Small Business Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.22 Billion |

| Market Size (2031) | USD 5.93 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

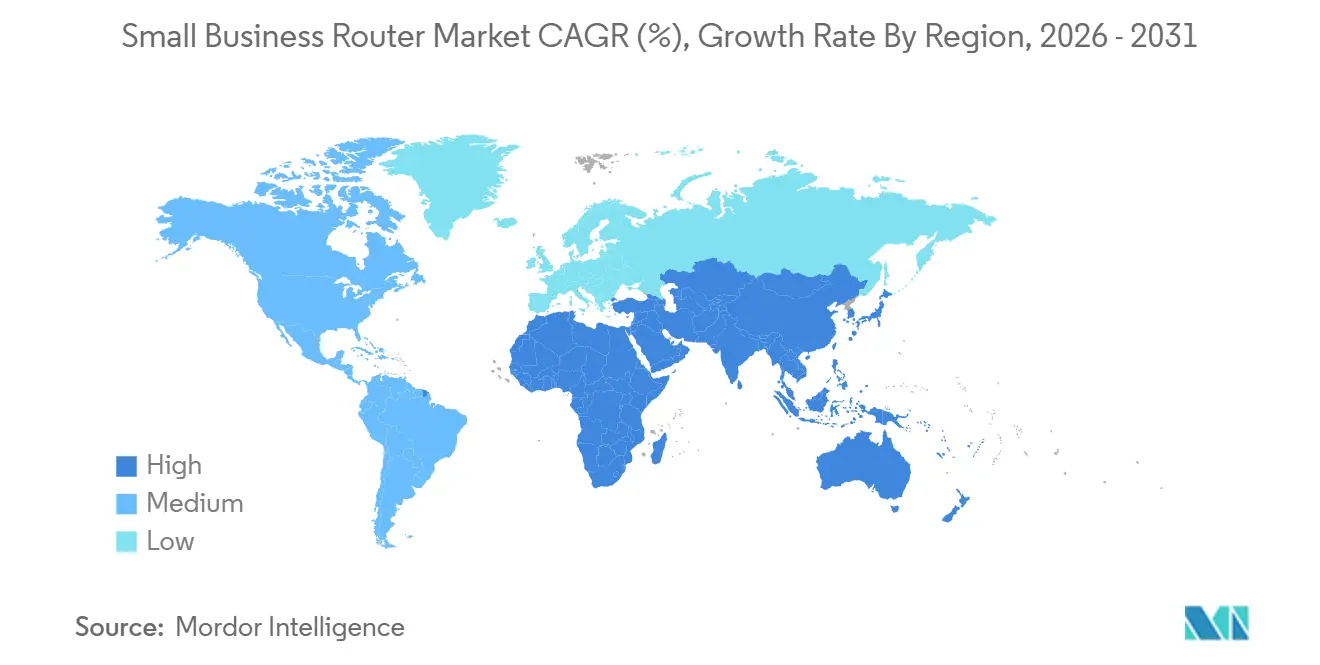

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

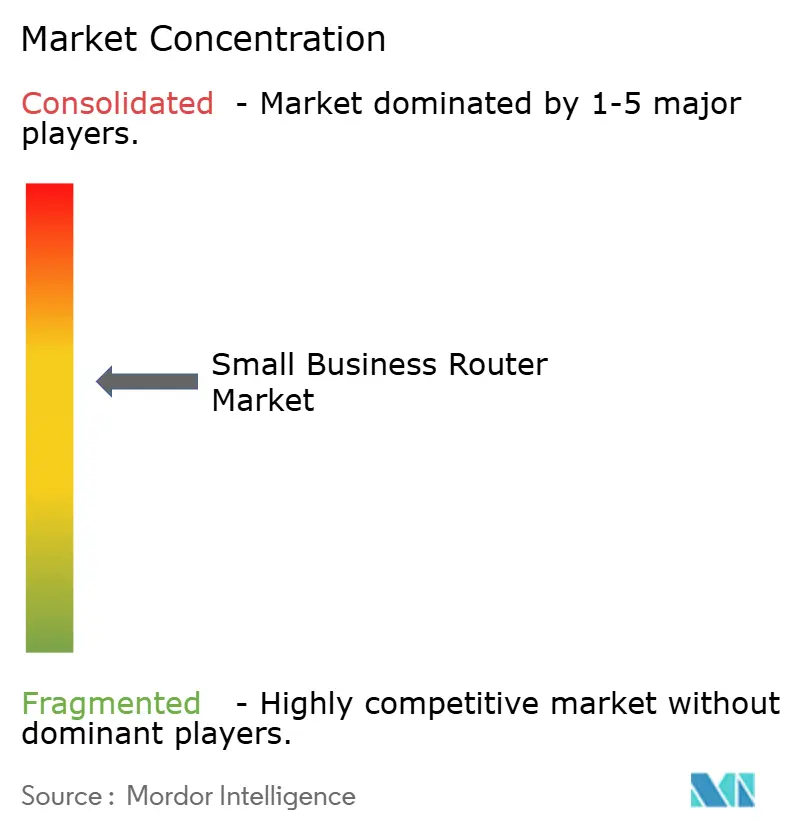

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Business Router Market Analysis by Mordor Intelligence

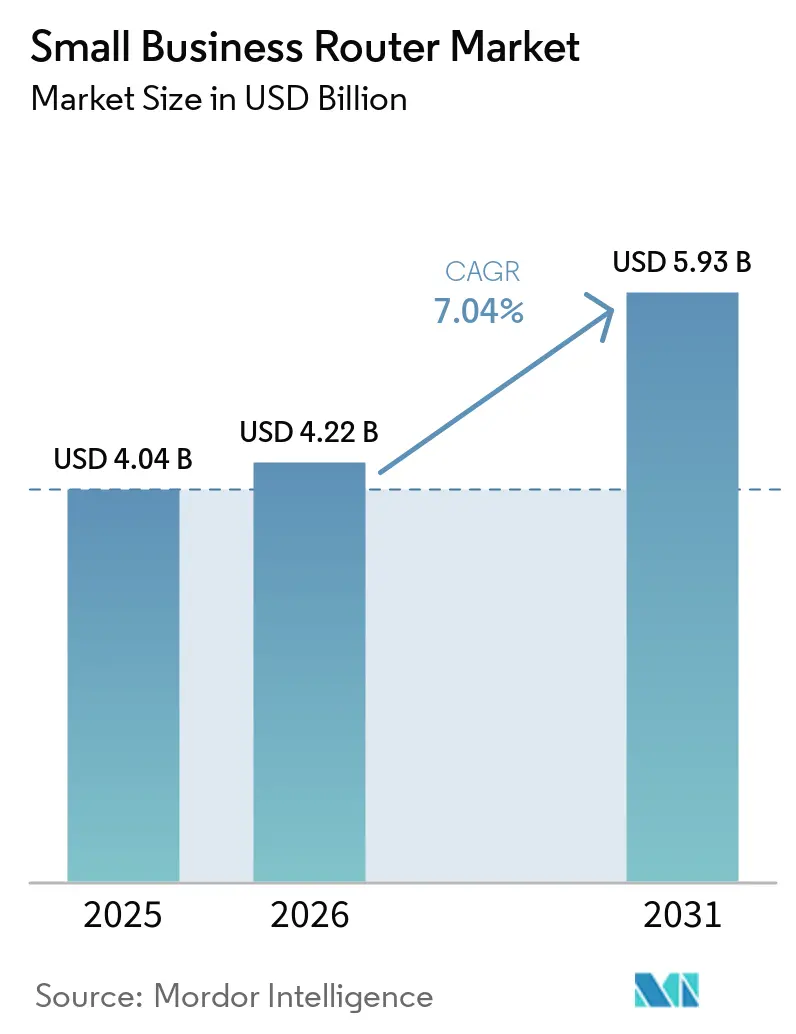

The small business router market size was valued at USD 4.04 billion in 2025 and is estimated to grow from USD 4.22 billion in 2026 to reach USD 5.93 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031). Rising adoption of hybrid work, cloud migration, and 5G fixed-wireless access is pushing firms to replace legacy single-band devices with multi-WAN, Wi-Fi 6, and Wi-Fi 7 hardware that can sustain higher device densities. Vendors are leaning on subscription-based network-as-a-service bundles to soften up-front costs and accelerate refresh cycles. Supply-chain realignment, sparked by new United States import restrictions on foreign-produced routers, is reshaping where devices are built and how quickly they reach end users. Government digitalization grants in Canada, Australia, and China are also acting as catalysts, while memory price inflation continues to squeeze margins for vendors targeting price-sensitive micro-enterprises.

Key Report Takeaways

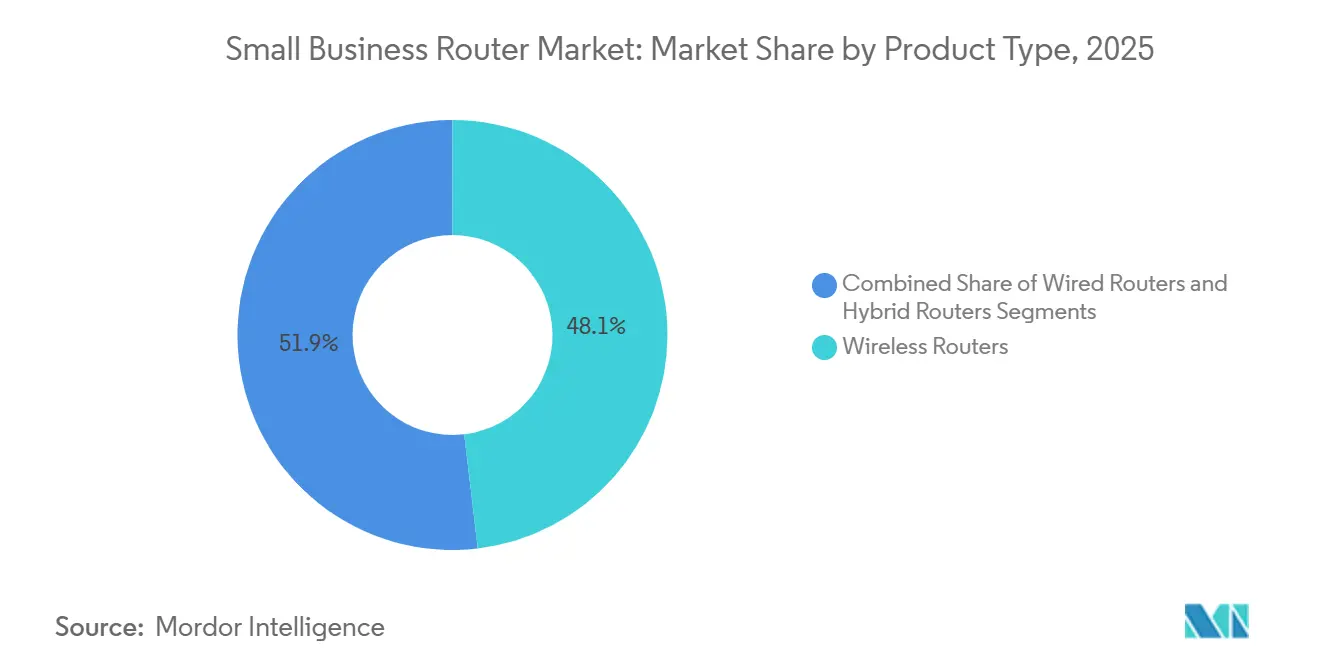

- By product type, wireless routers led with 48.13% revenue share in 2025, while hybrid routers are projected to expand at a 10.82% CAGR to 2031.

- By port count, models offering 5-8 ports captured 46.37% of the market in 2025; units with more than 8 ports are forecast to post a 10.53% CAGR through 2031.

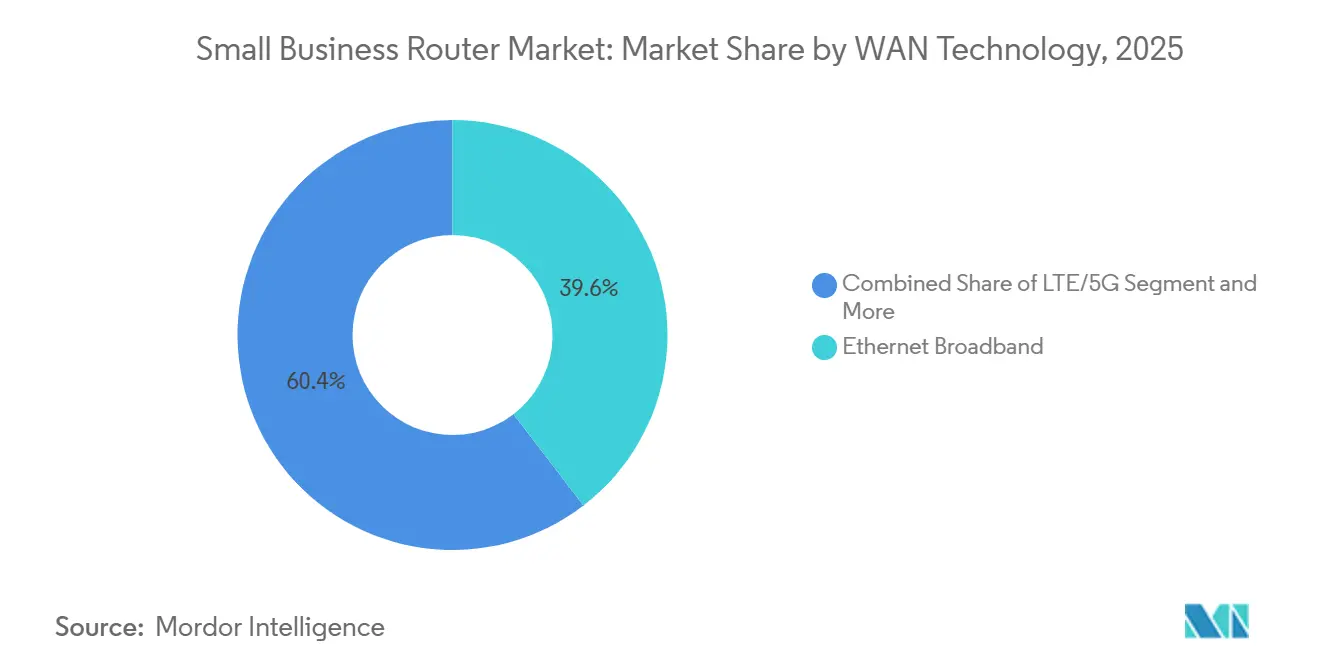

- By WAN technology, Ethernet broadband accounted for 39.58% of the base year value, whereas LTE/5G WAN devices are advancing at an 11.21% CAGR over the outlook period.

- By sales channel, e-commerce accounted for 41.72% of 2025 revenue and is on track to grow at a 11.61% CAGR through 2031.

- By geography, Asia-Pacific accounted for 34.29% of 2025 sales, and Africa is expected to log the fastest growth at 11.90% per year through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small Business Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Hybrid Work Models by Small Businesses | +1.80% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising Internet Bandwidth Demands for Cloud Applications | +1.50% | Global | Medium term (2-4 years) |

| Increasing Availability of Affordable Wi-Fi 6 Routers | +1.20% | Global, with early gains in Asia-Pacific and North America | Short term (= 2 years) |

| Emergence of Subscription Based Network-as-a-Service Offerings | +1.00% | North America, Europe, with spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Integration of SD-WAN Features into Entry-Level Routers | +0.90% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Government Small Business Digitalization Incentives | +0.70% | Canada, Australia, China, European Union, with selective programs in Africa and Middle East | Short term (= 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Hybrid Work Models by Small Businesses

Hybrid work arrangements are compelling small businesses to replace consumer-grade routers with devices that support simultaneous high-definition video streams, virtual private network tunnels, and quality-of-service policies for latency-sensitive applications. A peer-reviewed study in 2025 found that hybrid work improved small and medium enterprise productivity by 4.8%, creating a measurable return on investment for connectivity upgrades. A 2025 small business survey reported that 47% of respondents implemented new technology in the past 12 months, with 38% deploying artificial intelligence tools that require low-latency, high-throughput connections. Another industry study found that 86% of small and medium enterprises stated poor connectivity negatively impacted operations, while 5G deployment could contribute GBP 79 billion (USD 100 billion) to the United Kingdom economy. The shift is accelerating demand for routers with multi-gigabit Ethernet ports, Wi-Fi 6E tri-band radios, and integrated security features that can segment guest, employee, and Internet of Things traffic. In August 2025, ASUS launched the RT-BE58 Go, a Wi-Fi 7 mini travel router with 2.5 gigabit per second WAN, 5G/4G USB tethering, and pre-installed virtual private network support for up to 30 service providers, targeting mobile and hybrid workers.[1]PLOS ONE, “Hybrid Work and Productivity: Evidence from a Field Experiment,” PLOS.org

Rising Internet Bandwidth Demands for Cloud Applications

Migration to software-as-a-service platforms for customer relationship management, enterprise resource planning, and collaboration is driving small businesses to upgrade from asymmetric digital subscriber line and cable connections to fiber and 5G fixed wireless access. One telecom operator reported 24.6 million fixed wireless access locations in service, representing 21.2% of broadband serviceable locations, while two major competitors combined for 37.8% coverage and 145% growth in fixed wireless access broadband serviceable locations. A survey of Canadian small and medium businesses found that 63% believe 5G will benefit their operations, while 40% of United Kingdom retailer small and medium businesses are investing in 5G connectivity.Cloud application providers recommend minimum upload speeds of 5 megabits per second per concurrent user for video conferencing and 10 megabits per second for real-time collaboration, pushing small businesses toward routers that can bond multiple WAN links or prioritize traffic using deep packet inspection. In 2025, DrayTek introduced the Vigor2767 series, integrating SD-WAN load balancing across Ethernet, xDSL, and LTE interfaces, enabling bandwidth aggregation from multiple carriers. The trend is particularly pronounced in markets with unreliable single-carrier service, where hybrid routers provide failover and load distribution.[2]Verizon Communications, “Small Business Survey 2025,” Verizon.com

Increasing Availability of Affordable Wi-Fi 6 Routers

Price declines for Wi-Fi 6 chipsets and the introduction of Wi-Fi 7 products at the premium tier are pushing Wi-Fi 6 routers into the sub-USD 200 small business segment. In November 2025, D-Link launched its Guardian Series, including the DBR-600-P, DBR-700, and DBR-X3000-AP, targeting small businesses with Wi-Fi 6 dual-band radios, integrated firewall, and cloud management at accessible price points. In September 2024, NETGEAR introduced three Wi-Fi 7 routers, the RS600, RS500, and RS200, creating downward pricing pressure on Wi-Fi 6 inventory as retailers clear stock. The Wi-Fi Alliance certified over 350 Wi-Fi 6E devices by mid-2025, expanding the ecosystem and driving economies of scale in component production. Small businesses are adopting Wi-Fi 6 to support higher device densities, with orthogonal frequency-division multiple access and target wake time features reducing latency and power consumption for Internet of Things sensors, point-of-sale terminals, and security cameras. In January 2026, ASUS announced the ROG Strix GS-BE7200, offering Wi-Fi 7 with multi-link operation and 4K quadrature amplitude modulation in a dual-band configuration, positioning it as a cost-effective alternative to tri-band models for small offices requiring high throughput without 6 gigahertz spectrum.[3]DrayTek Corp., “Vigor2767 Series,” DrayTek.com

Emergence of Subscription Based Network-as-a-Service Offerings

Telecommunications carriers and managed service providers are bundling routers, software-defined wide area network orchestration, and security subscriptions into monthly fees, lowering upfront capital expenditure for small businesses. Verizon Business Complete packages routers, unified threat management, and 24/7 support into tiered subscriptions starting at USD 50 per month per location. AT&T Managed Network Services offers similar bundles with Cisco Meraki hardware and cloud-based analytics. In 2025, RUCKUS One was launched, providing cloud-managed Wi-Fi access points and switches with artificial intelligence-driven troubleshooting and zero-touch provisioning, targeting small businesses without dedicated information technology staff. XTIUM Cloud Managed Networking and SkyPulse offer comparable platforms with per-device monthly pricing, while T-Mobile Business Internet bundles 5G fixed wireless access gateways with unlimited data plans. The subscription model aligns router refresh cycles with technology evolution, enabling small businesses to upgrade to Wi-Fi 7 or 5G-Advanced devices as they become available without incurring large one-time costs. In February 2026, NETGEAR partnered with Xyte to deliver artificial intelligence-driven audio-visual management as a subscription service, signaling vendor interest in recurring revenue streams.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity Among Micro-Enterprises | -0.90% | Global, with acute impact in South America, Africa, and rural Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Disruptions for Semiconductor Components | -0.70% | Global, with concentration in North America and Europe due to regulatory shifts | Short term (≤ 2 years) |

| Growing Preference for All-in-One Cellular Hotspots over Routers | -0.50% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Limited IT Expertise in Very Small Offices Delaying Upgrades | -0.40% | Global, with higher incidence in rural and developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Among Micro-Enterprises

Micro-enterprises with fewer than 10 employees often allocate less than USD 500 annually for networking equipment, constraining the adoption of advanced routers with SD-WAN, Wi-Fi 6E, or integrated security appliances. Memory price inflation surged 600% in February 2026, compressing vendor margins and limiting the availability of entry-level models below USD 100. Small businesses in emerging markets face additional budget constraints due to currency depreciation and limited access to financing. The Federal Communications Commission's March 2026 decision to add all foreign-produced routers to its Covered List triggered conditional approval processes that increased compliance costs, which vendors are passing to buyers. China-origin routers fell to 1.1% of the United States import value share, while Vietnam-origin devices rose to 38.3%, reflecting a supply chain reconfiguration that added logistics and tariff expenses. Vendors are responding by introducing tiered product lines, with D-Link's DBR-600-P offering basic Wi-Fi 6 and firewall features at a lower price than its flagship DBR-X3000-AP. The constraint is most acute in Africa and South America, where small businesses prioritize connectivity over advanced features and often extend router lifecycles beyond five years.

Supply Chain Disruptions for Semiconductor Components

Semiconductor shortages and geopolitical trade restrictions continue to constrain router production, particularly for models that require advanced application-specific integrated circuits and multi-gigabit Ethernet physical-layer transceivers. Memory prices surged 600% in February 2026 due to supply tightness, affecting routers that require large dynamic random-access memory buffers for deep packet inspection and traffic shaping. The Federal Communications Commission added all foreign-produced routers to its Covered List in March 2026, requiring conditional approval for devices manufactured outside the United States and extending lead times by 6 to 12 months for vendors seeking market access. TP-Link pledged hundreds of millions of dollars in April 2026 to establish United States manufacturing capacity, but the production ramp-up will not be complete until 2027, leaving a near-term supply gap. China-origin router imports to the United States fell to 1.1% of value share, while Vietnam-origin devices rose to 38.3%, indicating rapid but incomplete supply chain diversification. Vendors with diversified manufacturing footprints, such as Cisco and Hewlett Packard Enterprise, are better positioned to navigate regulatory shifts, while smaller players face longer backlogs and higher component costs.[4]Federal Communications Commission, “FCC Adds Foreign-Produced Routers to Covered List,” FCC.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Routers Gain Resilience Edge

Hybrid routers, which merge wired, wireless, and cellular WAN interfaces, are projected to expand at 10.82% annually through 2031 as firms seek seamless failover and bandwidth aggregation. Wireless models still account for 48.13% of the small-business router market in 2025 due to mobility and guest-access requirements. The hybrid segment is expected to grow fastest because single-link outages impose higher operational costs in always-connected environments. Zyxel’s Nebula FWA515 integrates 5G WAN with dual 2.5 gigabit LAN, demonstrating feature convergence toward multi-access architectures that ensure continuity and performance under fluctuating network conditions.

Convergence is increasingly blurring category boundaries, with many wireless routers incorporating SIM slots or USB-based cellular backup, effectively shifting toward hybrid-first architectures. Wired models continue to serve niche applications such as manufacturing systems and point-of-sale environments that require deterministic throughput over copper infrastructure. ASUS’s RT-BE88U, equipped with 10G RJ-45 and SFP+ ports, supports automatic multi-WAN and 4G/5G tethering, indicating that even high-end wired devices are evolving into hybrid platforms to address redundancy, scalability, and performance-optimization requirements.

By Port Count: Multi-Gigabit Adoption Spurs Higher Density

Routers offering 5–8 ports captured 46.37% of the 2025 value, but units with more than 8 ports are projected to grow at 10.53% annually through 2031 as content-creation firms and data-intensive small businesses adopt 10 gigabit Ethernet. Power-over-Ethernet integration within routers is reducing equipment sprawl by enabling video surveillance systems, Wi-Fi 6E access points, and voice infrastructure to be powered directly from a single device. D-Link’s DGS-1250 switches can be chained from multi-gigabit router uplinks, simplifying cabling and improving scalability in dense network environments where multiple high-bandwidth endpoints operate simultaneously.

The 1–4 port segment remains relevant among micro-enterprises that depend primarily on wireless connectivity and USB-based 5G dongles for internet access. In developed markets, declining fiber costs are accelerating upgrades to 2.5-gigabit and 10-gigabit ports, driving future demand for higher-density routers with enhanced throughput capabilities. ASUS’s ZenWiFi BQ16 Pro integrates dual 10-gigabit ports into a mesh node, highlighting a broader transition toward multi-gig wired backhaul even in compact, consumer-oriented designs adapted for small-business use cases.

By WAN Technology: LTE/5G Bridges the Fiber Gap

Ethernet broadband still accounts for 39.58% of spending, yet LTE and 5G WAN devices are forecast to grow at 11.21% CAGR through 2031. The small business router market is benefiting from carriers expanding 5G fixed wireless access in rural and semi-urban areas, avoiding the high capital expenditure associated with fiber trenching. Major telecom operators collectively cover more than one-third of serviceable locations with fixed wireless access, with rapid year-on-year expansion. This dynamic is accelerating adoption of cellular-enabled routers among small businesses that require faster deployment and flexible connectivity without reliance on wired infrastructure.

Fiber continues to expand in urban centers, supported by large-scale infrastructure investments such as backbone network rollouts extending tens of thousands of kilometers. However, many small retailers initially deploy LTE or 5G routers as primary connections due to ease of installation, later integrating Ethernet as fiber becomes available. This phased connectivity model is increasing demand for hybrid routers capable of automatic failover between SIM-based and wired WAN interfaces. Devices that support seamless switching and bandwidth aggregation are gaining premium positioning, as they minimize downtime and optimize network performance across variable connectivity conditions.

By Sales Channel: E-Commerce Captures Value Chain

E-commerce commanded 41.72% of 2025 revenue and is on pace for an 11.61% CAGR as small business owners prioritize transparent pricing, rapid fulfillment, and broader product availability. TP-Link established a 72,000 sq ft distribution hub in Newbury to enable next-day delivery and reduce reliance on traditional distributors. Vendors are increasingly investing in direct-to-customer online storefronts to capture first-party data, improve margin control, and personalize offerings. In parallel, value-added resellers are shifting toward managed services, cybersecurity, and subscription-based support models to offset declining margins in hardware resale.

North America and Europe exhibit the highest e-commerce penetration due to mature logistics infrastructure and advanced digital procurement, while fragmented supply chains in parts of the Asia-Pacific continue to favor local distributors. The small business router market is undergoing channel transformation as self-service procurement platforms and artificial intelligence-driven product recommendation engines reduce dependence on traditional consultative sales. This transition is compressing sales cycles, increasing price transparency, and forcing channel partners to differentiate through integration, support, and lifecycle management services rather than pure product distribution.

Geography Analysis

Asia-Pacific held 34.29% of the small business router market in 2025, driven by China's Ministry of Industry and Information Technology Small and Medium Enterprise Digital Empowerment Plan for 2025–2027, which targets 40,000 SMEs and aims to achieve a cloud adoption rate exceeding 40% by 2027 through fiscal subsidies and financing support. TP-Link announced its largest global factory in India in October 2025, with an investment exceeding INR 100 crore (USD 12 million), and expanded its workforce while unveiling a research and development center focused on Wi-Fi 7, Internet of Things, and artificial intelligence in July 2025. Japan and South Korea are early adopters of Wi-Fi 7 routers, with ASUS launching the ROG Rapture GT-BE19000AI in October 2025, featuring a dedicated artificial intelligence core and native Docker Engine support for edge computing workloads. Southeast Asia is benefiting from subsea cable investments such as the 2Africa cable, which became operational in 2025 and connects 33 countries across Africa, Europe, and Asia, reducing latency for cloud applications.

North America remains a high-value market, with Canada's Digital Adoption Program allocating CAD 4 billion (USD 2.96 billion) in grants up to CAD 15,000 (USD 11,100) and loans up to CAD 100,000 (USD 74,000) to help small businesses adopt e-commerce, cybersecurity, and cloud-based tools. The United States National Science Foundation launched TechAccess AI-Ready America in 2025, committing USD 168 to 224 million to expand artificial intelligence infrastructure, which will drive demand for routers capable of supporting edge artificial intelligence workloads. Mexico is experiencing growth in 5G fixed wireless access deployments, with carriers targeting small businesses in peri-urban zones lacking fiber infrastructure. Europe is characterized by fragmented regulatory frameworks, with the European Union Radio Equipment Directive mandating compliance with EN 18031 security standards, which Zyxel's Nebula FWA515 claims to meet as among the first network products.

Africa is forecast to grow at 11.90% annually through 2031, the fastest rate among all geographies, driven by large-scale fiber deployments and government digitalization initiatives. Nigeria's D-VIBE project secured USD 200 million from the African Development Bank and USD 500 million from the World Bank to deploy 90,000 kilometers of fiber, connecting underserved communities and small businesses. South Africa and Morocco lead the continent in digital infrastructure maturity, with the Africa Digital Infrastructure Index scoring South Africa at 88 and Morocco at 79. Middle East markets such as Saudi Arabia and the United Arab Emirates are investing in smart city initiatives that require high-density Wi-Fi 6E and 5G routers for small businesses operating in free zones and innovation districts. South America is constrained by currency volatility and limited government subsidies, with Brazil and Argentina representing the largest markets but facing budget pressures that delay router upgrades.

Competitive Landscape

The small business router market is moderately concentrated, with the top five vendors, Cisco, Hewlett Packard Enterprise, Netgear, TP-Link, and Ubiquiti, accounting for approximately 45% to 50% of global revenue. Hewlett Packard Enterprise’s USD 14 billion acquisition of Juniper Networks in 2025 consolidated complementary routing and switching portfolios, strengthening capabilities in artificial intelligence-driven analytics and zero trust security. Competitive positioning is increasingly defined by integration depth across hardware, software, and security layers rather than standalone device performance.

Vendors are recalibrating product strategies toward affordability and performance convergence, particularly focusing on Wi-Fi 7 and embedded 5G capabilities at sub-USD 500 price points to attract cost-sensitive small businesses. Netgear’s collaboration with Samsung to validate Wi-Fi 7 interoperability for Galaxy devices reflects a strategy to bridge the premium consumer and small business segments. This approach leverages ecosystem alignment to drive adoption while reducing compatibility risks, particularly for high-bandwidth, multi-device environments increasingly dependent on seamless connectivity.

Manufacturing strategies are undergoing realignment in response to regulatory shifts and supply chain risks. TP-Link is expanding its United States production capacity to meet compliance requirements, while Cisco and Hewlett-Packard Enterprise use diversified global supply networks to mitigate semiconductor volatility. White space opportunities remain below USD 300 for hybrid Wi Fi 7 routers with integrated 5G, where feature availability is still limited. ASUS is targeting this segment with the ROG Strix GS BE7200, combining multi-link operation and hardware acceleration for distributed and remote work deployments.

Small Business Router Industry Leaders

Cisco Systems, Inc.

Hewlett Packard Enterprise Company

Netgear, Inc.

TP-Link Technologies Co., Ltd.

Ubiquiti Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: TP-Link pledged hundreds of millions of dollars to launch United States manufacturing and is awaiting conditional Federal Communications Commission clearance.

- February 2026: Netgear partnered with Xyte to offer cloud-based audiovisual network management as a subscription service.

- January 2026: Seacom unveiled a USD 1.5-2 billion plan to build Seacom 2.0, a subsea cable linking East Africa to Europe and Asia.

- January 2026: ASUS debuted the ROG Strix GS-BE7200 Wi-Fi 7 router with multi-link operation and support for up to 30 VPN clients.

Global Small Business Router Market Report Scope

The small business router market comprises networking devices designed to provide secure, reliable, and scalable internet connectivity for enterprises with limited IT resources. These routers integrate wired, wireless, and increasingly cellular WAN capabilities, supporting applications such as cloud services, video collaboration, and IoT, while offering features like traffic management, security, and remote administration.

The Small Business Router Market Report is Segmented by Product Type (Wired Routers, Wireless Routers, and Hybrid Routers), Port Count (1-4 Ports, 5-8 Ports, and More Than 8 Ports), WAN Technology (Ethernet Broadband, xDSL, LTE/5G, and Fiber), Sales Channel (Direct Sales, Distributors and VARs, and E-commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Wired Routers |

| Wireless Routers |

| Hybrid Routers |

| 1-4 Ports |

| 5-8 Ports |

| More Than 8 Ports |

| Ethernet Broadband |

| xDSL |

| LTE/5G |

| Fiber |

| Direct Sales |

| Distributors and VARs |

| E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Wired Routers | |

| Wireless Routers | ||

| Hybrid Routers | ||

| By Port Count | 1-4 Ports | |

| 5-8 Ports | ||

| More Than 8 Ports | ||

| By WAN Technology | Ethernet Broadband | |

| xDSL | ||

| LTE/5G | ||

| Fiber | ||

| By Sales Channel | Direct Sales | |

| Distributors and VARs | ||

| E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the small business router market?

The home wi-fi market size is projected to reach USD 21.88 billion by 2031, expanding at a 7.53% CAGR over 2026-2031.

Which component segment is growing fastest?

Software and services are forecast to rise at an 11.84% CAGR, outstripping hardware demand as ISPs monetize managed Wi-Fi bundles.

What is the current share of Wi-Fi 7 devices?

Wi-Fi 7 shipments are accelerating rapidly and are expected to surpass 1.1 billion units in 2026, giving the standard a rising slice of home wi-fi market share.

Why are ISPs bundling routers with broadband plans?

Carrier-supplied gateways cut support calls, ensure timely security patches and create recurring rental revenue that offsets falling retail margins.

Which region offers the strongest growth outlook?

Africa leads regional growth with a 14.21% CAGR through 2031 as nations leapfrog to fiber and 5G fixed wireless.

How is regulation affecting hardware sourcing?

The FCCs 2026 import restrictions require conditional approvals for foreign-made routers, prompting vendors to diversify assembly into Vietnam, Mexico and the United States.

Page last updated on: