Network Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

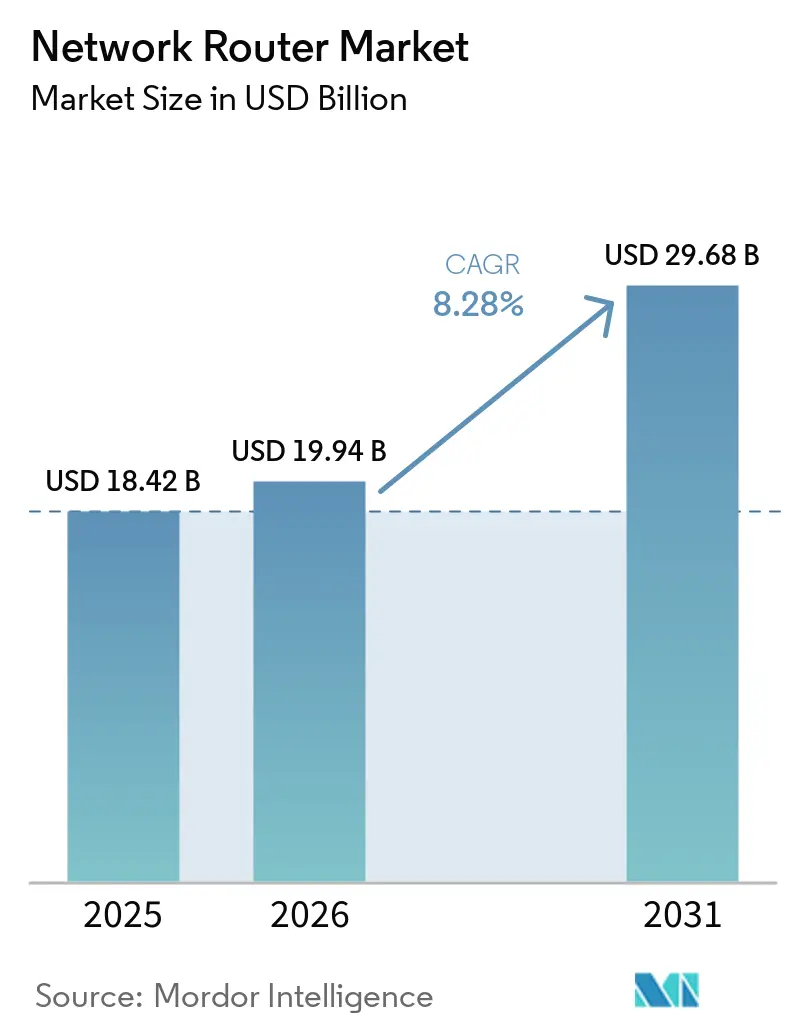

| Market Size (2026) | USD 19.94 Billion |

| Market Size (2031) | USD 29.68 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

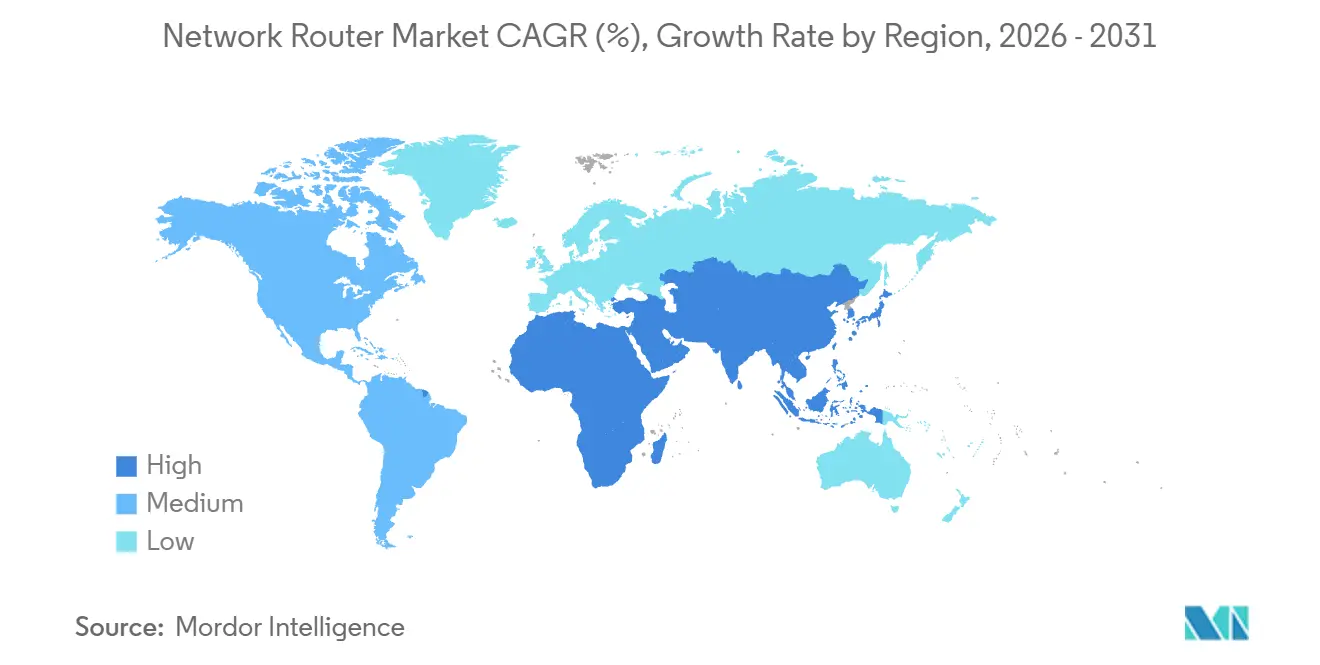

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Router Market Analysis by Mordor Intelligence

The network router market size is projected to expand from USD 18.42 billion in 2025 and USD 19.94 billion in 2026 to USD 29.68 billion by 2031, registering a CAGR of 8.28% between 2026 and 2031. Structural demand is accelerating as hyperscale data-center operators standardize on spine-and-leaf fabrics, mobile-network operators upgrade 5 G backhaul, and enterprises replace legacy wide-area links with software-defined overlays that decouple control planes from proprietary hardware. Vendors are compressing innovation cycles through merchant-silicon designs and open network operating systems, which lowers entry barriers for white-box suppliers and intensifies price competition. Regional growth profiles are diverging: North America currently holds the largest revenue pool, yet public broadband subsidies and 5 G-Advanced deployments are setting Asia-Pacific on the fastest expansion path. Meanwhile, silicon supply-chain risk and overlapping cybersecurity mandates keep margin pressure elevated, rewarding companies that control chip design and firmware roadmaps and can navigate export-control regimes.

Key Report Takeaways

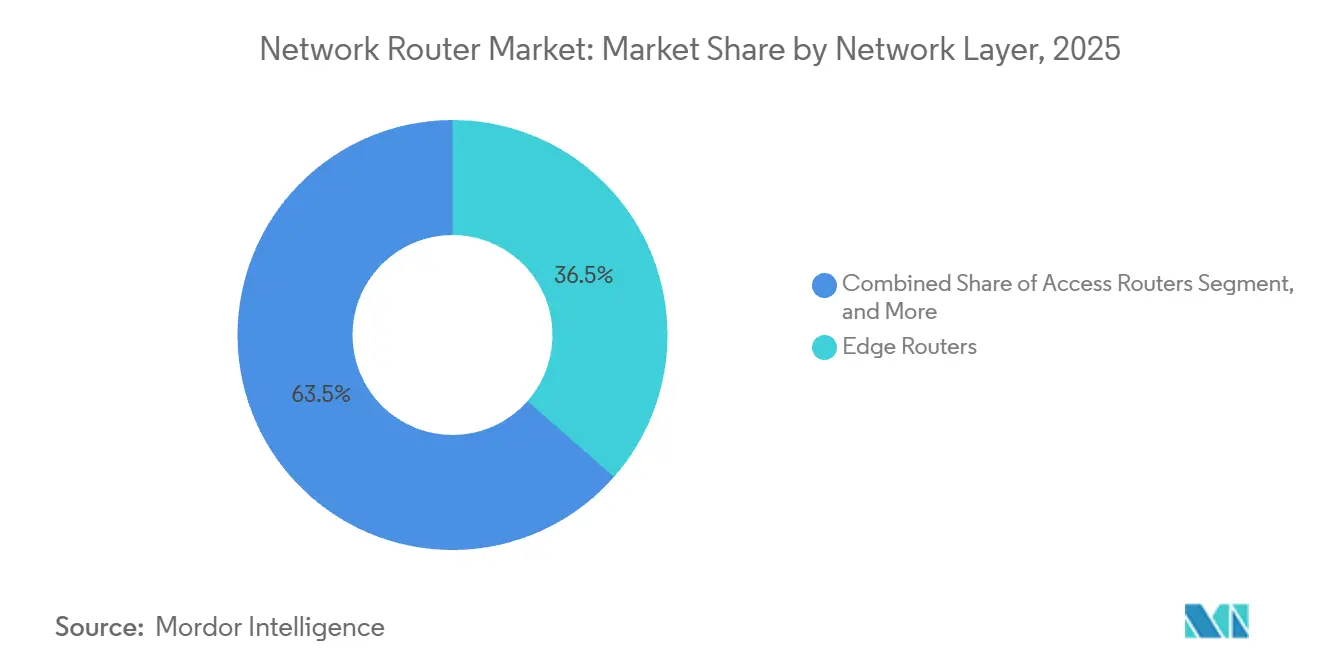

- By network layer, edge routers led the network router market with 36.48% share in 2025, while aggregation routers are forecast to grow at a 9.62% CAGR through 2031.

- By performance tier, mid-throughput platforms captured 38.92% of 2025 revenue, whereas ultra-high-throughput systems above 100 Gbps are projected to advance at an 11.84% CAGR between 2026 and 2031.

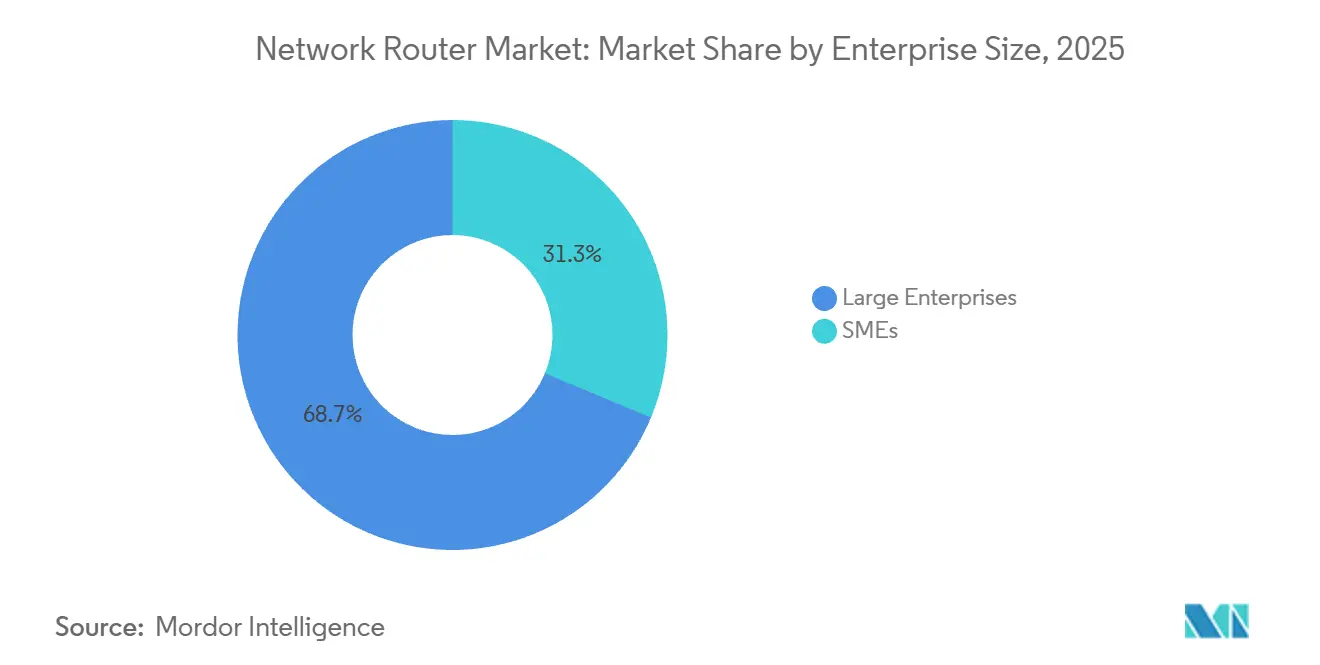

- By enterprise size, large enterprises accounted for 68.74% of 2025 spending, but small and medium enterprises are expected to post a 9.18% CAGR during the forecast period.

- By end user industry, IT and telecom dominated end-user demand, accounting for 41.26% in 2025; manufacturing is set to record the fastest growth at a 9.76% CAGR.

- By geography, North America accounted for 35.12% of 2025 revenue, yet Asia-Pacific is poised to accelerate at a 10.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Network Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing IP Traffic Volume in Data Centers | +2.1% | Global, concentration in North America and Asia-Pacific hubs | Medium term (2-4 years) |

| Rapid 5 G Backhaul Deployment Requiring High-Capacity Routers | +1.8% | Asia-Pacific core, Middle East and Africa emerging markets | Short term (≤ 2 years) |

| Enterprise Shift to SD-WAN Architectures | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Government Broadband Stimulus Programs | +1.3% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Edge Computing Creating Demand for Compact Aggregation Routers | +0.9% | Global | Medium term (2-4 years) |

| Open-Source NOS Adoption Reducing Vendor Lock-In | +0.6% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing IP Traffic Volume in Data Centers

Hyperscale and colocation facilities are scaling to support generative-AI clusters that exchange petabytes of gradient updates, driving demand for routers that forward 400 GbE and 800 GbE traffic with sub-microsecond latency. Cisco projects global data-center IP traffic will surpass 20 zettabytes annually by 2026, with AI workloads accounting for an outsized share.[1]Cisco Systems, “Annual Internet Report,” Cisco.com Operators therefore prioritize programmable silicon that embeds telemetry engines and supports lossless congestion control, ensuring deterministic performance for mixed-precision tensors. Distributed inference further increases east-west traffic as edge nodes synchronize with centralized parameter servers. Router vendors responding to this pattern are integrating coherent optics that span 80 km without regeneration, simplifying metro fabrics. These capabilities collectively sustain premium pricing for high-radix chassis at the core of the network router market.

Rapid 5 G Backhaul Deployment Requiring High-Capacity Routers

Mobile network operators upgrading to 5 G standalone architectures must aggregate cell-site traffic that now peaks above 10 Gbps per sector. China Mobile crossed 4 million 5 G base stations by 2025, while MTN Group committed USD 1 billion for 5 G across 17 African countries. Backhaul routers consequently need segment routing and flexible Ethernet interfaces to slice bandwidth for autonomous-vehicle telemetry, industrial automation, and enhanced mobile broadband. Vendors unable to demonstrate Open RAN interoperability risk exclusion from government-funded spectrum awards. The surge in backhaul capacity translates into sustained orders for high-capacity platforms, adding momentum to the network router market size growth in emerging regions.

Enterprise Shift to SD-WAN Architectures

Organizations are replacing private MPLS circuits with overlay networks that dynamically steer traffic across broadband, LTE, and direct Internet links, reducing wide-area costs by as much as 40%. Cisco found that 81% of enterprises had deployed or planned to deploy SD-WAN by 2025. This architecture relocates routing intelligence to cloud controllers, enabling zero-touch provisioning and uniform security policy. Edge routers now bundle firewall, secure web gateway, and data-loss-prevention features, transforming into universal customer-premises equipment. Application-aware path selection optimizes voice, video, and SaaS flows based on jitter and loss metrics, driving refresh cycles even in budget-constrained verticals. The shift materially expands the addressable base of the network router industry among small and medium enterprises.

Government Broadband Stimulus Programs

Public-sector funding is closing digital divides and underwriting large-scale router deployments. The United States BEAD program has earmarked USD 42.45 billion for fiber and fixed-wireless rollouts, while India’s BharatNet seeks to connect more than 600,000 villages. Contracts typically stipulate open-access architectures and interoperable equipment, favoring vendors that expose standardized management APIs. Domestic-content clauses further influence tender eligibility, prompting global suppliers to establish local manufacturing. Because milestones drive revenue recognition, vendors with robust project financing capabilities can manage elongated cash cycles and still capitalize on multi-year build-outs, reinforcing the long-term growth outlook for the network router market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility for Advanced ASICs | -1.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Rising Cyber-Security Compliance Costs | -0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Talent Shortage in Network Automation Skill Sets | -0.5% | Global | Long term (≥ 4 years) |

| Geopolitical Export Controls on High-End Silicon | -0.7% | Asia-Pacific, spillover to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility for Advanced ASICs

Foundry capacity remains tight because automotive, mobile, and AI accelerators compete for leading-edge nodes, stretching router ASIC lead times beyond 40 weeks and inflating high-bandwidth-memory prices by over 30% year-over-year in early 2025. Vendors hedge through dual-source strategies across multiple foundries, yet mid-tier suppliers struggle to secure priority allocations, compressing gross margins. Chiplet-based designs that disaggregate forwarding, telemetry, and crypto engines add packaging complexity and expose additional choke points. These dynamics curtail near-term shipment volumes and temper the otherwise robust outlook for the network router market size.

Rising Cyber-Security Compliance Costs

Routers must satisfy Secure-by-Design principles from the U.S. Cybersecurity and Infrastructure Security Agency and overlapping EU certification schemes, requiring recurring penetration tests, SBOM audits, and FIPS 140-3 validation.[2]Cybersecurity and Infrastructure Security Agency, “Secure by Design Principles,” cisa.gov Engineering overhead extends release schedules, while regulated buyers mandate zero-trust segmentation and encrypted management planes, raising bill-of-materials costs. Insurers now impose stricter underwriting, increasing the total cost of ownership for operators. These expenses particularly burden small vendors, limiting competitive diversity within the network router industry and modestly dampening overall market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Network Layer: Edge Platforms Retain Spending Priority

Edge routers accounted for 36.48% of the network router market share in 2025, confirming their role as the critical demarcation point between enterprise LANs and carrier WANs. These devices fold firewall, VPN, and application-aware routing into compact formats that branch offices can deploy without on-site engineers. Cloud-based controllers automate zero-touch setup, appealing to retailers and remote campuses that lack full-time networking staff. Aggregation routers sit one tier upstream and are projected to register a 9.62% CAGR, supported by edge-computing workloads that require localized packet consolidation. Segment routing and flexible Ethernet interfaces are now standard, enabling deterministic control for industrial sensors and autonomous vehicles and bolstering the network router market size for mid-tier platforms.

Core routers emphasize sheer throughput and port density, anchoring hyperscale spines at hundreds of terabits per second. Access routers, although more modest, are integrating passive-optical termination and LTE links to backfill last-mile gaps. Coherent pluggables now allow routers to modulate wavelengths directly, collapsing traditional layer boundaries and eliminating separate transponders for metro networks. This routed-optical approach reduces latency in 5 G backhaul and inter-data-center links, expanding use cases for aggregation and edge platforms across the network router market.

By Performance Tier: Ultra-High Throughput Accelerates Adoption

Mid-throughput systems ranging from 1 Gbps to 10 Gbps held 38.92% revenue share in 2025, dominating branch and campus installations. Hyperscalers, however, are upgrading to routers exceeding 100 Gbps, a tier forecast to grow at an 11.84% CAGR as 400 GbE and 800 GbE optics drop below USD 0.50 per gigabit. AI training networks that exchange gradient updates across thousands of GPUs saturate lower-speed fabrics, forcing a shift toward high-radix designs with on-chip telemetry and lossless congestion control. These capabilities, combined with coherent optics that maintain reach beyond 80 km, are expanding the ultra-high-throughput slice of the network router market.

Routers in the 10 Gbps to 100 Gbps bracket bridge cost and performance for mid-sized enterprises and regional carriers. Single-rack-unit platforms now deliver aggregate bandwidth once reserved for multi-chassis systems, shrinking data-center footprints and cooling loads. Low-throughput routers below 1 Gbps persist in IoT gateways and small offices where power budgets are tight. Programmable network processors and FPGAs are increasingly offloading encryption and DPI, preserving forwarding-plane speed. The declining cost of coherent DSPs further democratizes high-capacity interfaces, accelerating migration up the performance ladder.

By Enterprise Size: Cloud-Managed Solutions Unlock SME Growth

Large enterprises directed 68.74% of 2025 spending, relying on chassis-based routers with redundant control planes and line-card modularity. Long procurement cycles and enterprise license agreements bundle hardware, software, and support into predictable three- to five-year budgets. Small and medium enterprises, by contrast, benefit from cloud-managed SD-WAN appliances that trade capital expense for subscription fees, a model expected to drive a 9.18% CAGR in SME spending through 2031. Web portals enable non-specialists to spin up branch connectivity, while automated path steering optimizes SaaS performance without manual tuning, expanding SME participation in the network router market.

Appliances built for SMEs combine routing, firewall, and secure web gateway functionality in fanless enclosures that withstand harsh environments. Managed service providers increasingly resell network-as-a-service bundles, offering 24/7 monitoring and policy updates for a monthly fee. Large enterprises are simultaneously adopting zero-trust segmentation and identity-aware routing, which demands hardware-accelerated crypto and deep directory integrations. This divergence forces vendors to maintain distinct product lines aligned to simple, preset templates for SMEs and granular policy tools for corporate buyers.

By End User Industry: Manufacturing Emerges as Fastest-Growing Vertical

Information technology and telecom combined for 41.26% of 2025 demand because data-center operators and carriers refresh gear on two- to three-year cycles. Manufacturing is now on track for the fastest expansion with a 9.76% CAGR as factories roll out Industry 4.0 automation that hinges on deterministic Ethernet. Time-sensitive networking extensions guarantee bounded latency for robotic assembly lines, and private 5G converges OT and IT traffic onto unified routers.[3]Siemens AG, “Industry 4.0 Networking Solutions,” siemens.com As a result, deterministic routing capabilities and hardware-based precision-time protocols are entering mainstream portfolios, widening the network router market size across industrial campuses.

Financial services institutions prioritize microsecond-grade latency for algorithmic trading, deploying dedicated circuits and hardware-accelerated encryption. Healthcare providers demand HIPAA-compliant segmentation and video optimization for telemedicine. Retailers focus on rapid, low-cost store rollouts enabled by cloud-managed routers. Education institutions turn to open-source NOS options to stretch limited budgets, but broadband grants are upgrading rural school connectivity. Government entities require domestic content and extended security certifications, lengthening deal cycles yet anchoring multi-year revenue streams.

Geography Analysis

North America retained 35.12% of 2025 revenue, anchored by the world’s highest concentration of hyperscale data centers and enterprise SD-WAN adoption. The United States BEAD program is funding fiber builds in underserved counties, pulling demand for aggregation routers into rural exchanges. Canada and Mexico are modernizing cross-border corridors as reshoring in automotive and electronics drives demand for low-latency connectivity. Currency swings and import rules in South America create price sensitivity, yet Brazil leads regional deployments, where major carriers roll out 5G standalone cores.

Asia-Pacific is expected to post a 10.44% CAGR, making it the fastest-growing slice of the network router market. China surpassed 4 million 5G base stations by 2025 and is transitioning to 5G-Advanced, which drives core and aggregation upgrades.[4]Press Information Bureau, “Digital Infrastructure Investment Initiatives,” pib.gov.in India’s USD 1.3 trillion digital infrastructure plan underpins mass fiber backhaul to villages, requiring tens of thousands of compact aggregation routers. Japan invests in beyond-5 G terahertz backhaul, prompting trials of routers that aggregate multi-gigabit wireless flows. Australia and New Zealand co-fund rural broadband, while Indonesia and Vietnam attract data-center FDI that triggers large spine-and-leaf orders.

Europe balances continent-wide policy with national preferences under the Digital Decade mandate for gigabit access by 2030. Germany, the United Kingdom, and France remain the largest buyers, each emphasizing secure-by-design routers for critical infrastructure. Sanctions constrain Russia, encouraging domestic silicon substitutes. The Middle East funnels oil revenue into smart-city projects, with Saudi Arabia and the United Arab Emirates specifying routers for autonomous transport and surveillance grids. Africa’s volume is concentrated in South Africa and Nigeria, but currency volatility and limited power infrastructure slow adoption elsewhere. Global suppliers respond by opening regional service hubs to satisfy local-content clauses and minimize shipping delays, actions that expand their addressable network router market.

Competitive Landscape

The industry is moderately concentrated, with the top five suppliers accounting for a substantial share of total revenue, while regional and white-box vendors cater to price-sensitive segments. Cisco Systems and Juniper Networks differentiate through vertically integrated silicon, such as Cisco Silicon One, which combines switching, routing, and optical functions in a single programmable pipeline. Huawei Technologies and Nokia remain strong in carrier networks through local manufacturing and compliance with national requirements. Arista Networks continues to gain share among hyperscalers with its cloud-native EOS operating system and rapid software innovation model.

Adoption of open-source network operating systems is accelerating disaggregation, allowing hyperscalers to combine commodity hardware with software such as SONiC, which Meta Platforms uses across its network fabric. This approach increases flexibility and reduces reliance on proprietary systems, but it also puts pressure on incumbent margins. Organizations with strong in-house integration capabilities are better positioned to benefit from lower costs and greater control over network architecture.

Geopolitical factors, particularly export controls, are reshaping supply chains by pushing Chinese hyperscalers toward domestic semiconductor ecosystems while requiring Western vendors to redesign around compliant components. Vendors that secure multi-foundry capacity, maintain regulatory compliance, and invest in automation tools are likely to stay competitive. As hardware differentiation narrows, buying decisions increasingly depend on total cost of ownership, operational efficiency, and software-driven capabilities.

Network Router Industry Leaders

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Nokia Corporation

Hewlett Packard Enterprise Company

Extreme Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Arista Networks completed its acquisition of a European optical-component partner, expediting development of 1.6-Tbps coherent interfaces for its 7800 Series routers.

- January 2026: Cisco Systems began volume shipments of the Catalyst 9000X with integrated 800 GbE ports and on-chip AI inference engines targeting lossless data-center fabrics.

- December 2025: Hewlett Packard Enterprise introduced the Aruba CX 10000 with modular 400 GbE slots under its GreenLake consumption model.

- October 2025: Nokia signed a USD 300 million, five-year routing partnership with an Indian operator to support 5 G standalone cores across 22 states.

Global Network Router Market Report Scope

The network router market refers to the revenue generated from devices that route data packets between networks, enabling communication across enterprise systems, telecom infrastructure, data centers, and end-user environments. These devices determine the optimal path for data transmission and are essential for connecting local networks to wide-area networks, cloud platforms, and internet backbones.

The Network Router Market Report is Segmented by Network Layer (Access Routers, Aggregation Routers, Core Routers, and Edge Routers), Performance Tier (Low Throughput, Mid Throughput, High Throughput, and Ultra-High), Enterprise Size (Large Enterprises, and SMEs), End User Industry (BFSI, IT and Telecom, Manufacturing, Government and Public Sector, Healthcare and Lifesciences, Retail and E-commerce, Education, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Access Routers |

| Aggregation Routers |

| Core Routers |

| Edge Routers |

| Low Throughput (<1 Gbps) |

| Mid Throughput (1-10 Gbps) |

| High Throughput (10-100 Gbps) |

| Ultra-High (>100 Gbps) |

| Large Enterprises |

| SMEs |

| BFSI |

| IT and Telecom |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Education |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Network Layer | Access Routers | |

| Aggregation Routers | ||

| Core Routers | ||

| Edge Routers | ||

| By Performance Tier | Low Throughput (<1 Gbps) | |

| Mid Throughput (1-10 Gbps) | ||

| High Throughput (10-100 Gbps) | ||

| Ultra-High (>100 Gbps) | ||

| By Enterprise Size | Large Enterprises | |

| SMEs | ||

| By End User Industry | BFSI | |

| IT and Telecom | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Education | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the network router market be by 2031?

It is projected to reach USD 29.68 billion by 2031, expanding at an 8.28% CAGR from 2026 to 2031.

Which segment leads current revenue within the network router market?

Edge routers held 36.48% of network router market share in 2025, making them the largest segment.

What segment is growing fastest through 2031?

Ultra-high-throughput platforms above 100 Gbps are forecast to grow at an 11.84% CAGR, outpacing all other performance tiers.

Which region will record the highest growth?

Asia-Pacific is expected to post a 10.44% CAGR through 2031, fueled by large-scale investments in broadband and 5G-Advanced networks.

How are small and medium enterprises influencing demand?

SMEs are adopting cloud-managed SD-WAN appliances, leading to a projected 9.18% CAGR in their spending as subscription models replace large upfront purchases.

Page last updated on: