Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

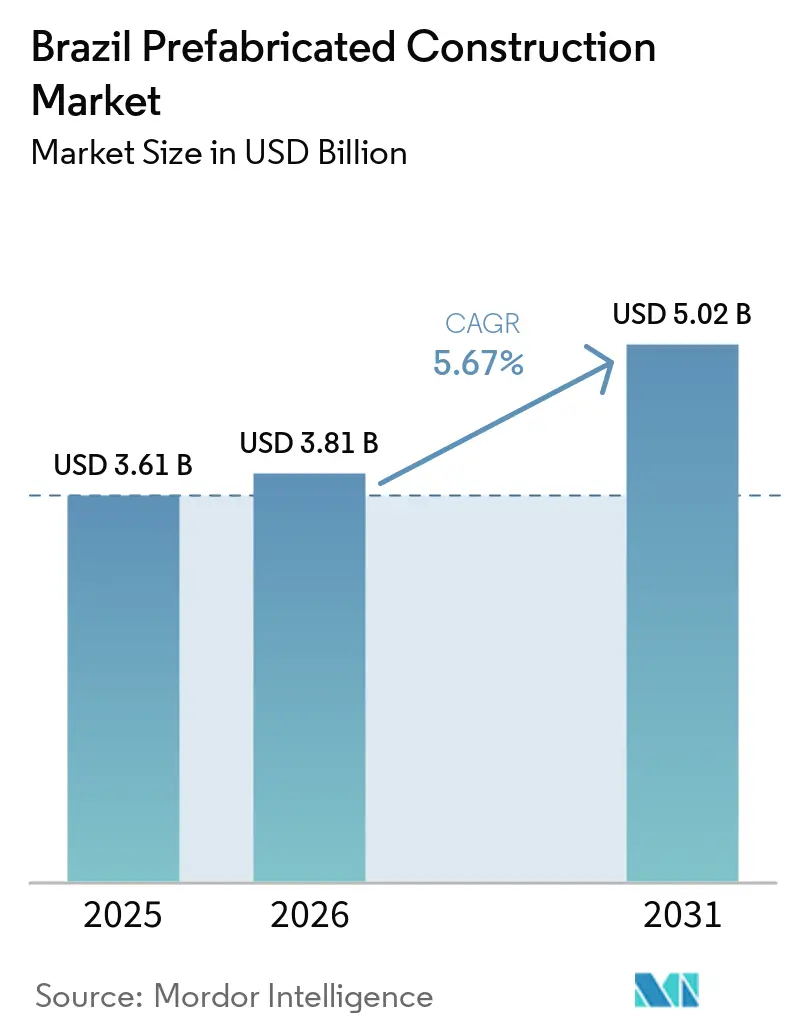

| Base Year Market Size (2025) | USD 3.61 Billion |

| Market Size (2026) | USD 3.81 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Prefabricated Construction Market Analysis by Mordor Intelligence

The Brazil Prefabricated Construction Market size is expected to grow from USD 3.61 billion in 2025 to USD 3.81 billion in 2026 and is forecast to reach USD 5.02 billion by 2031 at 5.67% CAGR over 2026-2031.

Demand is accelerating as federal housing subsidies, industrial nearshoring, and public-infrastructure upgrades converge, while factory production slashes site labor and compresses delivery schedules. Developers in São Paulo, Rio de Janeiro, and emerging Northeast corridors now treat off-site fabrication as a hedge against skilled-labor shortages and weather-related delays. Material choice is fragmented along carbon and cost lines as concrete keeps its stronghold in high-rise residential, timber captures low-rise public facilities, and steel frames dominate fast-track industrial halls. Suppliers investing in automated panel lines, cross-laminated-timber presses, and BIM-enabled workflows report lower defect rates and higher bid-win percentages. Federal and state financing incentives tied to embodied-carbon reduction further tilt project specifications toward engineered wood and hybrid systems, creating fresh revenue pockets for vertically integrated players.

Key Report Takeaways

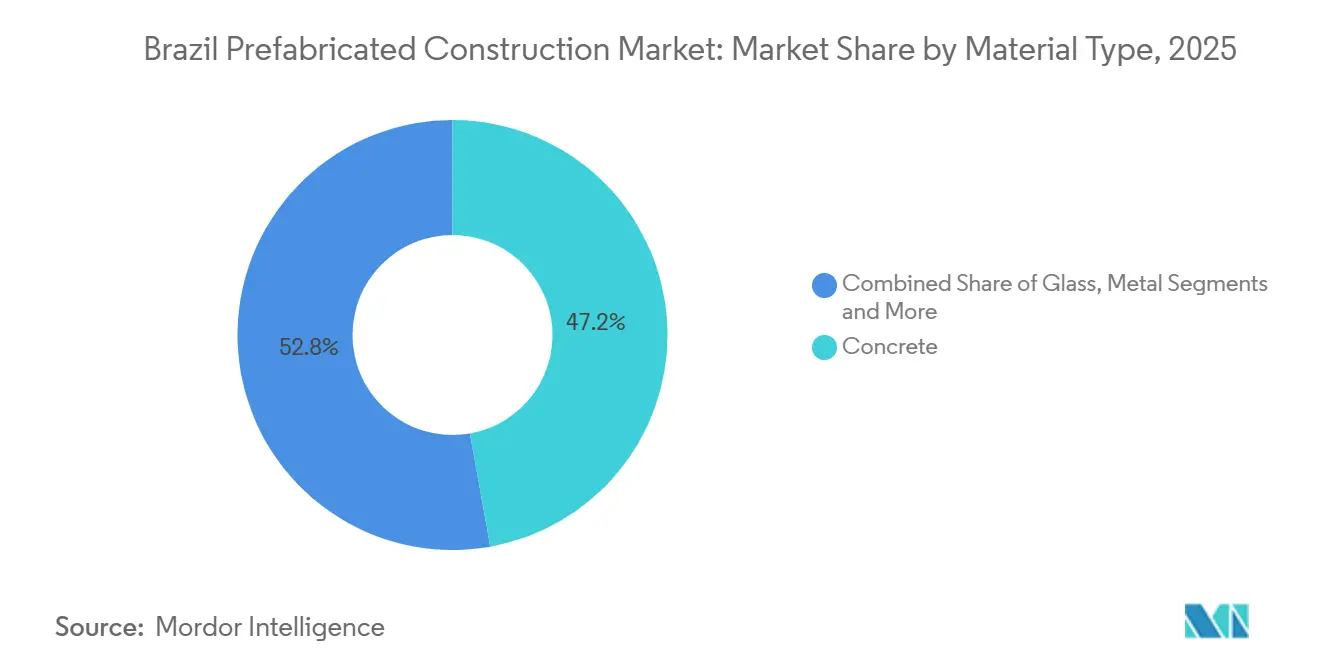

- By material, concrete led with 47.2% of the Brazil prefabricated construction market share in 2025, while timber is projected to advance at a 6.71% CAGR from 2026 to 2031.

- By application, residential projects commanded 55.6% of the Brazil prefabricated construction market size in 2025; commercial builds are forecast to expand at a 6.52% CAGR through 2031.

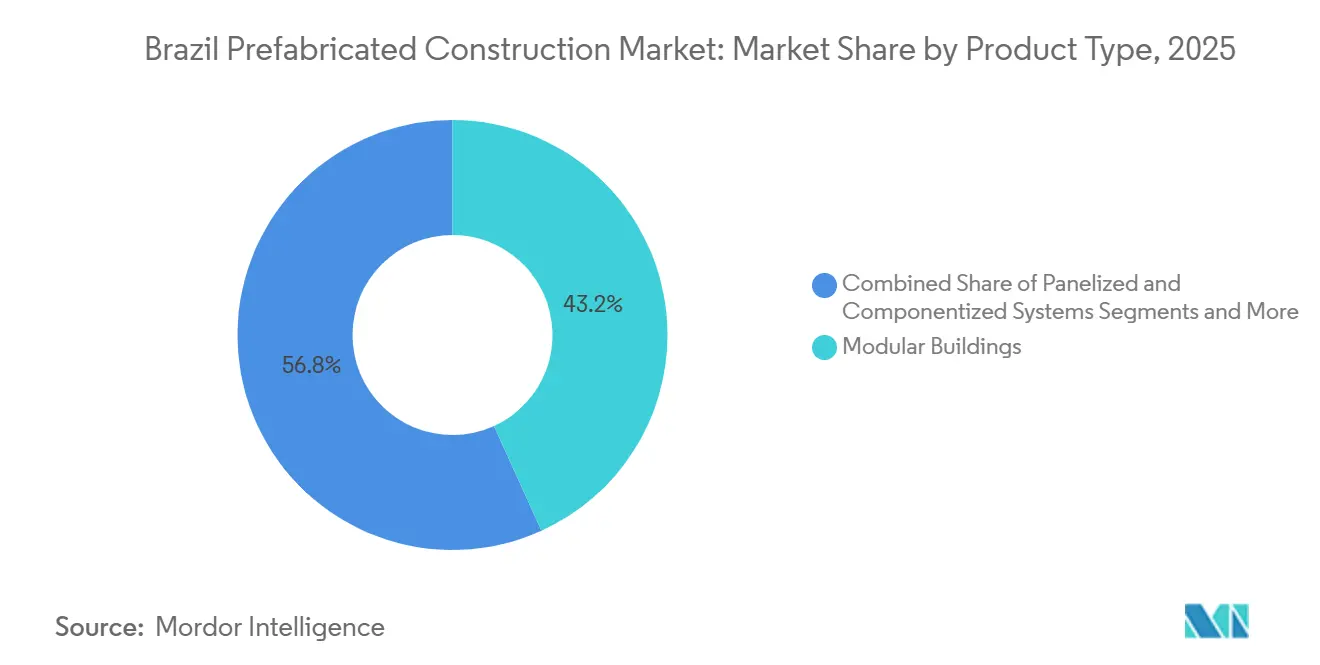

- By product type, modular buildings accounted for 43.2% revenue share in 2025 and will post the fastest 6.91% CAGR to 2031.

- By geography, São Paulo captured 33.9% value in 2025, whereas Salvador is poised for the swiftest 7.32% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing push (Minha Casa Minha Vida) | +1.8% | National, clustered in São Paulo, Rio de Janeiro, Salvador | Medium term (2-4 years) |

| Industrial / logistics expansion | +1.5% | São Paulo, Rio de Janeiro, Bahia, Pernambuco | Short term (≤ 2 years) |

| Public assets adopting modular | +1.2% | Nationwide, early gains in Salvador and Recife | Medium term (2-4 years) |

| Decarbonization goals and green incentives | +0.9% | Major cities with green-building programs | Long term (≥ 4 years) |

| Disaster-response and remote-site demand | +0.6% | Amazon Basin, Minas Gerais, coastal risk zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Housing Push Accelerates Offsite Adoption

Minha Casa Minha Vida earmarked USD 2.4 billion in 2025 to deliver 400,000 subsidized units by 2027, and the guidelines now reward bidders that prove factory-level quality control and sub-12-month handovers. Municipal housing agencies therefore favor panelized concrete and light-gauge steel, awarding contracts to suppliers able to certify a six-to-nine-month build cycle. Capacity is spreading beyond São Paulo as Bahia and Pernambuco license new precast plants that trim logistics costs and foster local jobs. Expanded income thresholds lifted demand from families earning up to USD 1,600 per month, ensuring a steady pipeline for modular-residential specialists through the next election cycle[1]Caixa Econômica Federal, “Minha Casa Minha Vida 2025 – Diretrizes,” caixa.gov.br .

Industrial Nearshoring Fuels Commercial Modular Demand

Foreign direct investment in Brazilian manufacturing rose 18% year-on-year during H1 2025 as automakers, electronics assemblers, and pharmaceutical firms shifted capacity closer to Mercosur consumers. These tenants stipulate commissioning deadlines that conventional builds seldom meet; a European auto supplier in São Paulo moved from groundbreaking to first-car roll-out in nine months by erecting a steel-frame modular hall. E-commerce and hyperscale data-center operators adopt similar tactics, choosing prefab metal envelopes that enable phased expansion without shutting live zones. Activity clusters around ABC Paulista and the Camaçari industrial hub, underscoring how logistics access shapes the Brazil prefabricated construction market[2]Agência Brasileira de Desenvolvimento Industrial, “Nearshoring no Setor Automotivo,” abdi.com.br.

Public Infrastructure Embraces Modular for Speed and Certainty

State and municipal buyers commissioned 120 schools and 45 clinics in modular form during 2024, a 35% jump over 2023. Salvador alone ordered 18 prefab schools with a seven-month delivery cap, leveraging standardized concrete panels and trusses to avoid classroom shortages. Federal health guidelines issued in 2024 made modular clinics eligible for reimbursement, unlocking co-funding for municipalities short on upfront capital. The policy dovetails with national plans to add 1,000 primary-care posts in underserved regions by 2028[3]Ministério da Saúde, “Portaria 1.043 – Reconhecimento de Clínicas Modulares,” saude.gov.br.

Decarbonization Targets Shift Material and Process Choices

Brazil’s updated Nationally Determined Contribution seeks a 50% emissions cut by 2030, casting a spotlight on construction, which emits roughly one-fifth of national greenhouse gases. Cross-laminated timber trials show 40-60% embodied-carbon savings versus reinforced concrete, and annual inquiry volumes at domestic CLT mills doubled between 2023 and 2025. The development bank BNDES sweetened financing by 150 basis points for projects documenting carbon savings, nudging developers toward engineered wood and hybrid systems.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency and financing cost volatility | -0.9% | Nationwide, sharper for import-heavy suppliers | Short term (≤ 2 years) |

| Complex permitting and tax variability | -0.7% | Highest friction in Rio de Janeiro and small municipalities | Medium term (2-4 years) |

| Logistics distance and supplier capacity | -0.5% | Interior states and Amazon Basin far from core fabrication hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility and Financing Costs Pressure Feasibility

Brazil’s benchmark SELIC rate reached 12.25% in December 2025, pushing mortgage coupons toward the 11-13% corridor and squeezing middle-income buyers. The Brazilian Real slid 8% against the USD during 2025, inflating cost lines for imported HVAC pods, elevators, and specialty facade panels. Suppliers locked into fixed-price contracts from 2024 now face margin compression, while international modular entrants defer market launches until exchange-rate headwinds abate.

Permitting Complexity and Tax Variability Slow Standardization

Brazil’s municipal building codes vary widely; a panel system approved in São Paulo can require re-engineering in Salvador, eroding economies of scale. Divergent ICMS rates apply to prefab components classified alternately as industrial goods or construction materials, occasionally triggering double taxation on cross-state shipments. Although São Paulo processes 60% of approvals online, many smaller cities still rely on in-person reviews that nullify prefab’s timeline advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Dominates, Timber Accelerates

Concrete captured 47.2% of the Brazil prefabricated construction market share in 2025 thanks to deep local expertise, robust cement supply, and compliance with stringent fire and seismic codes. Precast beams, slabs, and façade panels remain the default choice for high-rise housing and public works across São Paulo and Rio de Janeiro. Timber, however, is the fastest climber at a 6.71% CAGR through 2031, buoyed by cross-laminated-timber schools and clinics that deliver lower embodied carbon and 40% quicker erection. Early adopters, such as a three-story CLT school in Salvador, shaved six weeks off the baseline schedule, validating the material’s speed and sustainability credentials.

Concrete suppliers are defending their share by trialing low-carbon mixes with blast-furnace slag substitutes, while steel-frame vendors tout recyclability and modular flexibility. Three new CLT mills under construction in southern Brazil will lift national capacity by 50,000 m³ by 2027, easing supply bottlenecks. Metal systems remain the workhorse for warehouses and data centers where long spans and relocatability are priorities. Glass and composite panels fill niche façade roles, rounding out a diversified material palette that lets architects balance cost, carbon, and performance.

By Application: Residential Leads, Commercial Gains Momentum

Residential builds accounted for 55.6% of the Brazil prefabricated construction market size in 2025, propelled by Minha Casa Minha Vida subsidies and private-sector panelized towers that mitigate São Paulo’s labor constraints. Developers lock in fixed pricing, knowing that factory output resists wage inflation and weather-driven delays. Mortgage headwinds limit premium demand, prompting a shift toward smaller units and standardized finishes that dovetail with off-site production.

Commercial projects are primed for a 6.52% CAGR through 2031 as nearshoring, e-commerce, and cloud services require rapid commissioning. A USD 1.2 billion hyperscale data-center campus in São Paulo trimmed build time from 24 to 16 months by executing power and cooling blocks as volumetric modules. Logistics operators expanding fulfillment hubs in Belo Horizonte and Fortaleza now specify steel-frame warehouses that can bolt on extra bays without pausing live operations. Schools, clinics, disaster-relief shelters, and mining camps provide steady civic demand, illustrating prefab’s versatility across public and private domains.

By Product Type: Volumetric Modules Outpace Alternatives

Modular buildings held 43.2% revenue in 2025 and are on track for a 6.91% CAGR to 2031, reflecting their all-inclusive nature - factory-finished units arrive with mechanical, electrical, and plumbing systems in place. Energy firms running remote wind-farm construction camps and mining giants in Pará favor volumetric dorms that assemble in days and demobilize just as fast. Panelized systems still dominate mid-rise urban projects where architects want flexibility; semi-volumetric wall panels with integrated windows and wiring blur the line between categories.

Automated welding and robotic painting introduced since 2023 cut defect rates by 60% at leading São Paulo plants, narrowing the cost gap against site-built methods. Digital configurators now let small developers select layouts and finishes online, triggering four-week production cycles and democratizing access to mass-customized homes. Hybrid approaches - volumumetric wet cores married to panelized shells - gain traction in high-density sites that need both speed and design freedom, confirming that the Brazil prefabricated construction market is evolving toward a continuum of off-site solutions.

Geography Analysis

The Brazil prefabricated construction market is most mature in the Southeast, where São Paulo’s 33.9% share reflects concentrated factory capacity, dense populations, and municipal fast-track permitting that shortens approval cycles. Mega-projects ranging from vertical social-housing towers to hyperscale data centers stream through the city’s digital portal, illustrating how policy alignment accelerates uptake. Near-term growth, however, is pivoting toward secondary municipalities within the state where land is plentiful and modular plants can still truck panels overnight, blunting logistics premiums.

Salvador exemplifies the next growth wave. Fresh federal transfers for education and health programs position Bahia to allocate capital toward standardized modular prototypes. Contracts for 18 schools and the first tranche of rural primary-care posts already validate the model’s replicability. As three new CLT mills open in southern states, an integrated timber-construction corridor is set to supply Salvador’s public-building pipeline, tightening delivery loops and lowering embodied-carbon footprints.

Rio de Janeiro’s topology - steep hills, flood-prone valleys, and tightly packed favelas - rewards modular infill that negotiates constrained sites. City planners also leverage volumetric shelters to resettle landslide-displaced families within weeks rather than months. Beyond the coastal metropolises, the Rest-of-Brazil segment splits between resource corridors - where mining and agribusiness finance relocatable camps - and interior regions where long-haul logistics inflate costs. Expanded inland rail and road investments scheduled for completion after 2027 should shave transport surcharges, unlocking latent demand across Goiás and Mato Grosso.

Competitive Landscape

Competition is moderate yet fluid, with no single firm controlling more than 8% national revenue, placing the market in a mid-fragmented zone. Approximately 180 precast plants, 50 volumetric factories, and scores of smaller component suppliers battle on lead time, customization scope, and financing support. Leading São Paulo companies vertically integrated into steel or timber processing between 2023 and 2025, hedging material risk and trimming input costs. Early BIM adopters now claim 25-40% rework reductions, translating into sharper bids that squeeze traditional players.

Strategic alliances illustrate a shift from pure fabrication to platform economics. Joint ventures between established developers and European modular specialists import automated production lines and design libraries, cutting engineering cycles and expanding product catalogs. Construction-tech startups facilitate digital marketplaces where small builders compare quotes and track fabrication milestones, injecting price transparency and shortening procurement loops. Industry associations organize DfMA workshops that disseminate best practices, fostering incremental efficiency gains across the long tail of regional suppliers.

White-space niches beckon. Disaster-response units lack a dedicated supplier able to stock finished inventory for immediate dispatch, while retrofit façade panels for Brazil’s aging 1970s residential blocks remain underexploited. Players capable of marrying mass customization with just-in-time logistics stand to secure outsized share as the Brazil prefabricated construction industry matures. Foreign entrants eye these gaps but tread cautiously given currency swings and regulatory complexity; those securing local financing and municipal code expertise will advance fastest.

Brazil Prefabricated Construction Industry Leaders

Medabil Indústria em Sistemas Construtivos Ltda

Cassol Pré-Fabricados

Modularis

Skanska Brasil Ltda

Siscobras

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: MRV & Co partnered with a European modular specialist to roll out a panelized concrete system aimed at trimming residential tower schedules by 25%.

- November 2024: Skanska Brasil won a USD 36 million contract for 12 modular schools in Salvador, its largest public prefab deal to date.

- September 2024: Direcional Engenharia opened a USD 8 million panel plant in Belo Horizonte, targeting 200,000 m² annual output for in-house projects.

- August 2024: Gafisa formed a joint venture with a São Paulo steel-frame fabricator to launch 1,000 mid-income modular units by 2027.

- June 2024: Cassol Pré-Fabricados expanded its Rio Grande do Sul precast plant by 50%, adding automated curing chambers.

Brazil Prefabricated Construction Market Report Scope

A prefabricated building, informally a prefab, is a building that is manufactured and constructed using prefabrication. It comprises factory-made components or units transported and assembled on-site to form the complete building.

Brazil's Prefabricated Buildings Industry is segmented by material type (concrete, glass, metal, timber, and other material types) and application (residential, commercial, and other applications (industrial, institutional, and infrastructure)). The report offers market size and forecasts for the Brazil prefabricated buildings industry in value (USD) for all the above segments.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By City

| São Paulo |

| Rio de Janeiro |

| Salvador |

| Rest of Brazil |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By City | São Paulo |

| Rio de Janeiro | |

| Salvador | |

| Rest of Brazil |

Key Questions Answered in the Report

How large is the Brazil prefabricated construction market in 2026?

The Brazil prefabricated construction market size stood at USD 3.81 billion in 2026 and is forecast to reach USD 5.02 billion by 2031.

Which material leads current demand?

Concrete remains dominant with a 47.2% share in 2025, thanks to established precast capacity and compliance with stringent fire-safety rules.

What segment is growing fastest?

Timber-based systems will post the fastest 6.71% CAGR to 2031 as decarbonization incentives and new CLT plants expand supply.

Why are modular buildings gaining traction?

Fully volumetric modules cut on-site activity and meet tight commissioning windows for mining camps, data centers, and emergency housing, supporting a 6.91% CAGR outlook.

Which city is poised for the strongest growth?

Salvador should log a market-leading 7.32% CAGR between 2026 and 2031 due to state funding for modular schools and clinics.

How fragmented is supplier competition?

The sector is moderately fragmented; no firm controls more than 8% of national revenue.

Page last updated on: