SOHO Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.83 Billion |

| Market Size (2031) | USD 17.82 Billion |

| Growth Rate (2026 - 2031) | 8.54% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

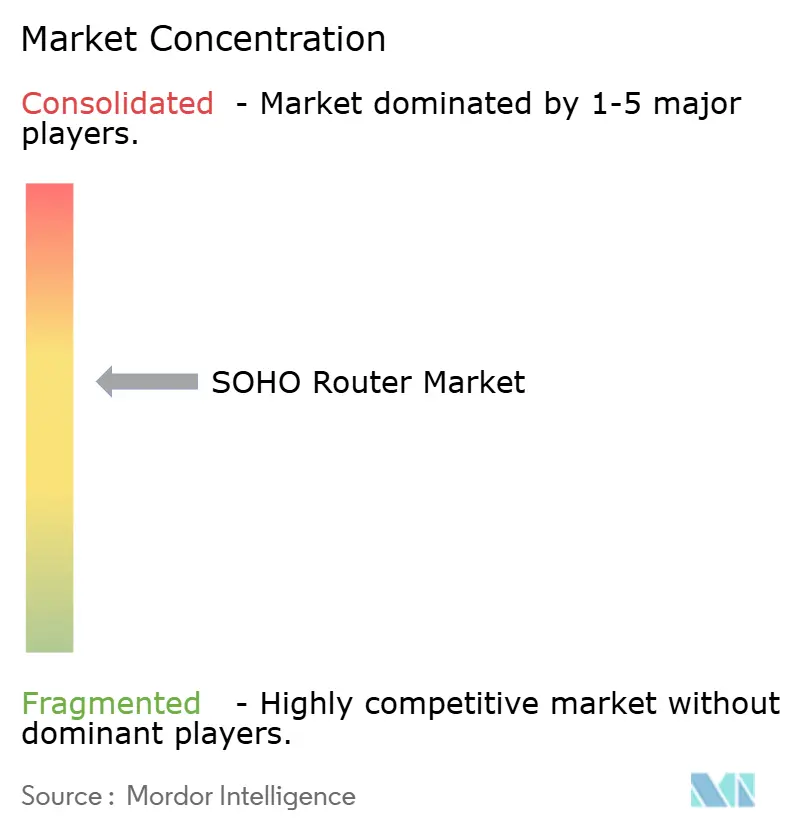

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SOHO Router Market Analysis by Mordor Intelligence

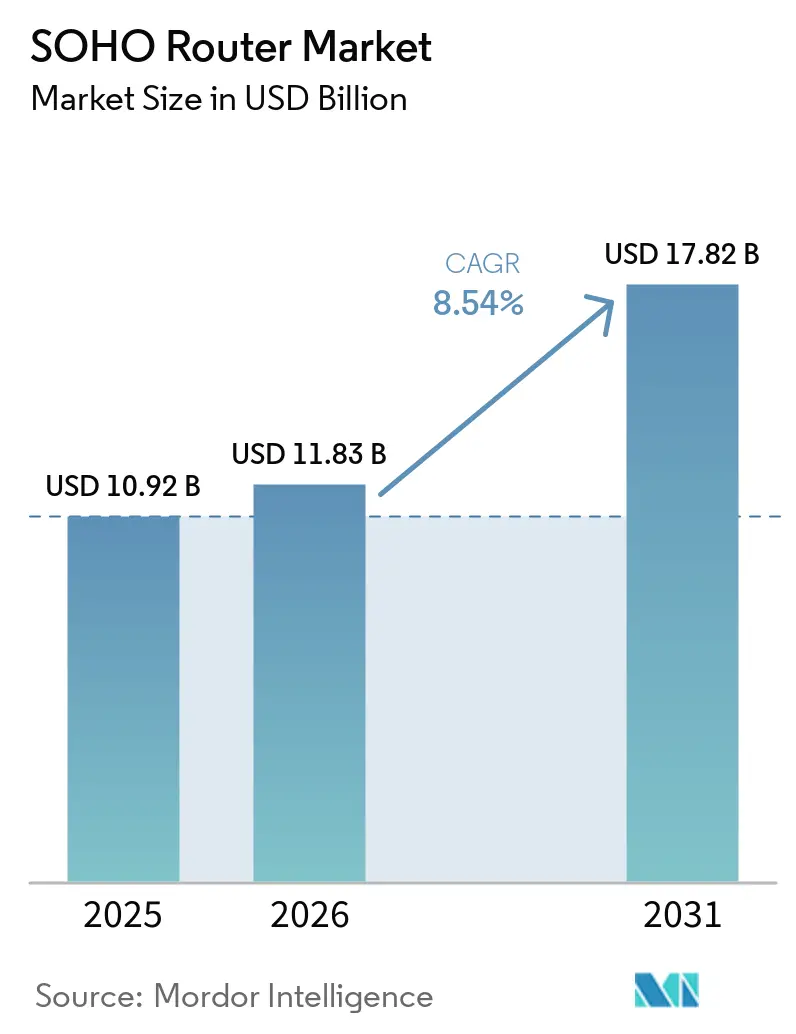

The SOHO router market size was valued at USD 10.92 billion in 2025 and estimated to grow from USD 11.83 billion in 2026 to reach USD 17.82 billion by 2031, at a CAGR of 8.54% during the forecast period (2026-2031). Rising hybrid work adoption, continued fiber rollouts, and the rapid commercialization of Wi-Fi 6E and Wi-Fi 7 chipsets are expanding the addressable market for tri-band and quad-band units. U.S. teleworking remained elevated at 22.6% of employed persons in March 2026, sustaining upstream-bandwidth demand that legacy single-band solutions cannot serve. Service-provider bundling of premium routers with symmetrical-gigabit plans is accelerating refresh cycles, while FCC approval for standard-power 6 GHz devices enables multi-gigabit coverage in homes and small offices. Competitive intensity remains moderate as established brands face pricing pressure from white-box vendors and substitution threats from 5G fixed-wireless gateways.

Key Report Takeaways

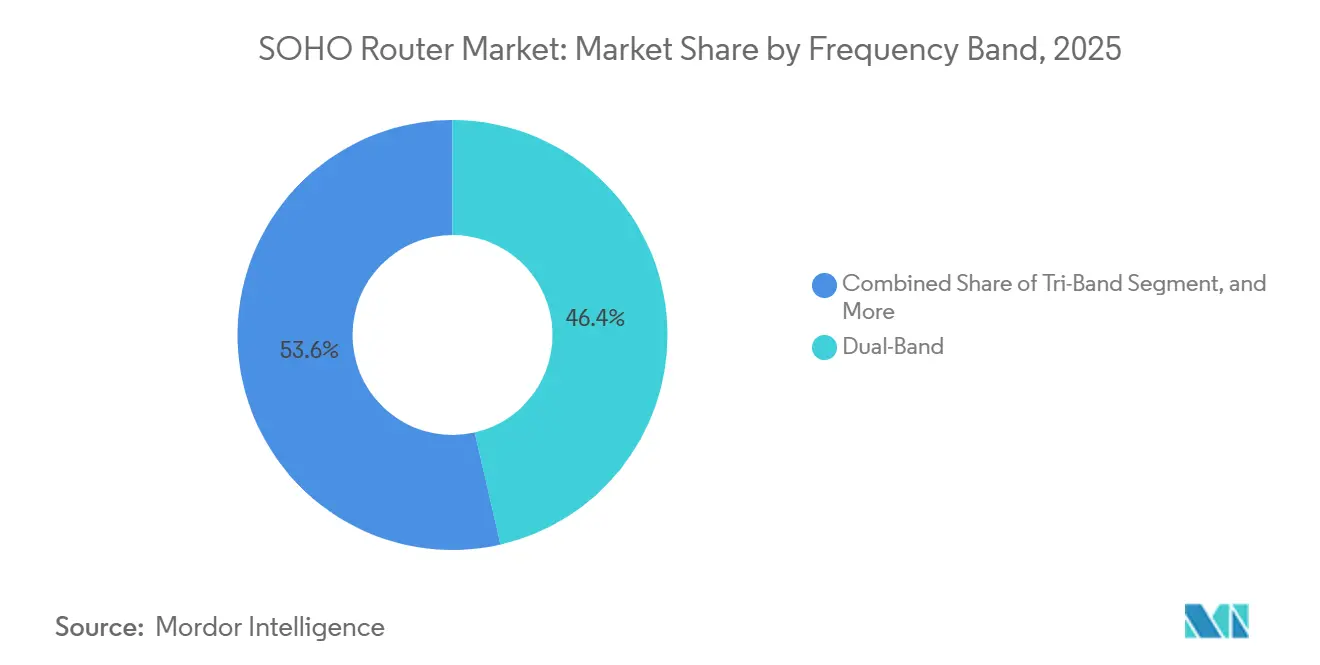

- By frequency band, dual-band routers led with 46.41% revenue share in 2025; tri-band configurations are projected to expand at a 12.64% CAGR through 2031.

- By Wi-Fi standard, Wi-Fi 5 accounted for 41.64% of shipments in 2025, while Wi-Fi 7 is forecast to grow at a 24.76% CAGR over 2026-2031.

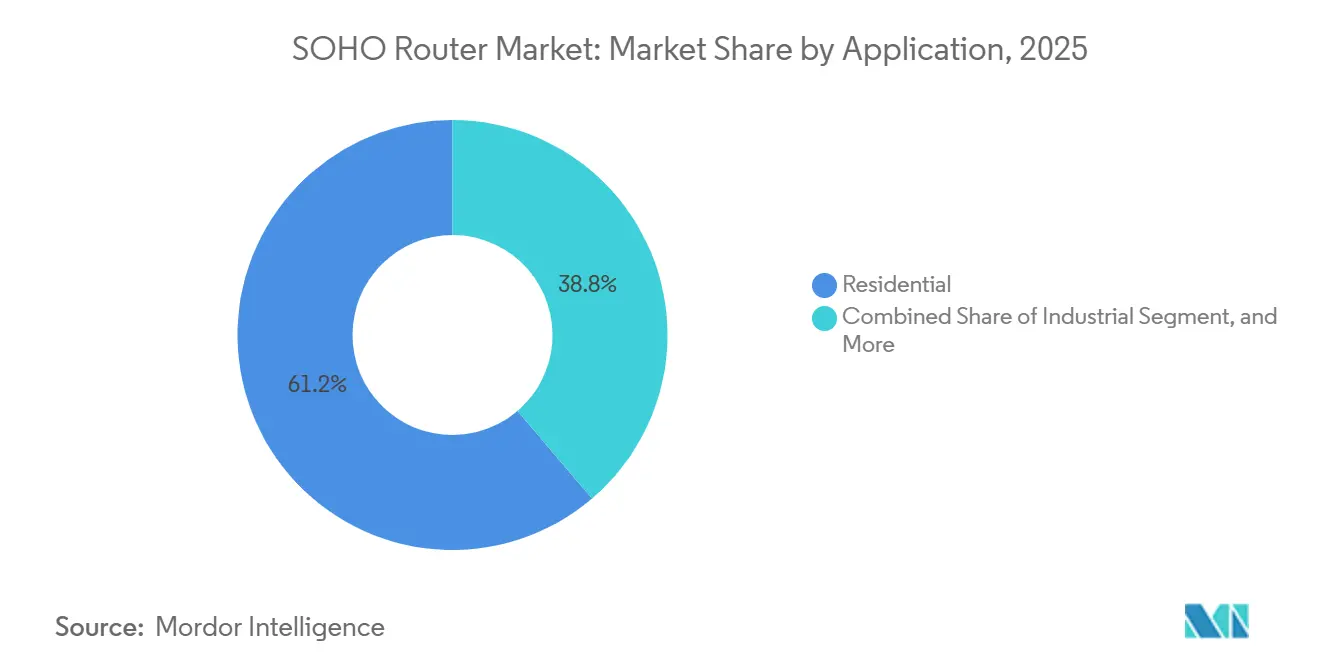

- By application, residential deployments held 61.24% share in 2025, and industrial small-office installations are advancing at a 12.34% CAGR through 2031.

- By distribution channel, ISP-bundled customer-premises equipment captured 45.63% share in 2025; online retail is rising at an 11.16% CAGR to 2031.

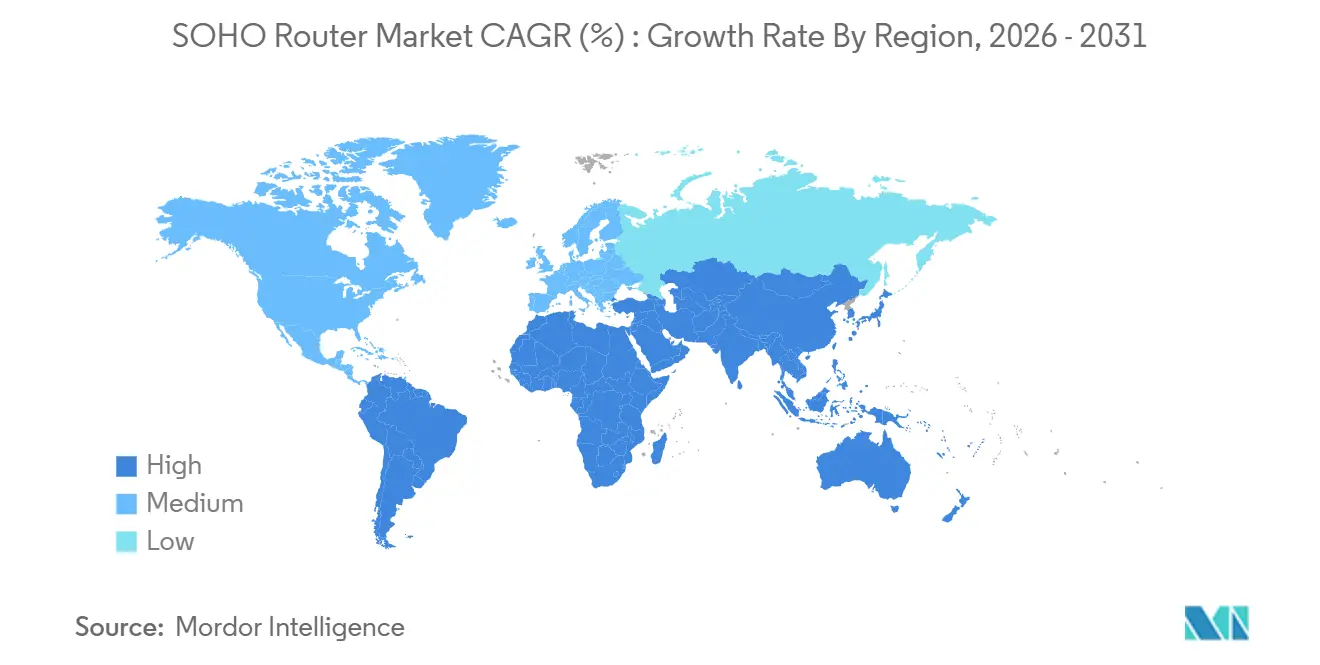

- By geography, Asia-Pacific commanded a 36.52% share in 2025, while South America is the fastest-growing region, with a 10.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SOHO Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of AI accelerators in routers enabling real-time traffic optimization | +2.1% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of Wi-Fi 6 and Wi-Fi 7 standards | +1.8% | Global, led by North America, Europe, and developed Asia-Pacific markets | Short term (≤ 2 years) |

| Accelerated rollout of fiber and 5G home broadband services | +1.5% | Global, with strongest impact in Asia-Pacific and South America | Medium term (2-4 years) |

| ISPs transitioning to subscription-based managed Wi-Fi services for SOHO customers | +1.3% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Surge in remote work and home learning post-2025 | +1.0% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Regulatory opening of 6 GHz spectrum in emerging economies | +0.8% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of AI Accelerators in Routers Enabling Real-Time Traffic Optimization

Routers embedding neural-processing units have shifted from passive packet forwarding to active orchestration. Charter Spectrum introduced Wi-Fi 7 gateways with on-device AI in 2025, reporting lower support calls after dynamic congestion rerouting. Qualcomm confirmed more than 250 networking designs using Wi-Fi 7 chipsets equipped with inference engines in its 2025 investor briefing. Such silicon classifies traffic flows and prioritizes latency-sensitive packets without manual quality-of-service rules. Households running simultaneous video conferences, cloud gaming, and IoT sensors benefit from lower jitter, reducing churn for service providers. Predictive alerts that flag anomalous traffic create upsell opportunities for managed security subscriptions.

Rapid Adoption of Wi-Fi 6 and Wi-Fi 7 Standards

The Wi-Fi Alliance certified 233 million Wi-Fi 7 devices in 2024 and forecasts 2.1 billion by 2028, eclipsing the ramp of Wi-Fi 6. MediaTek’s Filogic 880 and 660 platforms began shipping in 2025, enabling sub-USD 200 tri-band routers.[1]Qualcomm Technologies Inc., “Wi-Fi 7 Portfolio Briefing Broadcom and Qualcomm followed with quad-band reference designs that exploit 320-MHz channels and 4096-QAM to achieve 40 Gbps throughput. January 2026 FCC authorization for standard-power 6 GHz devices removed indoor-range limits, catalyzing small-office and industrial uptake. Together, lower chipset costs and regulatory clarity compress replacement windows for Wi-Fi 5 hardware.

Accelerated Rollout of Fiber and 5G Home Broadband Services

The United States surpassed 100 million fiber passings by September 2025, with AT&T alone covering 30 million premises. Brazil reached 77.2% fiber penetration in November 2024, while Argentina’s regulators pushed coverage to 41.6% by March 2025.[2]MediaTek Inc., “Filogic 880 and 660 Product Brief,” mediatek.com Symmetrical-gigabit links expose throughput bottlenecks in single-band routers, prompting upgrades to tri-band and quad-band devices that can sustain multi-gigabit backhaul. The Fiber Broadband Association projects upstream demand to grow up to tenfold within a decade, driven by 4K uploads, edge AI training, and dense IoT deployments.

ISPs Transitioning to Subscription-Based Managed Wi-Fi Services for SOHO Customers

North American cable operators are bundling hardware, software updates, and cybersecurity monitoring into monthly fees. Comcast’s xFi and Charter’s managed Wi-Fi have raised average revenue per user while lowering truck rolls. Customers perceive routers as part of a managed service, dampening price sensitivity for premium tri-band units. Vendors gain assured volumes but concede margin as carriers negotiate low bill-of-materials costs, pushing manufacturers toward white-label customization and cloud APIs.[3]Fiber Broadband Association, “Bandwidth Demand Study,” fiberbroadband.org

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing substitution threat from 5G fixed-wireless gateways bundled by carriers | -1.2% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Cybersecurity vulnerabilities and firmware update negligence | -0.9% | Global, with heightened risk in developing markets | Medium term (2-4 years) |

| Price sensitivity in developing markets limits premium router uptake | -0.7% | Asia-Pacific (excluding Japan, South Korea), Middle East, Africa, South America | Medium term (2-4 years) |

| Supply chain constraints for high-end RF front-end modules | -0.5% | Global, with acute impact on premium tri-band and quad-band segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Substitution Threat from 5G Fixed-Wireless Gateways Bundled by Carriers

T-Mobile bundles Inseego’s FX4200 and FX4100 gateways at zero upfront cost, integrating tri-band Wi-Fi 7 and 5G backhaul to displace standalone routers. Qualcomm’s single-die Dragonwing platform further lowers bill-of-materials, letting carriers subsidize hardware. Small enterprises seeking unified billing opt for these gateways, eroding retail router volumes, especially in areas where fiber is scarce.

Cybersecurity Vulnerabilities and Firmware Update Negligence

CISA listed critical flaws, including ASUS CVE-2025-59367 and Linksys CVE-2026-4558, that enable remote code execution on millions of devices.[4]Cybersecurity and Infrastructure Security Agency, “ASUS CVE-2025-59367,” cisa.gov Consumer-owned routers often remain unpatched for years, expanding attack surfaces and drawing regulatory scrutiny. ISP-managed models mitigate risk through automated updates, yet the large installed base of unmanaged units undermines buyer confidence, particularly among small businesses seeking to comply with emerging security standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Band: Tri-Band Adoption Accelerates In Congested Homes

Tri-band routers boosted the SOHO router market share by capturing latency-sensitive 4K streaming and cloud gaming demand in 2025. Dual-band systems still dominate the mid-priced tiers, but tri-band shipments are forecast to grow faster than the overall SOHO router market through 2031. Lower-cost Wi-Fi 7 silicon from MediaTek and Broadcom lowered street prices beneath USD 200, bringing multi-gigabit capacity to mass-market budgets.

Mesh networking is the principal catalyst: quad-band designs dedicate a 6 GHz radio for backhaul, delivering deterministic latency without Ethernet cabling. Regulatory clearance for standard-power 6 GHz radios in January 2026 allows tri-band kits to cover larger floorplates, boosting attachment rates in suburban homes. Single-band devices linger only in ultra-low-cost brackets and embedded IoT endpoints, signaling eventual obsolescence as chipset costs continue to fall.

By Wi-Fi Standard: Wi-Fi 7 Compresses the Upgrade Window

Wi-Fi 5 still anchors value-tier ISP bundles in 2025, yet Wi-Fi 7’s 24.76% CAGR positions it as the volume engine for the SOHO router market size beyond 2027. FCC authorization for higher-power 6 GHz operation expanded viable coverage footprints, while chipset vendors raced to integrate 320 MHz channels and multi-link operation. Early adopters in gaming and prosumer niches validated willingness to upgrade ahead of device cycles, shortening refresh intervals.

Enterprise-grade small offices prize Wi-Fi 6E for its OFDMA efficiency and target wake time features that prolong IoT battery life. Wi-Fi 4 and earlier generations are in steady decline, limited to legacy industrial controllers pending retrofit budgets. As more client devices ship with tri-band radios, interoperability concerns recede, widening replacement opportunities for vendors.

By Application: Industrial Small-Office Deployments Rise on Edge-Computing Adoption

Residential use cases accounted for the largest portion of the SOHO router market share in 2025, yet industrial small-office demand is expanding more rapidly. Manufacturers connecting machine-vision cameras and collaborative robots require deterministic latency and dual-WAN redundancy, which is driving the adoption of ruggedized Wi-Fi 7 routers. Home-office configurations now emphasize upstream throughput for cloud backups and real-time collaboration.

Gaming households seek advanced traffic shaping and low jitter performance, reinforcing premium tiers that bundle AI-based quality-of-service engines. The Fiber Broadband Association expects upstream traffic per home to multiply up to tenfold, bolstering the case for multi-gigabit architectures across all application segments.

By Distribution Channel: Online Retail Gains as Prosumers Seek Unlocked Tri-Band Units

ISP-bundled equipment anchored nearly half of the 2025 SOHO router market, but online retail is outpacing overall growth. Prosumers favor unlocked models with custom firmware and advanced VPN acceleration unavailable in carrier-supplied units. Xiaomi exploited flash-sale tactics and smartphone ecosystem lock-in to push routers across India and South America, while NETGEAR reduced reliance on brick-and-mortar stores amid inventory destocking.

Offline retail, big-box, and specialty outlets cater to buyers needing immediate replacement units or in-store support, yet face a margin squeeze from e-commerce price transparency. Enterprise VARs bundle routers with cloud-management platforms for multisite small-business networks, commanding service premiums.

Geography Analysis

Asia-Pacific contributed 36.52% to the SOHO router market in 2025, buoyed by China’s universal-broadband policy and India’s tier-2 fiber rollouts. Xiaomi monetized 904.6 million connected devices across its ecosystem, leveraging flash sales to lift router penetration in India (13.4% unit share) and Southeast Asia (16.7%). Japan’s dense apartment clusters accelerated Wi-Fi 6E adoption, while Australia’s NBN upgrades drove replacements of legacy ADSL hardware. The region’s heterogeneity divides demand between cost-optimized dual-band units and premium quad-band offerings.

South America leads growth at 10.46% CAGR as carriers extend fiber to secondary cities. Brazil, Chile, Peru and Mexico each exceeded 70% fiber penetration by late 2024, exposing bandwidth constraints in 2.4 GHz-only routers. TP-Link’s upcoming Brazilian factory will shorten supply chains and lower landed costs, while Xiaomi ranks second in regional share at 17.9%. Economic headwinds and currency depreciation heighten price sensitivity, but mesh bundles gain traction in urban São Paulo and Buenos Aires.

North America and Europe show mature penetration yet sustain replacement demand through Wi-Fi 7 upgrades and managed-service transitions. U.S. fiber passings crossed 100 million by September 2025, driving the adoption of routers capable of gigabit symmetric throughput. Charter’s Wi-Fi 7 gateway with 5G failover reduced support overhead and improved customer satisfaction, validating the managed model. Middle East smart-city agendas in the UAE and Saudi Arabia drive enterprise-grade router demand, whereas much of Africa relies on mobile broadband, limiting high-end router adoption.

Competitive Landscape

The SOHO router market remains moderately fragmented. TP-Link, NETGEAR, ASUS, and Xiaomi occupy the top tier, yet their collective share falls short of levels that would indicate high concentration. TP-Link restructured corporate governance between 2022 and 2024, adding U.S. and Singapore headquarters to buffer trade-policy risk. NETGEAR’s 2024 10-K highlighted dependence on sole-source Wi-Fi silicon as foundries diverted capacity to AI accelerators, pressuring product launch schedules and gross margins. ASUS grew AIoT revenue 10-15% year-over-year in Q1 2025 on gamer-focused tri-band routers, while Xiaomi’s IoT segment surged 30% in 2024 by cross-selling mesh nodes through its smartphone base.

White-box entrants intensify price competition in developing markets, and carrier-bundled 5G gateways threaten substitution in urbanized regions. Vendors counter by integrating AI traffic optimization, dual-WAN failover, and compliance features aligned with evolving cybersecurity mandates. Ubiquiti courts prosumers with controller-based management priced between consumer and enterprise tiers, and GL.iNet attracts privacy-minded users with open-source firmware and WireGuard acceleration. Forward integration into cloud management and subscription services is emerging as the primary hedge against commoditization.

SOHO Router Industry Leaders

TP-Link Corporation Limited

NETGEAR, Inc.

ASUSTeK Computer Inc.

D-Link Corporation

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Federal Communications Commission authorized standard-power devices for indoor and outdoor 6 GHz operation, clearing the way for Wi-Fi 6E and Wi-Fi 7 routers with extended range

- October 2025: Inseego launched the FX4200 5G fixed-wireless gateway with tri-band Wi-Fi 7, targeting small and medium enterprises on T-Mobile networks.

- May 2025: Inseego introduced the FX4100 5G fixed-wireless gateway, bundling Ethernet ports and cloud management for small offices.

- May 2025: The FCC’s December 2024 ruling permitting very-low-power 6 GHz devices took effect, enabling sub-USD 200 tri-band routers to reach the market.

Global SOHO Router Market Report Scope

The SOHO router market comprises networking devices designed for small office and home office environments that enable internet connectivity, local area networking, and traffic management across multiple devices. These routers integrate wired and wireless access technologies, such as Ethernet, Wi-Fi 5, Wi-Fi 6, and Wi-Fi 7, and increasingly include features such as network security, cloud-based management, and application-level traffic prioritization. The market covers standalone retail routers as well as ISP-bundled gateways, serving residential users, freelancers, and SMEs that require cost-effective, reliable, and scalable connectivity solutions for mixed workloads, including video conferencing, cloud applications, and IoT operations.

The SOHO Router Market Report is Segmented by Frequency Band (Single-Band, Dual-Band, Tri-Band, and Quad-Band), Wi-Fi Standard (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Application (Residential, Home Office, Small Office, and Gaming and Entertainment), Distribution Channel (Online Retail, Offline Retail, ISP Bundled CPE, and Enterprise Channel Partners), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Wi-Fi 5 |

| Wi-Fi 6 |

| Wi-Fi 6E |

| Wi-Fi 7 |

| Single-band Router |

| Dual-band Router |

| Tri-band Router |

| Mesh Wi-Fi System |

| Gaming Router |

| Portable Travel Router |

| Online Retail |

| ISP/Telecom Provider Bundles |

| Electronics Specialty Stores |

| Mass Market/Hypermarket |

| Residential Home |

| Small Office/Home Office (SOHO) |

| Small Business (SMB) |

| Remote Workforce |

| Gaming Enthusiasts |

| Smart Home/IoT |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Bandwidth Standard | Wi-Fi 5 | |

| Wi-Fi 6 | ||

| Wi-Fi 6E | ||

| Wi-Fi 7 | ||

| By Product Type | Single-band Router | |

| Dual-band Router | ||

| Tri-band Router | ||

| Mesh Wi-Fi System | ||

| Gaming Router | ||

| Portable Travel Router | ||

| By Distribution Channel | Online Retail | |

| ISP/Telecom Provider Bundles | ||

| Electronics Specialty Stores | ||

| Mass Market/Hypermarket | ||

| By Application/User Type | Residential Home | |

| Small Office/Home Office (SOHO) | ||

| Small Business (SMB) | ||

| Remote Workforce | ||

| Gaming Enthusiasts | ||

| Smart Home/IoT | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the SOHO router market be by 2031?

The SOHO router market size is forecast to reach USD 17.82 billion by 2031, expanding at an 8.54% CAGR during 2026-2031.

Which frequency band segment is growing the fastest?

Tri-band routers are projected to expand at a 12.64% CAGR thanks to the widespread adoption of 6 GHz spectrum and rising in-home device density.

What share do residential deployments hold?

Residential environments accounted for 61.24% of 2025 revenue and remain the largest application segment, according to Mordor Intelligence.

Which region will record the highest growth through 2031?

South America is poised for a 10.46% CAGR as fiber penetration accelerates, particularly in Brazil, Chile, and Peru.

How quickly is Wi-Fi 7 being adopted?

Wi-Fi 7 shipments are expected to grow at a 24.76% CAGR, compressing the upgrade cycle and overtaking Wi-Fi 6E in premium tiers.

Who are the leading companies in the SOHO router industry?

TP-Link, NETGEAR, ASUS, and Xiaomi currently anchor the competitive landscape, but white-box vendors and carrier-bundled 5G gateways are intensifying rivalry.

Page last updated on: