Brazil Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

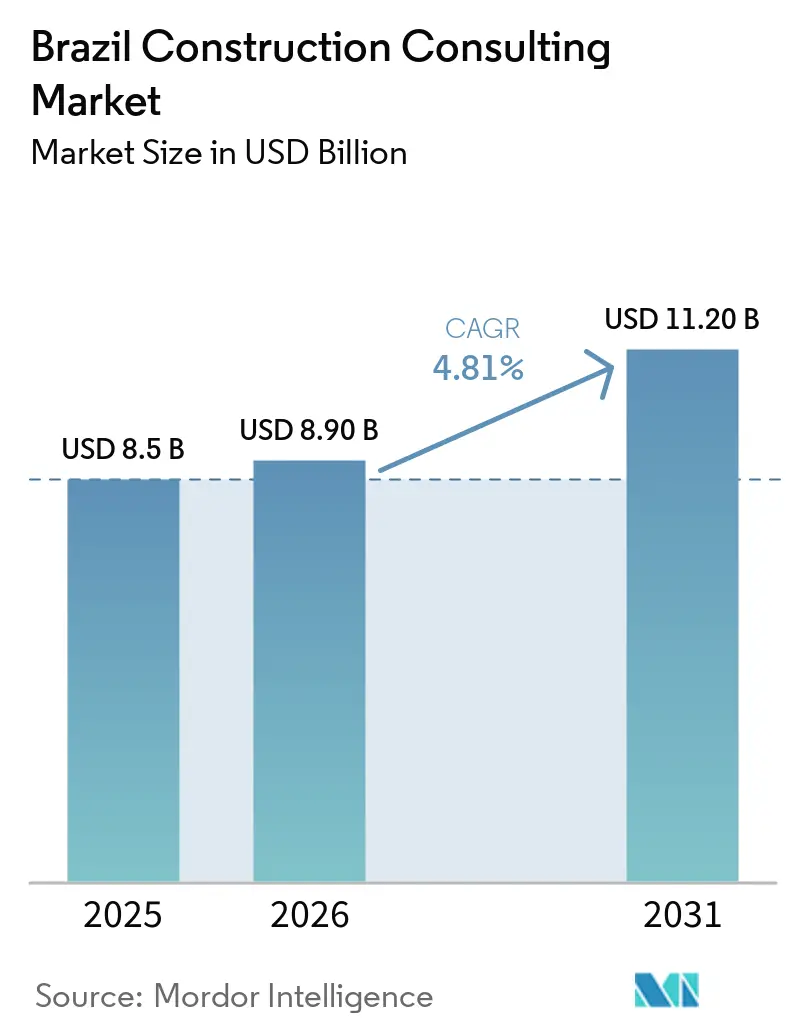

| Base Year Market Size (2025) | USD 8.5 Billion |

| Market Size (2026) | USD 8.90 Billion |

| Market Size (2031) | USD 11.20 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Construction Consulting Market Analysis by Mordor Intelligence

The Brazil construction consulting market size is expected to grow from USD 8.5 billion in 2025 to USD 8.9 billion in 2026 and is forecast to reach USD 11.2 billion by 2031 at 4.81% CAGR over 2026-2031. Accelerated infrastructure spending under the Novo PAC program, mandatory third-party technical supervision in public works, and the spread of Building Information Modeling (BIM) mandates are combining to lift project-management and design workloads. However, lowest-price procurement rules and bundled engineering-procurement-construction (EPC) contracts continue to depress fee levels for undifferentiated advisors. Demand is concentrating in data center developments, adaptive-reuse renovations, and concessionaire due diligence assignments that require specialized financial, environmental, and digital-twin expertise. International majors are leveraging global BIM platforms to win complex mandates, while domestic firms retain local advantage in state and municipal tenders that reward pre-existing relationships.

Key Report Takeaways

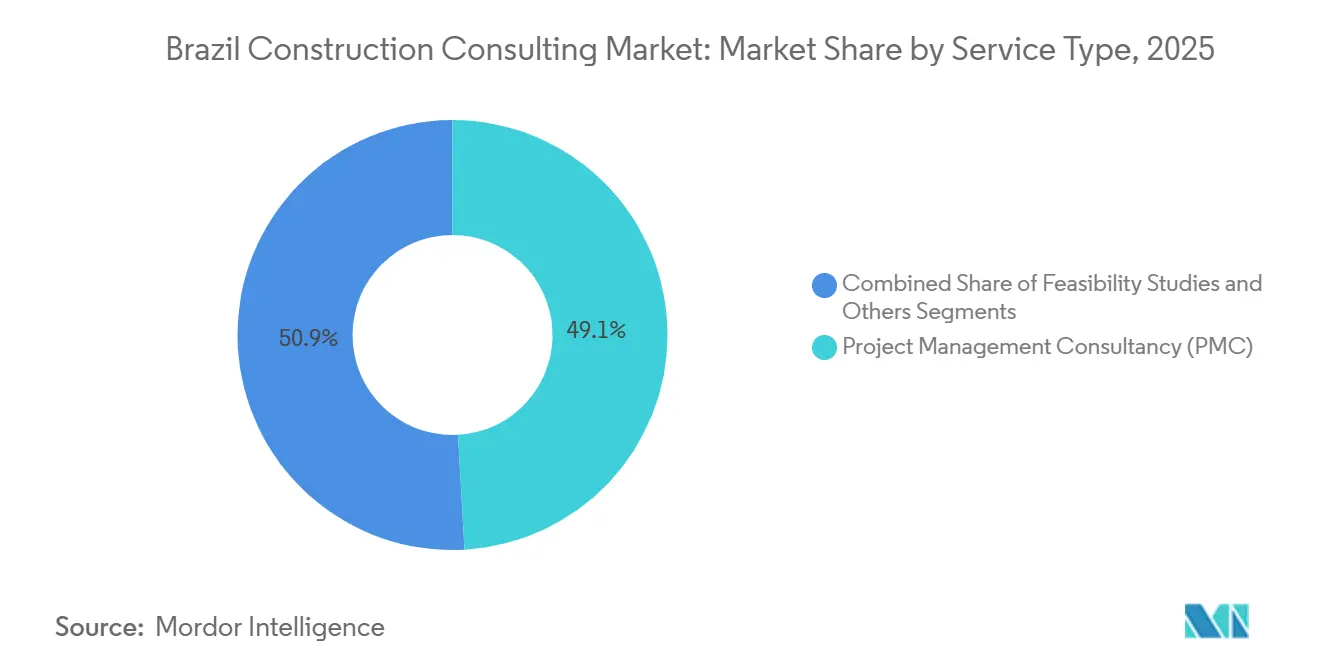

- By service type, Project Management Consultancy led with 49.12% of Brazil construction consulting market share in 2025, while Design and Engineering Services is projected to advance at a 6.16% CAGR through 2031.

- By sector, Residential held 43.22% share of the Brazil construction consulting market size in 2025, yet Infrastructure is on track to expand at 5.58% CAGR over the forecast window.

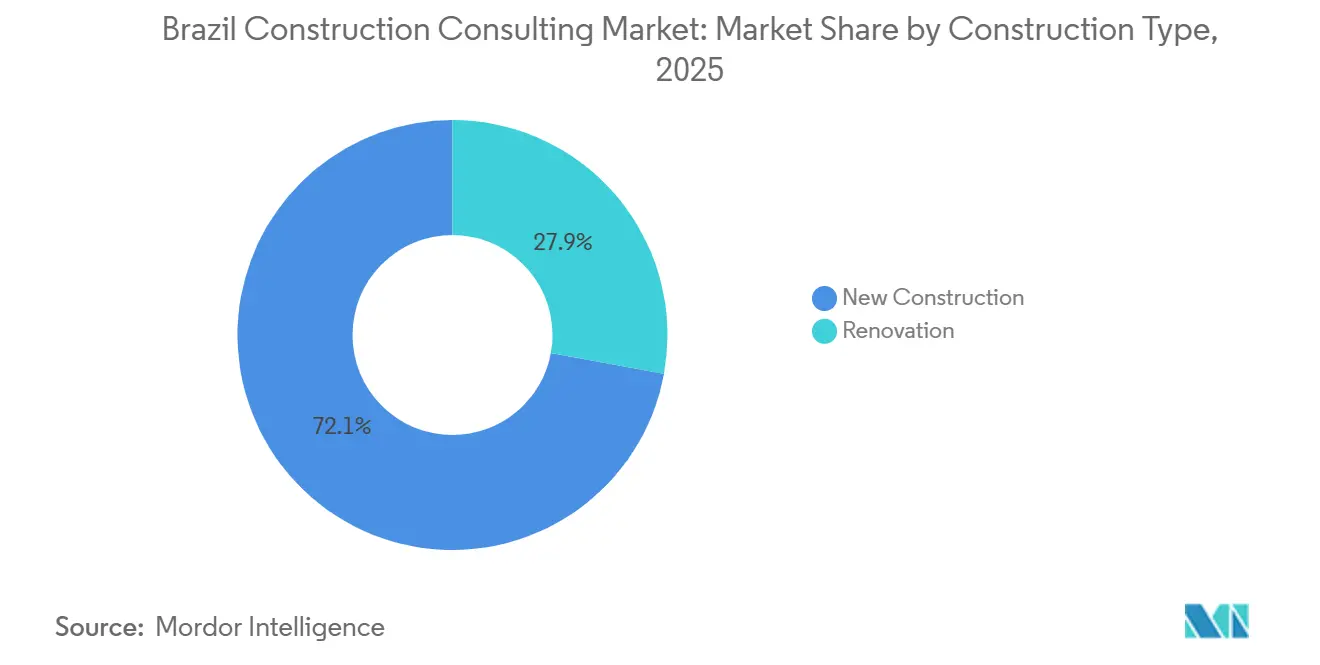

- By construction type, New construction commanded 72.12% of the market in 2025; Renovation consulting is forecast to grow faster at 6.45% CAGR to 2031.

- By investment source, Public project consulting generated 63.45% of 2025 revenues, while Private consulting are projected to rise at 5.72% CAGR through 2031.

- By geography, São Paulo captured 25.33% of 2025 spend, whereas Rio de Janeiro is expected to record the highest 5.82% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | CAGR | Key Geographic Focus | Timeline |

|---|---|---|---|

| Front-loaded PAC and Novo PAC spending boosts demand for project management consultants | +1.8% | Nationwide, greatest in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Complex PPP and concession structures needing financial and technical due diligence | +1.5% | Highway, port, and utility concessions nationwide | Medium term (2-4 years) |

| Stricter federal environmental licensing and mandatory third-party technical audits | +1.2% | All regions, especially transport, energy corridors | Long term (≥ 4 years) |

| Expansion of ESG, LEED, and AQUA-HQE certification requirements | +0.9% | Major commercial hubs and new urban developments | Short term (≤ 2 years) |

| Mandatory BIM adoption for federal projects and growing digital twin requirements in urban infrastructure | +1.1% | Federal projects nationwide, concentrated in São Paulo, Brasília, Belo Horizonte | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Front-loaded PAC and Novo PAC spending boosts demand for project management consultants

Novo PAC earmarked USD 260 billion through 2026, with 70.8% already executed, compressing project timelines and boosting the need for rigorous project-management consultancy to coordinate multi-agency approvals and lender milestones[1]Governo Federal do Brasil, “Novo PAC: R$ 1.3 trilhão em investimentos até 2026,” gov.br. BNDES approved a record USD 6 billion for highways in 2025, fueling feasibility studies as sub-national authorities race to meet co-financing requirements. Fifteen highway auctions worth USD 32 billion are slated for 2025, creating ongoing advisory demand in traffic modeling and concession finance. The Brazil construction consulting market is therefore capturing workload earlier in the project cycle and retaining it through post-award supervision.

Complex PPP and concession structures needing financial and technical due diligence

Highway concessions valued at USD 30.6 billion involve revenue-sharing formulas and long-term performance clauses, driving demand for integrated legal, financial, and engineering reviews. Multilateral lenders in Porto Alegre stipulate quality and cost selection frameworks, rewarding firms with strong safeguards and compliance expertise. Tailings-dam liabilities highlighted by the USD 32.3 billion Fundão agreement have further increased demand for independent review boards and risk audits. The Brazil construction consulting market is therefore embedding forensic analysis and risk-allocation support alongside traditional feasibility services.

Stricter federal environmental licensing and mandatory third-party technical audits

IBAMA issued 1,044 licenses between 2023 and 2024, and Law 15,190/2025 tightened Environmental Impact Study requirements for strategic projects[2]IBAMA, “Licenciamento Ambiental: 1.044 licenças emitidas 2023-2024,” ibama.gov.br. Lei 14.133/2021 obliges public works to hire independent technical supervision, embedding consulting fees into every approved budget. Risk-matrix documentation and preliminary technical studies have shifted advisory scope upstream, locking in demand even when execution is postponed. The Brazil construction consulting market now sees environmental and safety compliance as baseline services rather than optional add-ons.

Expansion of ESG, LEED, and AQUA-HQE certification requirements

Brazil counted 993 certified or pipeline green buildings in 2025, and the 2024 AQUA-HQE version raised energy-performance thresholds. Institutional investors now require certification for financing, making sustainability consulting a prerequisite. São Paulo’s 80% ground-floor retail vacancy has triggered adaptive-reuse projects that depend on MEP and sustainability consultants to meet new occupancy standards. Recurring verification contracts tied to ESG-linked loans are enlarging the services menu within the Brazil construction consulting market.

Restraints Impact Analysis*

| Restraints | Impact on Forecast CAGR | Key Geographic Focus | Expected Timeline |

|---|---|---|---|

| Lowest-price procurement criteria reduce margins for quality consultants | –1.3% | Federal, state, and municipal tenders countrywide | Long term (≥ 4 years) |

| Growing preference for bundled EPC contracts over standalone advisory services | –0.8% | Industrial and energy projects across Brazil | Medium term (2-4 years) |

| Shortage of certified project management professionals (PMP) | -0.9% | São Paulo, Rio de Janeiro, and expanding infrastructure corridors | Medium term (2-4 years) |

| Limited enforcement of consultant liability frameworks post-project failure | -1.0% | National, with acute gaps in mid-tier cities and state-level projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lowest-price procurement criteria reduce margins for quality consultants

The Tribunal de Contas da União audited USD 3.6 billion of projects in 2025 and found that 46% of severe irregularities stemmed from contract-management failures, highlighting the limitations of lowest-price award mechanisms. CADE opened a bid-rigging probe covering USD 1.9 billion of procurements, revealing instances of collusion despite formal competitive processes[3]CADE, “Investigação de cartel em licitações,” cade.gov.br. Municipalities continue to underutilize life-cycle cost criteria, even though federal law permits their adoption, thereby discouraging engagement with high-quality advisory firms within Brazil’s construction consulting market.

Growing preference for bundled EPC contracts over standalone advisory services

Design-build regimes sanctioned by Lei 14.133/2021 enable contractors to internalize design and supervision, reducing opportunities for independent consultants. Hyperscale data-center developers, expected to invest approximately USD 11.4–19.0 billion by 2030, favor turnkey EPC accountability under the Redata tax incentive. Similar bundling dominates Minha Casa Minha Vida housing contracts, compressing the addressable share for standalone advisors. Mandatory third-party oversight partially offsets this effect, but margin pressure remains visible across the Brazil construction consulting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Compliance-Driven PMC Pre-eminence

Project Management Consultancy retained a 49.12% position in the Brazil construction consulting market share during 2025 while Design and Engineering Services is forecast to grow the fastest at 6.16% CAGR owing to July 2025 BIM mandates for federal highway concessions. Upstream feasibility and detailed project report assignments swell as sub-national agencies prepare bankable packages for BNDES co-financing.

Advisors using digital clash-detection and cloud collaboration tools are winning contracts ahead of firms offering commoditized templates. Arcadis secured Sabesp’s wastewater and universalization programs after demonstrating its EDA platform, highlighting how early BIM investment is separating leaders from followers in the Brazil construction consulting market.

By Sector: Infrastructure Momentum Overtakes Residential Scale

Residential projects accounted for 43.22% of 2025 consulting demand, underpinned by Minha Casa Minha Vida’s 1.9 million contracted units. Infrastructure work, however, is projected to expand at a 5.58% CAGR as USD 30.6 billion in highway auctions and USD 36.1 billion in São Paulo rail projects move toward award. Data-center builds have accelerated following the Redata regime and are already attracting specialized electrical and cooling expertise. Office-to-residential conversions and adaptive reuse of vacant retail spaces are also supplementing workloads, helping diversify Brazil’s construction consulting market beyond traditional housing programs.

By Construction Type: Renovation Ascends on Adaptive-Reuse Trend

New construction represented 72.12% of the market in 2025, yet renovation assignments will climb at 6.45% CAGR through 2031 as landlords retrofit obsolete offices and retail frontages. The Brazil construction consulting market size linked to renovations is benefiting from structural assessments, code upgrades, and phased delivery services that command premium rates.

Limited new office supply, tight AAA vacancies, and heritage-building protection statutes in city centers are driving conversion schemes that demand multi-disciplinary consulting. Climate-resilience retrofits and energy-efficiency upgrades aligned with ESG loan covenants further enrich the renovation pipeline.

By Investment Source: Private Engagements Accelerate Despite Public Weight

Public entities generated 63.45% of consulting revenue in 2025 thanks to Novo PAC disbursements and multilateral programs that stipulate independent supervision. Private-sector fees are set to grow at 5.72% CAGR, encouraged by faster payment cycles and specialized needs in hyperscale data centers and build-to-suit logistics facilities.

High Selic rates have redirected many private investors toward pre-construction feasibility reviews that stretch assignments but also position consultants for execution once financing closes. Political uncertainty heading into the 2026 election is nudging firms to balance public exposure with private pipelines, stabilizing the Brazil construction consulting market.

Geography Analysis

Brazil’s leading economic hub, São Paulo, continues to dominate consulting demand, yet growth is normalizing as large rail and highway packages advance past peak planning. Industrial-logistics absorption of 6.35 million ft² in H1-2025 sustains warehouse-design workflows, and vacancy of 7.5% keeps rental rates firm enough to justify continued speculative development. Adaptive reuse of surplus retail frontage is adding renovation complexity that favors firms with mixed-use planning credentials.

Rio de Janeiro’s consulting upturn rests on resumed Metro Line 4 works, federal port-modernization funds, and southern-zone office tightness that now sits below 8% vacancy. Selective industrial demand around energy-services clusters is also generating layout optimization and permitting assignments.

Brasília and the Rest of Brazil depend heavily on federal housing and social-infrastructure budgets. Fragmented municipal pipelines and payment delays explain the prevalence of smaller local consultancies with deep political familiarity. Multilateral lender safeguards increasingly require these local firms to partner with national or international advisors, broadening the reach of established players across the Brazil construction consulting market.

Competitive Landscape

The Brazil construction consulting market is moderately fragmented. International majors such as AECOM, Arcadis, and WSP compete with domestic engineering houses like Concremat and Promon, alongside niche outfits that specialize in tailings-dam remediation or forensic engineering. BIM adoption mandated by federal agencies is a clear differentiator: early movers capture higher-margin assignments in highway concessions and utility PPPs. Lowest-price tendering, however, continues to compress margins for firms that lack digital advantages or multilateral experience.

AFRY’s 2025 acquisition of Reta Engenharia underscores a trend of targeted bolt-ons aimed at securing CREA-licensed talent and sector expertise. Technology disruptors offering cloud-based cost estimation remain nascent owing to data-sovereignty concerns and client risk aversion but may gradually erode the traditional hours-based billing model. Compliance with Lei 14.133/2021 favors incumbents with established methodology libraries, further segmenting the Brazil construction consulting market between scale-driven generalists and agile specialists.

Brazil Construction Consulting Industry Leaders

AECOM Brazil

Arcadis Brazil

WSP Brazil (includes Genivar and Louis Berger)

Mott MacDonald Brazil

Jacobs Brazil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: São Paulo office vacancy fell to 15.9% as limited new supply encouraged landlord upgrades.

- December 2025: CADE opened a bid-rigging investigation into USD 2 billion of procurements, heightening demand for compliance consulting services.

- November 2025: TCU’s Fiscobras audit found severe irregularities in 15 federal projects totaling USD 3.6 billion, reinforcing the need for stronger oversight mechanisms.

- September 2025: The Redata tax regime was launched to attract approximately USD 11.4–19.0 billion in data-center investment by 2030.

Brazil Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| São Paulo |

| Rio de Janeiro |

| Brasília |

| Rest of Brazil |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Key Cities | São Paulo | |

| Rio de Janeiro | ||

| Brasília | ||

| Rest of Brazil | ||

Key Questions Answered in the Report

What is the 2026 value of the Brazil construction consulting market?

The sector is valued at USD 8.9 billion in 2026.

How fast will consulting demand in Brazil’s infrastructure sector grow?

Infrastructure consulting is projected to rise at 5.58% CAGR between 2026 and 2031.

Which service category is expanding the quickest?

Design and Engineering Services are expected to grow at a 6.16% CAGR through 2031.

Why are renovation assignments gaining traction?

High office vacancy and surplus retail frontage are spurring adaptive-reuse projects that need specialized consulting.

Page last updated on: