Enterprise Routers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

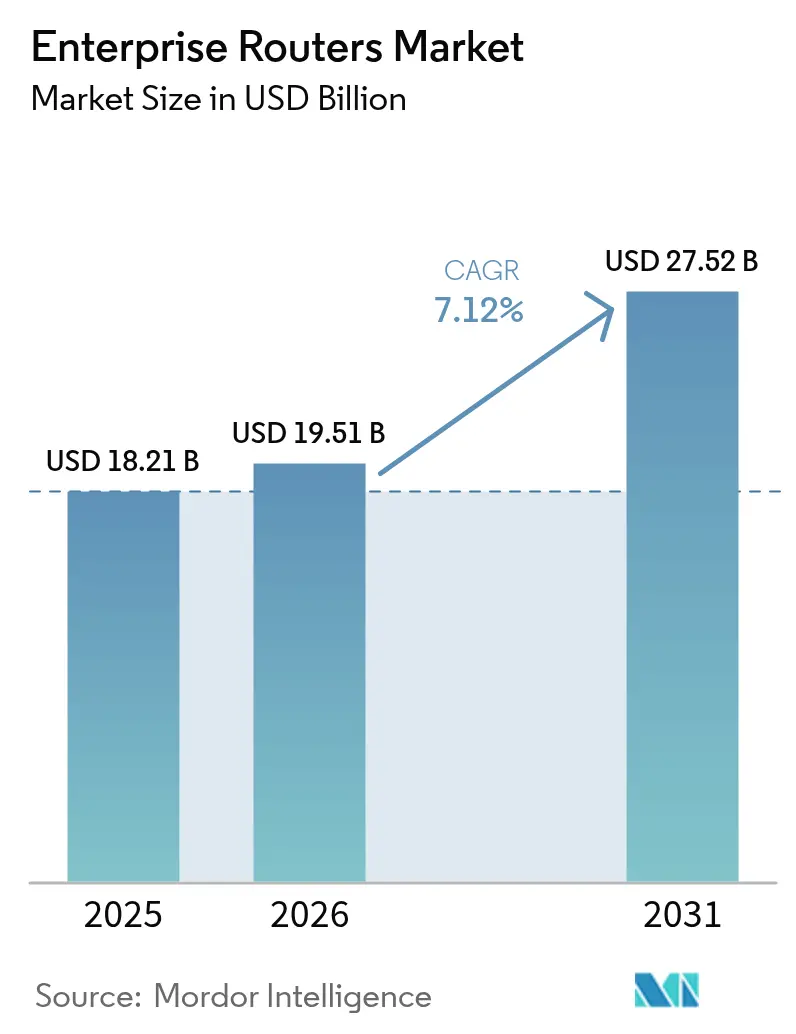

| Market Size (2026) | USD 19.51 Billion |

| Market Size (2031) | USD 27.52 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Routers Market Analysis by Mordor Intelligence

The enterprise routers market size was valued at USD 18.21 billion in 2025 and estimated to grow from USD 19.51 billion in 2026 to reach USD 27.52 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Growth reflects enterprises’ shift from legacy WANs to software-defined architectures that support hybrid work, multi-cloud connectivity, and edge intelligence. Wired connectivity continues to anchor critical backbones yet wireless upgrades are accelerating as organizations deploy IoT devices and mobile-first workflows. Consolidation among leading vendors coincides with rising demand for AI-driven automation, energy efficiency, and embedded security, all of which are now viewed as baseline purchase criteria rather than premium features. Regionally, North America retains scale advantages, but Asia Pacific’s manufacturing digitization and 5G rollouts are generating the fastest incremental revenue. Midsize enterprises are emerging as influential buyers because SD-WAN and intent-based networking lower both capital and operating costs.

Key Report Takeaways

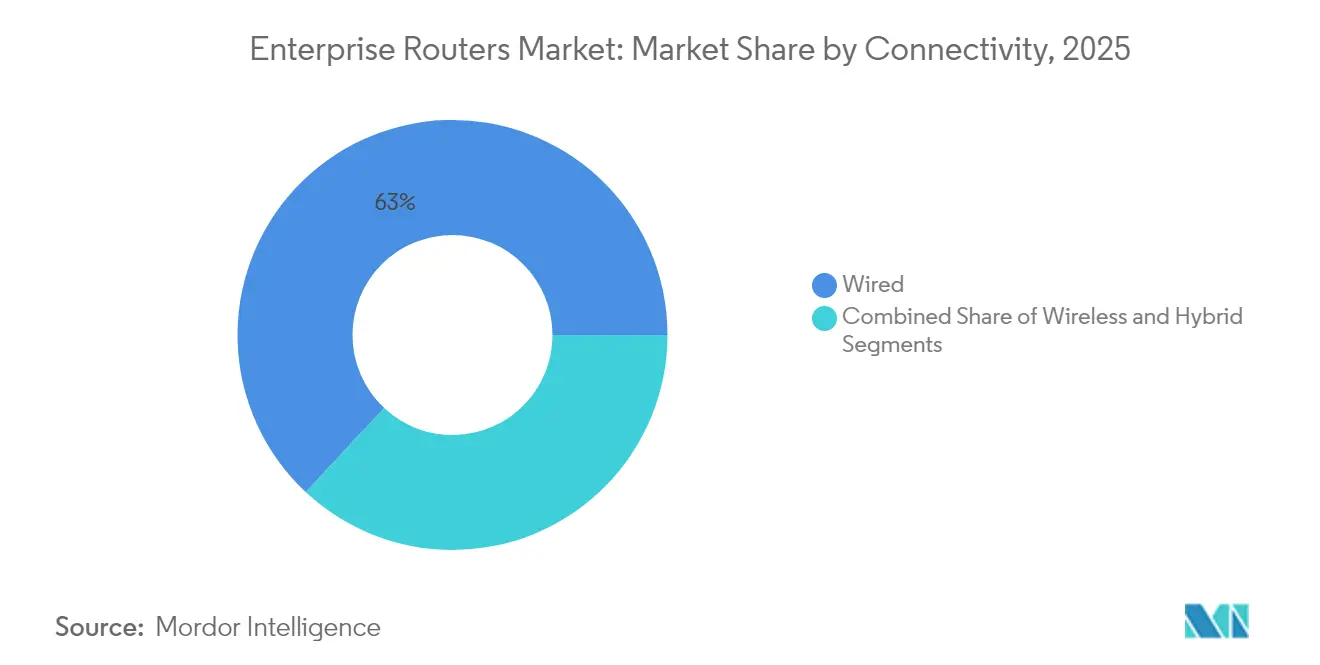

- By connectivity, wired solutions controlled 63.04% of 2025 revenue in the enterprise routers market, while wireless installations are advancing at an 8.53% CAGR through 2031.

- By port density, 9-24-port systems accounted for a 48.10% enterprise routers market share in 2025, whereas configurations above 24 ports are expanding at 8.01% CAGR.

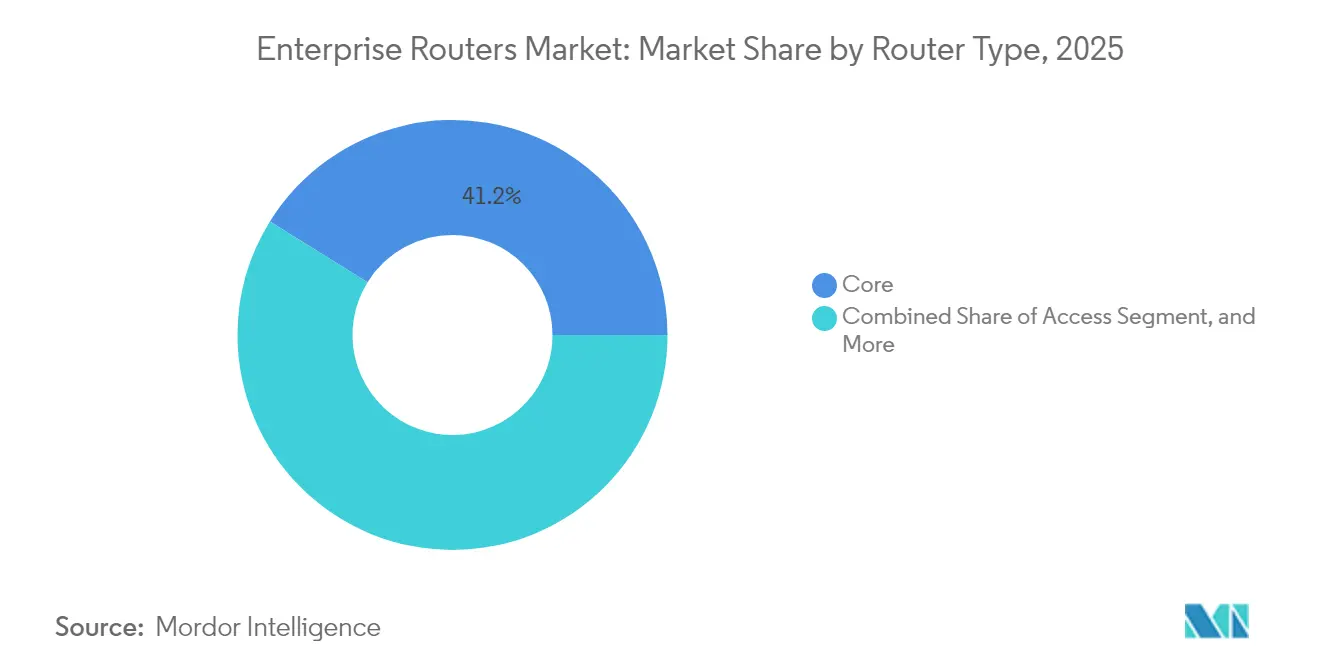

- By router type, core platforms held 41.15% revenue in 2025 in the enterprise routers market; SD-WAN appliances offer the quickest growth at 7.58% CAGR through 2031.

- By end-user industry, IT and Telecom led with 29.25% of 2025 spending in the enterprise routers market, while Retail and E-commerce are set to climb at a 7.55% CAGR to 2031.

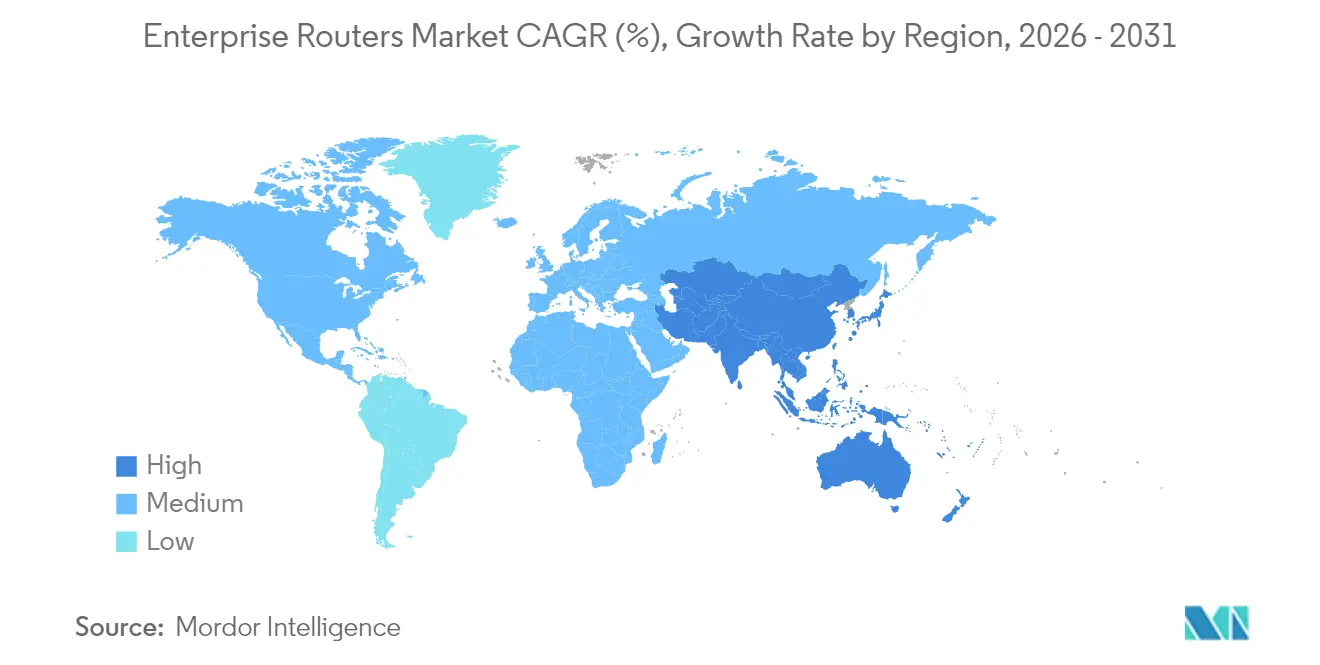

- By geography, North America represented 38.40% of global sales in 2025 in the enterprise routers market, yet Asia Pacific is pacing the field with a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Routers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing SD-WAN adoption | +1.2% | Global, with North America leading adoption | Medium term (2-4 years) |

| Surge in enterprise cloud migration | +0.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Edge-compute traffic explosion | +1.1% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Sustainability-driven router refresh | +0.9% | Europe and North America regulatory focus | Medium term (2-4 years) |

| AI-driven intent-based networking | +1.0% | Global, early adoption in tech-forward enterprises | Long term (≥ 4 years) |

| Government secure-routing mandates | +0.7% | National security focus, global implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing SD-WAN Adoption

Software-defined WAN has altered the economics of wide-area connectivity by minimizing MPLS spend and simplifying policy control. Cisco processed a 15% year-over-year increase in SD-WAN product orders during Q2 2025, bringing its Catalyst SD-WAN customer base above 50,000 enterprises.[1]Cisco Systems, “Cisco Reports Second Quarter Earnings,” cisco.com Mid-market organizations that once deemed enterprise-grade WAN unaffordable can now trim network operating expenses by 30–50% while improving application response through dynamic path selection. Security remains integral as zero-trust principles steer procurement, making integrated firewalls and segmentation table-stakes for router vendors. The momentum is likely to sustain medium-term market expansion because SD-WAN refresh cycles average three to five years, creating repeat demand within the forecast horizon.

Surge in Enterprise Cloud Migration

Enterprises consolidating on-premises data centers by 40% while elevating cloud workload density are re-architecting networks around direct internet access and multi-cloud links.[2]Dell Technologies, “Dell Technologies Reports Third Quarter Fiscal 2025 Financial Results,” dell.com Routers must manage dynamic bandwidth, granular QoS, and automated route policies that honor data-sovereignty rules. Latency-sensitive apps such as real-time analytics are encouraging edge routers that decide traffic flows in milliseconds rather than backhauling packets to centralized gateways. Vendor roadmaps therefore emphasize cloud gateways and API-level orchestration that align route decisions with compute location and compliance tags.

Edge-Compute Traffic Explosion

Industry 4.0 rollouts in manufacturing generate terabytes of sensor data demanding local processing; Siemens has demonstrated selective cloud synchronization models that cut WAN traffic while upholding sub-millisecond control-loop latency.[3]Siemens, “Fiscal 2024 Results,” siemens.com Enterprise routers situated at micro data centers now bundle switching and compute to execute AI inference, handle protocol translation, and enforce zero-trust segmentation. Retail, automotive, and logistics sectors mimic this architecture to power real-time inventory analytics, autonomous vehicle telemetry, and augmented-reality workflows. The need to ingest and analyze data at the edge is converting traditional access routers into converged appliances that add CPUs and accelerators alongside packet-forwarding ASICs.

Sustainability-Driven Router Refresh

Energy efficiency mandates and carbon pricing in Europe and North America have elevated power draw as a decisive buying factor. Cisco’s latest Catalyst 9000 platforms deliver 40% lower consumption yet triple performance density, enabling large enterprises to retire thousands of legacy devices and shrink data-center footprints. Power accounts for 15–20% of IT operating costs for such firms, so the ROI on green networking is immediate. Vendors additionally roll out take-back and refurbishment programs; Juniper’s circular-economy initiative keeps equipment in productive use and diverts e-waste from landfills. Sustainability metrics are now embedded in RFP scorecards, forcing suppliers to publish life-cycle assessments and material traceability records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent supply-chain chip shortages | +0.6% | Global, acute in APAC manufacturing hubs | Short term (≤ 2 years) |

| Skill-gap in programmable networking | +0.3% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Rising SASE cannibalisation | +0.4% | Global, concentrated in cloud-forward enterprises | Medium term (2-4 years) |

| Open-source white-box disruption | +0.2% | North America and Europe early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Supply-Chain Chip Shortages

Specialized ASICs powering high-end routing platforms remain in tight supply, stretching lead times to 20-26 weeks and inflating component costs. Enterprises respond by adopting multi-vendor frameworks and committing to longer procurement contracts, yet mission-critical projects still face deferrals. Basic access routers see smaller impact because they can swap in more common merchant silicon, but data-center cores experience acute shortages due to cutting-edge process node dependence.

Rising SASE Cannibalization

Secure Access Service Edge bundles networking and security functions into cloud-delivered subscriptions, reducing the need for branch routers. The SASE segment reached USD 4.2 billion in 2024 and is growing at 24.7% CAGR, siphoning mid-market accounts toward providers like Palo Alto Networks and Zscaler. Large enterprises with regulatory obligations still prefer on-premises routing, tempering cannibalization, yet OEMs are hedging by embedding SASE agents directly into new router lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity: Wireless Momentum Challenges Wired Dominance

Wired links captured 63.04% of 2025 revenue, underpinning workloads that demand deterministic throughput and strong electromagnetic shielding. Simultaneously, wireless deployments are gaining an 8.53% CAGR as companies pursue flexible floorplans, IoT sensor grids, and campus mobility. Hybrid designs that marry fiber backbones with Wi-Fi 6E access deliver the reliability of cable and the agility of radio, shrinking deployment timelines by up to 60%. Private 5G networks now achieve sub-millisecond latency once reserved for copper links, unleashing industrial robots and autonomous guided vehicles across factory floors.

Enterprises also weigh spectrum governance, interference, and battery life in deciding between Ethernet and wireless endpoints. Wi-Fi 6E’s 6 GHz channels supply 1.2 GHz of fresh spectrum, reducing contention and enabling 160 MHz-wide channels that approximate cabled performance. For disaster recovery, LTE and 5G routers furnish immediate connectivity when terrestrial lines fail, a feature prized by retail chains that cannot tolerate point-of-sale downtime. The enterprise routers market continues to bifurcate: mission-critical segments stay on fiber while edge and branch environments adopt radio first, sustaining parallel demand paths across the forecast horizon.

By Port Density: High-Density Solutions Accelerate Infrastructure Consolidation

Routers with 9–24 ports held a 48.10% enterprise routers market share in 2025, reflecting their role as workhorse aggregation nodes in medium server closets. Yet platforms exceeding 24 ports are expanding at 8.01% CAGR as data-center operators consolidate racks and strive for two-tier leaf-spine topologies that minimize cabling and latency. High-density chassis reduce per-port costs by up to 35% and free valuable floor space, allowing operators to defer expensive building expansions.

Virtualization and containerization have magnified east-west traffic, driving 400GbE interface adoption on routers that can fan out numerous virtual connections. Conversely, edge micro-data centers advocate compact eight-port designs with PoE profiles tailored for cameras and sensors. Regulatory demands for network segmentation in healthcare and finance require port-level policy control, encouraging modular line-cards that let administrators allocate physical interfaces by trust zone. The enterprise routers market therefore supports simultaneous demand for dense cores and compact edges, depending on workload placement strategies.

By Router Type: SD-WAN Appliances Disrupt Traditional Hierarchies

Core routers retained 41.15% revenue in 2025 on the strength of hyperscale and telecom orders, but SD-WAN appliances are expanding at 7.58% CAGR by collapsing routing, optimization, and security into software-defined overlays. Edge and aggregation tiers still matter for fail-safe redundancy in manufacturing and banking, where downtime carries heavy penalties.

Artificial-intelligence telemetry increasingly steers router selection, with platforms embedding inference engines that predict faults and automate ticket escalation. Access routers face substitution from Wi-Fi and 5G gateways that natively handle routing functions, cutting hardware SKUs at branch sites. Regulatory frameworks such as NIST SP 800-53 prompt buyers to prioritize routers offering integrated threat prevention and encrypted telemetry, nudging OEM roadmaps toward converged network-security appliances.

By End-User Industry: Retail Digitization Accelerates Infrastructure Demands

IT and Telecom contributed 29.25% of 2025 spending, given their constant need for backbone upgrades and service delivery platforms. Retail and e-commerce however are poised for 7.55% CAGR growth as omnichannel strategies hinge on real-time inventory and personalized promotions. A 100-millisecond latency cut can lift conversion rates by up to 2%, translating networking investments directly into revenue.

Manufacturers adopting deterministic Ethernet and time-sensitive networking demand routers with microburst buffering and precise clock synchronization. Healthcare facilities integrate medical IoT while obeying HIPAA and GDPR, mandating segmented networks with zero-trust policy enforcement. Financial institutions prioritize sub-microsecond latency for high-frequency trading while meeting strict compliance audits, sustaining premium pricing for performance-optimized routing platforms. Government and defense contracts specify FIPS-validated encryption and supply-chain provenance, enlarging the addressable pool for secure routing equipment.

Geography Analysis

North America commanded a 38.40% enterprise routers market share in 2025 on the back of established fiber backbones, early SD-WAN adoption, and stringent federal cybersecurity directives. Demand persists as agencies migrate toward zero-trust architectures and enterprises refresh for energy efficiency, though unit growth slows relative to emerging regions. Canadian enterprises in oil, gas, and mining adopt ruggedized routers rated for temperature swings and airborne particulates.

Asia Pacific is the fastest-growing territory at a 7.61% CAGR through 2031, buoyed by 5G buildouts and state-sponsored manufacturing digitization. China’s policy of indigenous technology preference nurtures domestic router OEMs while compelling multinationals to localize production and firmware audits. India’s Digital India program fosters broadband to rural districts and data-center corridors, catalyzing edge-router installations across fintech, healthcare, and BPO verticals. Japan’s Society 5.0 roadmap spurs investments in automation and smart infrastructure, sustaining premium demand for deterministic and low-latency routing gear.

Europe exhibits steady revenue progression anchored in sustainability regulations and GDPR-driven data-sovereignty rules, prompting on-premises router deployments that pair green design with compliance guarantees. Circular-economy incentives encourage take-back schemes and refurbished hardware. Latin America upgrades telco backbones and mining operations, favoring high-temperature tolerant hardware. Middle Eastern smart-city programs in the UAE and Saudi Arabia require AI-enabled routers to direct video analytics and IoT telemetry, while African nations begin leapfrogging to 5G fixed-wireless access, sparking demand for integrated cellular routers in enterprise branches.

Mordor Intelligence provides coverage of the enterprise routers market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Enterprise router shipments increasingly hinge on cybersecurity, encryption, and equipment authorization requirements across major markets. In the United States, FCC equipment authorization is a gating step for radio-enabled enterprise routing products, and the FCC Covered List update dated March 23, 2026 tightened national-security related scrutiny for routers produced in certain foreign countries. Public-sector and regulated-industry procurements also frequently require FIPS 140-3 validated cryptographic modules under NIST's Cryptographic Module Validation Program (CMVP), which shapes hardware and software choices for VPN, secure management, and telemetry.

In the European Union, the Cyber Resilience Act (Regulation (EU) 2024/2847) formalizes cybersecurity obligations for products with digital elements, including routers intended for internet connection within its stated scope. The CRA pushes secure-by-design and vulnerability handling into compliance deliverables (including coordinated disclosure processes and documentation such as SBOM practices), increasing the compliance workload for OEMs and integrators selling enterprise routing platforms into EU member states.

Value Chain Analysis

The enterprise router value chain runs from silicon IP and advanced packaging through OEM hardware design, OS and security software, contract manufacturing, and global distribution via direct enterprise sales and channel partners (VARs, distributors, MSPs, and cloud-managed networking providers). Component availability remains a key swing factor for lead times, with high-end routing ASICs, optics, and memory (DRAM/NAND) affecting delivery schedules for core and high-density platforms; this has shown up in 2026 through vendor pricing actions and tighter focus on supply assurance. OEMs also differentiate through vertically integrated silicon and optics roadmaps (for example, Cisco Silicon One and Acacia optics) to reduce exposure to merchant-silicon constraints and improve cost-per-bit and power efficiency.

Downstream, regulatory and authorization workflows feed back into manufacturing and logistics decisions. The FCC's March 2026 restrictions on certain imported routers added friction for suppliers relying on overseas assembly, while US operators and industry groups sought waivers to keep previously certified models shipping amid component substitution needs tied to substrate and memory shortages. Together, these pressures favor multi-region manufacturing footprints, tighter BOM governance, and closer coordination between OEM engineering teams and channel ecosystems to manage certifications, firmware provenance, and lifecycle support for enterprise deployments.

Competitive Landscape

The enterprise routers market sits in a mid-consolidated state as leading players chase scale and software prowess. HPE’s USD 14 billion acquisition of Juniper Networks in July 2025 positions the combined entity as an end-to-end rival to Cisco by unifying compute, storage, and AI-driven networking under one orchestration fabric. Cisco retains volume leadership through a broad catalog and channel depth yet pivots toward subscription-based licenses to lock in recurring revenue.

Arista focuses on hyperscale data-center routers; its 7280R4 line delivers 25.6 Tbps switching at 400 GbE while cutting power by 40%, aligning with cloud operators’ TCO metrics. Fortinet and Palo Alto Networks extend firewall franchises into routing by embedding SD-WAN and SASE, threatening incumbents in the branch segment. Microsoft champions the open-source SONiC network OS, enabling white-box entrants that erode hardware margins.

Competitive parameters now orbit software automation, security convergence, and sustainability credentials rather than raw port counts. Vendors advertise AI telemetry, intent-based orchestration, and zero-touch provisioning to cut operational overhead for skill-constrained IT teams. Buyers also assess life-cycle carbon impact and circular-economy participation. As hardware commoditizes, ecosystems, training, support, app marketplaces, become decisive tiebreakers in multi-million-dollar RFPs.

Enterprise Routers Industry Leaders

Cisco Systems, Inc.

Juniper Networks, Inc.

Hewlett Packard Enterprise Co.

Huawei Technologies Co., Ltd.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise buyers are seeking routing platforms that can support AI-era infrastructure, combining high throughput with automation, telemetry, and security convergence. Product activity highlights whitespace around dense, fixed-form-factor core and WAN routing optimized for power and space constraints: Juniper's PTX10002-60MR (introduced March 2026) targets core, WAN, and AI-driven data center use cases in a 2RU system with 14.4 Tbps forwarding capacity, reflecting demand for compact systems that raise radix and bandwidth without reverting to large modular footprints. At the same time, feature velocity in carrier and large-enterprise routing stacks supports differentiated upgrade cycles, such as Cisco IOS XR updates for ASR 9000 series (June 2026) that expand capabilities including P-BNG and cnBNG coexistence and nV satellite enhancements.

Security and compliance-driven refresh also opens opportunity, particularly for public-sector and regulated industries that require validated cryptography and demonstrable vulnerability handling. The FCC Covered List update in March 2026 and the EU's Cyber Resilience Act framework raise the emphasis on supply-chain traceability, secure management planes, and coordinated vulnerability processes, favoring vendors that productize compliance (for example, FIPS-aligned cryptographic implementations, hardened telemetry, and documented lifecycle processes). Edge and branch modernization continues to expand demand for industrial-grade and cloud-managed form factors, supported by portfolio additions for ruggedized edge models and platforms designed to host localized workloads and policy enforcement closer to devices and sites.

Recent Industry Developments

- March 2026: Juniper Networks introduced the PTX10002-60MR, a 2RU fixed-form router built on the Express 5 ASIC and positioned for core, WAN, and AI-driven data center deployments. The launch points to continued migration toward dense, fixed platforms that prioritize throughput-per-rack-unit and power efficiency for modern fabrics.

- October 2025: Cisco unveiled the Cisco 8223 fixed routing system, a 51.2 Tbps Ethernet router using the Silicon One P200 chip aimed at distributed AI workload connectivity. It reinforces the competitive push toward very high-capacity systems and tighter integration between routing silicon, software, and automated operations.

- March 2024: Juniper Networks launched the PTX10002-36QDD, a 28.8 Tbps fixed-form router powered by the Express 5 ASIC. This product step-up advanced fixed-form adoption in high-performance routing footprints, shaping how enterprises and operators plan upgrades for 400G and emerging 800G design cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers enterprise-grade routers that route and secure data traffic across corporate WAN and campus networks, branches, and enterprise edge locations. The sizing is based on revenue generated from the sale of these routers across major regions.

Scope exclusions: Consumer home routers, operator core routing sold primarily for telecom backbone buildouts, and general IT services not bundled with the router sale are excluded.

Segmentation Overview

- By Connectivity

- Wired

- Wireless

- Hybrid

- By Port Density

- less than or equal to 8 Ports

- 9 – 24 Ports

- above 24 Ports

- By Router Type

- Core

- Edge / Aggregation

- Access

- SD-WAN Appliance

- By End-user Industry

- BFSI

- IT and Telecom

- Healthcare

- Retail and E-commerce

- Manufacturing

- Government and Defense

- Education

- By Geography

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South-East Asia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping what is counted as an enterprise router sale and where demand is coming from across regions and industries. We relied on public sources such as FCC filings and related equipment authorization references, OECD and World Bank digital economy indicators, ITU connectivity statistics, and U.S. International Trade Commission trade data to cross-check macro direction and network equipment movement.

To keep the model grounded, we also reviewed company annual reports, earnings call transcripts, investor presentations, product documentation, and credible press coverage on enterprise network refresh cycles and SD-WAN adoption. In a few places, we used paid subscriptions for company financials and news intelligence, plus a patent database to understand refresh timing around routing silicon and software features. The desk sources listed here are illustrative, and other public references were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test what we learned from public information, especially on router replacement timing, typical deal sizing, and how SD-WAN appliances are counted inside enterprise routing budgets. We spoke with a mix of manufacturers, channel partners, enterprise IT buyers, and network architects across APAC, EMEA, and the Americas, and then re-contact was done when large gaps showed up between regions or verticals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 43% |

| Mid tier: 58% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 14% | Managers: 57% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing is built using top-down and bottom-up logic, where the top-down approach reconstructs the demand pool from enterprise network spend signals and router refresh cycles, and then assigns shares to enterprise router categories. Totals are corroborated using selective bottom-up approximations such as sampled average selling price ranges by router class, channel checks on shipment momentum, and supplier revenue consistency checks before final totals are locked.

Key inputs used in the model include enterprise IT and network capex direction, SD-WAN appliance adoption as a share of branch routing, port density mix (lower port versus high port systems), typical replacement cycles in core and edge environments, and region-level rollout pace tied to hybrid work and multi-cloud connectivity needs. Where a bottom-up view is incomplete for smaller suppliers, we fill gaps using channel partner feedback and a conservative revenue banding approach, then reconcile it back to the top-down demand envelope.

Forecasts are generated using scenario analysis supported by short-run smoothing on the core drivers, since buying cycles can shift when budgets tighten or when large refresh programs kick in. The final forecast set is reviewed with primary respondents to confirm that assumed price progression and mix shifts align with real procurement behavior.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent signals such as enterprise infrastructure budget commentary, regional network equipment trade direction, and the pace of SD-WAN rollout discussed by practitioners. When variances appear, we check for mix errors, timing mismatches in currency conversion, or double counting between traditional routers and SD-WAN appliances, and then adjust assumptions in a controlled way.

Before sign-off, the model and narrative go through multi-step analyst review, and callbacks are triggered if any large regional swings or unusual growth rates are detected. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp pricing shifts, major technology transitions, or policy changes affecting network equipment procurement. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Enterprise Routers Market Estimate Compared With Other Published Estimates

Published market values for enterprise routers often do not match because companies count slightly different products, pick different base years, and make different choices on how to treat pricing and refresh cycles. Even when the topic name looks the same, small scope decisions can move the number by several billions.

The table shows a wide spread mainly because some estimates roll enterprise routers into a broader enterprise networking equipment bucket, and others count software and services as part of the router value even when they are sold separately. In Mordor Intelligence's model, SD-WAN appliances are included only when they are positioned and purchased as routing endpoints for enterprise WAN use cases, which reduces overlap with general security appliances and broader networking spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.51 B (2026) | |

| Global Consultancy A | USD 27.01 B (2024) | Uses an enterprise networking segmentation lens where the enterprise routers figure can reflect a broader equipment revenue pool, and the base year timing differs, which can inflate comparisons versus a router-only scope. |

| Industry Publisher B | USD 16.94 B (2024) | Base year and pricing progression assumptions are set earlier in the cycle, and treatment of router classes can vary, especially when SD-WAN and edge devices are grouped differently across categories. |

Taken together, the comparison suggests the main swing comes from what is counted alongside enterprise routers and how mixed devices are classified, not from arithmetic differences. By keeping the value build tied to clear router demand indicators, practical pricing ranges, and repeatable checks, we get an estimate that is easier to trace and update when market conditions change.

Key Questions Answered in the Report

What is the current revenue pool for enterprise routers?

The enterprise routers market size is USD 19.51 billion in 2026 and is forecast to reach USD 27.52 billion by 2031.

How fast is wireless adoption growing relative to wired deployments?

Wireless router revenue is rising at an 8.53% CAGR through 2031, outpacing wired upgrades yet complementing them in hybrid designs.

Which region offers the highest growth potential for vendors?

Asia Pacific is projected to expand at a 7.61% CAGR through 2031 on the back of 5G rollouts and manufacturing digitization initiatives.

What role does SD-WAN play in refresh decisions?

SD-WAN appliances are the fastest-growing router type at 7.58% CAGR because they cut MPLS spend and embed security into software overlays.

How are sustainability goals affecting purchase criteria?

Buyers prioritize models delivering up to 40% lower power consumption and vendors offering take-back programs aligned with circular-economy principles.

Page last updated on: