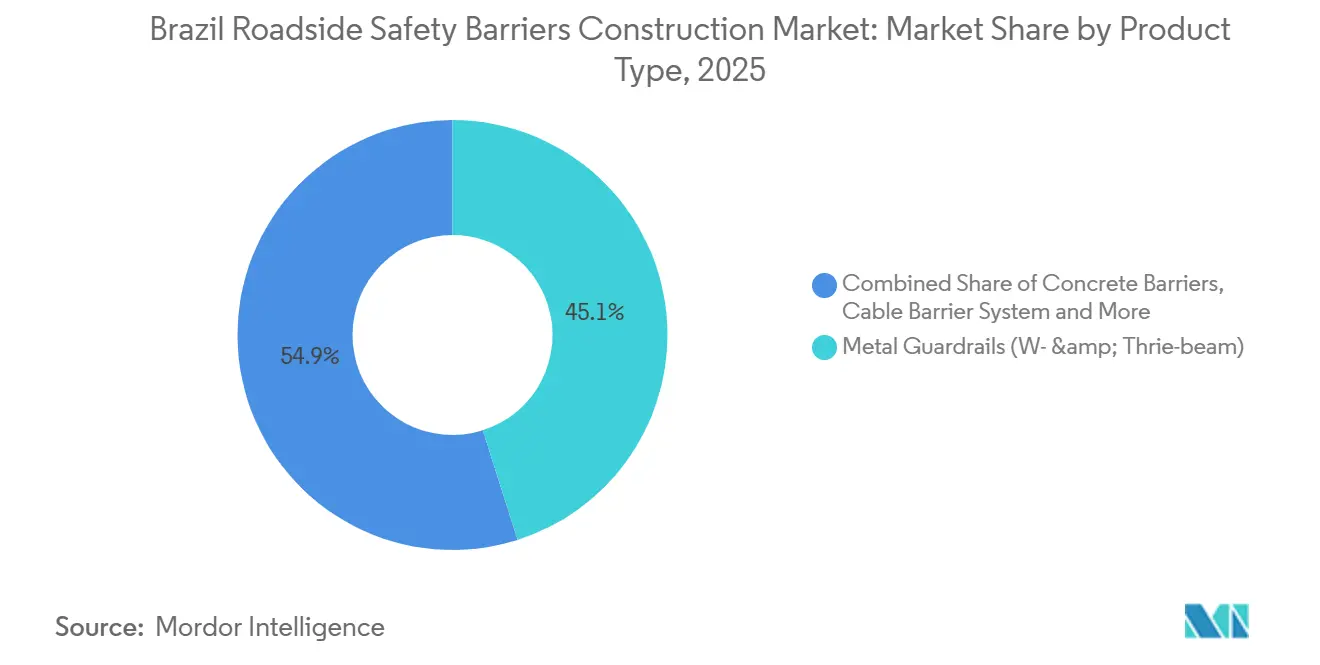

- By product type, metal guardrails captured 45.1% of Brazil roadside safety barriers construction market share in 2025; crash cushions are projected to advance at 6.71% CAGR through 2031.

- By material, steel accounted for 56.7% of the Brazil roadside safety barriers construction market size in 2025, while plastic & composites are poised to expand at 6.89% CAGR over 2026-2031.

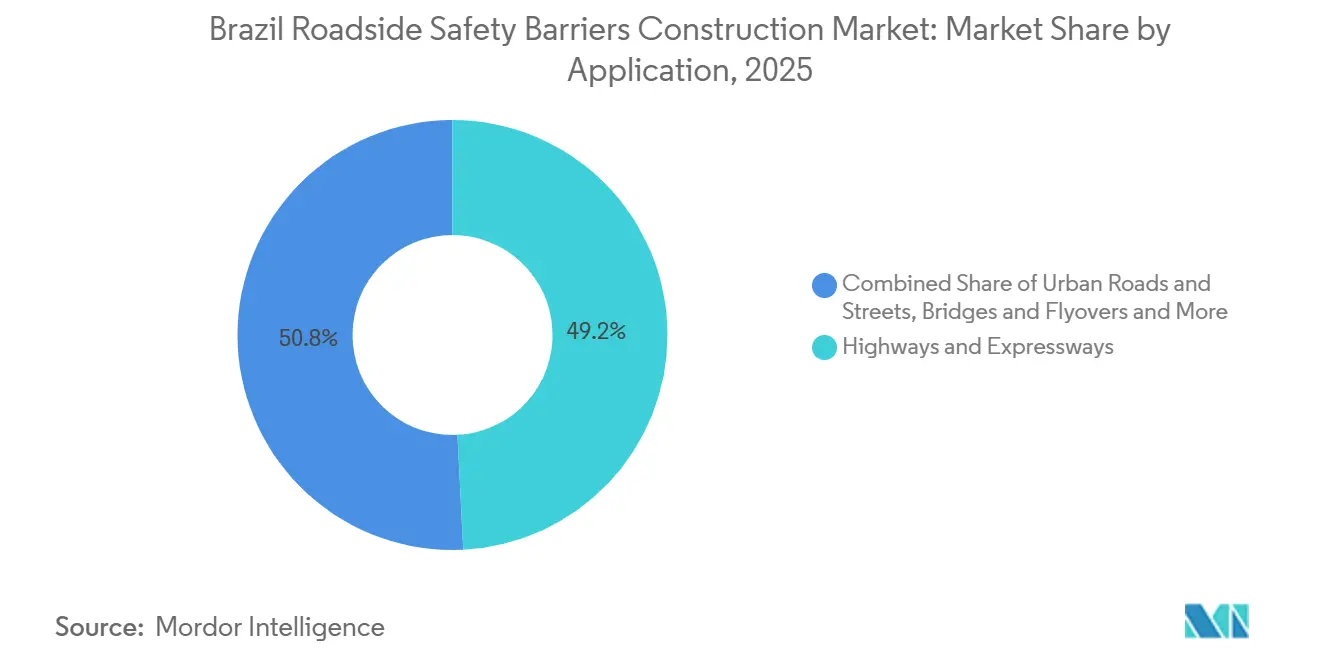

- By application, highways & expressways led with 49.2% revenue in 2025; bridges & flyovers represent the fastest-growing use, rising at 6.65% CAGR to 2031.

- By installation, new projects held 62.8% of the 2025 spend; renovation and retrofit work is expected to grow at 6.49% CAGR as aging infrastructure reaches end-of-life standards.

- At the city level, São Paulo generated 38.9% of 2025 demand, whereas Salvador is forecast to deliver the highest growth at 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal and state highway concession programs increasing barrier upgrades across tolled corridors | +1.7% | São Paulo, Rio de Janeiro, Bahia, Minas Gerais corridors | Medium term (2–4 years) |

| BrazilRAP and DNIT road-safety initiatives driving installations on high-risk highway stretches | +1.5% | 54,500 km federal network; São Paulo state | Medium term (2–4 years) |

| Highway duplication, widening, and rehabilitation works expanding demand for median and roadside barriers | +1.2% | BR-040, BR-101, BR-163, BR-116, BR-381 | Long term (≥ 4 years) |

| Freight-heavy corridors and bridge approaches increasing need for stronger edge-protection systems | +0.9% | BR-163, BR-040, BR-116 | Medium term (2–4 years) |

| Crash-reduction priorities on federal roads accelerating replacement of outdated roadside protection hardware | +0.7% | BR-116, BR-101, other high-fatality segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Federal and State Highway Concession Programs Accelerating Upgrades

Long-duration concessions require operators to comply with staged ABNT NBR 15486 standards, leading to the systematic replacement of outdated guardrails with crash-tested systems. VINCI's BR-040 concession (594 km, 30 years, BRL 10.1 billion [USD 2.02 billion]) initiated this trend, followed by Arteris on BR-101/RJ and EcoRodovias on the 735 km Rota Gerais corridor. Operators recover their investments through toll revenues and long-term debt, avoiding reliance on federal budgets. This approach results in a two-tier network, where concessioned highways implement high-containment barriers years ahead of directly managed roads.

BrazilRAP and DNIT road-safety initiatives driving installations on high-risk highway stretches

BrazilRAP’s iRAP assessments provide star ratings that enable DNIT to allocate limited funds to the most hazardous road segments. In 2025, the agency allocated BRL 320 million (USD 64 million) for safety countermeasures, with 70% designated for installing barriers on one- and two-star roads. São Paulo adopted this model for its state road network, offering municipalities a standardized approach to prioritization. Enhanced data transparency fosters public pressure to address safety gaps on non-tolled road sections.[1]International Road Assessment Programme, “BrazilRAP Star Rating Results,” irap.org.

Highway duplication, widening, and rehabilitation works expanding demand for median and roadside barriers

The conversion of single to dual carriageways includes the addition of a median that requires proper shielding. The duplication of the BR-163 corridor reduced fatalities by 25% within a year following the installation of concrete and cable barriers. Bridge renovation projects, such as the BR-101/BA Jequitinhonha initiative (BRL 104.7 million [USD 20.9 million]), combine barrier upgrades with deck repairs, achieving economies of scale[2]Departamento Nacional de Infraestrutura de Transportes, “Programa de Duplicação e Restauração de Rodovias Federais 2025-2028,” gov.br.

Freight-heavy corridors and bridge approaches increasing need for stronger edge-protection systems

Corridors accommodating 38-ton trucks experience higher impact loads, while historic standards permitted lower-containment rails. Recent concessions now require H4-class equivalent barriers, leading to the implementation of systems such as Deltabloc’s DB 120 precast concrete barrier on SP-270. At bridge entries, operators install energy-absorbing crash cushions, with Lindsay’s ABSORB and TAU II lines being the most commonly used, to reduce fatal run-off-road collisions[3]Agência Nacional de Transportes Terrestres, “Perfil de Carga Pesada nos Corredores BR-040, BR-163 e BR-116,” gov.br.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited public budgets outside concessioned networks constrain barrier deployment on secondary roads | −0.5% | North and Northeast non-concessioned networks | Long term (≥ 4 years) |

| Steel-intensive barrier systems remain exposed to input-cost pressure and higher replacement costs | −0.4% | Nationwide fabricators using hot-rolled coil and galvanized sheet | Short term (≤ 2 years) |

| Fragmented federal and state implementation processes are slowing procurement and installation timelines | −0.3% | States without centralized road agencies | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Limited public budgets outside concessioned networks constrain barrier deployment on secondary roads

DNIT’s 2025 maintenance budget of BRL 7.95 billion [USD 1.59 billion] addressed only about half of the identified requirements, compelling the agency to delay barrier projects outside major routes. State amendments have resulted in a broad distribution of funds—2,607 municipalities shared BRL 2.9 billion [USD 580 million] in 2024—leaving rural roads in the North and Northeast regions with limited protection. Unless there is a transition to performance-based state concessions, improvement efforts will remain concentrated on tolled corridors.

Steel-intensive barrier systems remain exposed to input-cost pressure and higher replacement costs

Imports accounted for 18.5% of Brazilian steel demand in 2024, exposing local guardrail manufacturers to currency fluctuations. While ArcelorMittal is investing BRL 3.8-4.0 billion (USD 0.76-0.8 billion) to expand coated-sheet production capacity, the facility is not expected to become operational until 2029. In the interim, fluctuating coil prices are reducing contractor margins and could delay retrofit projects when budgets are tendered under fixed-price agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Crash Cushions Gain Traction at High-Risk Terminals

Metal guardrails accounted for 45.1% of Brazil's roadside safety barrier construction market share in 2025. Their low installation cost, ease of installation, and compliance with ABNT NBR 6971 standards make them the preferred choice for greenfield lanes and rural shoulders. Local companies such as Armco Staco and Hexxa Metal supply galvanized W-beam and Thrie-beam rails that integrate seamlessly into DNIT bid templates. However, concessionaires managing bridge-heavy corridors are increasingly opting for higher-energy absorption devices.

Crash cushions are projected to grow at a compound annual growth rate (CAGR) of 6.71%, the highest among product categories. ANTT’s concession contracts require operators to safeguard toll islands, gore areas, and bridge abutments using ABNT NBR 15486-certified attenuators. Products such as Lindsay Corporation’s ABSORB modular system, the TAU II family, and Deltabloc’s Stop + Go units have become popular choices, as they reduce occupant deceleration and minimize post-impact repair time. As more corridors undergo their five-year audits, crash cushions are expected to transition from isolated applications to systematic deployment plans aligned with global Vision Zero objectives.

By Material: Composites Challenge Steel’s Incumbency

Steel accounted for 56.7% of the projected 2025 revenue, driven by the availability of domestic coil supply and a well-established fabrication ecosystem. Pre-galvanized guardrails, with a lifespan of 15-20 years under tropical conditions, remain the most cost-effective option per meter, making them a key component in calculating the size of Brazil's roadside safety barriers construction market. Concrete is primarily used in median applications, with precast Jersey walls, such as Deltabloc’s DB 80 and DB 120 units, offering H4-class containment for freight-heavy lanes.

Plastic and composite barriers are expected to grow at a CAGR of 6.89% through 2031. A notable innovation in this segment is DI Concrete’s tire-rubber concrete rail, which incorporates 25% shredded rubber into the concrete mix. Two pilot projects in São Paulo demonstrated impact strength comparable to traditional precast barriers while repurposing 32 million end-of-life tires, reducing landfill waste. A broader implementation across 3,200 km of DER-SP and concessionaire networks could significantly increase the composite market share and enhance ESG credentials for upcoming concession tenders.

By Application: Bridge and Flyover Rehabilitation Drives Demand

Highways and expressways accounted for 49.2% of the projected 2025 spending, as each new lane duplication includes median and roadside rails. Operators are expanding BR-163 and BR-381 using precast concrete or steel guardrails to meet H3/H4 containment standards, integrating barrier costs into pavement contracts. Urban streets receive comparatively lower funding, as municipal budgets prioritize signage, lighting, and drainage over safety rails.

Bridges and flyovers exhibit the highest growth potential, with a projected CAGR of 6.65%. The DNIT has classified over 1,000 structures as “sofrível” or worse, necessitating remedial work that mandates compliance with ABNT NBR 15486 barrier standards. The BR-101/BA Jequitinhonha bridge project, completed in December 2025 for BRL 104.7 million (USD 20.9 million), serves as a benchmark. The project included deck replacement, seismic bearings, and the installation of new concrete parapets with TAU II crash cushions at both ends. As similar projects are implemented, demand for bridge-specific products—such as stiff posts, taller parapets, and stainless anchor bolts—is expected to increase within the Brazil roadside safety barriers construction market.

By Installation Type: Retrofit Momentum Builds

New installations accounted for 62.8% of the 2025 expenditures, driven by lane expansions on BR-040 and BR-101, as well as the initiation of concessions earlier in the year. W-beam guardrails and DB 80 concrete segments were installed in new medians efficiently, ensuring adherence to project timelines.

The retrofit and repair segment is expected to grow at a CAGR of 6.49% due to the aging federal road network. According to ABNT NBR 6971 standards, reuse is permitted only if the steel's structural integrity and galvanization remain intact, a requirement that many rails from the 2000s fail to meet. Continuous maintenance contracts in Minas Gerais cover 1,000 km and allocate BRL 700 million (USD 140 million) for barrier replacements through 2027. Municipal projects, such as those in Valinhos (1.5 km, BRL 727,000 [USD 145,400]) and Piracema (BRL 92,904 [USD 18,580]), highlight localized demand that complements large-scale federal initiatives.

Geography Analysis

São Paulo accounted for 38.9% of the projected 2025 expenditure, reinforcing its position as the cornerstone of Brazil's roadside safety barriers construction market. The state's extensive concession network—including Nova Raposo, Rota Sorocabana, and Entrevias—combines multi-lane traffic with consistent toll revenue, enabling operators to implement high-containment Deltabloc DB 120 barriers in dense urban medians. Additionally, São Paulo's 2024 adoption of iRAP star ratings shifts the focus from kilometers of barriers installed to the reduction of crash severity, prioritizing investments in areas where barriers can most effectively reduce accident impacts. Pilot projects using tire-rubber concrete on Raposo Tavares and the Tietê ring road further position São Paulo as a leader in adopting environmentally sustainable materials.

Salvador and its BA-093 road system represent a significant growth area. During the June 2024 São João holiday, the six-road hub handled 295,000 vehicles, prompting Bahia Norte, the concessionaire, to allocate BRL 236 million (USD 47.2 million) for slope stabilization and roadside barrier installations. Furthermore, a World Bank-supported USD 200 million asset-management program will establish 10-year performance contracts covering 1,000 km of roads, incorporating barrier requirements aligned with federal concession standards.

The remaining market activity is spread across Rio de Janeiro, Minas Gerais, Mato Grosso, and Rio Grande do Sul. In Rio de Janeiro, Arteris' BR-101/RJ project involves an investment of BRL 10.1 billion (USD 2.02 billion) for 322 km of coastal roadways, including 12 bridges requiring ABNT NBR 15486-rated crash cushions. Meanwhile, EcoRodovias' Rota Gerais and Motiva's Fernão Dias corridors connect agricultural regions to export ports, embedding higher-containment standards into the center-south transportation network. In contrast, northern regions face budgetary constraints under DNIT, but the potential involvement of multilateral lenders, guided by BrazilRAP data, could lead to targeted retrofitting initiatives in the future.

Competitive Landscape

Brazil's supplier base for roadside safety barriers is divided between volume-focused guardrail manufacturers and technology-driven specialty providers. Armco Staco, with a 111-year history of local fabrication, leads in municipal contracts where cost efficiency and rapid delivery are key priorities. Companies like Transit Soluções and smaller galvanizers handle overflow projects, supplying W-beam kits that are installed using pneumatic drivers at rates exceeding 800 meters per crew per day.

International companies are gaining market share in Brazil's concession corridors. Lindsay Corporation operates from a Campinas hub, offering ABSORB and TAU II cushions that meet both NCHRP 350 and ABNT NBR 15486 certifications, addressing operator liability requirements. Deltabloc supplies EN 1317 H4b-compliant precast concrete barriers, which are widely used on São Paulo's SP-270 and SP-280 expressways. These barriers are valued for their 80 km/h impact resistance and low maintenance needs. Recent projects include a 16-kilometer installation of DB 120 barriers for a VINCI-operated segment, completed overnight to minimize traffic disruptions.

Innovative materials are introducing new competition in the market. DI Concrete's patent-pending tire-rubber mix has been used in pilot installations and has received a conditional award for 3,200 kilometers of DER-SP and concession roads, pending full-scale crash testing scheduled for 2026. Meanwhile, ArcelorMittal and Tata Steel LATAM are strengthening the coil supply chain, with plans to expand into coated sheet production. This move is expected to increase domestic value capture once the Tubarão cold-strip line becomes operational in 2029. Additionally, as ANTT phases out legacy NBR 14885 concrete rails on tolled lanes, existing players will need updated crash-test data and CE factory certification to remain competitive in Brazil's roadside safety barriers construction market.

Brazil Roadside Safety Barriers Construction Industry Leaders

Armco Staco S.A.

ArcelorMittal Brasil

Marangoni

Segurvia

Deltabloc do Brasil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EcoRodovias won the BR-101 (ES–BA) optimization auction and committed R$10.3 billion over 10 years for duplications, bypasses, 40 pedestrian footbridges, and the associated roadside-safety-barrier upgrades.

- June 2025: Segurvia began field deployment of licensed precast “New Jersey” concrete barriers on EcoRodovias corridors in São Paulo and Paraná—the first large-scale Brazilian use of the 6 m interlocking modules.

- May 2025: Marangoni’s Limeira plant obtained CE “Constancy of Performance” certification, confirming local production of >100 Road Steel crash-tested H2/H4 bridge and urban barrier models for Brazil.

Brazil Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| São Paulo |

| Rio de Janeiro |

| Salvador |

| Rest of Brazil |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By City | São Paulo |

| Rio de Janeiro | |

| Salvador | |

| Rest of Brazil |

Key Questions Answered in the Report

How large will the Brazil roadside safety barriers construction market be by 2031?

It is forecast to reach USD 708.03 million by 2031, growing at a 5.96% CAGR from 2026 to 2031.

Which product line is gaining the most momentum?

Crash cushions and impact attenuators are projected to expand at 6.71% CAGR as concessions make them mandatory at high-risk terminals.

Why is São Paulo the largest regional market?

A dense toll-road network, IRAP-based prioritization, and early adoption of composite barriers give São Paulo 38.9% of 2025 spending.

What role do composites play in future growth?

Plastic & composite barriers, led by tire-rubber concrete, are set to grow 6.89% CAGR as ESG criteria influence concession awards.

How are private concessions influencing standards?

Concession contracts mandate staged compliance with ABNT NBR 15486, accelerating the replacement of outdated barriers across tolled corridors.

Are retrofit projects becoming more common?

Yes, retrofit and repair work is forecast to rise 6.49% CAGR as thousands of kilometers of early-2000s guardrails reach the end of their service life.

Page last updated on: