Branch Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.10 Billion |

| Market Size (2031) | USD 11.05 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

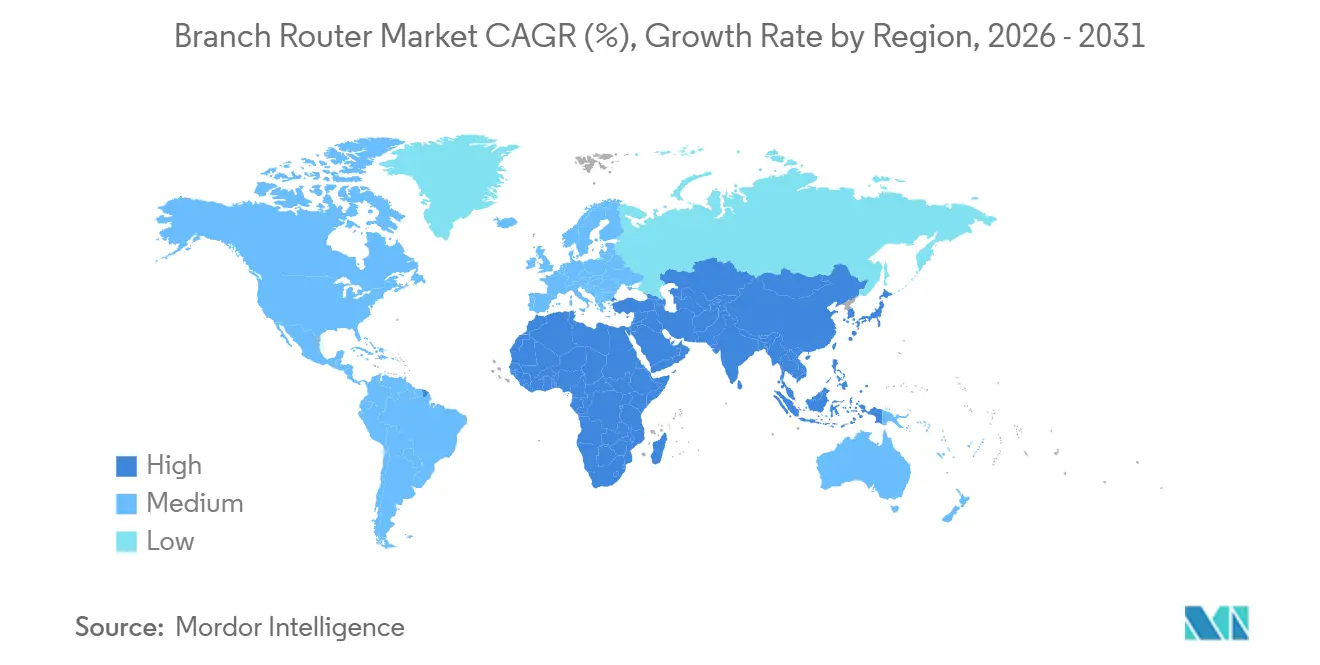

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Branch Router Market Analysis by Mordor Intelligence

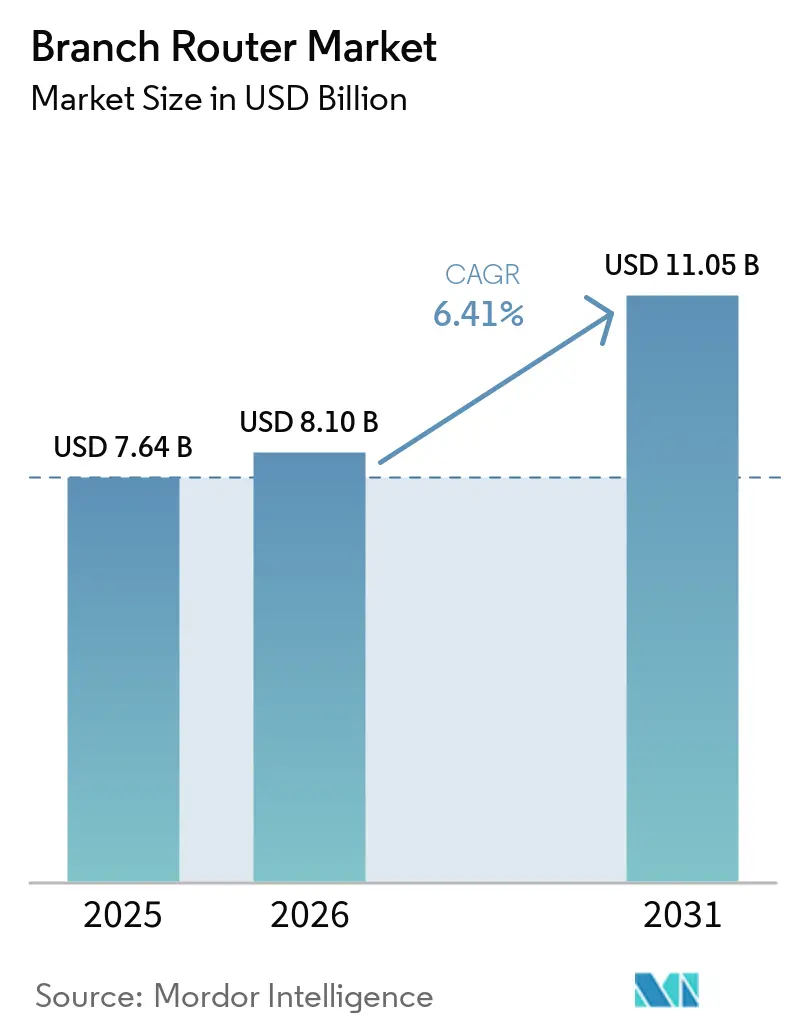

The branch router market size is expected to grow from USD 7.64 billion in 2025 to USD 8.10 billion in 2026 and is forecast to reach USD 11.05 billion by 2031 at a 6.41% CAGR over 2026-2031. Memory component shortages, rising DRAM costs, and expanding bandwidth needs continue to reshape vendor sourcing strategies and price structures. Vendors are placing larger advance-purchase commitments for memory, integrating flex-pricing clauses into partner contracts, and redesigning platforms around merchant silicon to preserve gross margins. At the same time, Secure Access Service Edge adoption, private 5G expansion, and edge AI inference are elevating performance and security requirements at every site. Collectively, these forces are accelerating refresh cycles while pushing branch router specifications toward higher throughput, integrated security, and software-defined management, ensuring that the branch router market remains a centerpiece of enterprise edge investment through the forecast horizon.

Key Report Takeaways

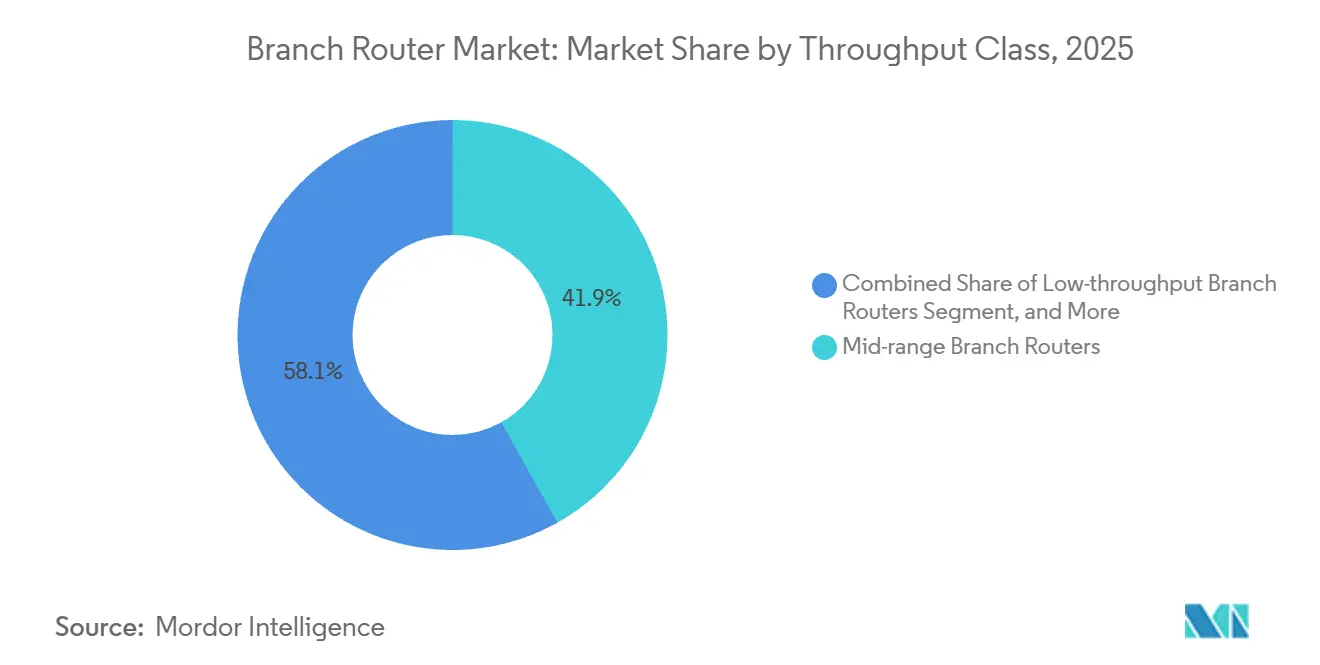

- By throughput class, mid-range branch routers led with 41.88% of the branch router market share in 2025, while high-performance models are projected to expand at a 7.12% CAGR through 2031.

- By branch size, medium sites accounted for 43.62% of the branch router market in 2025, and small branches are advancing at a 6.84% CAGR through 2031.

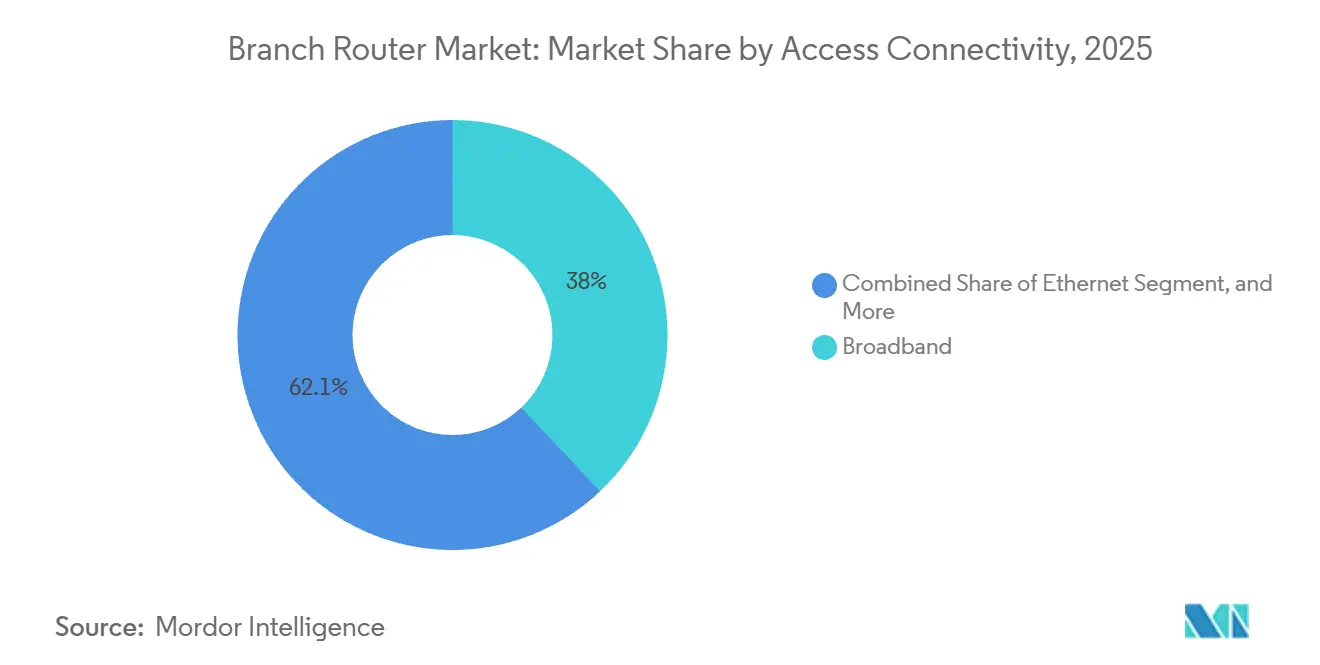

- By access connectivity, broadband lines accounted for 37.95% of 2025 deployments, and 5G links are growing at a 9.36% CAGR through 2031.

- By end user industry, BFSI accounted for 25.94% of demand in 2025, whereas retail and e-commerce are forecast to post the fastest 7.04% CAGR over 2026-2031.

- By geography, North America captured 34.48% revenue share in 2025, while Asia-Pacific is on track for the highest 8.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Branch Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Secure Remote Connectivity Post Pandemic | +1.2% | Global with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of Retail and BFSI Branch Networks in Emerging Markets | +1.4% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Increasing Bandwidth Requirements with Cloud Migration | +1.0% | Global | Medium term (2-4 years) |

| Shift Toward SD-WAN and Software-Defined Branch Architectures | +1.3% | North America and Europe early adoption, Asia-Pacific rapid catch-up | Short term (≤ 2 years) |

| Edge AI Workload Offloading Necessitating On-Device Compute in Branch Routers | +0.8% | North America and Asia-Pacific manufacturing zones | Long term (≥ 4 years) |

| Availability of Private 5G and LTE Spectrum for Enterprises Accelerating Wireless WAN Routers | +0.7% | United States CBRS, Europe licensed bands, India post-2026 direct spectrum | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand For Secure Remote Connectivity Post Pandemic

Hybrid work has turned every site into a security enforcement point, pushing organizations to combine routing, firewall, and zero-trust functions in one device. Vendors now embed next-generation firewall engines, encrypted tunnel orchestration, and AI-driven visibility directly inside branch routers rather than relying on separate appliances. Cisco’s Unified Branch bundle and Fortinet’s SASE Outpost illustrate how single-vendor stacks shorten deployment cycles while tightening policy consistency.[1]Butaney Vikas, “Redefining Branch Networking, Cisco Secure Routers and Unified Branch,” Cisco Blogs, cisco.com Platform roadmaps are also adding post-quantum cryptography controls in anticipation of commercial quantum computing, ensuring that key exchange and device management remain future-proof. As enterprises refresh hardware, secure connectivity features increasingly outweigh raw port counts, driving specification upgrades even in cost-sensitive tiers.

Expansion Of Retail And BFSI Branch Networks In Emerging Markets

Banks, quick-service restaurants, and convenience chains are rolling out thousands of compact outlets across India, Indonesia, Egypt, and the Gulf states. These footprints demand small-form-factor routers that can power point-of-sale devices, video analytics, and digital signage while surviving harsh environmental conditions. Government fiber programs and nationwide 5G launches further multiply the number of viable branch locations, making network coverage, not compute cost, the primary constraint. Vendors able to preload compliance templates for financial services and to certify hardware against local telecom rules capture a disproportionate share of tenders. As branch counts climb, centralized controller platforms and zero-touch provisioning become essential, turning management software into a deciding factor during procurement.

Increasing Bandwidth Requirements With Cloud Migration

Traffic patterns have shifted from hub-and-spoke MPLS toward direct internet breakout and multi-cloud access. Enterprises report 30-70% savings in circuit costs after adopting SD-WAN, yet those savings are often redeployed into higher-specification edge devices that support dynamic path selection, SaaS prioritization, and encrypted overlay tunnels. MPLS remains for latency-sensitive workloads, so routers must interoperate with legacy protocols while steering most traffic over broadband or 5G. Silicon roadmaps therefore emphasize additional packet-processing cores, in-line encryption accelerators, and deterministic quality-of-service scheduling to ensure that voice, video, and AI inference flows receive guaranteed treatment across heterogeneous underlays.

Shift Toward SD-WAN And Software-Defined Branch Architectures

Centralized controllers now orchestrate routing intelligence, reducing the perceived strategic value of proprietary hardware. Service providers package universal customer premises equipment that integrates routing, firewalling, and wireless WAN, allowing enterprises to outsource day-to-day policy management. Roughly four out of five organizations therefore procure managed SD-WAN rather than self-deploying, shifting the point of sale from OEM to telecom operator. The result is a buyer preference for standards-based interfaces, API-first design, and white-box-ready operating systems. Hardware vendors respond by opening their software stacks, supporting containerized services, and partnering with cloud orchestration platforms to avoid margin-eroding commoditization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security Vulnerabilities Due to Legacy Firmware | -0.60% | Global with acute exposure in consumer-grade deployments | Short term (≤ 2 years) |

| Intense Price Competition and Commoditization | -0.50% | Global, most pronounced in Asia-Pacific and low-tier segments | Medium term (2-4 years) |

| Chip Supply Chain Volatility Affecting Lead Times | -0.70% | Global supply chains, manufacturing concentrated in Asia | Short term (≤ 2 years) |

| Skills Shortage in Managing SD-WAN Policies at Scale | -0.40% | North America and Europe enterprise deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security Vulnerabilities Due To Legacy Firmware

Out-of-date code leaves branch devices exposed to remote takeover, with consumer models averaging more than ten times the CVE count of enterprise units. High-severity flaws disclosed in 2025-2026 demonstrate that routers remain prime targets for espionage and botnets. Regulatory bodies now block uncertified imports, forcing buyers to prioritize brands that publish regular patches and support automated fleet-wide updates. Enterprises consequently phase out gray-market appliances, but many small businesses struggle to fund replacements, limiting near-term upgrade velocity and shaving growth off the overall branch router market.

Intense Price Competition And Commoditization

Tier-1 OEMs, white-box builders, and original design manufacturers are locked in a race to meet sub-USD 100 price points for entry routers that still promise Wi-Fi 6, multi-gigabit ports, and basic firewalling. Sudden DRAM price spikes amplify cost pressure, with memory now representing roughly one-fifth of the bill of materials on low-end platforms. Vendors without long-term supply contracts face margin compression or shipment delays, prompting consolidation and production relocation to lower-cost regions. As hardware differentiators erode, software ecosystems and managed services become decisive, but smaller manufacturers lack the resources to build competitive controller stacks, limiting their ability to sustain aggressive discount strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Throughput Class: High-Performance Designs Move Center Stage

High-performance appliances commanded 41.88% branch router market share in 2025, underscoring their suitability for medium branches that balance bandwidth and cost. The class is forecast to advance at a 7.12% CAGR through 2031 as enterprises adopt edge AI inference, private 5G cores, and full-tunnel SASE. These workloads demand integrated encryption accelerators and multi-gigabit interfaces, features that mid-range silicon increasingly embeds by default. Cisco’s 8000 Series Secure Routers, with up to 95 Gbps IPsec throughput, exemplify the pivot toward compute-heavy edge gear. Conversely, low-throughput models risk disintermediation by virtualized network functions running on commodity boxes, shrinking their addressable slice of the branch router market size.

Ultra-high platforms target carrier aggregation, hyperscale interconnection, and AI fabric spines, shipping terabit capacities once reserved for core routers. Arista’s 7800R4 system fits 576 ports of 800 GbE in one chassis, foreshadowing trickle-down effects as silicon costs fall. Over the forecast, compute and routing will increasingly converge, blurring throughput categories and encouraging buyers to select chassis based on available expansion slots and power budgets rather than on static packet-per-second ratings.

By Branch Size: Fleets Of Small Sites Drive Volume

Medium branches delivered 43.62% of the 2025 branch router market size, reflecting standardized deployment kits that cover everything from retail banking to regional warehouses. Nonetheless, the fastest 6.84% CAGR belongs to small outlets created by proliferating convenience chains, bank kiosks, and pop-up healthcare clinics. Low-touch provisioning and cloud-first management are mandatory, leading vendors to embed zero-touch onboarding scripts and integrate Wi-Fi and LTE hardware into one enclosure. At the other extreme, large branches act as aggregation nodes with redundant uplinks, edge data storage, and local analytics clusters, sustaining demand for chassis that support modular line cards and power-over-Ethernet budgets above 1.2 kilowatts.

Network teams now deploy “branch as code” toolkits that store desired state in Git repositories, automatically push updates, and roll back failed commits. This shift lowers the incremental cost of operating hundreds of micro-branches but raises the skill threshold for infrastructure engineers, indirectly increasing demand for managed SD-WAN services among various organizations lacking DevOps-grade talent.

By Access Connectivity: Cellular Links Accelerate While Fiber Dominates Base

Broadband fixed lines accounted for 37.95% of 2025 deployments owing to fiber-to-the-premises expansion and cable-DOCSIS upgrades. Yet 5G links represent the breakout segment with a 9.36% CAGR to 2031, propelled by shared-spectrum frameworks such as Citizens Broadband Radio Service and by enterprise private 5G programs in manufacturing corridors. Branch routers must therefore support dual SIM slots, sub-6 GHz and millimeter-wave radios, and dynamic link steering that treats cellular, broadband, and residual MPLS as equal peers. Ericsson's Private 5G Compact solution, launched in January 2025, supports 4G LTE CBRS in the United States with a cloud-native architecture, API-first design, and a zero-trust granular policy framework, listing Cradlepoint branch router models, including R500-PLTE, IBR1700, R920, R1900 5G, R2100 5G, E100, E300, and E3000 as preferred endpoints for best end-to-end management and user experience.[2]Cradlepoint, “Ericsson Private 5G Compact Data Sheet,” cradlepoint.com

Hybrid connectivity packages grow popular, combining deterministic SLA paths with inexpensive over-the-top circuits under a single SD-WAN policy engine. Ethernet remains the choice for on-campus branches inside factories and universities requiring low-jitter backbones. LTE persists as a backup link in rural regions, especially where fiber economics remain challenging. Vendors that can certify devices across multiple global cellular bands and integrate cloud-native 5G user-plane functions will capitalize on the accelerating shift from fixed to wireless-first branch design.

By End User Industry: Retail Roars Ahead, BFSI Safeguards Core Revenues

BFSI generated 25.94% of 2025 volumes through its vast estate of bank branches, ATMs, and cash-management centers, all of which need always-on encrypted transport and auditable policy enforcement. Nevertheless, retail and e-commerce is on track for a 7.04% CAGR as omnichannel strategies demand low-latency links for real-time inventory, contactless checkout, and edge video analytics. Branch routers, therefore, bundle AI modules that can run loss-prevention inference or customer heat-map engines locally, reducing upstream bandwidth while enhancing shopper insight.

The manufacturing, healthcare, and government segments show a rising appetite for private 5G-enabled routers that integrate deterministic networking for industrial robots, HIPAA-compliant encryption, or post-quantum security for classified workloads. Education rounds out demand by seeking Wi-Fi 7 backbones and easy student device onboarding across sprawling campuses. Each vertical values centralized management, but compliance tooling and localized language support often tip the scales to regionally entrenched vendors.

Geography Analysis

North America controlled 34.48% of 2025 revenue, aided by mature SD-WAN uptake, CBRS commercialization, and federal zero-trust mandates that specify post-quantum readiness for edge devices. Procurement, however, now grapples with memory price inflation and lead-time volatility, raising the total cost of ownership for refresh cycles. Consolidation among platform suppliers creates additional supply-chain dependencies that large enterprises manage through multi-vendor qualification programs and cloud-agnostic controller strategies.

Asia-Pacific is projected to post the highest 8.18% CAGR. The growth is fueled by private 5G rollouts in India and China, retail chain expansion, and banking branch proliferation across Indonesia, Vietnam, and the Philippines. India's anticipated direct spectrum access policy changes in 2026 could lower private network costs by approximately 40%, accelerating enterprise-owned deployments and creating demand for on-premise branch routers with flexible integration to cloud-native 5G cores and support for massive IoT device density.[3]Niral Networks, “Private 5G and Edge Computing in Industry 4.0, 2026 Outlook,” niralnetworks.com Governments are subsidizing fiber builds and campus-5G pilots, lifting baseline connectivity and making small-branch deployment viable in secondary and tertiary cities. Local system integrators bundle routers with managed services, masking channel complexity and accelerating penetration of cloud-managed portfolios.

Europe exhibits steady replacement demand driven by GDPR compliance, data-sovereignty requirements, and energy-efficiency regulations that favor newer ASIC designs. Economic headwinds and cautious capital spending limit upside, yet sustainability mandates encourage enterprises to retire power-hungry legacy routers in favor of energy-aware models that dynamically scale CPU clocks and idle unused ports. Middle East and Africa, buoyed by mega-projects such as Digital Egypt and the prevalence of greenfield 5G rollouts, show double-digit local growth pockets despite lower absolute volume. South America’s expansion is moderated by currency volatility and fiber backhaul gaps, but shared-tower agreements and cloud point-of-presence proliferation are beginning to unlock latent demand.

Competitive Landscape

Cisco Systems remains the benchmark in the branch router market, with a broad portfolio spanning Meraki cloud-managed appliances, Catalyst SD-WAN solutions, and the high-end 8000 Series that incorporates quantum-safe cryptography for advanced security. The combination of Hewlett Packard Enterprise and Juniper Networks has significantly strengthened HPE’s networking position by integrating Aruba’s campus networking capabilities with Juniper’s Mist AI platform, creating a unified offering that brings routing, Wi-Fi, and security into a single cloud-managed interface. Arista Networks has expanded its footprint beyond data centers by leveraging its acquisition of the VeloCloud SD-WAN portfolio, enabling CloudEOS to extend from core environments to branch edges while emphasizing programmability and readiness for 800 GbE environments.[4]Arista Networks, “Next Generation SD-WAN in the AI Era,” arista.com

At the same time, smaller and specialized vendors such as Peplink, Cradlepoint, Teltonika Networks, and Ubiquiti compete by focusing on niche strengths, including ruggedized hardware, strong cellular WAN integration, and competitive pricing. Ericsson has further reinforced this ecosystem by positioning Cradlepoint hardware as preferred endpoints within its private 5G Compact solutions, highlighting the growing collaboration between telecom infrastructure providers and router vendors to deliver end-to-end industrial connectivity. Meanwhile, Huawei Technologies continues to enhance its NetEngine 8000 series and invest in quantum key distribution capabilities, although its expansion remains constrained in regions such as North America and parts of Europe due to geopolitical restrictions.

In parallel, partnerships such as those between Dell Technologies and Nokia are driving the development of compact 5G user-plane appliances that separate control and data planes, indicating a shift away from traditional monolithic branch router architectures. As edge computing, AI inference, and private 5G deployments increasingly converge, competitive advantage is expected to favor vendors that can deliver open and flexible operating systems, AI-driven network management and troubleshooting, and transparent, secure supply chains. This evolution underscores a broader transition toward software-defined, service-oriented networking models where agility, automation, and integration capabilities play a central role in long-term market leadership.

Branch Router Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Hewlett Packard Enterprise Company

Nokia Corporation

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Huawei unveiled its upgraded Xinghe Intelligent Network, adding pre-Wi-Fi 8 access, intrinsic security boards, and generative AI SOC automation for campus and branch deployments.

- April 2026: Dell Technologies, Nokia, and Intel introduced a low-footprint user-plane function device based on Intel Xeon 6, targeting distributed 5G edge rollouts with planned availability in H2 2026.

- March 2026: The United States Federal Communications Commission prohibited new foreign-manufactured consumer routers from gaining authorization, citing national security concerns.

- March 2026: Fortinet released FortiOS 8.0 with AI-aware application control, multipath IPsec, SASE Outpost, and post-quantum cryptography options.

Global Branch Router Market Report Scope

The branch router market refers to the revenue generated from routers deployed at distributed enterprise locations such as branch offices, retail outlets, bank branches, healthcare facilities, and remote sites to enable secure and reliable connectivity with central data centers, cloud platforms, and wide-area networks. These routers manage traffic between local branch networks and external networks while supporting applications such as secure internet access, VPN connectivity, and cloud-based services.

The Branch Router Market Report is Segmented by Throughput Class (Low-throughput Branch Routers, Mid-range Branch Routers, High-performance Branch Routers, and Ultra-high Branch Routers), Branch Size (Small branch, Medium branch, and Large branch), Access Connectivity (Ethernet, Broadband, 4G/LTE, 5G, and Hybrid), End User Industry (IT and Telecom, BFSI, Retail and E-commerce, Healthcare and Lifesciences, Government and Public Sector, Manufacturing, Education, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Low-throughput Branch Routers |

| Mid-range Branch Routers |

| High-performance Branch Routers |

| Ultra-high Branch Routers |

| Small Branch |

| Medium Branch |

| Large Branch |

| Ethernet |

| Broadband |

| 4G/LTE |

| 5G |

| Hybrid |

| IT and Telecom |

| BFSI |

| Retail and E-commerce |

| Healthcare and Lifesciences |

| Government and Public Sector |

| Manufacturing |

| Education |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Throughput Class | Low-throughput Branch Routers | |

| Mid-range Branch Routers | ||

| High-performance Branch Routers | ||

| Ultra-high Branch Routers | ||

| By Branch Size | Small Branch | |

| Medium Branch | ||

| Large Branch | ||

| By Access Connectivity | Ethernet | |

| Broadband | ||

| 4G/LTE | ||

| 5G | ||

| Hybrid | ||

| By End User Industry | IT and Telecom | |

| BFSI | ||

| Retail and E-commerce | ||

| Healthcare and Lifesciences | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Education | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the branch router market be by 2031?

Mordor Intelligence projects the branch router market size to reach USD 11.05 billion by 2031, advancing at a 6.41% CAGR over 2026-2031.

Which throughput class is growing the fastest?

High-performance branch routers are forecast to grow at a 7.12% CAGR through 2031, supported by edge AI and private 5G workloads.

Which industry segment is expanding most rapidly?

Retail and e-commerce is projected to post the highest 7.04% CAGR between 2026-2031 as omnichannel models demand resilient branch connectivity.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to lead with an 8.18% CAGR through 2031, driven by manufacturing digitalization and widespread private 5G rollouts.

What is driving cellular adoption at branch sites?

Expanded private-spectrum options, Citizens Broadband Radio Service availability, and falling 5G equipment costs are accelerating the move toward cellular-first or hybrid WAN designs for enterprise branches.

Page last updated on: